Understanding Management Accounting Systems: Jaguar Land Rover Report

VerifiedAdded on 2021/02/19

|18

|5717

|77

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems within Jaguar Land Rover Automotive Plc. It begins with an introduction to management accounting, its significance in decision-making, and the essential requirements of its systems. The report then delves into the different types of management accounting systems, including cost accounting, inventory management, job costing, and price optimization systems, highlighting their advantages. Furthermore, it explores various methods of management accounting reporting, such as budget reports, account receivable reports, performance reports, and cost reports. The core of the report focuses on calculation methods, including marginal costing and absorption costing, with detailed calculations and comparisons presented in the annexure. The report also provides financial analysis, including calculations with cost analysis techniques and preparation of income statements, offering a clear understanding of how Jaguar Land Rover uses management accounting to address financial challenges and improve business operations. This report is a valuable resource for students studying management accounting.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management accounting is related with the process of preparation and formation of

financial reports containing both the financial as well as non financial, statistical information. It

assists management of the business organization so that they can facilitate decision-making in

the business. It involves evaluating and providing the company's internal reports to the managers

which helps them to make further decisions and strategies for the organization. Management

accounting represents the internal errors and complications related to the company's financial

position and helps the managers to set effective measures to overcome those problems. This

report is on Jaguar land Rover Automotive Plc, which is one of the British multinational

company engaged in Automotive services. The company is having its headquartered in Coventry,

United Kingdom. The company manufactures luxury vehicles and sport utility vehicles. This

company carry a strong brand name in the market and they are famous for its unique designs.

The company has the revenue of over £25.8 billion and consists of 43,224 employees across the

world.

This report will demonstrate the understanding of MA systems with different methods

used in framing reports. The report will also include calculations with cost analysis techniques

and preparation of income statement. Report will define different planning tools as used in

management accounting along with their benefits and drawbacks. At last, emphasis will be made

on comparing how organization uses MA system for dealing with financial problem.

MAIN BODY

LO 1

P1 Understanding MA and essential requirements of its systems.

Management accounting- It provides base for effective decision-making process

thereby framing plan and improving performance of the business. It also helps in providing

assistance in financial report making for managers in framing and implementing the strategies

and effective measures for the organization. It involves preparation of various components such

as Capital budgeting, valuation of stock, break even analysis, cost estimation for a product,

forecasting the demand of the market and strategies to overcome the financial problems which

1

Management accounting is related with the process of preparation and formation of

financial reports containing both the financial as well as non financial, statistical information. It

assists management of the business organization so that they can facilitate decision-making in

the business. It involves evaluating and providing the company's internal reports to the managers

which helps them to make further decisions and strategies for the organization. Management

accounting represents the internal errors and complications related to the company's financial

position and helps the managers to set effective measures to overcome those problems. This

report is on Jaguar land Rover Automotive Plc, which is one of the British multinational

company engaged in Automotive services. The company is having its headquartered in Coventry,

United Kingdom. The company manufactures luxury vehicles and sport utility vehicles. This

company carry a strong brand name in the market and they are famous for its unique designs.

The company has the revenue of over £25.8 billion and consists of 43,224 employees across the

world.

This report will demonstrate the understanding of MA systems with different methods

used in framing reports. The report will also include calculations with cost analysis techniques

and preparation of income statement. Report will define different planning tools as used in

management accounting along with their benefits and drawbacks. At last, emphasis will be made

on comparing how organization uses MA system for dealing with financial problem.

MAIN BODY

LO 1

P1 Understanding MA and essential requirements of its systems.

Management accounting- It provides base for effective decision-making process

thereby framing plan and improving performance of the business. It also helps in providing

assistance in financial report making for managers in framing and implementing the strategies

and effective measures for the organization. It involves preparation of various components such

as Capital budgeting, valuation of stock, break even analysis, cost estimation for a product,

forecasting the demand of the market and strategies to overcome the financial problems which

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

drives towards the long term sustainable growth of the organization (Mack and Goretzki, 2017).

Management accounting helps the businesses to eliminate their costs as well as reduce their

risks.

MA systems- It helps in making improvement in performance level as well as making overall

efficiency of production of the organization in order to possess higher profitability and greater

market share for its business growth and development. It helps in decision-making for the

managers related to the various issues and problems in an organization. Management accounting

systems are classified into-

Cost accounting system- It is a technique that enables Jaguar Land Rover Plc in cost

estimation for various activities in order to determine profitability analysis, inventory valuation

and controlling cost factor (Maskell and et.al., 2016). It mainly used to determine the cost of

different products in relation with the production department of the organization. This in turn

helps the organization to determine the profitability and revenue as well. It includes activities

such as work in progress, inventory and finished goods cost etc.

The important elements of the cost accounting are direct and indirect material, labour

costs, overhead expenses- fixed and variable. Cost accounting is helpful and effective in

analysing and evaluating the future cost of production of goods and considers direct costing in

relation to production function. It includes factors such as salary, wages, production expenses,

etc. and other direct cost of production.

Inventory management system- A method of determining the levels of finished goods in

warehouse, delivery of products and sales demand. In simple words, it involves management of

the supply chain process. It enables organization to monitor on the movement of business

operations which further enables the company in effective decision-making and investments. It

manages the orders from the market and the products supplied and all the activities related to

these activities and helps the organization in better delivery of goods in market to overcome the

sales demand. Inventory management system uses various methods for managing the stock as

such- First in First out method (FIFO), Last in first out method (LIFO), ABC analysis, Just in

time approach and weighted average method.

