Comprehensive IT Audit Report: NSW City Council Governance & Security

VerifiedAdded on 2023/01/11

|10

|3129

|49

Report

AI Summary

This report presents an IT audit of the NSW City Council, evaluating its IT governance, general controls, and cyber security management. The audit identifies high-risk issues, including deficiencies in IT policies, risk management, user access management, and program change management. Key findings highlight the need for improved IT governance frameworks like COBIT, enhanced user access controls, and robust disaster recovery planning. The report also examines cyber security management, emphasizing the importance of protecting data and systems from unauthorized access and attacks. Recommendations include formalizing IT policies, implementing stronger user access controls, improving change management procedures, and developing comprehensive disaster recovery plans to mitigate risks and ensure the integrity and confidentiality of the Council's data and systems. The report underscores the importance of addressing these issues to safeguard the Council's operations and financial assets.

IT Audit and Controls

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Determine audit focus along with scope of audit report.........................................................3

Illustrate high risk issues within NSW City council..............................................................3

Portray audit findings associated with IT governance in NSW City......................................4

Depict audit findings in context of IT general controls..........................................................5

Portray audit findings linked with cyber security management within NSW City................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Introduction......................................................................................................................................3

Determine audit focus along with scope of audit report.........................................................3

Illustrate high risk issues within NSW City council..............................................................3

Portray audit findings associated with IT governance in NSW City......................................4

Depict audit findings in context of IT general controls..........................................................5

Portray audit findings linked with cyber security management within NSW City................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Introduction

The systematic evaluation of security aspects of firms information system through

measuring of how well they conforms to set of formulated criteria is referred to as IT security

audit (Agyei-Mensah, Agyemang and Ansong, 2020). This presents higher level of description

with respect to ways in which firm can test as well as access their security postures that

comprises of cyber security. To have an understanding related with this aspect NSW City

Council is being taken into regards which are liable for allocating financial reporting process.

This report will provide an insight into scope of audit report, high risk issues and findings

associated with IT governance. Furthermore, it also involves IT general controls along with

aspects associated with cyber security.

Determine audit focus along with scope of audit report

The Councils are responsible for allocation of resources along with time for financial

reporting process and for this they have adequate processes, resources and systems which are

liable for executing new standards for accounting. The scope of this report is to furnish an audit

for strengthening quality, timelines of financial reporting along with recommendations in context

of internal governance and controls (Chopra and Chaudhary, 2020). Here, emphasis is laid on

high risk issues so that firm can have adequate services without having any compromise within

their services. Along with this, IT policies has to be formalised as well as reviewed regularly to

make sure emerging risks have been taken into consideration and adequate policies are reflective

in context of alterations within IT environment. It is necessary to identify risks and manage them

adequately so that third person or intruders do not have access to particular information.

Moreover, focus will be on improvisation of user access management processes for ensuring that

information systems are secured as well as possess significant controls through which

modifications can be made easily within information system as per requirements. In addition to

this, asset registers needs to be updated, reconcile them with asset management system that

comprises have significant controls for ensuring integrity in context of manual spreadsheet.

Illustrate high risk issues within NSW City council

Councils are dependent on IT (information technology) for delivering their services as

well as manage their data and information. While IT is responsible for delivering considerable

benefits, it also possesses present risks which Council have to acknowledge (Chopra and

The systematic evaluation of security aspects of firms information system through

measuring of how well they conforms to set of formulated criteria is referred to as IT security

audit (Agyei-Mensah, Agyemang and Ansong, 2020). This presents higher level of description

with respect to ways in which firm can test as well as access their security postures that

comprises of cyber security. To have an understanding related with this aspect NSW City

Council is being taken into regards which are liable for allocating financial reporting process.

This report will provide an insight into scope of audit report, high risk issues and findings

associated with IT governance. Furthermore, it also involves IT general controls along with

aspects associated with cyber security.

