Financial Analysis of Jet2 and Ryanair: Performance Comparison Report

VerifiedAdded on 2020/04/21

|43

|7621

|169

Report

AI Summary

This report provides a financial comparison between Jet2, a British low-cost airline, and Ryanair, an Irish low-cost airline. The analysis focuses on profitability, liquidity, and debt ratios using data from 2013 to 2015. The report examines operating margin, net margin, return on equity, return on total assets, current ratio, quick ratio, and debt ratio to assess the financial health of both airlines. It includes time series and cross-sectional analyses, comparing their performance and identifying similarities and dissimilarities. The study concludes with recommendations for improving financial performance, considering the impact of the Eurozone and Brexit. The report highlights Ryanair's profitability and stable liquidity, while Jet2 faces challenges with debt and declining profit margins. The analysis offers valuable insights into the financial strategies and performance of these two major European airlines.

Running head: FINANCIAL ANALYSIS FOR MANAGERS

Financial Analysis for Managers

Name of the Student:

Name of the University

Author’ Note:

Course ID:

Financial Analysis for Managers

Name of the Student:

Name of the University

Author’ Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL ANALYSIS FOR MANAGERS

Table of Contents

Terms of reference:..........................................................................................................................2

Executive Summary:........................................................................................................................4

Ratio analysis:..................................................................................................................................5

Analysis of Jet2:..............................................................................................................................8

Analysis of Ryanair:......................................................................................................................14

Comparison between Jet2 and Ryanair:........................................................................................21

Conclusion and recommendations:................................................................................................26

References and Bibliographies:.....................................................................................................27

Appendices:...................................................................................................................................31

Table of Contents

Terms of reference:..........................................................................................................................2

Executive Summary:........................................................................................................................4

Ratio analysis:..................................................................................................................................5

Analysis of Jet2:..............................................................................................................................8

Analysis of Ryanair:......................................................................................................................14

Comparison between Jet2 and Ryanair:........................................................................................21

Conclusion and recommendations:................................................................................................26

References and Bibliographies:.....................................................................................................27

Appendices:...................................................................................................................................31

2FINANCIAL ANALYSIS FOR MANAGERS

Terms of reference:

In this report, a financial comparison has been carried out between two airlines, one is the

British low-cost airline, Jet2 and another is an Irish low-cost airline, Ryanair. Both had been

European carriers before the Brexit effect and these two airlines have benefitted and suffered

being members of the Euro zone, particularly during the declining stock market.

Ryanair is a low-cost airline in Ireland established in 1984 and it’s headquarter is located

in Swords, Dublin, Ireland. The primary operational bases of the airline are at London Stansted

and Dublin airports. It is the largest European airline in terms of scheduled passengers flown and

it has carried most global passengers in contrast to any other airline in 2016 (Ryanair.com

2017). The rapid expansion helps in characterising the airline, which is due to the deregulation of

the aviation industry in Europe in 1997 along with the success of its low-cost business model.

The route network of Ryanair serves 34 nations in Europe, the Middle East (Israel) and Africa

(Morocco).

Jet2 is a British low-cost airline based at Leeds Bradford Airport, England. It is the fourth

biggest scheduled airline in UK. In addition, the airline holds a “UK Civil Aviation Authority

Type A Operating Licence” for carrying passengers, cargo and mail aircrafts having 20 or

additional seats (Jet2.com 2017). The route network of Jet2 serves 47 sun destinations and its

employee base is around 4,000 in April 2015.

The financial analysis would be made for assessing the non-financial measures including

breakdown by various divisions and measures of corporate social responsibility, efficiency,

liquidity, profitability and gearing constituting of both time series and cross-sectional analyses

for both the airlines. Along with this, the similarities and dissimilarities of both the airlines

Terms of reference:

In this report, a financial comparison has been carried out between two airlines, one is the

British low-cost airline, Jet2 and another is an Irish low-cost airline, Ryanair. Both had been

European carriers before the Brexit effect and these two airlines have benefitted and suffered

being members of the Euro zone, particularly during the declining stock market.

