Management Accounting Report: Cost Analysis, Budgeting, and Variances

VerifiedAdded on 2020/01/28

|20

|5348

|89

Report

AI Summary

This management accounting report provides a comprehensive analysis of cost accounting principles applied to Jeffrey & Son's. The report begins with a classification of costs based on element, nature, function, and behavior. It then computes the unit cost for Job no. 444 using the job costing method and determines the cost of the Exquisite product using absorption costing. The report includes an analysis of cost data using appropriate techniques, followed by the preparation of a cost report for September, including variance analysis. The report also discusses indicators for identifying areas for potential improvement and ways to reduce costs while improving quality and enhancing value. Additionally, the report covers budgeting processes, including production, material purchase, and cash budgets. Finally, it computes variances, identifies possible causes, recommends corrective actions, and presents an operating statement with a discussion on responsibility centers. The analysis highlights the importance of effective cost management for business performance and profitability.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction..........................................................................................................................................

TASK 1.................................................................................................................................................

AC 1.1 Cost classification on the basis of element, nature, function and behaviour..................1

AC 1.2 Computation of unit cost for Job no. 444 using job costing method..............................2

AC 1.3 Cost determination of Exquisite product on the basis of absorption costing method.....3

AC 1.4 Analysis of cost data of Exquisite through using appropriate technique........................6

TASK 2.................................................................................................................................................

AC 2.1 Preparation of cost report for September with comment on the computed variances.....7

AC 2.2 Indicators for identifying areas for potential improvement............................................8

AC 2.3 Ways to reduce cost, improving quality and enhance value...........................................8

Task 3...................................................................................................................................................

3.1 Nature and Purpose of Budgeting process.............................................................................9

3.2 Appropriate budgetary method and its need........................................................................10

3.3 Production and Material purchase budget...........................................................................10

3.4 Preparing Jeffrey & Son's cash budget................................................................................11

Working note:..........................................................................................................................12

Task 4.................................................................................................................................................

4.1 Computing variances, identify possible causes and recommend corrective actions...........13

4.2 Operating Statement............................................................................................................14

4.3 Responsibility centers..........................................................................................................15

Conclusion..........................................................................................................................................

References..........................................................................................................................................

Introduction..........................................................................................................................................

TASK 1.................................................................................................................................................

AC 1.1 Cost classification on the basis of element, nature, function and behaviour..................1

AC 1.2 Computation of unit cost for Job no. 444 using job costing method..............................2

AC 1.3 Cost determination of Exquisite product on the basis of absorption costing method.....3

AC 1.4 Analysis of cost data of Exquisite through using appropriate technique........................6

TASK 2.................................................................................................................................................

AC 2.1 Preparation of cost report for September with comment on the computed variances.....7

AC 2.2 Indicators for identifying areas for potential improvement............................................8

AC 2.3 Ways to reduce cost, improving quality and enhance value...........................................8

Task 3...................................................................................................................................................

3.1 Nature and Purpose of Budgeting process.............................................................................9

3.2 Appropriate budgetary method and its need........................................................................10

3.3 Production and Material purchase budget...........................................................................10

3.4 Preparing Jeffrey & Son's cash budget................................................................................11

Working note:..........................................................................................................................12

Task 4.................................................................................................................................................

4.1 Computing variances, identify possible causes and recommend corrective actions...........13

4.2 Operating Statement............................................................................................................14

4.3 Responsibility centers..........................................................................................................15

Conclusion..........................................................................................................................................

References..........................................................................................................................................

List of tables

Table 1: Fixed/variable expenditures...............................................................................................3

Table 2: Working Note....................................................................................................................4

Table 3: Allocation of costs.............................................................................................................5

Table 4: Re-appointment of cost......................................................................................................6

Table 5: Total product cost..............................................................................................................6

Table 6: Cost report.........................................................................................................................8

Table 7: Cost elements.....................................................................................................................8

Table 8: Production budget............................................................................................................12

Table 9: Material purchase budget................................................................................................12

Table 10: Cash budget...................................................................................................................13

Table 11: Variances.......................................................................................................................15

Table 12: Operating statement.......................................................................................................16

1

Table 1: Fixed/variable expenditures...............................................................................................3

Table 2: Working Note....................................................................................................................4

Table 3: Allocation of costs.............................................................................................................5

Table 4: Re-appointment of cost......................................................................................................6

Table 5: Total product cost..............................................................................................................6

Table 6: Cost report.........................................................................................................................8

Table 7: Cost elements.....................................................................................................................8

Table 8: Production budget............................................................................................................12

Table 9: Material purchase budget................................................................................................12

Table 10: Cash budget...................................................................................................................13

Table 11: Variances.......................................................................................................................15

Table 12: Operating statement.......................................................................................................16

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Looking at the present condition of corporate market, there are several firms which are

competing with each other on the basis of price irrespective of their sectors. But maintaining the

position within the sector, it makes inevitable for the companies to reduce their costs of different

departments. In this, management accounting plays a significant role because it helps in

controlling the expenditures of the organization .Herein, researcher focuses on evaluating the

classification of different costs on various bases. Thereafter, various performance indicators have

been identified for measuring actual position of the company. Further, researcher focuses on

analysing those measures which can reduce the costs of businesses. Lastly, it also emphasizes on

budgeting techniques and its importance for the management of income and expenditure of the

company.