Job costing system- It monitors all the expenses thereby allocating costs to every product

manufactured to keep track on expenses incurred. The manufacturing costs covers overheads,

material cost and labour costs and estimating their actual value. Jaguar Land rover uses such

2

Management accounting helps the businesses to eliminate their costs as well as reduce their

risks.

MA systems- It helps in making improvement in performance level as well as making overall

efficiency of production of the organization in order to possess higher profitability and greater

market share for its business growth and development. It helps in decision-making for the

managers related to the various issues and problems in an organization. Management accounting

systems are classified into-

Cost accounting system- It is a technique that enables Jaguar Land Rover Plc in cost

estimation for various activities in order to determine profitability analysis, inventory valuation

and controlling cost factor (Maskell and et.al., 2016). It mainly used to determine the cost of

different products in relation with the production department of the organization. This in turn

helps the organization to determine the profitability and revenue as well. It includes activities

such as work in progress, inventory and finished goods cost etc.

The important elements of the cost accounting are direct and indirect material, labour

costs, overhead expenses- fixed and variable. Cost accounting is helpful and effective in

analysing and evaluating the future cost of production of goods and considers direct costing in

relation to production function. It includes factors such as salary, wages, production expenses,

etc. and other direct cost of production.

Inventory management system- A method of determining the levels of finished goods in

warehouse, delivery of products and sales demand. In simple words, it involves management of

the supply chain process. It enables organization to monitor on the movement of business

operations which further enables the company in effective decision-making and investments. It

manages the orders from the market and the products supplied and all the activities related to

these activities and helps the organization in better delivery of goods in market to overcome the

sales demand. Inventory management system uses various methods for managing the stock as

such- First in First out method (FIFO), Last in first out method (LIFO), ABC analysis, Just in

time approach and weighted average method.

Job costing system- It monitors all the expenses thereby allocating costs to every product

manufactured to keep track on expenses incurred. The manufacturing costs covers overheads,

material cost and labour costs and estimating their actual value. Jaguar Land rover uses such

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system to control raw material usage, labour time and equipment cost which all in turn

determines the cost of single unit of product which in turn helps in making estimates of the

profits and preparation of financial reports for strategic decision-making for the company.

Price optimization system- Helps in assessing prices of the products and services as

delivered by the business firm It helps the company to maximize its profits and pursue its goals

and objectives for the growth its business. It understands the change in behaviour of customer

due to change in the price level thereby determining demand and supply of such products in the

market. Price optimization system includes collection of historical data, product volumes,

company's product prices, competitor's prices, economic conditions of the market and the

determination of prices of the products is done by considering these factors (Mills, 2018). With

the help of all these factors the organization can set effective prices of their products so that the

customers are influenced and also the company earn profits and understands the behaviour and

reaction of customer towards the set prices.

Advantages of MA system- It enables Jaguar Land Rover Plc in planning, organizing,

controlling and coordinating its business activities for betterment and growth of the organization.

It also improves the efficiency and performance as well as productivity in order to attain

different economies of scale. Management accounting reports enables the stakeholders in

identification of the problem in the organization and frame effective measures and strategies to

overcome those problems. It also helps in budget planning and various cost estimations for the

organization.

P2 Methods of MA reporting

Are different tools which helps in determining and understanding the business operations

of an organization accurately. It provides relevant information to the managers which further

enables in making effective decisions related the different issues being identified in the report.

This reports highlights performance of the business consisting all the elements of the

organization and helps the managers and the top-level personnel to understand the productivity

and capability of the company and what all things to be planned to match the actual one with the

primary objectives of the business. The following are types of such reports-

Budget report- Assist in performance evaluation by comparing actual outcome with the

prepared budgeted plan in order to identify the differences between them. It is concerned with

comparison of the company's past performance with the current one and implements necessary

3

determines the cost of single unit of product which in turn helps in making estimates of the

profits and preparation of financial reports for strategic decision-making for the company.

Price optimization system- Helps in assessing prices of the products and services as

delivered by the business firm It helps the company to maximize its profits and pursue its goals

and objectives for the growth its business. It understands the change in behaviour of customer

due to change in the price level thereby determining demand and supply of such products in the

market. Price optimization system includes collection of historical data, product volumes,

company's product prices, competitor's prices, economic conditions of the market and the

determination of prices of the products is done by considering these factors (Mills, 2018). With

the help of all these factors the organization can set effective prices of their products so that the

customers are influenced and also the company earn profits and understands the behaviour and

reaction of customer towards the set prices.

Advantages of MA system- It enables Jaguar Land Rover Plc in planning, organizing,

controlling and coordinating its business activities for betterment and growth of the organization.

It also improves the efficiency and performance as well as productivity in order to attain

different economies of scale. Management accounting reports enables the stakeholders in

identification of the problem in the organization and frame effective measures and strategies to

overcome those problems. It also helps in budget planning and various cost estimations for the

organization.

P2 Methods of MA reporting

Are different tools which helps in determining and understanding the business operations

of an organization accurately. It provides relevant information to the managers which further

enables in making effective decisions related the different issues being identified in the report.

This reports highlights performance of the business consisting all the elements of the

organization and helps the managers and the top-level personnel to understand the productivity

and capability of the company and what all things to be planned to match the actual one with the

primary objectives of the business. The following are types of such reports-

Budget report- Assist in performance evaluation by comparing actual outcome with the

prepared budgeted plan in order to identify the differences between them. It is concerned with

comparison of the company's past performance with the current one and implements necessary

3

steps and actions to initiate higher profits. Budget report involves estimation of the revenue and

expenses of the company in the future, which in turn later helps to determine the variances in the

performance as well.

