Corporate Finance Project: Jaguar and Ford Acquisition Analysis

VerifiedAdded on 2021/04/20

|14

|3013

|259

Project

AI Summary

This project provides a comprehensive analysis of Jaguar's financial performance, exploring the potential value creation resulting from its combination with Ford. It employs the Discounted Cash Flow (DCF) method to determine Jaguar's share price under various interest rate scenarios, including increases and decreases in US dollar, Deutsche Mark (DM), and Yen interest rates. The analysis delves into the currency management strategies Jaguar should adopt, focusing on the significant exposure to the US dollar and recommending hedging strategies, both financial and industrial, to mitigate currency risks. The project identifies Jaguar's exposure to the Yen, evaluates the exchange rates relevant to Ford, and determines which exposures Ford should prioritize, concluding with recommendations on whether Ford should implement hedging strategies to safeguard its financial interests. The project utilizes financial data from 1990 to 1995 to support its analysis and conclusions.

Running head: CORPORATE FINANCE

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Corporate Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

1

Table of Contents

1. Depicting how value will be created by combining Jaguar and Ford:...................................2

2. Calculating share price of Jaguar suing DCF method:...........................................................2

3. Evaluating prices of Jaguar under different scenarios:..........................................................4

3a. Increase in $ interest rate by 25%:.......................................................................................4

3b. Increase in DM interest rate by 25%:...................................................................................4

3c. Increase in Yen interest rate by 25%:...................................................................................4

3d. Decrease in $ interest rate by 10%:......................................................................................5

3e. Decrease in DM interest rate by 10%:..................................................................................5

3f. Decrease in Yen interest rate by 10%:..................................................................................5

4. Depicting the currency Jaguar should manage more:............................................................6

5. Stating the exposure of Jaguar to dollar:................................................................................7

6. Stating how much should jaguar hedge, while describing financial and industrial hedging: 8

7. Depicting the exposure of Jaguar to Yen:..............................................................................9

8a. Stating which exchange rate is Jaguar exposed:..................................................................9

8b. Depicting the source of each exposure:...............................................................................9

8c. Stating which exposure should Ford care about:................................................................10

8d. Stating should Ford hedge:.................................................................................................10

Reference and Bibliography:....................................................................................................12

1

Table of Contents

1. Depicting how value will be created by combining Jaguar and Ford:...................................2

2. Calculating share price of Jaguar suing DCF method:...........................................................2

3. Evaluating prices of Jaguar under different scenarios:..........................................................4

3a. Increase in $ interest rate by 25%:.......................................................................................4

3b. Increase in DM interest rate by 25%:...................................................................................4

3c. Increase in Yen interest rate by 25%:...................................................................................4

3d. Decrease in $ interest rate by 10%:......................................................................................5

3e. Decrease in DM interest rate by 10%:..................................................................................5

3f. Decrease in Yen interest rate by 10%:..................................................................................5

4. Depicting the currency Jaguar should manage more:............................................................6

5. Stating the exposure of Jaguar to dollar:................................................................................7

6. Stating how much should jaguar hedge, while describing financial and industrial hedging: 8

7. Depicting the exposure of Jaguar to Yen:..............................................................................9

8a. Stating which exchange rate is Jaguar exposed:..................................................................9

8b. Depicting the source of each exposure:...............................................................................9

8c. Stating which exposure should Ford care about:................................................................10

8d. Stating should Ford hedge:.................................................................................................10

Reference and Bibliography:....................................................................................................12

CORPORATE FINANCE

2

1. Depicting how value will be created by combining Jaguar and Ford:

Jaguar and Ford mainly fall under automobile industry and are considered competitors

of each other. Hence, the acquisition of Jaguar could create the highest value for Ford, which

might help the company increasing value. In addition, the values will only be created with the

help of synergies that will be created by the company with the acquisition process. This

acquisition process might mainly help in generating the levels of synergies in production, and

revenue stream that could create value for Ford. Moreover, the combination of Jaguar and

Ford could allow both companies to combine their production and dealership. This could help

in generating high level of return from investment. In this context, Aliu, Pavelkova and

Dehning (2017) stated that companies with the help of acquisitions and mergers can create

value by combining their operations and increase the overall profitability.

In addition, the value will be created by combing the production system of both the

companies and reduce the actual cost of production. This value creation might help the

company in declining the costs and increasing the level of returns. Therefore, the combined

valuation of the company could help in generating the level of returns from investment.

Furthermore, the combination could help in generating high level of sales for the company, as

the combined dealership would increase the sales of the firm, while reducing the actual cost

of production. This combined valuation would allow both the companies to generate high

level of synergies and valuation for investment. Beshears et al. (2016) argued that without the

identification of synergies companies are not able to create the relevant value, which might

reduce financial stability of the combined company.

2. Calculating share price of Jaguar suing DCF method:

Period

1 2 3 4 5 6

2

1. Depicting how value will be created by combining Jaguar and Ford:

Jaguar and Ford mainly fall under automobile industry and are considered competitors

of each other. Hence, the acquisition of Jaguar could create the highest value for Ford, which

might help the company increasing value. In addition, the values will only be created with the

help of synergies that will be created by the company with the acquisition process. This

acquisition process might mainly help in generating the levels of synergies in production, and

revenue stream that could create value for Ford. Moreover, the combination of Jaguar and

Ford could allow both companies to combine their production and dealership. This could help

in generating high level of return from investment. In this context, Aliu, Pavelkova and

Dehning (2017) stated that companies with the help of acquisitions and mergers can create

value by combining their operations and increase the overall profitability.

In addition, the value will be created by combing the production system of both the

companies and reduce the actual cost of production. This value creation might help the

company in declining the costs and increasing the level of returns. Therefore, the combined

valuation of the company could help in generating the level of returns from investment.

Furthermore, the combination could help in generating high level of sales for the company, as

the combined dealership would increase the sales of the firm, while reducing the actual cost

of production. This combined valuation would allow both the companies to generate high

level of synergies and valuation for investment. Beshears et al. (2016) argued that without the

identification of synergies companies are not able to create the relevant value, which might

reduce financial stability of the combined company.

