Comprehensive Analysis of Islamic Finance Principles and Practices

VerifiedAdded on 2020/05/16

|9

|2322

|692

Homework Assignment

AI Summary

This assignment provides a comprehensive overview of Islamic finance, addressing Sharia compliance, the prohibition of riba (interest), and the adaptation of Islamic financial practices to modern technologies. It explores key concepts such as Mudaraba and Musharaka contracts as alternatives to conventional interest-based financing, detailing their structures and risk-sharing mechanisms. The assignment further examines Sukuk (Islamic bonds), including different structures and their viability based on underlying assets. It also discusses the role of Sharia boards and scholars in ensuring compliance, the use of LIBOR alternatives, and the ethical considerations in Islamic finance, such as screening investments. The document highlights the importance of risk management and the application of Islamic finance in various financial instruments and partnerships. Finally, the assignment covers the role of financial institutions and the importance of Sharia compliance in the context of Islamic financial transactions and the prevention of unethical practices.

ISLAMIC FINANCE

Name

Institution

Name

Institution

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ISLAMIC FINANCE

Q1: Shari’a remains a dynamic body of rules and can adopt to conditions or technologies

which may emerge in the future. The Shari’a dynamisms has structures on how the Islamic banks

are run and how emerging issues are raised and resolved. There Committees and Boards that

supervise the financial institutions and listen to their comments and complaints. The Shari’a

compliance is paramount and there are areas of flexibilities through which adaptation to new

trends have been effected while still remaining in compliance with Shari’a. For example, some of

the Islamic banks have got their own alternative to LIBOR called Islamic Interbank Benchmark

Rate, IIBR that complies with the Shariah moral codes. 1

Q2: Riba means not solely usury but also all form of unearned income. It is classified

into al-nasi’ah an al-fadl. The former denotes loan interests and the latter is extra over and above

loan paid in kind. It depends on payment of an extra by debtor to creditor in exchange of

products of same type. The Sharia’ah desires to remove not only exploitation which remains

intrinsic in institution of interests, but further that which remains inherent in each form of unjust

exchange in transacting business. 2

The former riba’s prohibition means that fixing in advance of a plus return on the loan as

an incentive for waiting is never allowed in Islam. Despite the fact that interests takes a key role

in contemporary economic system and that interest became the financial institutions life blood,

1 Askari, Hossein, Noureddine Krichene, and Abbas Mirakhor. "On the stability of an Islamic financial system."

(2014).

2 El-Karanshawy, Hatem A., Azmi Omar, Tariqullah Khan, Salman Syed Ali, Hylmun Izhar, Wijdan Tariq, Karim

Ginena, and Bahnaz Al Quradaghi. "Financial Stability and Risk Management in Islamic Financial Institutions."

(2015).

ISLAMIC FINANCE

Q1: Shari’a remains a dynamic body of rules and can adopt to conditions or technologies

which may emerge in the future. The Shari’a dynamisms has structures on how the Islamic banks

are run and how emerging issues are raised and resolved. There Committees and Boards that

supervise the financial institutions and listen to their comments and complaints. The Shari’a

compliance is paramount and there are areas of flexibilities through which adaptation to new

trends have been effected while still remaining in compliance with Shari’a. For example, some of

the Islamic banks have got their own alternative to LIBOR called Islamic Interbank Benchmark

Rate, IIBR that complies with the Shariah moral codes. 1

Q2: Riba means not solely usury but also all form of unearned income. It is classified

into al-nasi’ah an al-fadl. The former denotes loan interests and the latter is extra over and above

loan paid in kind. It depends on payment of an extra by debtor to creditor in exchange of

products of same type. The Sharia’ah desires to remove not only exploitation which remains

intrinsic in institution of interests, but further that which remains inherent in each form of unjust

exchange in transacting business. 2

The former riba’s prohibition means that fixing in advance of a plus return on the loan as

an incentive for waiting is never allowed in Islam. Despite the fact that interests takes a key role

in contemporary economic system and that interest became the financial institutions life blood,

1 Askari, Hossein, Noureddine Krichene, and Abbas Mirakhor. "On the stability of an Islamic financial system."

(2014).

