Corporate Accounting Project: JB HI FI & Kathmandu Analysis

VerifiedAdded on 2023/06/04

|18

|4162

|266

Report

AI Summary

This report presents a corporate accounting study comparing JB HI FI and Kathmandu Limited, two Australian retail companies. It examines owner's equity, cash flow statements, other comprehensive income, and corporate income tax accounting. The analysis includes comparative assessments of equity items, debt-equity positions, cash flow statement items, and comprehensive income statement components. Managerial performance and effective tax rates are also evaluated. The report concludes by summarizing the key financial similarities and differences between the two companies based on their annual reports.

Running Head: Corporate Accounting

1

Project Report: Corporate Accounting

1

Project Report: Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

2

Executive summary

In the report, the corporate accounting study has been performed on two Australian

companies, JB HI FI and Kathmandu limited. Both the companies are operating their

business under the Australian retail industry. The corporate accountant mainly checks that

whether the company has followed the proper recording and presentation rules of AASB

while showing the financial statement in the annual report of the business. The study explains

that the recording and presentation position of both the companies are similar and thus it was

easier to conduct the study and compare the position of both the companies.

2

Executive summary

In the report, the corporate accounting study has been performed on two Australian

companies, JB HI FI and Kathmandu limited. Both the companies are operating their

business under the Australian retail industry. The corporate accountant mainly checks that

whether the company has followed the proper recording and presentation rules of AASB

while showing the financial statement in the annual report of the business. The study explains

that the recording and presentation position of both the companies are similar and thus it was

easier to conduct the study and compare the position of both the companies.

Corporate Accounting

3

Contents

Introduction of report........................................................................................................4

Company’s introduction...................................................................................................4

Owner’s equity..................................................................................................................5

1.Equity items...............................................................................................................5

2.Debt and equity position............................................................................................6

Cash flow statement..........................................................................................................6

3.Cash flow statement items.........................................................................................6

4.Comparative analysis from last year..........................................................................8

5.Comparative analysis among the companies.............................................................9

Other comprehensive income statement...........................................................................9

6.Comprehensive income statement items.................................................................10

7.Profit and loss statement..........................................................................................10

8.Comparative analysis...............................................................................................11

9.Manager’s performance...........................................................................................12

Accounting for corporate income tax.............................................................................12

10.Tax expenses in annual report...............................................................................12

11.Effective tax rate....................................................................................................12

12.Deferred tax assets and liabilities..........................................................................13

13.Changes in Deferred tax assets and liabilities.......................................................13

14.Cash tax amount....................................................................................................14

15.Calculation of cash tax rate....................................................................................14

16.Book tax rate and cash tax rate..............................................................................15

Conclusion......................................................................................................................15

3

Contents

Introduction of report........................................................................................................4

Company’s introduction...................................................................................................4

Owner’s equity..................................................................................................................5

1.Equity items...............................................................................................................5

2.Debt and equity position............................................................................................6

Cash flow statement..........................................................................................................6

3.Cash flow statement items.........................................................................................6

4.Comparative analysis from last year..........................................................................8

5.Comparative analysis among the companies.............................................................9

Other comprehensive income statement...........................................................................9

6.Comprehensive income statement items.................................................................10

7.Profit and loss statement..........................................................................................10

8.Comparative analysis...............................................................................................11

9.Manager’s performance...........................................................................................12

Accounting for corporate income tax.............................................................................12

10.Tax expenses in annual report...............................................................................12

11.Effective tax rate....................................................................................................12

12.Deferred tax assets and liabilities..........................................................................13

13.Changes in Deferred tax assets and liabilities.......................................................13

14.Cash tax amount....................................................................................................14

15.Calculation of cash tax rate....................................................................................14

16.Book tax rate and cash tax rate..............................................................................15

Conclusion......................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

4

References.......................................................................................................................16

4

References.......................................................................................................................16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

5

Introduction of report:

Corporate accounting is an accounting part which focuses on the annual report of the

business and the other reports which contains the accounting and financial items. The main

operations of corporate accountant is to check that whether the proper recording and

presentation rules of AASB has been followed and applied by the company in order to depict

and present the financial statement in the annual report of the business (Bhasin, 2015). It also

focuses that the proper financial notes about the accounting and financial transaction has been

given in the annual report or not.

The main motto of corporate accounting is to set a similarity among the annual reports

of all the companies so that the shareholder can’t get confuse in the performance and position

of any of the business. The better outcome could be concluded by the shareholders ad other

stakeholders of the business on the basis of the comparison. In the report, JB HI FI and

Kathmandu limited has been taken into the context to perform the corporate accounting

study. Australian retail industry is the industry of the both the firms.

Company’s introduction:

The brief about both the Australian retail firm has been given below:

JB HI FI:

JB HI FI is an Australian retailing company which is operating its business from last

44 years in the Australian market. The main products of the company includes electronic

products, video games, CDs and DVDs, home appliances, hardware product, ultra HB blu

rays etc. the main subsidiary company of JB HI FI is “the good guys” which manages all the

operations and the services of the business (Home, 2018). The company is currently

managing 244 stores and it is horizontally diversifying the product market t improve the

market performance.

KATHMANDU LIMITED:

Kathmandu limited is also an Australian retailing company which is operating its

business from last 31years in the Australian market. It is a transaction chain of retail stores in

the Australian market which offers the travel, adventures and outdoor equipment and the

apparels to its customers. Headquarter of the company is in New Zealand market. The

5

Introduction of report:

Corporate accounting is an accounting part which focuses on the annual report of the

business and the other reports which contains the accounting and financial items. The main

operations of corporate accountant is to check that whether the proper recording and

presentation rules of AASB has been followed and applied by the company in order to depict

and present the financial statement in the annual report of the business (Bhasin, 2015). It also

focuses that the proper financial notes about the accounting and financial transaction has been

given in the annual report or not.