2. Calculating share price of Jaguar suing DCF method:

Period

1 2 3 4 5 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

3

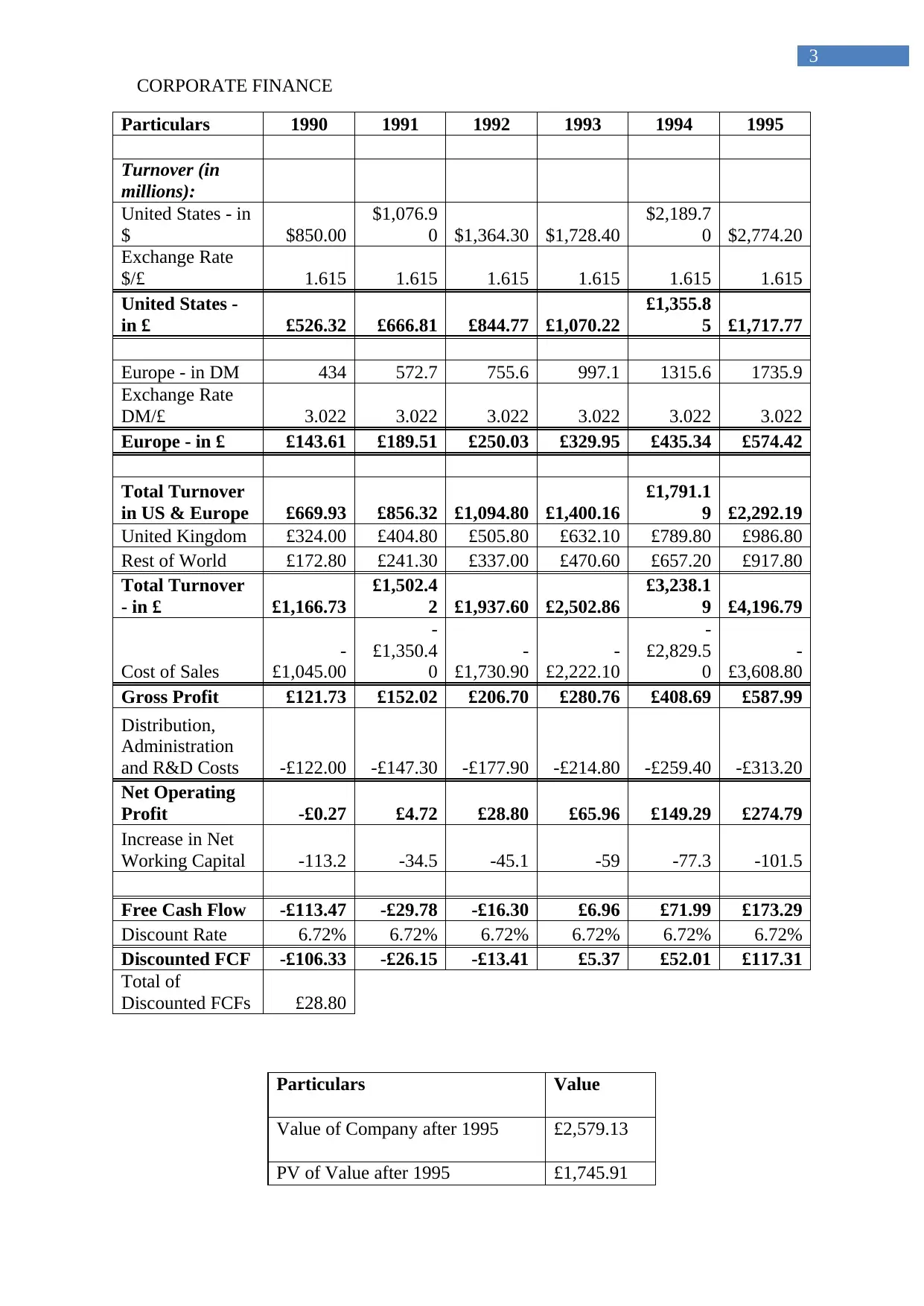

Particulars 1990 1991 1992 1993 1994 1995

Turnover (in

millions):

United States - in

$ $850.00

$1,076.9

0 $1,364.30 $1,728.40

$2,189.7

0 $2,774.20

Exchange Rate

$/£ 1.615 1.615 1.615 1.615 1.615 1.615

United States -

in £ £526.32 £666.81 £844.77 £1,070.22

£1,355.8

5 £1,717.77

Europe - in DM 434 572.7 755.6 997.1 1315.6 1735.9

Exchange Rate

DM/£ 3.022 3.022 3.022 3.022 3.022 3.022

Europe - in £ £143.61 £189.51 £250.03 £329.95 £435.34 £574.42

Total Turnover

in US & Europe £669.93 £856.32 £1,094.80 £1,400.16

£1,791.1

9 £2,292.19

United Kingdom £324.00 £404.80 £505.80 £632.10 £789.80 £986.80

Rest of World £172.80 £241.30 £337.00 £470.60 £657.20 £917.80

Total Turnover

- in £ £1,166.73

£1,502.4

2 £1,937.60 £2,502.86

£3,238.1

9 £4,196.79

Cost of Sales

-

£1,045.00

-

£1,350.4

0

-

£1,730.90

-

£2,222.10

-

£2,829.5

0

-

£3,608.80

Gross Profit £121.73 £152.02 £206.70 £280.76 £408.69 £587.99

Distribution,

Administration

and R&D Costs -£122.00 -£147.30 -£177.90 -£214.80 -£259.40 -£313.20

Net Operating

Profit -£0.27 £4.72 £28.80 £65.96 £149.29 £274.79

Increase in Net

Working Capital -113.2 -34.5 -45.1 -59 -77.3 -101.5

Free Cash Flow -£113.47 -£29.78 -£16.30 £6.96 £71.99 £173.29

Discount Rate 6.72% 6.72% 6.72% 6.72% 6.72% 6.72%

Discounted FCF -£106.33 -£26.15 -£13.41 £5.37 £52.01 £117.31

Total of

Discounted FCFs £28.80

Particulars Value

Value of Company after 1995 £2,579.13

PV of Value after 1995 £1,745.91

3

Particulars 1990 1991 1992 1993 1994 1995

Turnover (in

millions):

