Comprehensive Financial Analysis: IT Industry, Investment and Risk

VerifiedAdded on 2023/06/17

|15

|4312

|142

Report

AI Summary

This report provides a financial evaluation of the IT industry, examining its position within the business cycle and the impact of COVID-19 and global financial crises. It discusses the Arbitrage Pricing Theory and Fama-French three-factor model, evaluating their advantages and disadvantages. Porter’s Five Forces are applied to analyze industry trends and forecast future movements. The report computes call and put option prices, assesses portfolio performance using Sharpe ratio, Treynor measure, Jensen’s alpha, and the information ratio, and recommends maintaining a 70% debt and 30% equity investment ratio for optimal returns. It also advises using forward contracts and SWAP options to minimize foreign exposure risk. Desklib offers a variety of solved assignments for students.

CAPSTONE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report has discussed the two theories i.e. Arbitrage Pricing Theory and Fama-French

three factor model along with their advantage and disadvantage. Along with that, the report also

evaluates IT industry and its prevalent trends by implementing Porter’s 5 Forces. This helps in

forecasting the industry movements and practices for next 3 years. On the basis of research

conducted, it was identified that the IT industry can overcome loss in its sales after the Covid and

global financial crises. Further, the call and put option prices have been calculated along with

their limitations. After that, the report computes the four ratios i.e., Sharpe ratio, Treynor

measure, Jensen’s alpha and the information ratio. Lastly, the analysis helped in identifying that

IT industry should maintain debt equity investment ratio at 70% and 30% respectively so that

better returns can be garnered. Also, report recommended that forward contracts and SWAP

options should be preferred to minimise risk in foreign exposure.

The report has discussed the two theories i.e. Arbitrage Pricing Theory and Fama-French

three factor model along with their advantage and disadvantage. Along with that, the report also

evaluates IT industry and its prevalent trends by implementing Porter’s 5 Forces. This helps in

forecasting the industry movements and practices for next 3 years. On the basis of research

conducted, it was identified that the IT industry can overcome loss in its sales after the Covid and

global financial crises. Further, the call and put option prices have been calculated along with

their limitations. After that, the report computes the four ratios i.e., Sharpe ratio, Treynor

measure, Jensen’s alpha and the information ratio. Lastly, the analysis helped in identifying that

IT industry should maintain debt equity investment ratio at 70% and 30% respectively so that

better returns can be garnered. Also, report recommended that forward contracts and SWAP

options should be preferred to minimise risk in foreign exposure.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

QUESTION 1..................................................................................................................................4

QUESTION 2..................................................................................................................................6

Question: 3.......................................................................................................................................8

Computation of call and option prices.........................................................................................8

Question 4......................................................................................................................................11

CONCLUSION..............................................................................................................................12

RECOMMENDATION.................................................................................................................12

REFERENCES................................................................................................................................1

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

QUESTION 1..................................................................................................................................4

QUESTION 2..................................................................................................................................6

Question: 3.......................................................................................................................................8

Computation of call and option prices.........................................................................................8

Question 4......................................................................................................................................11

CONCLUSION..............................................................................................................................12

RECOMMENDATION.................................................................................................................12

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The present report is based on financial evaluation of various components of the

economy such as industry, stock market and derivative market. In this report, major emphasis

will be given on Information technology or IT industry by evaluating the position of the industry

within the business cycle through various economic indicators. The various factors that has affect

the performance of IT industry during the pandemic 19 will be critically analysed in this report to

highlight how the industry get affected due to the onset of COVID – 19 and what would be the

outlook of this industry in the next three years. Before this, it will be explained that why

academics and practitioners generally use or avoid the arbitrage pricing theory and Fama-French

three-factor model in an attempt to predict the asset prices. Further, the report will include the

valuation of call and put option by applying Black-Scholes model along with the explanation of

uses and limitations of call and put options and the results derived from this model. At last, in

this report, the portfolio of WealthPlus will be evaluated through various measures such as

Sharpe ratio, Traynor ratio, Jensen's alpha and information ratio to indicate whether the portfolio

is outperforming or underperforming than the market. The usefulness and reliability of all these

measures will also be included in this report. The report will be ended by recommending the best

asset class, where to allocate resources and what strategy should the investor or fund manager

should adopt by considering the global financial crisis within the Australian economy.