The main motto of corporate accounting is to set a similarity among the annual reports

of all the companies so that the shareholder can’t get confuse in the performance and position

of any of the business. The better outcome could be concluded by the shareholders ad other

stakeholders of the business on the basis of the comparison. In the report, JB HI FI and

Kathmandu limited has been taken into the context to perform the corporate accounting

study. Australian retail industry is the industry of the both the firms.

Company’s introduction:

The brief about both the Australian retail firm has been given below:

JB HI FI:

JB HI FI is an Australian retailing company which is operating its business from last

44 years in the Australian market. The main products of the company includes electronic

products, video games, CDs and DVDs, home appliances, hardware product, ultra HB blu

rays etc. the main subsidiary company of JB HI FI is “the good guys” which manages all the

operations and the services of the business (Home, 2018). The company is currently

managing 244 stores and it is horizontally diversifying the product market t improve the

market performance.

KATHMANDU LIMITED:

Kathmandu limited is also an Australian retailing company which is operating its

business from last 31years in the Australian market. It is a transaction chain of retail stores in

the Australian market which offers the travel, adventures and outdoor equipment and the

apparels to its customers. Headquarter of the company is in New Zealand market. The

Corporate Accounting

6

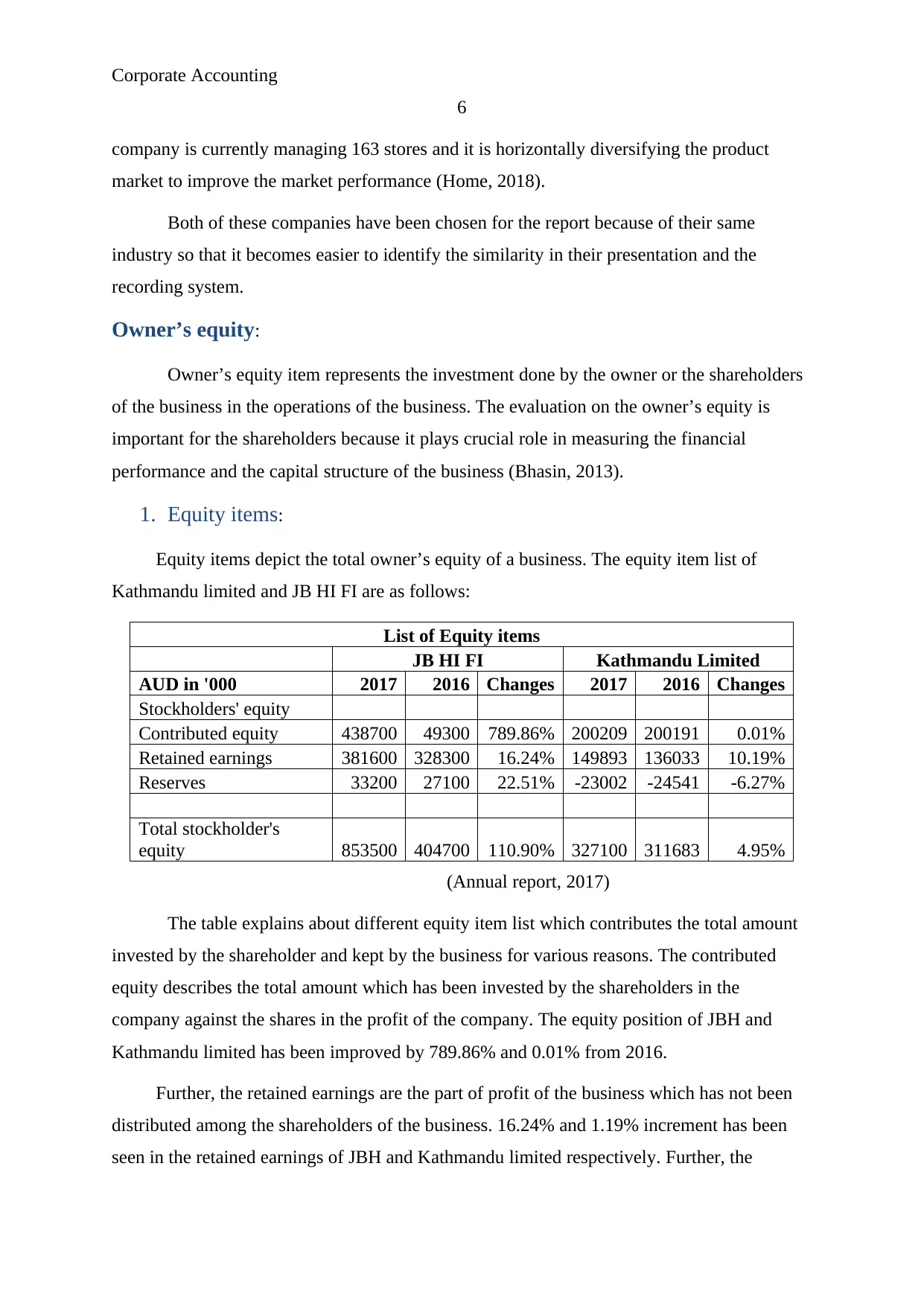

company is currently managing 163 stores and it is horizontally diversifying the product

market to improve the market performance (Home, 2018).