United States - in

$ $850.00

$1,076.9

0 $1,364.30 $1,728.40

$2,189.7

0 $2,774.20

Exchange Rate

$/£ 1.615 1.615 1.615 1.615 1.615 1.615

United States -

in £ £526.32 £666.81 £844.77 £1,070.22

£1,355.8

5 £1,717.77

Europe - in DM 434 572.7 755.6 997.1 1315.6 1735.9

Exchange Rate

DM/£ 3.022 3.022 3.022 3.022 3.022 3.022

Europe - in £ £143.61 £189.51 £250.03 £329.95 £435.34 £574.42

Total Turnover

in US & Europe £669.93 £856.32 £1,094.80 £1,400.16

£1,791.1

9 £2,292.19

United Kingdom £324.00 £404.80 £505.80 £632.10 £789.80 £986.80

Rest of World £172.80 £241.30 £337.00 £470.60 £657.20 £917.80

Total Turnover

- in £ £1,166.73

£1,502.4

2 £1,937.60 £2,502.86

£3,238.1

9 £4,196.79

Cost of Sales

-

£1,045.00

-

£1,350.4

0

-

£1,730.90

-

£2,222.10

-

£2,829.5

0

-

£3,608.80

Gross Profit £121.73 £152.02 £206.70 £280.76 £408.69 £587.99

Distribution,

Administration

and R&D Costs -£122.00 -£147.30 -£177.90 -£214.80 -£259.40 -£313.20

Net Operating

Profit -£0.27 £4.72 £28.80 £65.96 £149.29 £274.79

Increase in Net

Working Capital -113.2 -34.5 -45.1 -59 -77.3 -101.5

Free Cash Flow -£113.47 -£29.78 -£16.30 £6.96 £71.99 £173.29

Discount Rate 6.72% 6.72% 6.72% 6.72% 6.72% 6.72%

Discounted FCF -£106.33 -£26.15 -£13.41 £5.37 £52.01 £117.31

Total of

Discounted FCFs £28.80

Particulars Value

Value of Company after 1995 £2,579.13

PV of Value after 1995 £1,745.91

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

4

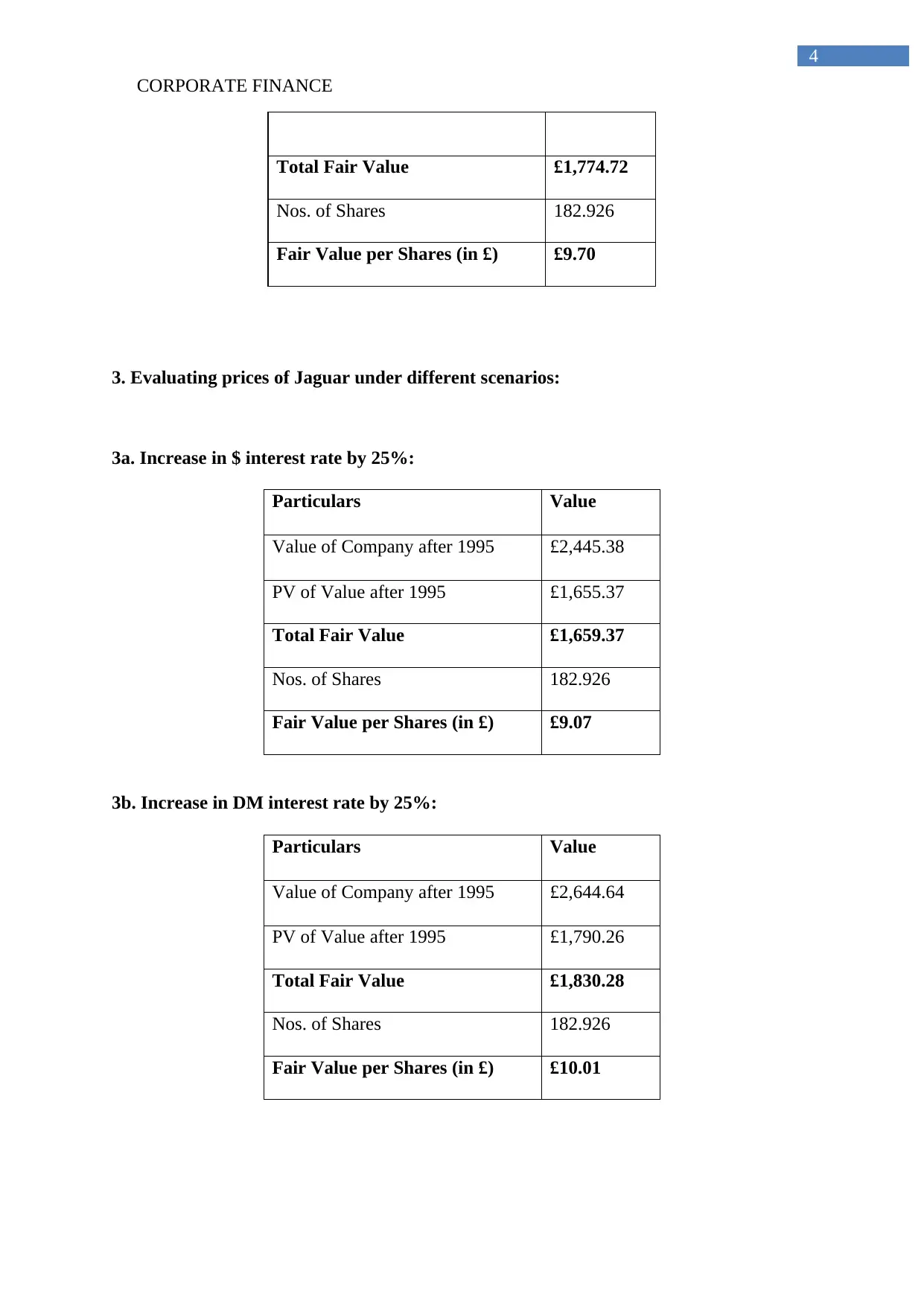

Total Fair Value £1,774.72

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.70

3. Evaluating prices of Jaguar under different scenarios:

3a. Increase in $ interest rate by 25%:

Particulars Value

Value of Company after 1995 £2,445.38

PV of Value after 1995 £1,655.37

Total Fair Value £1,659.37

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.07

3b. Increase in DM interest rate by 25%:

Particulars Value

Value of Company after 1995 £2,644.64

PV of Value after 1995 £1,790.26

Total Fair Value £1,830.28

Nos. of Shares 182.926

Fair Value per Shares (in £) £10.01

4

Total Fair Value £1,774.72

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.70

3. Evaluating prices of Jaguar under different scenarios:

3a. Increase in $ interest rate by 25%:

Particulars Value

Value of Company after 1995 £2,445.38

PV of Value after 1995 £1,655.37

Total Fair Value £1,659.37

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.07

3b. Increase in DM interest rate by 25%:

Particulars Value

Value of Company after 1995 £2,644.64

PV of Value after 1995 £1,790.26

Total Fair Value £1,830.28

Nos. of Shares 182.926

Fair Value per Shares (in £) £10.01

CORPORATE FINANCE

5

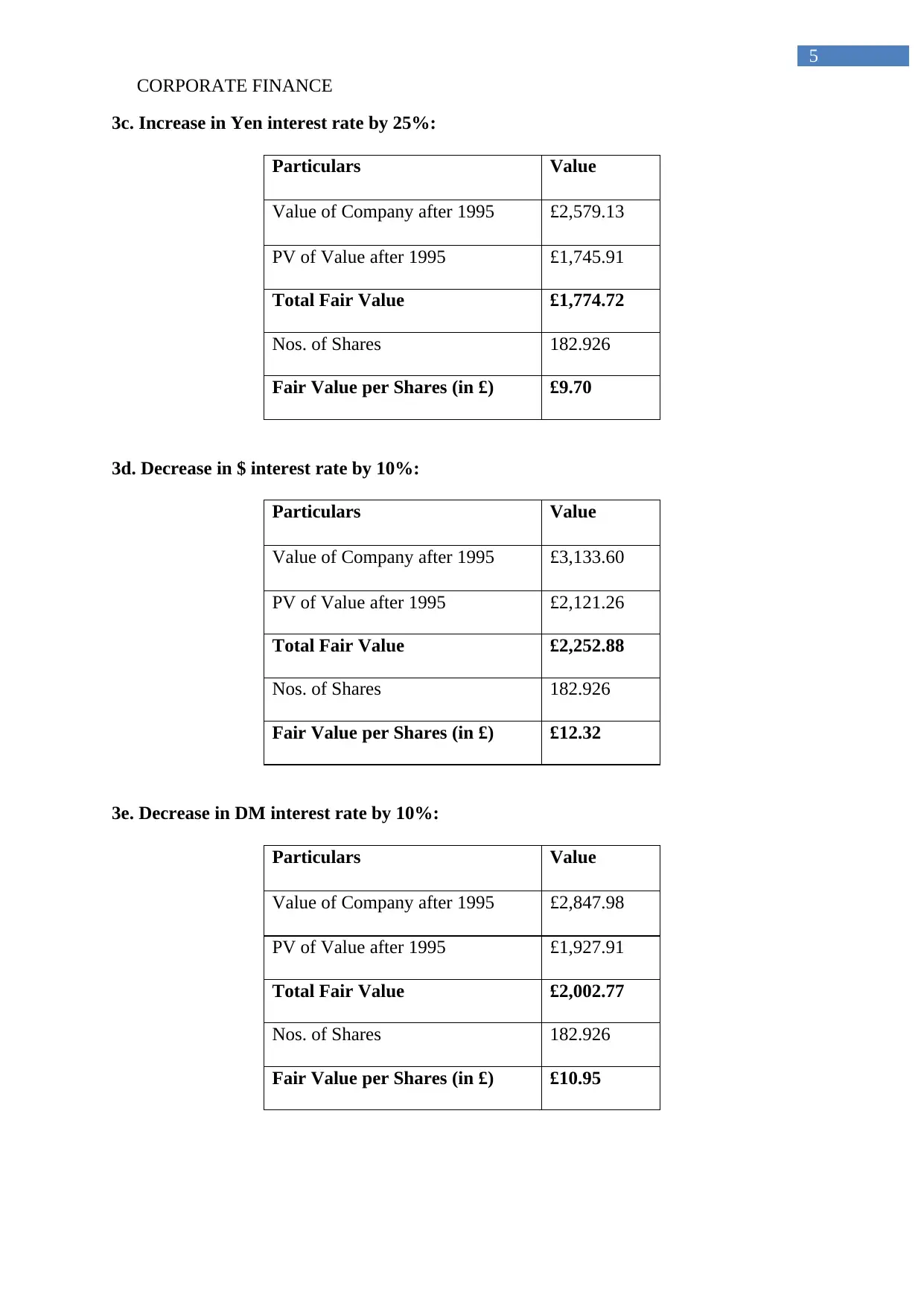

3c. Increase in Yen interest rate by 25%:

Particulars Value

Value of Company after 1995 £2,579.13

PV of Value after 1995 £1,745.91

Total Fair Value £1,774.72

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.70

3d. Decrease in $ interest rate by 10%:

Particulars Value

Value of Company after 1995 £3,133.60

PV of Value after 1995 £2,121.26

Total Fair Value £2,252.88

Nos. of Shares 182.926

Fair Value per Shares (in £) £12.32

3e. Decrease in DM interest rate by 10%:

Particulars Value

Value of Company after 1995 £2,847.98

PV of Value after 1995 £1,927.91

Total Fair Value £2,002.77

Nos. of Shares 182.926

Fair Value per Shares (in £) £10.95

5

3c. Increase in Yen interest rate by 25%:

Particulars Value

Value of Company after 1995 £2,579.13

PV of Value after 1995 £1,745.91

Total Fair Value £1,774.72

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.70

3d. Decrease in $ interest rate by 10%:

Particulars Value

Value of Company after 1995 £3,133.60

PV of Value after 1995 £2,121.26

Total Fair Value £2,252.88

Nos. of Shares 182.926

Fair Value per Shares (in £) £12.32

3e. Decrease in DM interest rate by 10%:

Particulars Value

Value of Company after 1995 £2,847.98

PV of Value after 1995 £1,927.91

Total Fair Value £2,002.77

Nos. of Shares 182.926

Fair Value per Shares (in £) £10.95

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

6

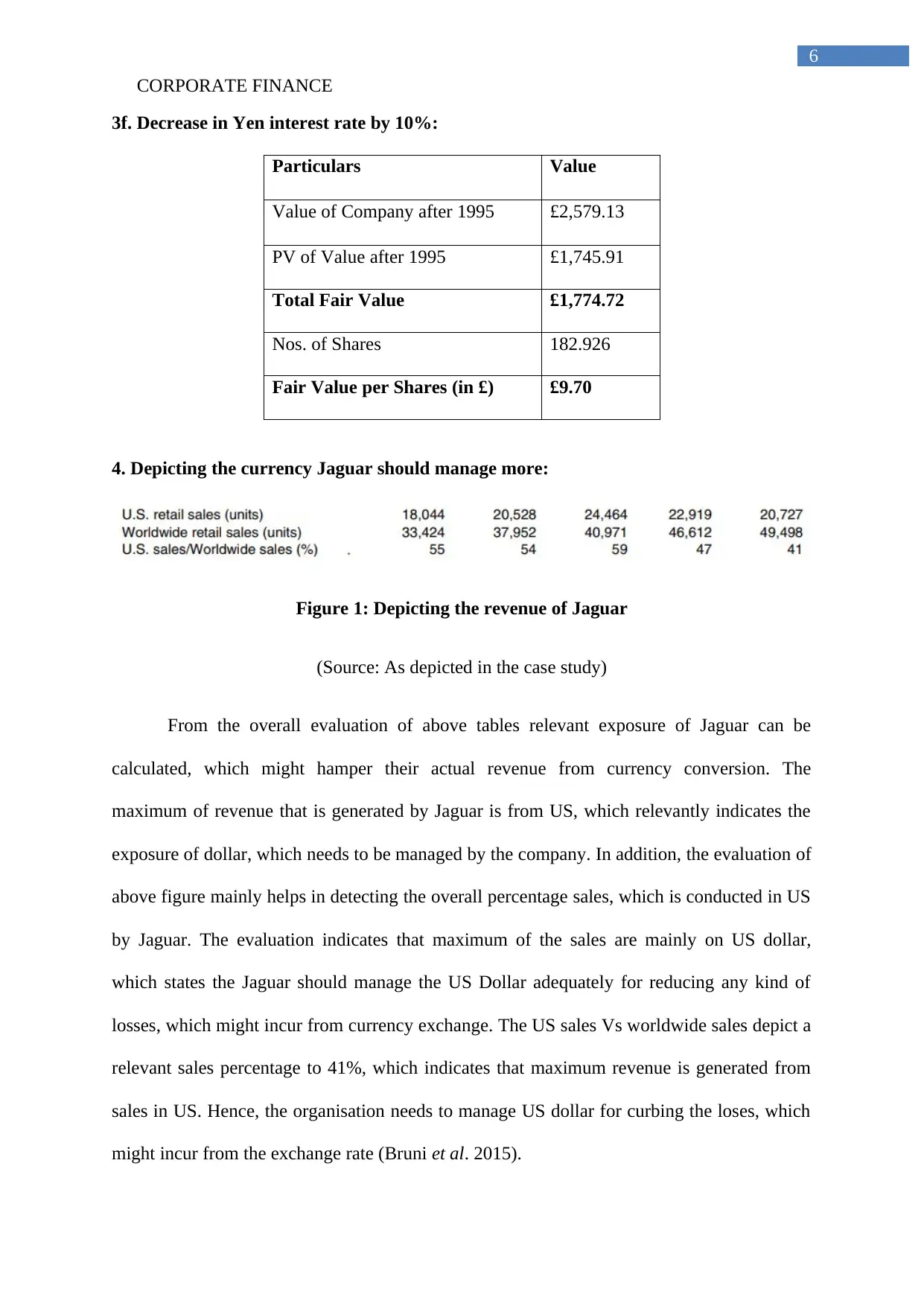

3f. Decrease in Yen interest rate by 10%:

Particulars Value

Value of Company after 1995 £2,579.13

PV of Value after 1995 £1,745.91

Total Fair Value £1,774.72

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.70

4. Depicting the currency Jaguar should manage more:

Figure 1: Depicting the revenue of Jaguar

(Source: As depicted in the case study)

From the overall evaluation of above tables relevant exposure of Jaguar can be

calculated, which might hamper their actual revenue from currency conversion. The

maximum of revenue that is generated by Jaguar is from US, which relevantly indicates the

exposure of dollar, which needs to be managed by the company. In addition, the evaluation of

above figure mainly helps in detecting the overall percentage sales, which is conducted in US

by Jaguar. The evaluation indicates that maximum of the sales are mainly on US dollar,

which states the Jaguar should manage the US Dollar adequately for reducing any kind of

losses, which might incur from currency exchange. The US sales Vs worldwide sales depict a

relevant sales percentage to 41%, which indicates that maximum revenue is generated from

sales in US. Hence, the organisation needs to manage US dollar for curbing the loses, which

might incur from the exchange rate (Bruni et al. 2015).

6

3f. Decrease in Yen interest rate by 10%:

Particulars Value

Value of Company after 1995 £2,579.13

PV of Value after 1995 £1,745.91

Total Fair Value £1,774.72

Nos. of Shares 182.926

Fair Value per Shares (in £) £9.70

4. Depicting the currency Jaguar should manage more:

Figure 1: Depicting the revenue of Jaguar

(Source: As depicted in the case study)

From the overall evaluation of above tables relevant exposure of Jaguar can be

calculated, which might hamper their actual revenue from currency conversion. The

maximum of revenue that is generated by Jaguar is from US, which relevantly indicates the

exposure of dollar, which needs to be managed by the company. In addition, the evaluation of

above figure mainly helps in detecting the overall percentage sales, which is conducted in US

by Jaguar. The evaluation indicates that maximum of the sales are mainly on US dollar,

which states the Jaguar should manage the US Dollar adequately for reducing any kind of

losses, which might incur from currency exchange. The US sales Vs worldwide sales depict a

relevant sales percentage to 41%, which indicates that maximum revenue is generated from

sales in US. Hence, the organisation needs to manage US dollar for curbing the loses, which

might incur from the exchange rate (Bruni et al. 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

