Corporate Accounting: Financial Analysis of JB Hi-Fi & Harvey Norman

VerifiedAdded on 2023/06/05

|22

|3443

|251

Report

AI Summary

This report provides a comparative financial analysis of JB Hi-Fi and Harvey Norman Holdings Limited, two major players in the Australian retail industry. It examines key aspects of their financial statements, including owners' equity, debt-equity ratio, cash flow statements, and other comprehensive income. The report analyzes the companies' financial positions, investment activities, and tax implications, highlighting differences in their financial strategies and performance. The analysis covers key metrics such as effective tax rates and provides insights into the companies' debt management and profitability. This document is available on Desklib, a platform offering a wealth of study resources for students.

HI5020 Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

Globalisation has brought all the organisations of the world on a common parlance.

There is a need to make the corporate reporting open and transparent. The current report is

based to highlight the same requirement. The two big competing corporations in the retailing

industry in Australia, JB Hi-Fi and Harvey Norman Holdings Limited are taken as the

reference companies for this assignment.

2

Globalisation has brought all the organisations of the world on a common parlance.

There is a need to make the corporate reporting open and transparent. The current report is

based to highlight the same requirement. The two big competing corporations in the retailing

industry in Australia, JB Hi-Fi and Harvey Norman Holdings Limited are taken as the

reference companies for this assignment.

2

Table of Contents

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................3

JB HI-FI LIMITED....................................................................................................................4

HARVEY NORMAN LIMITED...............................................................................................4

OWNERS’ EQUITY..................................................................................................................4

QUESTION (i)...........................................................................................................................4

QUESTION (ii)..........................................................................................................................5

CASH FLOW STATEMENT....................................................................................................5

QUESTION (iii).........................................................................................................................5

QUESTION (iv).........................................................................................................................7

QUESTION (v)..........................................................................................................................8

OTHER COMPREHENSIVE INCOME STATEMENT..........................................................8

QUESTION (vi).........................................................................................................................8

QUESTION (vii)........................................................................................................................9

QUESTION (viii).......................................................................................................................9

QUESTION (ix).......................................................................................................................10

ACCOUNTING FOR CORPORATE INCOME TAX............................................................10

QUESTION (x)........................................................................................................................10

QUESTION (xi).......................................................................................................................10

3

EXECUTIVE SUMMARY........................................................................................................2

INTRODUCTION......................................................................................................................3

JB HI-FI LIMITED....................................................................................................................4

HARVEY NORMAN LIMITED...............................................................................................4

OWNERS’ EQUITY..................................................................................................................4

QUESTION (i)...........................................................................................................................4

QUESTION (ii)..........................................................................................................................5

CASH FLOW STATEMENT....................................................................................................5

QUESTION (iii).........................................................................................................................5

QUESTION (iv).........................................................................................................................7

QUESTION (v)..........................................................................................................................8

OTHER COMPREHENSIVE INCOME STATEMENT..........................................................8

QUESTION (vi).........................................................................................................................8

QUESTION (vii)........................................................................................................................9

QUESTION (viii).......................................................................................................................9

QUESTION (ix).......................................................................................................................10

ACCOUNTING FOR CORPORATE INCOME TAX............................................................10

QUESTION (x)........................................................................................................................10

QUESTION (xi).......................................................................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION (xii)......................................................................................................................10

QUESTION (xiii).....................................................................................................................11

QUESTION (xiv).....................................................................................................................11

QUESTION (xv)......................................................................................................................11

QUESTION (xvi).....................................................................................................................11

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................12

4

QUESTION (xiii).....................................................................................................................11

QUESTION (xiv).....................................................................................................................11

QUESTION (xv)......................................................................................................................11

QUESTION (xvi).....................................................................................................................11

CONCLUSION........................................................................................................................12

REFERENCES.........................................................................................................................12

