Management Accounting Report: Financial Strength of Jaguar Land Rover

VerifiedAdded on 2023/01/19

|17

|4654

|65

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Jaguar Land Rover. It begins with an executive summary, outlining the assessment of financial strength through accounting tools, and evaluating economic growth via management accounting processes. The report delves into various aspects of management accounting, including the explanation of management accounting, essential requirements of different management accounting systems, and methods used for reporting. It also covers management accounting techniques such as inventory management and job costing systems, alongside the benefits of these systems and their applications. The report further evaluates the integration of management accounting systems and reporting, and explores cost calculations using marginal and absorption costs. It compares and contrasts planning tools, assessing their effectiveness, and examines the adaptation of management accounting systems to address financial problems in different organizations. The report concludes with a detailed reference list supporting the analysis.

Unit 5

MANAGEMENT ACCOUNTING

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report has assessed the financial strength through the tool of accounting present in the

management of Jaguar Land Rover. The growth of economic status has been evaluated through

the management accounting process. The financial condition of Jaguar Land Rover has been

assessed with the help of the accounting tools is provided in the report. Different planning tools

help organisations to achieve an effective strategy for the budgetary plan with estimated

planning. It increases the performance of the company. It also helps in measuring the

performance of the employees to acquire effective growth.

2

The report has assessed the financial strength through the tool of accounting present in the

management of Jaguar Land Rover. The growth of economic status has been evaluated through

the management accounting process. The financial condition of Jaguar Land Rover has been

assessed with the help of the accounting tools is provided in the report. Different planning tools

help organisations to achieve an effective strategy for the budgetary plan with estimated

planning. It increases the performance of the company. It also helps in measuring the

performance of the employees to acquire effective growth.

2

Table of Contents

Introduction........................................................................................................................4

Activity 1............................................................................................................................4

Part A..............................................................................................................................4

Explanation of Management Accounting (P1)............................................................4

Essential requirements of different types of management accounting systems (P1) 4

Explanation of the different methods used for management accounting reporting

(P2).............................................................................................................................5

Management Accounting Techniques............................................................................6

Benefits of management accounting systems and their application (M1)..................6

Critical evaluation of the integration of management accounting systems and

management accounting reporting (D1).....................................................................7

Part B..............................................................................................................................7

Calculating the costs using appropriate techniques of cost analysis for preparing an

income statement using marginal and absorption costs (P3, M2, D2).......................8

Activity 2..........................................................................................................................12

Part A............................................................................................................................12

Compare and contrast three planning tools used in management accounting,

indicating how effective (P4, M3, D3)..........................................................................12

Planning tools ..............................................................................................................12

Part B............................................................................................................................14

Comparison of adapting management accounting systems to respond to financial

problems in different organisations (P5)...................................................................14

Conclusion.......................................................................................................................16

Reference List .................................................................................................................17

3

Introduction........................................................................................................................4

Activity 1............................................................................................................................4

Part A..............................................................................................................................4

Explanation of Management Accounting (P1)............................................................4

Essential requirements of different types of management accounting systems (P1) 4

Explanation of the different methods used for management accounting reporting

(P2).............................................................................................................................5

Management Accounting Techniques............................................................................6

Benefits of management accounting systems and their application (M1)..................6

Critical evaluation of the integration of management accounting systems and

management accounting reporting (D1).....................................................................7

Part B..............................................................................................................................7

Calculating the costs using appropriate techniques of cost analysis for preparing an

income statement using marginal and absorption costs (P3, M2, D2).......................8

Activity 2..........................................................................................................................12

Part A............................................................................................................................12

Compare and contrast three planning tools used in management accounting,

indicating how effective (P4, M3, D3)..........................................................................12

Planning tools ..............................................................................................................12

Part B............................................................................................................................14

Comparison of adapting management accounting systems to respond to financial

problems in different organisations (P5)...................................................................14

Conclusion.......................................................................................................................16

Reference List .................................................................................................................17

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The report has provided an analysis of the management accounting for Jaguar Land Rover to

assess their financial strength. Management Accounting has been one of the management

analytical tools for any organisations for increasing the growth in monetary status. It provides

the role of the management and technique for analysing the financial condition of the company.

The report has reflected the benefits of using management accounting along with the process of

implementation for the company. It provides a way to eliminate the financial problem from the

company effectively.

Activity 1

Part A

Explanation of Management Accounting (P1)

The advancement of technology has manifested a continuous change in the accounting system as

well as other aspects of life. The methods of creating a report of management through analysing

the accounts of any companies accurately with the period can be termed as the management

accounting. It provides statistical information which has been required by the managers for

evaluating the short-term and long-term decision. It provides both financial accounting reports

that analyse the external stakeholders; however, it has reflected a weekly summary of the

organisation's internal stakeholders. The report generally shows the current financial status of

any companies such as cash, sales revenue, debts and other inventory. As suggested by Messner

(2016), the concept of management accounting has accepted as tools of the manager to assess the

company’s financial report to understand the current state it and creating an easy way for

decision-making process. In order to sustainability in the market, companies have been shifting

from the traditional accounting system to the modern management accounting system. It

provides the information of both internal and external stakeholders to forecast the organisation's

inventory management for the value position of it in the market. The tool helps in tracking the

status of the stakeholders for identifying most efficient of them for the betterment of the

organisations.

Jaguar Land Rover has implemented the management accounting system which has been

controlled by Joshua Lee. He possesses the skill of management accounting form the CIMA

(Chartered Institute of Management Accountants). The management accounting has helped the

company to assess the current matrix and value position in the market. The accounting tools

have helped to assess both financial data and non-financial data for the present and future

prospects of the business. It has often contributed to identify the risk prevails in the organisation

and mitigate through quick decision and planning of operational development. It analyses the

cost and periodic cost along with constraints analysis for the organisation.

Essential requirements of different types of management accounting systems (P1)

The main purpose of the management accounting system is to provide relevant data to the

managerial department for creating a suitable decision-making process. As suggested by

Schaltegger and Burritt (2017), there have been various parameters which should be measured

4

The report has provided an analysis of the management accounting for Jaguar Land Rover to

assess their financial strength. Management Accounting has been one of the management

analytical tools for any organisations for increasing the growth in monetary status. It provides

the role of the management and technique for analysing the financial condition of the company.