7

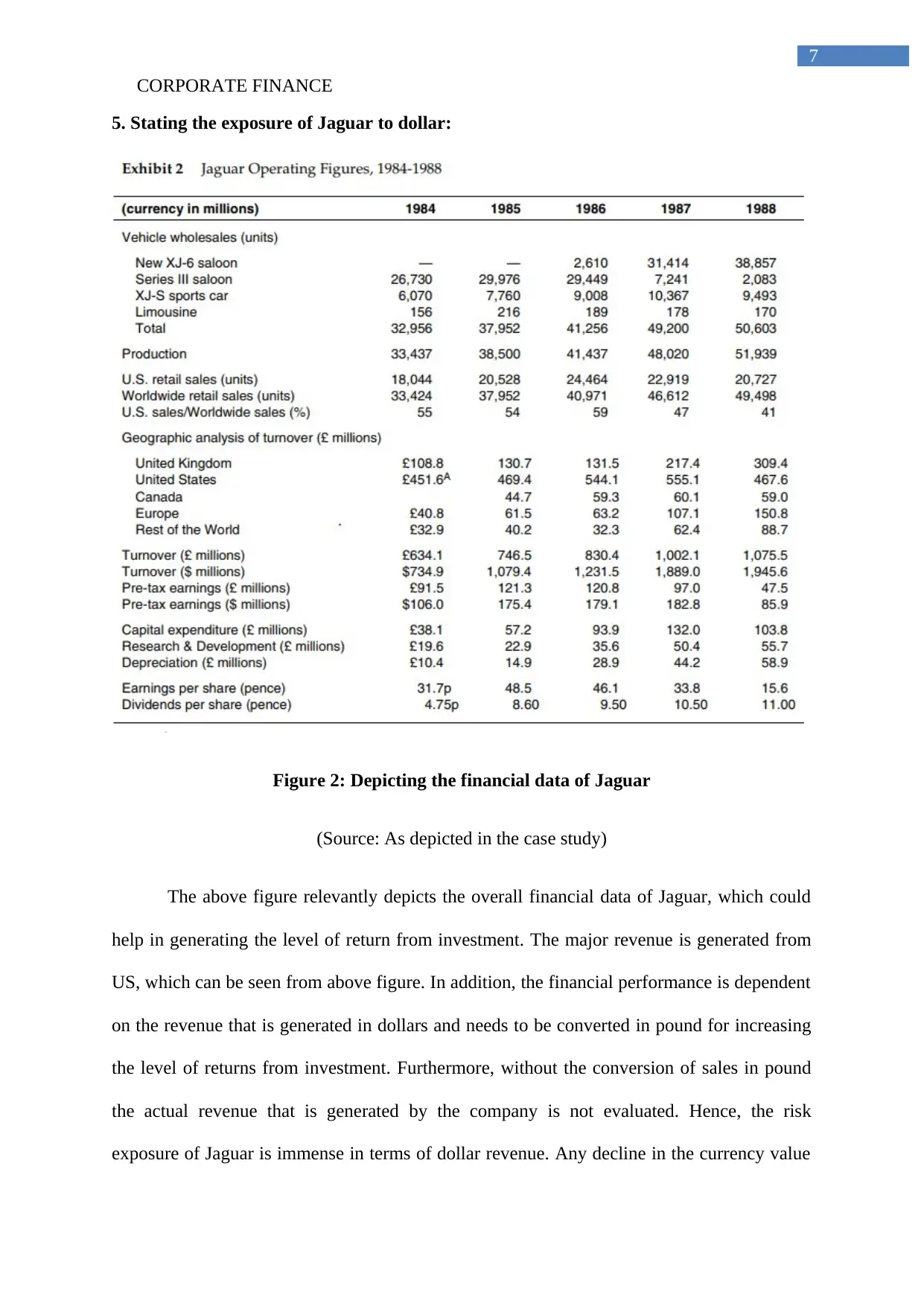

5. Stating the exposure of Jaguar to dollar:

Figure 2: Depicting the financial data of Jaguar

(Source: As depicted in the case study)

The above figure relevantly depicts the overall financial data of Jaguar, which could

help in generating the level of return from investment. The major revenue is generated from

US, which can be seen from above figure. In addition, the financial performance is dependent

on the revenue that is generated in dollars and needs to be converted in pound for increasing

the level of returns from investment. Furthermore, without the conversion of sales in pound

the actual revenue that is generated by the company is not evaluated. Hence, the risk

exposure of Jaguar is immense in terms of dollar revenue. Any decline in the currency value

7

5. Stating the exposure of Jaguar to dollar:

Figure 2: Depicting the financial data of Jaguar

(Source: As depicted in the case study)

The above figure relevantly depicts the overall financial data of Jaguar, which could

help in generating the level of return from investment. The major revenue is generated from

US, which can be seen from above figure. In addition, the financial performance is dependent

on the revenue that is generated in dollars and needs to be converted in pound for increasing

the level of returns from investment. Furthermore, without the conversion of sales in pound

the actual revenue that is generated by the company is not evaluated. Hence, the risk

exposure of Jaguar is immense in terms of dollar revenue. Any decline in the currency value

CORPORATE FINANCE

8

might hamper actual valuation of the stock and directly affect its revenue generating capacity.

Therefore, Jaguar needs to conduct adequate valuation and adjust for their exposure in the

market, which could help in reducing the losses from currency conversion (Hung et al. 2018).

