Financial Analysis: Management Accounting Report for Jeffrey and Son's

VerifiedAdded on 2020/02/05

|23

|5849

|40

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to a case study of Jeffrey and Son's, a company that manufactures the Exquisite brand products. The report begins with an introduction to management accounting and its importance, followed by an analysis of cost classification, including direct and indirect costs, and cost behavior. It then delves into the calculation of unit costs and total job costs, along with an explanation of absorption costing techniques. The report also covers the preparation and analysis of cost reports, the use of performance indicators for identifying areas for improvement, and strategies for cost reduction and value enhancement. Furthermore, it examines the budgeting process, including different budgeting methods and the preparation of various budgets, such as production and cash budgets. The report concludes with a discussion of variance calculations, reconciliation statements, and findings presented to management, providing insights into the company's financial performance and areas for potential improvement.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Different types of cost classification......................................................................................3

1.2 Calculating unit cost and total job cost..................................................................................4

1.3 Calculating cost of Exquisite using absorption costing technique ........................................4

1.4 Analyzing cost of Exquisite...................................................................................................8

TASK 2 ...........................................................................................................................................8

2.1 Preparing and analyzing cost report for the month of September ........................................8

2.2 Using performance indicators to identify areas for potential improvement........................10

2.3 Ways to reduce cost and enhance value, quality..................................................................10

TASK 3 .........................................................................................................................................11

3.1 Purpose and nature of budgeting process.............................................................................11

3.2 Selecting appropriate budgeting methods for organization.................................................11

3.3 Preparation of different types of budget..............................................................................12

3.4 Preparation of cash budget ..................................................................................................13

TASK 4 .........................................................................................................................................17

4.1 Calculation of variance .......................................................................................................17

4.2 Preparation of reconciliation operating statement .............................................................18

4.3 Findings to management in accordance with identified responsibility centers...................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Different types of cost classification......................................................................................3

1.2 Calculating unit cost and total job cost..................................................................................4

1.3 Calculating cost of Exquisite using absorption costing technique ........................................4

1.4 Analyzing cost of Exquisite...................................................................................................8

TASK 2 ...........................................................................................................................................8

2.1 Preparing and analyzing cost report for the month of September ........................................8

2.2 Using performance indicators to identify areas for potential improvement........................10

2.3 Ways to reduce cost and enhance value, quality..................................................................10

TASK 3 .........................................................................................................................................11

3.1 Purpose and nature of budgeting process.............................................................................11

3.2 Selecting appropriate budgeting methods for organization.................................................11

3.3 Preparation of different types of budget..............................................................................12

3.4 Preparation of cash budget ..................................................................................................13

TASK 4 .........................................................................................................................................17

4.1 Calculation of variance .......................................................................................................17

4.2 Preparation of reconciliation operating statement .............................................................18

4.3 Findings to management in accordance with identified responsibility centers...................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................21

2

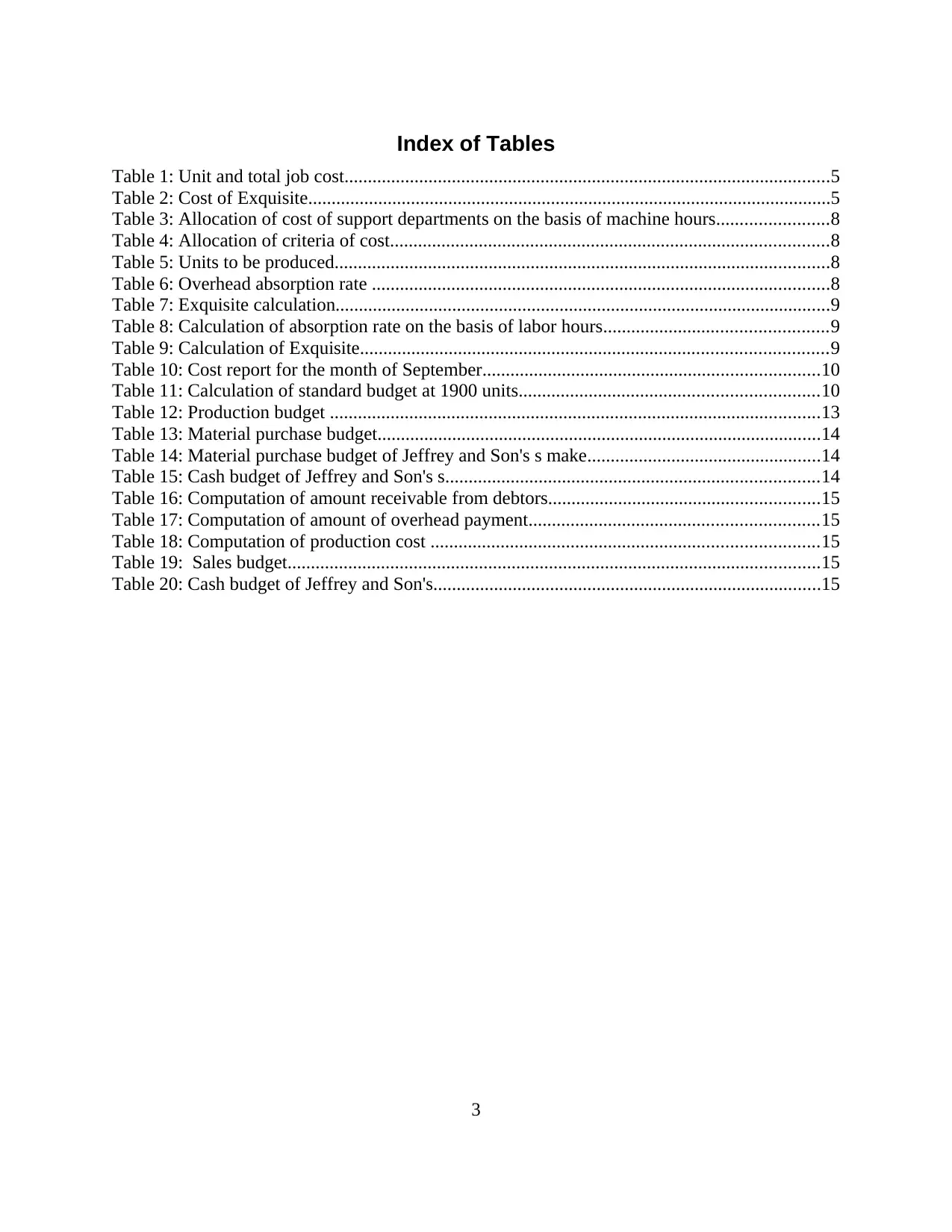

Index of Tables

Table 1: Unit and total job cost........................................................................................................5

