Investigating ISO 9000 Adoption Factors & Impact on Firm Performance

VerifiedAdded on 2023/06/11

|18

|3943

|409

Report

AI Summary

This report investigates the factors influencing the adoption of ISO 9000 certification and its subsequent impact on firm performance, focusing on service firms in China from 2004 to 2008. Using a panel data approach and ordinary least squares regression, the study examines the relationship between ISO 9000 certification and variables such as employee number, company age, return on sales, and return on assets. The research also employs an independent samples t-test to compare the financial performance of certified and non-certified firms. The findings indicate a significant association between certification status and industry, with certified firms demonstrating higher profitability. Key determinants of ISO 9000 certification include employee number and company age (positively related) and return on sales and return on assets (negatively related). The report concludes with managerial advice and suggestions for future research, acknowledging limitations in the current study.

Statistics and business research method

Name:

Institution:

26th May 2018

Name:

Institution:

26th May 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

Research Questions......................................................................................................................5

Literature review and hypothesis development...............................................................................5

Research methodology and design..................................................................................................7

Analyses and findings......................................................................................................................8

Descriptive statistics:...................................................................................................................8

Inferential statistics:...................................................................................................................10

Chi-Square test.......................................................................................................................10

Independent t-test...................................................................................................................11

Logistic regression.................................................................................................................12

Discussion and managerial advises...............................................................................................14

Limitations and directions for future research...............................................................................14

References......................................................................................................................................15

Appendix........................................................................................................................................18

Executive Summary.........................................................................................................................3

Introduction......................................................................................................................................4

Research Questions......................................................................................................................5

Literature review and hypothesis development...............................................................................5

Research methodology and design..................................................................................................7

Analyses and findings......................................................................................................................8

Descriptive statistics:...................................................................................................................8

Inferential statistics:...................................................................................................................10

Chi-Square test.......................................................................................................................10

Independent t-test...................................................................................................................11

Logistic regression.................................................................................................................12

Discussion and managerial advises...............................................................................................14

Limitations and directions for future research...............................................................................14

References......................................................................................................................................15

Appendix........................................................................................................................................18

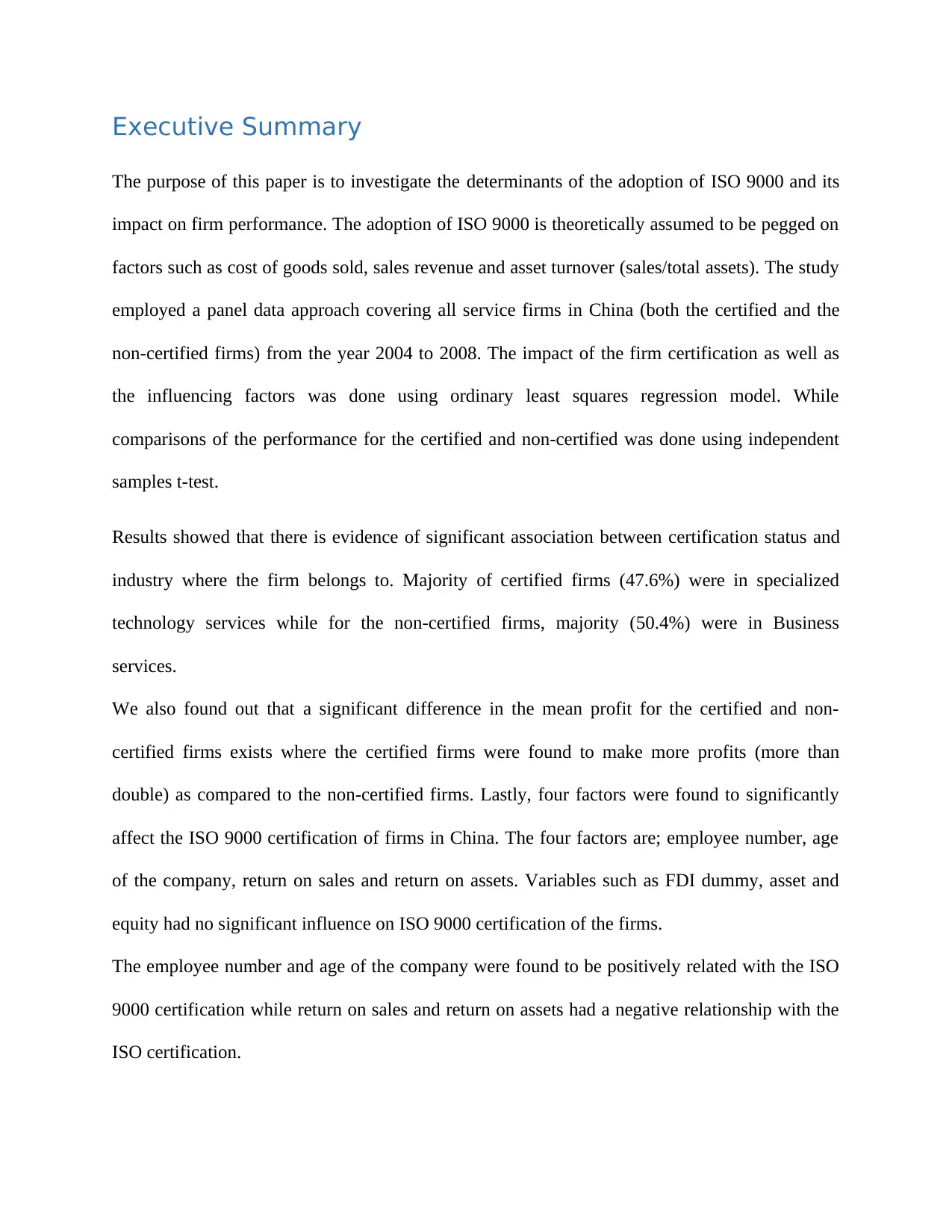

Executive Summary

The purpose of this paper is to investigate the determinants of the adoption of ISO 9000 and its