TASK 1

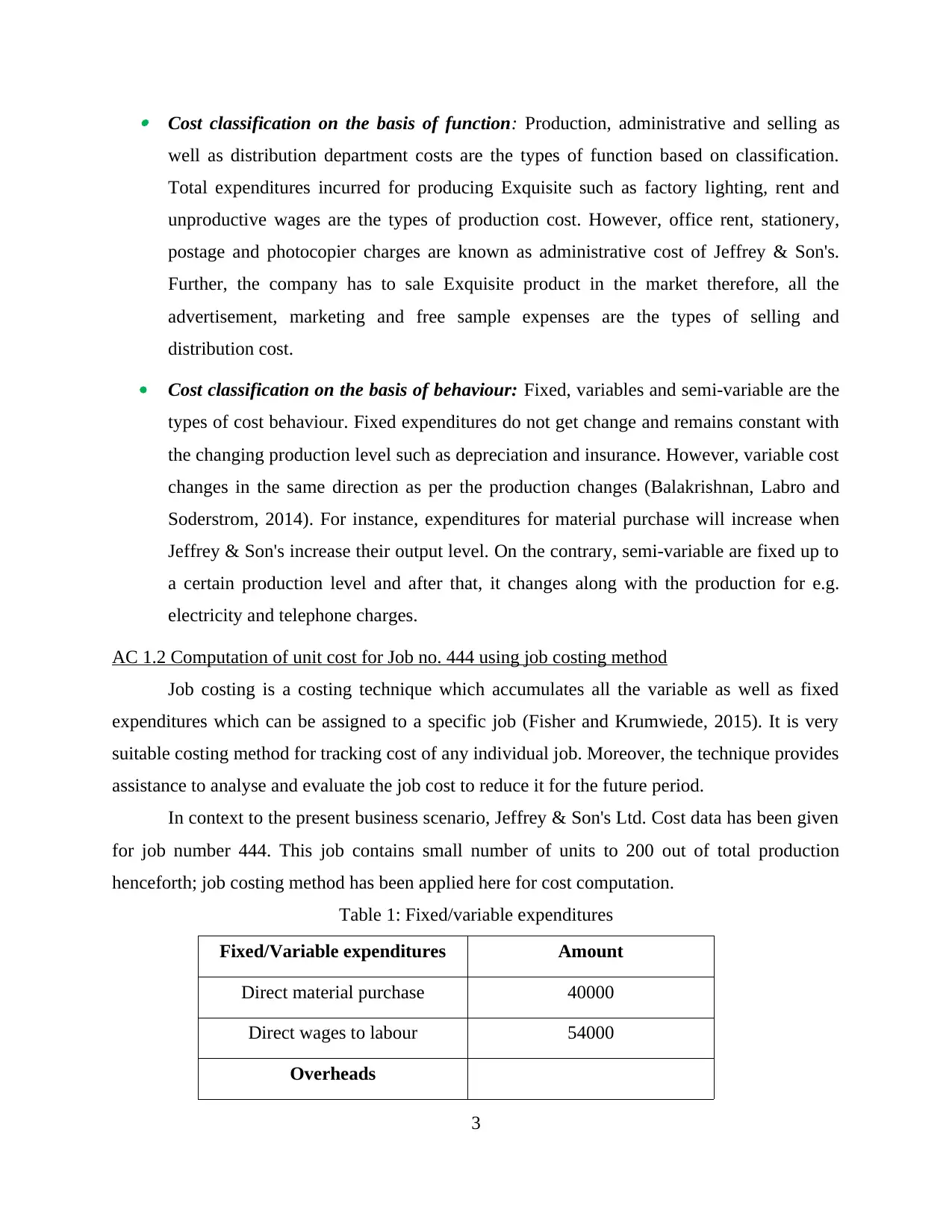

AC 1.1 Cost classification on the basis of element, nature, function and behaviour

Cost is the amount of total expenses which have been incurred in Jeffrey & Son's

production process. Different cost classifications have been described here under: Cost classification on the basis of element: Jeffrey & Son's produce product called

Exquisite contains three elements that are material, labour and overheads. Material cost is

the total expenses that have been incurred for purchasing raw material. This is the basic

element and without this the production cannot be carried out. However, Jeffrey & Son's

pay wages to their labour is known as labour cost (Rajan, Datar and Horngren, 2015).

Labour are the persons who put necessary efforts and convert raw material into the

finished product. All the other expenditures are termed as overheads such as stationery,

rent, postage and others. Cost classification on the basis of nature: There are two types of cost nature which are

direct and indirect. Direct manufacturing cost involves all the expenses that can be

directly traced to a specific cost object (Greenberg and Wilner, 2015). For example, cost

of material and labour’s wages are the type of direct cost. On contrary to it, indirect costs

are the total of expenses which cannot be directly charged and traced to a specific object.

For instance, payment which has been incurred by Jeffrey & Son's for rent and rates,

building insurance and machinery depreciation are the type of indirect cost.

2

Looking at the present condition of corporate market, there are several firms which are

competing with each other on the basis of price irrespective of their sectors. But maintaining the

position within the sector, it makes inevitable for the companies to reduce their costs of different

departments. In this, management accounting plays a significant role because it helps in

controlling the expenditures of the organization .Herein, researcher focuses on evaluating the

classification of different costs on various bases. Thereafter, various performance indicators have

been identified for measuring actual position of the company. Further, researcher focuses on

analysing those measures which can reduce the costs of businesses. Lastly, it also emphasizes on

budgeting techniques and its importance for the management of income and expenditure of the

company.

TASK 1

AC 1.1 Cost classification on the basis of element, nature, function and behaviour

Cost is the amount of total expenses which have been incurred in Jeffrey & Son's

production process. Different cost classifications have been described here under: Cost classification on the basis of element: Jeffrey & Son's produce product called

Exquisite contains three elements that are material, labour and overheads. Material cost is

the total expenses that have been incurred for purchasing raw material. This is the basic

element and without this the production cannot be carried out. However, Jeffrey & Son's

pay wages to their labour is known as labour cost (Rajan, Datar and Horngren, 2015).

Labour are the persons who put necessary efforts and convert raw material into the

finished product. All the other expenditures are termed as overheads such as stationery,

rent, postage and others. Cost classification on the basis of nature: There are two types of cost nature which are

direct and indirect. Direct manufacturing cost involves all the expenses that can be

directly traced to a specific cost object (Greenberg and Wilner, 2015). For example, cost

of material and labour’s wages are the type of direct cost. On contrary to it, indirect costs

are the total of expenses which cannot be directly charged and traced to a specific object.

For instance, payment which has been incurred by Jeffrey & Son's for rent and rates,

building insurance and machinery depreciation are the type of indirect cost.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost classification on the basis of function: Production, administrative and selling as

well as distribution department costs are the types of function based on classification.

Total expenditures incurred for producing Exquisite such as factory lighting, rent and

unproductive wages are the types of production cost. However, office rent, stationery,

postage and photocopier charges are known as administrative cost of Jeffrey & Son's.

Further, the company has to sale Exquisite product in the market therefore, all the

advertisement, marketing and free sample expenses are the types of selling and

distribution cost.

Cost classification on the basis of behaviour: Fixed, variables and semi-variable are the

types of cost behaviour. Fixed expenditures do not get change and remains constant with

the changing production level such as depreciation and insurance. However, variable cost

changes in the same direction as per the production changes (Balakrishnan, Labro and

Soderstrom, 2014). For instance, expenditures for material purchase will increase when

Jeffrey & Son's increase their output level. On the contrary, semi-variable are fixed up to

a certain production level and after that, it changes along with the production for e.g.

electricity and telephone charges.

AC 1.2 Computation of unit cost for Job no. 444 using job costing method

Job costing is a costing technique which accumulates all the variable as well as fixed

expenditures which can be assigned to a specific job (Fisher and Krumwiede, 2015). It is very

suitable costing method for tracking cost of any individual job. Moreover, the technique provides

assistance to analyse and evaluate the job cost to reduce it for the future period.