QUESTION 1

Arbitrage Pricing Theory Model

This is a pricing models with the help of which the returns on the assets can be determine using

the linear relationship between the assets expected return and a number of macroeconomics

variable (Lane and Milesi-Ferretti, 2018). The variables must capture the systematic risk. It is

best for analysing the portfolio for the purpose of investing and identifying securities which is

temporarily mispriced. The formula of Arbitrage Pricing Theory is

E(R)i=E(R)z+(E(I)−E(R)z) ×βn

Where E(R)I = Expected return on the assets

E(R)z = Risk-free rate of return

E(I) = Risk premium attached with i

βn = Sensitivity of the assets price to macroeconomic factor n

The present report is based on financial evaluation of various components of the

economy such as industry, stock market and derivative market. In this report, major emphasis

will be given on Information technology or IT industry by evaluating the position of the industry

within the business cycle through various economic indicators. The various factors that has affect

the performance of IT industry during the pandemic 19 will be critically analysed in this report to

highlight how the industry get affected due to the onset of COVID – 19 and what would be the

outlook of this industry in the next three years. Before this, it will be explained that why

academics and practitioners generally use or avoid the arbitrage pricing theory and Fama-French

three-factor model in an attempt to predict the asset prices. Further, the report will include the

valuation of call and put option by applying Black-Scholes model along with the explanation of

uses and limitations of call and put options and the results derived from this model. At last, in

this report, the portfolio of WealthPlus will be evaluated through various measures such as

Sharpe ratio, Traynor ratio, Jensen's alpha and information ratio to indicate whether the portfolio

is outperforming or underperforming than the market. The usefulness and reliability of all these

measures will also be included in this report. The report will be ended by recommending the best

asset class, where to allocate resources and what strategy should the investor or fund manager

should adopt by considering the global financial crisis within the Australian economy.

QUESTION 1

Arbitrage Pricing Theory Model

This is a pricing models with the help of which the returns on the assets can be determine using

the linear relationship between the assets expected return and a number of macroeconomics

variable (Lane and Milesi-Ferretti, 2018). The variables must capture the systematic risk. It is

best for analysing the portfolio for the purpose of investing and identifying securities which is

temporarily mispriced. The formula of Arbitrage Pricing Theory is

E(R)i=E(R)z+(E(I)−E(R)z) ×βn

Where E(R)I = Expected return on the assets

E(R)z = Risk-free rate of return

E(I) = Risk premium attached with i

βn = Sensitivity of the assets price to macroeconomic factor n

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Why academics and practitioner use this theory?

They use this theory because of its various benefits which are as follows:

The restriction related to information required to predict the returns of the assets in APT

theory is fewer as compared to any other pricing model.

It helps the investors to know about the specific stock’s direction with the help of

multiple risk factor examinations. The various sources of risk are included in the dataset

which make this theory best from others (Harijanto Rahmawaty and Entang, 2021).

It does not offer specific factors rather than this theory look out the four factors such as

change in inflation, industrial production, shift in risk premium and interest rates.

The presence of unanticipated change helps the investors to identify the assets that have

strongest potential for growth or failure.

Why academics and practitioner do not use this theory?

They do not use APT theory because of its disadvantage which includes the following:

It generates large amount of data which require lot of time for sorting and sometime

result of unfamiliar data create loss to the investors. This makes the tool useless.

Because of the non-clear perception of the sources and level of risks, the accurate and

reasonable estimates are not identifying (Bodie, Kane & Marcus, 2020).

The APT theory does not provide guarantee of results thus is not used by the investors in

wide range. It is because some risks are not real risk.

Fama-French (FF) Three Factor Model

This is also an assets pricing model which is developed in the year 1992. This is the expansion of

capital assets pricing model (CAPM) which consist of three factors such as size of firms, book-

to-market value and excess return on the market factor (Spears, 2020). Because of this addition,

the model has given the outperforming tendency and the formula of which is

Rit−Rft=αit+β1(RMt−Rft) +β2SMBt+β3HMLt+ϵit.

Where Rit = total return of a stock or portfolio

Rft = risk free rate of return

RMt=total market portfolio returns at time t

They use this theory because of its various benefits which are as follows:

The restriction related to information required to predict the returns of the assets in APT

theory is fewer as compared to any other pricing model.

It helps the investors to know about the specific stock’s direction with the help of

multiple risk factor examinations. The various sources of risk are included in the dataset

which make this theory best from others (Harijanto Rahmawaty and Entang, 2021).

It does not offer specific factors rather than this theory look out the four factors such as

change in inflation, industrial production, shift in risk premium and interest rates.

The presence of unanticipated change helps the investors to identify the assets that have

strongest potential for growth or failure.

Why academics and practitioner do not use this theory?