2 El-Karanshawy, Hatem A., Azmi Omar, Tariqullah Khan, Salman Syed Ali, Hylmun Izhar, Wijdan Tariq, Karim

Ginena, and Bahnaz Al Quradaghi. "Financial Stability and Risk Management in Islamic Financial Institutions."

(2015).

2

Islam regards the principle of interest charging as quite contrary to that business in spirit of

sharing as well as cooperation and that lending based on interest is never as a business in

practice. 3 Islam, in legalizing trade but condemning interest, regards that fundamental

difference exists between profit nature arising from charges of interest and those earned via

trade. The interest prohibition rationale denotes how risk-reward sharing might be increasingly

conductive to equity realization and entrepreneurship promotion. 4

The concepts that replace riba include the Mudaraba and Musharaka contracts in Islamic

finance. This is because, it has been argued that Mudaraba provides functions likened to interest

or riba. This is because it provides chance of pure finance in that the capital owner is able to

invest in absence of personal management of capital investment and in absence of being exposed

to infinite liabilities. Nevertheless, these concepts deviate from riba or interests in the sense that

they keep a fair balance between the capital owner and the implementing entrepreneur.

LIBOR denotes a benchmark rate charged by certain top banks for loans (short-run). It

acts as the 1st move in calculation of interest rates on a range of loans globally. LIBOR has

established a ‘role’ in Islamic finance in that it has brought transparency to Islamic financing

course and might motivate wider utilization of Islamic banks. Despite being prohibited from

earning or paying interest, Islamic banks have been using LIBOR right from 1986. Some of the

Islamic banks have got their own alternative to LIBOR called Islamic Interbank Benchmark

Rate, IIBR that complies with the Shariah moral codes. Other known alternatives to LIBOR

include return on assets (ROA), Murabaha profit rates and retail deposit rates.

3 Kenourgios, Dimitris, Nader Naifar, and Dimitrios Dimitriou. "Islamic financial markets and global crises:

Contagion or decoupling?." Economic Modelling 57 (2016): 36-46.

4 Rahman, Farhat Naz. "Theory of Islamic Financial System and Economic growth." JOURNAL OF CREATIVE

WRITING| ISSN 2410-6259 3, no. 01 (2017): 66-82.

Islam regards the principle of interest charging as quite contrary to that business in spirit of

sharing as well as cooperation and that lending based on interest is never as a business in

practice. 3 Islam, in legalizing trade but condemning interest, regards that fundamental

difference exists between profit nature arising from charges of interest and those earned via

trade. The interest prohibition rationale denotes how risk-reward sharing might be increasingly

conductive to equity realization and entrepreneurship promotion. 4

The concepts that replace riba include the Mudaraba and Musharaka contracts in Islamic

finance. This is because, it has been argued that Mudaraba provides functions likened to interest

or riba. This is because it provides chance of pure finance in that the capital owner is able to

invest in absence of personal management of capital investment and in absence of being exposed

to infinite liabilities. Nevertheless, these concepts deviate from riba or interests in the sense that

they keep a fair balance between the capital owner and the implementing entrepreneur.

LIBOR denotes a benchmark rate charged by certain top banks for loans (short-run). It

acts as the 1st move in calculation of interest rates on a range of loans globally. LIBOR has

established a ‘role’ in Islamic finance in that it has brought transparency to Islamic financing

course and might motivate wider utilization of Islamic banks. Despite being prohibited from

earning or paying interest, Islamic banks have been using LIBOR right from 1986. Some of the

Islamic banks have got their own alternative to LIBOR called Islamic Interbank Benchmark

Rate, IIBR that complies with the Shariah moral codes. Other known alternatives to LIBOR

include return on assets (ROA), Murabaha profit rates and retail deposit rates.

3 Kenourgios, Dimitris, Nader Naifar, and Dimitrios Dimitriou. "Islamic financial markets and global crises:

Contagion or decoupling?." Economic Modelling 57 (2016): 36-46.