Both of these companies have been chosen for the report because of their same

industry so that it becomes easier to identify the similarity in their presentation and the

recording system.

Owner’s equity:

Owner’s equity item represents the investment done by the owner or the shareholders

of the business in the operations of the business. The evaluation on the owner’s equity is

important for the shareholders because it plays crucial role in measuring the financial

performance and the capital structure of the business (Bhasin, 2013).

1. Equity items:

Equity items depict the total owner’s equity of a business. The equity item list of

Kathmandu limited and JB HI FI are as follows:

List of Equity items

JB HI FI Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Stockholders' equity

Contributed equity 438700 49300 789.86% 200209 200191 0.01%

Retained earnings 381600 328300 16.24% 149893 136033 10.19%

Reserves 33200 27100 22.51% -23002 -24541 -6.27%

Total stockholder's

equity 853500 404700 110.90% 327100 311683 4.95%

(Annual report, 2017)

The table explains about different equity item list which contributes the total amount

invested by the shareholder and kept by the business for various reasons. The contributed

equity describes the total amount which has been invested by the shareholders in the

company against the shares in the profit of the company. The equity position of JBH and

Kathmandu limited has been improved by 789.86% and 0.01% from 2016.

Further, the retained earnings are the part of profit of the business which has not been

distributed among the shareholders of the business. 16.24% and 1.19% increment has been

seen in the retained earnings of JBH and Kathmandu limited respectively. Further, the

6

company is currently managing 163 stores and it is horizontally diversifying the product

market to improve the market performance (Home, 2018).

Both of these companies have been chosen for the report because of their same

industry so that it becomes easier to identify the similarity in their presentation and the

recording system.

Owner’s equity:

Owner’s equity item represents the investment done by the owner or the shareholders

of the business in the operations of the business. The evaluation on the owner’s equity is

important for the shareholders because it plays crucial role in measuring the financial

performance and the capital structure of the business (Bhasin, 2013).

1. Equity items:

Equity items depict the total owner’s equity of a business. The equity item list of

Kathmandu limited and JB HI FI are as follows:

List of Equity items

JB HI FI Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Stockholders' equity

Contributed equity 438700 49300 789.86% 200209 200191 0.01%

Retained earnings 381600 328300 16.24% 149893 136033 10.19%

Reserves 33200 27100 22.51% -23002 -24541 -6.27%

Total stockholder's

equity 853500 404700 110.90% 327100 311683 4.95%

(Annual report, 2017)

The table explains about different equity item list which contributes the total amount

invested by the shareholder and kept by the business for various reasons. The contributed

equity describes the total amount which has been invested by the shareholders in the

company against the shares in the profit of the company. The equity position of JBH and

Kathmandu limited has been improved by 789.86% and 0.01% from 2016.

Further, the retained earnings are the part of profit of the business which has not been

distributed among the shareholders of the business. 16.24% and 1.19% increment has been

seen in the retained earnings of JBH and Kathmandu limited respectively. Further, the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

7

reserves are the provisions which are maintained by the business against any operational risk

of the business (Fan, Gillan and Yu, 2013). The JBH has improved the reserves amount by

22.51% and Kathmandu limited has reduced the level by -6.27%.

2. Debt and equity position:

The debt and equity position mainly depict about the financial gearing position of the

business and the total cost of capital of the business. Through evaluation on the annual report

(2017) of both the companies, it has been found that the JB HI FI is holding a great debt

amount against the equity level of the business which expresses about higher financial

gearing position and lesser cost of the business. Further, the table describes that the debt

position of Kathmandu limited is just 13.67% of total equity of the business which expresses

about lower financial gearing position and higher cost of the business.

Debt and Equity position

JB HI FI Kathmandu Limited

AUD in '000 2017 2017

Long term debt 713000 44723

Equity 853500 327100

Debt / Equity 83.54% 13.67%

(Annual report, 2017)

Cash flow statement:

Cash flow statement, its items and the figures of cash flow statement represent the

total cash which either has been paid by the business or received in order to manage and run

the business activities. The evaluation on the cash flow statement is important for the

stakeholders because it plays crucial role in identifying the cash management capability and

the cash conversion cycle of the business (Bowen, Rajgopal and Venkatachalam, 2008).

3. Cash flow statement items:

The cash flow statement items depict the cash management position and the reason

behind the changes into the cash level of the business. The cash flow statement item list of

Kathmandu limited and JB HI FI are as follows:

7

reserves are the provisions which are maintained by the business against any operational risk

of the business (Fan, Gillan and Yu, 2013). The JBH has improved the reserves amount by

22.51% and Kathmandu limited has reduced the level by -6.27%.

2. Debt and equity position:

The debt and equity position mainly depict about the financial gearing position of the

business and the total cost of capital of the business. Through evaluation on the annual report

(2017) of both the companies, it has been found that the JB HI FI is holding a great debt

amount against the equity level of the business which expresses about higher financial

gearing position and lesser cost of the business. Further, the table describes that the debt

position of Kathmandu limited is just 13.67% of total equity of the business which expresses

about lower financial gearing position and higher cost of the business.

Debt and Equity position

JB HI FI Kathmandu Limited

AUD in '000 2017 2017

Long term debt 713000 44723

Equity 853500 327100

Debt / Equity 83.54% 13.67%

(Annual report, 2017)

Cash flow statement:

Cash flow statement, its items and the figures of cash flow statement represent the

total cash which either has been paid by the business or received in order to manage and run

the business activities. The evaluation on the cash flow statement is important for the

stakeholders because it plays crucial role in identifying the cash management capability and

the cash conversion cycle of the business (Bowen, Rajgopal and Venkatachalam, 2008).