They do not use APT theory because of its disadvantage which includes the following:

It generates large amount of data which require lot of time for sorting and sometime

result of unfamiliar data create loss to the investors. This makes the tool useless.

Because of the non-clear perception of the sources and level of risks, the accurate and

reasonable estimates are not identifying (Bodie, Kane & Marcus, 2020).

The APT theory does not provide guarantee of results thus is not used by the investors in

wide range. It is because some risks are not real risk.

Fama-French (FF) Three Factor Model

This is also an assets pricing model which is developed in the year 1992. This is the expansion of

capital assets pricing model (CAPM) which consist of three factors such as size of firms, book-

to-market value and excess return on the market factor (Spears, 2020). Because of this addition,

the model has given the outperforming tendency and the formula of which is

Rit−Rft=αit+β1(RMt−Rft) +β2SMBt+β3HMLt+ϵit.

Where Rit = total return of a stock or portfolio

Rft = risk free rate of return

RMt=total market portfolio returns at time t

Rit−Rft=expected excess return

RMt−Rft=excess return on the market portfolio (index)

SMBt=size premium (small minus big)

HMLt=value premium (high minus low)

β1,2,3=factor coefficients

Why academics and practitioner use this theory?

They use this theory because of following reasons:

It helps in calculating the rate of return of an investment based on the three elements such

as market risk, size of companies and book-to-market value. This result into accurate

returns which helps investors in their investment.

As per this model, the small companies overperform large companies and value

companies beat growth companies.

This model is also uses by the investors in present time because it can explain returns of

more than 90% of diversified portfolios.

It is also based on the assumptions that risker investment provides higher returns to

investors thus they invest in this way only (Schill, 2021).

The diversified portfolio eliminates the unsystematic risk which is also helpful for

managing the business and financial risk variability.

Why academics do not use this theory?

The Rf is state the yield which change continuously on daily basis creating volatility of

the portfolio or securities.

This model is based on the assumption that investors can borrow and lend securities at a

risk-free rate which is not possible in real world.

It is one of the most difficult pricing models to apply because there are no theoretical

models present in the pricing theory (Mann, 2019).

There is no clarity about whether the HML and SMB captures risk or not and the wrong

results are determined if investors just persist the mistakes rather than identifying risk.

QUESTION 2

Porter’s five forces factors imapct over performance of IT industry in the next three years

RMt−Rft=excess return on the market portfolio (index)

SMBt=size premium (small minus big)

HMLt=value premium (high minus low)

β1,2,3=factor coefficients

Why academics and practitioner use this theory?

They use this theory because of following reasons:

It helps in calculating the rate of return of an investment based on the three elements such

as market risk, size of companies and book-to-market value. This result into accurate

returns which helps investors in their investment.

As per this model, the small companies overperform large companies and value

companies beat growth companies.

This model is also uses by the investors in present time because it can explain returns of

more than 90% of diversified portfolios.

It is also based on the assumptions that risker investment provides higher returns to

investors thus they invest in this way only (Schill, 2021).

The diversified portfolio eliminates the unsystematic risk which is also helpful for

managing the business and financial risk variability.

Why academics do not use this theory?

The Rf is state the yield which change continuously on daily basis creating volatility of

the portfolio or securities.

This model is based on the assumption that investors can borrow and lend securities at a

risk-free rate which is not possible in real world.

It is one of the most difficult pricing models to apply because there are no theoretical

models present in the pricing theory (Mann, 2019).

There is no clarity about whether the HML and SMB captures risk or not and the wrong

results are determined if investors just persist the mistakes rather than identifying risk.

QUESTION 2

Porter’s five forces factors imapct over performance of IT industry in the next three years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The five factors and their future performance of the IT industry are as follows:

Bargaining Power of Buyers: Majority of people can access and use computers and

technology all around the world which state large number of buyers of IT firms. This

state that the bargaining power of customers are high. In the next three year, many

companies in order to provide training to employees can use IT products which will

increases the industry demand. It is likely that in the next three year the GDP of IT

industry will grow at a rate of 4.2% p.a. (Dunning, 2021).

Bargaining Power of Suppliers: The bargaining power of supplier of IT industry are not

that much instance because of the various IT company such as Intel, AMD etc. But it is

also look out that in the upcoming years the suppliers will not end their relationship with

firms just to became competitors. It is also forecast that the inflation rate in Australia will

increase at the rate of 3.80% p.a. till next three years.

Threat of New Entrants: The IT industry already has major established brands with the

impact of which entering of new firm is difficult. It required lots of investment to deals

with the strong IT firms (Lane, and Milesi-Ferretti, 2021). It is look out that in the future

the entering of fresh firms is not too much because this industry is less attractive as

compare to others.