Determine audit focus along with scope of audit report

The Councils are responsible for allocation of resources along with time for financial

reporting process and for this they have adequate processes, resources and systems which are

liable for executing new standards for accounting. The scope of this report is to furnish an audit

for strengthening quality, timelines of financial reporting along with recommendations in context

of internal governance and controls (Chopra and Chaudhary, 2020). Here, emphasis is laid on

high risk issues so that firm can have adequate services without having any compromise within

their services. Along with this, IT policies has to be formalised as well as reviewed regularly to

make sure emerging risks have been taken into consideration and adequate policies are reflective

in context of alterations within IT environment. It is necessary to identify risks and manage them

adequately so that third person or intruders do not have access to particular information.

Moreover, focus will be on improvisation of user access management processes for ensuring that

information systems are secured as well as possess significant controls through which

modifications can be made easily within information system as per requirements. In addition to

this, asset registers needs to be updated, reconcile them with asset management system that

comprises have significant controls for ensuring integrity in context of manual spreadsheet.

Illustrate high risk issues within NSW City council

Councils are dependent on IT (information technology) for delivering their services as

well as manage their data and information. While IT is responsible for delivering considerable

benefits, it also possesses present risks which Council have to acknowledge (Chopra and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Chaudhary, 2020). Within prior years, it has been recognised that that they have to improvise IT

governance as well as controls for managing their key financial systems. As per audit, it has been

recognized that there are 575 issues associated with information technology and out of this 448

were identified. Along with this, 68% are related with user access management. Apart from this,

total numbers of control deficiencies which have been reported within management letters have

been enhanced in comparison to previous year and ample numbers of high risks have been

declined. Furthermore, there are some high risk issues associated with lack of key information

technology procedures and policies, minimised risk management activities related with IT and

user access reviews within key financial systems are not carried out. This also involves shared

user accounts and segregation of duties is not adequately enforced within key financial system.

An instance can be taken into consideration like if systems are not managed adequately then

intruder or any other insider can have access to data then it could have adverse impact on ways in

which Council works. This involves not only loss of financial assets but also sensitive

information which may lead to huge impact on their overall functionalities.

In addition to this, privileged user access is not restricted as well as monitored for

identification of any kind of suspicious activity that is carried out. For an example when IT is

being used within NSW Council then it will lead to increase the probability of risks lie individual

can track activities happening on network and may compromise the integrity of data that is being

held by them. Thus it becomes essential to monitor activities or functions which are being carried

out as well as restrict access to all employees at different levels (Hussein, 2020). It will lead the

Council to ensure security levels within working area up to some extent. Furthermore, this has to

be made sure that strong passwords are being used and this can be done by having some

guidelines or a peculiar pattern that has to be entered within the password field. Along with this,

it will also ensure that password like dictionary words are not used which can be easily broken

up by dictionary or brute force attack or just by hit and trial method. The other major issues are

system execution with missing sign offs, unresolved flaws and documentation. As per the audit,

with respect to IT control deficiencies, they have been grouped into three crucial areas, they are

IT governance, general controls (comprises of disaster recovery planning, program change

management and user access management) and cyber security management (Lai, Liu and Chen,

2020). These sections are illustrated below provides an insight into these aspects with respect to

NSW Council.

governance as well as controls for managing their key financial systems. As per audit, it has been

recognized that there are 575 issues associated with information technology and out of this 448

were identified. Along with this, 68% are related with user access management. Apart from this,

total numbers of control deficiencies which have been reported within management letters have

been enhanced in comparison to previous year and ample numbers of high risks have been

declined. Furthermore, there are some high risk issues associated with lack of key information

technology procedures and policies, minimised risk management activities related with IT and

user access reviews within key financial systems are not carried out. This also involves shared

user accounts and segregation of duties is not adequately enforced within key financial system.

An instance can be taken into consideration like if systems are not managed adequately then

intruder or any other insider can have access to data then it could have adverse impact on ways in

which Council works. This involves not only loss of financial assets but also sensitive

information which may lead to huge impact on their overall functionalities.