Table 2: Cost of Exquisite................................................................................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................8

Table 4: Allocation of criteria of cost..............................................................................................8

Table 5: Units to be produced..........................................................................................................8

Table 6: Overhead absorption rate ..................................................................................................8

Table 7: Exquisite calculation..........................................................................................................9

Table 8: Calculation of absorption rate on the basis of labor hours................................................9

Table 9: Calculation of Exquisite....................................................................................................9

Table 10: Cost report for the month of September........................................................................10

Table 11: Calculation of standard budget at 1900 units................................................................10

Table 12: Production budget .........................................................................................................13

Table 13: Material purchase budget...............................................................................................14

Table 14: Material purchase budget of Jeffrey and Son's s make..................................................14

Table 15: Cash budget of Jeffrey and Son's s................................................................................14

Table 16: Computation of amount receivable from debtors..........................................................15

Table 17: Computation of amount of overhead payment..............................................................15

Table 18: Computation of production cost ...................................................................................15

Table 19: Sales budget..................................................................................................................15

Table 20: Cash budget of Jeffrey and Son's...................................................................................15

3

Table 1: Unit and total job cost........................................................................................................5

Table 2: Cost of Exquisite................................................................................................................5

Table 3: Allocation of cost of support departments on the basis of machine hours........................8

Table 4: Allocation of criteria of cost..............................................................................................8

Table 5: Units to be produced..........................................................................................................8

Table 6: Overhead absorption rate ..................................................................................................8

Table 7: Exquisite calculation..........................................................................................................9

Table 8: Calculation of absorption rate on the basis of labor hours................................................9

Table 9: Calculation of Exquisite....................................................................................................9

Table 10: Cost report for the month of September........................................................................10

Table 11: Calculation of standard budget at 1900 units................................................................10

Table 12: Production budget .........................................................................................................13

Table 13: Material purchase budget...............................................................................................14

Table 14: Material purchase budget of Jeffrey and Son's s make..................................................14

Table 15: Cash budget of Jeffrey and Son's s................................................................................14

Table 16: Computation of amount receivable from debtors..........................................................15

Table 17: Computation of amount of overhead payment..............................................................15

Table 18: Computation of production cost ...................................................................................15

Table 19: Sales budget..................................................................................................................15

Table 20: Cash budget of Jeffrey and Son's...................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the imperative aspect for any organization as it determine

organization long run growth and success. It enables management to allocate financial resources

for all business activities effectively so as to achieve long as well as short term objectives.

Present report is based on case study of Jeffrey and Son's which manufactures popular brand

products as Exquisite. The cited organization want to reduce operating cost due to competitive

nature of environment. In this regard cost of products and services has been calculated by taking

into account margin of profit. Furthermore, absorption of costing techniques have been

explained. In addition to this, appropriate budgeting methods are also described.

TASK 1

1.1 Different types of cost classification

Cost are classified in different aspect and these are explained as follows- Element-It is the most important factor in allocating cost of products and services. Here,

cost is classified into direct and indirect which are related to production activities or other

related. Further, direct cost consists of lighting, heating and material. On the other hand,

examples of indirect cost are not directly related to production. It includes administrative

expenses and salaries of higher staff etc (Cohen and Kaimenaki, 2011). Function- There are several functions performed in Jeffrey and Son's such as

production, finance, sales and marketing. It facilitates to carry out business activities in

an effectual manner. It helps to select pricing strategy effectively and increase overall

flow of production in the marketplace (Jones and Clatworthy, 2006). Nature-According to nature cost is divided into three parts such as labour, overhead

expense and material. It assists corporation to differentiate all the functions effectively

and accordingly allocate cost for each department (Kate-Riin Kont, 2012).

Behavior-According to behavior cost is mainly divided into three parts such fixed, semi

fixed and variables (Mock, Coram and Monroe, 2011). Here, variable cost includes labor

and material whereas example of semi fixed cost is telephone bill which remain constant

to a particular level.

4

Management accounting is the imperative aspect for any organization as it determine

organization long run growth and success. It enables management to allocate financial resources

for all business activities effectively so as to achieve long as well as short term objectives.

Present report is based on case study of Jeffrey and Son's which manufactures popular brand

products as Exquisite. The cited organization want to reduce operating cost due to competitive

nature of environment. In this regard cost of products and services has been calculated by taking

into account margin of profit. Furthermore, absorption of costing techniques have been

explained. In addition to this, appropriate budgeting methods are also described.

TASK 1

1.1 Different types of cost classification

Cost are classified in different aspect and these are explained as follows- Element-It is the most important factor in allocating cost of products and services. Here,

cost is classified into direct and indirect which are related to production activities or other

related. Further, direct cost consists of lighting, heating and material. On the other hand,

examples of indirect cost are not directly related to production. It includes administrative

expenses and salaries of higher staff etc (Cohen and Kaimenaki, 2011). Function- There are several functions performed in Jeffrey and Son's such as

production, finance, sales and marketing. It facilitates to carry out business activities in

an effectual manner. It helps to select pricing strategy effectively and increase overall

flow of production in the marketplace (Jones and Clatworthy, 2006). Nature-According to nature cost is divided into three parts such as labour, overhead

expense and material. It assists corporation to differentiate all the functions effectively

and accordingly allocate cost for each department (Kate-Riin Kont, 2012).