In context to the present business scenario, Jeffrey & Son's Ltd. Cost data has been given

for job number 444. This job contains small number of units to 200 out of total production

henceforth; job costing method has been applied here for cost computation.

Table 1: Fixed/variable expenditures

Fixed/Variable expenditures Amount

Direct material purchase 40000

Direct wages to labour 54000

Overheads

3

well as distribution department costs are the types of function based on classification.

Total expenditures incurred for producing Exquisite such as factory lighting, rent and

unproductive wages are the types of production cost. However, office rent, stationery,

postage and photocopier charges are known as administrative cost of Jeffrey & Son's.

Further, the company has to sale Exquisite product in the market therefore, all the

advertisement, marketing and free sample expenses are the types of selling and

distribution cost.

Cost classification on the basis of behaviour: Fixed, variables and semi-variable are the

types of cost behaviour. Fixed expenditures do not get change and remains constant with

the changing production level such as depreciation and insurance. However, variable cost

changes in the same direction as per the production changes (Balakrishnan, Labro and

Soderstrom, 2014). For instance, expenditures for material purchase will increase when

Jeffrey & Son's increase their output level. On the contrary, semi-variable are fixed up to

a certain production level and after that, it changes along with the production for e.g.

electricity and telephone charges.

AC 1.2 Computation of unit cost for Job no. 444 using job costing method

Job costing is a costing technique which accumulates all the variable as well as fixed

expenditures which can be assigned to a specific job (Fisher and Krumwiede, 2015). It is very

suitable costing method for tracking cost of any individual job. Moreover, the technique provides

assistance to analyse and evaluate the job cost to reduce it for the future period.

In context to the present business scenario, Jeffrey & Son's Ltd. Cost data has been given

for job number 444. This job contains small number of units to 200 out of total production

henceforth; job costing method has been applied here for cost computation.

Table 1: Fixed/variable expenditures

Fixed/Variable expenditures Amount

Direct material purchase 40000

Direct wages to labour 54000

Overheads

3

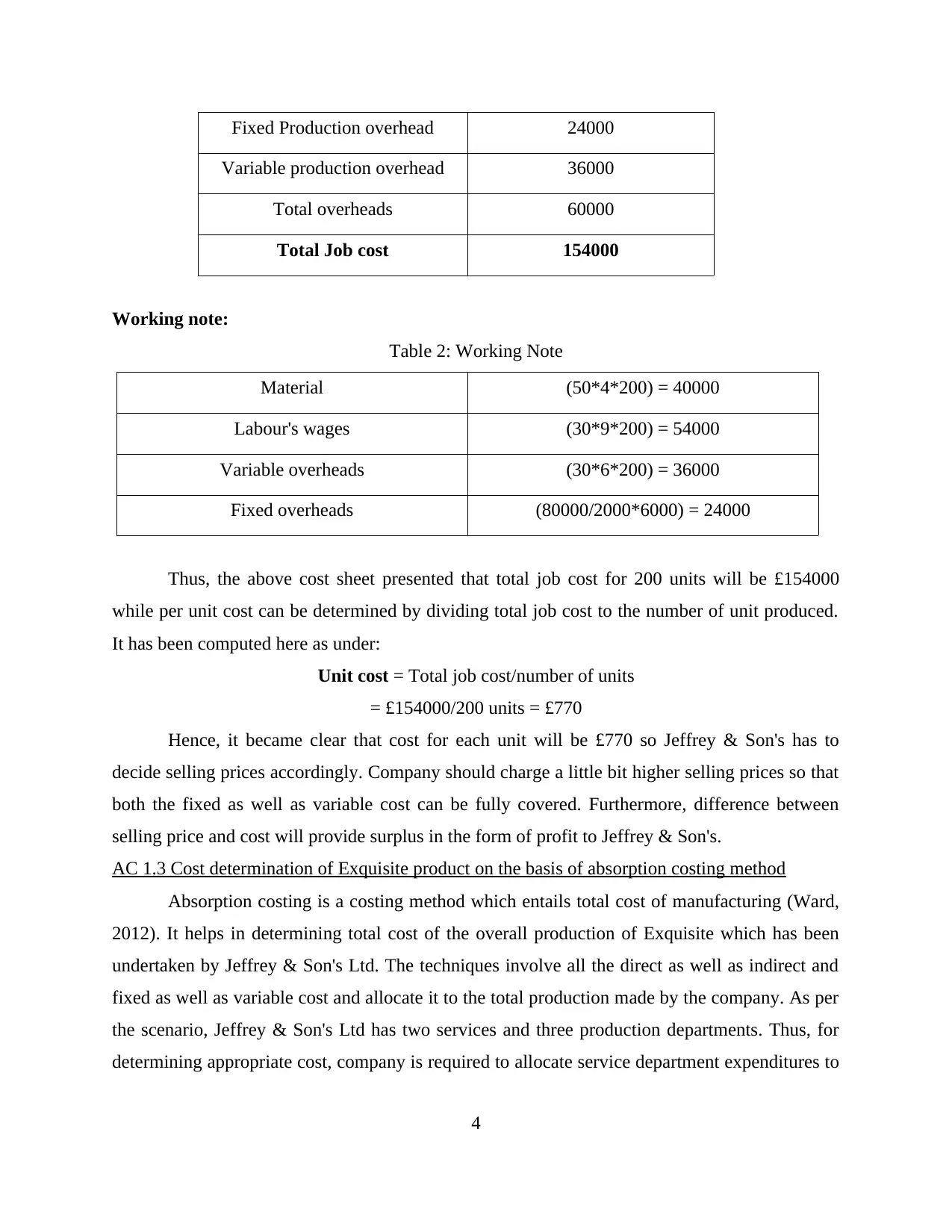

Fixed Production overhead 24000

Variable production overhead 36000

Total overheads 60000

Total Job cost 154000

Working note:

Table 2: Working Note

Material (50*4*200) = 40000

Labour's wages (30*9*200) = 54000

Variable overheads (30*6*200) = 36000

Fixed overheads (80000/2000*6000) = 24000

Thus, the above cost sheet presented that total job cost for 200 units will be £154000

while per unit cost can be determined by dividing total job cost to the number of unit produced.

It has been computed here as under:

Unit cost = Total job cost/number of units

= £154000/200 units = £770

Hence, it became clear that cost for each unit will be £770 so Jeffrey & Son's has to

decide selling prices accordingly. Company should charge a little bit higher selling prices so that

both the fixed as well as variable cost can be fully covered. Furthermore, difference between

selling price and cost will provide surplus in the form of profit to Jeffrey & Son's.