In addition to this, privileged user access is not restricted as well as monitored for

identification of any kind of suspicious activity that is carried out. For an example when IT is

being used within NSW Council then it will lead to increase the probability of risks lie individual

can track activities happening on network and may compromise the integrity of data that is being

held by them. Thus it becomes essential to monitor activities or functions which are being carried

out as well as restrict access to all employees at different levels (Hussein, 2020). It will lead the

Council to ensure security levels within working area up to some extent. Furthermore, this has to

be made sure that strong passwords are being used and this can be done by having some

guidelines or a peculiar pattern that has to be entered within the password field. Along with this,

it will also ensure that password like dictionary words are not used which can be easily broken

up by dictionary or brute force attack or just by hit and trial method. The other major issues are

system execution with missing sign offs, unresolved flaws and documentation. As per the audit,

with respect to IT control deficiencies, they have been grouped into three crucial areas, they are

IT governance, general controls (comprises of disaster recovery planning, program change

management and user access management) and cyber security management (Lai, Liu and Chen,

2020). These sections are illustrated below provides an insight into these aspects with respect to

NSW Council.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Portray audit findings associated with IT governance in NSW City

IT governance is liable for furnishing a structure which enables council within effective

management of their IT risks as well as make sure that related activities are aligned for attaining

their objectives. Councils fail to maintain their information technology policies formalised and

even up to date which acts as a critical aspect that brings in risks. This makes it crucial for to

review emerging risks that will render reflection to IT environment. Here, lack of adequate

procedures leads to inappropriate as well as inconsistent practices that leads to enhanced

likelihood for third person access to their key systems (Lee and Levine, 2020). Much

improvisation have been not executed by Councils with respect to this aspect and they need to

review them regularly. They need to identify as well as interact risks related with making use of

IT so they can have significant knowledge about risks and accordingly respond to them within

acceptable timeframe.