Account receivable report- This report consists of amount to be received by the company

from different individuals and stakeholders. It represents the time of the money to be receive and

the amount received, Greater the time limit lower will be the credit limit to be initiated by the

company (Otley, 2016). It helps to determine the credits to be provided to the customers by the

company. Account receivable report includes all the information regarding the people who owe

the company's money and keep track on it.

Performance report- Performance report analyses and evaluates the performance of the

company. It provides detailed understanding of the company's performance which further

represents the productivity of Jaguar Land rover company. It provides all the necessary data

related to the performance of the company to the stakeholders so that they can make the

decisions for the improvement of the same. It also helps in estimation of the profitability for the

company by representing the current status of its performance.

Cost report- It is concerned with the identification of the cost incurred for undertaking

business operations. Such report determines cost of every element of the organization that

includes products, services, manufacturing process, distribution and other elements. This in turn

enables the managers to keep a watch on each and every cost and assist in determining strategies

to reduce down extra cost and expenses in certain areas.

LO 2

P 3 Calculation

Methods for Management accounting systems

Marginal costing- Marginal costing refers to the change in the actual cost with adding up of

one more unit in the production. It helps Jaguar Land Rover company to determine the

additional cost being incurred by the company while producing one extra unit. The

following are the advantages and disadvantages of marginal costing-

Advantages- An easy way of determining and controlling cost of production. It also eliminates

the differences in the cost as there is no change in fixed overheads of the production process.

It helps to determine the production capacity from the available raw materials and determine

the ways for optimum production.

4

expenses of the company in the future, which in turn later helps to determine the variances in the

performance as well.

Account receivable report- This report consists of amount to be received by the company

from different individuals and stakeholders. It represents the time of the money to be receive and

the amount received, Greater the time limit lower will be the credit limit to be initiated by the

company (Otley, 2016). It helps to determine the credits to be provided to the customers by the

company. Account receivable report includes all the information regarding the people who owe

the company's money and keep track on it.

Performance report- Performance report analyses and evaluates the performance of the

company. It provides detailed understanding of the company's performance which further

represents the productivity of Jaguar Land rover company. It provides all the necessary data

related to the performance of the company to the stakeholders so that they can make the

decisions for the improvement of the same. It also helps in estimation of the profitability for the

company by representing the current status of its performance.

Cost report- It is concerned with the identification of the cost incurred for undertaking

business operations. Such report determines cost of every element of the organization that

includes products, services, manufacturing process, distribution and other elements. This in turn

enables the managers to keep a watch on each and every cost and assist in determining strategies

to reduce down extra cost and expenses in certain areas.

LO 2

P 3 Calculation

Methods for Management accounting systems

Marginal costing- Marginal costing refers to the change in the actual cost with adding up of

one more unit in the production. It helps Jaguar Land Rover company to determine the

additional cost being incurred by the company while producing one extra unit. The

following are the advantages and disadvantages of marginal costing-

Advantages- An easy way of determining and controlling cost of production. It also eliminates

the differences in the cost as there is no change in fixed overheads of the production process.

It helps to determine the production capacity from the available raw materials and determine

the ways for optimum production.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Disadvantages- It is complex in determining the degree of variances as marginal costing does

not consider all the variable costs in it. Marginal cost remains constant for shorter time

duration only.

Absorption Costing- Absorption costing is concerned with calculating and considering all

the cost involved in the process of production. It includes direct, indirect and all other cost to

derive accurate results and helps in decision-making further (Quattrone, 2016). The

following are the advantages and disadvantages of absorption costing-

Advantages- It is the simplests method and ideal for decision-making process by the managers as

it contains fewer fluctuations in calculating the profit margins. This method determines the

profits accurately as it considers all the costs of production.

Disadvantages- This technique is not suitable in improvement of business operations. It is only

concerned with the profits of the company and is not useful for comparing different product

lines.