3. Cash flow statement items:

The cash flow statement items depict the cash management position and the reason

behind the changes into the cash level of the business. The cash flow statement item list of

Kathmandu limited and JB HI FI are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

8

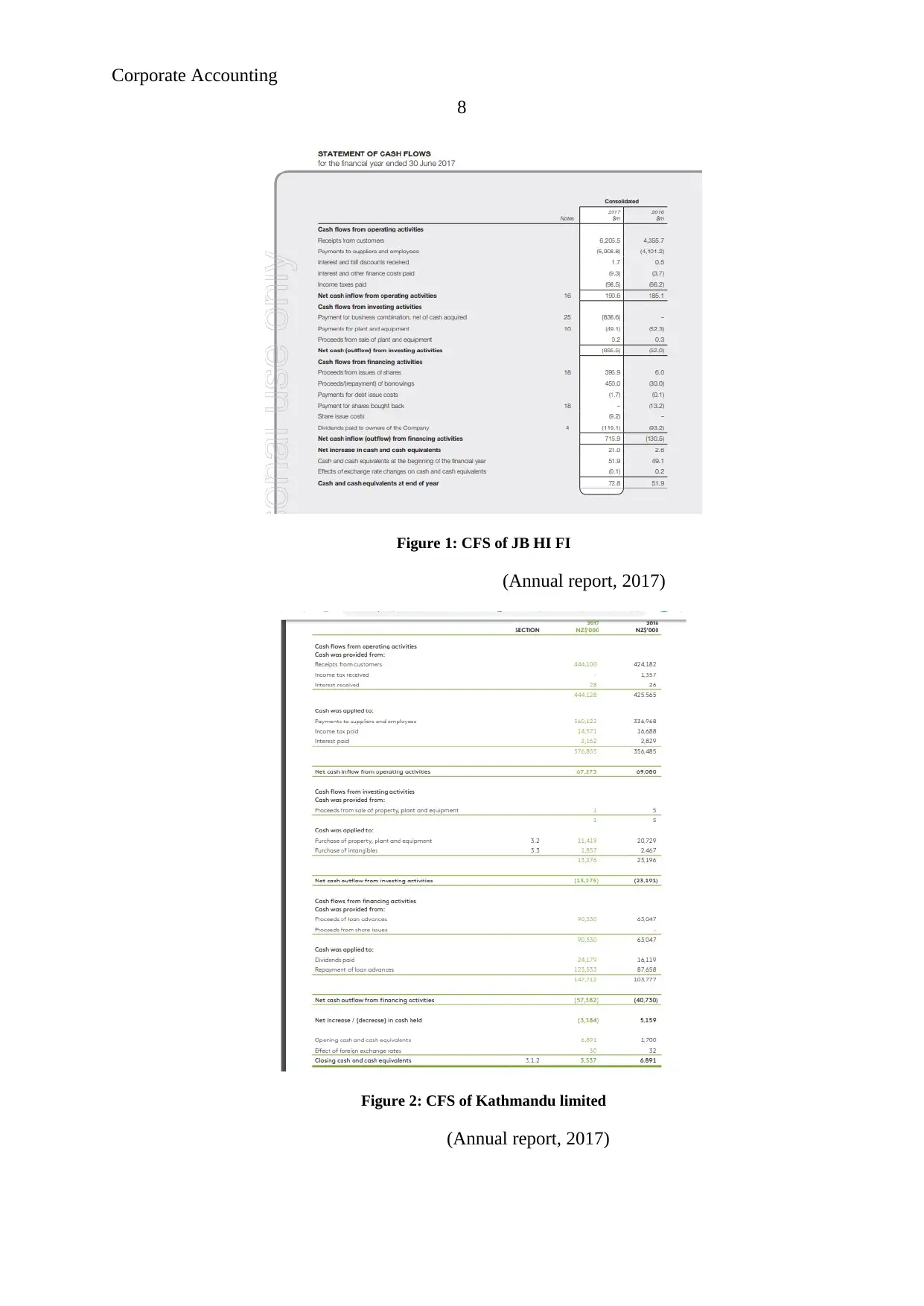

Figure 1: CFS of JB HI FI

(Annual report, 2017)