Threat of Substitute: There is basically no true substitute of IT industry which indicate

that there is no product which can replace computer not even scientific calculators. This

means that in the next three year, no products can beat the products offer by IT firms

which will definitely increase the sales of firm by 10% p.a (Mann, 2019).

Rivalry among existing players: This industry is known for its rapid growth and

effectiveness. The new entrants will not succeed in entering the IT market in next three

year because there is an instance rivalry among existing players.

Critical Analysis of Impact of COVID-19 and Global financial crises over IT Industry

performance and how they recover it in next three years

There is a huge impact of COVID-19 on IT Industry which involve both positive and

some negative. Basically, collaboration is the backbone of IT industry and with the help of

various tools and techniques the IT firms able to provide work form home solutions to their

business clients during pandemic. The virtual collaboration platform provided by the IT firms

Bargaining Power of Buyers: Majority of people can access and use computers and

technology all around the world which state large number of buyers of IT firms. This

state that the bargaining power of customers are high. In the next three year, many

companies in order to provide training to employees can use IT products which will

increases the industry demand. It is likely that in the next three year the GDP of IT

industry will grow at a rate of 4.2% p.a. (Dunning, 2021).

Bargaining Power of Suppliers: The bargaining power of supplier of IT industry are not

that much instance because of the various IT company such as Intel, AMD etc. But it is

also look out that in the upcoming years the suppliers will not end their relationship with

firms just to became competitors. It is also forecast that the inflation rate in Australia will

increase at the rate of 3.80% p.a. till next three years.

Threat of New Entrants: The IT industry already has major established brands with the

impact of which entering of new firm is difficult. It required lots of investment to deals

with the strong IT firms (Lane, and Milesi-Ferretti, 2021). It is look out that in the future

the entering of fresh firms is not too much because this industry is less attractive as

compare to others.

Threat of Substitute: There is basically no true substitute of IT industry which indicate

that there is no product which can replace computer not even scientific calculators. This

means that in the next three year, no products can beat the products offer by IT firms

which will definitely increase the sales of firm by 10% p.a (Mann, 2019).

Rivalry among existing players: This industry is known for its rapid growth and

effectiveness. The new entrants will not succeed in entering the IT market in next three

year because there is an instance rivalry among existing players.

Critical Analysis of Impact of COVID-19 and Global financial crises over IT Industry

performance and how they recover it in next three years

There is a huge impact of COVID-19 on IT Industry which involve both positive and

some negative. Basically, collaboration is the backbone of IT industry and with the help of

various tools and techniques the IT firms able to provide work form home solutions to their

business clients during pandemic. The virtual collaboration platform provided by the IT firms

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps the companies to conduct meetings with their employees and business partners. This helps

the customers all around the world to buy goods as services via using online channels and

internet (Bodie, Kane & Marcus, 2020). It is also put positive impact over business operations

where all the work during the Covid – 19 runs smoothly with the help of remote working and

laying off workers. Because of the IT solutions, various office which was taken on rent are

vacant which help them in cutting their extra cost.

However, beside positive impact there is also a negative impact of Covid on IT industry

is that they also face a downfall in their business. It may be because of the no innovative

products and low network. Beside this, the industry also faces decline in the investment and

capital because of the increase in the interest rate after the Global Financial Crises (Bodie, Kane

& Marcus, 2020). It became difficult for the IT industry to manage the returns from the equities

because they contain high risk (Spears, 2020). Basically, such a downfall in IT industry is

temporary which get easily recover by adopting and providing the four platforms such as:

cloud,

mobile,

social and

big data analytics to their clients.

Every firm in the industry has to provide this platform to the clients in order to grow. Beside this,

they can also recover it by adopting new technologies such as:

Artificial Intelligence.

Robotics

AR/VR

Blockchain etc.

Forecast/Outlook of IT industry in the next three years are as follows:

It is look out that even after the covid-19, the IT service market of Australia is expected to

register a CAGR of about 10.36% p.a. during the forecast period of 2021 to 2026 (Mann, 2019).

Question: 3

Computation of call and option prices

Information given in the question are as follows:

Stock price, S0 = $50

the customers all around the world to buy goods as services via using online channels and

internet (Bodie, Kane & Marcus, 2020). It is also put positive impact over business operations

where all the work during the Covid – 19 runs smoothly with the help of remote working and

laying off workers. Because of the IT solutions, various office which was taken on rent are

vacant which help them in cutting their extra cost.