Ryanair is a low-cost airline in Ireland established in 1984 and it’s headquarter is located

in Swords, Dublin, Ireland. The primary operational bases of the airline are at London Stansted

and Dublin airports. It is the largest European airline in terms of scheduled passengers flown and

it has carried most global passengers in contrast to any other airline in 2016 (Ryanair.com

2017). The rapid expansion helps in characterising the airline, which is due to the deregulation of

the aviation industry in Europe in 1997 along with the success of its low-cost business model.

The route network of Ryanair serves 34 nations in Europe, the Middle East (Israel) and Africa

(Morocco).

Jet2 is a British low-cost airline based at Leeds Bradford Airport, England. It is the fourth

biggest scheduled airline in UK. In addition, the airline holds a “UK Civil Aviation Authority

Type A Operating Licence” for carrying passengers, cargo and mail aircrafts having 20 or

additional seats (Jet2.com 2017). The route network of Jet2 serves 47 sun destinations and its

employee base is around 4,000 in April 2015.

The financial analysis would be made for assessing the non-financial measures including

breakdown by various divisions and measures of corporate social responsibility, efficiency,

liquidity, profitability and gearing constituting of both time series and cross-sectional analyses

for both the airlines. Along with this, the similarities and dissimilarities of both the airlines

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL ANALYSIS FOR MANAGERS

would be computed, after which a summary of the results would be drawn and suggestions

would be made for improving the financial performance of both the airlines.

would be computed, after which a summary of the results would be drawn and suggestions

would be made for improving the financial performance of both the airlines.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL ANALYSIS FOR MANAGERS

Executive Summary:

In this report, a financial comparison has been carried out between two airlines, one is the

British low-cost airline, Jet2 and another is an Irish low-cost airline, Ryanair. Both had been

European carriers before the Brexit effect and these two airlines have benefitted and suffered

being members of the Euro zone, particularly during the declining stock market. The primary

aim of ratio analysis is to compute and interpret the financial ratios for monitoring and

evaluating the financial position and performance of the organisations. The shareholders,

management and creditors of the concerned organisations would be interested in this analysis.

By comparing the profitability position, it could be inferred that Ryanair is leading in

terms of profit, while in terms of generating and providing returns, Jet2 is in a better position

compared to the former. Ryanair is enjoying a stable liquidity position in the UK aviation

industry compared to Jet2. Since the debt burden of Jet2 is greater in contrast to Ryanair, it could

be inferred that the former is more risky to become bankrupt in future. Although both the airlines

are struggling to maintain a competitive position in the market, Jet2 is in a better position

compared to Ryanair. Thus, it could be inferred that both the airlines are struggling to maintain

their solvency positions; however, if compared, Ryanair is in a favourable position in contrast to

Jet2.

To conclude, it could be observed that both the airlines being parts of the Euro zone, have

suffered as well as benefitted. Both the airlines depend on tax benefits for gains and in order to

restrict them from going into debt, they need to declare bankruptcy.

Executive Summary:

In this report, a financial comparison has been carried out between two airlines, one is the

British low-cost airline, Jet2 and another is an Irish low-cost airline, Ryanair. Both had been

European carriers before the Brexit effect and these two airlines have benefitted and suffered

being members of the Euro zone, particularly during the declining stock market. The primary

aim of ratio analysis is to compute and interpret the financial ratios for monitoring and

evaluating the financial position and performance of the organisations. The shareholders,

management and creditors of the concerned organisations would be interested in this analysis.

By comparing the profitability position, it could be inferred that Ryanair is leading in

terms of profit, while in terms of generating and providing returns, Jet2 is in a better position

compared to the former. Ryanair is enjoying a stable liquidity position in the UK aviation

industry compared to Jet2. Since the debt burden of Jet2 is greater in contrast to Ryanair, it could

be inferred that the former is more risky to become bankrupt in future. Although both the airlines

are struggling to maintain a competitive position in the market, Jet2 is in a better position

compared to Ryanair. Thus, it could be inferred that both the airlines are struggling to maintain

their solvency positions; however, if compared, Ryanair is in a favourable position in contrast to

Jet2.

To conclude, it could be observed that both the airlines being parts of the Euro zone, have

suffered as well as benefitted. Both the airlines depend on tax benefits for gains and in order to

restrict them from going into debt, they need to declare bankruptcy.