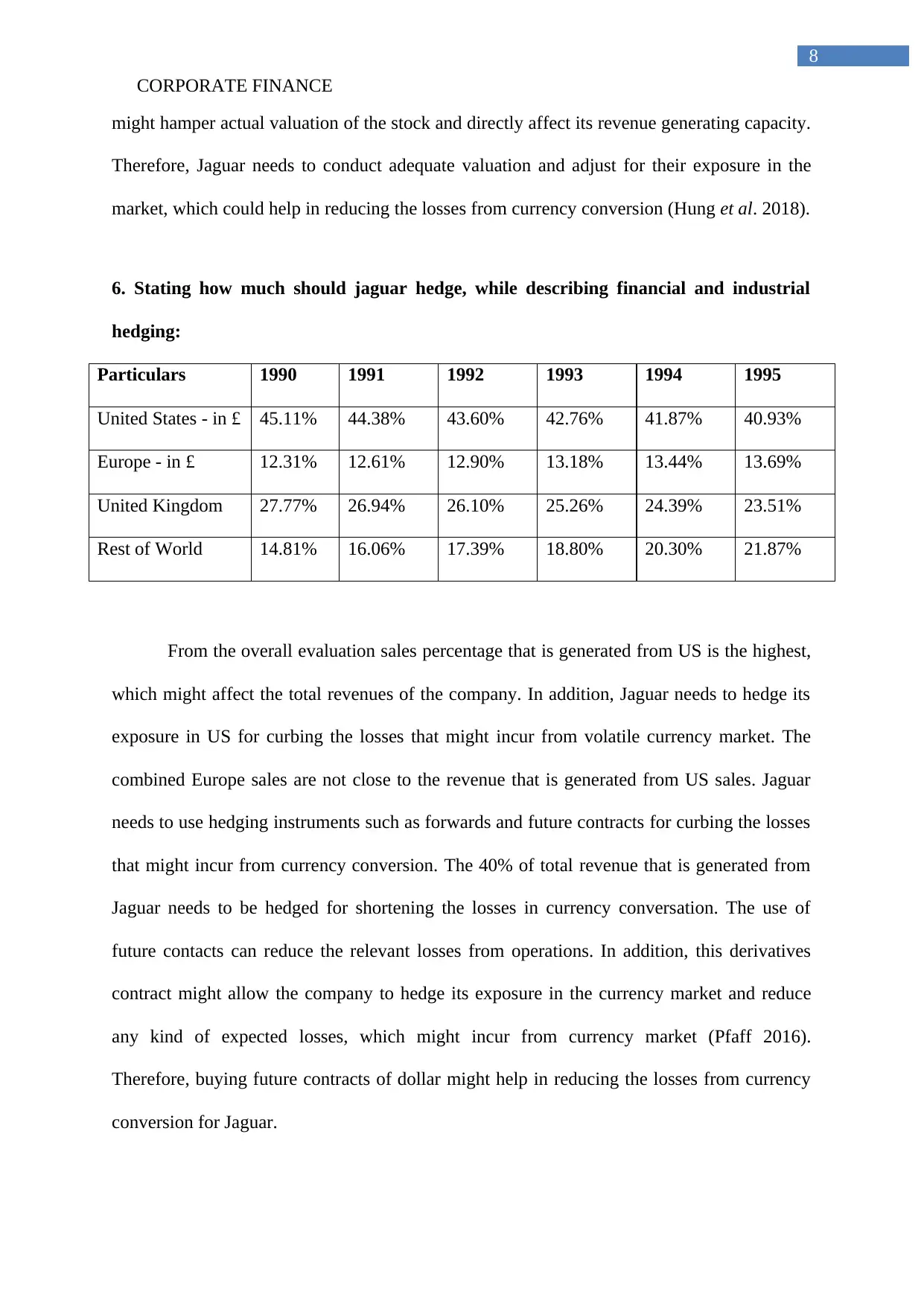

6. Stating how much should jaguar hedge, while describing financial and industrial

hedging:

Particulars 1990 1991 1992 1993 1994 1995

United States - in £ 45.11% 44.38% 43.60% 42.76% 41.87% 40.93%

Europe - in £ 12.31% 12.61% 12.90% 13.18% 13.44% 13.69%

United Kingdom 27.77% 26.94% 26.10% 25.26% 24.39% 23.51%

Rest of World 14.81% 16.06% 17.39% 18.80% 20.30% 21.87%

From the overall evaluation sales percentage that is generated from US is the highest,

which might affect the total revenues of the company. In addition, Jaguar needs to hedge its

exposure in US for curbing the losses that might incur from volatile currency market. The

combined Europe sales are not close to the revenue that is generated from US sales. Jaguar

needs to use hedging instruments such as forwards and future contracts for curbing the losses

that might incur from currency conversion. The 40% of total revenue that is generated from

Jaguar needs to be hedged for shortening the losses in currency conversation. The use of

future contacts can reduce the relevant losses from operations. In addition, this derivatives

contract might allow the company to hedge its exposure in the currency market and reduce

any kind of expected losses, which might incur from currency market (Pfaff 2016).

Therefore, buying future contracts of dollar might help in reducing the losses from currency

conversion for Jaguar.

8

might hamper actual valuation of the stock and directly affect its revenue generating capacity.

Therefore, Jaguar needs to conduct adequate valuation and adjust for their exposure in the

market, which could help in reducing the losses from currency conversion (Hung et al. 2018).

6. Stating how much should jaguar hedge, while describing financial and industrial

hedging:

Particulars 1990 1991 1992 1993 1994 1995

United States - in £ 45.11% 44.38% 43.60% 42.76% 41.87% 40.93%

Europe - in £ 12.31% 12.61% 12.90% 13.18% 13.44% 13.69%

United Kingdom 27.77% 26.94% 26.10% 25.26% 24.39% 23.51%

Rest of World 14.81% 16.06% 17.39% 18.80% 20.30% 21.87%

From the overall evaluation sales percentage that is generated from US is the highest,

which might affect the total revenues of the company. In addition, Jaguar needs to hedge its

exposure in US for curbing the losses that might incur from volatile currency market. The

combined Europe sales are not close to the revenue that is generated from US sales. Jaguar

needs to use hedging instruments such as forwards and future contracts for curbing the losses

that might incur from currency conversion. The 40% of total revenue that is generated from

Jaguar needs to be hedged for shortening the losses in currency conversation. The use of

future contacts can reduce the relevant losses from operations. In addition, this derivatives

contract might allow the company to hedge its exposure in the currency market and reduce

any kind of expected losses, which might incur from currency market (Pfaff 2016).

Therefore, buying future contracts of dollar might help in reducing the losses from currency

conversion for Jaguar.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE FINANCE

9

7. Depicting the exposure of Jaguar to Yen:

The current exposure of Jaguar in Japan is relatively lower than other countries, where

operations of the company has not been conducted adequately. In addition, the revenue

generated from japan is relevant low, which reduced the implication and exposure of Jaguar

in Yen. This relevant exposure of the company might directly affect the overall profitability,

which might incur from operations. This exposure from currency conversion is relatively low,

where the actual revenue that is generated in Japan can be hedged with using appropriate

instrument (Zhang, Liu and Xu 2014).

