Tax Law Assignment: Janice Brown's Net Capital Gain Calculation

VerifiedAdded on 2022/10/31

|13

|2478

|427

Homework Assignment

AI Summary

This tax law assignment focuses on calculating Janice Brown's net capital gain for the 2018/19 income year, excluding small business concessions. The assignment involves analyzing various transactions, including the sale of a Jet Ski, painting, rare book, investment house, Telstra shares, Rainbow Bay property, and Springwood property. The solution details the CGT events, asset classifications, and exemptions, particularly concerning the main residence exemption for the Rainbow Bay property. It also addresses the treatment of the land and house in Springwood, considering pre-CGT and post-CGT assets and the application of the indexation and discount methods. The calculation considers carried forward capital losses and determines the eligibility for the discount method, ultimately arriving at Janice Brown's net capital gain. The document provides a detailed breakdown of each transaction, applying relevant tax law principles and calculations to determine the final net capital gain.

Tax Law

30 June 2019

Seminar Number 8 2019

Question 1

You are required to just calculate Janice Brown’s “net capital gain” for the 2018/19 income

year. Assume Janice is not entitled to use any of the small business concessions in Division 152

ITAA 1997.

In addition to the transactions listed below, Janice also received salary income of $150,000 in

the 2018/19 and an unfranked divided of $3,000 from BHP shares. Janice also has carried

forward capital losses from:

the sale of a coin collection of $3,500, and

the sale of shares in Rio Tinto of $10,000

As we determined in Seminar #7 Janice had the following capital gains and/or losses (prior to

considering any capital losses, indexation method or discount method

Initial capital loss of $7,000 on Jet Ski (acquired 3 March 2014; disposed 12 June 2019);

Initial exempt capital gain of $1150 on a Painting (acquired 19 May 1990; disposed 12

June 2019);

Initial capital gain of $1,200 on Rare Book (acquired 5 April 2003; disposed 12 June

2019); and

Initial capital gain of $159,900 on Investment House (acquired 16 October 2010;

disposed 12 May 2019)

Initial capital gain of $340,000 on Telstra Shares (acquired 16 July 2016; disposed 6

April 2019).

1

30 June 2019

Seminar Number 8 2019

Question 1

You are required to just calculate Janice Brown’s “net capital gain” for the 2018/19 income

year. Assume Janice is not entitled to use any of the small business concessions in Division 152

ITAA 1997.

In addition to the transactions listed below, Janice also received salary income of $150,000 in

the 2018/19 and an unfranked divided of $3,000 from BHP shares. Janice also has carried

forward capital losses from:

the sale of a coin collection of $3,500, and

the sale of shares in Rio Tinto of $10,000

As we determined in Seminar #7 Janice had the following capital gains and/or losses (prior to

considering any capital losses, indexation method or discount method

Initial capital loss of $7,000 on Jet Ski (acquired 3 March 2014; disposed 12 June 2019);

Initial exempt capital gain of $1150 on a Painting (acquired 19 May 1990; disposed 12

June 2019);

Initial capital gain of $1,200 on Rare Book (acquired 5 April 2003; disposed 12 June

2019); and

Initial capital gain of $159,900 on Investment House (acquired 16 October 2010;

disposed 12 May 2019)

Initial capital gain of $340,000 on Telstra Shares (acquired 16 July 2016; disposed 6

April 2019).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

Rainbow Bay Property

Janice signed a contract to purchase a house (on 0.2 hectares) at 19 Finders Street Rainbow

Bay on the Gold Coast on 15 August 2008 for $350,000. Ownership transferred to her on 15

September 2008. Janice lived in Rainbow Bay Property as her home from the 15th September

2008 until to 20th November 2014.

On 21st November 2014, Janice decided to move to Brisbane so that her children could attend

an exclusive private school. She rented the Rainbow Bay house to tenants from the 21st

November 2014 and received approximately $35,000 per year in rent. The family moved into an

apartment at Kangaroo Point which they rented through a local real estate agent.

In April 2019 Janice decided that her family had settled well into the Brisbane lifestyle and as a

result she would buy a home in Brisbane. As a consequence, she had to sell the Rainbow Bay

house to fund the purchase. She placed the property on the market and sold the Rainbow Bay

house for $800,000 under a contract dated 13 June 2019. In relation to the sale, she paid a

$16,000 commission to the real estate agent and $2,500 in legal fees to her lawyer. The

ownership of the Rainbow Bay house transferred to the new owner on 13 July 2019.

2

30 June 2019

Rainbow Bay Property

Janice signed a contract to purchase a house (on 0.2 hectares) at 19 Finders Street Rainbow

Bay on the Gold Coast on 15 August 2008 for $350,000. Ownership transferred to her on 15

September 2008. Janice lived in Rainbow Bay Property as her home from the 15th September

2008 until to 20th November 2014.

On 21st November 2014, Janice decided to move to Brisbane so that her children could attend

an exclusive private school. She rented the Rainbow Bay house to tenants from the 21st

November 2014 and received approximately $35,000 per year in rent. The family moved into an

apartment at Kangaroo Point which they rented through a local real estate agent.

In April 2019 Janice decided that her family had settled well into the Brisbane lifestyle and as a

result she would buy a home in Brisbane. As a consequence, she had to sell the Rainbow Bay

house to fund the purchase. She placed the property on the market and sold the Rainbow Bay

house for $800,000 under a contract dated 13 June 2019. In relation to the sale, she paid a

$16,000 commission to the real estate agent and $2,500 in legal fees to her lawyer. The

ownership of the Rainbow Bay house transferred to the new owner on 13 July 2019.

2

Tax Law

30 June 2019

Springwood Property

On 10 January 1984 Janice Brown purchased a block of land for $20,000 in

Springwood on which to build a house. After receiving many quotations, Janice signed a

contract on 21 April 1988 with Construct with Us Pty Ltd to construct the house. The

house construction began on 1 July 1988 and was completed on the 31st October 1988 at

a cost of $95,000.

Instead of moving into the house, Janice rented it out to tenants. She continued to do this

until she eventually sold the property for $720,000 under a contract dated 11 June 2019

with the ownership transferring on 11 July 2019. An independent valuation revealed that

the land was worth $550,000 at the time of sale. (Hint! Could the house be considered

as separate asset to the land?)

===================

3

30 June 2019

Springwood Property

On 10 January 1984 Janice Brown purchased a block of land for $20,000 in

Springwood on which to build a house. After receiving many quotations, Janice signed a

contract on 21 April 1988 with Construct with Us Pty Ltd to construct the house. The

house construction began on 1 July 1988 and was completed on the 31st October 1988 at

a cost of $95,000.

Instead of moving into the house, Janice rented it out to tenants. She continued to do this

until she eventually sold the property for $720,000 under a contract dated 11 June 2019

with the ownership transferring on 11 July 2019. An independent valuation revealed that

the land was worth $550,000 at the time of sale. (Hint! Could the house be considered

as separate asset to the land?)