The report has reflected the benefits of using management accounting along with the process of

implementation for the company. It provides a way to eliminate the financial problem from the

company effectively.

Activity 1

Part A

Explanation of Management Accounting (P1)

The advancement of technology has manifested a continuous change in the accounting system as

well as other aspects of life. The methods of creating a report of management through analysing

the accounts of any companies accurately with the period can be termed as the management

accounting. It provides statistical information which has been required by the managers for

evaluating the short-term and long-term decision. It provides both financial accounting reports

that analyse the external stakeholders; however, it has reflected a weekly summary of the

organisation's internal stakeholders. The report generally shows the current financial status of

any companies such as cash, sales revenue, debts and other inventory. As suggested by Messner

(2016), the concept of management accounting has accepted as tools of the manager to assess the

company’s financial report to understand the current state it and creating an easy way for

decision-making process. In order to sustainability in the market, companies have been shifting

from the traditional accounting system to the modern management accounting system. It

provides the information of both internal and external stakeholders to forecast the organisation's

inventory management for the value position of it in the market. The tool helps in tracking the

status of the stakeholders for identifying most efficient of them for the betterment of the

organisations.

Jaguar Land Rover has implemented the management accounting system which has been

controlled by Joshua Lee. He possesses the skill of management accounting form the CIMA

(Chartered Institute of Management Accountants). The management accounting has helped the

company to assess the current matrix and value position in the market. The accounting tools

have helped to assess both financial data and non-financial data for the present and future

prospects of the business. It has often contributed to identify the risk prevails in the organisation

and mitigate through quick decision and planning of operational development. It analyses the

cost and periodic cost along with constraints analysis for the organisation.

Essential requirements of different types of management accounting systems (P1)

The main purpose of the management accounting system is to provide relevant data to the

managerial department for creating a suitable decision-making process. As suggested by

Schaltegger and Burritt (2017), there have been various parameters which should be measured

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

by the managerial department to prepare a report for the decision-making process. The essential

requirement has included the following parameters which should be assessed by Jaguar Land

Rover:

Organisation Structure: The organisational structure plays an important role in the company to

implement effective managerial accounting. The functional structure has helped the company to

acquire better management for it and increasing value position.

Management Style: The management style followed by Jaguar Land Rover is democratic, which

provides every employee with an equal chance to be part of the managerial decision. It helps the

company to assess most effective management accounting process. However, it should try to

improve the style and accumulate more employees for achieving the goal.

Reliability of the data: The security of data has been analysed in the management system to

acquire better information regarding the company. Moreover, it has been identified that Jaguar

Land Rover assesses the source of the data to analyse its reliability. In a further instance, the data

has been protected for securing the internal matter of the management.

Cost Systems: In order to identify the importance of the accounting system regarding its

application, the analysis of the cost has been essential. As suggested by Nitzl (2016), it would

provide better management system for the company. However, the cost analysis has been

performed by the company to understand the area for improvement in their accounting system.

Explanation of the different methods used for management accounting reporting (P2)

Methods of management accounting have been a central system which enables the management

for acquiring better decision by uses of private information. Different types of techniques used

for the reporting purpose has been provided as follows.

Budget report: This report has reflected the actual performance of the company and the

estimated performance. It provides the standards of the performance which has been focusing on

the revenues and expenditures of the company. According to Cooper et al. (2017), it helps in

scrutinizing the operation of the organisations to analyse the default in their management. Jaguar

Land Rover has been helped by the budget report to assess effective result for their performance.

Graphical report: This report provides the use of graphical tools to assess the current status of

the company. It has been analysed the internal performance of the company. Scatter graph, line

graph and pie charts are the tools for creating graphical report in the management accounting.

Accounts Report: This report has provided information about the company's client base along

with the amount of collection. It contains amounts which help in identifying the barriers in

accounting management.

Inventory report: Use of inventory report has provided Jaguar Land Rover to assess the stock of

inventories. As suggested by Johnstone (2018), it has also provides the labour cost, overhead

cost and material cost. The management of the company possesses information about the metrics

and provides an assessment of the current status of the company.

5

requirement has included the following parameters which should be assessed by Jaguar Land

Rover:

Organisation Structure: The organisational structure plays an important role in the company to

implement effective managerial accounting. The functional structure has helped the company to

acquire better management for it and increasing value position.

Management Style: The management style followed by Jaguar Land Rover is democratic, which

provides every employee with an equal chance to be part of the managerial decision. It helps the

company to assess most effective management accounting process. However, it should try to

improve the style and accumulate more employees for achieving the goal.

Reliability of the data: The security of data has been analysed in the management system to

acquire better information regarding the company. Moreover, it has been identified that Jaguar

Land Rover assesses the source of the data to analyse its reliability. In a further instance, the data

has been protected for securing the internal matter of the management.

Cost Systems: In order to identify the importance of the accounting system regarding its

application, the analysis of the cost has been essential. As suggested by Nitzl (2016), it would

provide better management system for the company. However, the cost analysis has been

performed by the company to understand the area for improvement in their accounting system.

Explanation of the different methods used for management accounting reporting (P2)

Methods of management accounting have been a central system which enables the management

for acquiring better decision by uses of private information. Different types of techniques used

for the reporting purpose has been provided as follows.

Budget report: This report has reflected the actual performance of the company and the

estimated performance. It provides the standards of the performance which has been focusing on

the revenues and expenditures of the company. According to Cooper et al. (2017), it helps in

scrutinizing the operation of the organisations to analyse the default in their management. Jaguar

Land Rover has been helped by the budget report to assess effective result for their performance.

Graphical report: This report provides the use of graphical tools to assess the current status of

the company. It has been analysed the internal performance of the company. Scatter graph, line

graph and pie charts are the tools for creating graphical report in the management accounting.

Accounts Report: This report has provided information about the company's client base along

with the amount of collection. It contains amounts which help in identifying the barriers in

accounting management.

Inventory report: Use of inventory report has provided Jaguar Land Rover to assess the stock of

inventories. As suggested by Johnstone (2018), it has also provides the labour cost, overhead

cost and material cost. The management of the company possesses information about the metrics

and provides an assessment of the current status of the company.