Behavior-According to behavior cost is mainly divided into three parts such fixed, semi

fixed and variables (Mock, Coram and Monroe, 2011). Here, variable cost includes labor

and material whereas example of semi fixed cost is telephone bill which remain constant

to a particular level.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

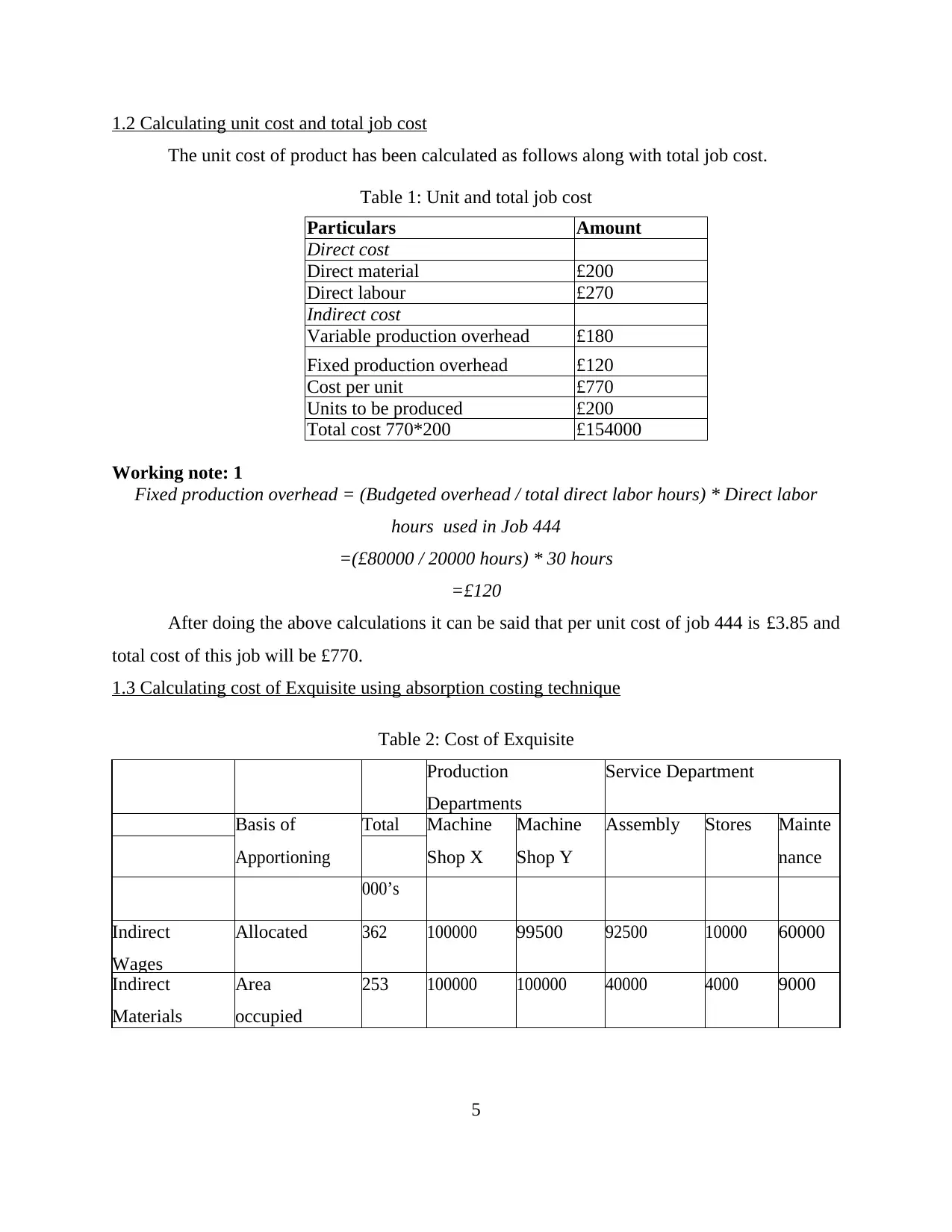

1.2 Calculating unit cost and total job cost

The unit cost of product has been calculated as follows along with total job cost.

Table 1: Unit and total job cost

Particulars Amount

Direct cost

Direct material £200

Direct labour £270

Indirect cost

Variable production overhead £180

Fixed production overhead £120

Cost per unit £770

Units to be produced £200

Total cost 770*200 £154000

Working note: 1

Fixed production overhead = (Budgeted overhead / total direct labor hours) * Direct labor

hours used in Job 444

=(£80000 / 20000 hours) * 30 hours

=£120

After doing the above calculations it can be said that per unit cost of job 444 is £3.85 and

total cost of this job will be £770.

1.3 Calculating cost of Exquisite using absorption costing technique

Table 2: Cost of Exquisite

Production

Departments

Service Department

Basis of

Apportioning

Total Machine

Shop X

Machine

Shop Y

Assembly Stores Mainte

nance

000’s

Indirect

Wages

Allocated 362 100000 99500 92500 10000 60000

Indirect

Materials

Area

occupied

253 100000 100000 40000 4000 9000

5

The unit cost of product has been calculated as follows along with total job cost.

Table 1: Unit and total job cost

Particulars Amount

Direct cost

Direct material £200

Direct labour £270

Indirect cost

Variable production overhead £180

Fixed production overhead £120

Cost per unit £770

Units to be produced £200

Total cost 770*200 £154000

Working note: 1

Fixed production overhead = (Budgeted overhead / total direct labor hours) * Direct labor

hours used in Job 444

=(£80000 / 20000 hours) * 30 hours

=£120

After doing the above calculations it can be said that per unit cost of job 444 is £3.85 and

total cost of this job will be £770.