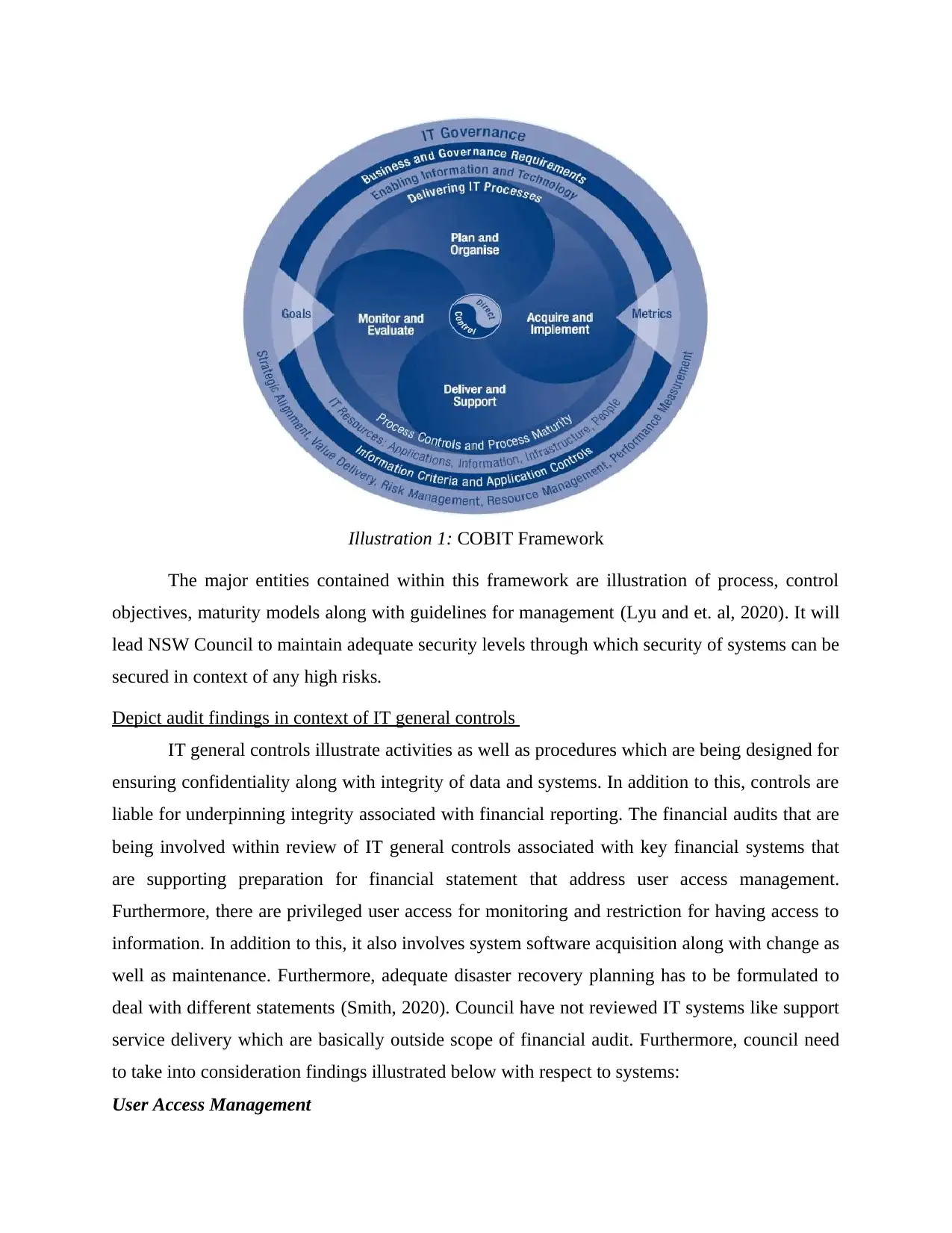

IT governance framework can be utilised by Council to through which they can identify

adequate ways to render their services by making use of information technology. The type

framework that is responsible for defining ways as well as methods by which firm can execute,

manage and track IT governance in working environment is referred to as IT governance

framework. With respect to this, Council can make use of COBIT, it has mentioned beneath:

Controlled objective for Information and related technology (COBIT) framework: This

is being developed for managing along with IT governance. This can be used by Council like a

supportive tool that aids within bridging gap in between risks, control needs and technical

concerns. This is accountable to make sure that control, quality and reliability for information

system those are being used by NSW Council is being attained. This framework possesses

capabilities according to which plans can be developed, organised, delivered, supported and

acquired. In addition to this, overall performance can be monitored as well as evaluated for

attaining desired goals with high efficiency in terms of security (Li, No and Boritz, 2020).

IT governance is liable for furnishing a structure which enables council within effective

management of their IT risks as well as make sure that related activities are aligned for attaining

their objectives. Councils fail to maintain their information technology policies formalised and

even up to date which acts as a critical aspect that brings in risks. This makes it crucial for to

review emerging risks that will render reflection to IT environment. Here, lack of adequate

procedures leads to inappropriate as well as inconsistent practices that leads to enhanced

likelihood for third person access to their key systems (Lee and Levine, 2020). Much

improvisation have been not executed by Councils with respect to this aspect and they need to

review them regularly. They need to identify as well as interact risks related with making use of

IT so they can have significant knowledge about risks and accordingly respond to them within

acceptable timeframe.

IT governance framework can be utilised by Council to through which they can identify

adequate ways to render their services by making use of information technology. The type

framework that is responsible for defining ways as well as methods by which firm can execute,

manage and track IT governance in working environment is referred to as IT governance

framework. With respect to this, Council can make use of COBIT, it has mentioned beneath:

Controlled objective for Information and related technology (COBIT) framework: This

is being developed for managing along with IT governance. This can be used by Council like a

supportive tool that aids within bridging gap in between risks, control needs and technical

concerns. This is accountable to make sure that control, quality and reliability for information

system those are being used by NSW Council is being attained. This framework possesses

capabilities according to which plans can be developed, organised, delivered, supported and

acquired. In addition to this, overall performance can be monitored as well as evaluated for

attaining desired goals with high efficiency in terms of security (Li, No and Boritz, 2020).