5

Income Statements: The income statement format has separated the fixed and variable cost from

each other. The separation has helped the management to overview the expense of volume. It has

been necessary for gaining inventory cost-effectively. Jaguar Land Rover has been helped by

these methods as it provides a suitable decision for increasing the stock and inventory of it.

Cost report: Companies such as Jaguar Land Rover deals with the various project in one time.

As suggested by Kihn and Ihantola (2015), the revenue collected by the company should be

recorded in a report structure which can gather crucial information for the company.

Management Accounting has been helped by the cost report to provide vital information for the

company.

Management Accounting Techniques

Inventory management system : It makes use of software for managing the inventory

level, to order inventory, raw material etc. It is required by the Jaguar Land Rover to manage

their order quantity so as to meet demand in the market. By managing the inventory level it will

reduce the maintenance cost of the inventory and will help the organization to take the decision

regarding the order level and order the quantity which they require.

Job costing system : In job costing report task is divided in different job and each job is

evaluate on the basis of its importance to the organization. It tracks financial effectiveness and

efficiency of Jaguar Land Rover to focus on those activities as required to be improved. It helps

the organization to focus on the activities which generate higher profit rather than wasting time

on unproductive one.

Price optimisation system : An effective reporting method used to ascertain the price of

product and services. It helps them to meet their goal and objective by increasing their profit and

revenue of the company. Jaguar Land Rover require the price optimization system so as to

measure the price of each activity to accomplish the project of providing scientific tool to the

customer.

Cost accounting system : Record and track production activity by using perpetual

inventory system. Makes estimation of cost of product help to prepare the budget which evaluate

the performance of the company by comparing its performance to the previous month

performance. It includes the various costing method such as job order costing, process costing,

traditional costing, activity based costing etc. Process costing is used to estimate the

manufacturing cost of process separately, so they can evaluate the cost required by each process

and control the process separately. It also helps the company to manage time and cost by

focusing on the individual process rather than to whole process.

Benefits of management accounting systems and their application (M1)

In the present era, management accounting has been the internal part of organisations. It

helps the organisation in various ways to assess their growth in the market. Some of the major

benefits have been provided below.

Maximisation of the profit: The tools deal with the cost analysis for an organisation. It provides

most cost-effective strategy for Jaguar Land Rover which provides maximisation of profits and

6

each other. The separation has helped the management to overview the expense of volume. It has

been necessary for gaining inventory cost-effectively. Jaguar Land Rover has been helped by

these methods as it provides a suitable decision for increasing the stock and inventory of it.

Cost report: Companies such as Jaguar Land Rover deals with the various project in one time.

As suggested by Kihn and Ihantola (2015), the revenue collected by the company should be

recorded in a report structure which can gather crucial information for the company.

Management Accounting has been helped by the cost report to provide vital information for the

company.

Management Accounting Techniques

Inventory management system : It makes use of software for managing the inventory

level, to order inventory, raw material etc. It is required by the Jaguar Land Rover to manage

their order quantity so as to meet demand in the market. By managing the inventory level it will

reduce the maintenance cost of the inventory and will help the organization to take the decision

regarding the order level and order the quantity which they require.

Job costing system : In job costing report task is divided in different job and each job is

evaluate on the basis of its importance to the organization. It tracks financial effectiveness and

efficiency of Jaguar Land Rover to focus on those activities as required to be improved. It helps

the organization to focus on the activities which generate higher profit rather than wasting time

on unproductive one.

Price optimisation system : An effective reporting method used to ascertain the price of

product and services. It helps them to meet their goal and objective by increasing their profit and

revenue of the company. Jaguar Land Rover require the price optimization system so as to

measure the price of each activity to accomplish the project of providing scientific tool to the

customer.

Cost accounting system : Record and track production activity by using perpetual

inventory system. Makes estimation of cost of product help to prepare the budget which evaluate

the performance of the company by comparing its performance to the previous month

performance. It includes the various costing method such as job order costing, process costing,

traditional costing, activity based costing etc. Process costing is used to estimate the

manufacturing cost of process separately, so they can evaluate the cost required by each process

and control the process separately. It also helps the company to manage time and cost by

focusing on the individual process rather than to whole process.

Benefits of management accounting systems and their application (M1)

In the present era, management accounting has been the internal part of organisations. It

helps the organisation in various ways to assess their growth in the market. Some of the major

benefits have been provided below.

Maximisation of the profit: The tools deal with the cost analysis for an organisation. It provides

most cost-effective strategy for Jaguar Land Rover which provides maximisation of profits and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increases the revenue eventually. It helps in mitigating low-cost strategy with higher income to

gain higher benefit.

Communication and coordination: It mitigates communication process among the management

and employees of Jaguar Land Rover to achieve the goal of the organisation. According to Wang

et al. (2019), it provides better coordination and team collaboration among the employees.

Responsibility: Management accounting tools provides the managerial department knowledge

about their responsibility and distributes the task among the management of Jaguar Land Rover.

This increases the ability of the company for managing cost, revenue and profit.

Capabilities: The tools help in assessing the skills of the organisation which provides

opportunities for the managerial department to procure the most fruitful way to achieve their

growth and advantages in the market.

Progression in business: Management Accounting has provided Jaguar Land Rover to create

continues production which progressively leads the company. It also provides the estimation of

the production cost of the next year or future. As suggested by Maskell et al. (2017), this would

provide an effective strategy for the organisation to gain a competitive advantage in the market.

Critical evaluation of the integration of management accounting systems and management

accounting reporting (D1)

Management accounting has been one of the analytical processes which provide accurate

information for Jaguar Land Rover. It helps in assessing effective decision-making process and

risk management process that increases the capabilities and profit margin of Jaguar Land Rover.

On the other hand, it has been analysed that the operational process of the organisation has been

compared with action of finance. It procures the prediction of the production and result for the

betterment of the organisations. According to Appelbaum et al. (2017), it has mitigated an

effective method for the employees of Jaguar Land Rover to motivate for a better output. It

defines the performance of the organisation along with the way for enhancement.

