Financial Accounting Project: Analysis of James Business Performance

VerifiedAdded on 2023/01/17

|12

|1856

|20

Project

AI Summary

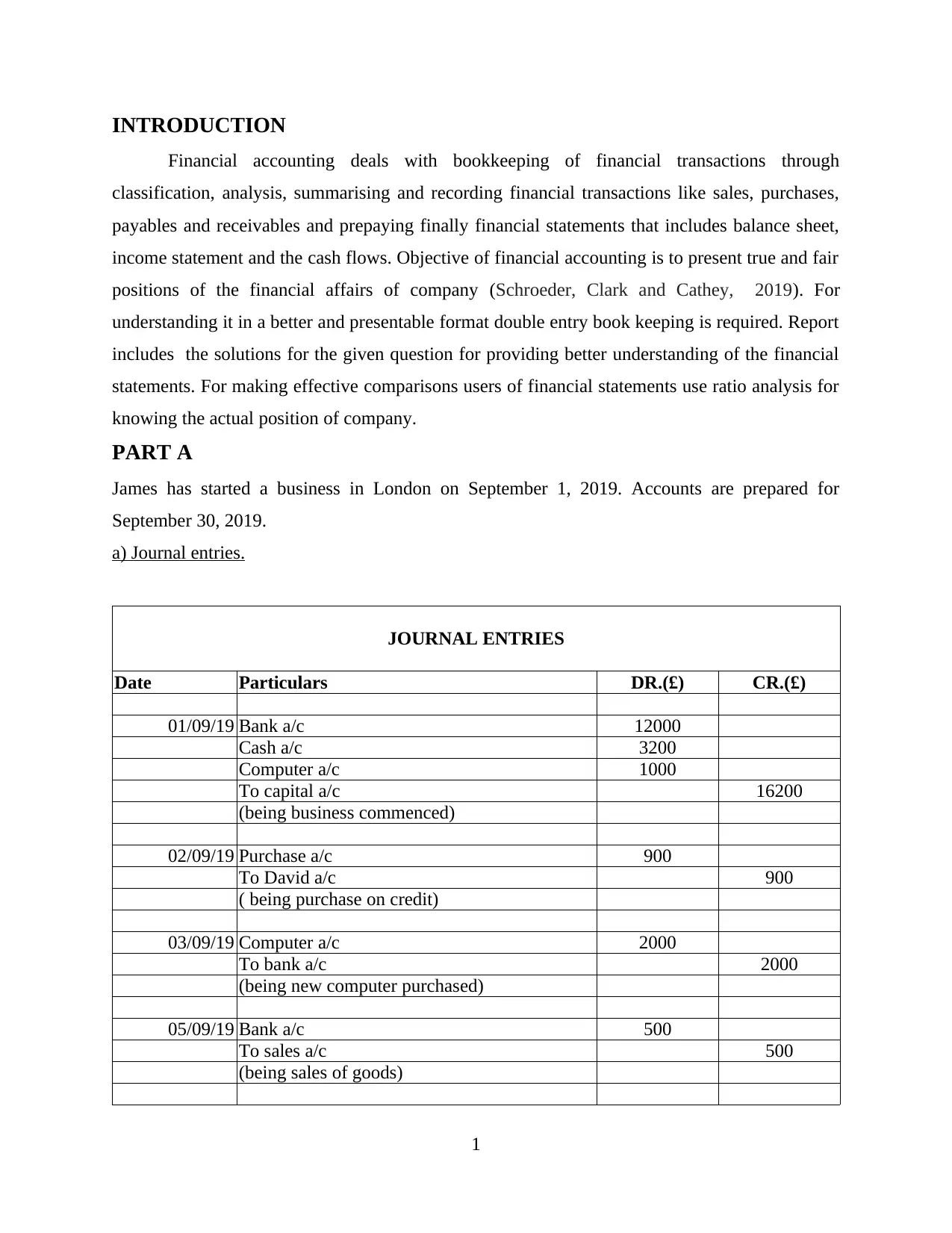