5FINANCIAL ANALYSIS FOR MANAGERS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL ANALYSIS FOR MANAGERS

Ratio analysis:

The primary aim of ratio analysis is to compute and interpret the financial ratios for

monitoring and evaluating the financial position and performance of the organisations. The

shareholders, management and creditors of the concerned organisations would be interested in

this analysis (Arrozio, Gonzales and Da Silva 2016). The following are the types of ratios that

would be computed:

Profitability ratios

Liquidity ratios

Debt ratios

Activity ratios

Gearing ratios

Profitability ratios:

In the words of Barnard et al. (2014), profitability ratios gauge the profit-generating

capability of an organisation in relation to assets, sales and equity. These ratios provide an

effective platform to judge the individual performance of an organisation and they are beneficial

to contrast a firm with its rivals in relation to the industrial benchmark. The profitability ratios

that would be considered in this report include the following:

Operating margin = Operating profit/ Sales revenue

Net margin = Net profit/ Sales revenue

Return on equity = Net profit/ Average shareholders’ equity

Ratio analysis:

The primary aim of ratio analysis is to compute and interpret the financial ratios for

monitoring and evaluating the financial position and performance of the organisations. The

shareholders, management and creditors of the concerned organisations would be interested in

this analysis (Arrozio, Gonzales and Da Silva 2016). The following are the types of ratios that

would be computed:

Profitability ratios

Liquidity ratios

Debt ratios

Activity ratios

Gearing ratios

Profitability ratios:

In the words of Barnard et al. (2014), profitability ratios gauge the profit-generating

capability of an organisation in relation to assets, sales and equity. These ratios provide an

effective platform to judge the individual performance of an organisation and they are beneficial

to contrast a firm with its rivals in relation to the industrial benchmark. The profitability ratios

that would be considered in this report include the following:

Operating margin = Operating profit/ Sales revenue

Net margin = Net profit/ Sales revenue

Return on equity = Net profit/ Average shareholders’ equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL ANALYSIS FOR MANAGERS

Return on total assets = Net profit/ Total assets

Liquidity ratios:

Liquidity explains the extent to which a security or an asset could be purchased quickly

or it could be sold in the market without having any impact on the price of the security or asset.

In this context, Attig and Cleary (2014) remarked that accounting liquidity gauges the ease

through which an individual or organisation could clear the financial obligations with liquid

assets available to them. The two liquidity ratios that would be applied in this report constitute of

the following:

Current ratio = Current assets/ Current liabilities

Quick ratio = (Current assets – Inventories – Prepaid expenses)/ Current liabilities

Debt ratios:

Debt ratios gauge the degree of leverage of an individual or a firm, which depicts the

portion of the assets owned on the part of the organisation and the amount financed through debt

(Bekaert and Hodrick 2017). The following debt ratio is taken into account in the form of

gearing, which is described later on in the report:

Debt ratio = Total liabilities/ Total assets

Activity ratios:

As pointed out by Bodie (2013), activity ratios gauge the ability of an organisation to

convert various accounts within the balance sheet statements into sales or cash. These ratios

gauge the relative efficacy of an organisation depending on asset utilisation, leverage and other

Return on total assets = Net profit/ Total assets

Liquidity ratios:

Liquidity explains the extent to which a security or an asset could be purchased quickly

or it could be sold in the market without having any impact on the price of the security or asset.

In this context, Attig and Cleary (2014) remarked that accounting liquidity gauges the ease

through which an individual or organisation could clear the financial obligations with liquid

assets available to them. The two liquidity ratios that would be applied in this report constitute of

the following:

Current ratio = Current assets/ Current liabilities

Quick ratio = (Current assets – Inventories – Prepaid expenses)/ Current liabilities

Debt ratios:

Debt ratios gauge the degree of leverage of an individual or a firm, which depicts the

portion of the assets owned on the part of the organisation and the amount financed through debt

(Bekaert and Hodrick 2017). The following debt ratio is taken into account in the form of

gearing, which is described later on in the report:

Debt ratio = Total liabilities/ Total assets

Activity ratios:

As pointed out by Bodie (2013), activity ratios gauge the ability of an organisation to

convert various accounts within the balance sheet statements into sales or cash. These ratios

gauge the relative efficacy of an organisation depending on asset utilisation, leverage and other

8FINANCIAL ANALYSIS FOR MANAGERS

items of balance sheet and they are significant in ascertaining whether the management of an

organisation is capable of generating cash and revenues from the available ratios. In this report,

the activity ratio that has been considered is the total asset turnover ratio, which would depict the

efficacy of an organisation in terms of asset utilisation for generating sales.