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

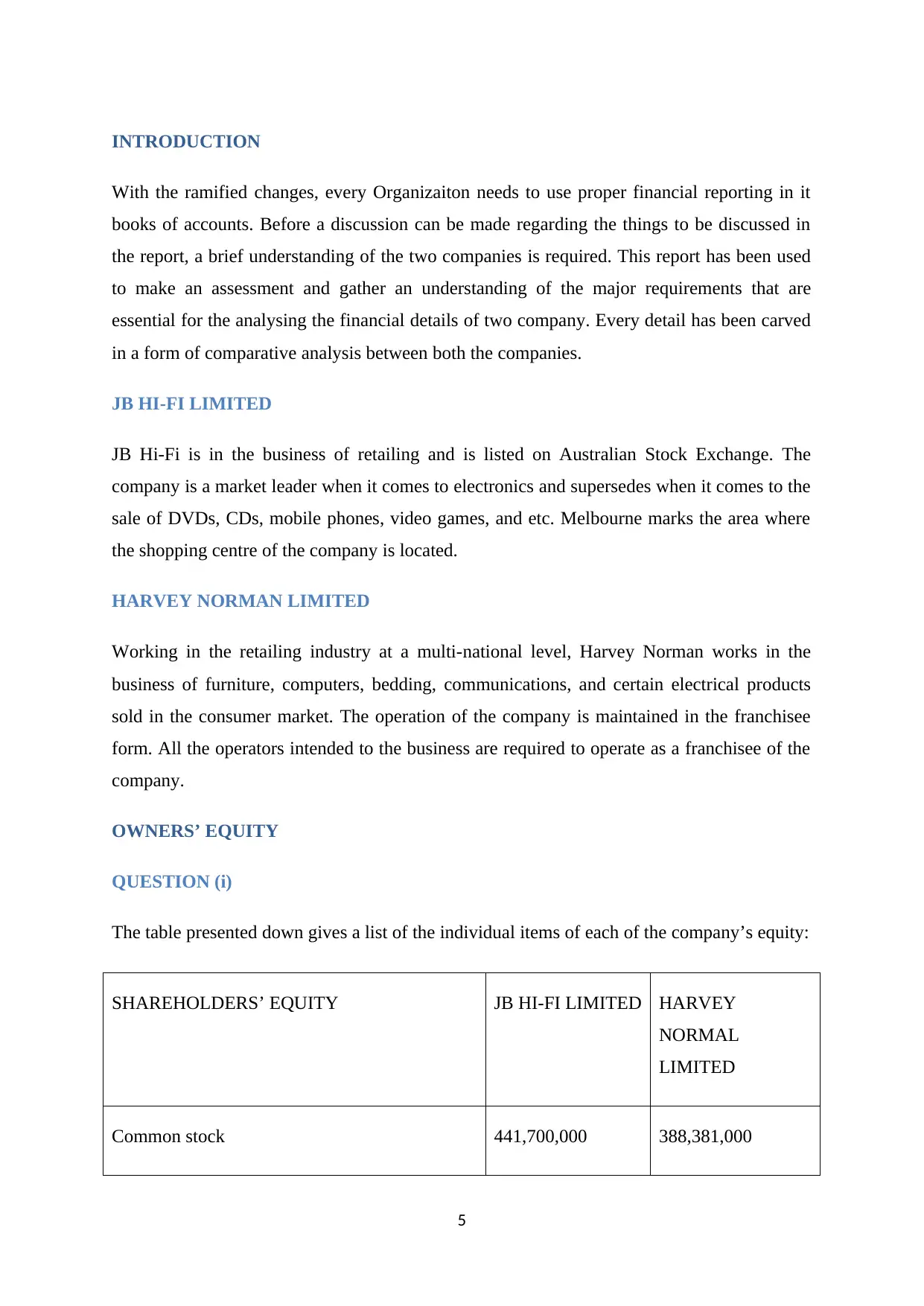

INTRODUCTION

With the ramified changes, every Organizaiton needs to use proper financial reporting in it

books of accounts. Before a discussion can be made regarding the things to be discussed in

the report, a brief understanding of the two companies is required. This report has been used

to make an assessment and gather an understanding of the major requirements that are

essential for the analysing the financial details of two company. Every detail has been carved

in a form of comparative analysis between both the companies.

JB HI-FI LIMITED

JB Hi-Fi is in the business of retailing and is listed on Australian Stock Exchange. The

company is a market leader when it comes to electronics and supersedes when it comes to the

sale of DVDs, CDs, mobile phones, video games, and etc. Melbourne marks the area where

the shopping centre of the company is located.

HARVEY NORMAN LIMITED

Working in the retailing industry at a multi-national level, Harvey Norman works in the

business of furniture, computers, bedding, communications, and certain electrical products

sold in the consumer market. The operation of the company is maintained in the franchisee

form. All the operators intended to the business are required to operate as a franchisee of the

company.

OWNERS’ EQUITY

QUESTION (i)

The table presented down gives a list of the individual items of each of the company’s equity:

SHAREHOLDERS’ EQUITY JB HI-FI LIMITED HARVEY

NORMAL

LIMITED

Common stock 441,700,000 388,381,000

5

With the ramified changes, every Organizaiton needs to use proper financial reporting in it

books of accounts. Before a discussion can be made regarding the things to be discussed in

the report, a brief understanding of the two companies is required. This report has been used

to make an assessment and gather an understanding of the major requirements that are

essential for the analysing the financial details of two company. Every detail has been carved

in a form of comparative analysis between both the companies.

JB HI-FI LIMITED

JB Hi-Fi is in the business of retailing and is listed on Australian Stock Exchange. The

company is a market leader when it comes to electronics and supersedes when it comes to the

sale of DVDs, CDs, mobile phones, video games, and etc. Melbourne marks the area where

the shopping centre of the company is located.

HARVEY NORMAN LIMITED

Working in the retailing industry at a multi-national level, Harvey Norman works in the

business of furniture, computers, bedding, communications, and certain electrical products

sold in the consumer market. The operation of the company is maintained in the franchisee

form. All the operators intended to the business are required to operate as a franchisee of the

company.

OWNERS’ EQUITY

QUESTION (i)

The table presented down gives a list of the individual items of each of the company’s equity:

SHAREHOLDERS’ EQUITY JB HI-FI LIMITED HARVEY

NORMAL

LIMITED

Common stock 441,700,000 388,381,000

5

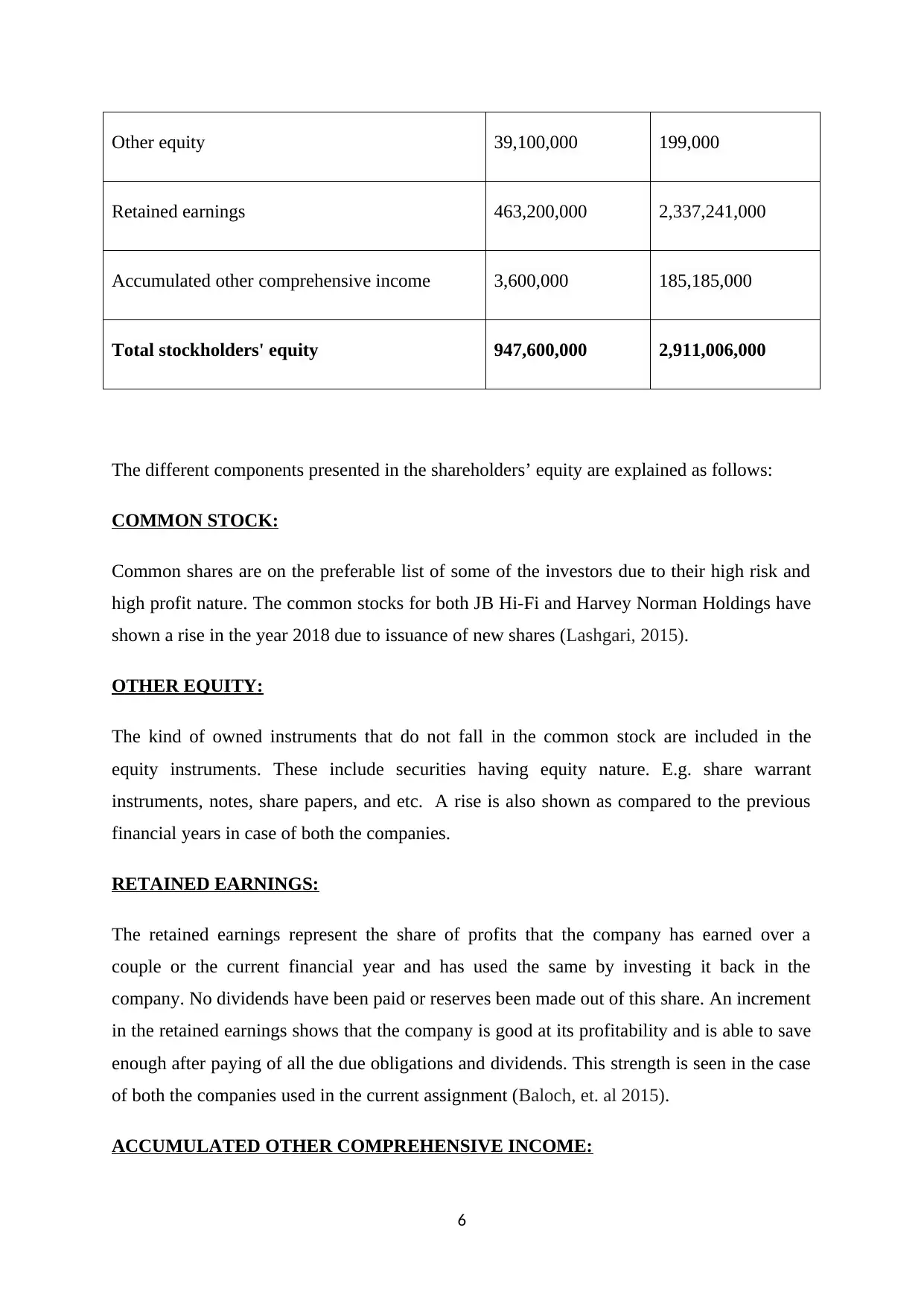

Other equity 39,100,000 199,000

Retained earnings 463,200,000 2,337,241,000

Accumulated other comprehensive income 3,600,000 185,185,000

Total stockholders' equity 947,600,000 2,911,006,000

The different components presented in the shareholders’ equity are explained as follows:

COMMON STOCK:

Common shares are on the preferable list of some of the investors due to their high risk and

high profit nature. The common stocks for both JB Hi-Fi and Harvey Norman Holdings have

shown a rise in the year 2018 due to issuance of new shares (Lashgari, 2015).

OTHER EQUITY:

The kind of owned instruments that do not fall in the common stock are included in the

equity instruments. These include securities having equity nature. E.g. share warrant

instruments, notes, share papers, and etc. A rise is also shown as compared to the previous

financial years in case of both the companies.

RETAINED EARNINGS:

The retained earnings represent the share of profits that the company has earned over a

couple or the current financial year and has used the same by investing it back in the

company. No dividends have been paid or reserves been made out of this share. An increment

in the retained earnings shows that the company is good at its profitability and is able to save

enough after paying of all the due obligations and dividends. This strength is seen in the case

of both the companies used in the current assignment (Baloch, et. al 2015).

ACCUMULATED OTHER COMPREHENSIVE INCOME:

6

Retained earnings 463,200,000 2,337,241,000

Accumulated other comprehensive income 3,600,000 185,185,000

Total stockholders' equity 947,600,000 2,911,006,000

The different components presented in the shareholders’ equity are explained as follows:

COMMON STOCK:

Common shares are on the preferable list of some of the investors due to their high risk and

high profit nature. The common stocks for both JB Hi-Fi and Harvey Norman Holdings have

shown a rise in the year 2018 due to issuance of new shares (Lashgari, 2015).

OTHER EQUITY:

The kind of owned instruments that do not fall in the common stock are included in the

equity instruments. These include securities having equity nature. E.g. share warrant

instruments, notes, share papers, and etc. A rise is also shown as compared to the previous

financial years in case of both the companies.

RETAINED EARNINGS:

The retained earnings represent the share of profits that the company has earned over a

couple or the current financial year and has used the same by investing it back in the

company. No dividends have been paid or reserves been made out of this share. An increment

in the retained earnings shows that the company is good at its profitability and is able to save

enough after paying of all the due obligations and dividends. This strength is seen in the case

of both the companies used in the current assignment (Baloch, et. al 2015).

ACCUMULATED OTHER COMPREHENSIVE INCOME:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This shows the total of unrealised losses and gains that have been reported by the

organisation for the current and/or previous financial years. For the JB Hi-Fi limited, the total

of the accumulated other comprehensive income has shown a decline, but for the Harvey

Norman Holdings Limited, the same has risen (Black, 2016).