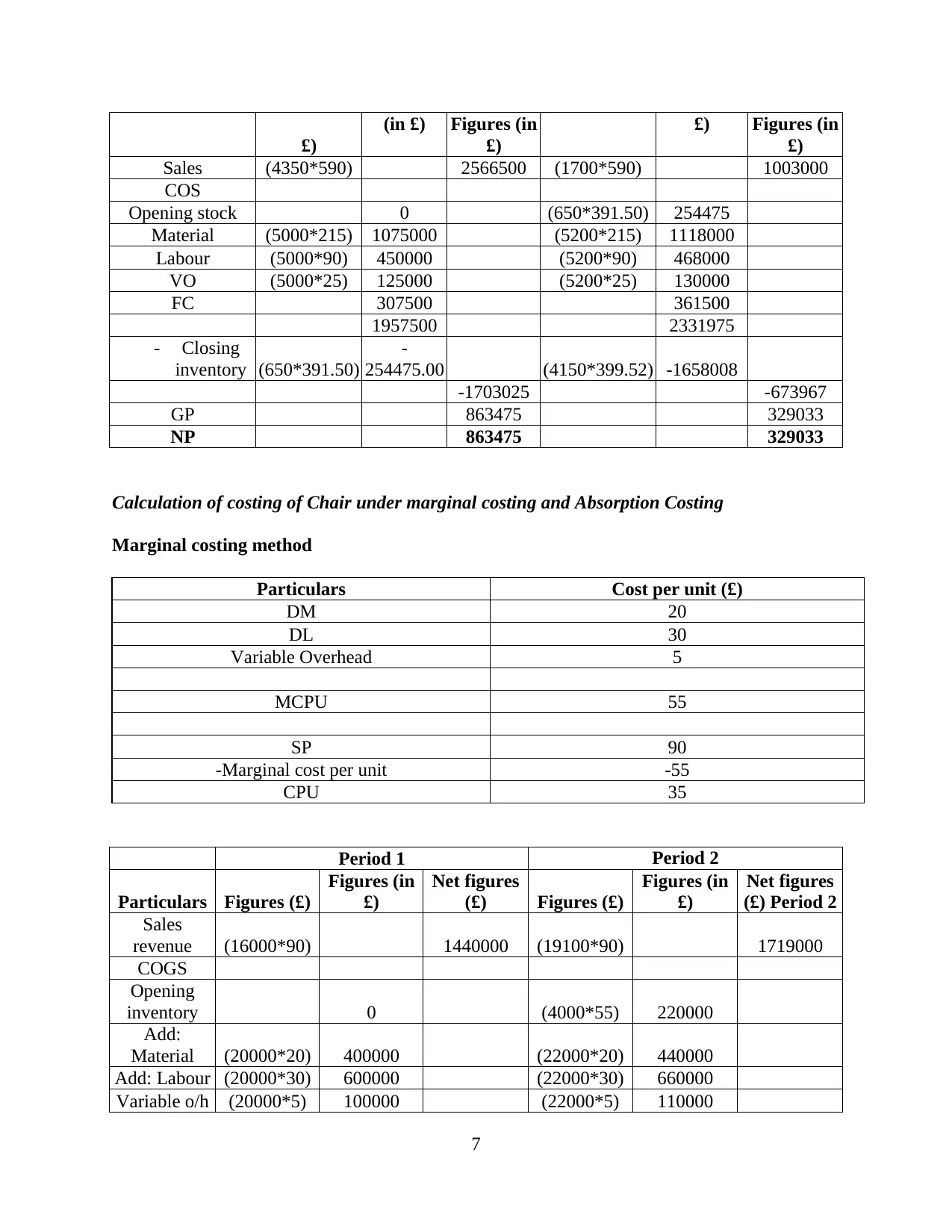

Annexure A

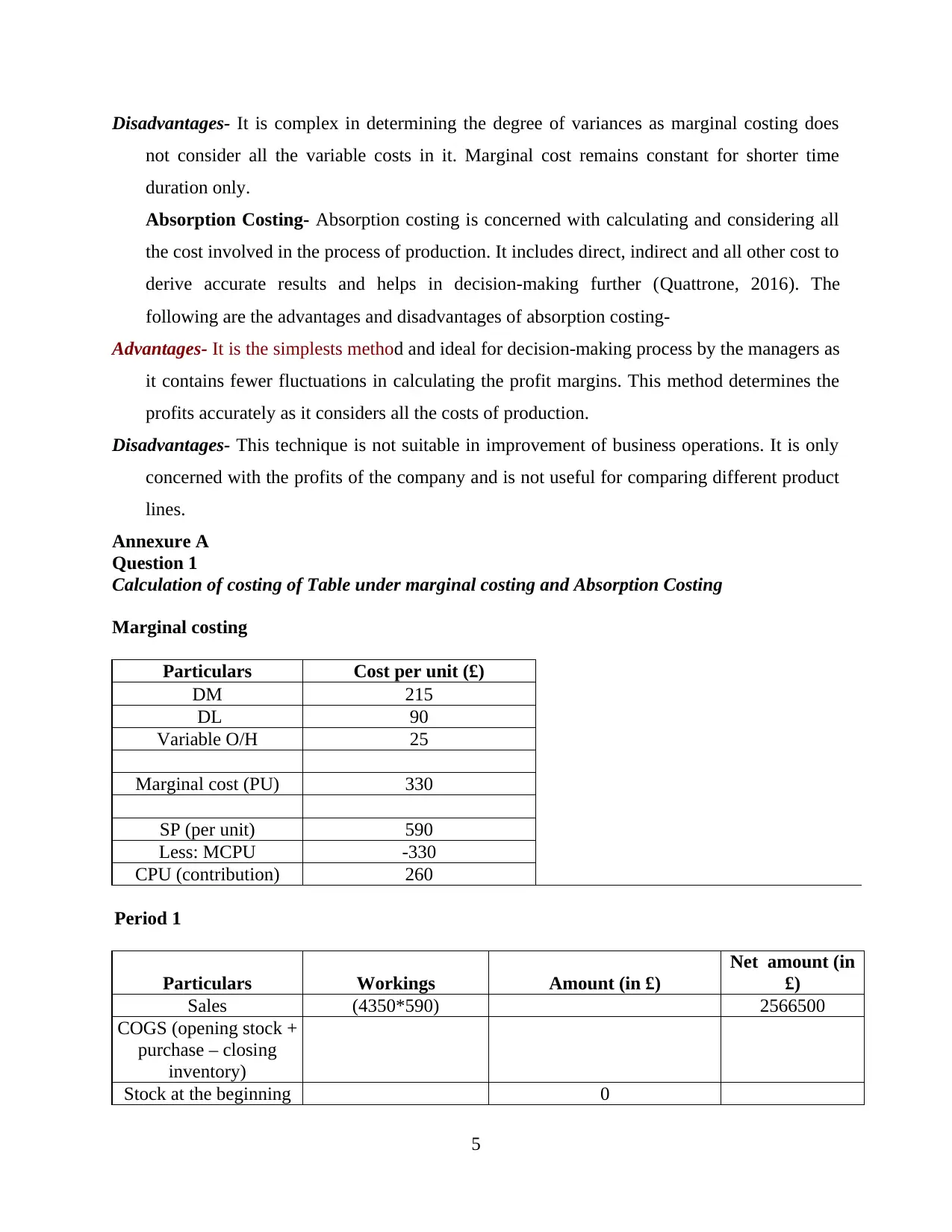

Question 1

Calculation of costing of Table under marginal costing and Absorption Costing

Marginal costing

Particulars Cost per unit (£)

DM 215

DL 90

Variable O/H 25

Marginal cost (PU) 330

SP (per unit) 590

Less: MCPU -330

CPU (contribution) 260

Period 1

Particulars Workings Amount (in £)

Net amount (in

£)

Sales (4350*590) 2566500

COGS (opening stock +

purchase – closing

inventory)

Stock at the beginning 0

5

not consider all the variable costs in it. Marginal cost remains constant for shorter time

duration only.