However, beside positive impact there is also a negative impact of Covid on IT industry

is that they also face a downfall in their business. It may be because of the no innovative

products and low network. Beside this, the industry also faces decline in the investment and

capital because of the increase in the interest rate after the Global Financial Crises (Bodie, Kane

& Marcus, 2020). It became difficult for the IT industry to manage the returns from the equities

because they contain high risk (Spears, 2020). Basically, such a downfall in IT industry is

temporary which get easily recover by adopting and providing the four platforms such as:

cloud,

mobile,

social and

big data analytics to their clients.

Every firm in the industry has to provide this platform to the clients in order to grow. Beside this,

they can also recover it by adopting new technologies such as:

Artificial Intelligence.

Robotics

AR/VR

Blockchain etc.

Forecast/Outlook of IT industry in the next three years are as follows:

It is look out that even after the covid-19, the IT service market of Australia is expected to

register a CAGR of about 10.36% p.a. during the forecast period of 2021 to 2026 (Mann, 2019).

Question: 3

Computation of call and option prices

Information given in the question are as follows:

Stock price, S0 = $50

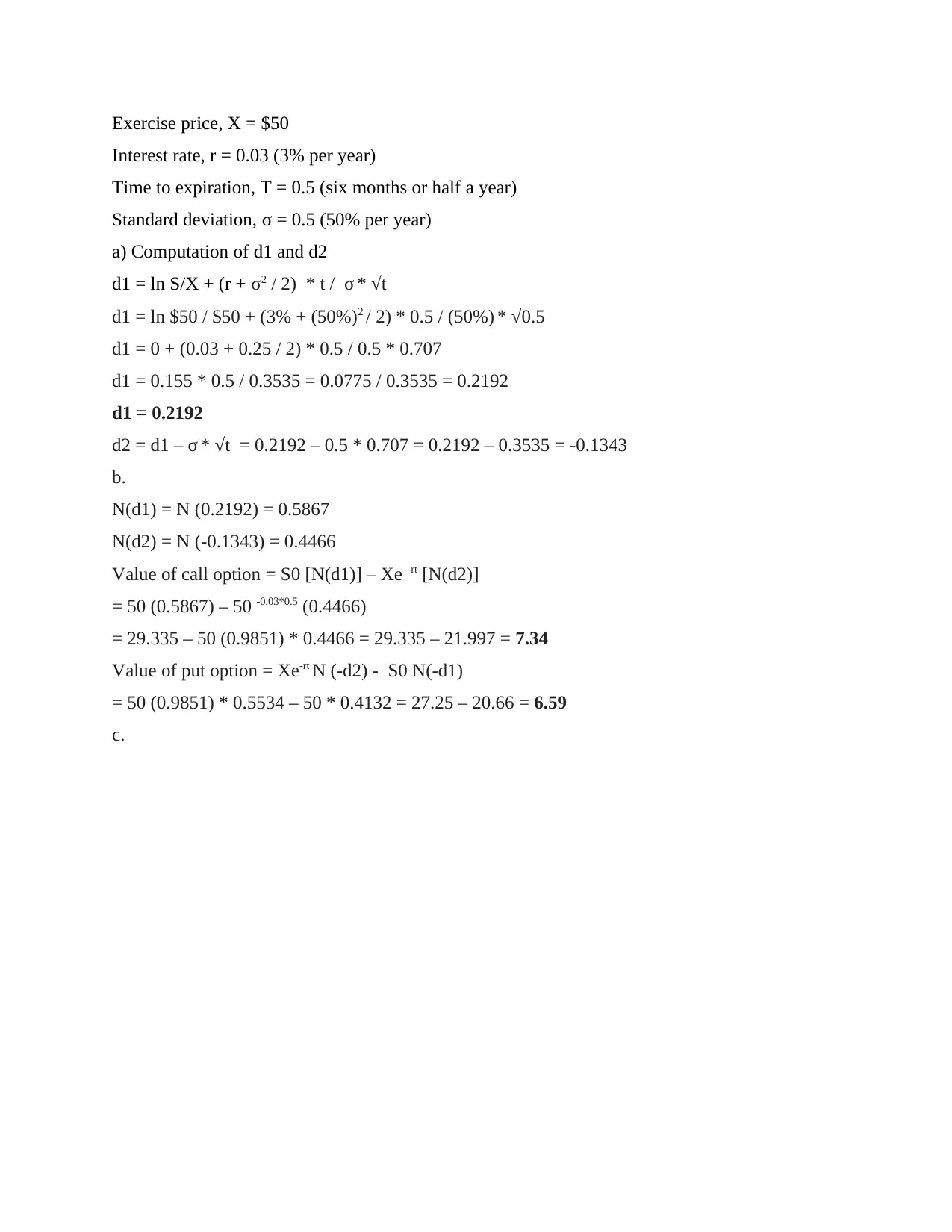

Exercise price, X = $50

Interest rate, r = 0.03 (3% per year)

