Management Accounting Project: Comparing Jackson Ltd Costing Methods

VerifiedAdded on 2019/10/31

|7

|1440

|265

Project

AI Summary

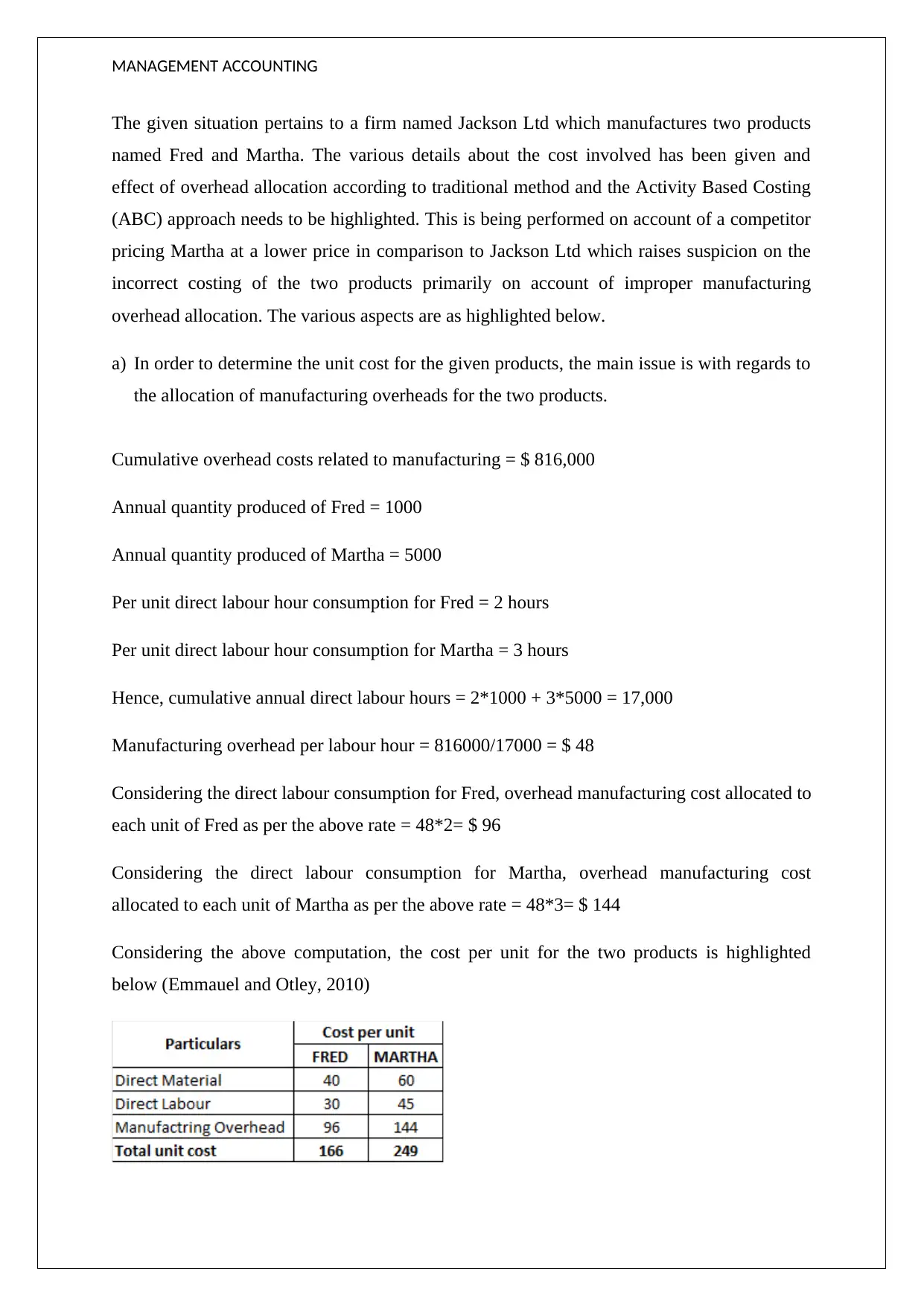

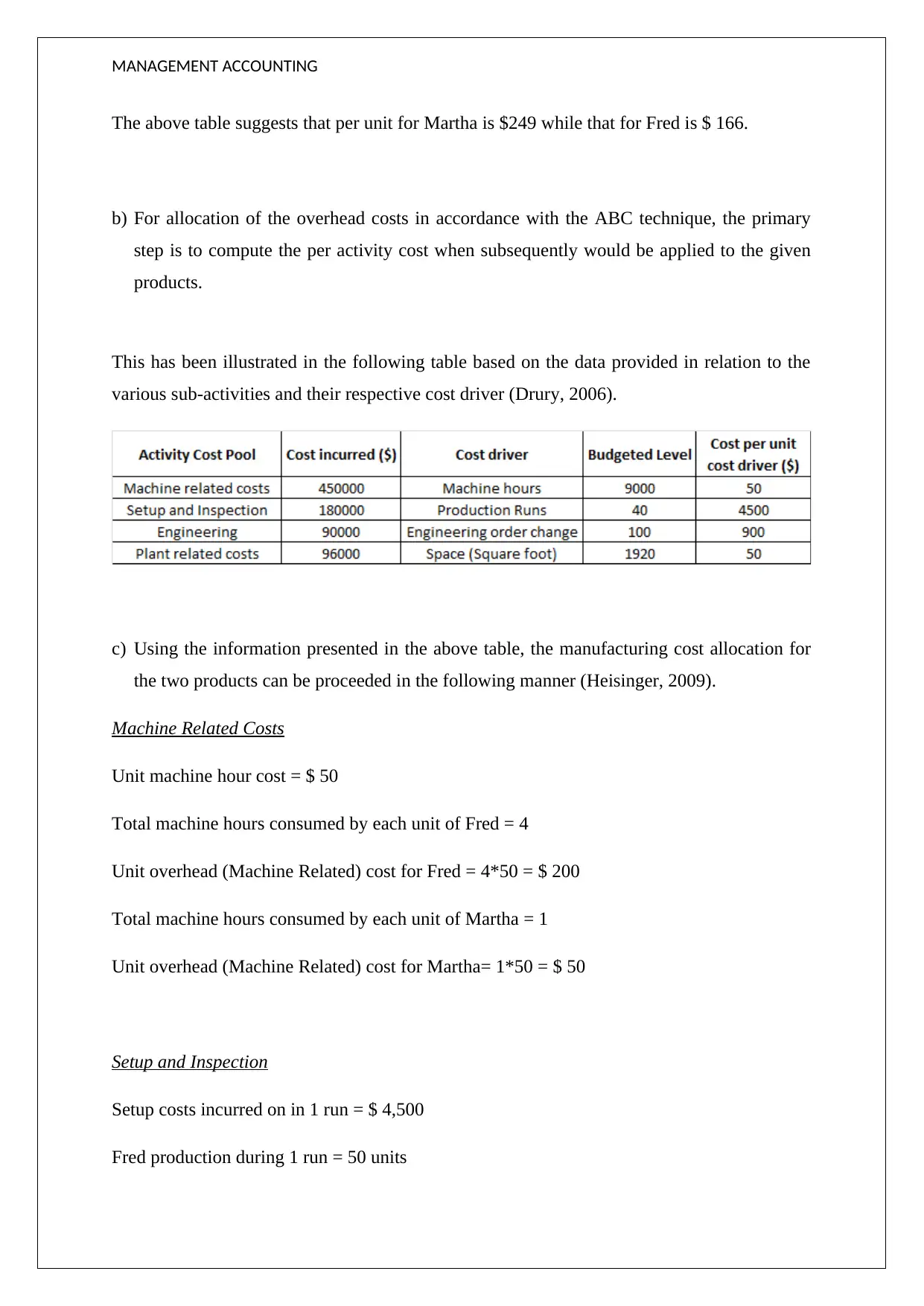

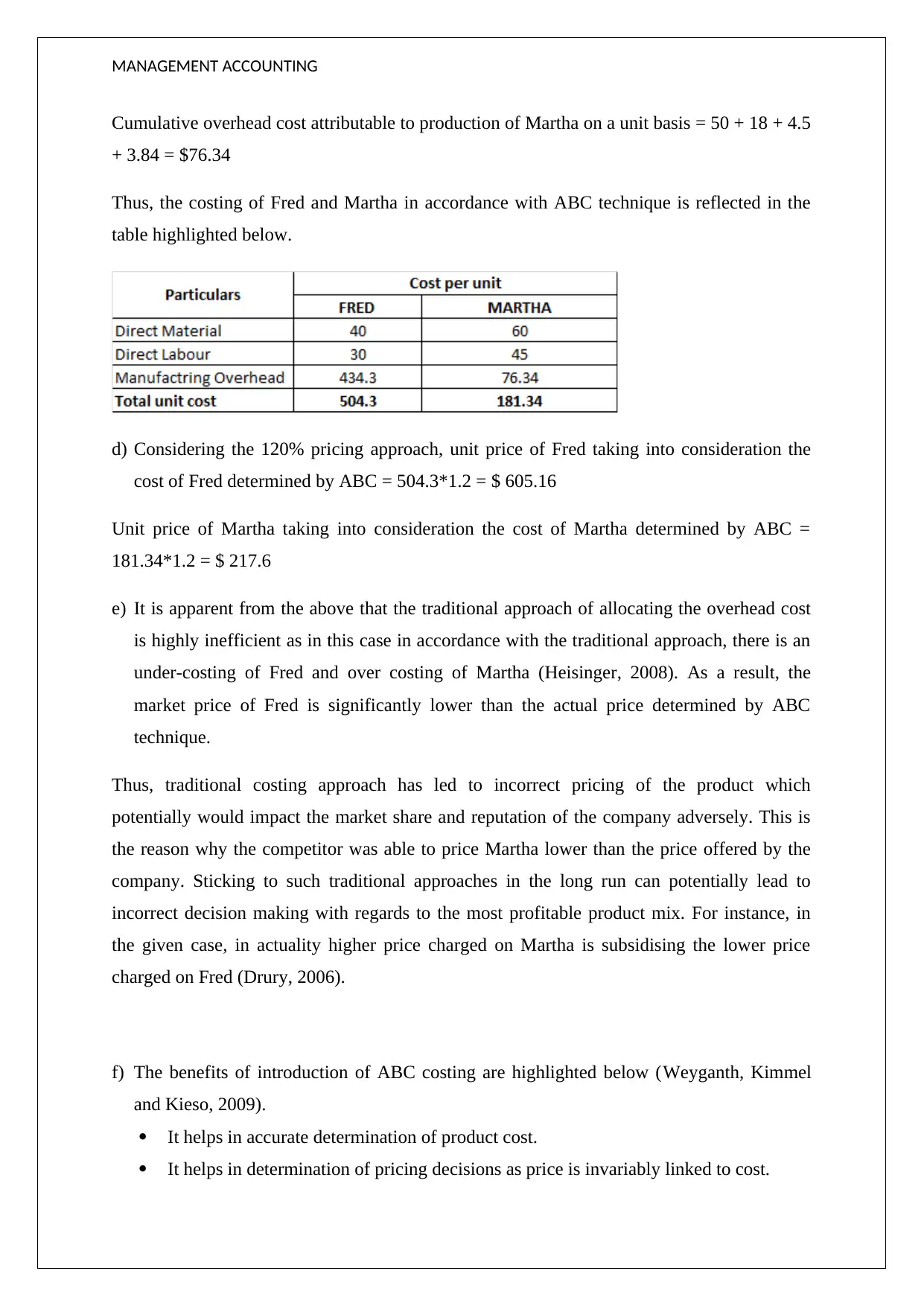

This project focuses on a management accounting analysis of Jackson Ltd, a firm producing two products, Fred and Martha. The assignment compares the traditional costing method with Activity-Based Costing (ABC) to determine unit costs and overhead allocation. The analysis highlights the inefficiencies of the traditional method, which leads to under-costing of one product and over-costing of the other, potentially impacting pricing decisions and market competitiveness. The project calculates overhead costs using both methods, demonstrating how ABC provides a more accurate product cost determination, which influences pricing, product mix decisions, and cost management. The project also discusses the advantages of ABC, such as improved decision-making and competitive advantage, while acknowledging its disadvantages, including implementation costs and potential resistance. References are provided to support the analysis.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.