AC 1.3 Cost determination of Exquisite product on the basis of absorption costing method

Absorption costing is a costing method which entails total cost of manufacturing (Ward,

2012). It helps in determining total cost of the overall production of Exquisite which has been

undertaken by Jeffrey & Son's Ltd. The techniques involve all the direct as well as indirect and

fixed as well as variable cost and allocate it to the total production made by the company. As per

the scenario, Jeffrey & Son's Ltd has two services and three production departments. Thus, for

determining appropriate cost, company is required to allocate service department expenditures to

4

Variable production overhead 36000

Total overheads 60000

Total Job cost 154000

Working note:

Table 2: Working Note

Material (50*4*200) = 40000

Labour's wages (30*9*200) = 54000

Variable overheads (30*6*200) = 36000

Fixed overheads (80000/2000*6000) = 24000

Thus, the above cost sheet presented that total job cost for 200 units will be £154000

while per unit cost can be determined by dividing total job cost to the number of unit produced.

It has been computed here as under:

Unit cost = Total job cost/number of units

= £154000/200 units = £770

Hence, it became clear that cost for each unit will be £770 so Jeffrey & Son's has to

decide selling prices accordingly. Company should charge a little bit higher selling prices so that

both the fixed as well as variable cost can be fully covered. Furthermore, difference between

selling price and cost will provide surplus in the form of profit to Jeffrey & Son's.

AC 1.3 Cost determination of Exquisite product on the basis of absorption costing method

Absorption costing is a costing method which entails total cost of manufacturing (Ward,

2012). It helps in determining total cost of the overall production of Exquisite which has been

undertaken by Jeffrey & Son's Ltd. The techniques involve all the direct as well as indirect and

fixed as well as variable cost and allocate it to the total production made by the company. As per

the scenario, Jeffrey & Son's Ltd has two services and three production departments. Thus, for

determining appropriate cost, company is required to allocate service department expenditures to

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

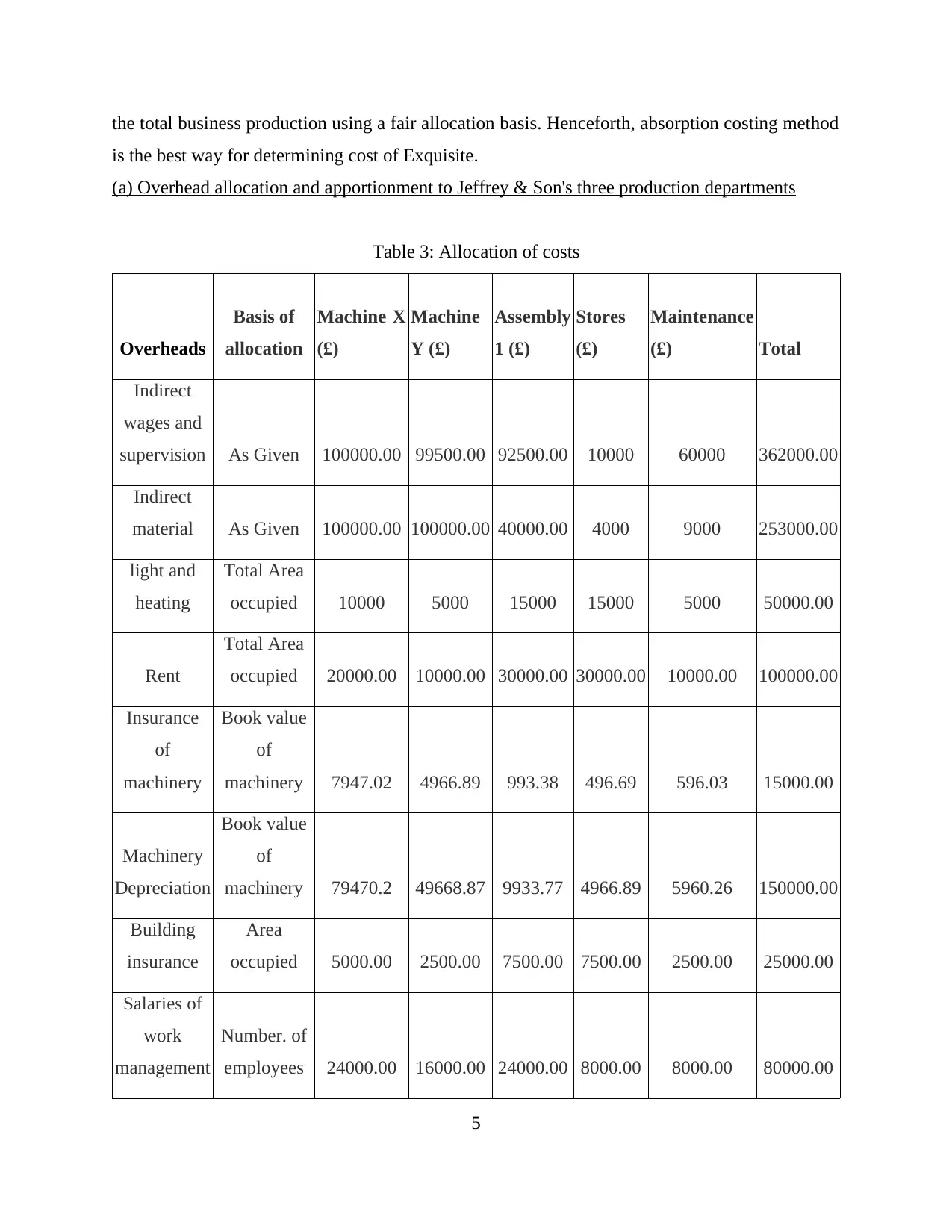

the total business production using a fair allocation basis. Henceforth, absorption costing method

is the best way for determining cost of Exquisite.

(a) Overhead allocation and apportionment to Jeffrey & Son's three production departments

Table 3: Allocation of costs

Overheads

Basis of

allocation

Machine X

(£)

Machine

Y (£)

Assembly

1 (£)

Stores

(£)

Maintenance

(£) Total

Indirect

wages and

supervision As Given 100000.00 99500.00 92500.00 10000 60000 362000.00

Indirect

material As Given 100000.00 100000.00 40000.00 4000 9000 253000.00

light and

heating

Total Area

occupied 10000 5000 15000 15000 5000 50000.00

Rent

Total Area

occupied 20000.00 10000.00 30000.00 30000.00 10000.00 100000.00

Insurance

of

machinery

Book value

of

machinery 7947.02 4966.89 993.38 496.69 596.03 15000.00

Machinery

Depreciation

Book value

of

machinery 79470.2 49668.87 9933.77 4966.89 5960.26 150000.00

Building

insurance

Area

occupied 5000.00 2500.00 7500.00 7500.00 2500.00 25000.00

Salaries of

work

management

Number. of

employees 24000.00 16000.00 24000.00 8000.00 8000.00 80000.00

5

is the best way for determining cost of Exquisite.