Time to expiration, T = 0.5 (six months or half a year)

Standard deviation, σ = 0.5 (50% per year)

a) Computation of d1 and d2

d1 = ln S/X + (r + σ2 / 2) * t / σ * √t

d1 = ln $50 / $50 + (3% + (50%)2 / 2) * 0.5 / (50%) * √0.5

d1 = 0 + (0.03 + 0.25 / 2) * 0.5 / 0.5 * 0.707

d1 = 0.155 * 0.5 / 0.3535 = 0.0775 / 0.3535 = 0.2192

d1 = 0.2192

d2 = d1 – σ * √t = 0.2192 – 0.5 * 0.707 = 0.2192 – 0.3535 = -0.1343

b.

N(d1) = N (0.2192) = 0.5867

N(d2) = N (-0.1343) = 0.4466

Value of call option = S0 [N(d1)] – Xe -rt [N(d2)]

= 50 (0.5867) – 50 -0.03*0.5 (0.4466)

= 29.335 – 50 (0.9851) * 0.4466 = 29.335 – 21.997 = 7.34

Value of put option = Xe-rt N (-d2) - S0 N(-d1)

= 50 (0.9851) * 0.5534 – 50 * 0.4132 = 27.25 – 20.66 = 6.59

c.

Interest rate, r = 0.03 (3% per year)

Time to expiration, T = 0.5 (six months or half a year)

Standard deviation, σ = 0.5 (50% per year)

a) Computation of d1 and d2

d1 = ln S/X + (r + σ2 / 2) * t / σ * √t

d1 = ln $50 / $50 + (3% + (50%)2 / 2) * 0.5 / (50%) * √0.5

d1 = 0 + (0.03 + 0.25 / 2) * 0.5 / 0.5 * 0.707

d1 = 0.155 * 0.5 / 0.3535 = 0.0775 / 0.3535 = 0.2192

d1 = 0.2192

d2 = d1 – σ * √t = 0.2192 – 0.5 * 0.707 = 0.2192 – 0.3535 = -0.1343

b.

N(d1) = N (0.2192) = 0.5867

N(d2) = N (-0.1343) = 0.4466

Value of call option = S0 [N(d1)] – Xe -rt [N(d2)]

= 50 (0.5867) – 50 -0.03*0.5 (0.4466)

= 29.335 – 50 (0.9851) * 0.4466 = 29.335 – 21.997 = 7.34

Value of put option = Xe-rt N (-d2) - S0 N(-d1)

= 50 (0.9851) * 0.5534 – 50 * 0.4132 = 27.25 – 20.66 = 6.59

c.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Uses of call and put options

The call option is used to gives its buyer the right but not an obligation to purchase the

underlying securities or an asset after the expiration of a specified time period at a

specified price (Gulen, Popescu and Sari, 2019).

The put option is used to provide its holder the right but not an obligation to sell the

underlying security or asset after the expiration of a specified time period at a specified

price.

Both options are used for the purpose of speculation and hedging.

Call option is used when the price of the stock is expected to rise in the market and the option

holder is planning to buy the stock at some future date.

Put option is being used when the price of the stock in the market is expected to go down and

the option holder is planning to sell the stock at some future date (Dar and Anuradha,

2018).

Both of these options are used to hedge the position against price volatility.

Limitations of call and put options

The premium paid on call option get 100% lost if the option is out of the money.

The options do not traded one on one with the underlying asset where if the price of

underlying gets changed by $1, the option price changed just by 0.7 cents.

If the price of the underlying asset moves in the opposite direction of what has been

expected by the trader, there must be a substantial losses for the option holder. When the liquidity of the options have poor liquidity, then the trader may face difficulty

in entering and exiting from and in the option market (Edeki, Ugbebor and Owoloko,

2017).

Uses and limitations of results obtained through Blackscholes Model

The results obtained through this model is useful as it has identified the value of call and

options by giving considerations risk and time factors.

The results are useful in determining whether the actual price is representing a better

value or not by comparing it with objective theoretical price (Dar and Anuradha, 2018).

The value of the call option increases with the increase in the stock price and value of the

put option increases with the decrease in stock prices in the market.