Absorption Costing- Absorption costing is concerned with calculating and considering all

the cost involved in the process of production. It includes direct, indirect and all other cost to

derive accurate results and helps in decision-making further (Quattrone, 2016). The

following are the advantages and disadvantages of absorption costing-

Advantages- It is the simplests method and ideal for decision-making process by the managers as

it contains fewer fluctuations in calculating the profit margins. This method determines the

profits accurately as it considers all the costs of production.

Disadvantages- This technique is not suitable in improvement of business operations. It is only

concerned with the profits of the company and is not useful for comparing different product

lines.

Annexure A

Question 1

Calculation of costing of Table under marginal costing and Absorption Costing

Marginal costing

Particulars Cost per unit (£)

DM 215

DL 90

Variable O/H 25

Marginal cost (PU) 330

SP (per unit) 590

Less: MCPU -330

CPU (contribution) 260

Period 1

Particulars Workings Amount (in £)

Net amount (in

£)

Sales (4350*590) 2566500

COGS (opening stock +

purchase – closing

inventory)

Stock at the beginning 0

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of period

Material (5000 * 215) 1075000

Labour (5000 * 90) 450000

Variable overhead (5000 * 25) 125000

M 1650000

Less: Closing stock (650*330) -214500

-1435500

1131000

Contribution 1131000

Less: FC -307500

NP 823500

Period 2

Particulars Workings Amount (£) Net amount (in £)

Revenue (1700*590) 1003000

COS

Opening stock (650*330) 214500

DM (5200*215) 1118000

DL (5200*90) 468000

Variable o/h (5200*25) 130000

1930500

- inventory at the end of

period (4150*330) -1369500

-561000

442000

Cont. 442000

Less: FC -361500

NP 80500

Under Absorption Costing

Determining cost per unit

Particulars

Period 1

Amount (in £)

Period 2

Amount (in £)

DM 215 215

DL 90 90

VO 25 25

FO 61.5 69.52

Total absorption cost

per unit 391.5 399.52

Period 1 Period 2

Particulars Figures (in Figures Net Figures (in £) Figures (in Net

6

Material (5000 * 215) 1075000

Labour (5000 * 90) 450000

Variable overhead (5000 * 25) 125000

M 1650000

Less: Closing stock (650*330) -214500

-1435500

1131000

Contribution 1131000

Less: FC -307500

NP 823500

Period 2

Particulars Workings Amount (£) Net amount (in £)

Revenue (1700*590) 1003000

COS

Opening stock (650*330) 214500

DM (5200*215) 1118000

DL (5200*90) 468000

Variable o/h (5200*25) 130000

1930500

- inventory at the end of

period (4150*330) -1369500

-561000

442000

Cont. 442000

Less: FC -361500

NP 80500

Under Absorption Costing

Determining cost per unit

Particulars

Period 1

Amount (in £)

Period 2

Amount (in £)

DM 215 215

DL 90 90

VO 25 25

FO 61.5 69.52

Total absorption cost

per unit 391.5 399.52

Period 1 Period 2

Particulars Figures (in Figures Net Figures (in £) Figures (in Net

6

£)

(in £) Figures (in

£)

£) Figures (in

£)

Sales (4350*590) 2566500 (1700*590) 1003000

COS

Opening stock 0 (650*391.50) 254475

Material (5000*215) 1075000 (5200*215) 1118000

Labour (5000*90) 450000 (5200*90) 468000

VO (5000*25) 125000 (5200*25) 130000

FC 307500 361500

1957500 2331975

- Closing

inventory (650*391.50)

-

254475.00 (4150*399.52) -1658008

-1703025 -673967

GP 863475 329033

NP 863475 329033

Calculation of costing of Chair under marginal costing and Absorption Costing

Marginal costing method

Particulars Cost per unit (£)