Illustration 1: COBIT Framework

The major entities contained within this framework are illustration of process, control

objectives, maturity models along with guidelines for management (Lyu and et. al, 2020). It will

lead NSW Council to maintain adequate security levels through which security of systems can be

secured in context of any high risks.

Depict audit findings in context of IT general controls

IT general controls illustrate activities as well as procedures which are being designed for

ensuring confidentiality along with integrity of data and systems. In addition to this, controls are

liable for underpinning integrity associated with financial reporting. The financial audits that are

being involved within review of IT general controls associated with key financial systems that

are supporting preparation for financial statement that address user access management.

Furthermore, there are privileged user access for monitoring and restriction for having access to

information. In addition to this, it also involves system software acquisition along with change as

well as maintenance. Furthermore, adequate disaster recovery planning has to be formulated to

deal with different statements (Smith, 2020). Council have not reviewed IT systems like support

service delivery which are basically outside scope of financial audit. Furthermore, council need

to take into consideration findings illustrated below with respect to systems:

User Access Management

The major entities contained within this framework are illustration of process, control

objectives, maturity models along with guidelines for management (Lyu and et. al, 2020). It will

lead NSW Council to maintain adequate security levels through which security of systems can be

secured in context of any high risks.

Depict audit findings in context of IT general controls

IT general controls illustrate activities as well as procedures which are being designed for

ensuring confidentiality along with integrity of data and systems. In addition to this, controls are

liable for underpinning integrity associated with financial reporting. The financial audits that are

being involved within review of IT general controls associated with key financial systems that

are supporting preparation for financial statement that address user access management.

Furthermore, there are privileged user access for monitoring and restriction for having access to

information. In addition to this, it also involves system software acquisition along with change as

well as maintenance. Furthermore, adequate disaster recovery planning has to be formulated to

deal with different statements (Smith, 2020). Council have not reviewed IT systems like support

service delivery which are basically outside scope of financial audit. Furthermore, council need

to take into consideration findings illustrated below with respect to systems:

User Access Management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Information technology is crucial for council in context of ways in which services are

being delivered. While IT improvises service delivery along with growing dependencies on

technology that illustrates that council may have certain risks related with misuse and

unauthorised access. The major areas which have to be taken into consideration in context of

access management comprises of adequate approval for new users as well as modification within

permission for access into IT system and timely removal for new given access. Furthermore,

strong password controls are being used for avoiding user access from being getting

compromised (Stoel and Havelka, 2020). In addition to this, there has to be periodic user access

review for identification of inadequate access and constraints for privileged access for adequate

employees along with monitoring their activities related with access. Council have improvised

their access for management processes. But, further enhancements are needed for tracking

privileged account activities for user along with periodic access reviews of actions carried out by

them.

Program Change Management

There has to be relevant controls over information technology systems so that they can be

improvised. Alterations are carried out in context of IT programs that are associated with

infrastructure components which have to be authorised prior for execution. It will lead to make

sure that modifications made are adequate as well as in line with needs of the business. Here,

controls within weak systems have to be altered as this expose Council to risk associated with

inaccurate or unauthorised alterations to programs, issues associated with integrity & data

accuracy (Yi and Long, 2020). This also involves unintended alterations with respect to ways in

which program report as well as process information and errors within financial reporting.

Council yet have not improvised change management controls over their IT systems in

comparison to previous year.