impact on firm performance. The adoption of ISO 9000 is theoretically assumed to be pegged on

factors such as cost of goods sold, sales revenue and asset turnover (sales/total assets). The study

employed a panel data approach covering all service firms in China (both the certified and the

non-certified firms) from the year 2004 to 2008. The impact of the firm certification as well as

the influencing factors was done using ordinary least squares regression model. While

comparisons of the performance for the certified and non-certified was done using independent

samples t-test.

Results showed that there is evidence of significant association between certification status and

industry where the firm belongs to. Majority of certified firms (47.6%) were in specialized

technology services while for the non-certified firms, majority (50.4%) were in Business

services.

We also found out that a significant difference in the mean profit for the certified and non-

certified firms exists where the certified firms were found to make more profits (more than

double) as compared to the non-certified firms. Lastly, four factors were found to significantly

affect the ISO 9000 certification of firms in China. The four factors are; employee number, age

of the company, return on sales and return on assets. Variables such as FDI dummy, asset and

equity had no significant influence on ISO 9000 certification of the firms.

The employee number and age of the company were found to be positively related with the ISO

9000 certification while return on sales and return on assets had a negative relationship with the

ISO certification.

The purpose of this paper is to investigate the determinants of the adoption of ISO 9000 and its

impact on firm performance. The adoption of ISO 9000 is theoretically assumed to be pegged on

factors such as cost of goods sold, sales revenue and asset turnover (sales/total assets). The study

employed a panel data approach covering all service firms in China (both the certified and the

non-certified firms) from the year 2004 to 2008. The impact of the firm certification as well as

the influencing factors was done using ordinary least squares regression model. While

comparisons of the performance for the certified and non-certified was done using independent

samples t-test.

Results showed that there is evidence of significant association between certification status and

industry where the firm belongs to. Majority of certified firms (47.6%) were in specialized

technology services while for the non-certified firms, majority (50.4%) were in Business

services.

We also found out that a significant difference in the mean profit for the certified and non-

certified firms exists where the certified firms were found to make more profits (more than

double) as compared to the non-certified firms. Lastly, four factors were found to significantly

affect the ISO 9000 certification of firms in China. The four factors are; employee number, age

of the company, return on sales and return on assets. Variables such as FDI dummy, asset and

equity had no significant influence on ISO 9000 certification of the firms.

The employee number and age of the company were found to be positively related with the ISO

9000 certification while return on sales and return on assets had a negative relationship with the

ISO certification.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The concept of ISO 9000 series of value administration frameworks standard has been broadly

applauded worldwide since its inception in 1987. Beginning of 2014 saw over 1million facilities

adopting ISO 9000 in close to 189 countries. Practitioners and academicians are enthusiastic in

understanding the influencing factors that determine the adoption of ISO 9000 and the impact

these factors have on financial performance of the firms (Benner & Veloso , 2008).

The current study sought to explore whether the ISO 9000 accreditation is a vital factor

influencing firms' present and future performance. Specifically, we center the study on whether

the ownership of an ISO 9000 affirmation, which is viewed as demonstrative of a company's

quality administration framework, is in the end converted into a change of the company's

financial performance (Du, Yin, & Zhang, 2016).

In doing as such, we look at the impact of the ISO 9000 accreditation on the monetary

performance of traded on an open market firms by contrasting the groups of firms that hold the

ISO 9000 accreditation with a control group of firms that have never gained such a certification,

utilizing both unmatched and matched analysis (Nakamura, Takahashi, & Vertinsky, 2001).

Moreover, the impact of the ISO 9000 affirmation is inspected by looking at the monetary

performance in the certified subgroups. The investigation is pegged on census data of the service

firms that was conducted by the National Bureau of Statistics of China in 2008.

The contributions from this investigation to existing body of knowledge is three-fold. Right off

the bat, the investigation utilizes a sample comprising of the considerable number of firms in the

The concept of ISO 9000 series of value administration frameworks standard has been broadly

applauded worldwide since its inception in 1987. Beginning of 2014 saw over 1million facilities

adopting ISO 9000 in close to 189 countries. Practitioners and academicians are enthusiastic in

understanding the influencing factors that determine the adoption of ISO 9000 and the impact

these factors have on financial performance of the firms (Benner & Veloso , 2008).

The current study sought to explore whether the ISO 9000 accreditation is a vital factor

influencing firms' present and future performance. Specifically, we center the study on whether

the ownership of an ISO 9000 affirmation, which is viewed as demonstrative of a company's

quality administration framework, is in the end converted into a change of the company's

financial performance (Du, Yin, & Zhang, 2016).

In doing as such, we look at the impact of the ISO 9000 accreditation on the monetary

performance of traded on an open market firms by contrasting the groups of firms that hold the

ISO 9000 accreditation with a control group of firms that have never gained such a certification,

utilizing both unmatched and matched analysis (Nakamura, Takahashi, & Vertinsky, 2001).

Moreover, the impact of the ISO 9000 affirmation is inspected by looking at the monetary

performance in the certified subgroups. The investigation is pegged on census data of the service

firms that was conducted by the National Bureau of Statistics of China in 2008.