(a) Overhead allocation and apportionment to Jeffrey & Son's three production departments

Table 3: Allocation of costs

Overheads

Basis of

allocation

Machine X

(£)

Machine

Y (£)

Assembly

1 (£)

Stores

(£)

Maintenance

(£) Total

Indirect

wages and

supervision As Given 100000.00 99500.00 92500.00 10000 60000 362000.00

Indirect

material As Given 100000.00 100000.00 40000.00 4000 9000 253000.00

light and

heating

Total Area

occupied 10000 5000 15000 15000 5000 50000.00

Rent

Total Area

occupied 20000.00 10000.00 30000.00 30000.00 10000.00 100000.00

Insurance

of

machinery

Book value

of

machinery 7947.02 4966.89 993.38 496.69 596.03 15000.00

Machinery

Depreciation

Book value

of

machinery 79470.2 49668.87 9933.77 4966.89 5960.26 150000.00

Building

insurance

Area

occupied 5000.00 2500.00 7500.00 7500.00 2500.00 25000.00

Salaries of

work

management

Number. of

employees 24000.00 16000.00 24000.00 8000.00 8000.00 80000.00

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

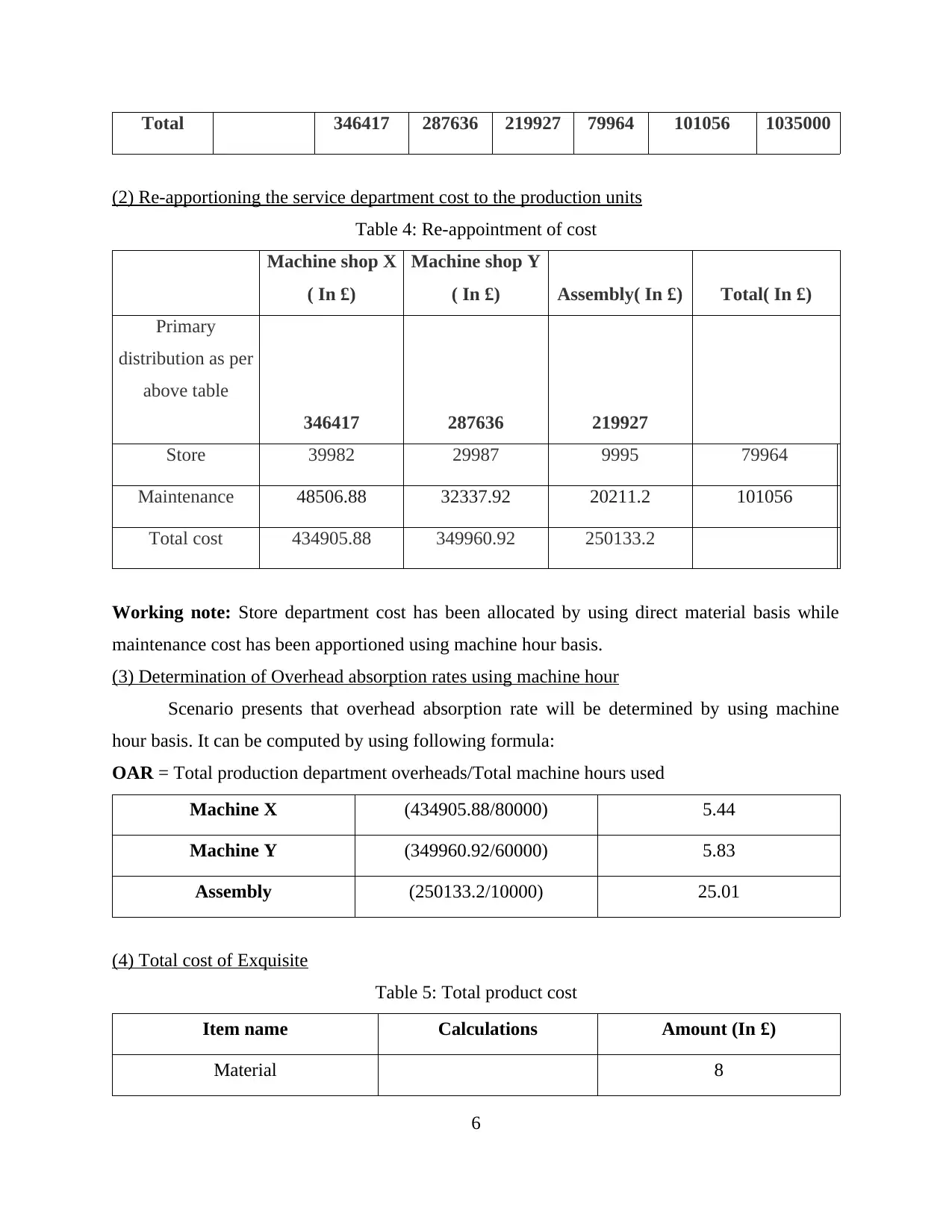

Total 346417 287636 219927 79964 101056 1035000

(2) Re-apportioning the service department cost to the production units

Table 4: Re-appointment of cost

Machine shop X

( In £)

Machine shop Y

( In £) Assembly( In £) Total( In £)

Primary

distribution as per

above table

346417 287636 219927

Store 39982 29987 9995 79964

Maintenance 48506.88 32337.92 20211.2 101056

Total cost 434905.88 349960.92 250133.2

Working note: Store department cost has been allocated by using direct material basis while

maintenance cost has been apportioned using machine hour basis.

(3) Determination of Overhead absorption rates using machine hour

Scenario presents that overhead absorption rate will be determined by using machine

hour basis. It can be computed by using following formula:

OAR = Total production department overheads/Total machine hours used

Machine X (434905.88/80000) 5.44

Machine Y (349960.92/60000) 5.83

Assembly (250133.2/10000) 25.01

(4) Total cost of Exquisite

Table 5: Total product cost

Item name Calculations Amount (In £)

Material 8

6

(2) Re-apportioning the service department cost to the production units

Table 4: Re-appointment of cost

Machine shop X

( In £)

Machine shop Y

( In £) Assembly( In £) Total( In £)

Primary

distribution as per

above table

346417 287636 219927

Store 39982 29987 9995 79964

Maintenance 48506.88 32337.92 20211.2 101056

Total cost 434905.88 349960.92 250133.2

Working note: Store department cost has been allocated by using direct material basis while

maintenance cost has been apportioned using machine hour basis.