Disaster Recovery Planning

Council needs improvise their planning as well as testing as it will aid them to

minimise disruption to functionalities within event of crucial systems outrage or any other kind

of disaster (Agyei-Mensah, Agyemang and Ansong, 2020). Without any kind of adequate

analysis as well as planning, council might not be able to adequately anticipate disruption,

identification of highest tolerate outages and recover from them successfully within event of

being delivered. While IT improvises service delivery along with growing dependencies on

technology that illustrates that council may have certain risks related with misuse and

unauthorised access. The major areas which have to be taken into consideration in context of

access management comprises of adequate approval for new users as well as modification within

permission for access into IT system and timely removal for new given access. Furthermore,

strong password controls are being used for avoiding user access from being getting

compromised (Stoel and Havelka, 2020). In addition to this, there has to be periodic user access

review for identification of inadequate access and constraints for privileged access for adequate

employees along with monitoring their activities related with access. Council have improvised

their access for management processes. But, further enhancements are needed for tracking

privileged account activities for user along with periodic access reviews of actions carried out by

them.

Program Change Management

There has to be relevant controls over information technology systems so that they can be

improvised. Alterations are carried out in context of IT programs that are associated with

infrastructure components which have to be authorised prior for execution. It will lead to make

sure that modifications made are adequate as well as in line with needs of the business. Here,

controls within weak systems have to be altered as this expose Council to risk associated with

inaccurate or unauthorised alterations to programs, issues associated with integrity & data

accuracy (Yi and Long, 2020). This also involves unintended alterations with respect to ways in

which program report as well as process information and errors within financial reporting.

Council yet have not improvised change management controls over their IT systems in

comparison to previous year.

Disaster Recovery Planning

Council needs improvise their planning as well as testing as it will aid them to

minimise disruption to functionalities within event of crucial systems outrage or any other kind

of disaster (Agyei-Mensah, Agyemang and Ansong, 2020). Without any kind of adequate

analysis as well as planning, council might not be able to adequately anticipate disruption,

identification of highest tolerate outages and recover from them successfully within event of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

disaster. Along with this, some councils does not have relevant as well as current disaster

recovery planning for dealing with distinct situations.

Portray audit findings linked with cyber security management within NSW City

The body of processes, practices and technologies that are designed for protecting

programs, data, devices and network from damage, unauthorised access or attacks is defined as

cyber security. NSW cyber security policy at State level illustrates that strong security is crucial

components of Digital Government strategies. The term is liable for covering all the essential

measures that are being utilised for protecting system along with information stored and

possessed within them from any kind of compromise in terms of integrity, availability and

confidentiality (Chopra and Chaudhary, 2020). Along with this, poor management in context of

cyber security can expose councils with reference to broad range of risks that comprises of

financial loss, data breaches and reputational damage. For an example, if third person get access

to servers or network of NSW City, it won’t be difficult for them to have entire details present

within the network, they may even have access to sensitive data.

Along with this, all the systems present within network can be accessed which means that

there are high risks for data leakage of ample number of people of NSW City that imply that it

can be used to exploit them or damage reputation of people. The probable influence associated

with this comprises of theft of financial along with information as well as intellectual property

information (Chopra and Chaudhary, 2020). Theft of money can be carried out, this can be done

by making use of wannacry attack in which intruders demanded for hefty amount for giving

access to data. This can have a strong influence both in financial and data loss aspects. There can

be multiple requests to servers of NSW City which may lead to denial of service that might even

lead to server or network crash and even this can cost heavy for them. Along with this,

destruction of information, cost associated with refurbishing impacted system, devices as well as

network, legal actions which occurs due to attacks like denial of service leads to system

downtime and may also have some legal fees.

Furthermore, this also involves third part losses in terms of data which is present within

government systems that are being utilised for criminal purposes. If in any case, this information

is exploited then it will have adverse impact on NSW City as decisions with any aspects have to

be changed if integrity and confidentiality of that specific data has been compromised (Hussein,

2020). To deal with such kind of issues higher level assessment have been formulated for

recovery planning for dealing with distinct situations.