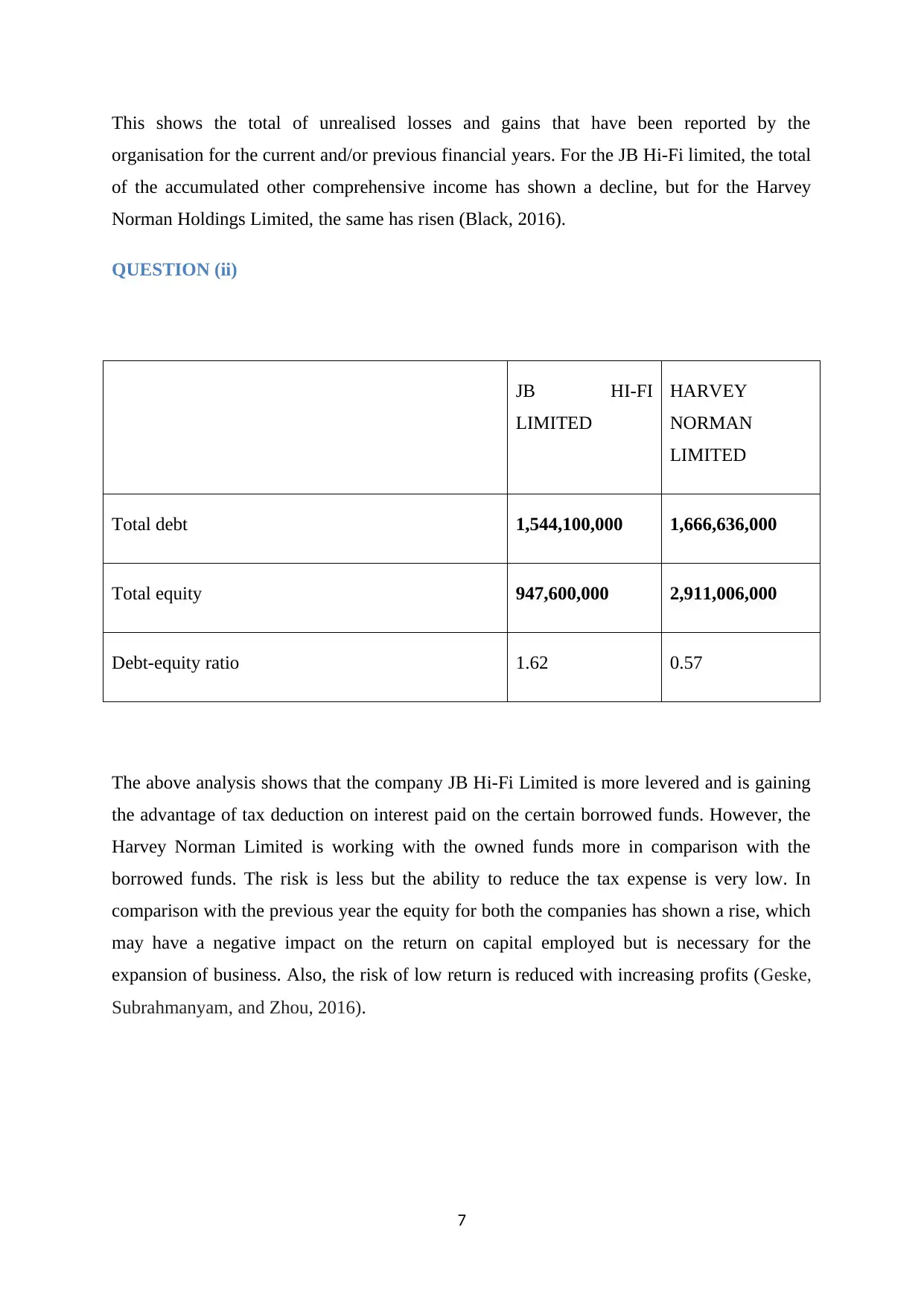

QUESTION (ii)

JB HI-FI

LIMITED

HARVEY

NORMAN

LIMITED

Total debt 1,544,100,000 1,666,636,000

Total equity 947,600,000 2,911,006,000

Debt-equity ratio 1.62 0.57

The above analysis shows that the company JB Hi-Fi Limited is more levered and is gaining

the advantage of tax deduction on interest paid on the certain borrowed funds. However, the

Harvey Norman Limited is working with the owned funds more in comparison with the

borrowed funds. The risk is less but the ability to reduce the tax expense is very low. In

comparison with the previous year the equity for both the companies has shown a rise, which

may have a negative impact on the return on capital employed but is necessary for the

expansion of business. Also, the risk of low return is reduced with increasing profits (Geske,

Subrahmanyam, and Zhou, 2016).

7

organisation for the current and/or previous financial years. For the JB Hi-Fi limited, the total

of the accumulated other comprehensive income has shown a decline, but for the Harvey

Norman Holdings Limited, the same has risen (Black, 2016).

QUESTION (ii)

JB HI-FI

LIMITED

HARVEY

NORMAN

LIMITED

Total debt 1,544,100,000 1,666,636,000

Total equity 947,600,000 2,911,006,000

Debt-equity ratio 1.62 0.57

The above analysis shows that the company JB Hi-Fi Limited is more levered and is gaining

the advantage of tax deduction on interest paid on the certain borrowed funds. However, the

Harvey Norman Limited is working with the owned funds more in comparison with the

borrowed funds. The risk is less but the ability to reduce the tax expense is very low. In

comparison with the previous year the equity for both the companies has shown a rise, which

may have a negative impact on the return on capital employed but is necessary for the

expansion of business. Also, the risk of low return is reduced with increasing profits (Geske,

Subrahmanyam, and Zhou, 2016).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CASH FLOW STATEMENT