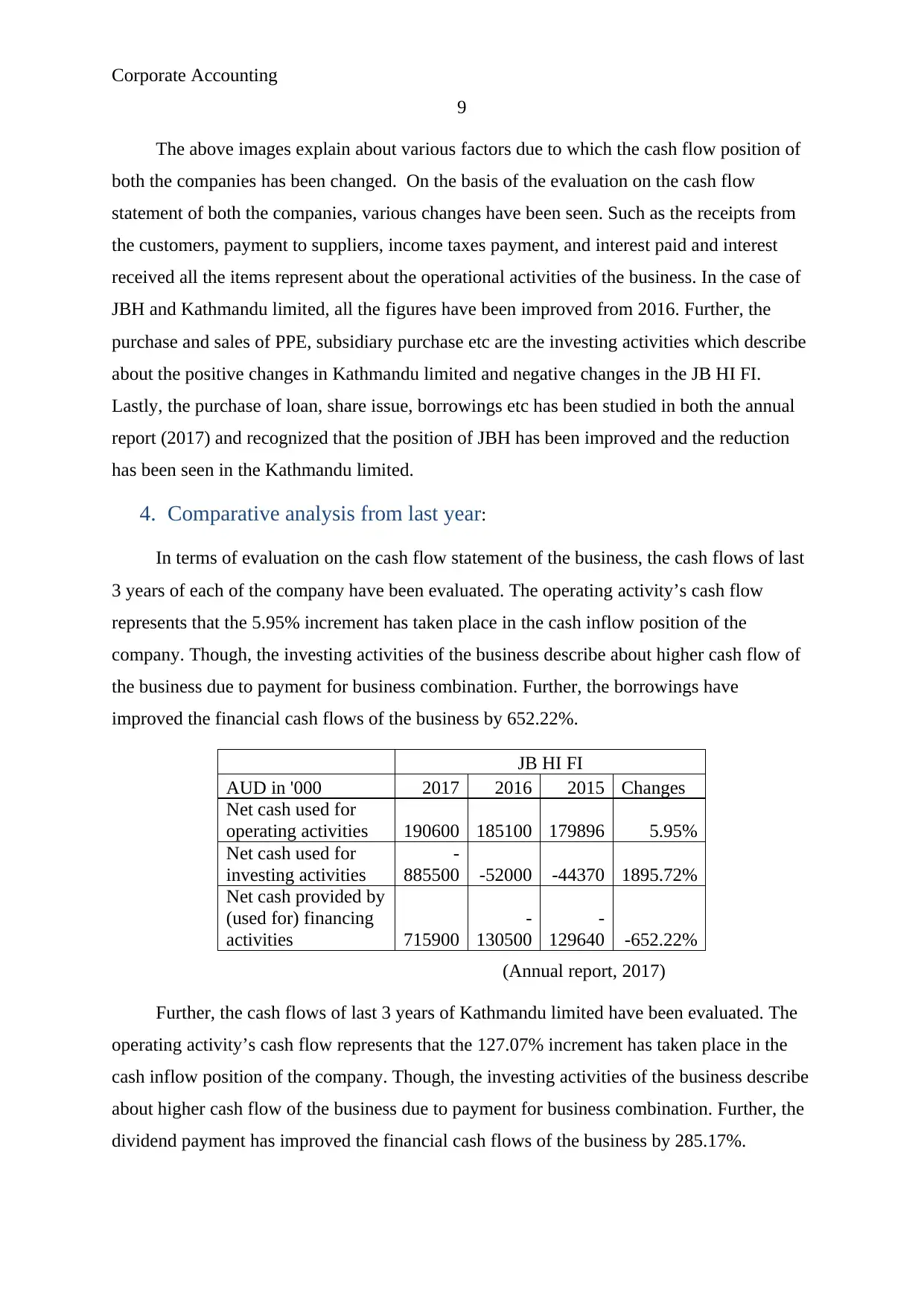

Figure 2: CFS of Kathmandu limited

(Annual report, 2017)

8

Figure 1: CFS of JB HI FI

(Annual report, 2017)

Figure 2: CFS of Kathmandu limited

(Annual report, 2017)

Corporate Accounting

9

The above images explain about various factors due to which the cash flow position of

both the companies has been changed. On the basis of the evaluation on the cash flow

statement of both the companies, various changes have been seen. Such as the receipts from

the customers, payment to suppliers, income taxes payment, and interest paid and interest

received all the items represent about the operational activities of the business. In the case of

JBH and Kathmandu limited, all the figures have been improved from 2016. Further, the

purchase and sales of PPE, subsidiary purchase etc are the investing activities which describe

about the positive changes in Kathmandu limited and negative changes in the JB HI FI.

Lastly, the purchase of loan, share issue, borrowings etc has been studied in both the annual

report (2017) and recognized that the position of JBH has been improved and the reduction

has been seen in the Kathmandu limited.

4. Comparative analysis from last year:

In terms of evaluation on the cash flow statement of the business, the cash flows of last

3 years of each of the company have been evaluated. The operating activity’s cash flow

represents that the 5.95% increment has taken place in the cash inflow position of the

company. Though, the investing activities of the business describe about higher cash flow of

the business due to payment for business combination. Further, the borrowings have

improved the financial cash flows of the business by 652.22%.

JB HI FI

AUD in '000 2017 2016 2015 Changes

Net cash used for

operating activities 190600 185100 179896 5.95%

Net cash used for

investing activities

-

885500 -52000 -44370 1895.72%

Net cash provided by

(used for) financing

activities 715900

-

130500

-

129640 -652.22%

(Annual report, 2017)

Further, the cash flows of last 3 years of Kathmandu limited have been evaluated. The

operating activity’s cash flow represents that the 127.07% increment has taken place in the

cash inflow position of the company. Though, the investing activities of the business describe

about higher cash flow of the business due to payment for business combination. Further, the

dividend payment has improved the financial cash flows of the business by 285.17%.

9

The above images explain about various factors due to which the cash flow position of

both the companies has been changed. On the basis of the evaluation on the cash flow

statement of both the companies, various changes have been seen. Such as the receipts from

the customers, payment to suppliers, income taxes payment, and interest paid and interest

received all the items represent about the operational activities of the business. In the case of

JBH and Kathmandu limited, all the figures have been improved from 2016. Further, the

purchase and sales of PPE, subsidiary purchase etc are the investing activities which describe

about the positive changes in Kathmandu limited and negative changes in the JB HI FI.

Lastly, the purchase of loan, share issue, borrowings etc has been studied in both the annual

report (2017) and recognized that the position of JBH has been improved and the reduction

has been seen in the Kathmandu limited.