4 Rahman, Farhat Naz. "Theory of Islamic Financial System and Economic growth." JOURNAL OF CREATIVE

WRITING| ISSN 2410-6259 3, no. 01 (2017): 66-82.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Q3: Mudaraba denotes a partnership in profit whereby a partner offers capital (rab-al-

mal) and another offers business expertise (mudarib) and labour. In a nutshell, Mudaraba denotes

a special instance of Musharaka/Sharika, with every kind on contract having its distinguishing

characteristics. Musharaka on the other hand, denotes an arrangement between 2 or additional

partners to merge their corresponding services, assets, liabilities or obligations to make profit. 5

A Mudaraba agreement is able to be distinguished from Musharaka agreement below:

Entitlement for a profit share is anchored on capital contribution in Musharaka of each partner

whether in terms of cash, tangible assets, goods, creditworthiness or services. The Musharaka

subject is a certain kind of capital contribution. The entitlement to profit share in a Mudaraba,

conversely, anchors on 2 aspects: (I) capital existence (subject to Musharaka capital conditions,

and (II) work carried out by Mudarib, a kind of contribution which is dissimilar from Mudaraba

capital. Another distinction is that, labor (with inclusion of business expertise and management

skills) is to be offered jointly by partners/parties, while in Mudaraba, labor is offered by Mudarib

with the contribution of the other parties limited to capital provision.