The contributions from this investigation to existing body of knowledge is three-fold. Right off

the bat, the investigation utilizes a sample comprising of the considerable number of firms in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

service industry (Chatzoglou, Chatzoudes, & Kipraios , The impact of ISO 9000 certification on

firms’ financial performance, 2015). Besides, a more significant examination is performed in

view of both unmatched and matched sample strategies utilizing coarsened exact matching

systems to match the ISO 9000 accredited firms with the control firms.

Research Questions

The study sought to answer three research questions. The three research questions are;

Q1: Is there significant difference in the financial performance of the ISO 9000 certified firms

and the non-certified firms?

Q2: What factors significantly influence the adoption of ISO 9000 certification by companies?

Q3: Is there association between ISO 900 certification and the industry where the firm operates

in?

Literature review and hypothesis development

Existing body of knowledge examines the impact on company's money related performance as a

result of the adoption of the ISO 9000 certification. As earlier mentioned, a substantial

assortment of existing literature gives blended and clashing confirmation with respect to the

connection between ISO 9000 accreditation and organization's financial performance. Different

investigations contend that there exists a solid and positive connection while other scholars

contend that such a connection are feeble or even negative. The non-existent or weak role of the

ISO 9000 accreditation on company's financial performance is accounted for by existing

examinations.

firms’ financial performance, 2015). Besides, a more significant examination is performed in

view of both unmatched and matched sample strategies utilizing coarsened exact matching

systems to match the ISO 9000 accredited firms with the control firms.

Research Questions

The study sought to answer three research questions. The three research questions are;

Q1: Is there significant difference in the financial performance of the ISO 9000 certified firms

and the non-certified firms?

Q2: What factors significantly influence the adoption of ISO 9000 certification by companies?

Q3: Is there association between ISO 900 certification and the industry where the firm operates

in?

Literature review and hypothesis development

Existing body of knowledge examines the impact on company's money related performance as a

result of the adoption of the ISO 9000 certification. As earlier mentioned, a substantial

assortment of existing literature gives blended and clashing confirmation with respect to the

connection between ISO 9000 accreditation and organization's financial performance. Different

investigations contend that there exists a solid and positive connection while other scholars

contend that such a connection are feeble or even negative. The non-existent or weak role of the

ISO 9000 accreditation on company's financial performance is accounted for by existing

examinations.

The investigation of Singels et al. (2001), finds that the execution of the ISO 9000 confirmed

firms isn't superior to that of non-certified firms. Additionally, the investigation of Lima et al.

(2005), finds that there is no distinction with respect to the financial performance between the

ISO 9000 affirmed firms and a control group of comparative non-certified firms.

In a similar line, the examination of Wayhan et al. (2002), reports that the effect of ISO 9000

accreditation on the organization's financial performance, measured by return on assets (ROA), is

extremely constrained and this impact rapidly blurs away after some time. Correspondingly, the

investigation of Martinez-Costa and Martinez-Lorente (2007), reports that the ISO 9000

accreditation effect is negative as affirmed firms receive less profit and ROA in the post three-

year accreditation period.

Moreover, the investigation of Naveh and Marcus (2005), reports that the ISO 9000 certified

firms are not profited from the accreditation as the accreditation does not prompt an expansion in

their profitability. Furthermore, the exploration of Tsekouras et al. (2002), utilizing a sample of

143 Greek firms that embraced ISO 9000 schemes in the vicinity of 1989 and 1993 and

comparative non-adopters, finds no impact of the ISO 9000 accreditation on firm's performance.

Then again, it creates the impression that more recent examinations demonstrate a solid and

positive relationship between ISO 9000 certification and company's financial performance.

The investigation of Sharma (2005), finds that the monetary performance of the ISO 9000

affirmed firms, is essentially more prominent in contrast with the money related performance of

matched non-certified firms (particularly in net revenue). In a similar vein, the investigation of

Corbett et al. (2005), finds that traded on an open market ISO 9000 accredited US firms

demonstrate essential unusual money related performance improvements three years after

accreditation, in all instances of the matched control groups studied. Moreover, the examination

firms isn't superior to that of non-certified firms. Additionally, the investigation of Lima et al.

(2005), finds that there is no distinction with respect to the financial performance between the

ISO 9000 affirmed firms and a control group of comparative non-certified firms.

In a similar line, the examination of Wayhan et al. (2002), reports that the effect of ISO 9000

accreditation on the organization's financial performance, measured by return on assets (ROA), is

extremely constrained and this impact rapidly blurs away after some time. Correspondingly, the

investigation of Martinez-Costa and Martinez-Lorente (2007), reports that the ISO 9000

accreditation effect is negative as affirmed firms receive less profit and ROA in the post three-

year accreditation period.

Moreover, the investigation of Naveh and Marcus (2005), reports that the ISO 9000 certified

firms are not profited from the accreditation as the accreditation does not prompt an expansion in

their profitability. Furthermore, the exploration of Tsekouras et al. (2002), utilizing a sample of

143 Greek firms that embraced ISO 9000 schemes in the vicinity of 1989 and 1993 and

comparative non-adopters, finds no impact of the ISO 9000 accreditation on firm's performance.

Then again, it creates the impression that more recent examinations demonstrate a solid and

positive relationship between ISO 9000 certification and company's financial performance.