(3) Determination of Overhead absorption rates using machine hour

Scenario presents that overhead absorption rate will be determined by using machine

hour basis. It can be computed by using following formula:

OAR = Total production department overheads/Total machine hours used

Machine X (434905.88/80000) 5.44

Machine Y (349960.92/60000) 5.83

Assembly (250133.2/10000) 25.01

(4) Total cost of Exquisite

Table 5: Total product cost

Item name Calculations Amount (In £)

Material 8

6

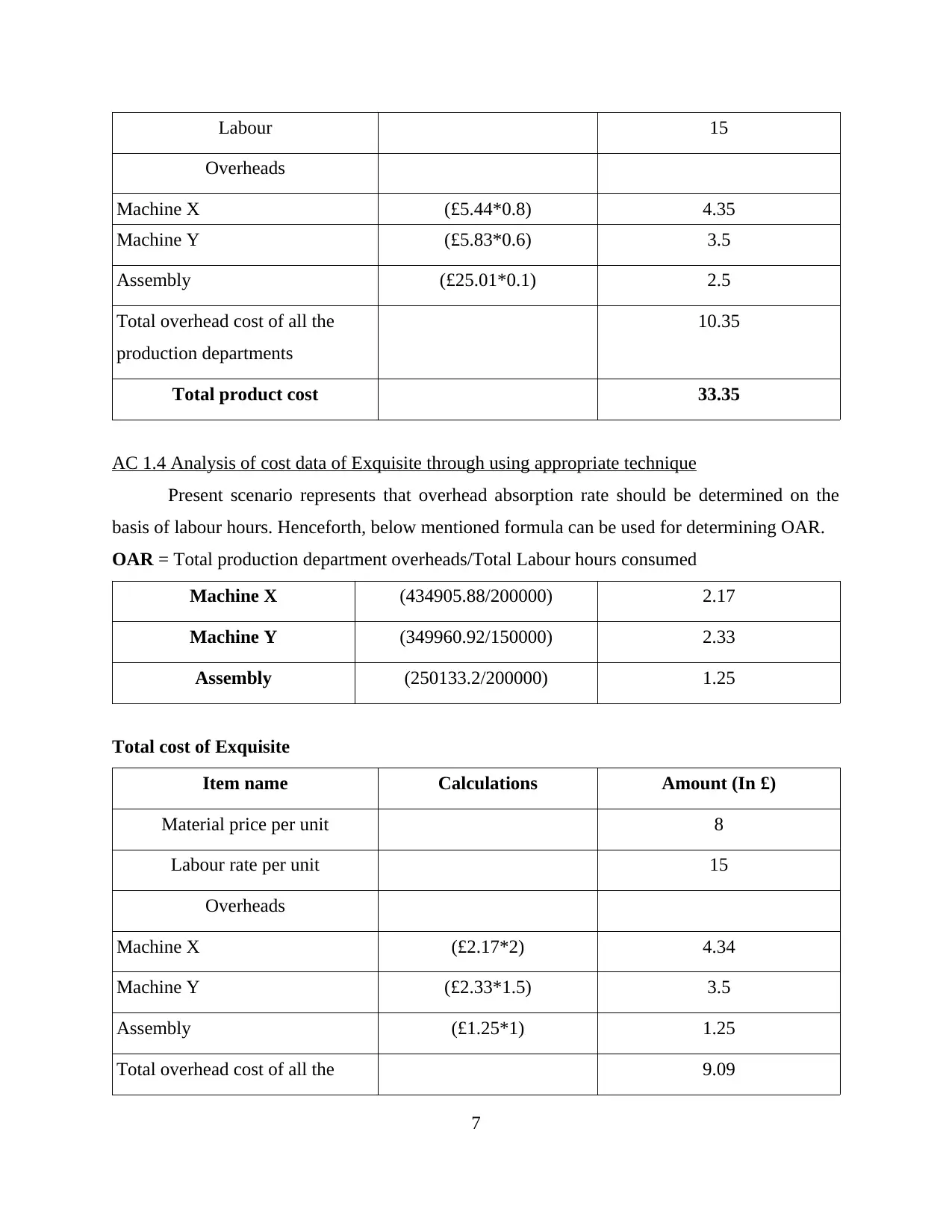

Labour 15

Overheads

Machine X (£5.44*0.8) 4.35

Machine Y (£5.83*0.6) 3.5

Assembly (£25.01*0.1) 2.5

Total overhead cost of all the

production departments

10.35

Total product cost 33.35

AC 1.4 Analysis of cost data of Exquisite through using appropriate technique

Present scenario represents that overhead absorption rate should be determined on the

basis of labour hours. Henceforth, below mentioned formula can be used for determining OAR.

OAR = Total production department overheads/Total Labour hours consumed

Machine X (434905.88/200000) 2.17

Machine Y (349960.92/150000) 2.33

Assembly (250133.2/200000) 1.25

Total cost of Exquisite

Item name Calculations Amount (In £)

Material price per unit 8

Labour rate per unit 15

Overheads

Machine X (£2.17*2) 4.34

Machine Y (£2.33*1.5) 3.5

Assembly (£1.25*1) 1.25

Total overhead cost of all the 9.09

7

Overheads

Machine X (£5.44*0.8) 4.35

Machine Y (£5.83*0.6) 3.5

Assembly (£25.01*0.1) 2.5

Total overhead cost of all the

production departments

10.35

Total product cost 33.35

AC 1.4 Analysis of cost data of Exquisite through using appropriate technique

Present scenario represents that overhead absorption rate should be determined on the

basis of labour hours. Henceforth, below mentioned formula can be used for determining OAR.

OAR = Total production department overheads/Total Labour hours consumed

Machine X (434905.88/200000) 2.17

Machine Y (349960.92/150000) 2.33

Assembly (250133.2/200000) 1.25

Total cost of Exquisite

Item name Calculations Amount (In £)

Material price per unit 8

Labour rate per unit 15

Overheads

Machine X (£2.17*2) 4.34

Machine Y (£2.33*1.5) 3.5

Assembly (£1.25*1) 1.25

Total overhead cost of all the 9.09

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production departments

Total product cost 32.09

Interpretation on difference: On the basis of above computation, it became clear that

labour hour is comparatively a better base for overhead absorption. The reason behind this is that

it minimizes the total product cost to £32.09 while in machine hour basis it was £33.35.

Henceforth, it is considered advisable that company should use this basis for cost determination.

It will maximize Jeffrey & Son's profitability so that firm will improve its operational

performance.

