Detailed Financial Performance Report: IVY HOLDCO LIMITED Analysis

VerifiedAdded on 2023/01/03

|9

|2001

|81

Report

AI Summary

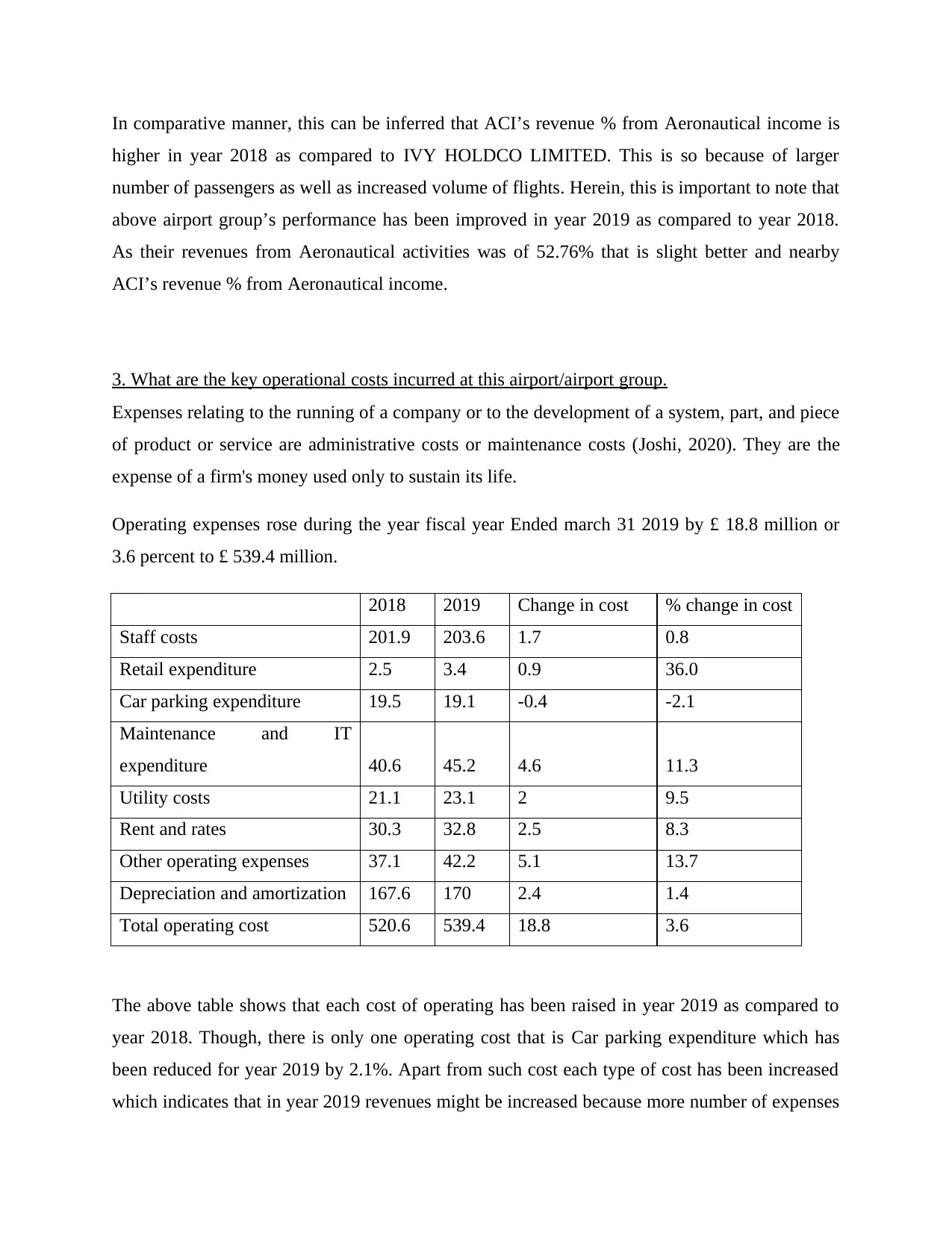

This report presents a detailed financial performance analysis of IVY HOLDCO LIMITED, an airport group. It examines passenger numbers, flight movements, key revenue sources (aeronautical, retail, car parking, etc.), and operational costs (staff, retail, maintenance, etc.). The analysis compares financial data from 2018 and 2019, highlighting growth in passenger numbers and revenues. The report identifies key factors influencing the airport group's long-term success, such as aeronautical and retail income, and staff and retail expenses. The conclusion summarizes the financial health of IVY HOLDCO LIMITED, emphasizing the importance of revenue and expense management for sustained success. The report uses data from financial statements to support its findings, providing a comprehensive overview of the airport group's financial performance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.