1.3 Calculating cost of Exquisite using absorption costing technique

Table 2: Cost of Exquisite

Production

Departments

Service Department

Basis of

Apportioning

Total Machine

Shop X

Machine

Shop Y

Assembly Stores Mainte

nance

000’s

Indirect

Wages

Allocated 362 100000 99500 92500 10000 60000

Indirect

Materials

Area

occupied

253 100000 100000 40000 4000 9000

5

Lighting

Heating

& Area

Occupied

50 10000 5000 15000 15000 5000

Rent Area

Occupied

100 20000 10000 30000 30000 10000

Insurance &

Machinery

Book value

of Machinery

15 7947 4967 993 497 596

Depreciation

of Machinery

Book value

of Machinery

150 79470 49669 9934 4967 5960

Insurance of

Building

Area

Occupied

25 5000 2500 7500

7500

2500

Salaries

Works

of No.

employees

of 80 24000 16000 24000 8000 8000

Sub Totals 1035 346417 287636 219927 79964 101056

Re-

of service

dept. cost

Stores Dept. 39982 29987 9995 (79964)

Maintenance 48507 32338 20211 (101056

Totals 434906 349961 250133 0 0

Working Note

Lighting & Heating: Machinery X 10/50 x £50000 — f10000

Machinery Y 5/50 x £50000 — £5000

Assembly 15/50 x £50000 — f 15000

Stores 15/50 x £50000 = £15000

Maintenance 5/50 x £50000 = £15000

Rent Machinery X 10/50 x £100000 = f20000

Machinery Y 5/50 x £100000 = £10000

Assembly 15/50 x £100000 = £30000 Stores

6

Heating

& Area

Occupied

50 10000 5000 15000 15000 5000

Rent Area

Occupied

100 20000 10000 30000 30000 10000

Insurance &

Machinery

Book value

of Machinery

15 7947 4967 993 497 596

Depreciation

of Machinery

Book value

of Machinery

150 79470 49669 9934 4967 5960

Insurance of

Building

Area

Occupied

25 5000 2500 7500

7500

2500

Salaries

Works

of No.

employees

of 80 24000 16000 24000 8000 8000

Sub Totals 1035 346417 287636 219927 79964 101056

Re-

of service

dept. cost

Stores Dept. 39982 29987 9995 (79964)