===================

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

Rainbow Bay Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

1 –

CGT event?

Yes, CGT event A1 was present. Janice sold the Rainbow property. This disposal led to a change of ownership of the

property from Janice to the buyer. s 104-10(2)

Timing -This aspect was depicted on 13-june-2019 when Janice got into contract that led to the disposal of the

Rainbow Bay property. s 104-10(3)

It was during the income year 2018/2019

2 –

CGT asset?

Yes, this is because the Rainbow Bay property is a type of property that can be considered as an asset s108-5

Firstly, as per s108-20(3) which states that buildings are not included as personal assets, the Rainbow Bay property

can be categorized as an asset under “other asset” category. Also, that Janice acquired the property after getting into

a purchase contract on 15th Aug 2008 hence it can be considered as a post CGT asset since its acquisition came after

21st sept 1985. s109-5

4

30 June 2019

Rainbow Bay Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

1 –

CGT event?

Yes, CGT event A1 was present. Janice sold the Rainbow property. This disposal led to a change of ownership of the

property from Janice to the buyer. s 104-10(2)

Timing -This aspect was depicted on 13-june-2019 when Janice got into contract that led to the disposal of the

Rainbow Bay property. s 104-10(3)

It was during the income year 2018/2019

2 –

CGT asset?

Yes, this is because the Rainbow Bay property is a type of property that can be considered as an asset s108-5

Firstly, as per s108-20(3) which states that buildings are not included as personal assets, the Rainbow Bay property

can be categorized as an asset under “other asset” category. Also, that Janice acquired the property after getting into

a purchase contract on 15th Aug 2008 hence it can be considered as a post CGT asset since its acquisition came after

21st sept 1985. s109-5

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

Rainbow Bay Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

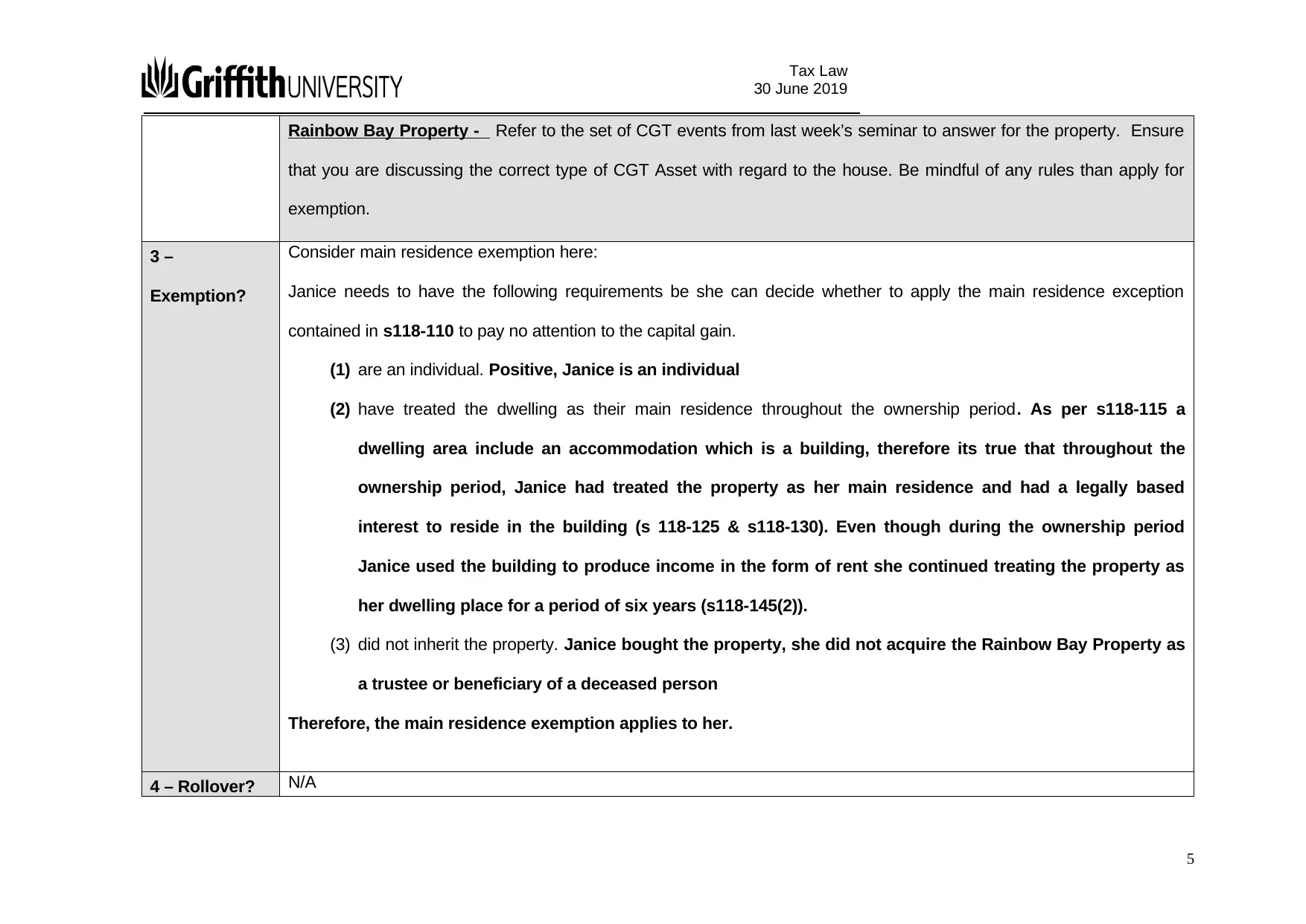

3 –

Exemption?

Consider main residence exemption here:

Janice needs to have the following requirements be she can decide whether to apply the main residence exception

contained in s118-110 to pay no attention to the capital gain.

(1) are an individual. Positive, Janice is an individual

(2) have treated the dwelling as their main residence throughout the ownership period. As per s118-115 a

dwelling area include an accommodation which is a building, therefore its true that throughout the

ownership period, Janice had treated the property as her main residence and had a legally based

interest to reside in the building (s 118-125 & s118-130). Even though during the ownership period

Janice used the building to produce income in the form of rent she continued treating the property as

her dwelling place for a period of six years (s118-145(2)).

(3) did not inherit the property. Janice bought the property, she did not acquire the Rainbow Bay Property as

a trustee or beneficiary of a deceased person

Therefore, the main residence exemption applies to her.

4 – Rollover? N/A

5

30 June 2019

Rainbow Bay Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

3 –

Exemption?

Consider main residence exemption here:

Janice needs to have the following requirements be she can decide whether to apply the main residence exception

contained in s118-110 to pay no attention to the capital gain.