The investigation of Sharma (2005), finds that the monetary performance of the ISO 9000

affirmed firms, is essentially more prominent in contrast with the money related performance of

matched non-certified firms (particularly in net revenue). In a similar vein, the investigation of

Corbett et al. (2005), finds that traded on an open market ISO 9000 accredited US firms

demonstrate essential unusual money related performance improvements three years after

accreditation, in all instances of the matched control groups studied. Moreover, the examination

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of Chow-Chua, et al. (2005), finds that the ISO 9000 accreditation prompts critical upgrades in

performance, in the five year time frame following confirmation paying little mind to matched

control group specification, however this isn't really the case for business performance

improvements. Also, the investigation of Levine and Toffel (2010), reports that the ISO 9000

accredited firms encounter significantly more prominent development after accreditation

concerning employment, sales and several employee results in contrast with the matched non-

accredited firms. In a similar line, the exploration of Ullah et al. (2014), finds that the ISO

affirmed firms display higher work efficiency and lower cost of sales when contrasted with a

matched control group of non-certified firms. Also, the investigation of Chatzoglou et al. (2015),

finds that the ISO 9000 accreditation is exceptionally connected with general monetary

performance improvements.

Research methodology and design

This section describes how to perform the unmatched and matched analysis of this study based

on the proposed group classification. The unmatched analysis involves comparing the

performance of the ISO 9000 certified groups with a control group of non-certified firms

irrespectively of the different characteristics of the compared firms. The matched analysis

involves comparing the relevant groups (the ISO certified group versus the non-certified) by

including those certified and non-certified firms that share similar characteristics based on

specific pre-certification matching criteria such as firm size, firm age and business. Independent

t-test will be used to compare the financial performance of the two groups (certified and non-

certified groups). In regard to factors influencing certification, a logistic regression model will be

used to test whether there is significant influence of the factors on the dummy variable for

certification (i.e. 1 = certified, 0 = non-certified).

performance, in the five year time frame following confirmation paying little mind to matched

control group specification, however this isn't really the case for business performance

improvements. Also, the investigation of Levine and Toffel (2010), reports that the ISO 9000

accredited firms encounter significantly more prominent development after accreditation

concerning employment, sales and several employee results in contrast with the matched non-

accredited firms. In a similar line, the exploration of Ullah et al. (2014), finds that the ISO

affirmed firms display higher work efficiency and lower cost of sales when contrasted with a

matched control group of non-certified firms. Also, the investigation of Chatzoglou et al. (2015),

finds that the ISO 9000 accreditation is exceptionally connected with general monetary

performance improvements.

Research methodology and design

This section describes how to perform the unmatched and matched analysis of this study based

on the proposed group classification. The unmatched analysis involves comparing the

performance of the ISO 9000 certified groups with a control group of non-certified firms

irrespectively of the different characteristics of the compared firms. The matched analysis

involves comparing the relevant groups (the ISO certified group versus the non-certified) by

including those certified and non-certified firms that share similar characteristics based on

specific pre-certification matching criteria such as firm size, firm age and business. Independent

t-test will be used to compare the financial performance of the two groups (certified and non-

certified groups). In regard to factors influencing certification, a logistic regression model will be

used to test whether there is significant influence of the factors on the dummy variable for

certification (i.e. 1 = certified, 0 = non-certified).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analyses and findings