Portray audit findings linked with cyber security management within NSW City

The body of processes, practices and technologies that are designed for protecting

programs, data, devices and network from damage, unauthorised access or attacks is defined as

cyber security. NSW cyber security policy at State level illustrates that strong security is crucial

components of Digital Government strategies. The term is liable for covering all the essential

measures that are being utilised for protecting system along with information stored and

possessed within them from any kind of compromise in terms of integrity, availability and

confidentiality (Chopra and Chaudhary, 2020). Along with this, poor management in context of

cyber security can expose councils with reference to broad range of risks that comprises of

financial loss, data breaches and reputational damage. For an example, if third person get access

to servers or network of NSW City, it won’t be difficult for them to have entire details present

within the network, they may even have access to sensitive data.

Along with this, all the systems present within network can be accessed which means that

there are high risks for data leakage of ample number of people of NSW City that imply that it

can be used to exploit them or damage reputation of people. The probable influence associated

with this comprises of theft of financial along with information as well as intellectual property

information (Chopra and Chaudhary, 2020). Theft of money can be carried out, this can be done

by making use of wannacry attack in which intruders demanded for hefty amount for giving

access to data. This can have a strong influence both in financial and data loss aspects. There can

be multiple requests to servers of NSW City which may lead to denial of service that might even

lead to server or network crash and even this can cost heavy for them. Along with this,

destruction of information, cost associated with refurbishing impacted system, devices as well as

network, legal actions which occurs due to attacks like denial of service leads to system

downtime and may also have some legal fees.

Furthermore, this also involves third part losses in terms of data which is present within

government systems that are being utilised for criminal purposes. If in any case, this information

is exploited then it will have adverse impact on NSW City as decisions with any aspects have to

be changed if integrity and confidentiality of that specific data has been compromised (Hussein,

2020). To deal with such kind of issues higher level assessment have been formulated for

determination of whether councils comprises basic governance along with internal controls for

managing cyber security. But this management needs improvisation in context that most of the

councils need to execute basic entities related with governance like cyber security framework

and policies. Here, emphasis has to be laid on upcoming performance audit which have been

planned with respect to cyber security (Lai, Liu and Chen, 2020).

Conclusion

Form the above it can be concluded that, it is necessary for each organisation to carry an

audit with respect to functionalities that are being carried out by them. The reason behind this is

that it will lead them to identify probable attacks or security aspects which may lead to create

adverse impact on overall operations. For this Council needs to monitor their activities by

tracking the network, identifying vulnerabilities as well as unauthenticated activities which are

conducted within. Furthermore, they can also formulate restrictions with respect to what kinds of

data can be accessed at distinct levels of employees in order to maintain privacy. Apart from this,

there are distinct IT governance framework that aids within formulating plans, monitoring,

evaluating performance and many other aspects which need to be tracked.

managing cyber security. But this management needs improvisation in context that most of the

councils need to execute basic entities related with governance like cyber security framework

and policies. Here, emphasis has to be laid on upcoming performance audit which have been

planned with respect to cyber security (Lai, Liu and Chen, 2020).

Conclusion

Form the above it can be concluded that, it is necessary for each organisation to carry an

audit with respect to functionalities that are being carried out by them. The reason behind this is

that it will lead them to identify probable attacks or security aspects which may lead to create

adverse impact on overall operations. For this Council needs to monitor their activities by

tracking the network, identifying vulnerabilities as well as unauthenticated activities which are

conducted within. Furthermore, they can also formulate restrictions with respect to what kinds of

data can be accessed at distinct levels of employees in order to maintain privacy. Apart from this,

there are distinct IT governance framework that aids within formulating plans, monitoring,

evaluating performance and many other aspects which need to be tracked.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Books & References

Agyei-Mensah, B.K., Agyemang, O.S. and Ansong, A., 2020. Audit Committee Effectiveness,

Audit Quality, and Internal Control Information Disclosures: An Empirical Study.

In Corporate Governance Models and Applications in Developing Economies (pp. 1-22).

IGI Global.