DM 20

DL 30

Variable Overhead 5

MCPU 55

SP 90

-Marginal cost per unit -55

CPU 35

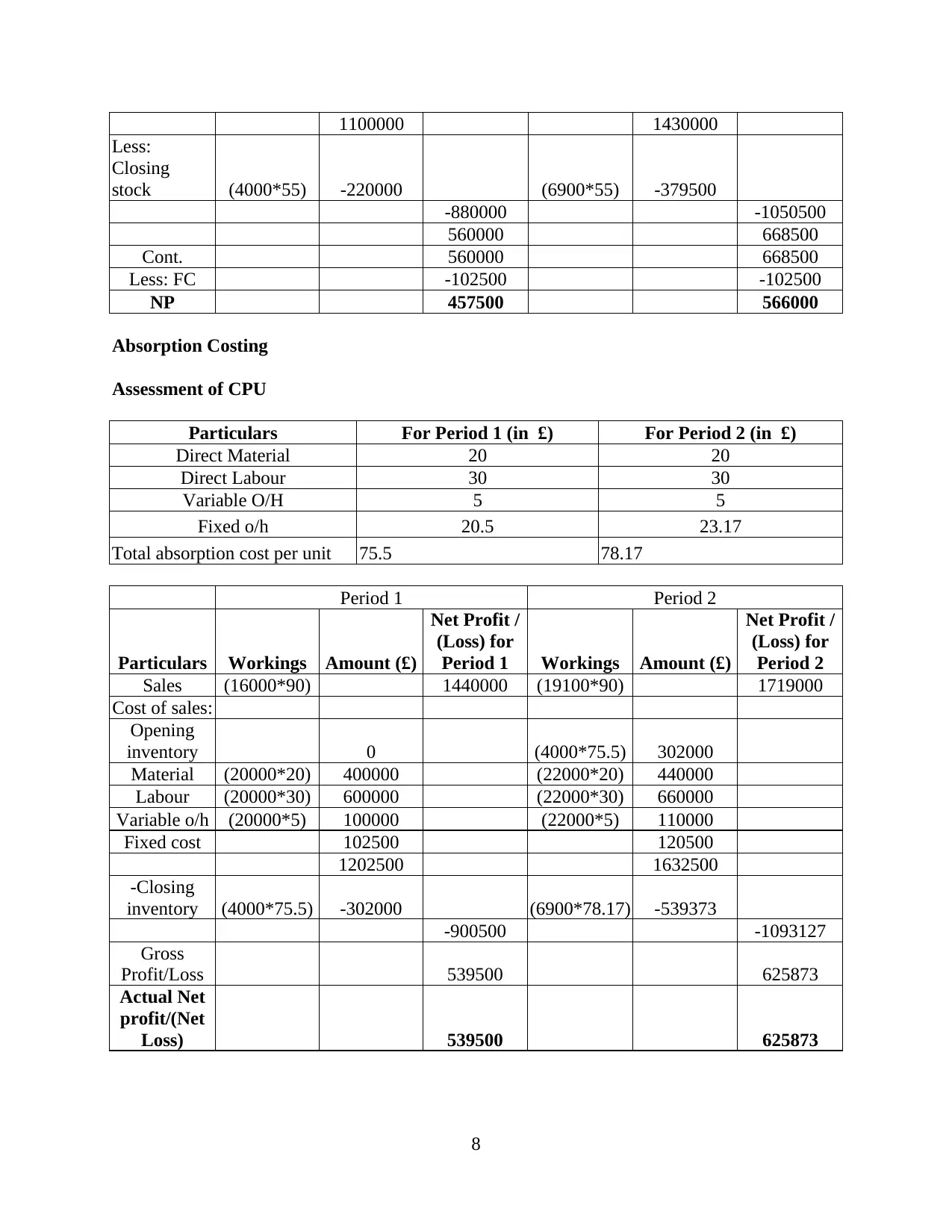

Period 1 Period 2

Particulars Figures (£)

Figures (in

£)

Net figures

(£) Figures (£)

Figures (in

£)

Net figures

(£) Period 2

Sales

revenue (16000*90) 1440000 (19100*90) 1719000

COGS

Opening

inventory 0 (4000*55) 220000

Add:

Material (20000*20) 400000 (22000*20) 440000

Add: Labour (20000*30) 600000 (22000*30) 660000

Variable o/h (20000*5) 100000 (22000*5) 110000

7

(in £) Figures (in

£)

£) Figures (in

£)

Sales (4350*590) 2566500 (1700*590) 1003000

COS

Opening stock 0 (650*391.50) 254475

Material (5000*215) 1075000 (5200*215) 1118000

Labour (5000*90) 450000 (5200*90) 468000

VO (5000*25) 125000 (5200*25) 130000

FC 307500 361500

1957500 2331975

- Closing

inventory (650*391.50)

-

254475.00 (4150*399.52) -1658008

-1703025 -673967

GP 863475 329033

NP 863475 329033

Calculation of costing of Chair under marginal costing and Absorption Costing

Marginal costing method

Particulars Cost per unit (£)

DM 20

DL 30

Variable Overhead 5

MCPU 55

SP 90

-Marginal cost per unit -55

CPU 35

Period 1 Period 2

Particulars Figures (£)

Figures (in

£)

Net figures

(£) Figures (£)

Figures (in

£)

Net figures

(£) Period 2

Sales

revenue (16000*90) 1440000 (19100*90) 1719000

COGS

Opening

inventory 0 (4000*55) 220000

Add:

Material (20000*20) 400000 (22000*20) 440000

Add: Labour (20000*30) 600000 (22000*30) 660000

Variable o/h (20000*5) 100000 (22000*5) 110000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1100000 1430000

Less:

Closing

stock (4000*55) -220000 (6900*55) -379500

-880000 -1050500

560000 668500

Cont. 560000 668500

Less: FC -102500 -102500

NP 457500 566000

Absorption Costing

Assessment of CPU

Particulars For Period 1 (in £) For Period 2 (in £)

Direct Material 20 20

Direct Labour 30 30

Variable O/H 5 5

Fixed o/h 20.5 23.17

Total absorption cost per unit 75.5 78.17

Period 1 Period 2

Particulars Workings Amount (£)

Net Profit /

(Loss) for

Period 1 Workings Amount (£)

Net Profit /

(Loss) for

Period 2

Sales (16000*90) 1440000 (19100*90) 1719000

Cost of sales:

Opening

inventory 0 (4000*75.5) 302000

Material (20000*20) 400000 (22000*20) 440000

Labour (20000*30) 600000 (22000*30) 660000

Variable o/h (20000*5) 100000 (22000*5) 110000

Fixed cost 102500 120500

1202500 1632500

-Closing

inventory (4000*75.5) -302000 (6900*78.17) -539373

-900500 -1093127

Gross

Profit/Loss 539500 625873

Actual Net

profit/(Net

Loss) 539500 625873

8

Less:

Closing

stock (4000*55) -220000 (6900*55) -379500

-880000 -1050500

560000 668500

Cont. 560000 668500

Less: FC -102500 -102500

NP 457500 566000

Absorption Costing

Assessment of CPU

Particulars For Period 1 (in £) For Period 2 (in £)

Direct Material 20 20

Direct Labour 30 30

Variable O/H 5 5

Fixed o/h 20.5 23.17

Total absorption cost per unit 75.5 78.17

Period 1 Period 2

Particulars Workings Amount (£)

Net Profit /

(Loss) for

Period 1 Workings Amount (£)

Net Profit /

(Loss) for

Period 2

Sales (16000*90) 1440000 (19100*90) 1719000

Cost of sales:

Opening

inventory 0 (4000*75.5) 302000

Material (20000*20) 400000 (22000*20) 440000

Labour (20000*30) 600000 (22000*30) 660000

Variable o/h (20000*5) 100000 (22000*5) 110000

Fixed cost 102500 120500

1202500 1632500

-Closing

inventory (4000*75.5) -302000 (6900*78.17) -539373

-900500 -1093127

Gross

Profit/Loss 539500 625873

Actual Net

profit/(Net

Loss) 539500 625873

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

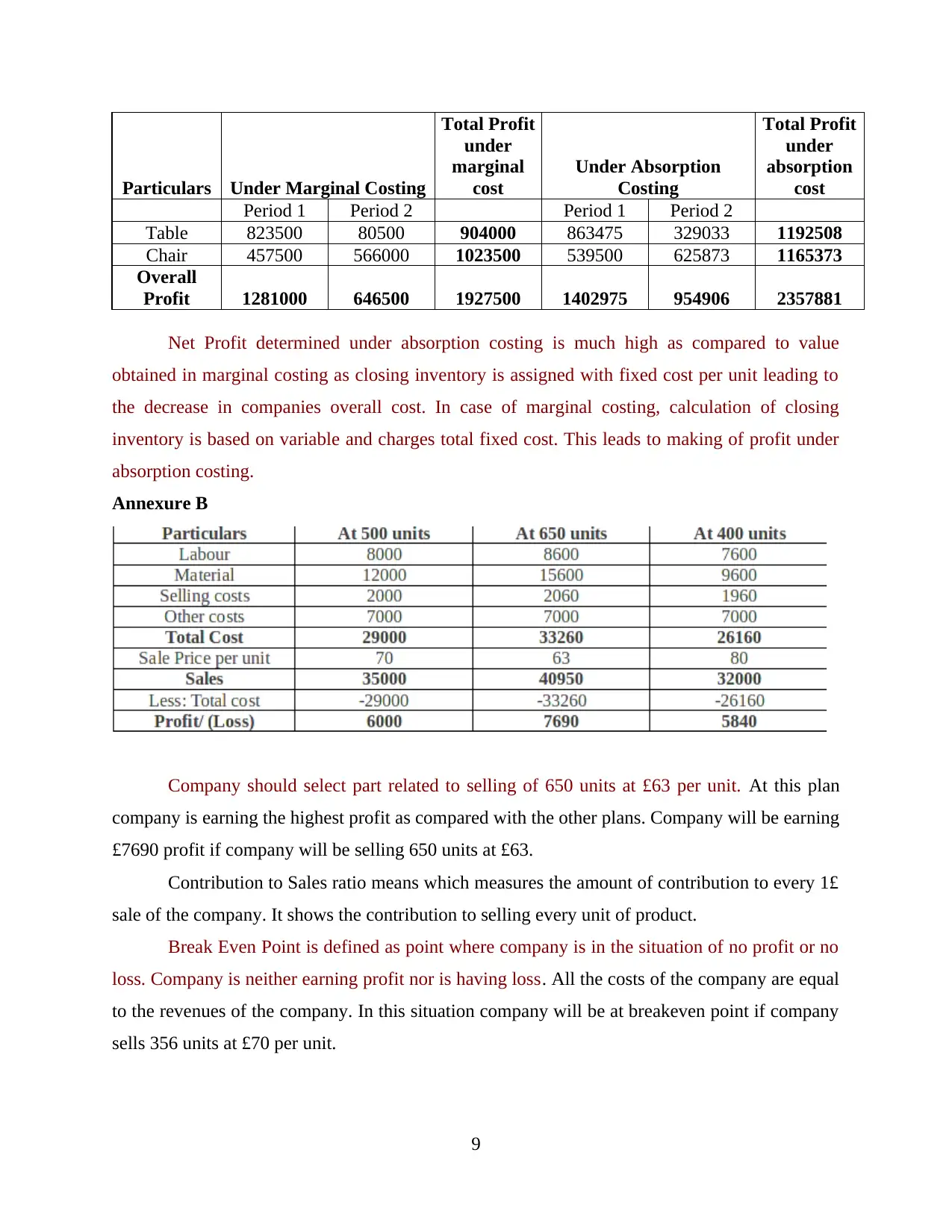

Particulars Under Marginal Costing

Total Profit

under

marginal

cost

Under Absorption

Costing

Total Profit

under

absorption

cost

Period 1 Period 2 Period 1 Period 2

Table 823500 80500 904000 863475 329033 1192508

Chair 457500 566000 1023500 539500 625873 1165373

Overall

Profit 1281000 646500 1927500 1402975 954906 2357881

Net Profit determined under absorption costing is much high as compared to value

obtained in marginal costing as closing inventory is assigned with fixed cost per unit leading to

the decrease in companies overall cost. In case of marginal costing, calculation of closing

inventory is based on variable and charges total fixed cost. This leads to making of profit under

absorption costing.