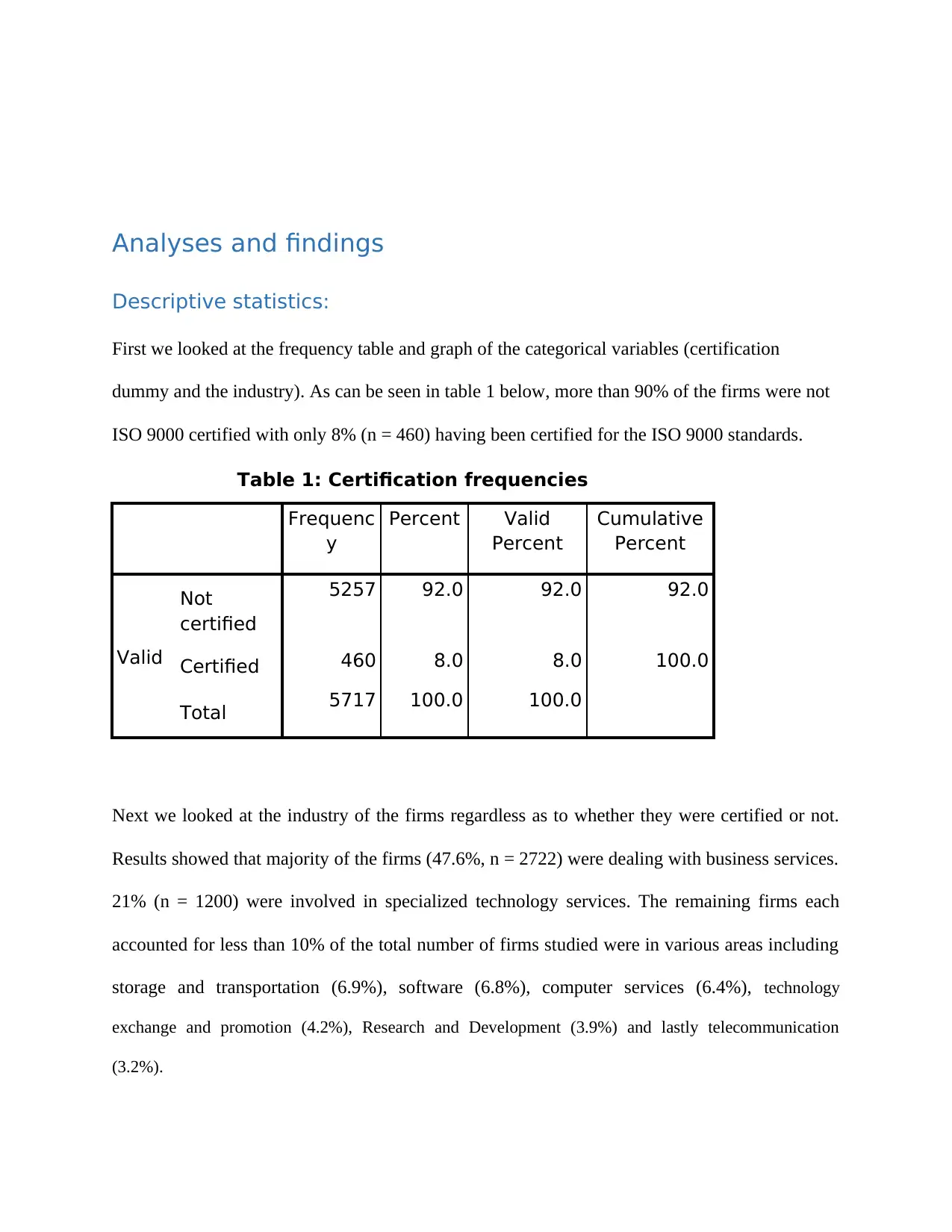

Descriptive statistics:

First we looked at the frequency table and graph of the categorical variables (certification

dummy and the industry). As can be seen in table 1 below, more than 90% of the firms were not

ISO 9000 certified with only 8% (n = 460) having been certified for the ISO 9000 standards.

Table 1: Certification frequencies

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid

Not

certified

5257 92.0 92.0 92.0

Certified 460 8.0 8.0 100.0

Total 5717 100.0 100.0

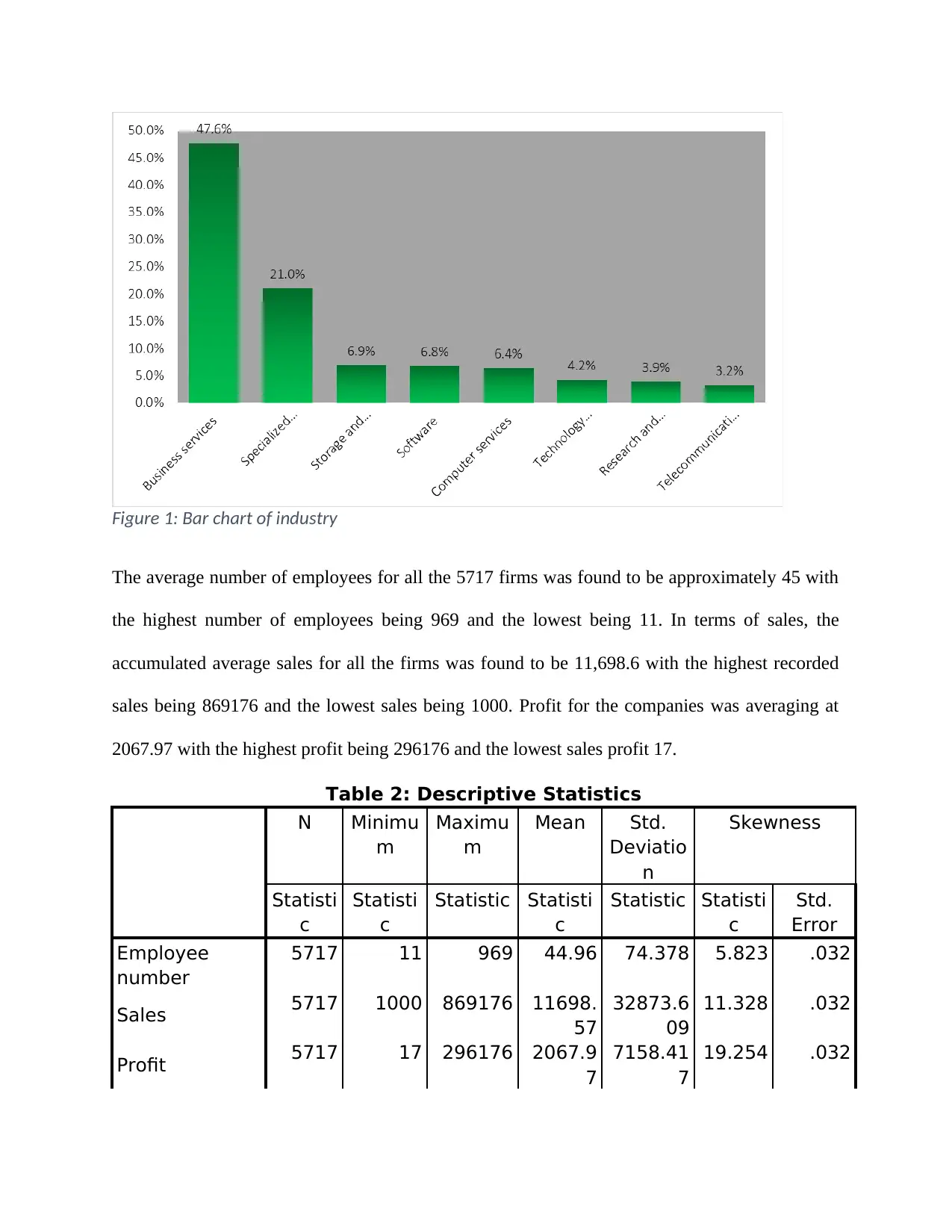

Next we looked at the industry of the firms regardless as to whether they were certified or not.