4. Comparative analysis from last year:

In terms of evaluation on the cash flow statement of the business, the cash flows of last

3 years of each of the company have been evaluated. The operating activity’s cash flow

represents that the 5.95% increment has taken place in the cash inflow position of the

company. Though, the investing activities of the business describe about higher cash flow of

the business due to payment for business combination. Further, the borrowings have

improved the financial cash flows of the business by 652.22%.

JB HI FI

AUD in '000 2017 2016 2015 Changes

Net cash used for

operating activities 190600 185100 179896 5.95%

Net cash used for

investing activities

-

885500 -52000 -44370 1895.72%

Net cash provided by

(used for) financing

activities 715900

-

130500

-

129640 -652.22%

(Annual report, 2017)

Further, the cash flows of last 3 years of Kathmandu limited have been evaluated. The

operating activity’s cash flow represents that the 127.07% increment has taken place in the

cash inflow position of the company. Though, the investing activities of the business describe

about higher cash flow of the business due to payment for business combination. Further, the

dividend payment has improved the financial cash flows of the business by 285.17%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

10

Kathmandu Limited

AUD in '000 2017 2016 2015 Changes

Net cash used for

operating activities 67273 69080 29627 127.07%

Net cash used for

investing activities -13275 -23191

-

19980 -33.56%

Net cash provided by

(used for) financing

activities -57382 -40730

-

14898 285.17%

(Annual report, 2016)

5. Comparative analysis among the companies:

The comparison of both the companies has been done further to measure that whether

the changes in both the companies are similar or the internal factors of the company have

derived the different changes in both the companies. On the basis of the below given table, it

has been recognized that the cash flow from operating activities of JBH and Kathmandu

limited is 2.97% and -2.62% which describes better cash level of JBH. Further, the cash flow

from financing activities of JBH and Kathmandu limited is -1602.88% and 42.76% which

describes better cash management position of Kathmandu limited. Lastly, the study describes

that the outflow of JBH has been controlled and the Kathmandu limited’s expenses have been

improved in the year of 2017.

JB HI FI Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Net cash used for operating activities 190600 185100 2.97% 67273 69080 -2.62%

Net cash used for investing activities

-

885500 -52000 1602.88%

-

13275

-

23191 -42.76%

Net cash provided by (used for)

financing activities 715900

-

130500 -648.58%

-

57382

-

40730 40.88%

(Annual report, 2017)

The similarity in recording the cash flow position of both the companies have helped

to compare the cash flow figures of both the companies and evaluate the cash management

level of both the companies.

Other comprehensive income statement:

10

Kathmandu Limited

AUD in '000 2017 2016 2015 Changes

Net cash used for

operating activities 67273 69080 29627 127.07%

Net cash used for

investing activities -13275 -23191

-

19980 -33.56%

Net cash provided by

(used for) financing

activities -57382 -40730

-

14898 285.17%

(Annual report, 2016)

5. Comparative analysis among the companies:

The comparison of both the companies has been done further to measure that whether

the changes in both the companies are similar or the internal factors of the company have

derived the different changes in both the companies. On the basis of the below given table, it

has been recognized that the cash flow from operating activities of JBH and Kathmandu

limited is 2.97% and -2.62% which describes better cash level of JBH. Further, the cash flow

from financing activities of JBH and Kathmandu limited is -1602.88% and 42.76% which

describes better cash management position of Kathmandu limited. Lastly, the study describes

that the outflow of JBH has been controlled and the Kathmandu limited’s expenses have been

improved in the year of 2017.

JB HI FI Kathmandu Limited

AUD in '000 2017 2016 Changes 2017 2016 Changes

Net cash used for operating activities 190600 185100 2.97% 67273 69080 -2.62%

Net cash used for investing activities

-

885500 -52000 1602.88%

-

13275

-

23191 -42.76%

Net cash provided by (used for)

financing activities 715900

-

130500 -648.58%

-

57382

-

40730 40.88%

(Annual report, 2017)

The similarity in recording the cash flow position of both the companies have helped

to compare the cash flow figures of both the companies and evaluate the cash management

level of both the companies.

Other comprehensive income statement:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