(1) are an individual. Positive, Janice is an individual

(2) have treated the dwelling as their main residence throughout the ownership period. As per s118-115 a

dwelling area include an accommodation which is a building, therefore its true that throughout the

ownership period, Janice had treated the property as her main residence and had a legally based

interest to reside in the building (s 118-125 & s118-130). Even though during the ownership period

Janice used the building to produce income in the form of rent she continued treating the property as

her dwelling place for a period of six years (s118-145(2)).

(3) did not inherit the property. Janice bought the property, she did not acquire the Rainbow Bay Property as

a trustee or beneficiary of a deceased person

Therefore, the main residence exemption applies to her.

4 – Rollover? N/A

5

Tax Law

30 June 2019

Rainbow Bay Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

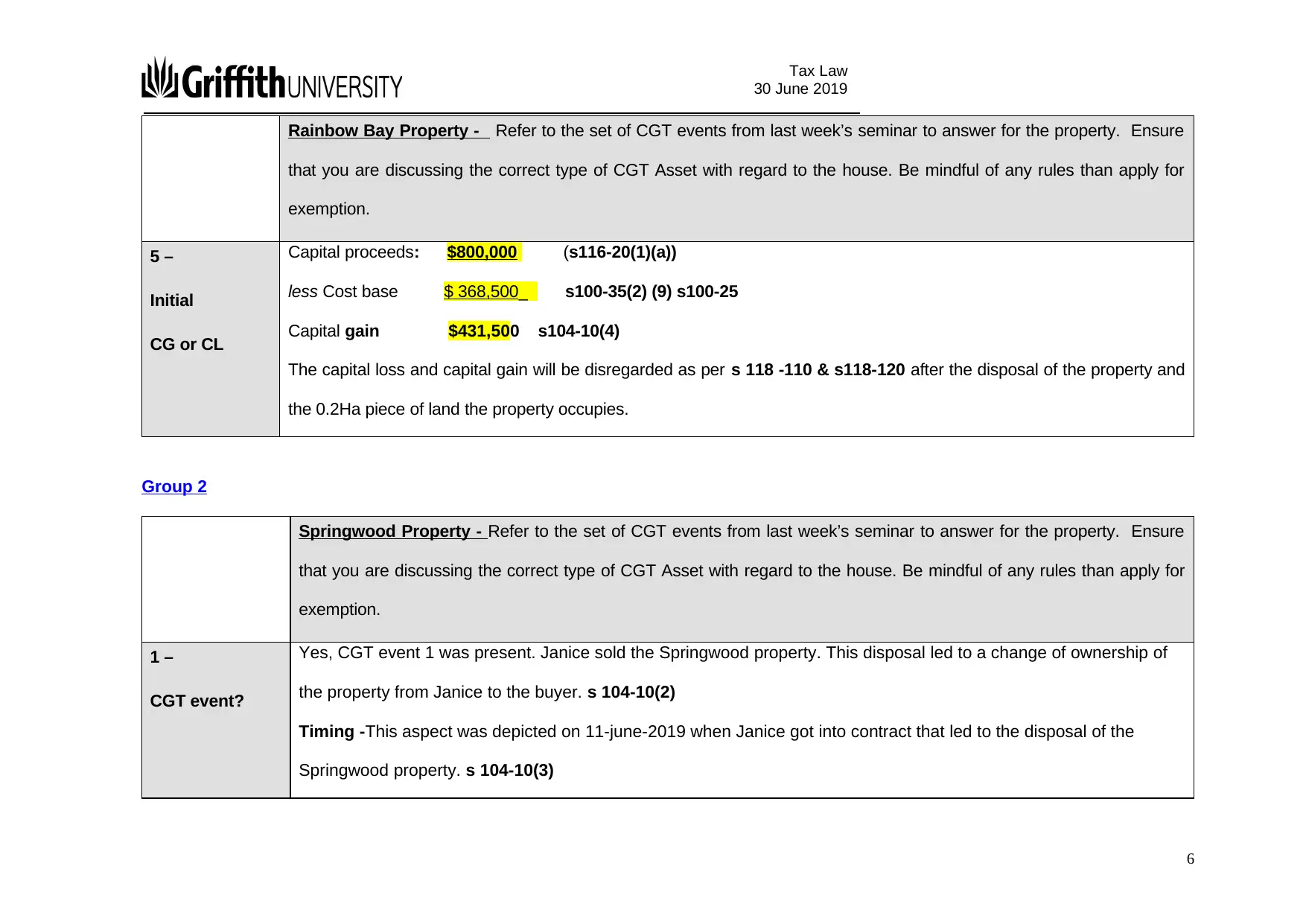

5 –

Initial

CG or CL

Capital proceeds: $800,000 (s116-20(1)(a))

less Cost base $ 368,500_ s100-35(2) (9) s100-25

Capital gain $431,500 s104-10(4)

The capital loss and capital gain will be disregarded as per s 118 -110 & s118-120 after the disposal of the property and

the 0.2Ha piece of land the property occupies.

Group 2

Springwood Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

1 –

CGT event?

Yes, CGT event 1 was present. Janice sold the Springwood property. This disposal led to a change of ownership of

the property from Janice to the buyer. s 104-10(2)

Timing -This aspect was depicted on 11-june-2019 when Janice got into contract that led to the disposal of the

Springwood property. s 104-10(3)

6

30 June 2019

Rainbow Bay Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

5 –

Initial

CG or CL

Capital proceeds: $800,000 (s116-20(1)(a))

less Cost base $ 368,500_ s100-35(2) (9) s100-25

Capital gain $431,500 s104-10(4)

The capital loss and capital gain will be disregarded as per s 118 -110 & s118-120 after the disposal of the property and

the 0.2Ha piece of land the property occupies.

Group 2

Springwood Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

1 –

CGT event?

Yes, CGT event 1 was present. Janice sold the Springwood property. This disposal led to a change of ownership of

the property from Janice to the buyer. s 104-10(2)

Timing -This aspect was depicted on 11-june-2019 when Janice got into contract that led to the disposal of the

Springwood property. s 104-10(3)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tax Law