Results showed that majority of the firms (47.6%, n = 2722) were dealing with business services.

21% (n = 1200) were involved in specialized technology services. The remaining firms each

accounted for less than 10% of the total number of firms studied were in various areas including

storage and transportation (6.9%), software (6.8%), computer services (6.4%), technology

exchange and promotion (4.2%), Research and Development (3.9%) and lastly telecommunication

(3.2%).

Descriptive statistics:

First we looked at the frequency table and graph of the categorical variables (certification

dummy and the industry). As can be seen in table 1 below, more than 90% of the firms were not

ISO 9000 certified with only 8% (n = 460) having been certified for the ISO 9000 standards.

Table 1: Certification frequencies

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid

Not

certified

5257 92.0 92.0 92.0

Certified 460 8.0 8.0 100.0

Total 5717 100.0 100.0

Next we looked at the industry of the firms regardless as to whether they were certified or not.

Results showed that majority of the firms (47.6%, n = 2722) were dealing with business services.

21% (n = 1200) were involved in specialized technology services. The remaining firms each

accounted for less than 10% of the total number of firms studied were in various areas including

storage and transportation (6.9%), software (6.8%), computer services (6.4%), technology

exchange and promotion (4.2%), Research and Development (3.9%) and lastly telecommunication

(3.2%).

Figure 1: Bar chart of industry

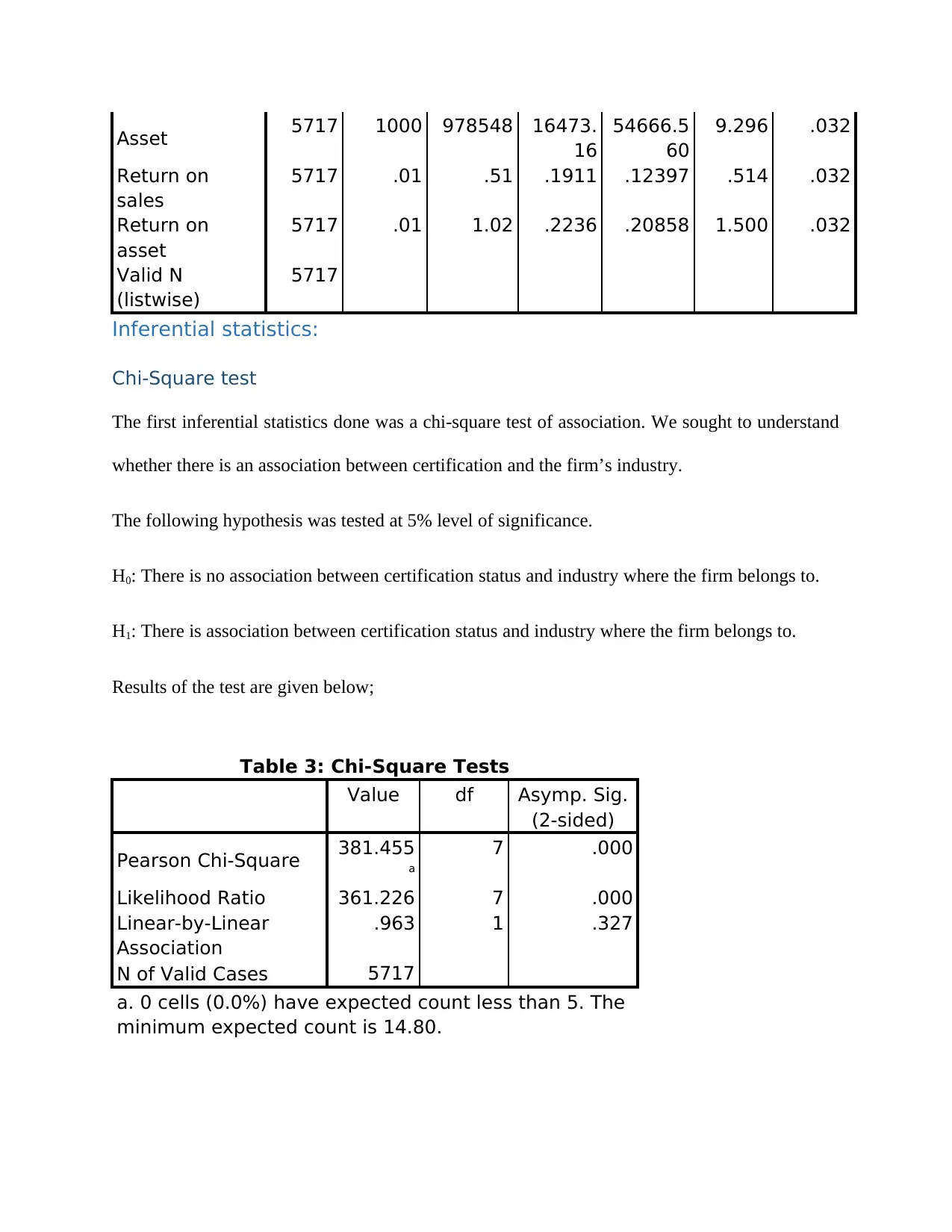

The average number of employees for all the 5717 firms was found to be approximately 45 with

the highest number of employees being 969 and the lowest being 11. In terms of sales, the

accumulated average sales for all the firms was found to be 11,698.6 with the highest recorded

sales being 869176 and the lowest sales being 1000. Profit for the companies was averaging at

2067.97 with the highest profit being 296176 and the lowest sales profit 17.