11

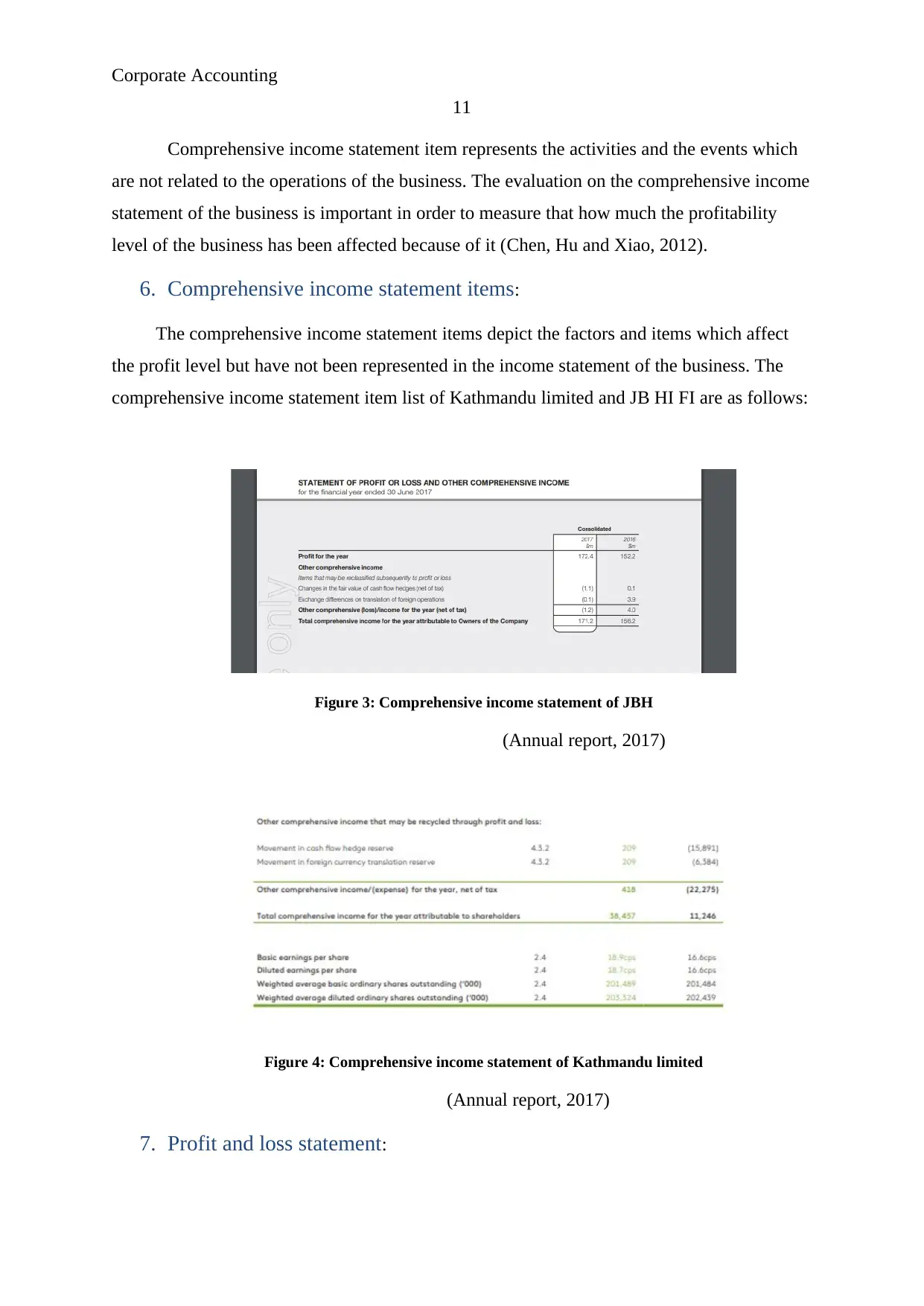

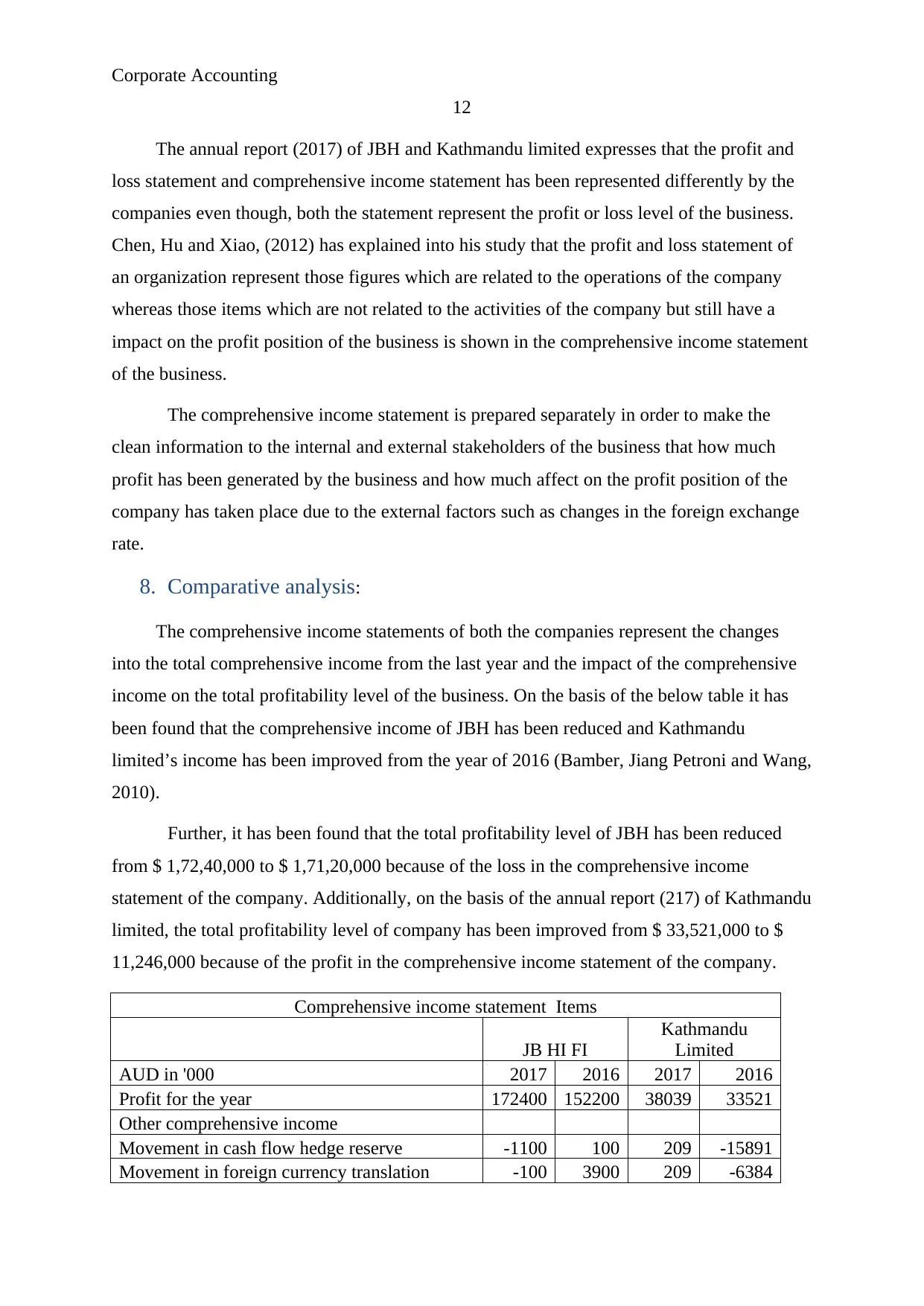

Comprehensive income statement item represents the activities and the events which