30 June 2019

Springwood Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

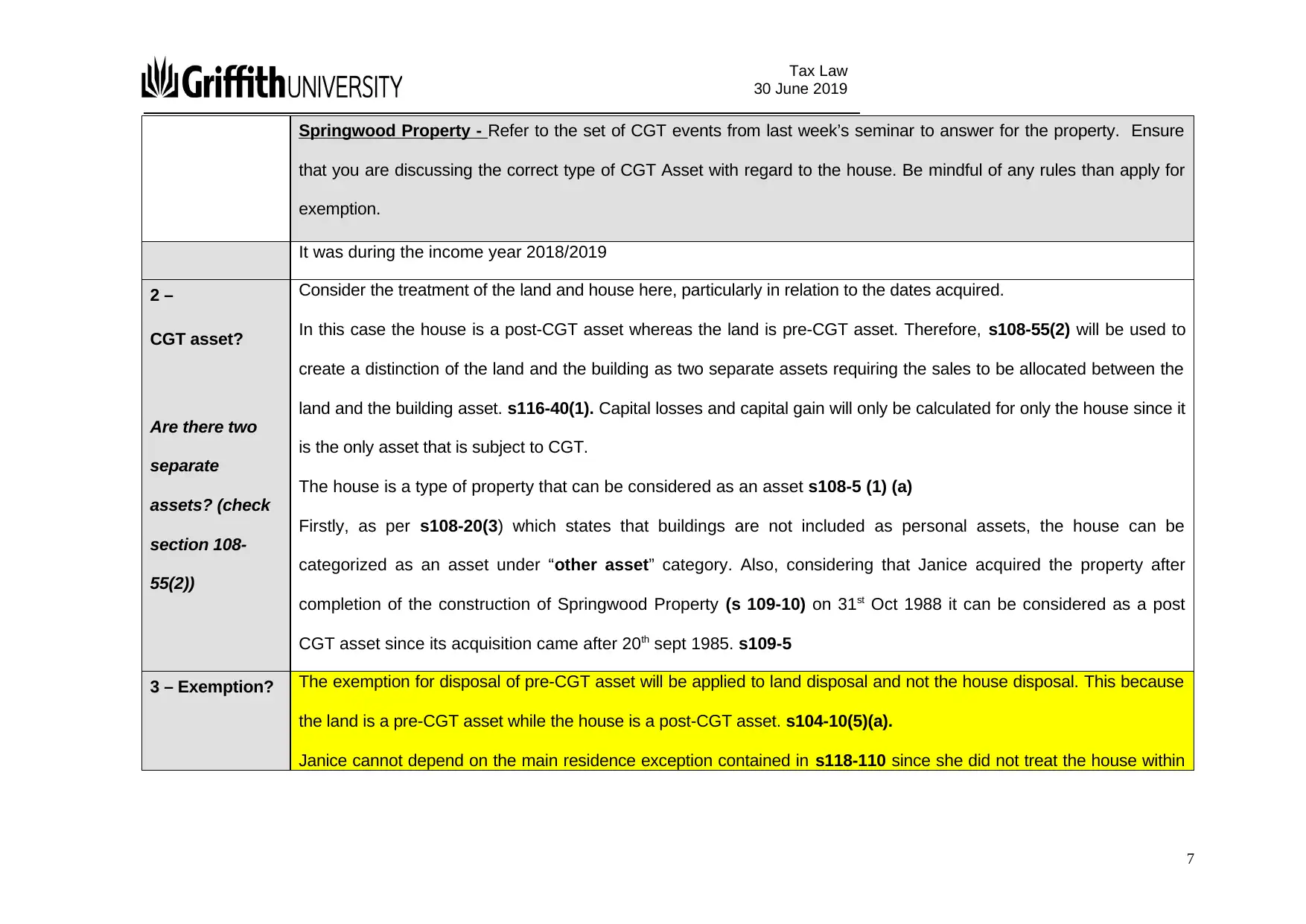

It was during the income year 2018/2019

2 –

CGT asset?

Are there two

separate

assets? (check

section 108-

55(2))

Consider the treatment of the land and house here, particularly in relation to the dates acquired.

In this case the house is a post-CGT asset whereas the land is pre-CGT asset. Therefore, s108-55(2) will be used to

create a distinction of the land and the building as two separate assets requiring the sales to be allocated between the

land and the building asset. s116-40(1). Capital losses and capital gain will only be calculated for only the house since it

is the only asset that is subject to CGT.

The house is a type of property that can be considered as an asset s108-5 (1) (a)

Firstly, as per s108-20(3) which states that buildings are not included as personal assets, the house can be

categorized as an asset under “other asset” category. Also, considering that Janice acquired the property after

completion of the construction of Springwood Property (s 109-10) on 31st Oct 1988 it can be considered as a post

CGT asset since its acquisition came after 20th sept 1985. s109-5

3 – Exemption? The exemption for disposal of pre-CGT asset will be applied to land disposal and not the house disposal. This because

the land is a pre-CGT asset while the house is a post-CGT asset. s104-10(5)(a).

Janice cannot depend on the main residence exception contained in s118-110 since she did not treat the house within

7

30 June 2019

Springwood Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

It was during the income year 2018/2019

2 –

CGT asset?

Are there two

separate

assets? (check

section 108-

55(2))

Consider the treatment of the land and house here, particularly in relation to the dates acquired.

In this case the house is a post-CGT asset whereas the land is pre-CGT asset. Therefore, s108-55(2) will be used to

create a distinction of the land and the building as two separate assets requiring the sales to be allocated between the

land and the building asset. s116-40(1). Capital losses and capital gain will only be calculated for only the house since it

is the only asset that is subject to CGT.

The house is a type of property that can be considered as an asset s108-5 (1) (a)

Firstly, as per s108-20(3) which states that buildings are not included as personal assets, the house can be

categorized as an asset under “other asset” category. Also, considering that Janice acquired the property after

completion of the construction of Springwood Property (s 109-10) on 31st Oct 1988 it can be considered as a post

CGT asset since its acquisition came after 20th sept 1985. s109-5

3 – Exemption? The exemption for disposal of pre-CGT asset will be applied to land disposal and not the house disposal. This because

the land is a pre-CGT asset while the house is a post-CGT asset. s104-10(5)(a).

Janice cannot depend on the main residence exception contained in s118-110 since she did not treat the house within