TASK 2

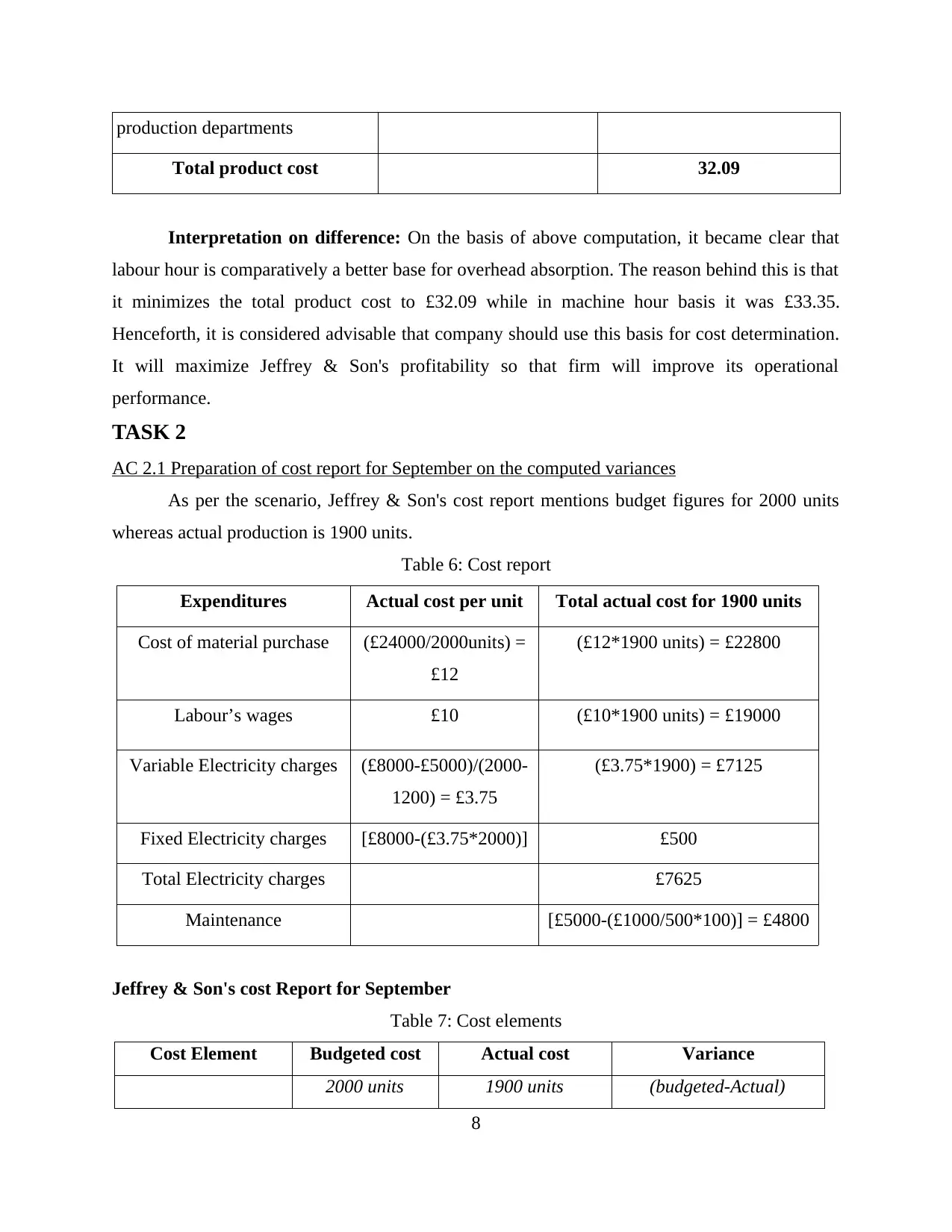

AC 2.1 Preparation of cost report for September on the computed variances

As per the scenario, Jeffrey & Son's cost report mentions budget figures for 2000 units

whereas actual production is 1900 units.

Table 6: Cost report

Expenditures Actual cost per unit Total actual cost for 1900 units

Cost of material purchase (£24000/2000units) =

£12

(£12*1900 units) = £22800

Labour’s wages £10 (£10*1900 units) = £19000

Variable Electricity charges (£8000-£5000)/(2000-

1200) = £3.75

(£3.75*1900) = £7125

Fixed Electricity charges [£8000-(£3.75*2000)] £500

Total Electricity charges £7625

Maintenance [£5000-(£1000/500*100)] = £4800

Jeffrey & Son's cost Report for September

Table 7: Cost elements

Cost Element Budgeted cost Actual cost Variance

2000 units 1900 units (budgeted-Actual)

8

Total product cost 32.09

Interpretation on difference: On the basis of above computation, it became clear that

labour hour is comparatively a better base for overhead absorption. The reason behind this is that

it minimizes the total product cost to £32.09 while in machine hour basis it was £33.35.

Henceforth, it is considered advisable that company should use this basis for cost determination.

It will maximize Jeffrey & Son's profitability so that firm will improve its operational

performance.

TASK 2

AC 2.1 Preparation of cost report for September on the computed variances

As per the scenario, Jeffrey & Son's cost report mentions budget figures for 2000 units

whereas actual production is 1900 units.

Table 6: Cost report

Expenditures Actual cost per unit Total actual cost for 1900 units

Cost of material purchase (£24000/2000units) =

£12

(£12*1900 units) = £22800

Labour’s wages £10 (£10*1900 units) = £19000

Variable Electricity charges (£8000-£5000)/(2000-

1200) = £3.75

(£3.75*1900) = £7125

Fixed Electricity charges [£8000-(£3.75*2000)] £500

Total Electricity charges £7625

Maintenance [£5000-(£1000/500*100)] = £4800

Jeffrey & Son's cost Report for September

Table 7: Cost elements

Cost Element Budgeted cost Actual cost Variance

2000 units 1900 units (budgeted-Actual)

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Material cost 24000£ 22800£ 1200£

Labour’s wages 18000£ 19000£ (1000£)

Fixed Overhead 15000£ 15000£ Nil

Electricity cost 8000£ 7625£ 375£

Maintenance cost 5000£ 4800£ 200£

Total 70000£ 69225£ 775£

Variances: Variances is the difference between actual and budgeted cost figures.

Material cost shows favourable variance of £1200 because of declined production level by 100

units. On the contrary, per unit material price remains constant to £12 which is good. On the

other hand, actual labour wages rate went up to £10 from budgeted of £9. This in turn, actual

wages payment was increased by £1000 which affected the profits adversely. However, fixed

overhead still remain same because they are not affected with the level of production. Another,

semi-variable cost electricity and stepped cost maintenance has been reduced because the

production declined by 100 units.