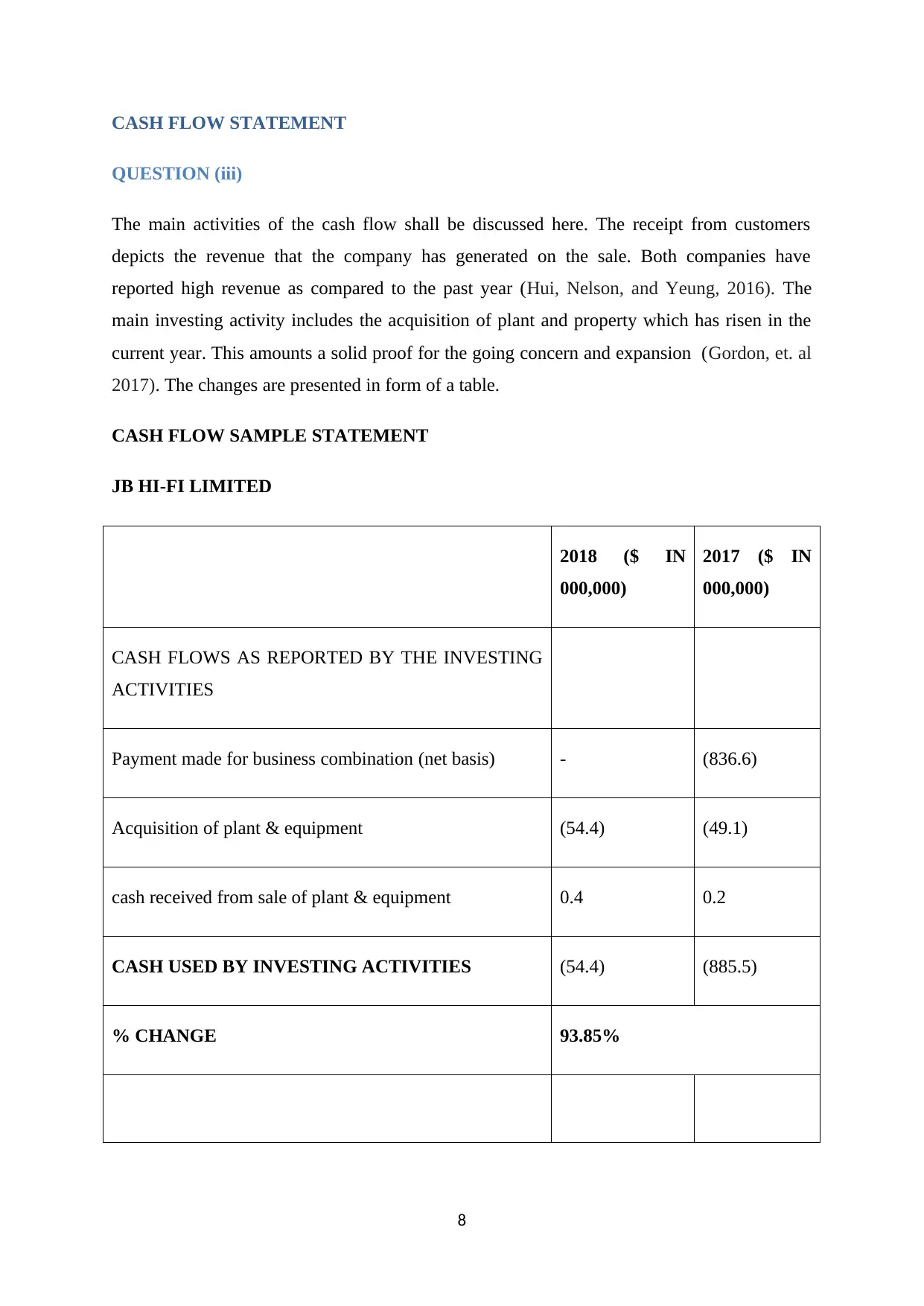

QUESTION (iii)

The main activities of the cash flow shall be discussed here. The receipt from customers

depicts the revenue that the company has generated on the sale. Both companies have

reported high revenue as compared to the past year (Hui, Nelson, and Yeung, 2016). The

main investing activity includes the acquisition of plant and property which has risen in the

current year. This amounts a solid proof for the going concern and expansion (Gordon, et. al

2017). The changes are presented in form of a table.

CASH FLOW SAMPLE STATEMENT

JB HI-FI LIMITED

2018 ($ IN

000,000)

2017 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE INVESTING

ACTIVITIES

Payment made for business combination (net basis) - (836.6)

Acquisition of plant & equipment (54.4) (49.1)

cash received from sale of plant & equipment 0.4 0.2

CASH USED BY INVESTING ACTIVITIES (54.4) (885.5)

% CHANGE 93.85%

8

QUESTION (iii)

The main activities of the cash flow shall be discussed here. The receipt from customers

depicts the revenue that the company has generated on the sale. Both companies have

reported high revenue as compared to the past year (Hui, Nelson, and Yeung, 2016). The

main investing activity includes the acquisition of plant and property which has risen in the

current year. This amounts a solid proof for the going concern and expansion (Gordon, et. al

2017). The changes are presented in form of a table.

CASH FLOW SAMPLE STATEMENT

JB HI-FI LIMITED

2018 ($ IN

000,000)

2017 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE INVESTING

ACTIVITIES

Payment made for business combination (net basis) - (836.6)

Acquisition of plant & equipment (54.4) (49.1)

cash received from sale of plant & equipment 0.4 0.2

CASH USED BY INVESTING ACTIVITIES (54.4) (885.5)