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

30 June 2019

Springwood Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

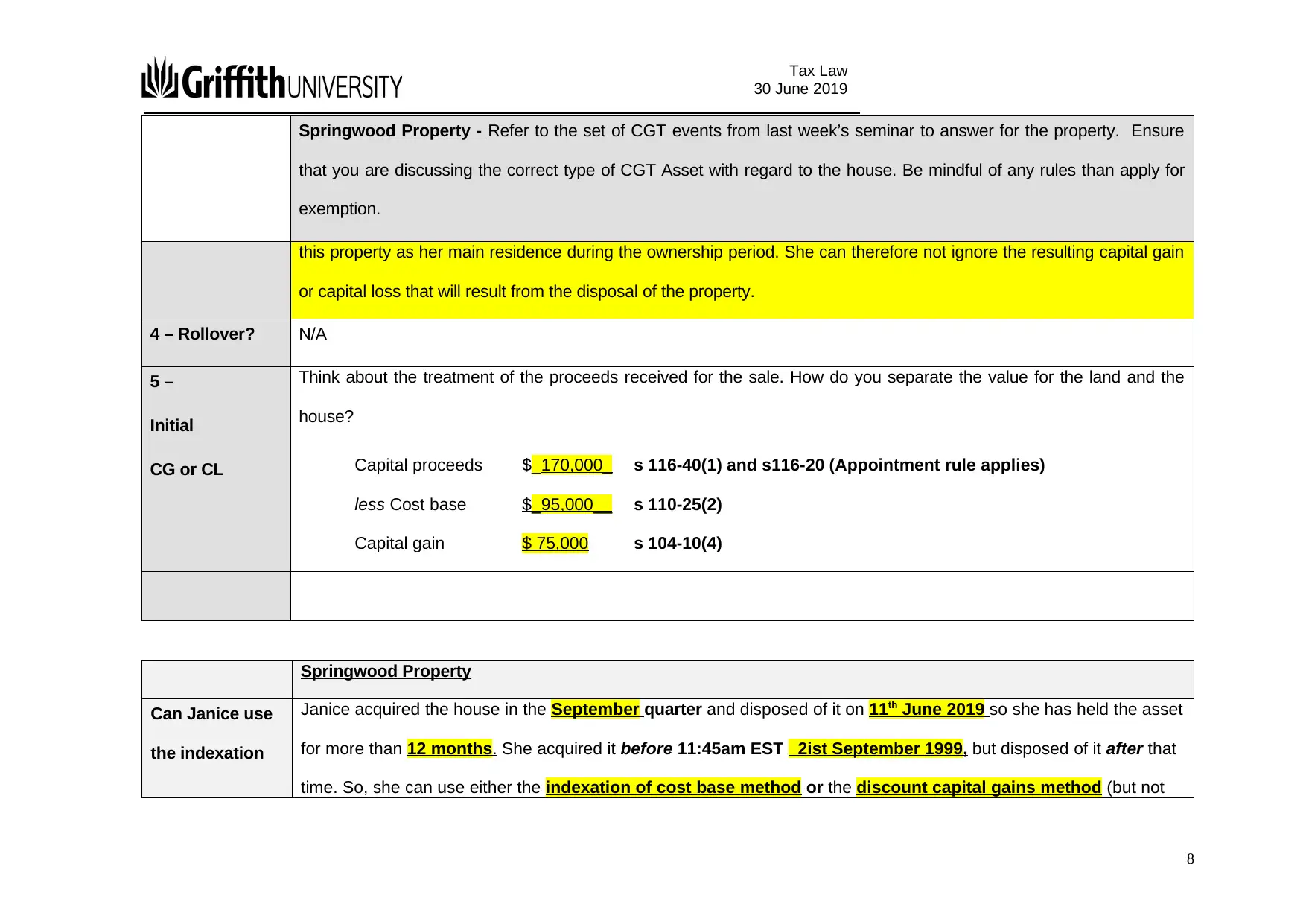

this property as her main residence during the ownership period. She can therefore not ignore the resulting capital gain

or capital loss that will result from the disposal of the property.

4 – Rollover? N/A

5 –

Initial

CG or CL

Think about the treatment of the proceeds received for the sale. How do you separate the value for the land and the

house?

Capital proceeds $_170,000_ s 116-40(1) and s116-20 (Appointment rule applies)

less Cost base $_95,000__ s 110-25(2)

Capital gain $ 75,000 s 104-10(4)

Springwood Property

Can Janice use

the indexation

Janice acquired the house in the September quarter and disposed of it on 11th June 2019 so she has held the asset

for more than 12 months. She acquired it before 11:45am EST _2ist September 1999, but disposed of it after that

time. So, she can use either the indexation of cost base method or the discount capital gains method (but not

8

30 June 2019

Springwood Property - Refer to the set of CGT events from last week’s seminar to answer for the property. Ensure

that you are discussing the correct type of CGT Asset with regard to the house. Be mindful of any rules than apply for

exemption.

this property as her main residence during the ownership period. She can therefore not ignore the resulting capital gain

or capital loss that will result from the disposal of the property.

4 – Rollover? N/A

5 –

Initial

CG or CL

Think about the treatment of the proceeds received for the sale. How do you separate the value for the land and the

house?

Capital proceeds $_170,000_ s 116-40(1) and s116-20 (Appointment rule applies)

less Cost base $_95,000__ s 110-25(2)

Capital gain $ 75,000 s 104-10(4)

Springwood Property

Can Janice use

the indexation

Janice acquired the house in the September quarter and disposed of it on 11th June 2019 so she has held the asset

for more than 12 months. She acquired it before 11:45am EST _2ist September 1999, but disposed of it after that

time. So, she can use either the indexation of cost base method or the discount capital gains method (but not