AC 2.2 Indicators for identifying areas for potential improvement

Revenue, cost and profits are one of the most important indicator that assess business

performance and determine areas for improvement. For instance, growth in revenues, declined

trend of cost and high profit of Jeffrey & sons are the sign of good performance and vice versa

(Demski, 2013). Moreover, Exquisite quality, price stability, customer satisfaction, production

cycle and customer waiting time are also helpful in examining Jeffrey & Son's performance.

Better quality, affordable prices, reducing customer waiting time through efficient production

process assist Jeffrey & Son's to improve their performance (Schuhmann, 2008). Furthermore, its

strategic capabilities such as human capital combines workers skills, knowledge, experiences,

their ability to do work and attributes also plays an crucial role in the Jeffrey& Son's future

success. Along with this, technological improvement also helps in enhancing firm’s potential

performance and assist in improving their competitive strength. Thus, it is considered advisable

that Jeffrey & Son's has to provide innovated products to their customers so that firm will be able

to grab large market share and compete effectively.

9

Labour’s wages 18000£ 19000£ (1000£)

Fixed Overhead 15000£ 15000£ Nil

Electricity cost 8000£ 7625£ 375£

Maintenance cost 5000£ 4800£ 200£

Total 70000£ 69225£ 775£

Variances: Variances is the difference between actual and budgeted cost figures.

Material cost shows favourable variance of £1200 because of declined production level by 100

units. On the contrary, per unit material price remains constant to £12 which is good. On the

other hand, actual labour wages rate went up to £10 from budgeted of £9. This in turn, actual

wages payment was increased by £1000 which affected the profits adversely. However, fixed

overhead still remain same because they are not affected with the level of production. Another,

semi-variable cost electricity and stepped cost maintenance has been reduced because the

production declined by 100 units.

AC 2.2 Indicators for identifying areas for potential improvement

Revenue, cost and profits are one of the most important indicator that assess business

performance and determine areas for improvement. For instance, growth in revenues, declined

trend of cost and high profit of Jeffrey & sons are the sign of good performance and vice versa

(Demski, 2013). Moreover, Exquisite quality, price stability, customer satisfaction, production

cycle and customer waiting time are also helpful in examining Jeffrey & Son's performance.

Better quality, affordable prices, reducing customer waiting time through efficient production

process assist Jeffrey & Son's to improve their performance (Schuhmann, 2008). Furthermore, its

strategic capabilities such as human capital combines workers skills, knowledge, experiences,

their ability to do work and attributes also plays an crucial role in the Jeffrey& Son's future

success. Along with this, technological improvement also helps in enhancing firm’s potential

performance and assist in improving their competitive strength. Thus, it is considered advisable

that Jeffrey & Son's has to provide innovated products to their customers so that firm will be able

to grab large market share and compete effectively.

9

AC 2.3 Ways to reduce cost, improving quality and enhance value Cost reduction: Regular monitoring of all the operational activities will help to manage

spending. In context to Jeffrey & Son's, material cost can be reduced through finding best

suppliers who can provide qualitative products at cost effective prices and reduce

material wastage. However, wages cost can be minimized through hiring labours at the

lower piece rate (Campbell and Brown, 2016). In addition, all the other overheads can be

controlled by effectively utilizing and allocating resources and continuous monitoring.

Moreover, large production level also provides benefits of economies of scale and

reduces per unit cost. Quality improvement: It is the most important factor in manufacturing industry. Jeffrey

&Sons can improve Exquisite quality by using good quality of material and innovated

technological process (Goetsch and Davis, 2014). Furthermore, TQM is a technique

which can be used for the overall quality management of company's product.

Enhance corporate value: Growth in shareholders worth, business expansion, large

investment, new product development, improving competitive position, large customer

base, brand loyalty and entering into new markets makes Jeffrey & Son's able to enhance

its business value (Chatterji and Fabrizio, 2014).

TASK 3

3.1 Nature and Purpose of Budgeting process

Nature of Budgeting Process:

By preparing the budget, finance manager of Jeffrey & Son’s focus on gathering all the

required information for preparing suitable and realistic budget (Anderson, 2011). The data can

be related to different departments such as production, sales, marketing etc. which company

possess. Further, all the sources of income are recorded in the budget so as to identify the

potential ways through which company can generate its revenue (Adler, 2013). Further, these

sources can be sales, lease, investment etc. as they are prepared for financial products. In this,

manager predicts the future sales performance of business on the basis of current economic

environment. In addition to this, manager of Jeffrey &Sons can forecast the expenditures with

the help of materials, labours and overheads. Further, by carrying out comparison between

revenue generated and expenditure incurred manager can easily evaluate deficit and surplus

position of the business (Debarishi, 2011). Thereafter, Jeffrey & Son’s managers have to focus

10

spending. In context to Jeffrey & Son's, material cost can be reduced through finding best

suppliers who can provide qualitative products at cost effective prices and reduce

material wastage. However, wages cost can be minimized through hiring labours at the

lower piece rate (Campbell and Brown, 2016). In addition, all the other overheads can be

controlled by effectively utilizing and allocating resources and continuous monitoring.

Moreover, large production level also provides benefits of economies of scale and

reduces per unit cost. Quality improvement: It is the most important factor in manufacturing industry. Jeffrey

&Sons can improve Exquisite quality by using good quality of material and innovated

technological process (Goetsch and Davis, 2014). Furthermore, TQM is a technique

which can be used for the overall quality management of company's product.

Enhance corporate value: Growth in shareholders worth, business expansion, large

investment, new product development, improving competitive position, large customer

base, brand loyalty and entering into new markets makes Jeffrey & Son's able to enhance

its business value (Chatterji and Fabrizio, 2014).

TASK 3

3.1 Nature and Purpose of Budgeting process

Nature of Budgeting Process:

By preparing the budget, finance manager of Jeffrey & Son’s focus on gathering all the

required information for preparing suitable and realistic budget (Anderson, 2011). The data can

be related to different departments such as production, sales, marketing etc. which company

possess. Further, all the sources of income are recorded in the budget so as to identify the

potential ways through which company can generate its revenue (Adler, 2013). Further, these

sources can be sales, lease, investment etc. as they are prepared for financial products. In this,

manager predicts the future sales performance of business on the basis of current economic

environment. In addition to this, manager of Jeffrey &Sons can forecast the expenditures with

the help of materials, labours and overheads. Further, by carrying out comparison between

revenue generated and expenditure incurred manager can easily evaluate deficit and surplus

position of the business (Debarishi, 2011). Thereafter, Jeffrey & Son’s managers have to focus

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.