Taxation Law Report: Assessing Tax Liabilities for Jack Jones's Income

VerifiedAdded on 2020/06/03

|8

|1981

|45

Report

AI Summary

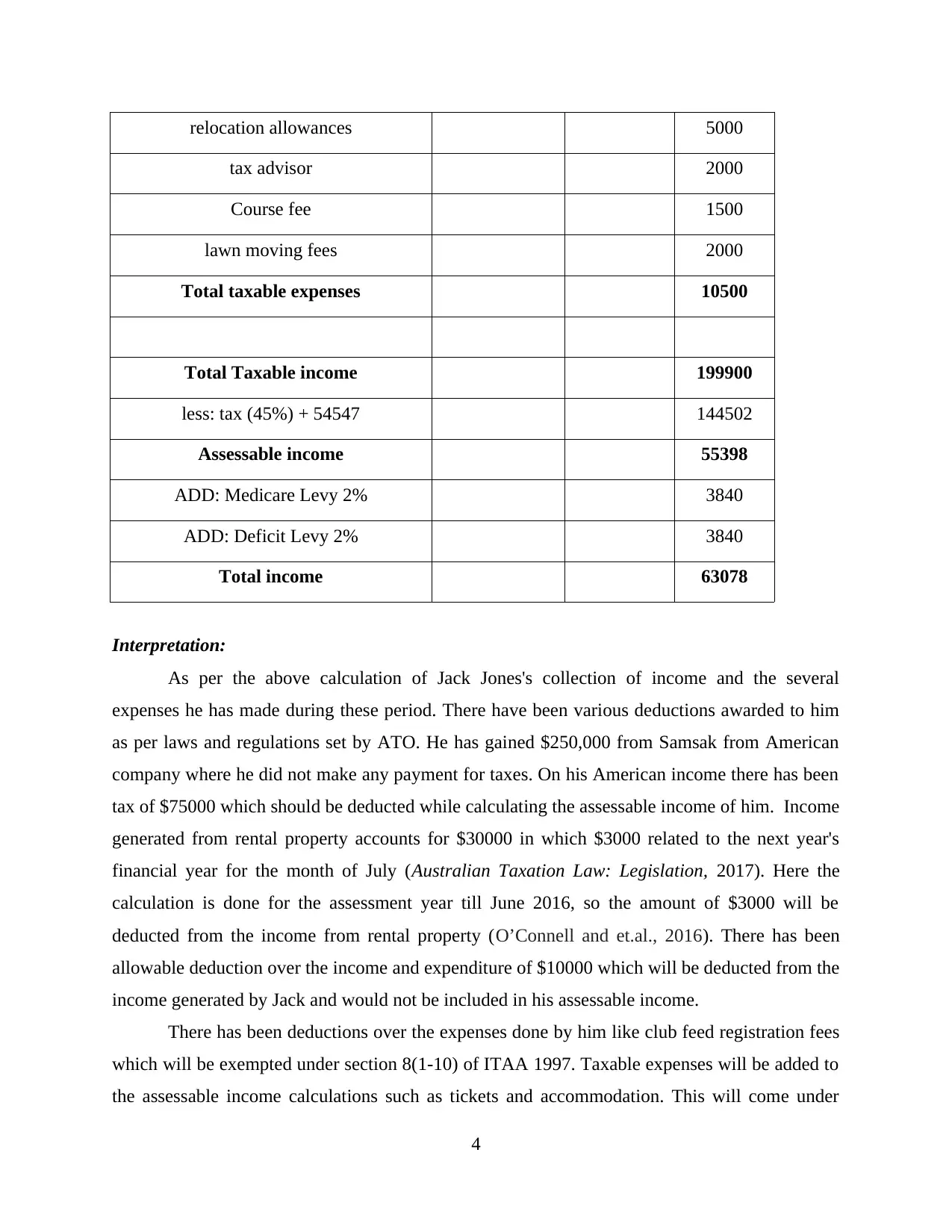

This report examines the tax implications for Jack Jones, a Canadian resident working in Australia. It addresses the determination of his residency status based on the 183-day test and visa duration, referencing relevant legislation and case law. The report then calculates his taxable income, considering income from both Australian and American sources, along with allowable deductions such as club fees, registration fees, and relocation allowances. The analysis includes an income statement outlining the calculation of assessable income, tax liabilities, and the application of Medicare and deficit levies, concluding with a final taxable income figure. The report references various sections of the Income Tax Assessment Acts and other relevant tax rulings and legislation to support its findings, offering a comprehensive overview of Jack Jones's tax obligations.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.