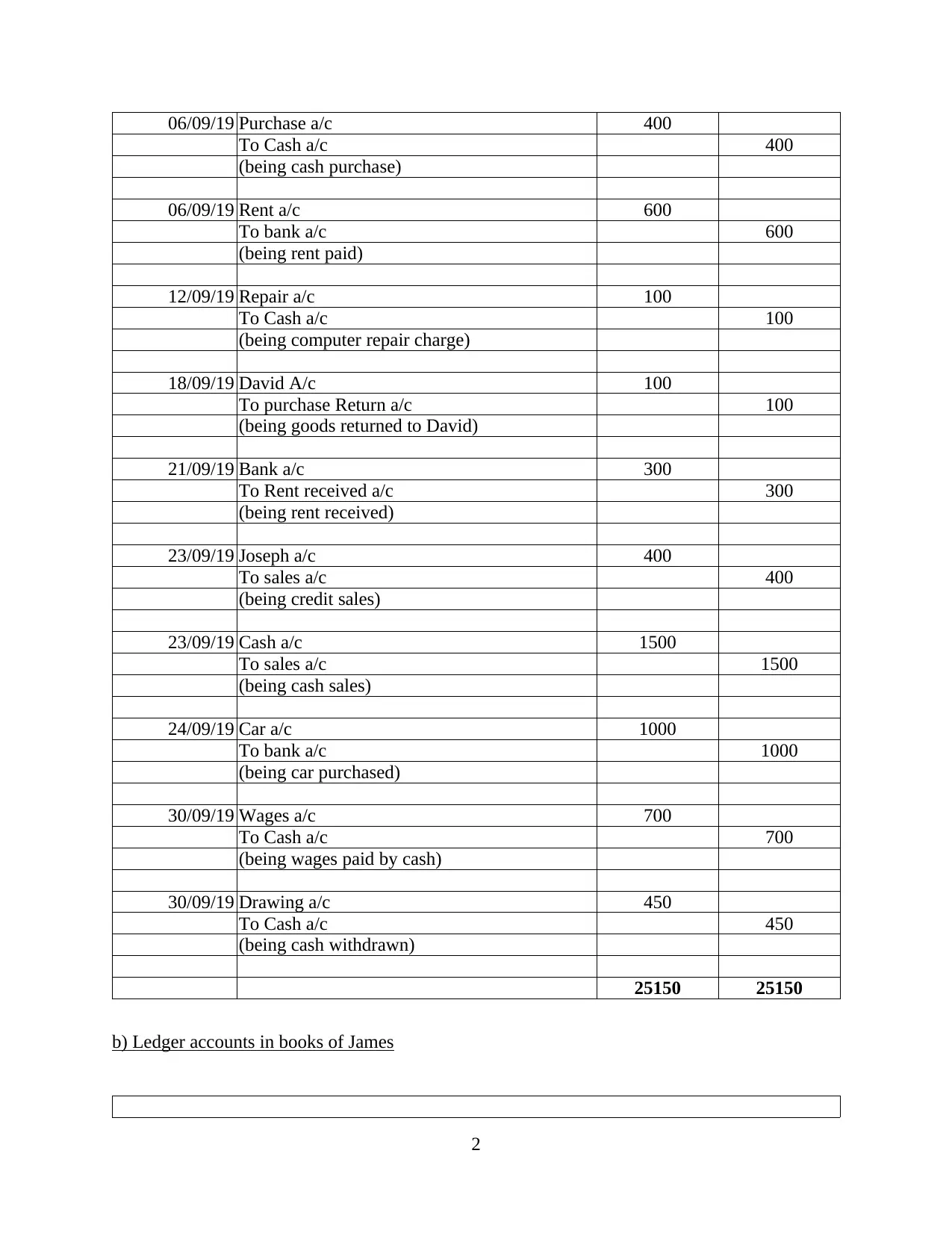

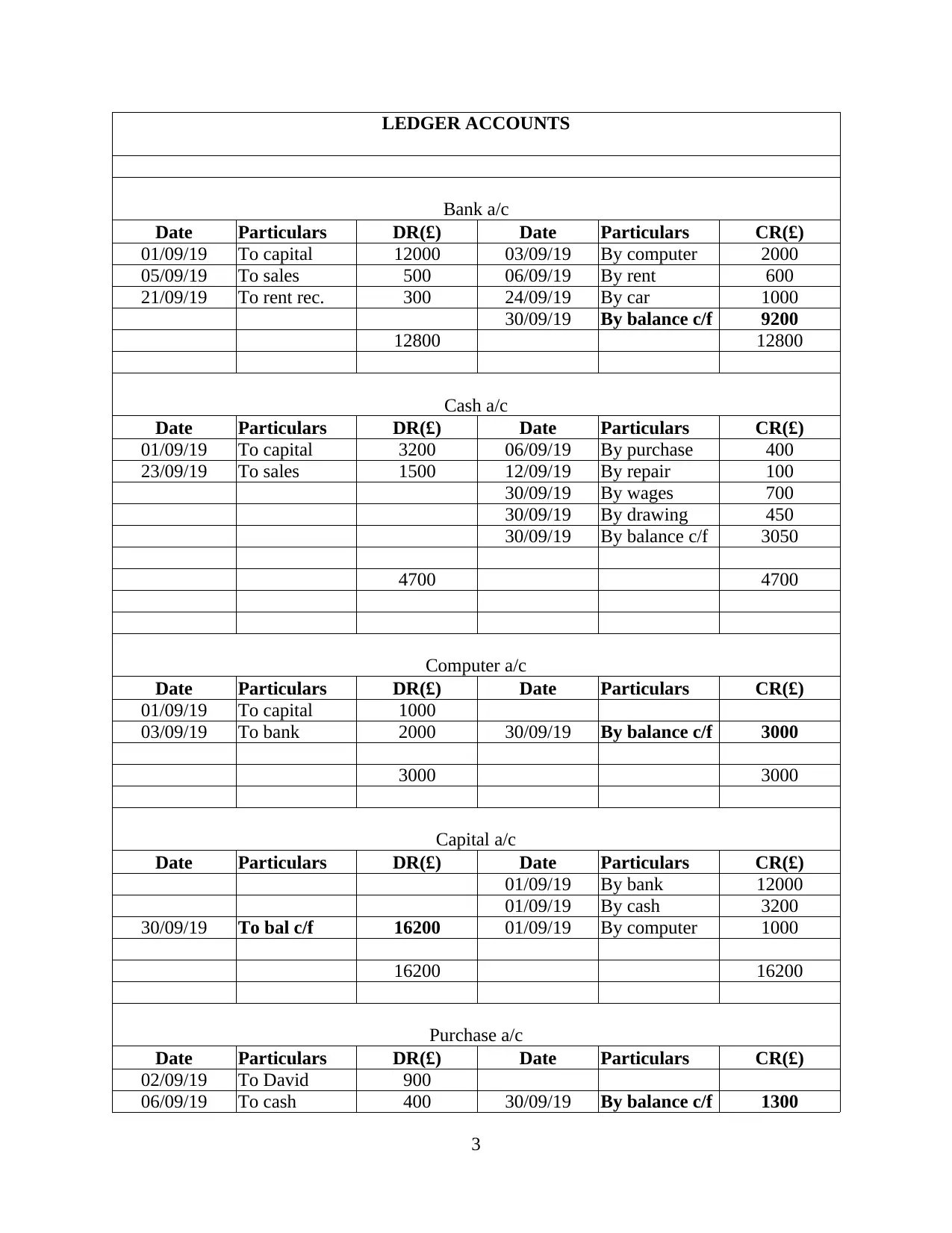

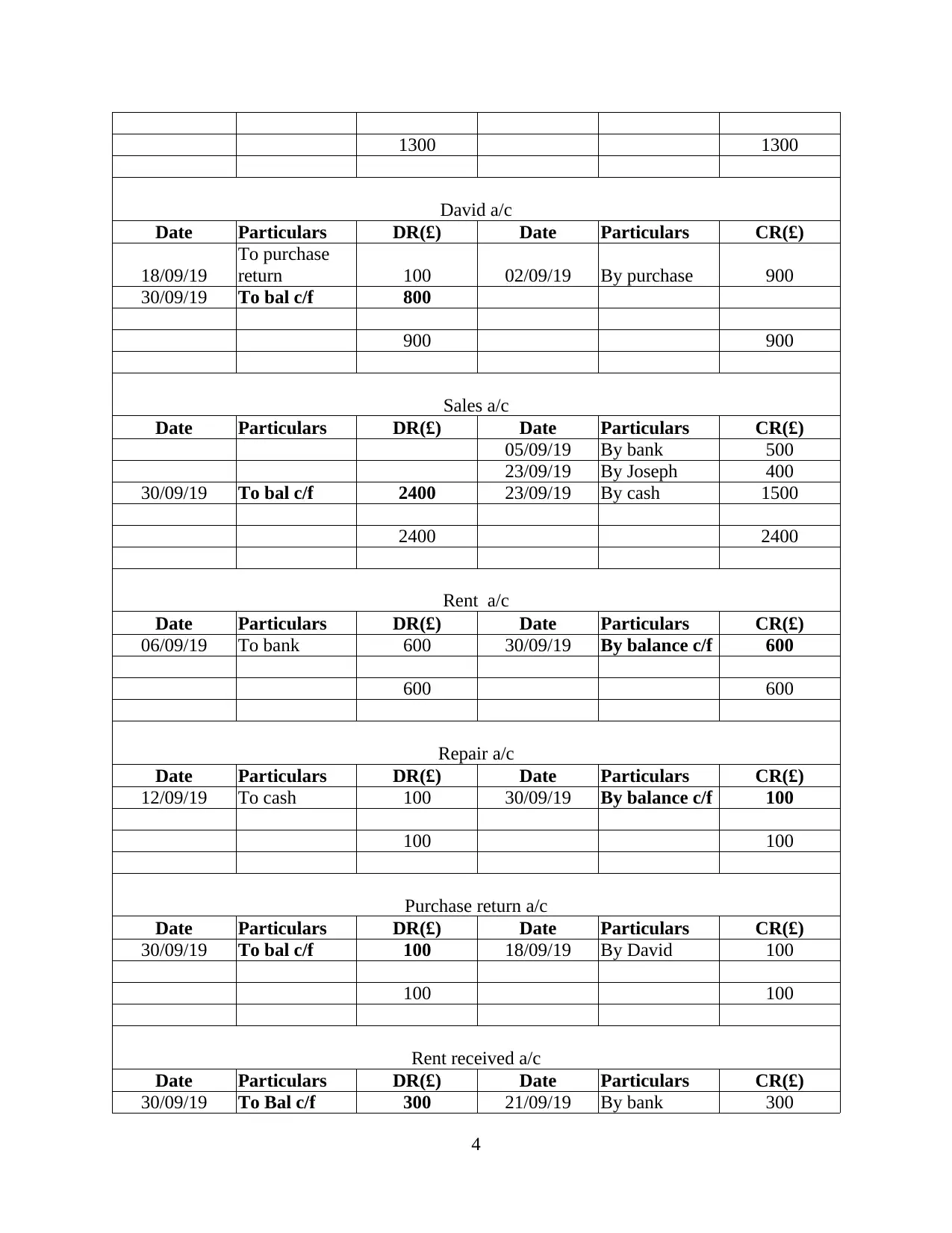

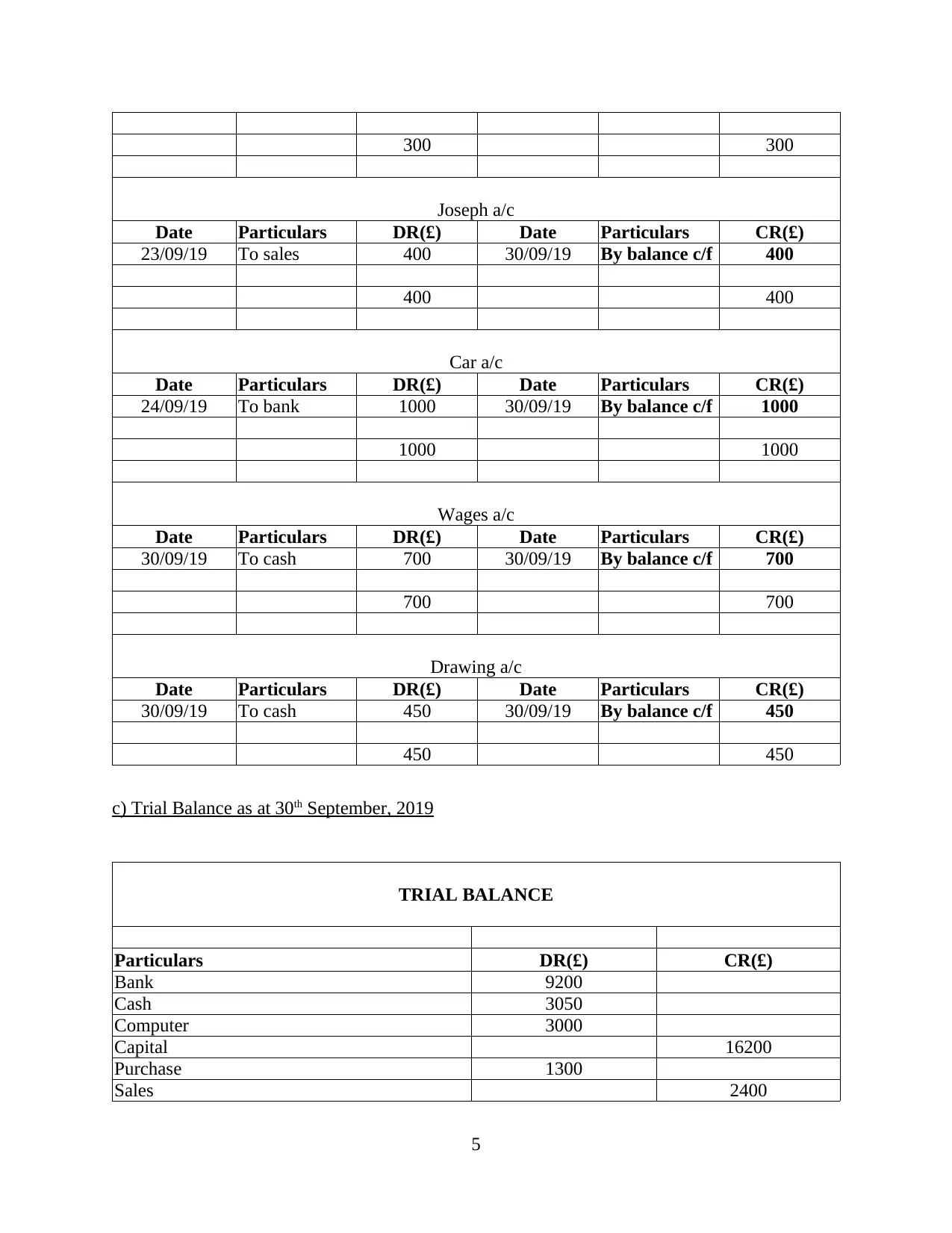