are not related to the operations of the business. The evaluation on the comprehensive income

statement of the business is important in order to measure that how much the profitability

level of the business has been affected because of it (Chen, Hu and Xiao, 2012).

6. Comprehensive income statement items:

The comprehensive income statement items depict the factors and items which affect

the profit level but have not been represented in the income statement of the business. The

comprehensive income statement item list of Kathmandu limited and JB HI FI are as follows:

Figure 3: Comprehensive income statement of JBH

(Annual report, 2017)

Figure 4: Comprehensive income statement of Kathmandu limited

(Annual report, 2017)

7. Profit and loss statement:

11

Comprehensive income statement item represents the activities and the events which

are not related to the operations of the business. The evaluation on the comprehensive income

statement of the business is important in order to measure that how much the profitability

level of the business has been affected because of it (Chen, Hu and Xiao, 2012).

6. Comprehensive income statement items:

The comprehensive income statement items depict the factors and items which affect

the profit level but have not been represented in the income statement of the business. The

comprehensive income statement item list of Kathmandu limited and JB HI FI are as follows:

Figure 3: Comprehensive income statement of JBH

(Annual report, 2017)

Figure 4: Comprehensive income statement of Kathmandu limited

(Annual report, 2017)

7. Profit and loss statement:

Corporate Accounting

12

The annual report (2017) of JBH and Kathmandu limited expresses that the profit and

loss statement and comprehensive income statement has been represented differently by the

companies even though, both the statement represent the profit or loss level of the business.

Chen, Hu and Xiao, (2012) has explained into his study that the profit and loss statement of

an organization represent those figures which are related to the operations of the company

whereas those items which are not related to the activities of the company but still have a

impact on the profit position of the business is shown in the comprehensive income statement

of the business.

The comprehensive income statement is prepared separately in order to make the

clean information to the internal and external stakeholders of the business that how much

profit has been generated by the business and how much affect on the profit position of the

company has taken place due to the external factors such as changes in the foreign exchange

rate.

8. Comparative analysis:

The comprehensive income statements of both the companies represent the changes

into the total comprehensive income from the last year and the impact of the comprehensive

income on the total profitability level of the business. On the basis of the below table it has

been found that the comprehensive income of JBH has been reduced and Kathmandu

limited’s income has been improved from the year of 2016 (Bamber, Jiang Petroni and Wang,

2010).

Further, it has been found that the total profitability level of JBH has been reduced

from $ 1,72,40,000 to $ 1,71,20,000 because of the loss in the comprehensive income

statement of the company. Additionally, on the basis of the annual report (217) of Kathmandu

limited, the total profitability level of company has been improved from $ 33,521,000 to $

11,246,000 because of the profit in the comprehensive income statement of the company.

Comprehensive income statement Items

JB HI FI

Kathmandu

Limited

AUD in '000 2017 2016 2017 2016

Profit for the year 172400 152200 38039 33521

Other comprehensive income

Movement in cash flow hedge reserve -1100 100 209 -15891

Movement in foreign currency translation -100 3900 209 -6384

12

The annual report (2017) of JBH and Kathmandu limited expresses that the profit and

loss statement and comprehensive income statement has been represented differently by the

companies even though, both the statement represent the profit or loss level of the business.

Chen, Hu and Xiao, (2012) has explained into his study that the profit and loss statement of

an organization represent those figures which are related to the operations of the company

whereas those items which are not related to the activities of the company but still have a

impact on the profit position of the business is shown in the comprehensive income statement

of the business.

The comprehensive income statement is prepared separately in order to make the

clean information to the internal and external stakeholders of the business that how much

profit has been generated by the business and how much affect on the profit position of the

company has taken place due to the external factors such as changes in the foreign exchange

rate.

8. Comparative analysis:

The comprehensive income statements of both the companies represent the changes

into the total comprehensive income from the last year and the impact of the comprehensive

income on the total profitability level of the business. On the basis of the below table it has

been found that the comprehensive income of JBH has been reduced and Kathmandu

limited’s income has been improved from the year of 2016 (Bamber, Jiang Petroni and Wang,

2010).

Further, it has been found that the total profitability level of JBH has been reduced

from $ 1,72,40,000 to $ 1,71,20,000 because of the loss in the comprehensive income

statement of the company. Additionally, on the basis of the annual report (217) of Kathmandu

limited, the total profitability level of company has been improved from $ 33,521,000 to $

11,246,000 because of the profit in the comprehensive income statement of the company.

Comprehensive income statement Items

JB HI FI

Kathmandu

Limited

AUD in '000 2017 2016 2017 2016

Profit for the year 172400 152200 38039 33521

Other comprehensive income

Movement in cash flow hedge reserve -1100 100 209 -15891

Movement in foreign currency translation -100 3900 209 -6384

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.