Chopra, A. and Chaudhary, M., 2020. External Audit. In Implementing an Information Security

Management System (pp. 247-258). Apress, Berkeley, CA.

Chopra, A. and Chaudhary, M., 2020. Internal Audit. In Implementing an Information Security

Management System (pp. 221-235). Apress, Berkeley, CA.

Hussein, W.N., 2020. Impact of Economic and Knowledge Transfer Advantages of Outsourcing

Internal Audit on the Internal Control Environment/An Investigative study for a group of

employees at Iraqi Industrial Sector. Tikrit Journal of Administration and Economics

Sciences, 16(49 part 1), pp.57-76.

Lai, S.M., Liu, C.L. and Chen, S.S., 2020. Internal Control Quality and Investment

Efficiency. Accounting Horizons.

Lee, K.K. and Levine, C.B., 2020. Audit partner identification and audit quality. Review of

Accounting Studies, pp.1-32.

Li, H., No, W.G. and Boritz, J.E., 2020. Are external auditors concerned about cyber incidents?

Evidence from audit fees. AUDITING: A Journal of Practice, 39(1), pp.151-171.

Lyu, Q. And et. al, 2020. SBAC: A secure blockchain-based access control framework for

information-centric networking. Journal of Network and Computer Applications, 149,

p.102444.

Smith, S.S., 2020. Internal Control Considerations. In Blockchain, Artificial Intelligence and

Financial Services (pp. 143-150). Springer, Cham.

Stoel, M.D. and Havelka, D., 2020. Information Technology Audit Quality: An Investigation of

the Impact of Individual and Organizational Factors. Journal of Information Systems.

Yi, T. and Long, H., 2020, April. Research on the Social Security Fund Risk Control and

Management Measures Based on Cloud Audit and Big Data Era. In Modern Economics

& Management Forum (pp. 26-29).

Books & References

Agyei-Mensah, B.K., Agyemang, O.S. and Ansong, A., 2020. Audit Committee Effectiveness,

Audit Quality, and Internal Control Information Disclosures: An Empirical Study.

In Corporate Governance Models and Applications in Developing Economies (pp. 1-22).

IGI Global.

Chopra, A. and Chaudhary, M., 2020. External Audit. In Implementing an Information Security

Management System (pp. 247-258). Apress, Berkeley, CA.

Chopra, A. and Chaudhary, M., 2020. Internal Audit. In Implementing an Information Security

Management System (pp. 221-235). Apress, Berkeley, CA.

Hussein, W.N., 2020. Impact of Economic and Knowledge Transfer Advantages of Outsourcing

Internal Audit on the Internal Control Environment/An Investigative study for a group of

employees at Iraqi Industrial Sector. Tikrit Journal of Administration and Economics

Sciences, 16(49 part 1), pp.57-76.

Lai, S.M., Liu, C.L. and Chen, S.S., 2020. Internal Control Quality and Investment

Efficiency. Accounting Horizons.

Lee, K.K. and Levine, C.B., 2020. Audit partner identification and audit quality. Review of

Accounting Studies, pp.1-32.

Li, H., No, W.G. and Boritz, J.E., 2020. Are external auditors concerned about cyber incidents?

Evidence from audit fees. AUDITING: A Journal of Practice, 39(1), pp.151-171.

Lyu, Q. And et. al, 2020. SBAC: A secure blockchain-based access control framework for

information-centric networking. Journal of Network and Computer Applications, 149,

p.102444.

Smith, S.S., 2020. Internal Control Considerations. In Blockchain, Artificial Intelligence and

Financial Services (pp. 143-150). Springer, Cham.

Stoel, M.D. and Havelka, D., 2020. Information Technology Audit Quality: An Investigation of

the Impact of Individual and Organizational Factors. Journal of Information Systems.

Yi, T. and Long, H., 2020, April. Research on the Social Security Fund Risk Control and

Management Measures Based on Cloud Audit and Big Data Era. In Modern Economics

& Management Forum (pp. 26-29).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.