8

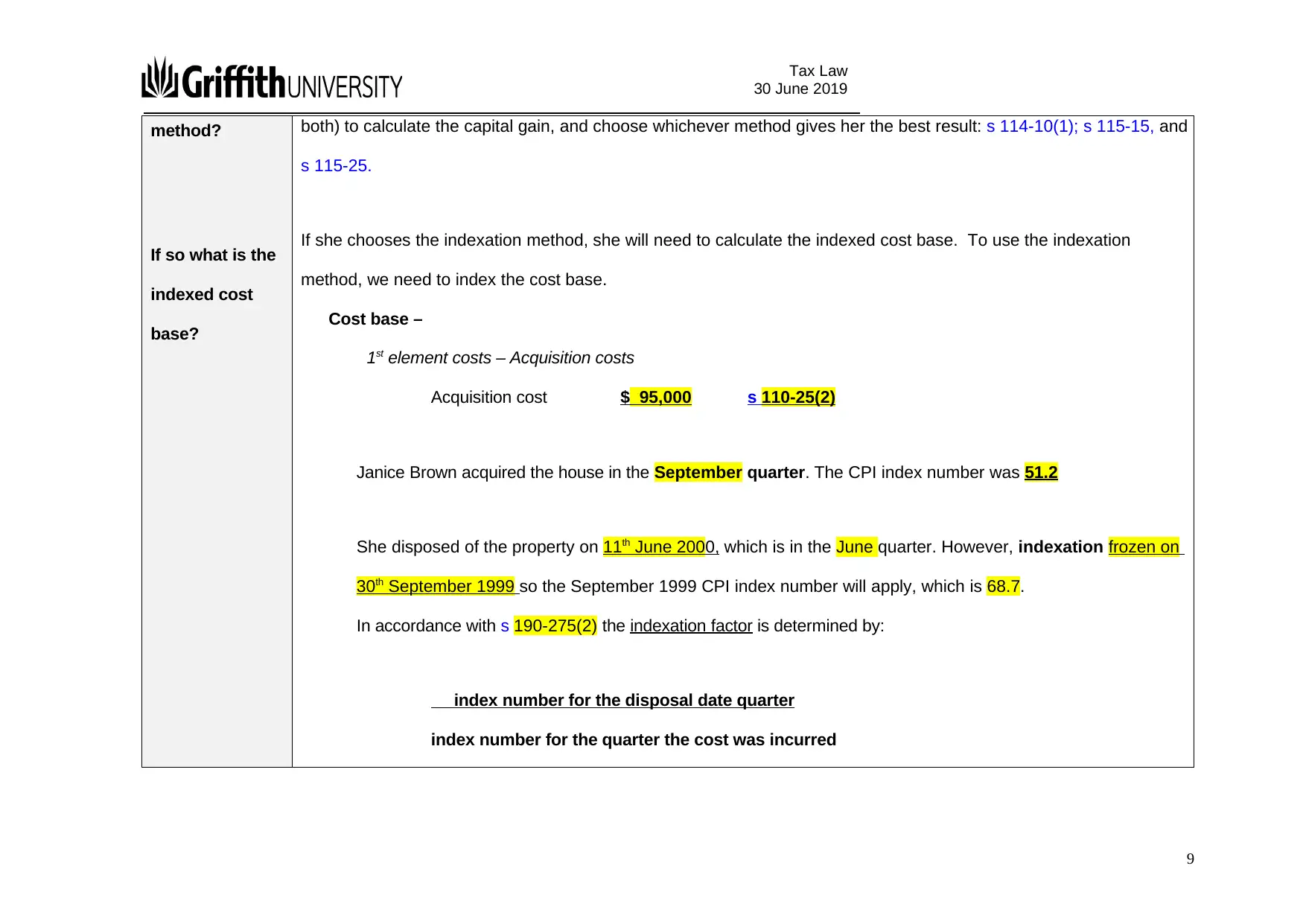

Tax Law

30 June 2019

method?

If so what is the

indexed cost

base?

both) to calculate the capital gain, and choose whichever method gives her the best result: s 114-10(1); s 115-15, and

s 115-25.

If she chooses the indexation method, she will need to calculate the indexed cost base. To use the indexation

method, we need to index the cost base.

Cost base –

1st element costs – Acquisition costs

Acquisition cost $_95,000 s 110-25(2)

Janice Brown acquired the house in the September quarter. The CPI index number was 51.2

She disposed of the property on 11th June 2000, which is in the June quarter. However, indexation frozen on

30th September 1999 so the September 1999 CPI index number will apply, which is 68.7.

In accordance with s 190-275(2) the indexation factor is determined by:

index number for the disposal date quarter

index number for the quarter the cost was incurred

9

30 June 2019

method?

If so what is the

indexed cost

base?

both) to calculate the capital gain, and choose whichever method gives her the best result: s 114-10(1); s 115-15, and

s 115-25.

If she chooses the indexation method, she will need to calculate the indexed cost base. To use the indexation

method, we need to index the cost base.

Cost base –

1st element costs – Acquisition costs

Acquisition cost $_95,000 s 110-25(2)

Janice Brown acquired the house in the September quarter. The CPI index number was 51.2

She disposed of the property on 11th June 2000, which is in the June quarter. However, indexation frozen on

30th September 1999 so the September 1999 CPI index number will apply, which is 68.7.

In accordance with s 190-275(2) the indexation factor is determined by:

index number for the disposal date quarter

index number for the quarter the cost was incurred

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

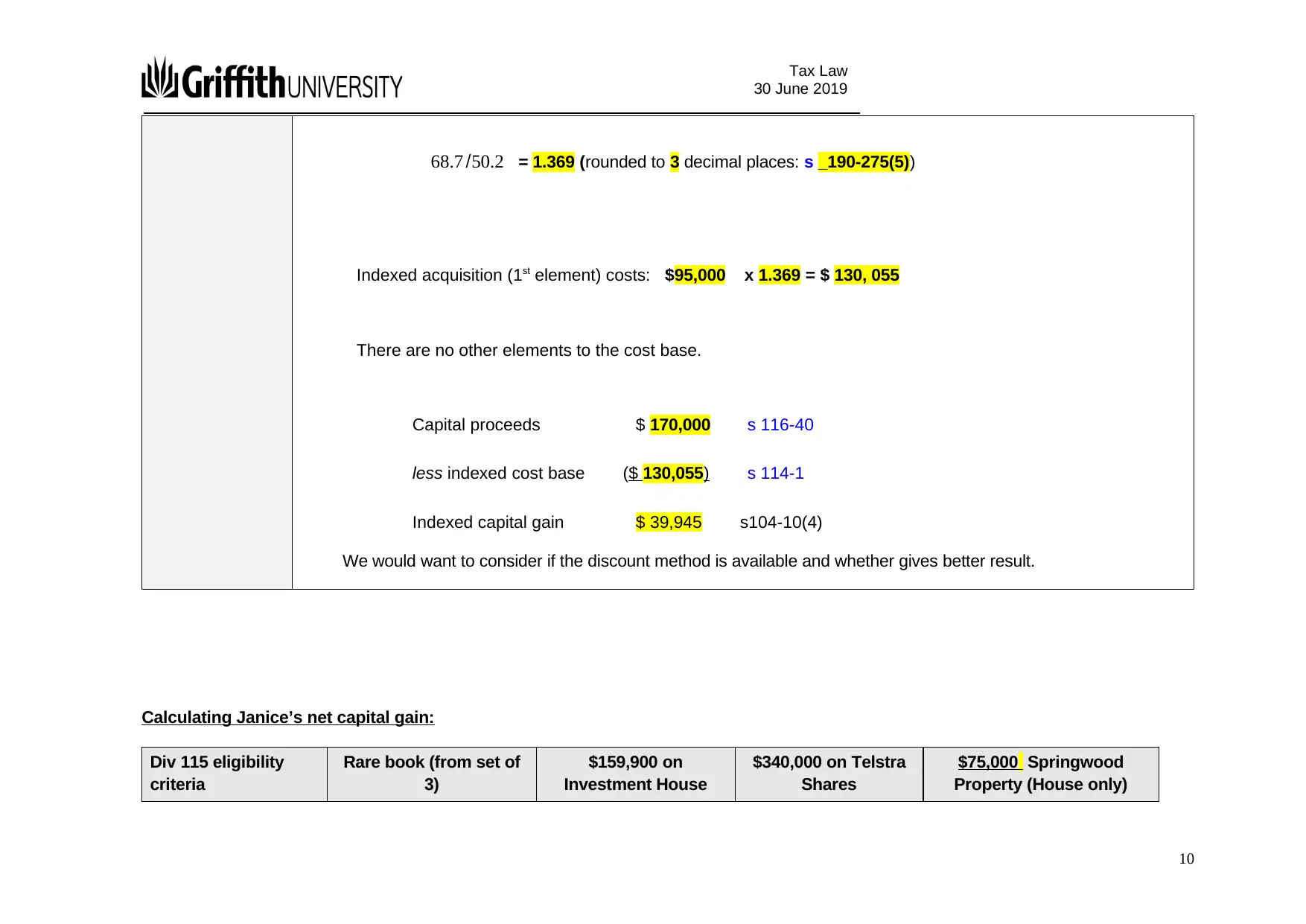

Tax Law

30 June 2019

68.7 /50.2 = 1.369 (rounded to 3 decimal places: s _190-275(5))

Indexed acquisition (1st element) costs: $95,000 x 1.369 = $ 130, 055

There are no other elements to the cost base.