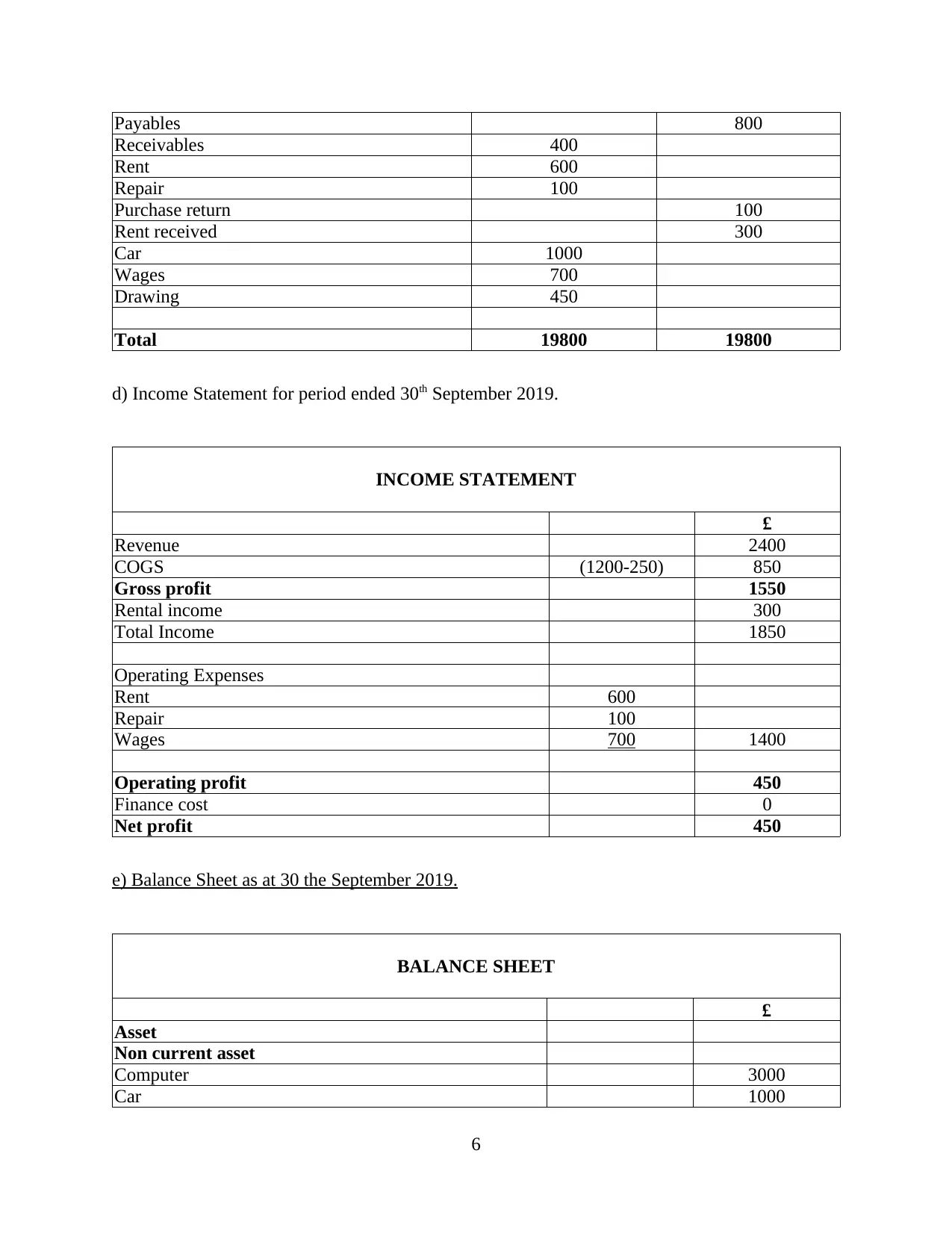

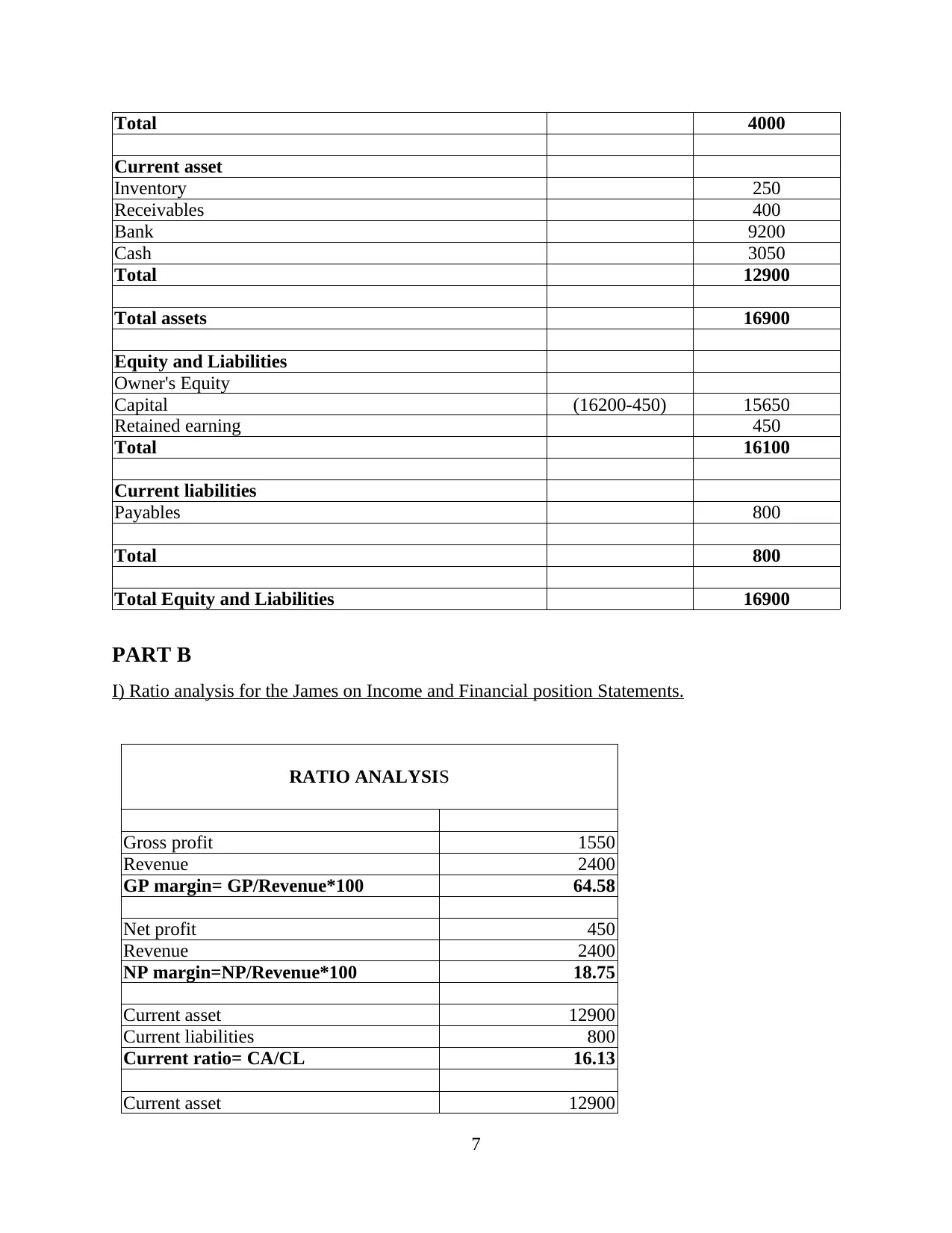

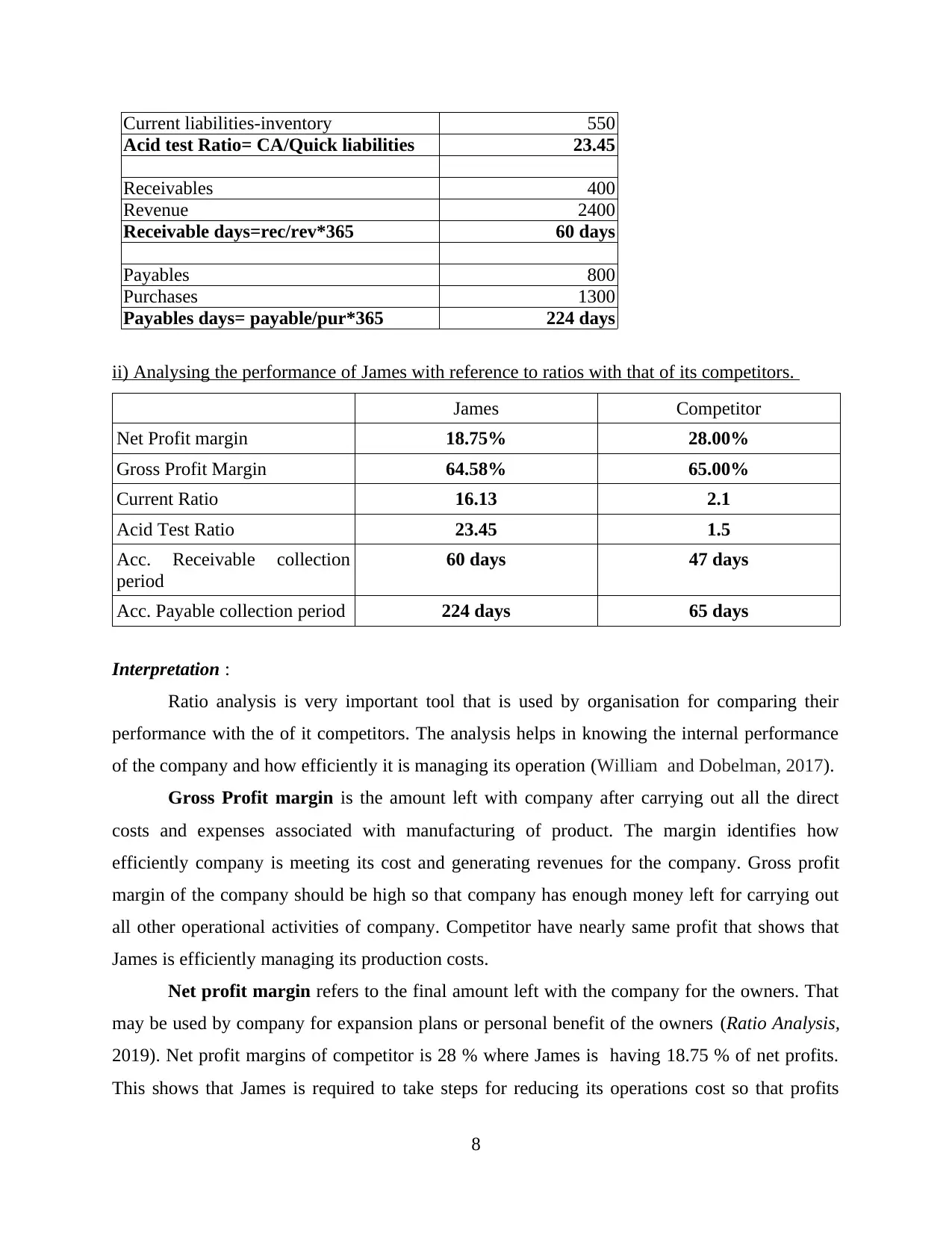

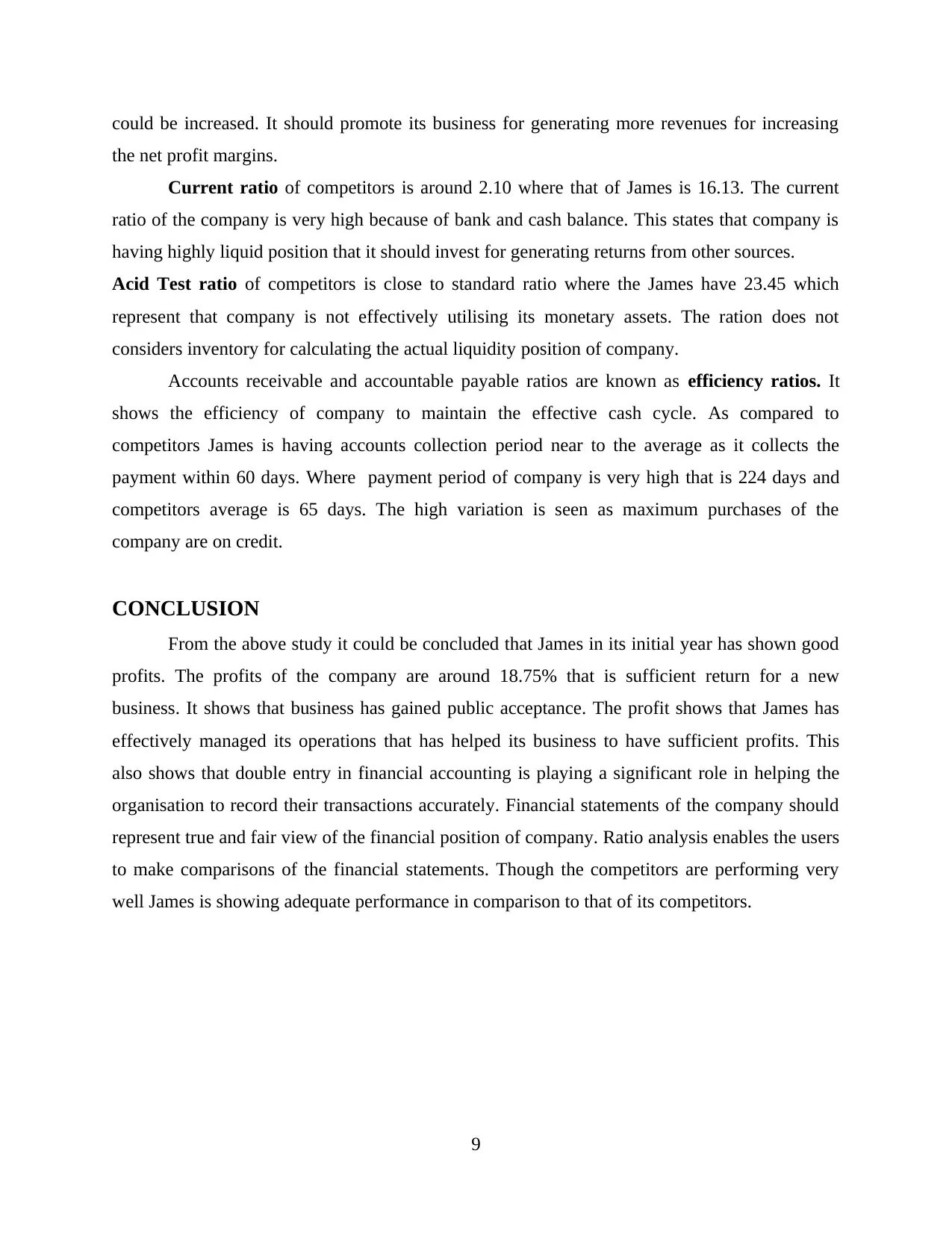

This project provides a comprehensive financial accounting analysis of James' business, which commenced operations in London on September 1, 2019. It begins with detailed journal entries for September, followed by the creation of ledger accounts. A trial balance as of September 30, 2019, is presented, along with an income statement and balance sheet. Part B focuses on ratio analysis, calculating gross profit margin, net profit margin, current ratio, acid-test ratio, and other relevant ratios to evaluate James' financial performance. The project includes a comparison of James' financial ratios with those of its competitors, providing insights into its operational efficiency and profitability. The analysis highlights areas for improvement, such as reducing operating costs and improving payment cycles, and concludes with an assessment of James' performance and financial standing.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.