Maintenance 48507 32338 20211 (101056

Totals 434906 349961 250133 0 0

Working Note

Lighting & Heating: Machinery X 10/50 x £50000 — f10000

Machinery Y 5/50 x £50000 — £5000

Assembly 15/50 x £50000 — f 15000

Stores 15/50 x £50000 = £15000

Maintenance 5/50 x £50000 = £15000

Rent Machinery X 10/50 x £100000 = f20000

Machinery Y 5/50 x £100000 = £10000

Assembly 15/50 x £100000 = £30000 Stores

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

15/50 x £100000= £30000 Maintenance 5/50

x £100000 = £10000

Insurance & Machinery Machinery X 800/1510 x £15000 = £7964

Machinery Y 500/1510 x £15000 — £4966

Assembly 100/1510 x 15000 — £994 Stores

50/1510 x £15000= f 497

Maintenance 5/1510 x £15000= £596

Depreciation of Machinery Machinery X 800/1510 x £150000 = £79470

Machinery Y 500/1510 x £150000 = £49669

Assembly 100/1510 x £150000 = £9934

Stores 50/1510 x £150000 = £497

Maintenance 60/1510 x £150000 = £596

Insurance of Buildings Machinery X 15/50 x £25000 — £5000

Machinery Y 5/50 x £25000 = £2500

Assembly 15/50 x £25000 = f7500 Stores

15/50 x £25000 — £7500

Maintenance 5/50 x £25000 = £2500

Salaries of works mgmt. Machinery X 3/10 x £80000 = £24000

Machinery Y 2/10 x :E80000 = £16000

Assembly 3/10 x £80000 = £24000

Stores 1/10 x £80000 — £8000

Maintenance 1/10 x £80000 = £8000

Reappointing workings: based on material issues

Machinery X 400/800* £79964 = £39982

Machinery Y 300/800 * £79964 = £29987

Assembly 100/800 * £79964 = £99995

Based on time spent

Machinery x 12/25 * £101056 = £48507

7

x £100000 = £10000

Insurance & Machinery Machinery X 800/1510 x £15000 = £7964

Machinery Y 500/1510 x £15000 — £4966

Assembly 100/1510 x 15000 — £994 Stores

50/1510 x £15000= f 497

Maintenance 5/1510 x £15000= £596

Depreciation of Machinery Machinery X 800/1510 x £150000 = £79470

Machinery Y 500/1510 x £150000 = £49669

Assembly 100/1510 x £150000 = £9934

Stores 50/1510 x £150000 = £497

Maintenance 60/1510 x £150000 = £596

Insurance of Buildings Machinery X 15/50 x £25000 — £5000

Machinery Y 5/50 x £25000 = £2500

Assembly 15/50 x £25000 = f7500 Stores

15/50 x £25000 — £7500

Maintenance 5/50 x £25000 = £2500

Salaries of works mgmt. Machinery X 3/10 x £80000 = £24000

Machinery Y 2/10 x :E80000 = £16000

Assembly 3/10 x £80000 = £24000

Stores 1/10 x £80000 — £8000

Maintenance 1/10 x £80000 = £8000

Reappointing workings: based on material issues

Machinery X 400/800* £79964 = £39982

Machinery Y 300/800 * £79964 = £29987

Assembly 100/800 * £79964 = £99995

Based on time spent

Machinery x 12/25 * £101056 = £48507

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

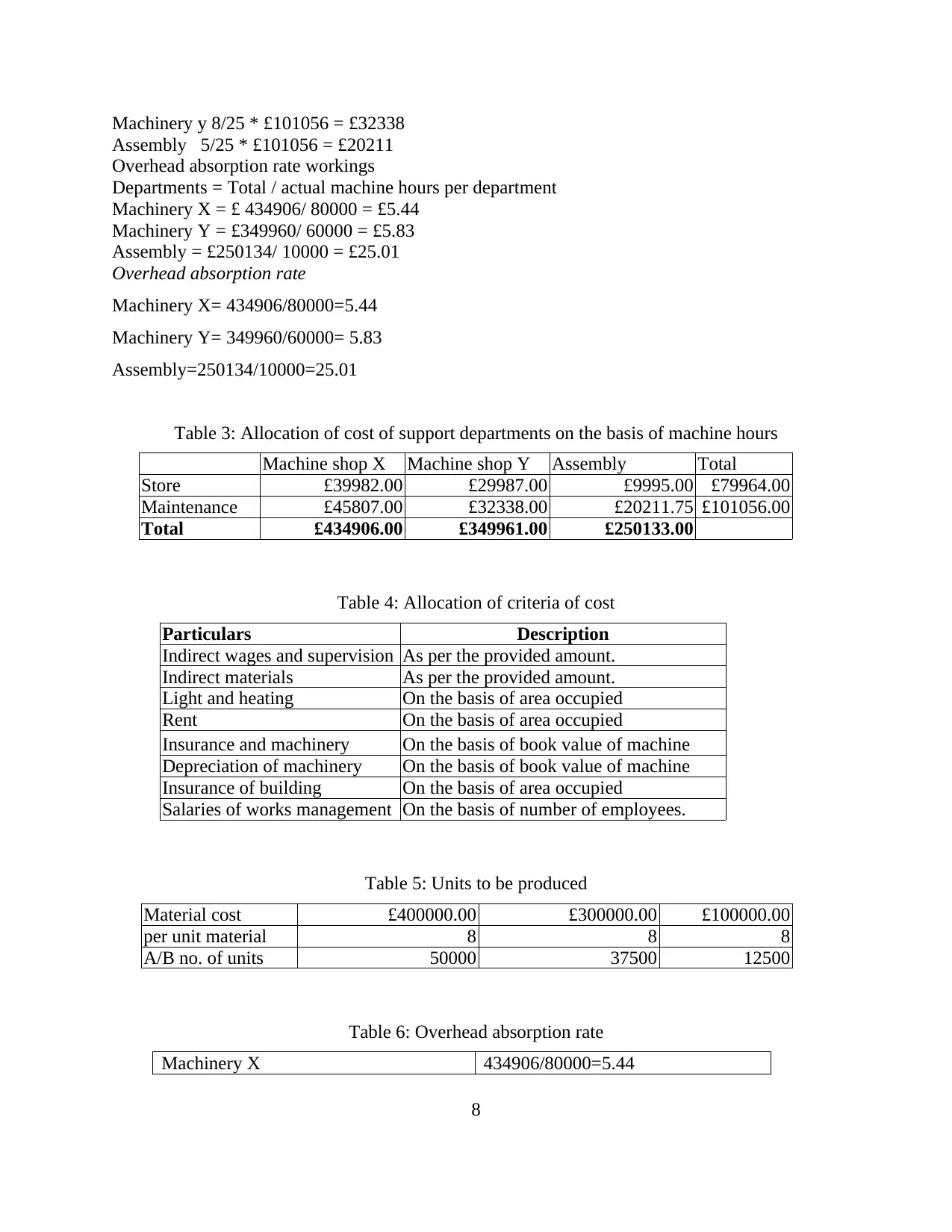

Machinery y 8/25 * £101056 = £32338