Capital proceeds $ 170,000 s 116-40

less indexed cost base ($ 130,055) s 114-1

Indexed capital gain $ 39,945 s104-10(4)

We would want to consider if the discount method is available and whether gives better result.

Calculating Janice’s net capital gain:

Div 115 eligibility

criteria

Rare book (from set of

3)

$159,900 on

Investment House

$340,000 on Telstra

Shares

$75,000 Springwood

Property (House only)

10

30 June 2019

68.7 /50.2 = 1.369 (rounded to 3 decimal places: s _190-275(5))

Indexed acquisition (1st element) costs: $95,000 x 1.369 = $ 130, 055

There are no other elements to the cost base.

Capital proceeds $ 170,000 s 116-40

less indexed cost base ($ 130,055) s 114-1

Indexed capital gain $ 39,945 s104-10(4)

We would want to consider if the discount method is available and whether gives better result.

Calculating Janice’s net capital gain:

Div 115 eligibility

criteria

Rare book (from set of

3)

$159,900 on

Investment House

$340,000 on Telstra

Shares

$75,000 Springwood

Property (House only)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax Law

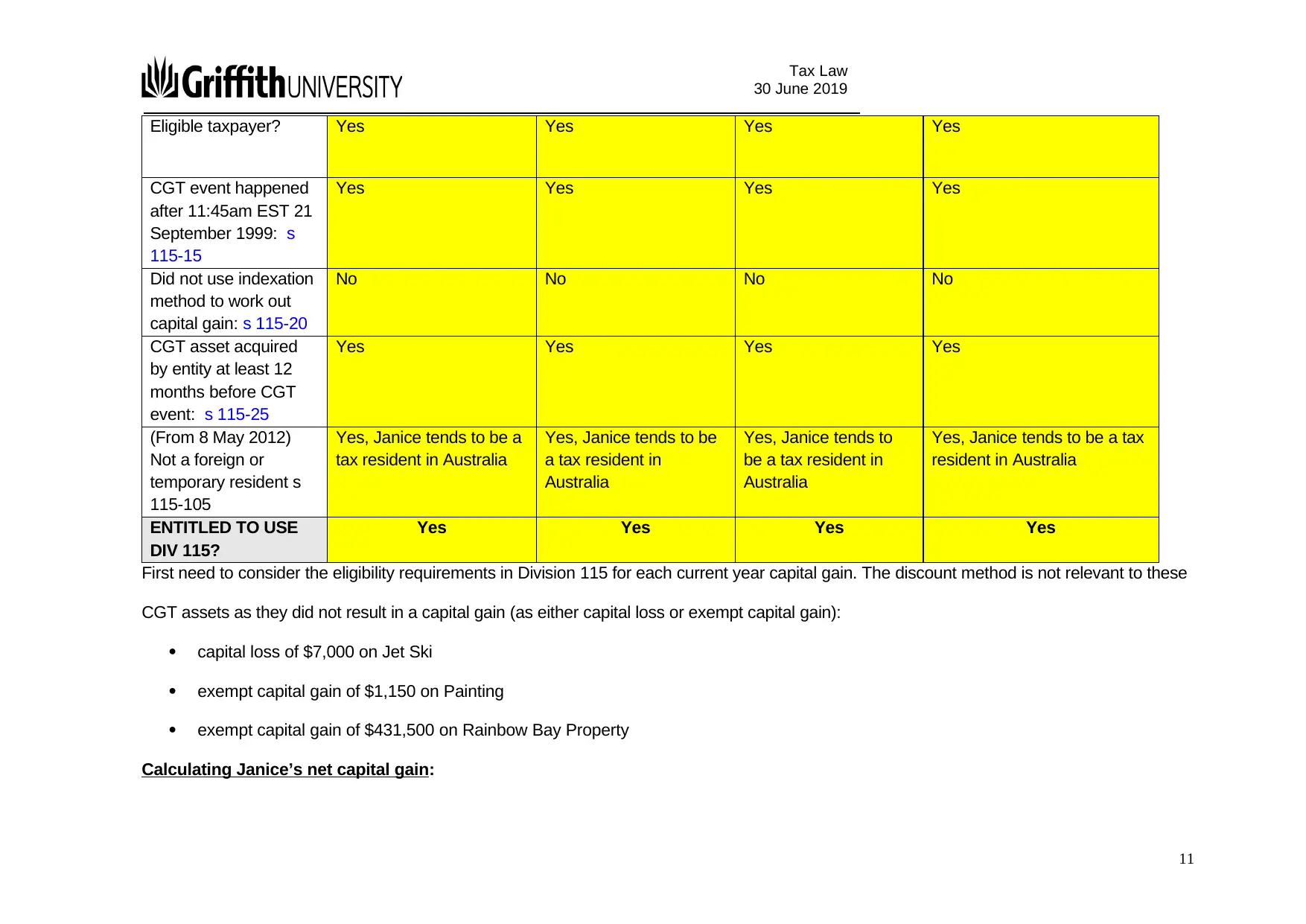

30 June 2019

Eligible taxpayer? Yes Yes Yes Yes

CGT event happened

after 11:45am EST 21

September 1999: s

115-15

Yes Yes Yes Yes

Did not use indexation

method to work out

capital gain: s 115-20

No No No No

CGT asset acquired

by entity at least 12

months before CGT

event: s 115-25

Yes Yes Yes Yes

(From 8 May 2012)

Not a foreign or

temporary resident s

115-105

Yes, Janice tends to be a

tax resident in Australia

Yes, Janice tends to be

a tax resident in

Australia

Yes, Janice tends to

be a tax resident in

Australia

Yes, Janice tends to be a tax

resident in Australia

ENTITLED TO USE

DIV 115?

Yes Yes Yes Yes

First need to consider the eligibility requirements in Division 115 for each current year capital gain. The discount method is not relevant to these

CGT assets as they did not result in a capital gain (as either capital loss or exempt capital gain):

capital loss of $7,000 on Jet Ski

exempt capital gain of $1,150 on Painting

exempt capital gain of $431,500 on Rainbow Bay Property

Calculating Janice’s net capital gain:

11

30 June 2019

Eligible taxpayer? Yes Yes Yes Yes

CGT event happened

after 11:45am EST 21

September 1999: s

115-15

Yes Yes Yes Yes

Did not use indexation

method to work out

capital gain: s 115-20

No No No No

CGT asset acquired

by entity at least 12

months before CGT

event: s 115-25

Yes Yes Yes Yes

(From 8 May 2012)

Not a foreign or

temporary resident s

115-105

Yes, Janice tends to be a

tax resident in Australia

Yes, Janice tends to be

a tax resident in

Australia

Yes, Janice tends to

be a tax resident in

Australia

Yes, Janice tends to be a tax

resident in Australia

ENTITLED TO USE

DIV 115?