The management accounting practice aims to improve the decision-making process for various

organisations. The process helps the management of Jaguar Land Rover to assess a suitable

method for decision-making. As suggested by Laudon and Laudon (2016), it provides direct

focus on the relevant areas which enables to achieve appropriate decision. However, the

application and function of the management accounting system have moved effectively. In

recent times, the process has been implemented in various organisations. On the other hand, the

process has been complicated and requires expertise in multiple fields. Moreover, it provides an

increment in the cost of labour for an organisation which creates problem for Jaguar Land Rover

to implement it in effective ways. Furthermore, it provides limited options for the management

system for the organisation. Therefore, implementation of the management accounting might not

be fruitful. On the contrary, the company acquire diverse expertise which has helped to achieve

efficient strategy for management accounting for the organisation.

Part B

7

gain higher benefit.

Communication and coordination: It mitigates communication process among the management

and employees of Jaguar Land Rover to achieve the goal of the organisation. According to Wang

et al. (2019), it provides better coordination and team collaboration among the employees.

Responsibility: Management accounting tools provides the managerial department knowledge

about their responsibility and distributes the task among the management of Jaguar Land Rover.

This increases the ability of the company for managing cost, revenue and profit.

Capabilities: The tools help in assessing the skills of the organisation which provides

opportunities for the managerial department to procure the most fruitful way to achieve their

growth and advantages in the market.

Progression in business: Management Accounting has provided Jaguar Land Rover to create

continues production which progressively leads the company. It also provides the estimation of

the production cost of the next year or future. As suggested by Maskell et al. (2017), this would

provide an effective strategy for the organisation to gain a competitive advantage in the market.

Critical evaluation of the integration of management accounting systems and management

accounting reporting (D1)

Management accounting has been one of the analytical processes which provide accurate

information for Jaguar Land Rover. It helps in assessing effective decision-making process and

risk management process that increases the capabilities and profit margin of Jaguar Land Rover.

On the other hand, it has been analysed that the operational process of the organisation has been

compared with action of finance. It procures the prediction of the production and result for the

betterment of the organisations. According to Appelbaum et al. (2017), it has mitigated an

effective method for the employees of Jaguar Land Rover to motivate for a better output. It

defines the performance of the organisation along with the way for enhancement.

The management accounting practice aims to improve the decision-making process for various

organisations. The process helps the management of Jaguar Land Rover to assess a suitable

method for decision-making. As suggested by Laudon and Laudon (2016), it provides direct

focus on the relevant areas which enables to achieve appropriate decision. However, the

application and function of the management accounting system have moved effectively. In

recent times, the process has been implemented in various organisations. On the other hand, the

process has been complicated and requires expertise in multiple fields. Moreover, it provides an

increment in the cost of labour for an organisation which creates problem for Jaguar Land Rover

to implement it in effective ways. Furthermore, it provides limited options for the management

system for the organisation. Therefore, implementation of the management accounting might not

be fruitful. On the contrary, the company acquire diverse expertise which has helped to achieve

efficient strategy for management accounting for the organisation.

Part B

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

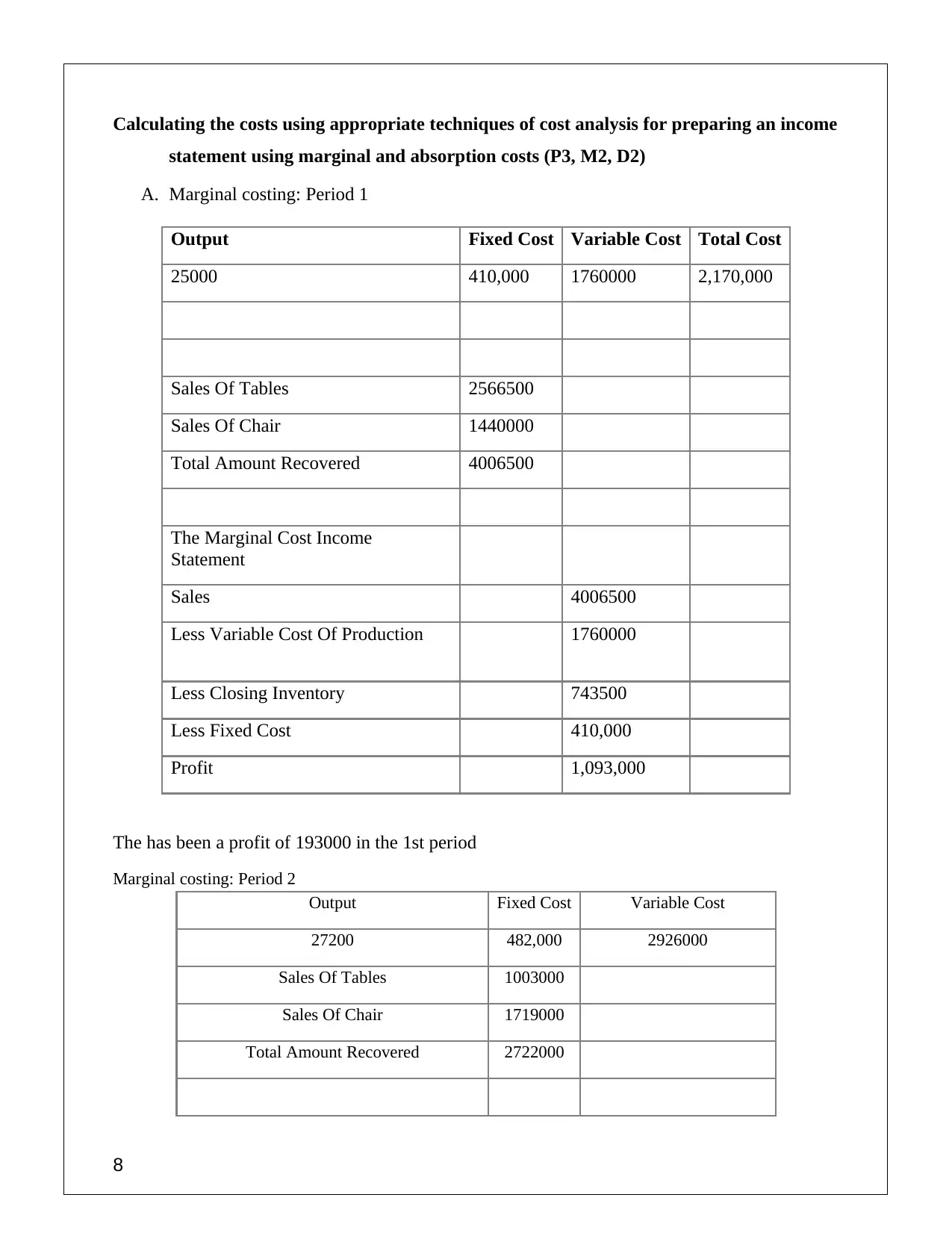

Calculating the costs using appropriate techniques of cost analysis for preparing an income

statement using marginal and absorption costs (P3, M2, D2)