The call option is used to gives its buyer the right but not an obligation to purchase the

underlying securities or an asset after the expiration of a specified time period at a

specified price (Gulen, Popescu and Sari, 2019).

The put option is used to provide its holder the right but not an obligation to sell the

underlying security or asset after the expiration of a specified time period at a specified

price.

Both options are used for the purpose of speculation and hedging.

Call option is used when the price of the stock is expected to rise in the market and the option

holder is planning to buy the stock at some future date.

Put option is being used when the price of the stock in the market is expected to go down and

the option holder is planning to sell the stock at some future date (Dar and Anuradha,

2018).

Both of these options are used to hedge the position against price volatility.

Limitations of call and put options

The premium paid on call option get 100% lost if the option is out of the money.

The options do not traded one on one with the underlying asset where if the price of

underlying gets changed by $1, the option price changed just by 0.7 cents.

If the price of the underlying asset moves in the opposite direction of what has been

expected by the trader, there must be a substantial losses for the option holder. When the liquidity of the options have poor liquidity, then the trader may face difficulty

in entering and exiting from and in the option market (Edeki, Ugbebor and Owoloko,

2017).

Uses and limitations of results obtained through Blackscholes Model

The results obtained through this model is useful as it has identified the value of call and

options by giving considerations risk and time factors.

The results are useful in determining whether the actual price is representing a better

value or not by comparing it with objective theoretical price (Dar and Anuradha, 2018).

The value of the call option increases with the increase in the stock price and value of the

put option increases with the decrease in stock prices in the market.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The value of call and put option determined above are much closer to each other due to the

equality between the stock price and strike price.

Question 4

Calculation of Sharpe ratio

Sharpe ratio = Expected return on portfolio Rp – risk free rate Rf / Standard deviation of portfolio

returns σp

= 15% - 1.75% / 11% = 0.15 – 0.0175 / 0.11 = 0.1325 / 0.11 = 1.20

Calculation of Traynor ratio

Traynor ratio = Expected portfolio return – risk free rate / portfolio beta

= 15% - 1.75% / 0.55 = 0.15 – 0.0175 / 0.55 = 0.1325 / 0.55 = 0.24

Calculation of Jensen's Alpha

Jensen's Alpha = Expected return on portfolio Rp - [Risk free rate Rf + Beta of the Portfolio Bp *

(Expected Market return Rm – Risk free rate Rf)]

= 15% - [1.75% + 0.55 (13% - 1.75%)]

= 0.15 – [0.0175 + 0.55 (0.13 – 0.0175)]

= 0.15 – 0.079 = 0.071

Calculation of information ratio

Information ratio = Expected portfolio return Rp – Expected Market return Rm / Tracking error

= 15% - 13% / 1.5% = 0.15 – 0.13 / 0.015 = 0.02 / 0.015 = 1.33

Usefulness and reliability of Sharpe ratio

It is used to evaluate how well a portfolio is performing against the risk free investments in the

market. Here the determined Sharpe ratio is 1.2 which indicates that it is good for the investors to

invest in the WealthPlus portfolio (do Castelo Gouveia and et.al., 2018).

Usefulness and reliability of Traynor ratio

Traynor ratio is useful in analysing how much excess return could be achieved for taking risk

attached to the security over and above the risk free investment. It indicates how much better

returns can be generated due to taking additional risks (Pangestuti, Wahyudi and Robiyanto,

2017).

A Traynor ratio of 0.24 indicates positive or excess return for taking risk attached to the security

against the risk free investment. In the given case, WealthPlus portfolio will give excess returns

to its investors for taking additional risks.

equality between the stock price and strike price.

Question 4

Calculation of Sharpe ratio

Sharpe ratio = Expected return on portfolio Rp – risk free rate Rf / Standard deviation of portfolio

returns σp

= 15% - 1.75% / 11% = 0.15 – 0.0175 / 0.11 = 0.1325 / 0.11 = 1.20

Calculation of Traynor ratio

Traynor ratio = Expected portfolio return – risk free rate / portfolio beta

= 15% - 1.75% / 0.55 = 0.15 – 0.0175 / 0.55 = 0.1325 / 0.55 = 0.24

Calculation of Jensen's Alpha

Jensen's Alpha = Expected return on portfolio Rp - [Risk free rate Rf + Beta of the Portfolio Bp *

(Expected Market return Rm – Risk free rate Rf)]

= 15% - [1.75% + 0.55 (13% - 1.75%)]

= 0.15 – [0.0175 + 0.55 (0.13 – 0.0175)]

= 0.15 – 0.079 = 0.071

Calculation of information ratio

Information ratio = Expected portfolio return Rp – Expected Market return Rm / Tracking error

= 15% - 13% / 1.5% = 0.15 – 0.13 / 0.015 = 0.02 / 0.015 = 1.33

Usefulness and reliability of Sharpe ratio

It is used to evaluate how well a portfolio is performing against the risk free investments in the

market. Here the determined Sharpe ratio is 1.2 which indicates that it is good for the investors to

invest in the WealthPlus portfolio (do Castelo Gouveia and et.al., 2018).