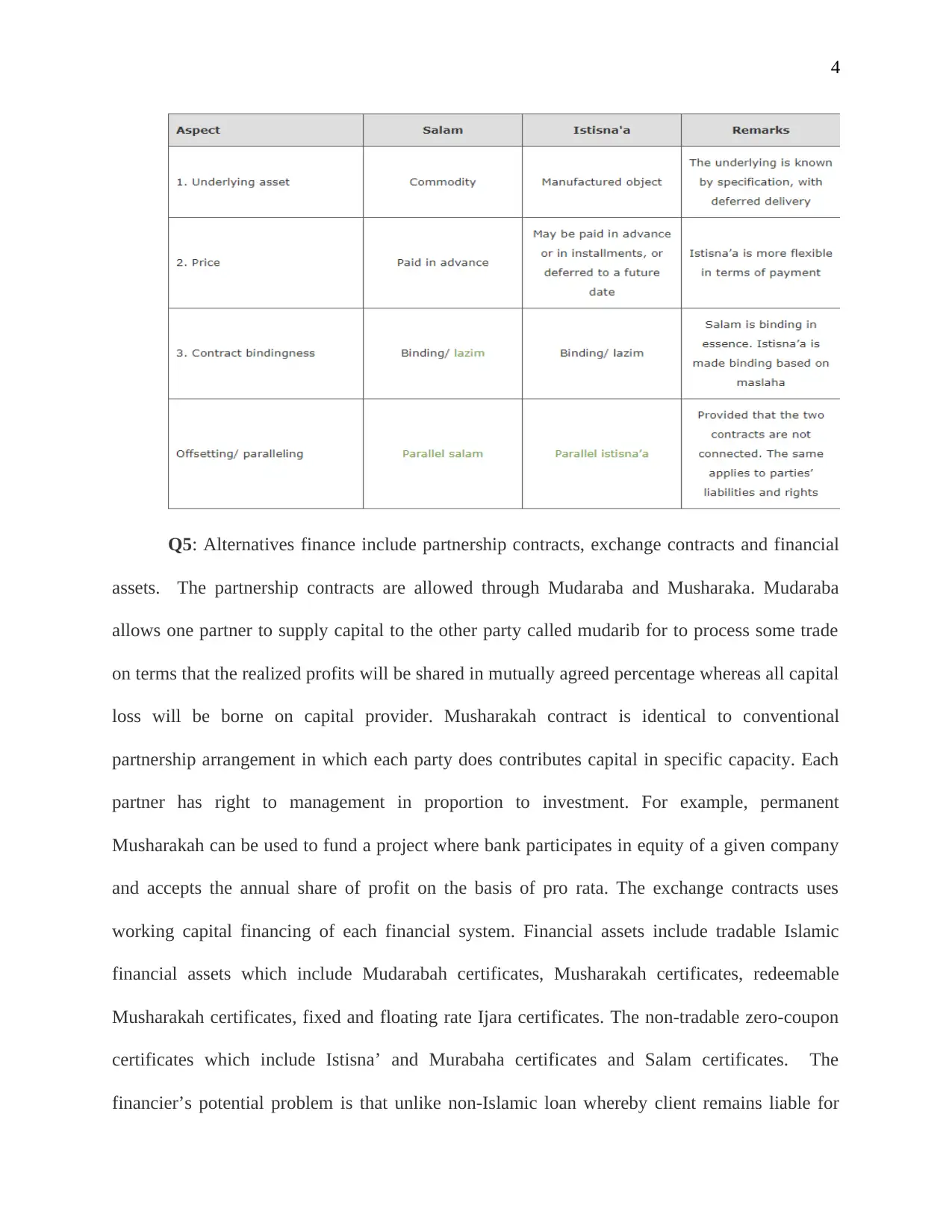

Q4: Istisna’a denotes a special instance of Salam and they both involve the delivery in

future of a specified item/object. The former is primarily utilized in both large and small scale

manufacturing field, construction, and Build Operate and Transfer (BOT). Salam, on the other

hand, remains limited to commodities trading, especially those which require from seller (al-

muslam ileihi) no alterations or additions. 6 Thus, both terms have a range of differences and

similarities as shown below:

5 Waemustafa, Waeibrorheem, and Suriani Sukri. "Systematic and unsystematic risk determinants of liquidity risk

between Islamic and conventional banks." (2016).

6 Samra, Emily. "Corporate governance in Islamic financial institutions." (2016).

Q3: Mudaraba denotes a partnership in profit whereby a partner offers capital (rab-al-

mal) and another offers business expertise (mudarib) and labour. In a nutshell, Mudaraba denotes

a special instance of Musharaka/Sharika, with every kind on contract having its distinguishing

characteristics. Musharaka on the other hand, denotes an arrangement between 2 or additional

partners to merge their corresponding services, assets, liabilities or obligations to make profit. 5

A Mudaraba agreement is able to be distinguished from Musharaka agreement below:

Entitlement for a profit share is anchored on capital contribution in Musharaka of each partner

whether in terms of cash, tangible assets, goods, creditworthiness or services. The Musharaka

subject is a certain kind of capital contribution. The entitlement to profit share in a Mudaraba,

conversely, anchors on 2 aspects: (I) capital existence (subject to Musharaka capital conditions,

and (II) work carried out by Mudarib, a kind of contribution which is dissimilar from Mudaraba

capital. Another distinction is that, labor (with inclusion of business expertise and management

skills) is to be offered jointly by partners/parties, while in Mudaraba, labor is offered by Mudarib

with the contribution of the other parties limited to capital provision.

Q4: Istisna’a denotes a special instance of Salam and they both involve the delivery in

future of a specified item/object. The former is primarily utilized in both large and small scale

manufacturing field, construction, and Build Operate and Transfer (BOT). Salam, on the other

hand, remains limited to commodities trading, especially those which require from seller (al-

muslam ileihi) no alterations or additions. 6 Thus, both terms have a range of differences and

similarities as shown below:

5 Waemustafa, Waeibrorheem, and Suriani Sukri. "Systematic and unsystematic risk determinants of liquidity risk

between Islamic and conventional banks." (2016).