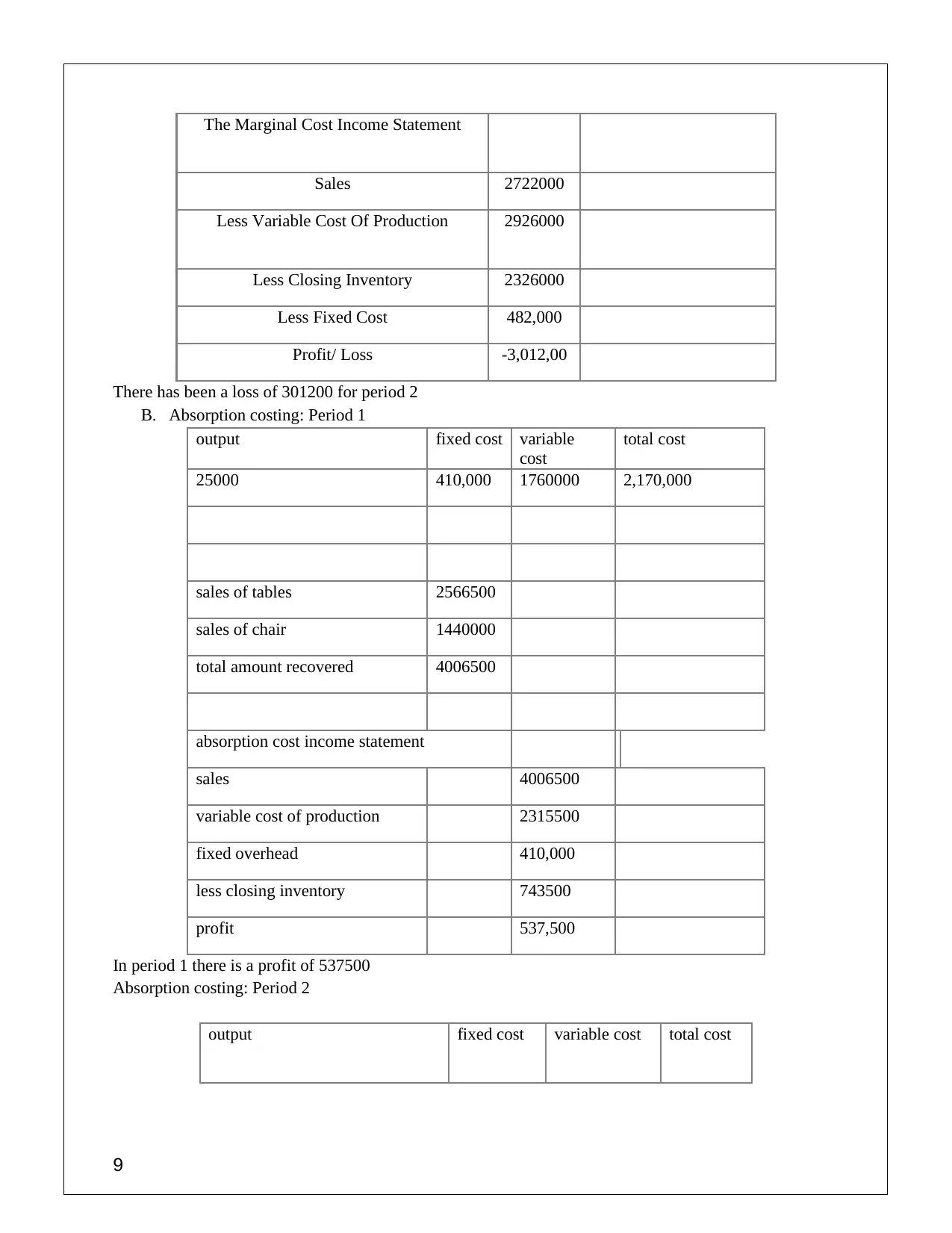

A. Marginal costing: Period 1

Output Fixed Cost Variable Cost Total Cost

25000 410,000 1760000 2,170,000

Sales Of Tables 2566500

Sales Of Chair 1440000

Total Amount Recovered 4006500

The Marginal Cost Income

Statement

Sales 4006500

Less Variable Cost Of Production 1760000

Less Closing Inventory 743500

Less Fixed Cost 410,000

Profit 1,093,000

The has been a profit of 193000 in the 1st period

Marginal costing: Period 2

Output Fixed Cost Variable Cost

27200 482,000 2926000

Sales Of Tables 1003000

Sales Of Chair 1719000

Total Amount Recovered 2722000

8

statement using marginal and absorption costs (P3, M2, D2)