Assembly 5/25 * £101056 = £20211

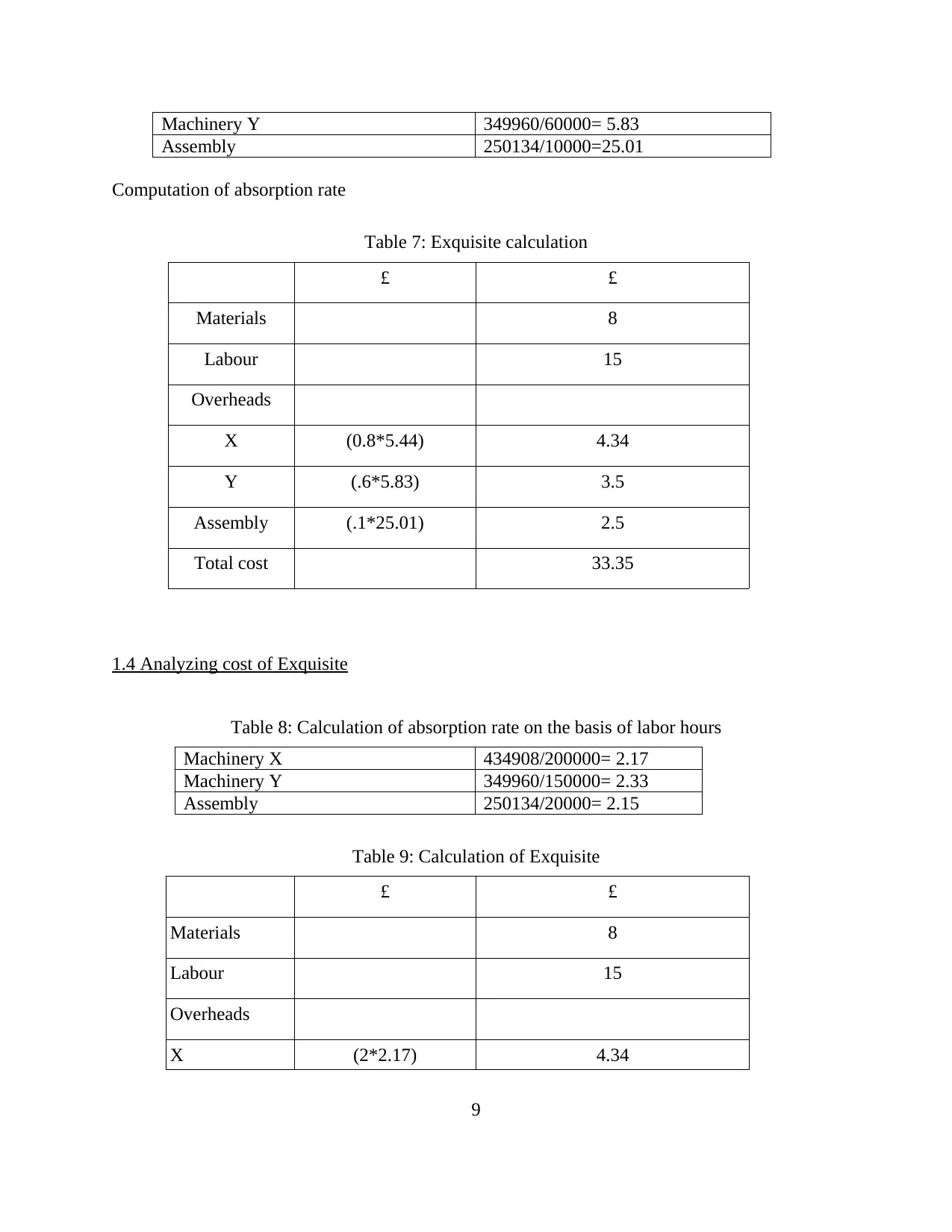

Overhead absorption rate workings

Departments = Total / actual machine hours per department

Machinery X = £ 434906/ 80000 = £5.44

Machinery Y = £349960/ 60000 = £5.83

Assembly = £250134/ 10000 = £25.01

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39982.00 £29987.00 £9995.00 £79964.00

Maintenance £45807.00 £32338.00 £20211.75 £101056.00

Total £434906.00 £349961.00 £250133.00

Table 4: Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 5: Units to be produced

Material cost £400000.00 £300000.00 £100000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Table 6: Overhead absorption rate

Machinery X 434906/80000=5.44

8

Assembly 5/25 * £101056 = £20211

Overhead absorption rate workings

Departments = Total / actual machine hours per department

Machinery X = £ 434906/ 80000 = £5.44

Machinery Y = £349960/ 60000 = £5.83

Assembly = £250134/ 10000 = £25.01

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Table 3: Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39982.00 £29987.00 £9995.00 £79964.00

Maintenance £45807.00 £32338.00 £20211.75 £101056.00

Total £434906.00 £349961.00 £250133.00

Table 4: Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

Salaries of works management On the basis of number of employees.

Table 5: Units to be produced

Material cost £400000.00 £300000.00 £100000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Table 6: Overhead absorption rate

Machinery X 434906/80000=5.44

8

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Table 7: Exquisite calculation

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing cost of Exquisite

Table 8: Calculation of absorption rate on the basis of labor hours

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

Assembly 250134/20000= 2.15

Table 9: Calculation of Exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

9

Assembly 250134/10000=25.01

Computation of absorption rate

Table 7: Exquisite calculation

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing cost of Exquisite

Table 8: Calculation of absorption rate on the basis of labor hours

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

Assembly 250134/20000= 2.15

Table 9: Calculation of Exquisite

£ £

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

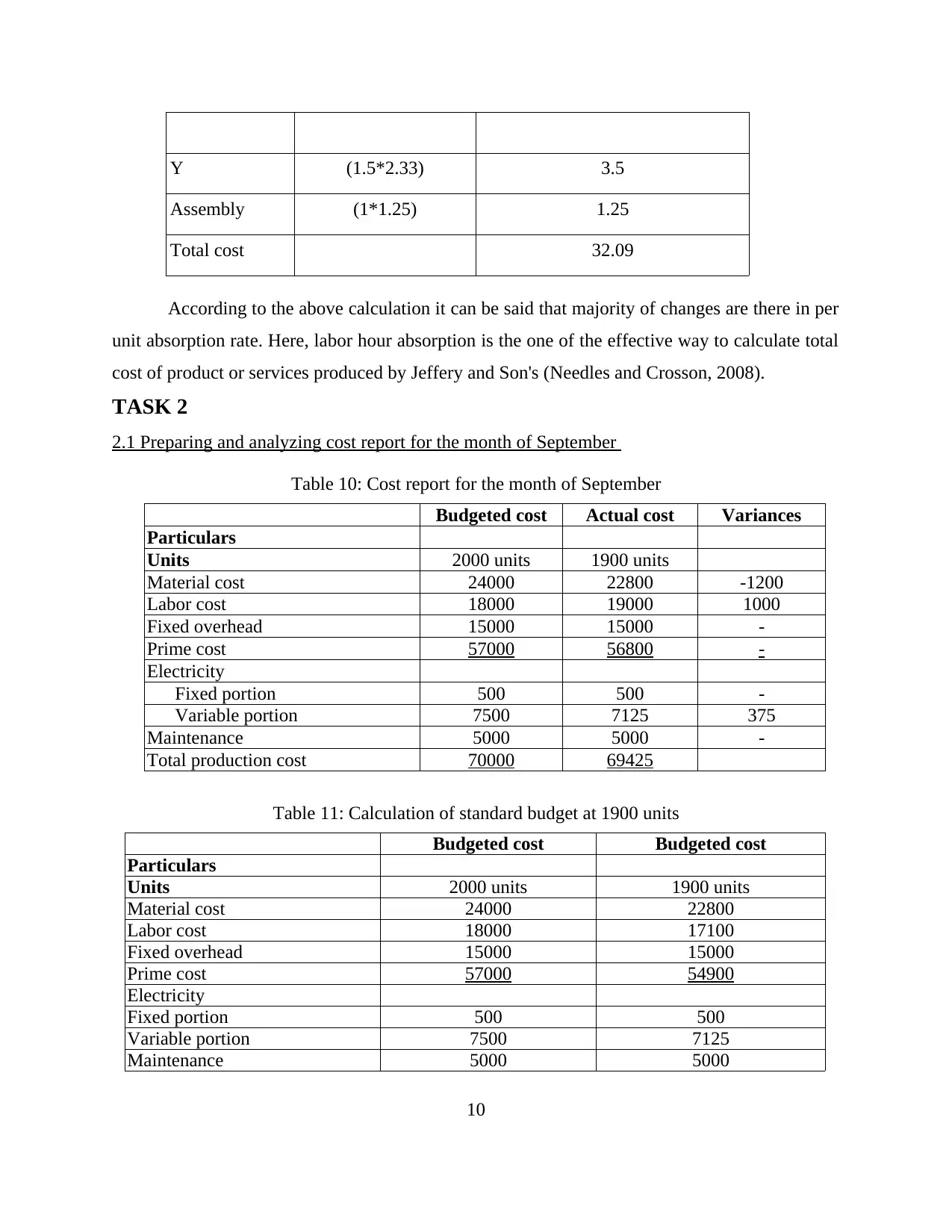

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

According to the above calculation it can be said that majority of changes are there in per

unit absorption rate. Here, labor hour absorption is the one of the effective way to calculate total

cost of product or services produced by Jeffery and Son's (Needles and Crosson, 2008).