6 Samra, Emily. "Corporate governance in Islamic financial institutions." (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Q5: Alternatives finance include partnership contracts, exchange contracts and financial

assets. The partnership contracts are allowed through Mudaraba and Musharaka. Mudaraba

allows one partner to supply capital to the other party called mudarib for to process some trade

on terms that the realized profits will be shared in mutually agreed percentage whereas all capital

loss will be borne on capital provider. Musharakah contract is identical to conventional

partnership arrangement in which each party does contributes capital in specific capacity. Each

partner has right to management in proportion to investment. For example, permanent

Musharakah can be used to fund a project where bank participates in equity of a given company

and accepts the annual share of profit on the basis of pro rata. The exchange contracts uses

working capital financing of each financial system. Financial assets include tradable Islamic

financial assets which include Mudarabah certificates, Musharakah certificates, redeemable

Musharakah certificates, fixed and floating rate Ijara certificates. The non-tradable zero-coupon

certificates which include Istisna’ and Murabaha certificates and Salam certificates. The

financier’s potential problem is that unlike non-Islamic loan whereby client remains liable for

Q5: Alternatives finance include partnership contracts, exchange contracts and financial

assets. The partnership contracts are allowed through Mudaraba and Musharaka. Mudaraba

allows one partner to supply capital to the other party called mudarib for to process some trade

on terms that the realized profits will be shared in mutually agreed percentage whereas all capital

loss will be borne on capital provider. Musharakah contract is identical to conventional

partnership arrangement in which each party does contributes capital in specific capacity. Each

partner has right to management in proportion to investment. For example, permanent

Musharakah can be used to fund a project where bank participates in equity of a given company

and accepts the annual share of profit on the basis of pro rata. The exchange contracts uses

working capital financing of each financial system. Financial assets include tradable Islamic

financial assets which include Mudarabah certificates, Musharakah certificates, redeemable

Musharakah certificates, fixed and floating rate Ijara certificates. The non-tradable zero-coupon

certificates which include Istisna’ and Murabaha certificates and Salam certificates. The

financier’s potential problem is that unlike non-Islamic loan whereby client remains liable for

5

each cost consumed because of natural disaster or even theft, under the Islamic home finance,

loss must be shared among asset co-owners based on their shares. In presence of default, the

financier gives the borrower duration to continue with share purchase. The financier can tackle

this problem by ensuring that they do not loan much and also by ensuring that they use the

diminishing Musharaka. 7

Q6: In Mudaraba structure, the risk to the lender is that where there is a capital loss, he

bears all of it alone despite having provided the capital alone. The entrepreneur or the recipient

of the capital only bears the brunt of opportunity cost of time as well as labor.

Q7: The board is established by a financial institution, Islamic bank/Islamic insurance

company for advising and certain financial products. The DJIM was launched in 1999 as the 1st

index established for investors pursuing investment in conformity with Muslim Sharia law. It

includes thousands of blue-chip, broad-market, fixed-income and strategy alongside thematic

indices which have passed rules-oriented screens for the compliance with Shari’ah. Some of the

known Shariah scholars include Mufti Muhammad Taqi Usmani, Sheik Abdul Sattar Abu

Ghuddah, Sheik Yusuf Talal DeLorenzo and Dr. Daud Baker.

Q8:8 There are different types of sukuk structures including pure Ijarah, pooled/hybrid,

variable rate redeemable, embedded, zero-coupon non-tradable sukuk. The most viable sukuk

structure in regards to underlying ‘asset’ which was an ‘Islamic receivable’ would be

hybrid/pooled sukuk. 9 This is because it is able to include Murabahah receivable, Istisna’ and

Ijarah. This portfolio with a range of classes permits a greater funds’ mobilization which was

7 Saiti, Buerhan, Obiyathulla Ismath Bacha, and Mansur Masih. "Testing the conventional and Islamic financial

market contagion: evidence from wavelet analysis." Emerging Markets Finance and Trade 52, no. 8 (2016): 1832-

1849.

8 Mohamed Naim, Asmadi, and Zairani Zainol. "Islamic banking: Operation and instruments." (2015).

each cost consumed because of natural disaster or even theft, under the Islamic home finance,

loss must be shared among asset co-owners based on their shares. In presence of default, the

financier gives the borrower duration to continue with share purchase. The financier can tackle

this problem by ensuring that they do not loan much and also by ensuring that they use the

diminishing Musharaka. 7

Q6: In Mudaraba structure, the risk to the lender is that where there is a capital loss, he

bears all of it alone despite having provided the capital alone. The entrepreneur or the recipient

of the capital only bears the brunt of opportunity cost of time as well as labor.