8a. Stating which exchange rate is Jaguar exposed:

In perspective of Ford a US-based shareholder Jaguar is mainly exposed to DM and

Pound currency, which could hamper relevant profits of the shareholders. In addition, the

major exposure of the company is mainly on pound, where the actual expenses are been

conducted for the production of cars. This exposure of the Jaguar after the acquisition might

be controlled with the help of hedging process, which might be useful for US-based

shareholder to increase their return from investment. Being a US-based shareholder the

relevant revenues that is been generated outside US needs to be hedged for reducing the

negative impact from currency conversion. In addition, the operations of Jaguar need to be

evaluated based on US dollars, which might help in generating high rate of return from

investment (Damodaran 2016).

8b. Depicting the source of each exposure:

There are two different sources of each exposure, which is generated from pound and

DM. The high-end exposure for US-Based shareholders can be conducted by hedging

adequate pound in comparison to dollar. In addition, the exposure from pound is due to the

production facility, which is located in UK. In addition, the sales revenue from Europe and

9

7. Depicting the exposure of Jaguar to Yen:

The current exposure of Jaguar in Japan is relatively lower than other countries, where

operations of the company has not been conducted adequately. In addition, the revenue

generated from japan is relevant low, which reduced the implication and exposure of Jaguar

in Yen. This relevant exposure of the company might directly affect the overall profitability,

which might incur from operations. This exposure from currency conversion is relatively low,

where the actual revenue that is generated in Japan can be hedged with using appropriate

instrument (Zhang, Liu and Xu 2014).

8a. Stating which exchange rate is Jaguar exposed:

In perspective of Ford a US-based shareholder Jaguar is mainly exposed to DM and

Pound currency, which could hamper relevant profits of the shareholders. In addition, the

major exposure of the company is mainly on pound, where the actual expenses are been

conducted for the production of cars. This exposure of the Jaguar after the acquisition might

be controlled with the help of hedging process, which might be useful for US-based

shareholder to increase their return from investment. Being a US-based shareholder the

relevant revenues that is been generated outside US needs to be hedged for reducing the

negative impact from currency conversion. In addition, the operations of Jaguar need to be

evaluated based on US dollars, which might help in generating high rate of return from

investment (Damodaran 2016).

8b. Depicting the source of each exposure:

There are two different sources of each exposure, which is generated from pound and

DM. The high-end exposure for US-Based shareholders can be conducted by hedging

adequate pound in comparison to dollar. In addition, the exposure from pound is due to the

production facility, which is located in UK. In addition, the sales revenue from Europe and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE FINANCE

10

Germany is also conducted by the company over the period. Therefore, the revenues and

expenses incurred in UK is the major source of exposure for the pound currency. The second

source of exposure is the currency DM, which is generated from Germany. Jaguar conducts

adequate sales in Germany, which could increase the accumulation of DM by the company

and needs to be converted in US dollar. Moreover, this source of exposure is relevantly high,

as the company obtains adequate revenue from the sales of cars in Germany, as depicted in

case study (Fracassi 2016).

8c. Stating which exposure should Ford care about:

From the overall evaluation, exposure in pound needs to be assessed by Ford and can

take relevant measure to control risk from currency exchange. In addition, Ford after

acquiring Jaguar needs to be concerned regarding exposure in pound that is made by the

company. Hence, the exposure in pound is the main concern for the company, as the overall

revenue and expense are in pound. This would directly hamper the actual performance of the

company if Ford is not careful in hedging their exposure in the UK market. Furthermore, the

exposure on DM also needs to be evaluated by Ford, as adequate revenue is generated from

Europe division of Jaguar (Foley and Manova 2015). Therefore, exposure in currency market

and commodity market needs to be conducted by Ford for reducing the risk from their

investment.

8d. Stating should Ford hedge:

From the overall evaluation, Jaguar has relevant exposure in pound and DM, which

needs to be hedged adequately for reducing risk from currency market. In addition, the

exposure in the current market mainly needs to be reduced by using adequate level of

hedging contracts such as futures and forward contracts. In this context, Scholes (2015)

mentioned that companies with the help of hedging process can reduce the risk from volatile

10

Germany is also conducted by the company over the period. Therefore, the revenues and

expenses incurred in UK is the major source of exposure for the pound currency. The second

source of exposure is the currency DM, which is generated from Germany. Jaguar conducts

adequate sales in Germany, which could increase the accumulation of DM by the company

and needs to be converted in US dollar. Moreover, this source of exposure is relevantly high,

as the company obtains adequate revenue from the sales of cars in Germany, as depicted in

case study (Fracassi 2016).

8c. Stating which exposure should Ford care about:

From the overall evaluation, exposure in pound needs to be assessed by Ford and can

take relevant measure to control risk from currency exchange. In addition, Ford after

acquiring Jaguar needs to be concerned regarding exposure in pound that is made by the

company. Hence, the exposure in pound is the main concern for the company, as the overall

revenue and expense are in pound. This would directly hamper the actual performance of the

company if Ford is not careful in hedging their exposure in the UK market. Furthermore, the

exposure on DM also needs to be evaluated by Ford, as adequate revenue is generated from

Europe division of Jaguar (Foley and Manova 2015). Therefore, exposure in currency market

and commodity market needs to be conducted by Ford for reducing the risk from their

investment.

8d. Stating should Ford hedge:

From the overall evaluation, Jaguar has relevant exposure in pound and DM, which

needs to be hedged adequately for reducing risk from currency market. In addition, the

exposure in the current market mainly needs to be reduced by using adequate level of

hedging contracts such as futures and forward contracts. In this context, Scholes (2015)

mentioned that companies with the help of hedging process can reduce the risk from volatile

CORPORATE FINANCE

11

markets in which they are trading. Furthermore, the evaluation mainly helps in depicting the

risk, which mouth hamper the actual profits of the organisation. On the other hand,

Bazdresch, Kahn and Whited (2017) criticises that hedging process without evaluation does

not provide adequate return for the organisation, while increase the chance of risk from

investment. Therefore, Ford needs to have adequate hedging contract for both pound and

DM, which could help in generating high level of returns from investment.

11

markets in which they are trading. Furthermore, the evaluation mainly helps in depicting the

risk, which mouth hamper the actual profits of the organisation. On the other hand,

Bazdresch, Kahn and Whited (2017) criticises that hedging process without evaluation does

not provide adequate return for the organisation, while increase the chance of risk from

investment. Therefore, Ford needs to have adequate hedging contract for both pound and

DM, which could help in generating high level of returns from investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.