Total asset turnover ratio = Sales revenue/ Total assets

Gearing ratios:

Gearing ratio is a common term explaining a financial ratio, which contrasts some kind of

owner’s equity to borrowed funds. In this context, Brigham and Daves (2014) cited that gearing

is a measure related to financial leverage describing the extent to which the activities of an

organisation are financed on the part of the owner’s funds in contrast to the funds of the

creditors. The greater the degree of leverage of an organisation, the greater is the risk for the

organisation. For majority of the ratios, an acceptable level is ascertained by the comparison to

ratios of firms in the identical industry. The following gearing ratios have been taken into

consideration for this report:

Debt-to-equity ratio = Total debt/ Total equity

Times interest earned ratio = Operating profit/ Interest expense

Equity ratio = Total equity/ Total assets

items of balance sheet and they are significant in ascertaining whether the management of an

organisation is capable of generating cash and revenues from the available ratios. In this report,

the activity ratio that has been considered is the total asset turnover ratio, which would depict the

efficacy of an organisation in terms of asset utilisation for generating sales.

Total asset turnover ratio = Sales revenue/ Total assets

Gearing ratios:

Gearing ratio is a common term explaining a financial ratio, which contrasts some kind of

owner’s equity to borrowed funds. In this context, Brigham and Daves (2014) cited that gearing

is a measure related to financial leverage describing the extent to which the activities of an

organisation are financed on the part of the owner’s funds in contrast to the funds of the

creditors. The greater the degree of leverage of an organisation, the greater is the risk for the

organisation. For majority of the ratios, an acceptable level is ascertained by the comparison to

ratios of firms in the identical industry. The following gearing ratios have been taken into

consideration for this report:

Debt-to-equity ratio = Total debt/ Total equity

Times interest earned ratio = Operating profit/ Interest expense

Equity ratio = Total equity/ Total assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL ANALYSIS FOR MANAGERS