TASK 2

2.1 Preparing and analyzing cost report for the month of September

Table 10: Cost report for the month of September

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

Table 11: Calculation of standard budget at 1900 units

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

10

Assembly (1*1.25) 1.25

Total cost 32.09

According to the above calculation it can be said that majority of changes are there in per

unit absorption rate. Here, labor hour absorption is the one of the effective way to calculate total

cost of product or services produced by Jeffery and Son's (Needles and Crosson, 2008).

TASK 2

2.1 Preparing and analyzing cost report for the month of September

Table 10: Cost report for the month of September

Budgeted cost Actual cost Variances

Particulars

Units 2000 units 1900 units

Material cost 24000 22800 -1200

Labor cost 18000 19000 1000

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 7500 7125 375

Maintenance 5000 5000 -

Total production cost 70000 69425

Table 11: Calculation of standard budget at 1900 units

Budgeted cost Budgeted cost

Particulars

Units 2000 units 1900 units

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 7500 7125

Maintenance 5000 5000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

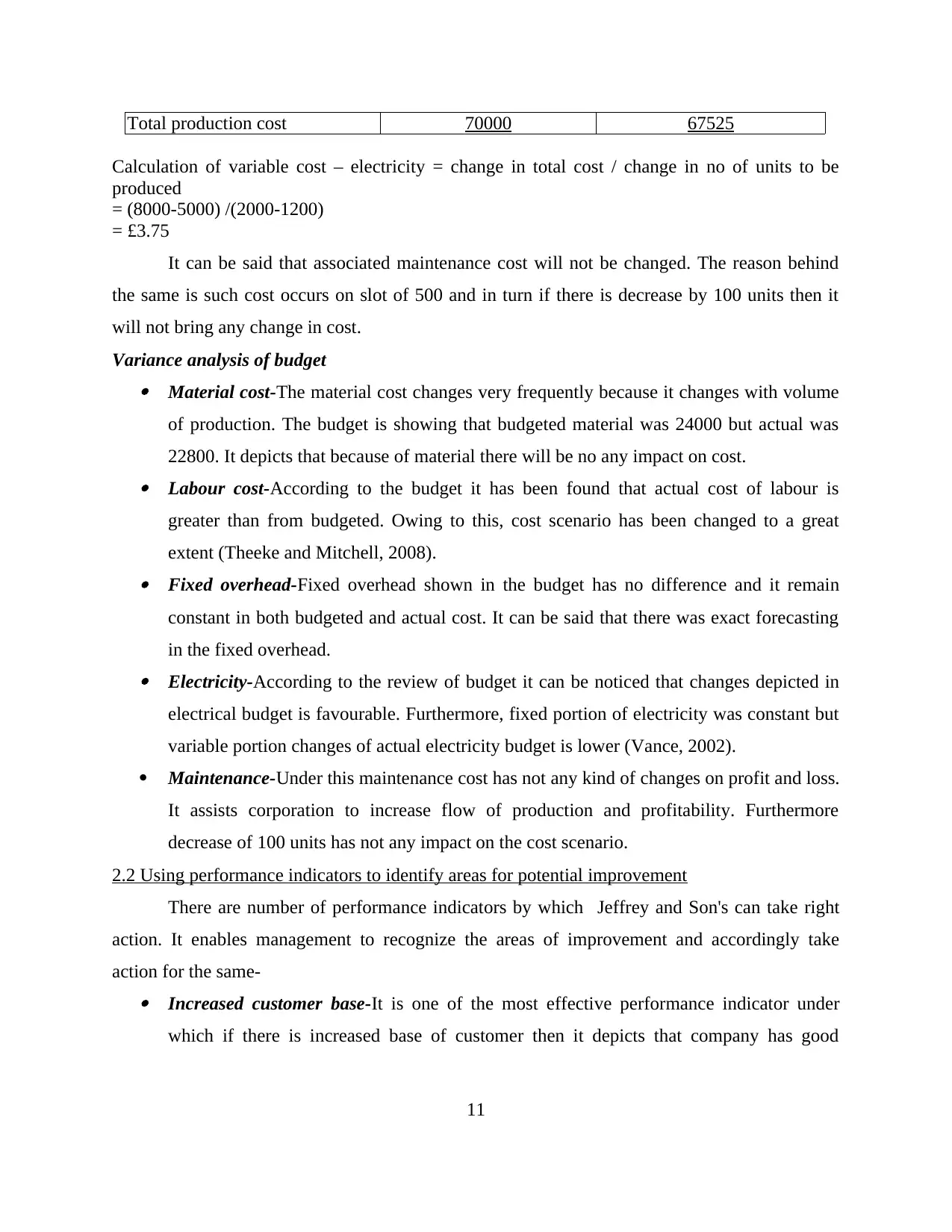

Total production cost 70000 67525

Calculation of variable cost – electricity = change in total cost / change in no of units to be

produced

= (8000-5000) /(2000-1200)

= £3.75

It can be said that associated maintenance cost will not be changed. The reason behind

the same is such cost occurs on slot of 500 and in turn if there is decrease by 100 units then it

will not bring any change in cost.