A. Marginal costing: Period 1

Output Fixed Cost Variable Cost Total Cost

25000 410,000 1760000 2,170,000

Sales Of Tables 2566500

Sales Of Chair 1440000

Total Amount Recovered 4006500

The Marginal Cost Income

Statement

Sales 4006500

Less Variable Cost Of Production 1760000

Less Closing Inventory 743500

Less Fixed Cost 410,000

Profit 1,093,000

The has been a profit of 193000 in the 1st period

Marginal costing: Period 2

Output Fixed Cost Variable Cost

27200 482,000 2926000

Sales Of Tables 1003000

Sales Of Chair 1719000

Total Amount Recovered 2722000

8

The Marginal Cost Income Statement

Sales 2722000

Less Variable Cost Of Production 2926000

Less Closing Inventory 2326000

Less Fixed Cost 482,000

Profit/ Loss -3,012,00

There has been a loss of 301200 for period 2

B. Absorption costing: Period 1

output fixed cost variable

cost

total cost

25000 410,000 1760000 2,170,000

sales of tables 2566500

sales of chair 1440000

total amount recovered 4006500

absorption cost income statement

sales 4006500

variable cost of production 2315500

fixed overhead 410,000

less closing inventory 743500

profit 537,500

In period 1 there is a profit of 537500

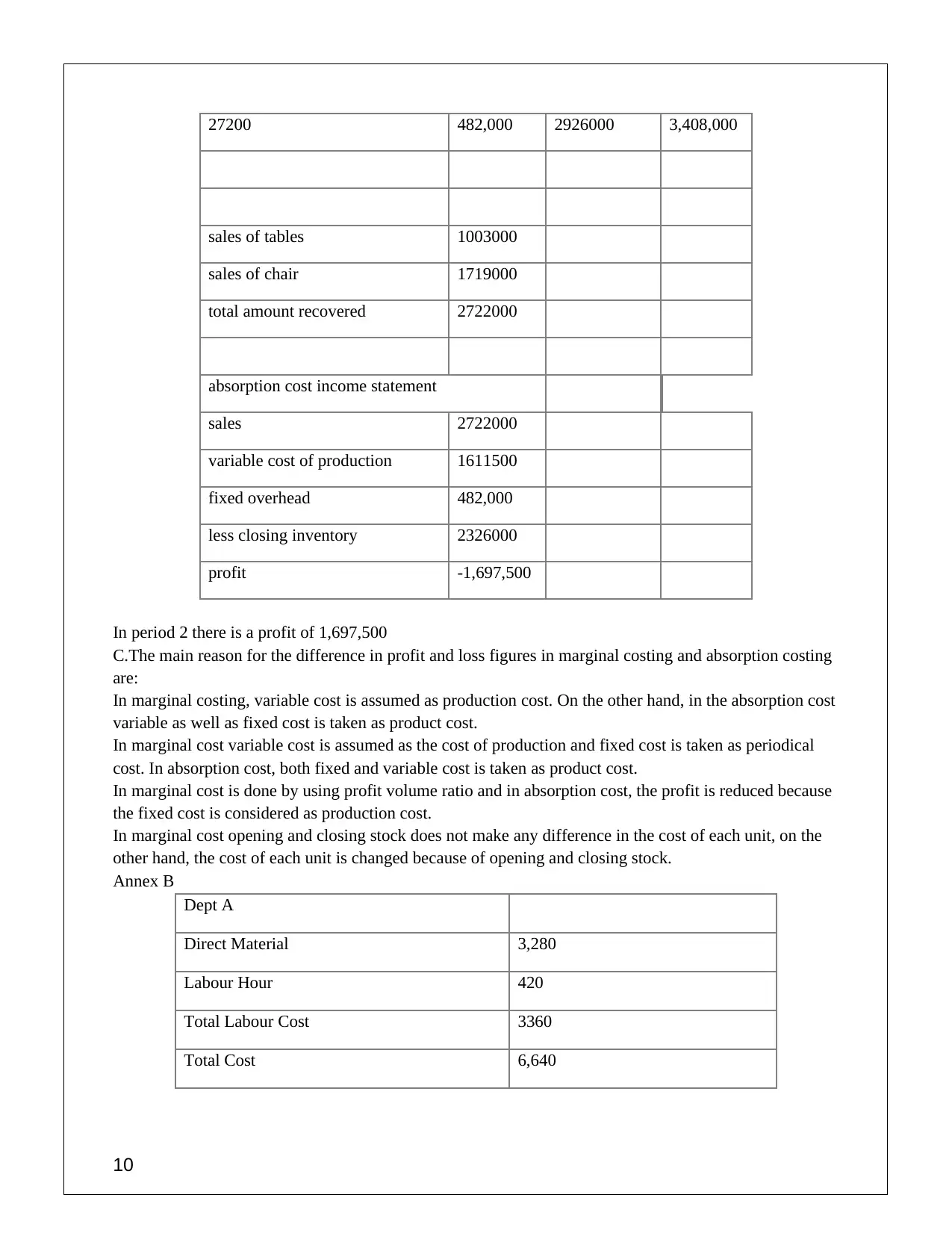

Absorption costing: Period 2

output fixed cost variable cost total cost

9

Sales 2722000

Less Variable Cost Of Production 2926000

Less Closing Inventory 2326000

Less Fixed Cost 482,000

Profit/ Loss -3,012,00

There has been a loss of 301200 for period 2

B. Absorption costing: Period 1

output fixed cost variable

cost

total cost

25000 410,000 1760000 2,170,000

sales of tables 2566500

sales of chair 1440000

total amount recovered 4006500

absorption cost income statement

sales 4006500

variable cost of production 2315500

fixed overhead 410,000

less closing inventory 743500

profit 537,500

In period 1 there is a profit of 537500

Absorption costing: Period 2

output fixed cost variable cost total cost

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

27200 482,000 2926000 3,408,000

sales of tables 1003000

sales of chair 1719000

total amount recovered 2722000

absorption cost income statement

sales 2722000

variable cost of production 1611500

fixed overhead 482,000

less closing inventory 2326000

profit -1,697,500

In period 2 there is a profit of 1,697,500

C.The main reason for the difference in profit and loss figures in marginal costing and absorption costing

are:

In marginal costing, variable cost is assumed as production cost. On the other hand, in the absorption cost

variable as well as fixed cost is taken as product cost.

In marginal cost variable cost is assumed as the cost of production and fixed cost is taken as periodical

cost. In absorption cost, both fixed and variable cost is taken as product cost.

In marginal cost is done by using profit volume ratio and in absorption cost, the profit is reduced because

the fixed cost is considered as production cost.

In marginal cost opening and closing stock does not make any difference in the cost of each unit, on the

other hand, the cost of each unit is changed because of opening and closing stock.

