Islamic FinTech: EWA, Shariah Compliance, and Regulatory Environment

VerifiedAdded on 2023/01/09

|14

|836

|56

Presentation

AI Summary

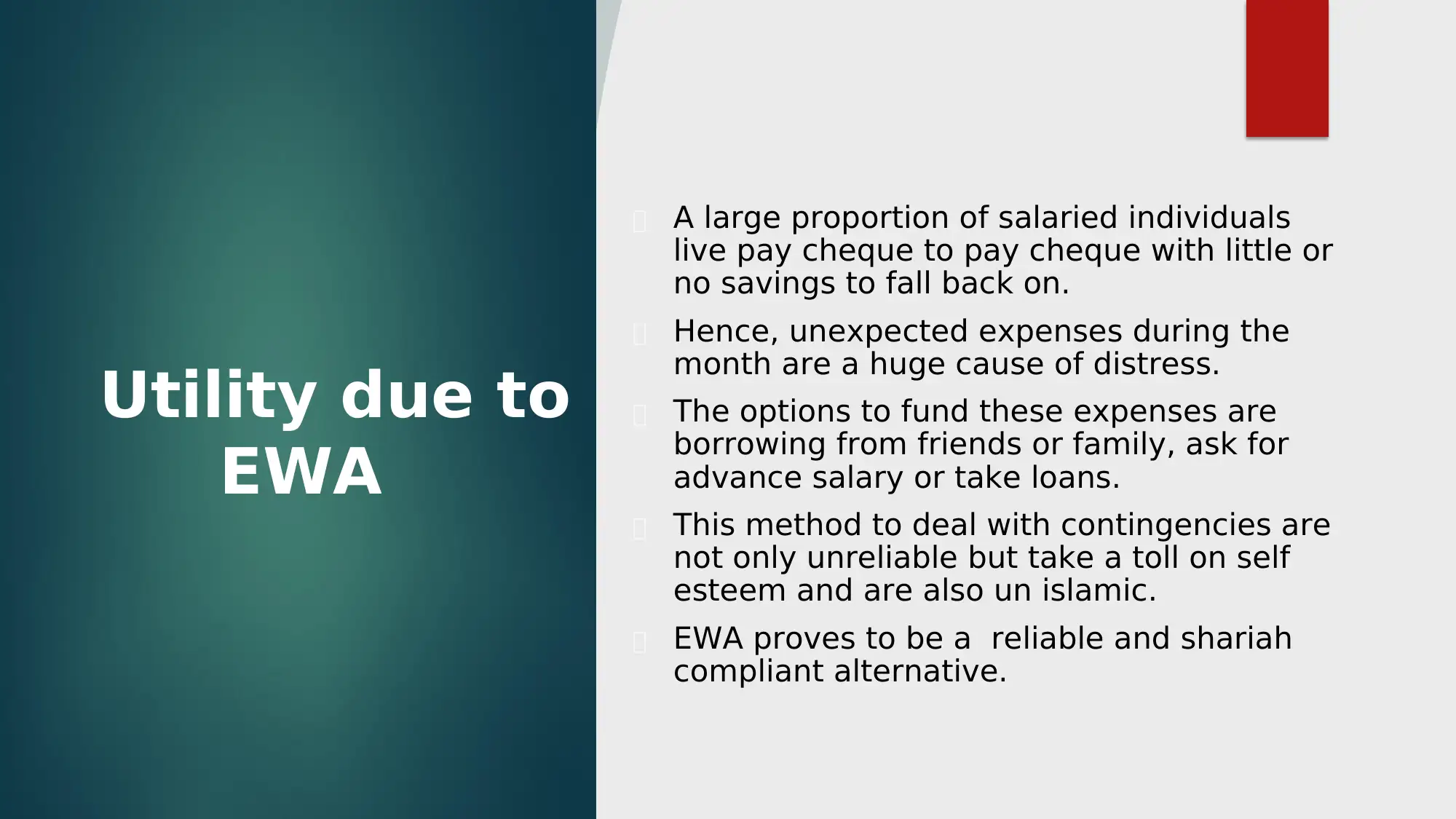

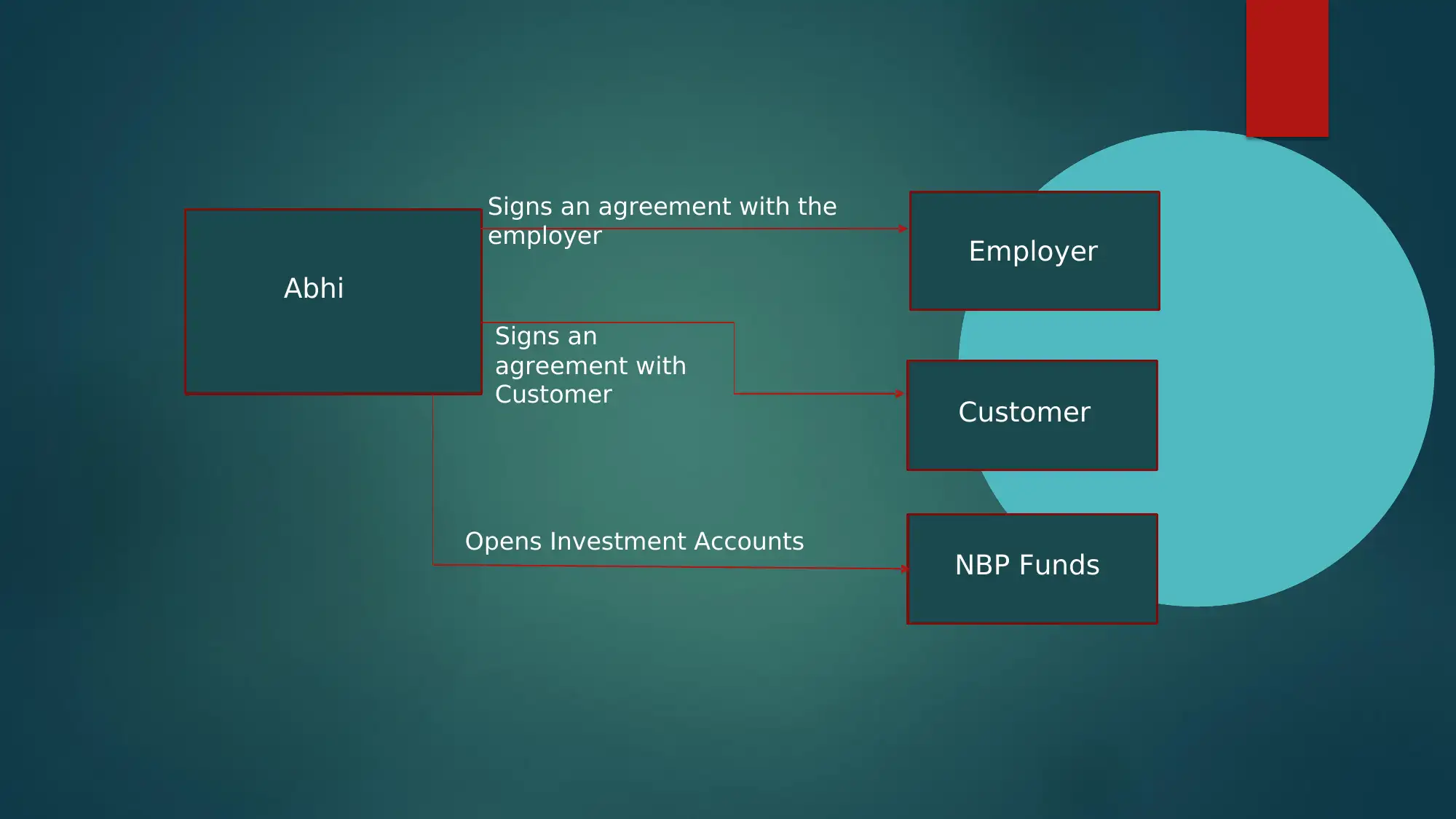