Table 2: Descriptive Statistics

N Minimu

m

Maximu

m

Mean Std.

Deviatio

n

Skewness

Statisti

c

Statisti

c

Statistic Statisti

c

Statistic Statisti

c

Std.

Error

Employee

number

5717 11 969 44.96 74.378 5.823 .032

Sales 5717 1000 869176 11698.

57

32873.6

09

11.328 .032

Profit 5717 17 296176 2067.9

7

7158.41

7

19.254 .032

The average number of employees for all the 5717 firms was found to be approximately 45 with

the highest number of employees being 969 and the lowest being 11. In terms of sales, the

accumulated average sales for all the firms was found to be 11,698.6 with the highest recorded

sales being 869176 and the lowest sales being 1000. Profit for the companies was averaging at

2067.97 with the highest profit being 296176 and the lowest sales profit 17.

Table 2: Descriptive Statistics

N Minimu

m

Maximu

m

Mean Std.

Deviatio

n

Skewness

Statisti

c

Statisti

c

Statistic Statisti

c

Statistic Statisti

c

Std.

Error

Employee

number

5717 11 969 44.96 74.378 5.823 .032

Sales 5717 1000 869176 11698.

57

32873.6

09

11.328 .032

Profit 5717 17 296176 2067.9

7

7158.41

7

19.254 .032

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Asset 5717 1000 978548 16473.

16

54666.5

60

9.296 .032

Return on

sales

5717 .01 .51 .1911 .12397 .514 .032

Return on

asset

5717 .01 1.02 .2236 .20858 1.500 .032

Valid N

(listwise)

5717

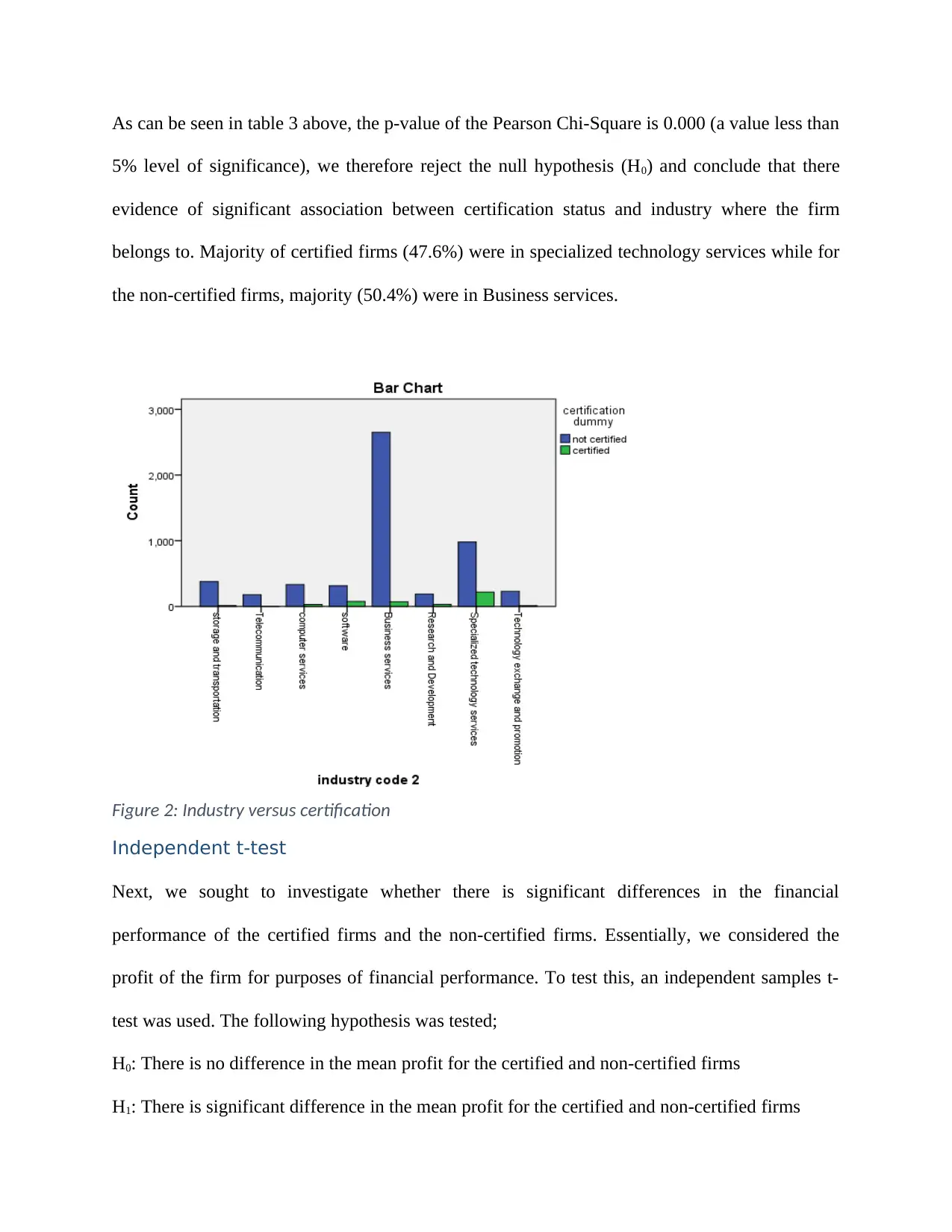

Inferential statistics:

Chi-Square test

The first inferential statistics done was a chi-square test of association. We sought to understand

whether there is an association between certification and the firm’s industry.