% CHANGE 93.85%

8

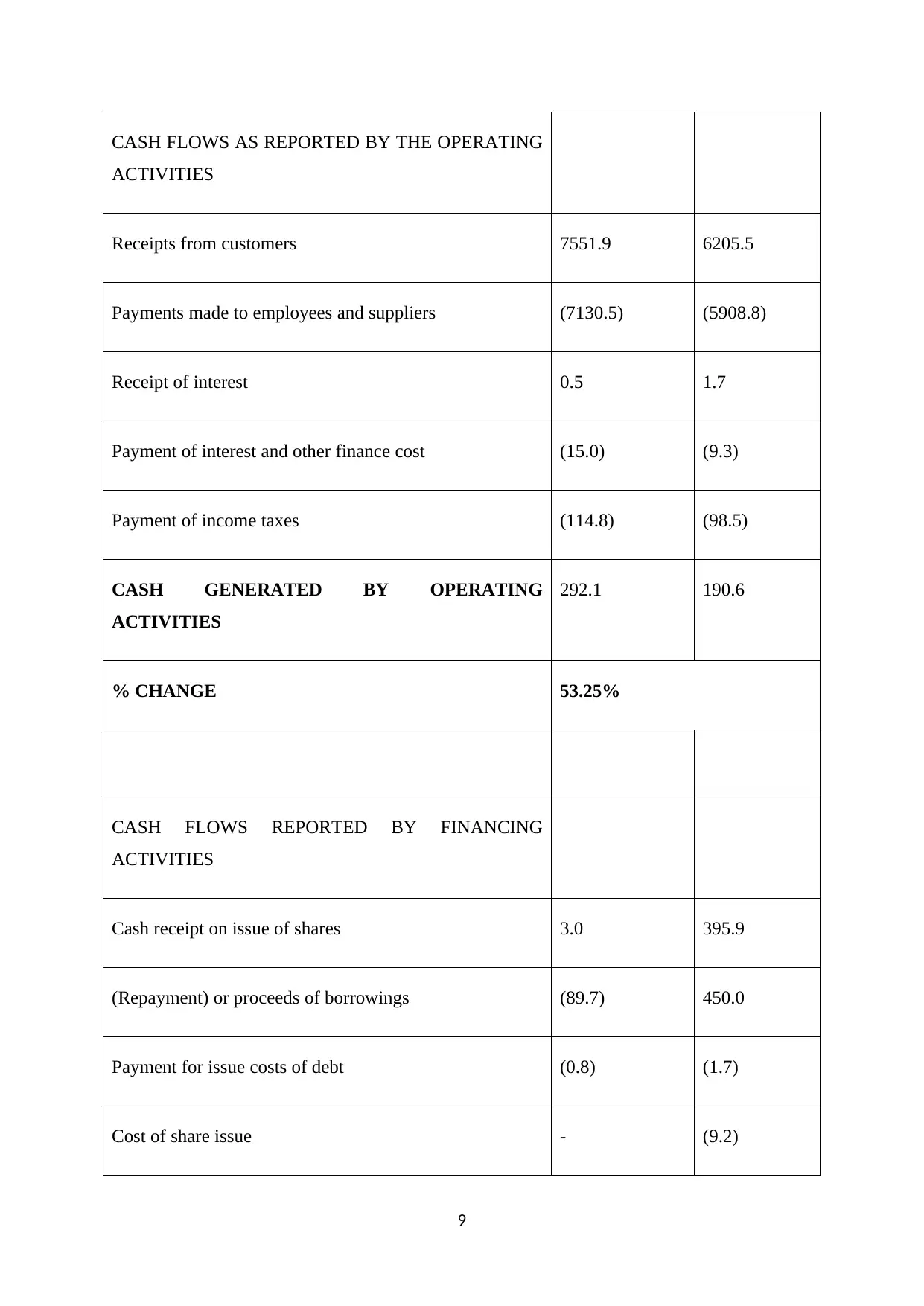

CASH FLOWS AS REPORTED BY THE OPERATING

ACTIVITIES

Receipts from customers 7551.9 6205.5

Payments made to employees and suppliers (7130.5) (5908.8)

Receipt of interest 0.5 1.7

Payment of interest and other finance cost (15.0) (9.3)

Payment of income taxes (114.8) (98.5)

CASH GENERATED BY OPERATING

ACTIVITIES

292.1 190.6

% CHANGE 53.25%

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 3.0 395.9

(Repayment) or proceeds of borrowings (89.7) 450.0

Payment for issue costs of debt (0.8) (1.7)

Cost of share issue - (9.2)

9

ACTIVITIES

Receipts from customers 7551.9 6205.5

Payments made to employees and suppliers (7130.5) (5908.8)

Receipt of interest 0.5 1.7

Payment of interest and other finance cost (15.0) (9.3)

Payment of income taxes (114.8) (98.5)

CASH GENERATED BY OPERATING

ACTIVITIES

292.1 190.6

% CHANGE 53.25%

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 3.0 395.9

(Repayment) or proceeds of borrowings (89.7) 450.0

Payment for issue costs of debt (0.8) (1.7)

Cost of share issue - (9.2)

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

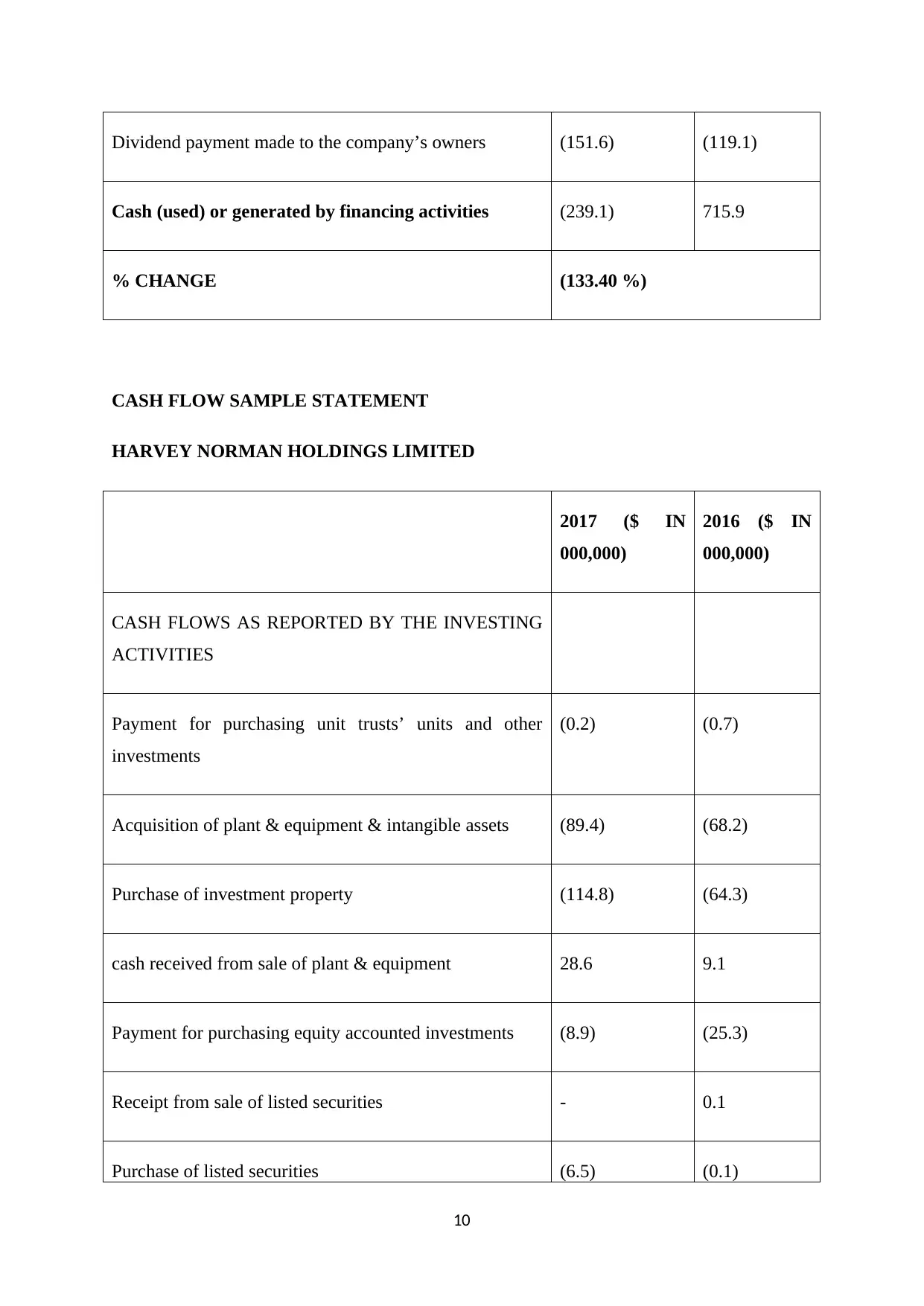

Dividend payment made to the company’s owners (151.6) (119.1)