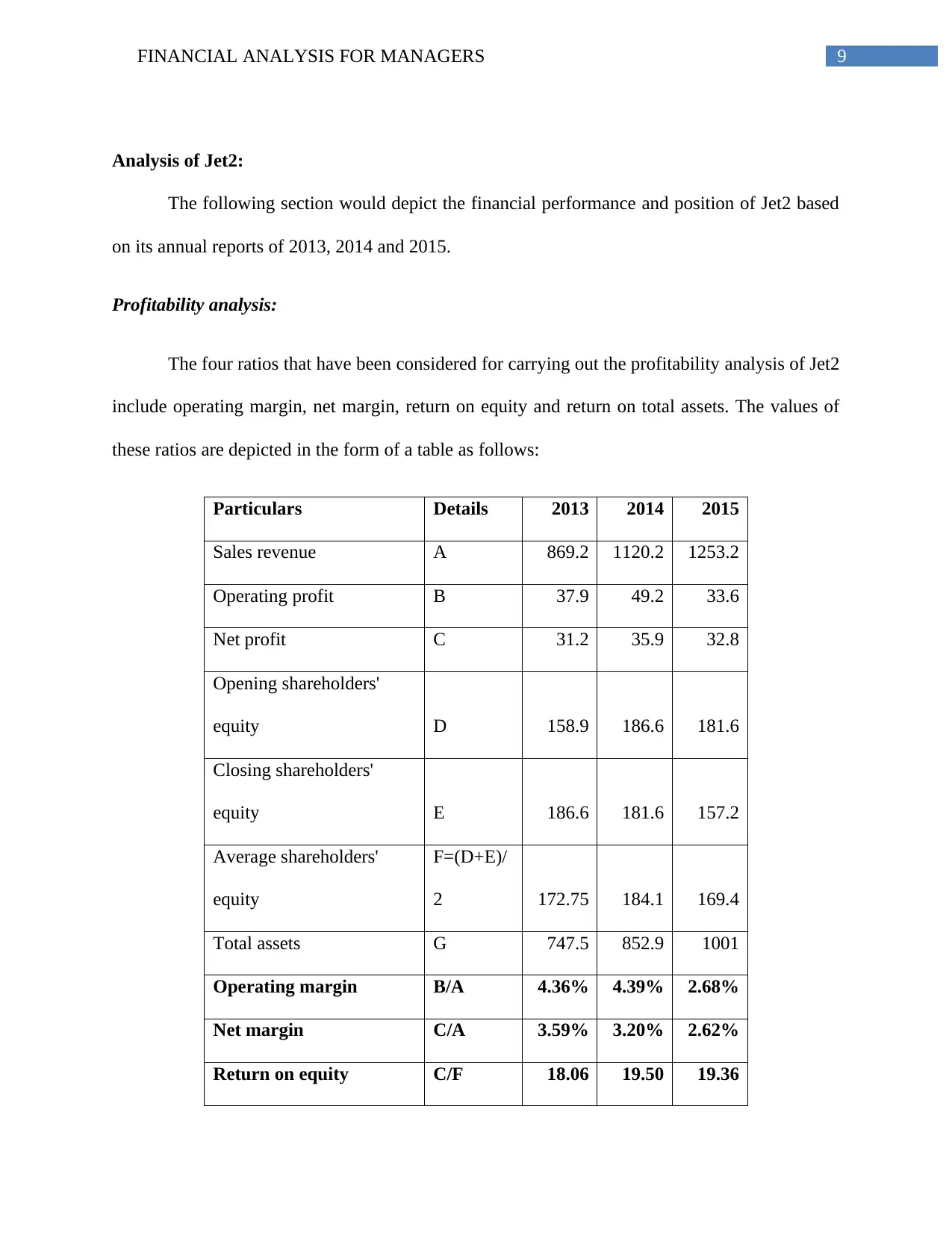

Analysis of Jet2:

The following section would depict the financial performance and position of Jet2 based

on its annual reports of 2013, 2014 and 2015.

Profitability analysis:

The four ratios that have been considered for carrying out the profitability analysis of Jet2

include operating margin, net margin, return on equity and return on total assets. The values of

these ratios are depicted in the form of a table as follows:

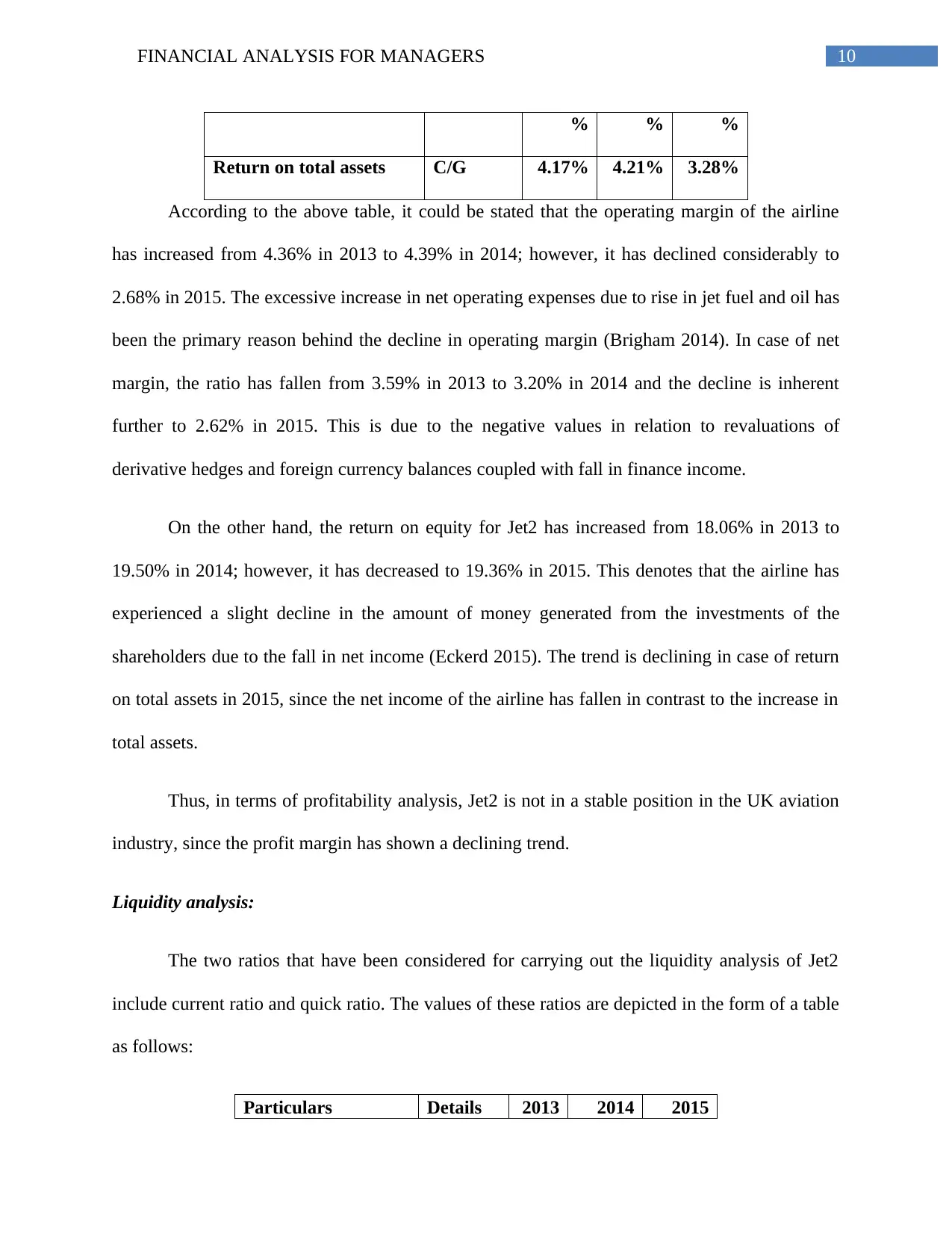

Particulars Details 2013 2014 2015

Sales revenue A 869.2 1120.2 1253.2

Operating profit B 37.9 49.2 33.6

Net profit C 31.2 35.9 32.8

Opening shareholders'

equity D 158.9 186.6 181.6

Closing shareholders'

equity E 186.6 181.6 157.2

Average shareholders'

equity

F=(D+E)/

2 172.75 184.1 169.4

Total assets G 747.5 852.9 1001

Operating margin B/A 4.36% 4.39% 2.68%

Net margin C/A 3.59% 3.20% 2.62%

Return on equity C/F 18.06 19.50 19.36

Analysis of Jet2:

The following section would depict the financial performance and position of Jet2 based

on its annual reports of 2013, 2014 and 2015.

Profitability analysis:

The four ratios that have been considered for carrying out the profitability analysis of Jet2

include operating margin, net margin, return on equity and return on total assets. The values of

these ratios are depicted in the form of a table as follows:

Particulars Details 2013 2014 2015

Sales revenue A 869.2 1120.2 1253.2

Operating profit B 37.9 49.2 33.6

Net profit C 31.2 35.9 32.8

Opening shareholders'

equity D 158.9 186.6 181.6

Closing shareholders'

equity E 186.6 181.6 157.2

Average shareholders'

equity

F=(D+E)/

2 172.75 184.1 169.4

Total assets G 747.5 852.9 1001

Operating margin B/A 4.36% 4.39% 2.68%

Net margin C/A 3.59% 3.20% 2.62%

Return on equity C/F 18.06 19.50 19.36

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL ANALYSIS FOR MANAGERS

% % %

Return on total assets C/G 4.17% 4.21% 3.28%

According to the above table, it could be stated that the operating margin of the airline

has increased from 4.36% in 2013 to 4.39% in 2014; however, it has declined considerably to

2.68% in 2015. The excessive increase in net operating expenses due to rise in jet fuel and oil has

been the primary reason behind the decline in operating margin (Brigham 2014). In case of net

margin, the ratio has fallen from 3.59% in 2013 to 3.20% in 2014 and the decline is inherent

further to 2.62% in 2015. This is due to the negative values in relation to revaluations of

derivative hedges and foreign currency balances coupled with fall in finance income.