Yes Yes Yes Yes

First need to consider the eligibility requirements in Division 115 for each current year capital gain. The discount method is not relevant to these

CGT assets as they did not result in a capital gain (as either capital loss or exempt capital gain):

capital loss of $7,000 on Jet Ski

exempt capital gain of $1,150 on Painting

exempt capital gain of $431,500 on Rainbow Bay Property

Calculating Janice’s net capital gain:

11

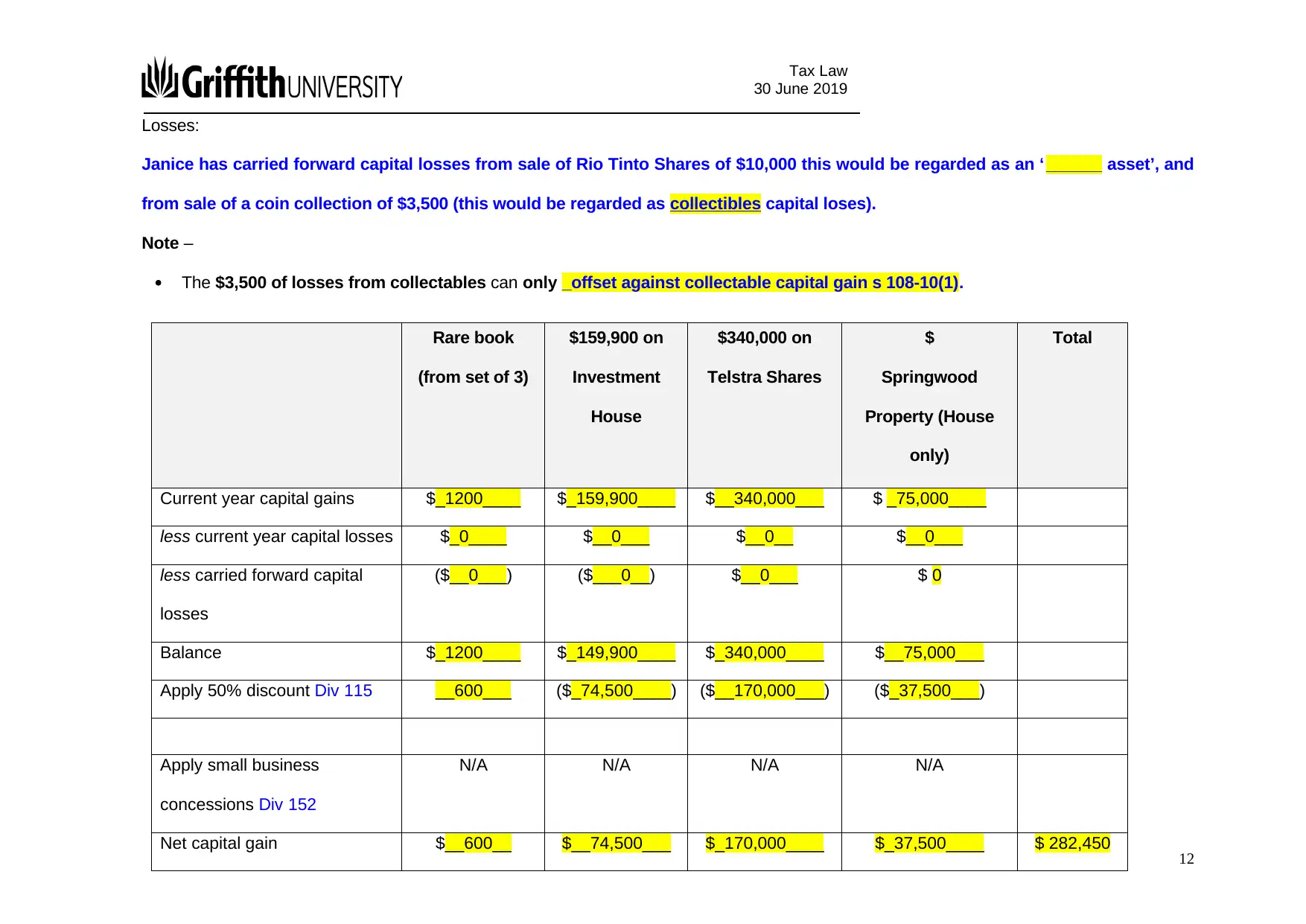

Tax Law

30 June 2019

Losses:

Janice has carried forward capital losses from sale of Rio Tinto Shares of $10,000 this would be regarded as an ‘ ______ asset’, and

from sale of a coin collection of $3,500 (this would be regarded as collectibles capital loses).

Note –

The $3,500 of losses from collectables can only _offset against collectable capital gain s 108-10(1).

Rare book

(from set of 3)

$159,900 on

Investment

House

$340,000 on

Telstra Shares

$

Springwood

Property (House

only)

Total

Current year capital gains $_1200____ $_159,900____ $__340,000___ $ _75,000____

less current year capital losses $_0____ $__0___ $__0__ $__0___

less carried forward capital

losses

($__0___) ($___0__) $__0___ $ 0

Balance $_1200____ $_149,900____ $_340,000____ $__75,000___

Apply 50% discount Div 115 __600___ ($_74,500____) ($__170,000___) ($_37,500___)

Apply small business

concessions Div 152

N/A N/A N/A N/A

Net capital gain $__600__ $__74,500___ $_170,000____ $_37,500____ $ 282,450 12

30 June 2019

Losses:

Janice has carried forward capital losses from sale of Rio Tinto Shares of $10,000 this would be regarded as an ‘ ______ asset’, and

from sale of a coin collection of $3,500 (this would be regarded as collectibles capital loses).

Note –

The $3,500 of losses from collectables can only _offset against collectable capital gain s 108-10(1).

Rare book

(from set of 3)

$159,900 on

Investment

House

$340,000 on

Telstra Shares

$

Springwood

Property (House

only)

Total

Current year capital gains $_1200____ $_159,900____ $__340,000___ $ _75,000____

less current year capital losses $_0____ $__0___ $__0__ $__0___

less carried forward capital

losses

($__0___) ($___0__) $__0___ $ 0

Balance $_1200____ $_149,900____ $_340,000____ $__75,000___

Apply 50% discount Div 115 __600___ ($_74,500____) ($__170,000___) ($_37,500___)

Apply small business

concessions Div 152

N/A N/A N/A N/A

Net capital gain $__600__ $__74,500___ $_170,000____ $_37,500____ $ 282,450 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.