Cash (used) or generated by financing activities (239.1) 715.9

% CHANGE (133.40 %)

CASH FLOW SAMPLE STATEMENT

HARVEY NORMAN HOLDINGS LIMITED

2017 ($ IN

000,000)

2016 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE INVESTING

ACTIVITIES

Payment for purchasing unit trusts’ units and other

investments

(0.2) (0.7)

Acquisition of plant & equipment & intangible assets (89.4) (68.2)

Purchase of investment property (114.8) (64.3)

cash received from sale of plant & equipment 28.6 9.1

Payment for purchasing equity accounted investments (8.9) (25.3)

Receipt from sale of listed securities - 0.1

Purchase of listed securities (6.5) (0.1)

10

Cash (used) or generated by financing activities (239.1) 715.9

% CHANGE (133.40 %)

CASH FLOW SAMPLE STATEMENT

HARVEY NORMAN HOLDINGS LIMITED

2017 ($ IN

000,000)

2016 ($ IN

000,000)

CASH FLOWS AS REPORTED BY THE INVESTING

ACTIVITIES

Payment for purchasing unit trusts’ units and other

investments

(0.2) (0.7)

Acquisition of plant & equipment & intangible assets (89.4) (68.2)

Purchase of investment property (114.8) (64.3)

cash received from sale of plant & equipment 28.6 9.1

Payment for purchasing equity accounted investments (8.9) (25.3)

Receipt from sale of listed securities - 0.1

Purchase of listed securities (6.5) (0.1)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

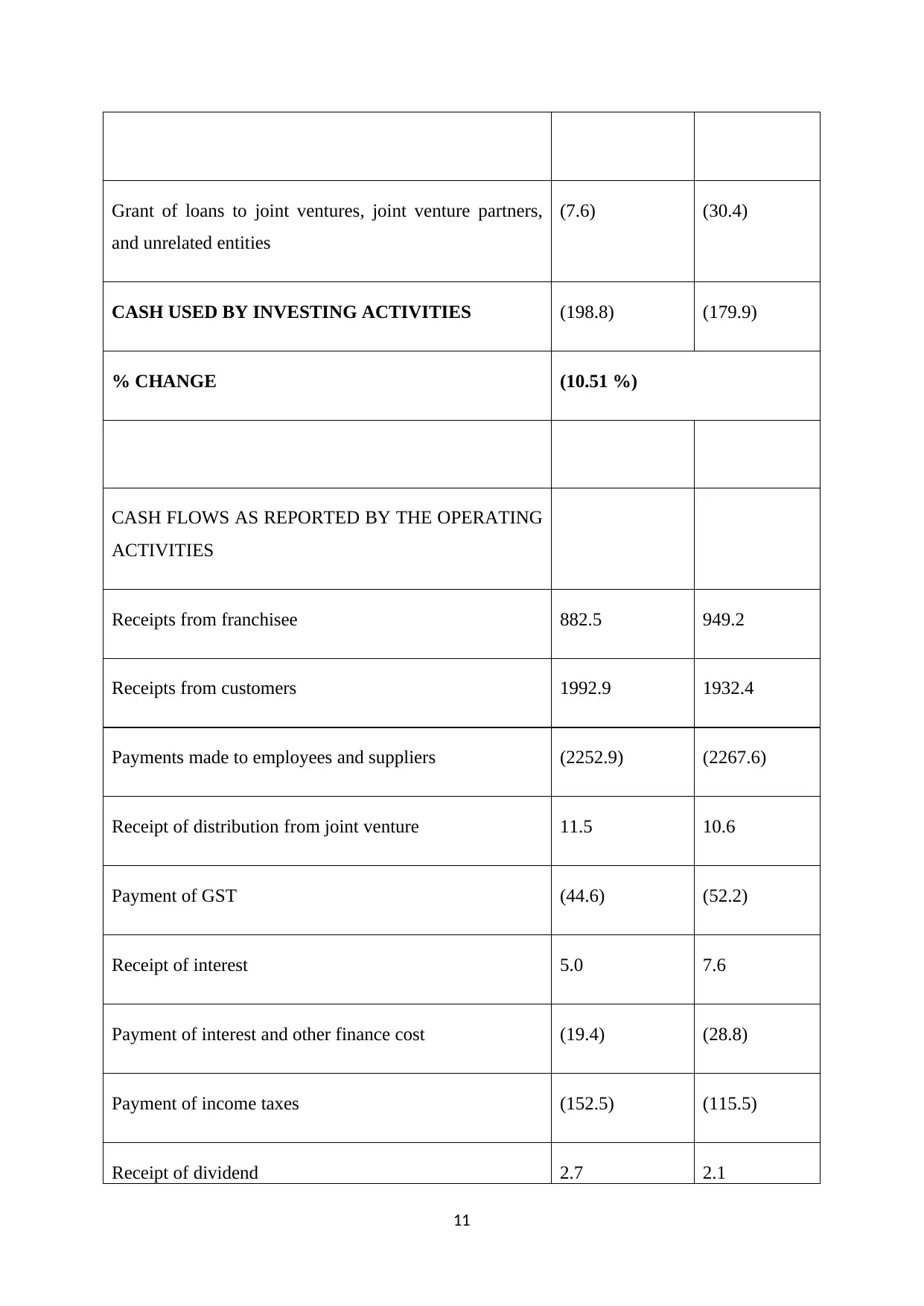

Grant of loans to joint ventures, joint venture partners,

and unrelated entities

(7.6) (30.4)

CASH USED BY INVESTING ACTIVITIES (198.8) (179.9)

% CHANGE (10.51 %)