Variance analysis of budget Material cost-The material cost changes very frequently because it changes with volume

of production. The budget is showing that budgeted material was 24000 but actual was

22800. It depicts that because of material there will be no any impact on cost. Labour cost-According to the budget it has been found that actual cost of labour is

greater than from budgeted. Owing to this, cost scenario has been changed to a great

extent (Theeke and Mitchell, 2008). Fixed overhead-Fixed overhead shown in the budget has no difference and it remain

constant in both budgeted and actual cost. It can be said that there was exact forecasting

in the fixed overhead. Electricity-According to the review of budget it can be noticed that changes depicted in

electrical budget is favourable. Furthermore, fixed portion of electricity was constant but

variable portion changes of actual electricity budget is lower (Vance, 2002).

Maintenance-Under this maintenance cost has not any kind of changes on profit and loss.

It assists corporation to increase flow of production and profitability. Furthermore

decrease of 100 units has not any impact on the cost scenario.

2.2 Using performance indicators to identify areas for potential improvement

There are number of performance indicators by which Jeffrey and Son's can take right

action. It enables management to recognize the areas of improvement and accordingly take

action for the same- Increased customer base-It is one of the most effective performance indicator under

which if there is increased base of customer then it depicts that company has good

11

Calculation of variable cost – electricity = change in total cost / change in no of units to be

produced

= (8000-5000) /(2000-1200)

= £3.75

It can be said that associated maintenance cost will not be changed. The reason behind

the same is such cost occurs on slot of 500 and in turn if there is decrease by 100 units then it

will not bring any change in cost.

Variance analysis of budget Material cost-The material cost changes very frequently because it changes with volume

of production. The budget is showing that budgeted material was 24000 but actual was

22800. It depicts that because of material there will be no any impact on cost. Labour cost-According to the budget it has been found that actual cost of labour is

greater than from budgeted. Owing to this, cost scenario has been changed to a great

extent (Theeke and Mitchell, 2008). Fixed overhead-Fixed overhead shown in the budget has no difference and it remain

constant in both budgeted and actual cost. It can be said that there was exact forecasting

in the fixed overhead. Electricity-According to the review of budget it can be noticed that changes depicted in

electrical budget is favourable. Furthermore, fixed portion of electricity was constant but

variable portion changes of actual electricity budget is lower (Vance, 2002).

Maintenance-Under this maintenance cost has not any kind of changes on profit and loss.

It assists corporation to increase flow of production and profitability. Furthermore

decrease of 100 units has not any impact on the cost scenario.

2.2 Using performance indicators to identify areas for potential improvement

There are number of performance indicators by which Jeffrey and Son's can take right

action. It enables management to recognize the areas of improvement and accordingly take

action for the same- Increased customer base-It is one of the most effective performance indicator under

which if there is increased base of customer then it depicts that company has good

11

performance. On the other hand, in case of decreasing base of buyers show downward

trend of corporation (Vanderbeck, 2012). High profitability-This is another effective method and decrease or increase in the same

depicts organization growth and success in the marketplace.

High market share-This shows that how well an organization is performing. For example

in case Jeffrey and Son's has low market share which depicts that company is not

performing good and its needs some improvement. Accordingly corrective actions are

taken (Weygandt and et. al., 2009).

2.3 Ways to reduce cost and enhance value, quality

There are several ways to reduce cost and enables value as well as quality of products and

services offered by company. It enables management to increase flow of production and cover

cost of the same by increasing profit margin (Young, 2008). On the other hand total quality

management is the most effective method under which quality of product is assessed in proper

manner. This aid to increase buyers and accordingly rate of return will also be increased.

Furthermore, training should be provided to personnel so as to reduce waste material and use

them in the production process. This will determine long run success of company in the

marketplace with increased rate of return (Elmassri and Harris, 2011).

TASK 3

3.1 Purpose and nature of budgeting process

The budget is most important process which facilitates to give certainty for future

business activities. It enables corporation to deliver good quality of services to large number of

buyers and maintaining flow of production in an effectual manner (Nyamori, 2009). Further,

budget process helps to control expenses and achieve the set objectives of company.

Nature of budgeting process

The budgeting process is most imperative aspect under which management need to

consider requirement of business as well as mission and vision of the same. In this regard all

experienced workforce are included in the team and they make collective decision in order to

achieve organizational objectives (Schoute and Wiersma, 2011). Furthermore, overall budgeting

process is based on uncertainty wherein company find that what the potential barriers which can

12

trend of corporation (Vanderbeck, 2012). High profitability-This is another effective method and decrease or increase in the same

depicts organization growth and success in the marketplace.

High market share-This shows that how well an organization is performing. For example

in case Jeffrey and Son's has low market share which depicts that company is not

performing good and its needs some improvement. Accordingly corrective actions are

taken (Weygandt and et. al., 2009).

2.3 Ways to reduce cost and enhance value, quality

There are several ways to reduce cost and enables value as well as quality of products and

services offered by company. It enables management to increase flow of production and cover

cost of the same by increasing profit margin (Young, 2008). On the other hand total quality

management is the most effective method under which quality of product is assessed in proper

manner. This aid to increase buyers and accordingly rate of return will also be increased.

Furthermore, training should be provided to personnel so as to reduce waste material and use

them in the production process. This will determine long run success of company in the

marketplace with increased rate of return (Elmassri and Harris, 2011).

TASK 3

3.1 Purpose and nature of budgeting process

The budget is most important process which facilitates to give certainty for future

business activities. It enables corporation to deliver good quality of services to large number of

buyers and maintaining flow of production in an effectual manner (Nyamori, 2009). Further,

budget process helps to control expenses and achieve the set objectives of company.

Nature of budgeting process

The budgeting process is most imperative aspect under which management need to

consider requirement of business as well as mission and vision of the same. In this regard all

experienced workforce are included in the team and they make collective decision in order to

achieve organizational objectives (Schoute and Wiersma, 2011). Furthermore, overall budgeting

process is based on uncertainty wherein company find that what the potential barriers which can

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.