Annexure B

Company should select part related to selling of 650 units at £63 per unit. At this plan

company is earning the highest profit as compared with the other plans. Company will be earning

£7690 profit if company will be selling 650 units at £63.

Contribution to Sales ratio means which measures the amount of contribution to every 1£

sale of the company. It shows the contribution to selling every unit of product.

Break Even Point is defined as point where company is in the situation of no profit or no

loss. Company is neither earning profit nor is having loss. All the costs of the company are equal

to the revenues of the company. In this situation company will be at breakeven point if company

sells 356 units at £70 per unit.

9

Total Profit

under

marginal

cost

Under Absorption

Costing

Total Profit

under

absorption

cost

Period 1 Period 2 Period 1 Period 2

Table 823500 80500 904000 863475 329033 1192508

Chair 457500 566000 1023500 539500 625873 1165373

Overall

Profit 1281000 646500 1927500 1402975 954906 2357881

Net Profit determined under absorption costing is much high as compared to value

obtained in marginal costing as closing inventory is assigned with fixed cost per unit leading to

the decrease in companies overall cost. In case of marginal costing, calculation of closing

inventory is based on variable and charges total fixed cost. This leads to making of profit under

absorption costing.

Annexure B

Company should select part related to selling of 650 units at £63 per unit. At this plan

company is earning the highest profit as compared with the other plans. Company will be earning

£7690 profit if company will be selling 650 units at £63.

Contribution to Sales ratio means which measures the amount of contribution to every 1£

sale of the company. It shows the contribution to selling every unit of product.

Break Even Point is defined as point where company is in the situation of no profit or no

loss. Company is neither earning profit nor is having loss. All the costs of the company are equal

to the revenues of the company. In this situation company will be at breakeven point if company

sells 356 units at £70 per unit.

9

LO 3

P4 Advantages and disadvantages of different planning tools

Planning tool is mainly used to manage their accounts and improve their performance by

adapting various strategies and method to control the factors which raises to maintain the

sustainability. It assists in making effective decision and formation of sound business plan

various objectives to achieve goal and success in the near future. Thus, major planning tool is

usually implemented by planning the proper budgets (Ax and Greve, 2017). Thus, budgets are

mainly prepared by company to examine their income and expenditure and interprets accurate

flow of income to identify the company structure to expand their business activities into

international market. Following are the types of budget:

1. Cash Flow Budgets: Prepared to examine actual cash incurred by estimating the cash

inflow and outflow from day to day activities. Through the cash flow budget, it helps

company to analyse actual cash balance for determining amount required for the project

for carrying any other activities for long term growth in the market (Cost Accounting

Systems, 2019). The advantages of cash flow budgets are as follows:

If company had surplus cash balance, it can can buy more resources to increase their

stability in the market.

They can easily borrow loan from investors and bank by presenting their stability and

reputation by having the surplus cash.

The disadvantages of Cash flow budgets are as follows:

There are more chances of theft and fraud which can manipulates the interests of

employees by viewing the surplus cash in the company (Chenhall and Moers, 2015).

If the budgets are not properly managed and accountable by the accounts, it results in

chances of loss of the money and also it eliminated the company to pay surplus rewards

to their employees.

Thus in case of Jaguar land Rover Automotive Plc, they use such planning tool to

examine the estimated cash inflow and outflow at the time of dealing in certain activities to gain

more profits. This also helps them to balance their process by analysis their expenses which is to

be incurred in near future and plan the strategies according to such activity.

10

P4 Advantages and disadvantages of different planning tools

Planning tool is mainly used to manage their accounts and improve their performance by

adapting various strategies and method to control the factors which raises to maintain the

sustainability. It assists in making effective decision and formation of sound business plan

various objectives to achieve goal and success in the near future. Thus, major planning tool is

usually implemented by planning the proper budgets (Ax and Greve, 2017). Thus, budgets are

mainly prepared by company to examine their income and expenditure and interprets accurate

flow of income to identify the company structure to expand their business activities into

international market. Following are the types of budget:

1. Cash Flow Budgets: Prepared to examine actual cash incurred by estimating the cash

inflow and outflow from day to day activities. Through the cash flow budget, it helps

company to analyse actual cash balance for determining amount required for the project

for carrying any other activities for long term growth in the market (Cost Accounting

Systems, 2019). The advantages of cash flow budgets are as follows:

If company had surplus cash balance, it can can buy more resources to increase their

stability in the market.

They can easily borrow loan from investors and bank by presenting their stability and

reputation by having the surplus cash.

The disadvantages of Cash flow budgets are as follows:

There are more chances of theft and fraud which can manipulates the interests of

employees by viewing the surplus cash in the company (Chenhall and Moers, 2015).

If the budgets are not properly managed and accountable by the accounts, it results in

chances of loss of the money and also it eliminated the company to pay surplus rewards

to their employees.

Thus in case of Jaguar land Rover Automotive Plc, they use such planning tool to

examine the estimated cash inflow and outflow at the time of dealing in certain activities to gain

more profits. This also helps them to balance their process by analysis their expenses which is to

be incurred in near future and plan the strategies according to such activity.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.