CASH FLOWS AS REPORTED BY THE OPERATING

ACTIVITIES

Receipts from franchisee 882.5 949.2

Receipts from customers 1992.9 1932.4

Payments made to employees and suppliers (2252.9) (2267.6)

Receipt of distribution from joint venture 11.5 10.6

Payment of GST (44.6) (52.2)

Receipt of interest 5.0 7.6

Payment of interest and other finance cost (19.4) (28.8)

Payment of income taxes (152.5) (115.5)

Receipt of dividend 2.7 2.1

11

and unrelated entities

(7.6) (30.4)

CASH USED BY INVESTING ACTIVITIES (198.8) (179.9)

% CHANGE (10.51 %)

CASH FLOWS AS REPORTED BY THE OPERATING

ACTIVITIES

Receipts from franchisee 882.5 949.2

Receipts from customers 1992.9 1932.4

Payments made to employees and suppliers (2252.9) (2267.6)

Receipt of distribution from joint venture 11.5 10.6

Payment of GST (44.6) (52.2)

Receipt of interest 5.0 7.6

Payment of interest and other finance cost (19.4) (28.8)

Payment of income taxes (152.5) (115.5)

Receipt of dividend 2.7 2.1

11

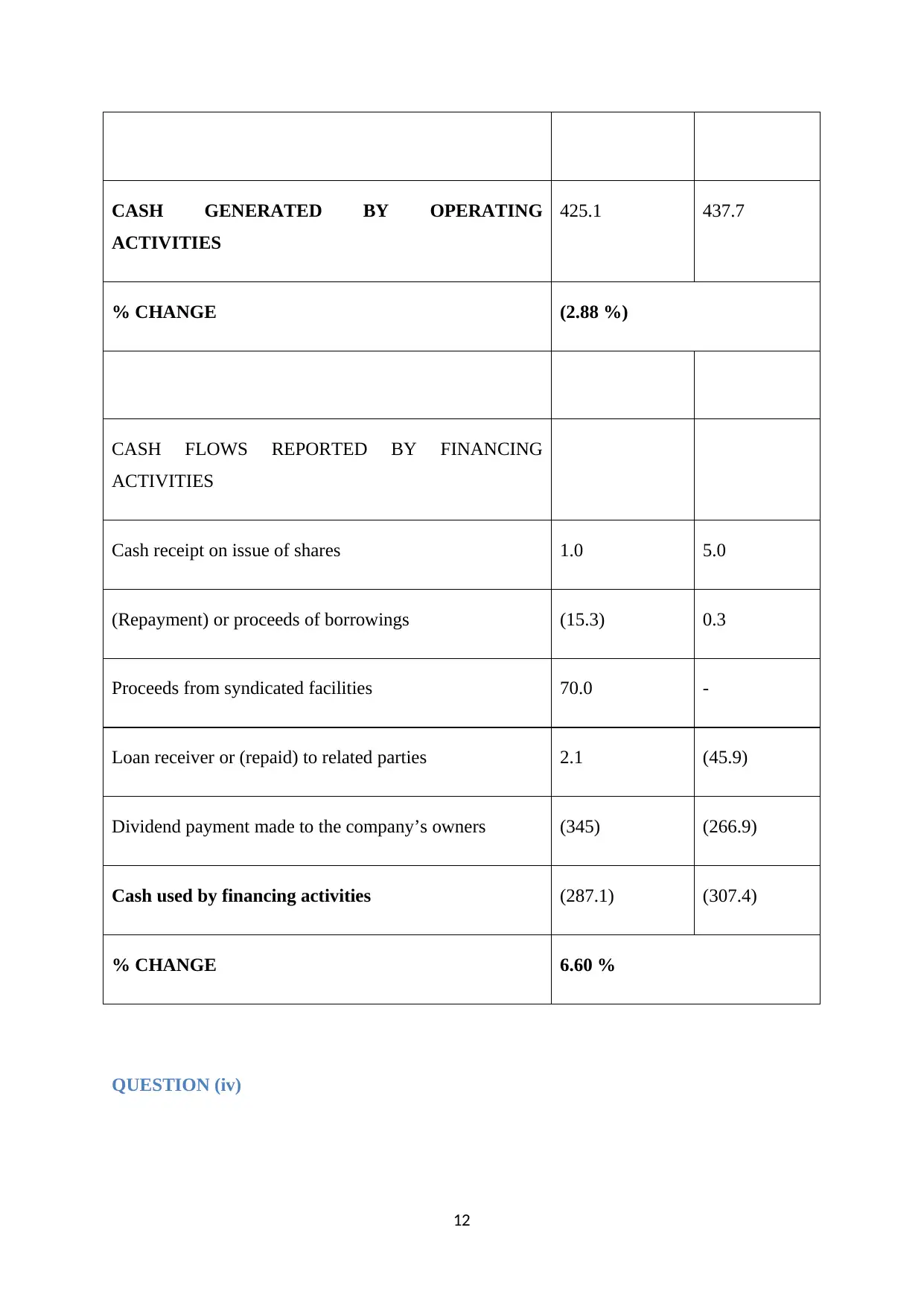

CASH GENERATED BY OPERATING

ACTIVITIES

425.1 437.7

% CHANGE (2.88 %)

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 1.0 5.0

(Repayment) or proceeds of borrowings (15.3) 0.3

Proceeds from syndicated facilities 70.0 -

Loan receiver or (repaid) to related parties 2.1 (45.9)

Dividend payment made to the company’s owners (345) (266.9)

Cash used by financing activities (287.1) (307.4)

% CHANGE 6.60 %

QUESTION (iv)

12

ACTIVITIES

425.1 437.7

% CHANGE (2.88 %)

CASH FLOWS REPORTED BY FINANCING

ACTIVITIES

Cash receipt on issue of shares 1.0 5.0

(Repayment) or proceeds of borrowings (15.3) 0.3

Proceeds from syndicated facilities 70.0 -

Loan receiver or (repaid) to related parties 2.1 (45.9)

Dividend payment made to the company’s owners (345) (266.9)

Cash used by financing activities (287.1) (307.4)

% CHANGE 6.60 %

QUESTION (iv)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.