On the other hand, the return on equity for Jet2 has increased from 18.06% in 2013 to

19.50% in 2014; however, it has decreased to 19.36% in 2015. This denotes that the airline has

experienced a slight decline in the amount of money generated from the investments of the

shareholders due to the fall in net income (Eckerd 2015). The trend is declining in case of return

on total assets in 2015, since the net income of the airline has fallen in contrast to the increase in

total assets.

Thus, in terms of profitability analysis, Jet2 is not in a stable position in the UK aviation

industry, since the profit margin has shown a declining trend.

Liquidity analysis:

The two ratios that have been considered for carrying out the liquidity analysis of Jet2

include current ratio and quick ratio. The values of these ratios are depicted in the form of a table

as follows:

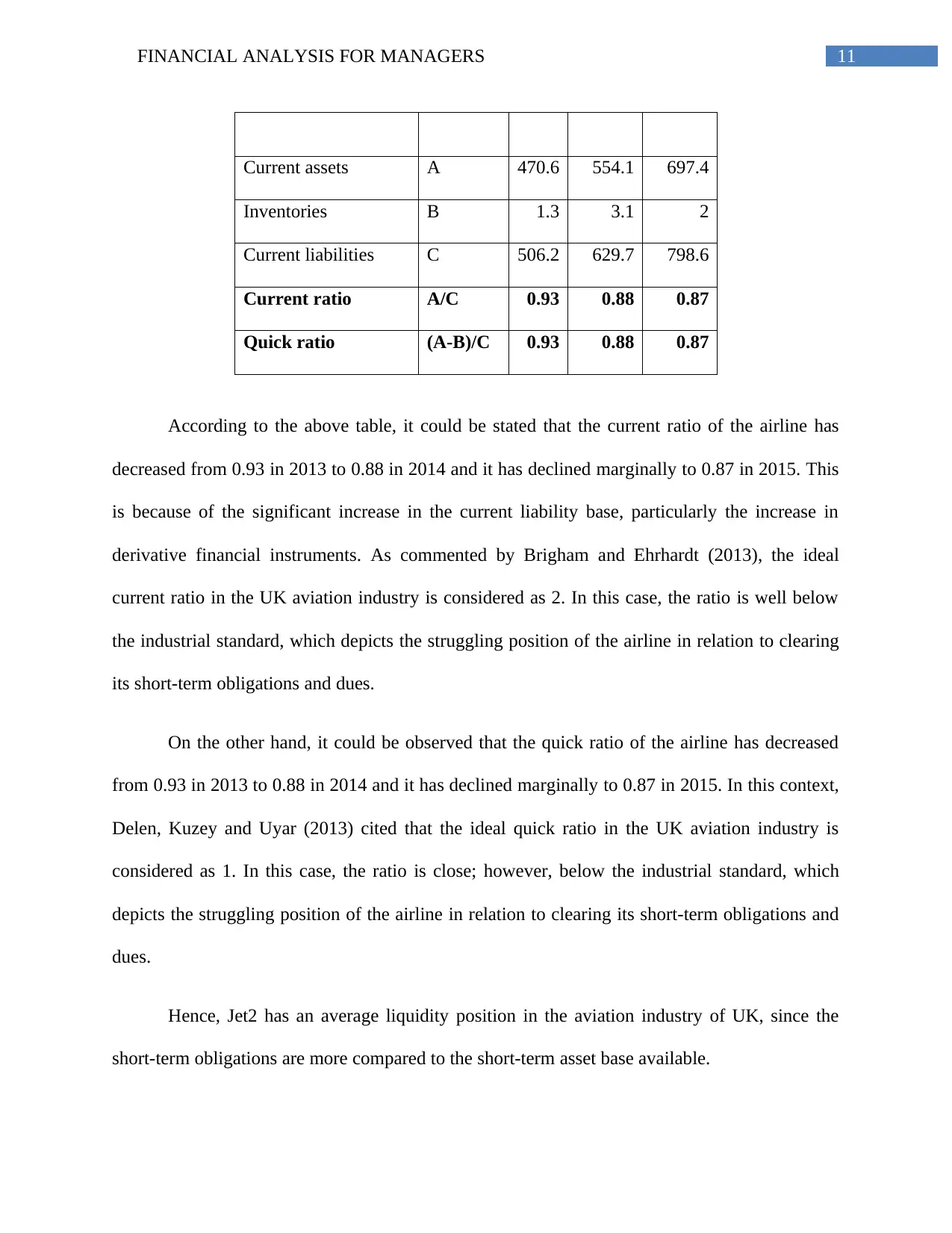

Particulars Details 2013 2014 2015

% % %

Return on total assets C/G 4.17% 4.21% 3.28%

According to the above table, it could be stated that the operating margin of the airline