Usefulness and reliability of Traynor ratio

Traynor ratio is useful in analysing how much excess return could be achieved for taking risk

attached to the security over and above the risk free investment. It indicates how much better

returns can be generated due to taking additional risks (Pangestuti, Wahyudi and Robiyanto,

2017).

A Traynor ratio of 0.24 indicates positive or excess return for taking risk attached to the security

against the risk free investment. In the given case, WealthPlus portfolio will give excess returns

to its investors for taking additional risks.

Usefulness and reliability of Jensen's alpha

Jensen's alpha allows for determining whether the portfolio is returning appropriate return for the

level of risk involved in the securities of the portfolio (Hsieh and et.al., 2020). The excess return

that the portfolio would generate is being represented through the positive value of derived

Jensen's alpha.

Here in the given case, the value of Jensen's alpha for the WealthPlus portfolio is positive that is,

0.071 which indicates that the portfolio has outperformed the market due to the stock picking

skills of the portfolio manager. Jensen's alpha indicates the fund manager's performance.

Usefulness and reliability of information ratio

Information ratio identified how many times and by how much a portfolio has traded better than

or in excess of its benchmark (Chrétien and Kammoun, 2017). The higher the information ratio,

the much better it is. A less than 0 ratios indicated underperformance or poor performance of the

portfolio in the market.

In the given case, the derived value of information ratio for WealthPlus portfolio is comes out as

1.33 which indicates better performance of the portfolio in the market in the past.

CONCLUSION

The report has concluded the reason why academics use and not use the Arbitrage Pricing

model and Fama-French three factor models. Further, the report has concluded the Porter’s five

forces effect on IT industry of Australia along with the impact of Covid and Global financial

crises over the IT industry performance. This has also included the ways to recover from this in

the next five years. The report has also concluded the calculation of call and put option along

with the four measure such as Sharpe ratio etc. Lastly, the report has also provided the

recommendations on the class and strategy of investment to IT industry.

RECOMMENDATION

The following recommendation is available to the IT industry which are as follows:

Because of the global financial crises, the IT industry faces difficulty in getting returns

from its investment in equities. Thus, it is recommendable to the firms of IT industry that

they have to invest more on the debt funds rather than equity funds. It is because debts

provide fixed returns despite of crises or covid. The debt funds contain low risk as

Jensen's alpha allows for determining whether the portfolio is returning appropriate return for the

level of risk involved in the securities of the portfolio (Hsieh and et.al., 2020). The excess return

that the portfolio would generate is being represented through the positive value of derived

Jensen's alpha.

Here in the given case, the value of Jensen's alpha for the WealthPlus portfolio is positive that is,

0.071 which indicates that the portfolio has outperformed the market due to the stock picking

skills of the portfolio manager. Jensen's alpha indicates the fund manager's performance.

Usefulness and reliability of information ratio

Information ratio identified how many times and by how much a portfolio has traded better than

or in excess of its benchmark (Chrétien and Kammoun, 2017). The higher the information ratio,

the much better it is. A less than 0 ratios indicated underperformance or poor performance of the

portfolio in the market.

In the given case, the derived value of information ratio for WealthPlus portfolio is comes out as

1.33 which indicates better performance of the portfolio in the market in the past.

CONCLUSION

The report has concluded the reason why academics use and not use the Arbitrage Pricing

model and Fama-French three factor models. Further, the report has concluded the Porter’s five

forces effect on IT industry of Australia along with the impact of Covid and Global financial

crises over the IT industry performance. This has also included the ways to recover from this in

the next five years. The report has also concluded the calculation of call and put option along

with the four measure such as Sharpe ratio etc. Lastly, the report has also provided the

recommendations on the class and strategy of investment to IT industry.

RECOMMENDATION

The following recommendation is available to the IT industry which are as follows:

Because of the global financial crises, the IT industry faces difficulty in getting returns

from its investment in equities. Thus, it is recommendable to the firms of IT industry that

they have to invest more on the debt funds rather than equity funds. It is because debts

provide fixed returns despite of crises or covid. The debt funds contain low risk as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.