Annex B

Dept A

Direct Material 3,280

Labour Hour 420

Total Labour Cost 3360

Total Cost 6,640

10

sales of tables 1003000

sales of chair 1719000

total amount recovered 2722000

absorption cost income statement

sales 2722000

variable cost of production 1611500

fixed overhead 482,000

less closing inventory 2326000

profit -1,697,500

In period 2 there is a profit of 1,697,500

C.The main reason for the difference in profit and loss figures in marginal costing and absorption costing

are:

In marginal costing, variable cost is assumed as production cost. On the other hand, in the absorption cost

variable as well as fixed cost is taken as product cost.

In marginal cost variable cost is assumed as the cost of production and fixed cost is taken as periodical

cost. In absorption cost, both fixed and variable cost is taken as product cost.

In marginal cost is done by using profit volume ratio and in absorption cost, the profit is reduced because

the fixed cost is considered as production cost.

In marginal cost opening and closing stock does not make any difference in the cost of each unit, on the

other hand, the cost of each unit is changed because of opening and closing stock.

Annex B

Dept A

Direct Material 3,280

Labour Hour 420

Total Labour Cost 3360

Total Cost 6,640

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

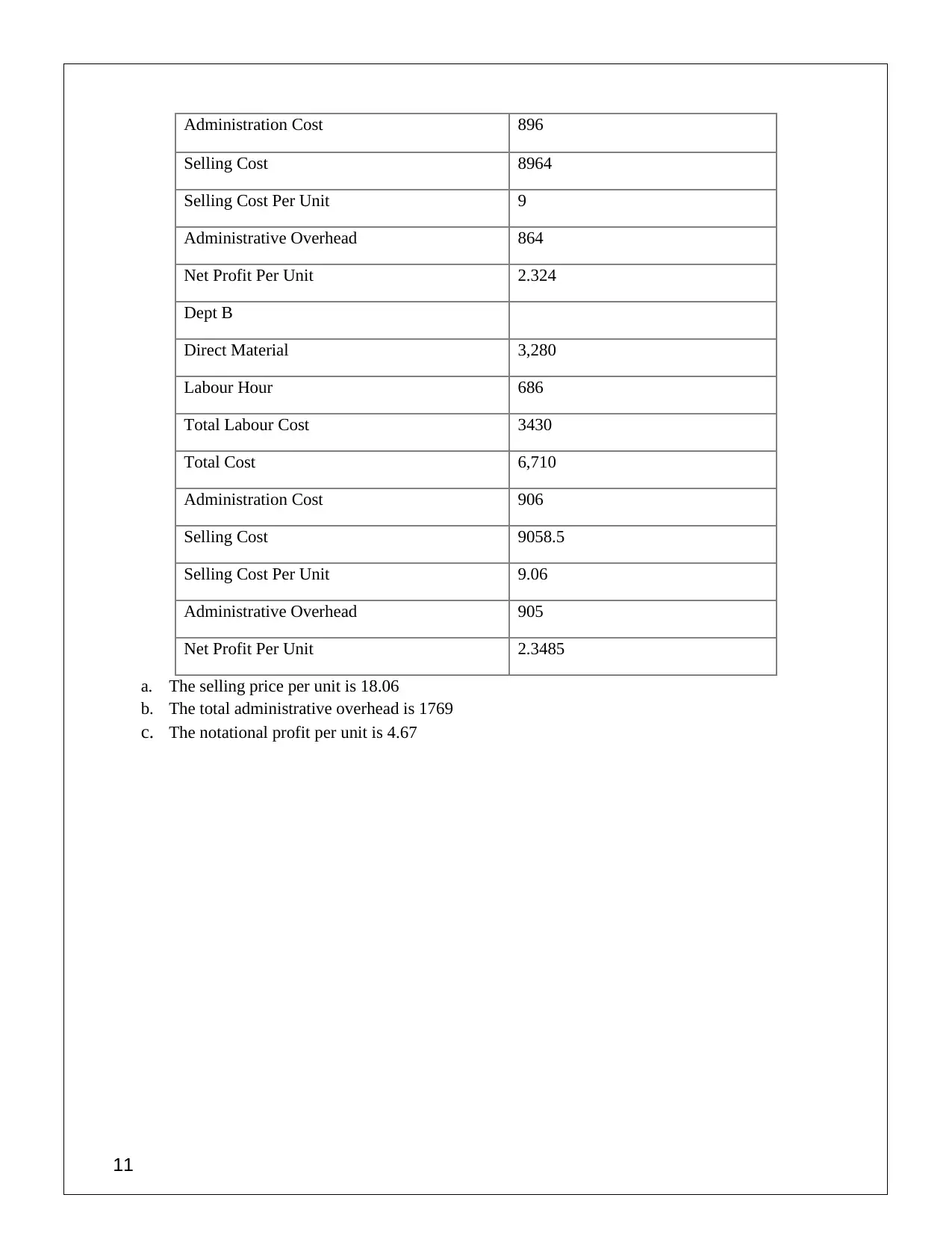

Administration Cost 896

Selling Cost 8964

Selling Cost Per Unit 9

Administrative Overhead 864

Net Profit Per Unit 2.324

Dept B

Direct Material 3,280

Labour Hour 686

Total Labour Cost 3430

Total Cost 6,710

Administration Cost 906

Selling Cost 9058.5

Selling Cost Per Unit 9.06

Administrative Overhead 905

Net Profit Per Unit 2.3485

a. The selling price per unit is 18.06

b. The total administrative overhead is 1769

c. The notational profit per unit is 4.67

11

Selling Cost 8964

Selling Cost Per Unit 9

Administrative Overhead 864

Net Profit Per Unit 2.324

Dept B

Direct Material 3,280

Labour Hour 686

Total Labour Cost 3430

Total Cost 6,710

Administration Cost 906

Selling Cost 9058.5

Selling Cost Per Unit 9.06

Administrative Overhead 905

Net Profit Per Unit 2.3485

a. The selling price per unit is 18.06

b. The total administrative overhead is 1769

c. The notational profit per unit is 4.67

11

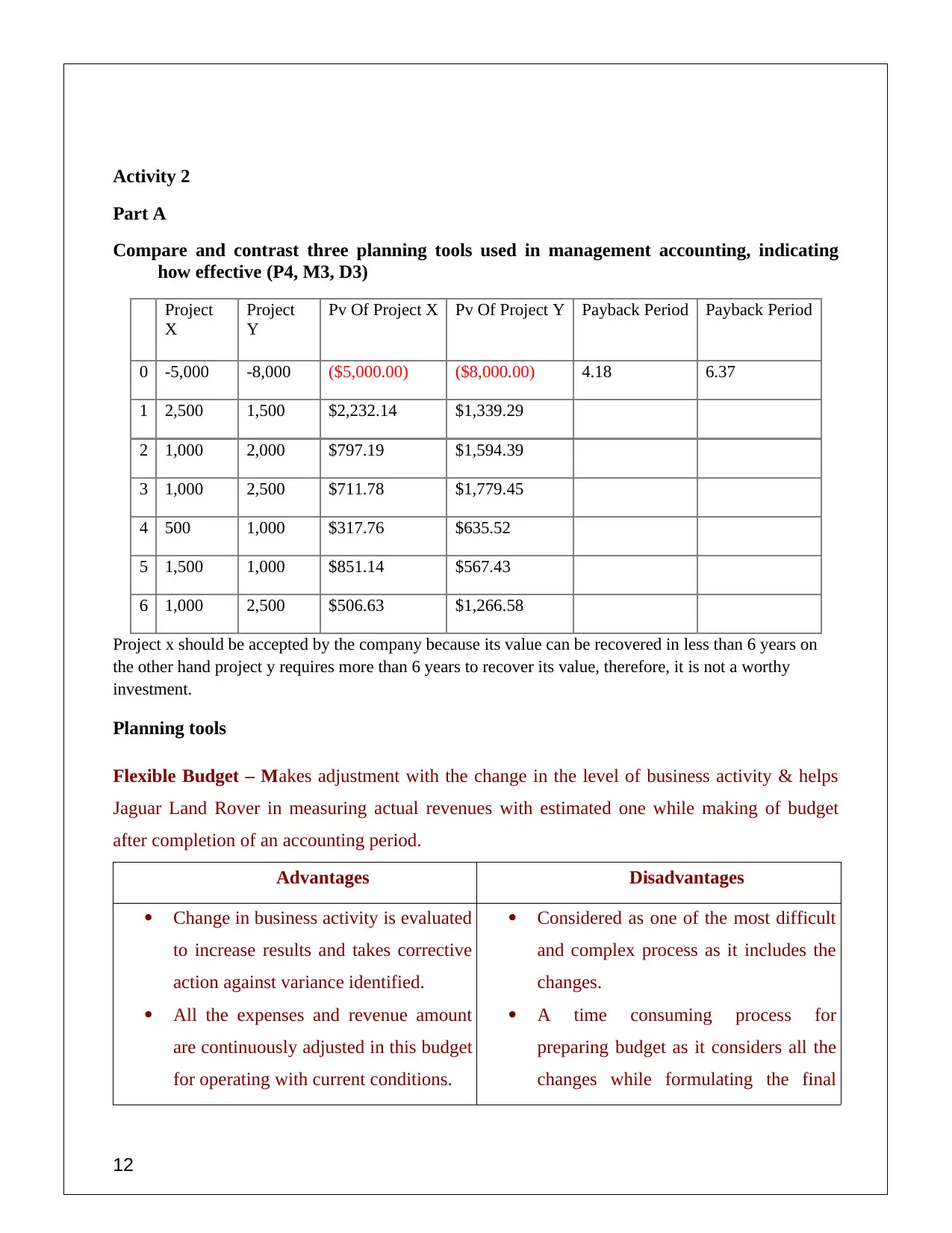

Activity 2

Part A

Compare and contrast three planning tools used in management accounting, indicating

how effective (P4, M3, D3)

Project

X

Project

Y

Pv Of Project X Pv Of Project Y Payback Period Payback Period