Q7: The board is established by a financial institution, Islamic bank/Islamic insurance

company for advising and certain financial products. The DJIM was launched in 1999 as the 1st

index established for investors pursuing investment in conformity with Muslim Sharia law. It

includes thousands of blue-chip, broad-market, fixed-income and strategy alongside thematic

indices which have passed rules-oriented screens for the compliance with Shari’ah. Some of the

known Shariah scholars include Mufti Muhammad Taqi Usmani, Sheik Abdul Sattar Abu

Ghuddah, Sheik Yusuf Talal DeLorenzo and Dr. Daud Baker.

Q8:8 There are different types of sukuk structures including pure Ijarah, pooled/hybrid,

variable rate redeemable, embedded, zero-coupon non-tradable sukuk. The most viable sukuk

structure in regards to underlying ‘asset’ which was an ‘Islamic receivable’ would be

hybrid/pooled sukuk. 9 This is because it is able to include Murabahah receivable, Istisna’ and

Ijarah. This portfolio with a range of classes permits a greater funds’ mobilization which was

7 Saiti, Buerhan, Obiyathulla Ismath Bacha, and Mansur Masih. "Testing the conventional and Islamic financial

market contagion: evidence from wavelet analysis." Emerging Markets Finance and Trade 52, no. 8 (2016): 1832-

1849.

8 Mohamed Naim, Asmadi, and Zairani Zainol. "Islamic banking: Operation and instruments." (2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

inaccessible previously in Istisna and Murabaha assets. Because Murabahah and Istisna’

receivable remained part of pool, the returns on such certificates are only pre-determined fixed

return rate.

Q9: The context which results in Sheik Muhammad Taqi Usmani to observe this

observation is the need to prevent the risk associated with Sukuk structures in order that their

transactions comply with the Shari’a. By having Islamic banks and financial institutions

cooperating among themselves and with effective guidance alongside encouragement of Sharia

supervisory board, the Sukuk transactions will always adhere to the Shari’a and hence beneficial

to the Islamic Finance. This will ensure that Islamic banks and financial institutions do not

engage in transactions that can violate the Sharia to which Muslims hold high regards. The banks

will be more compliance to the Shari’a laws and hence will adhere to such prohibitions including

riba, gharar and avoidance of the unethical investment as well as services. The Shariah scholars

are unanimous in the disapproval of investment in the business industry which could be deemed

unethical like tobacco companies, casinos, sex-business, and wineries. Thus they must adhere to

the market discipline which has transformed such ethical issues to the methods of screening

stock. This is exemplified in the Dow Jones as well as Financial Time’s Islamic market indices.

Thus these institutions must comply with Muslims who regard religion as more than the rituals

prescribed. Thus by this observation, the Sheik is coming from the context that without these

compliance, then Shariah laws can be violated.

9 Askari, Hossein, and Noureddine Krichene. "Islamic finance: an alternative financial system for stability, equity,

and growth." (2014).

inaccessible previously in Istisna and Murabaha assets. Because Murabahah and Istisna’

receivable remained part of pool, the returns on such certificates are only pre-determined fixed

return rate.

Q9: The context which results in Sheik Muhammad Taqi Usmani to observe this

observation is the need to prevent the risk associated with Sukuk structures in order that their

transactions comply with the Shari’a. By having Islamic banks and financial institutions

cooperating among themselves and with effective guidance alongside encouragement of Sharia

supervisory board, the Sukuk transactions will always adhere to the Shari’a and hence beneficial

to the Islamic Finance. This will ensure that Islamic banks and financial institutions do not

engage in transactions that can violate the Sharia to which Muslims hold high regards. The banks

will be more compliance to the Shari’a laws and hence will adhere to such prohibitions including

riba, gharar and avoidance of the unethical investment as well as services. The Shariah scholars

are unanimous in the disapproval of investment in the business industry which could be deemed

unethical like tobacco companies, casinos, sex-business, and wineries. Thus they must adhere to

the market discipline which has transformed such ethical issues to the methods of screening

stock. This is exemplified in the Dow Jones as well as Financial Time’s Islamic market indices.