The following hypothesis was tested at 5% level of significance.

H0: There is no association between certification status and industry where the firm belongs to.

H1: There is association between certification status and industry where the firm belongs to.

Results of the test are given below;

Table 3: Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 381.455

a

7 .000

Likelihood Ratio 361.226 7 .000

Linear-by-Linear

Association

.963 1 .327

N of Valid Cases 5717

a. 0 cells (0.0%) have expected count less than 5. The

minimum expected count is 14.80.

16

54666.5

60

9.296 .032

Return on

sales

5717 .01 .51 .1911 .12397 .514 .032

Return on

asset

5717 .01 1.02 .2236 .20858 1.500 .032

Valid N

(listwise)

5717

Inferential statistics:

Chi-Square test

The first inferential statistics done was a chi-square test of association. We sought to understand

whether there is an association between certification and the firm’s industry.

The following hypothesis was tested at 5% level of significance.

H0: There is no association between certification status and industry where the firm belongs to.

H1: There is association between certification status and industry where the firm belongs to.

Results of the test are given below;

Table 3: Chi-Square Tests

Value df Asymp. Sig.

(2-sided)

Pearson Chi-Square 381.455

a

7 .000

Likelihood Ratio 361.226 7 .000

Linear-by-Linear

Association

.963 1 .327

N of Valid Cases 5717

a. 0 cells (0.0%) have expected count less than 5. The

minimum expected count is 14.80.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As can be seen in table 3 above, the p-value of the Pearson Chi-Square is 0.000 (a value less than

5% level of significance), we therefore reject the null hypothesis (H0) and conclude that there

evidence of significant association between certification status and industry where the firm

belongs to. Majority of certified firms (47.6%) were in specialized technology services while for

the non-certified firms, majority (50.4%) were in Business services.

Figure 2: Industry versus certification

Independent t-test

Next, we sought to investigate whether there is significant differences in the financial

performance of the certified firms and the non-certified firms. Essentially, we considered the

profit of the firm for purposes of financial performance. To test this, an independent samples t-

test was used. The following hypothesis was tested;

H0: There is no difference in the mean profit for the certified and non-certified firms

H1: There is significant difference in the mean profit for the certified and non-certified firms

5% level of significance), we therefore reject the null hypothesis (H0) and conclude that there

evidence of significant association between certification status and industry where the firm

belongs to. Majority of certified firms (47.6%) were in specialized technology services while for

the non-certified firms, majority (50.4%) were in Business services.

Figure 2: Industry versus certification

Independent t-test

Next, we sought to investigate whether there is significant differences in the financial

performance of the certified firms and the non-certified firms. Essentially, we considered the

profit of the firm for purposes of financial performance. To test this, an independent samples t-

test was used. The following hypothesis was tested;

H0: There is no difference in the mean profit for the certified and non-certified firms

H1: There is significant difference in the mean profit for the certified and non-certified firms

Results of the test are given below;

Table 4: Group Statistics

Certification

dummy

N Mean Std.

Deviation

Std. Error

Mean

profit Not certified 5257 1865.26 6911.274 95.321

Certified 460 4384.67 9237.036 430.679

Table 5: Independent Samples Test

Levene's Test

for Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differen

ce

Std.

Error

Differen

ce

95%

Confidence

Interval of the

Difference

Lower Upper

profi

t

Equal

variances

assumed

82.96

3

.000 -7.271 5715 .000 -2519.4 346.491 -

3198.7

-

1840.2

Equal

variances

not assumed

-5.712 505 .000 -2519.4 441.101 -

3386.0

-

1652.8

An independent samples t-test was done to compare the mean profit realized by the ISO 9000

certified firms and non-certified firms. Results showed that the certified firms (M = 4384.67, SD

= 9237.04, N = 460) had significant difference in terms of the profit made when compared to the

non-certified firms (M = 1865.26, SD = 6911.27, N = 5257), t (5715) = -7.27, p < .05, two-tailed.

The difference of -2519.4 showed a strong significant difference. Essentially results showed that

ISO 9000 certified firms made huge profits (more than double) as compared to the non-certified

firms.

Table 4: Group Statistics

Certification

dummy

N Mean Std.

Deviation

Std. Error

Mean

profit Not certified 5257 1865.26 6911.274 95.321

Certified 460 4384.67 9237.036 430.679

Table 5: Independent Samples Test

Levene's Test

for Equality of

Variances

t-test for Equality of Means

F Sig. t df Sig. (2-

tailed)

Mean

Differen

ce

Std.

Error

Differen

ce

95%

Confidence

Interval of the

Difference

Lower Upper

profi

t

Equal

variances

assumed

82.96

3

.000 -7.271 5715 .000 -2519.4 346.491 -

3198.7

-

1840.2

Equal

variances

not assumed

-5.712 505 .000 -2519.4 441.101 -

3386.0

-

1652.8

An independent samples t-test was done to compare the mean profit realized by the ISO 9000

certified firms and non-certified firms. Results showed that the certified firms (M = 4384.67, SD

= 9237.04, N = 460) had significant difference in terms of the profit made when compared to the

non-certified firms (M = 1865.26, SD = 6911.27, N = 5257), t (5715) = -7.27, p < .05, two-tailed.

The difference of -2519.4 showed a strong significant difference. Essentially results showed that

ISO 9000 certified firms made huge profits (more than double) as compared to the non-certified

firms.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.