0 -5,000 -8,000 ($5,000.00) ($8,000.00) 4.18 6.37

1 2,500 1,500 $2,232.14 $1,339.29

2 1,000 2,000 $797.19 $1,594.39

3 1,000 2,500 $711.78 $1,779.45

4 500 1,000 $317.76 $635.52

5 1,500 1,000 $851.14 $567.43

6 1,000 2,500 $506.63 $1,266.58

Project x should be accepted by the company because its value can be recovered in less than 6 years on

the other hand project y requires more than 6 years to recover its value, therefore, it is not a worthy

investment.

Planning tools

Flexible Budget – Makes adjustment with the change in the level of business activity & helps

Jaguar Land Rover in measuring actual revenues with estimated one while making of budget

after completion of an accounting period.

Advantages Disadvantages

Change in business activity is evaluated

to increase results and takes corrective

action against variance identified.

All the expenses and revenue amount

are continuously adjusted in this budget

for operating with current conditions.

Considered as one of the most difficult

and complex process as it includes the

changes.

A time consuming process for

preparing budget as it considers all the

changes while formulating the final

12

Part A

Compare and contrast three planning tools used in management accounting, indicating

how effective (P4, M3, D3)

Project

X

Project

Y

Pv Of Project X Pv Of Project Y Payback Period Payback Period

0 -5,000 -8,000 ($5,000.00) ($8,000.00) 4.18 6.37

1 2,500 1,500 $2,232.14 $1,339.29

2 1,000 2,000 $797.19 $1,594.39

3 1,000 2,500 $711.78 $1,779.45

4 500 1,000 $317.76 $635.52

5 1,500 1,000 $851.14 $567.43

6 1,000 2,500 $506.63 $1,266.58

Project x should be accepted by the company because its value can be recovered in less than 6 years on

the other hand project y requires more than 6 years to recover its value, therefore, it is not a worthy

investment.

Planning tools

Flexible Budget – Makes adjustment with the change in the level of business activity & helps

Jaguar Land Rover in measuring actual revenues with estimated one while making of budget

after completion of an accounting period.

Advantages Disadvantages

Change in business activity is evaluated

to increase results and takes corrective

action against variance identified.

All the expenses and revenue amount

are continuously adjusted in this budget

for operating with current conditions.

Considered as one of the most difficult

and complex process as it includes the

changes.

A time consuming process for

preparing budget as it considers all the

changes while formulating the final

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.