Thus these institutions must comply with Muslims who regard religion as more than the rituals

prescribed. Thus by this observation, the Sheik is coming from the context that without these

compliance, then Shariah laws can be violated.

9 Askari, Hossein, and Noureddine Krichene. "Islamic finance: an alternative financial system for stability, equity,

and growth." (2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Bibliography

Askari, Hossein, and Noureddine Krichene. "Islamic finance: an alternative financial system for

stability, equity, and growth." (2014).

Askari, Hossein, Noureddine Krichene, and Abbas Mirakhor. "On the stability of an Islamic

financial system." (2014).

Bibliography

Askari, Hossein, and Noureddine Krichene. "Islamic finance: an alternative financial system for

stability, equity, and growth." (2014).

Askari, Hossein, Noureddine Krichene, and Abbas Mirakhor. "On the stability of an Islamic

financial system." (2014).

8

El-Karanshawy, Hatem A., Azmi Omar, Tariqullah Khan, Salman Syed Ali, Hylmun Izhar,

Wijdan Tariq, Karim Ginena, and Bahnaz Al Quradaghi. "Financial Stability and Risk

Management in Islamic Financial Institutions." (2015).

Kenourgios, Dimitris, Nader Naifar, and Dimitrios Dimitriou. "Islamic financial markets and

global crises: Contagion or decoupling?." Economic Modelling 57 (2016): 36-46.

Mohamed Naim, Asmadi, and Zairani Zainol. "Islamic banking: Operation and instruments."

(2015).

Rahman, Farhat Naz. "Theory of Islamic Financial System and Economic growth." JOURNAL

OF CREATIVE WRITING| ISSN 2410-6259 3, no. 01 (2017): 66-82.

Saiti, Buerhan, Obiyathulla Ismath Bacha, and Mansur Masih. "Testing the conventional and

Islamic financial market contagion: evidence from wavelet analysis." Emerging Markets Finance

and Trade 52, no. 8 (2016): 1832-1849.

Samra, Emily. "Corporate governance in Islamic financial institutions." (2016).

Waemustafa, Waeibrorheem, and Suriani Sukri. "Systematic and unsystematic risk determinants

of liquidity risk between Islamic and conventional banks." (2016).

http://sbp.org.pk/departments/ibd/sukuk-risks.pdf

El-Karanshawy, Hatem A., Azmi Omar, Tariqullah Khan, Salman Syed Ali, Hylmun Izhar,

Wijdan Tariq, Karim Ginena, and Bahnaz Al Quradaghi. "Financial Stability and Risk

Management in Islamic Financial Institutions." (2015).

Kenourgios, Dimitris, Nader Naifar, and Dimitrios Dimitriou. "Islamic financial markets and

global crises: Contagion or decoupling?." Economic Modelling 57 (2016): 36-46.

Mohamed Naim, Asmadi, and Zairani Zainol. "Islamic banking: Operation and instruments."

(2015).

Rahman, Farhat Naz. "Theory of Islamic Financial System and Economic growth." JOURNAL

OF CREATIVE WRITING| ISSN 2410-6259 3, no. 01 (2017): 66-82.

Saiti, Buerhan, Obiyathulla Ismath Bacha, and Mansur Masih. "Testing the conventional and

Islamic financial market contagion: evidence from wavelet analysis." Emerging Markets Finance

and Trade 52, no. 8 (2016): 1832-1849.

Samra, Emily. "Corporate governance in Islamic financial institutions." (2016).

Waemustafa, Waeibrorheem, and Suriani Sukri. "Systematic and unsystematic risk determinants

of liquidity risk between Islamic and conventional banks." (2016).

http://sbp.org.pk/departments/ibd/sukuk-risks.pdf

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.