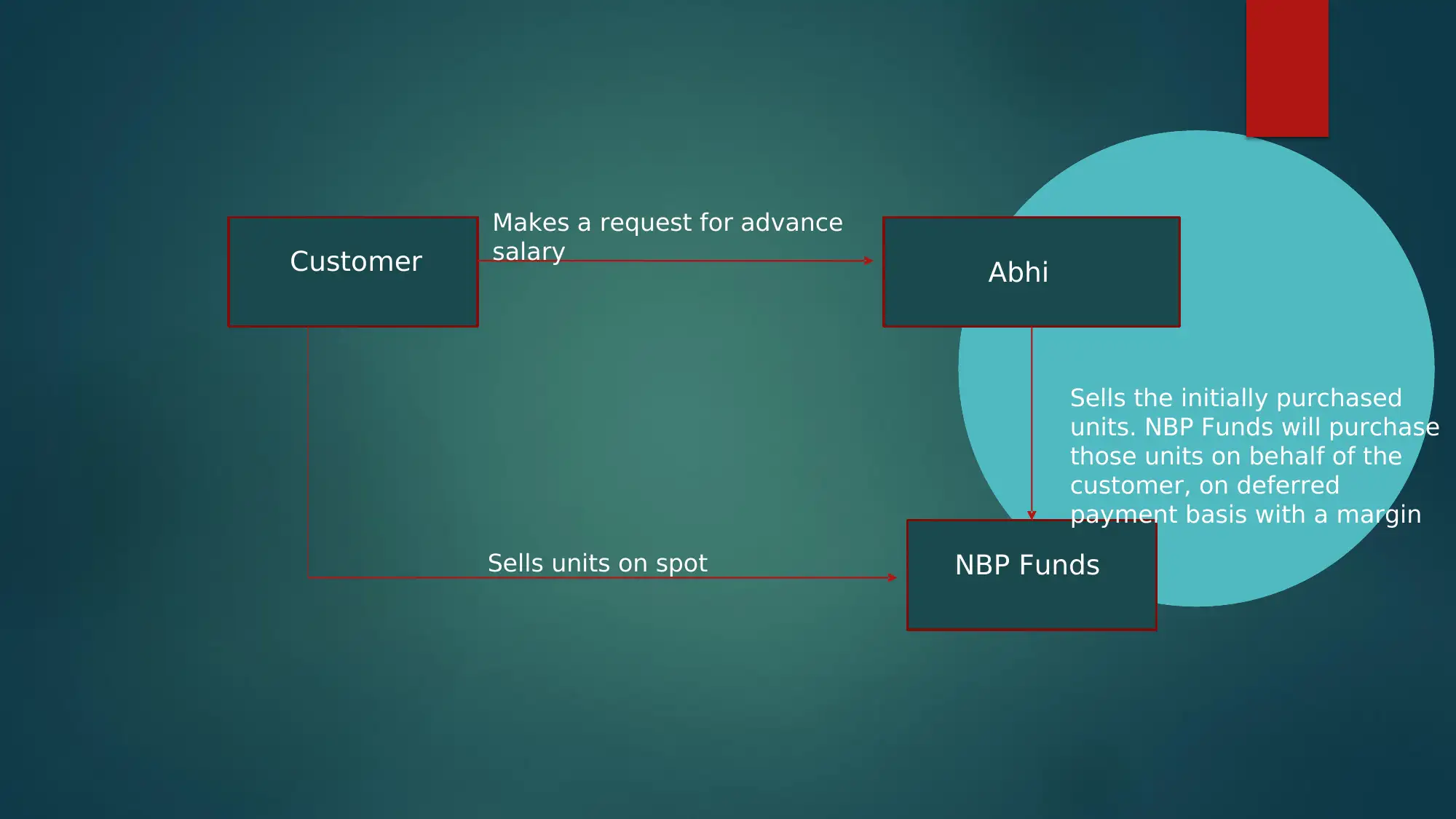

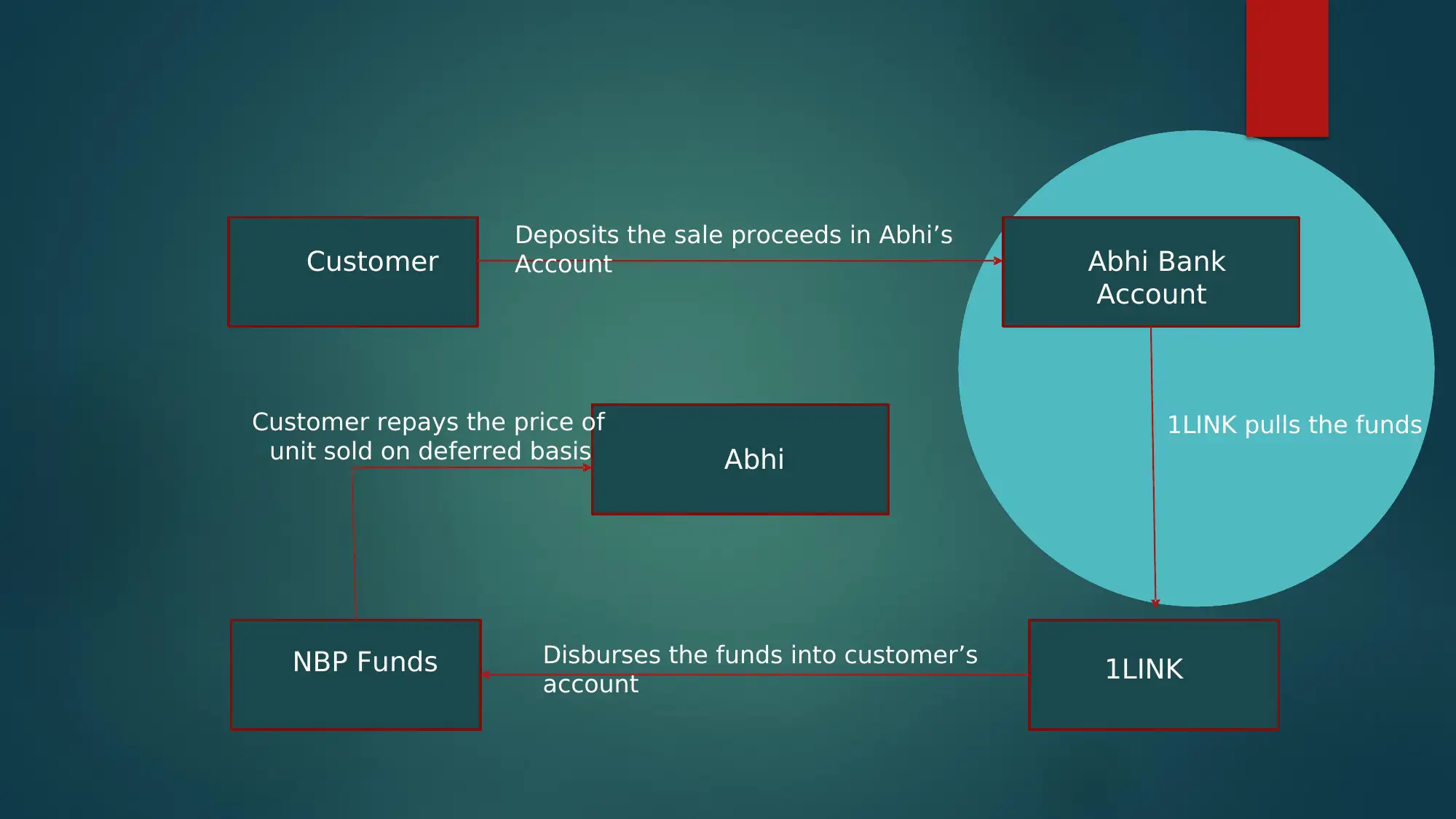

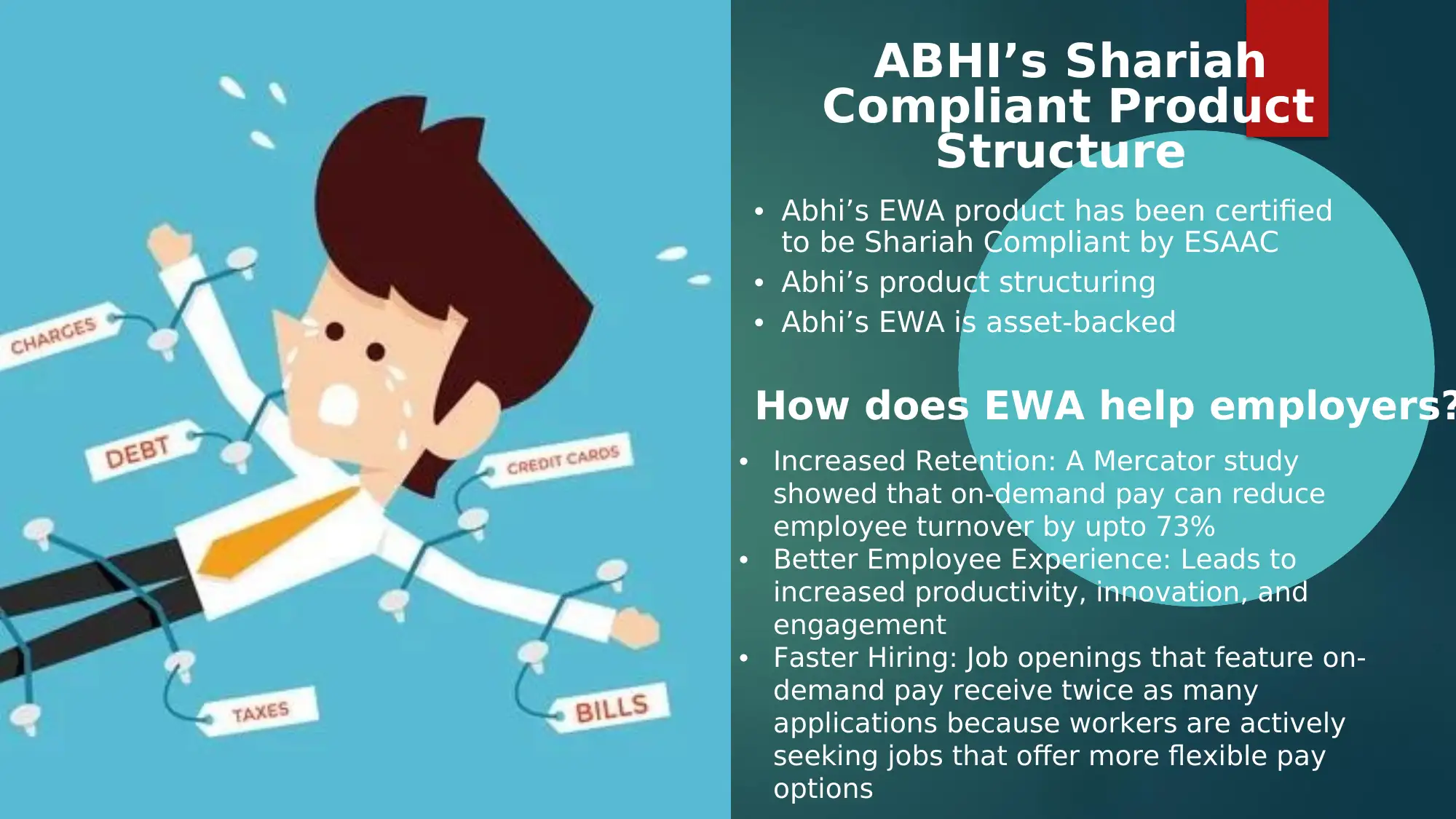

This presentation provides an overview of Islamic FinTech, explaining the core concepts of FinTech and its evolution, including the rise of Islamic FinTech. It delves into the regulatory environment and the significance of Shariah compliance within the industry. A major focus is placed on Earned Wage Access (EWA) as a specific Islamic FinTech product, highlighting its structure, benefits for both employers and employees, and its Shariah-compliant aspects, contrasting it with conventional non-Shariah-compliant EWA models. The presentation also examines the utility of EWA, addressing its role in providing a reliable and Shariah-compliant alternative to traditional financial challenges faced by salaried individuals, and concludes with a thank you slide.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.