has increased from 4.36% in 2013 to 4.39% in 2014; however, it has declined considerably to

2.68% in 2015. The excessive increase in net operating expenses due to rise in jet fuel and oil has

been the primary reason behind the decline in operating margin (Brigham 2014). In case of net

margin, the ratio has fallen from 3.59% in 2013 to 3.20% in 2014 and the decline is inherent

further to 2.62% in 2015. This is due to the negative values in relation to revaluations of

derivative hedges and foreign currency balances coupled with fall in finance income.

On the other hand, the return on equity for Jet2 has increased from 18.06% in 2013 to

19.50% in 2014; however, it has decreased to 19.36% in 2015. This denotes that the airline has

experienced a slight decline in the amount of money generated from the investments of the

shareholders due to the fall in net income (Eckerd 2015). The trend is declining in case of return

on total assets in 2015, since the net income of the airline has fallen in contrast to the increase in

total assets.

Thus, in terms of profitability analysis, Jet2 is not in a stable position in the UK aviation

industry, since the profit margin has shown a declining trend.

Liquidity analysis:

The two ratios that have been considered for carrying out the liquidity analysis of Jet2

include current ratio and quick ratio. The values of these ratios are depicted in the form of a table

as follows:

Particulars Details 2013 2014 2015

11FINANCIAL ANALYSIS FOR MANAGERS

Current assets A 470.6 554.1 697.4

Inventories B 1.3 3.1 2

Current liabilities C 506.2 629.7 798.6

Current ratio A/C 0.93 0.88 0.87

Quick ratio (A-B)/C 0.93 0.88 0.87

According to the above table, it could be stated that the current ratio of the airline has

decreased from 0.93 in 2013 to 0.88 in 2014 and it has declined marginally to 0.87 in 2015. This

is because of the significant increase in the current liability base, particularly the increase in

derivative financial instruments. As commented by Brigham and Ehrhardt (2013), the ideal

current ratio in the UK aviation industry is considered as 2. In this case, the ratio is well below

the industrial standard, which depicts the struggling position of the airline in relation to clearing

its short-term obligations and dues.

On the other hand, it could be observed that the quick ratio of the airline has decreased

from 0.93 in 2013 to 0.88 in 2014 and it has declined marginally to 0.87 in 2015. In this context,

Delen, Kuzey and Uyar (2013) cited that the ideal quick ratio in the UK aviation industry is

considered as 1. In this case, the ratio is close; however, below the industrial standard, which

depicts the struggling position of the airline in relation to clearing its short-term obligations and

dues.

Hence, Jet2 has an average liquidity position in the aviation industry of UK, since the

short-term obligations are more compared to the short-term asset base available.

Current assets A 470.6 554.1 697.4

Inventories B 1.3 3.1 2

Current liabilities C 506.2 629.7 798.6

Current ratio A/C 0.93 0.88 0.87

Quick ratio (A-B)/C 0.93 0.88 0.87

According to the above table, it could be stated that the current ratio of the airline has

decreased from 0.93 in 2013 to 0.88 in 2014 and it has declined marginally to 0.87 in 2015. This

is because of the significant increase in the current liability base, particularly the increase in

derivative financial instruments. As commented by Brigham and Ehrhardt (2013), the ideal

current ratio in the UK aviation industry is considered as 2. In this case, the ratio is well below

the industrial standard, which depicts the struggling position of the airline in relation to clearing

its short-term obligations and dues.

On the other hand, it could be observed that the quick ratio of the airline has decreased

from 0.93 in 2013 to 0.88 in 2014 and it has declined marginally to 0.87 in 2015. In this context,

Delen, Kuzey and Uyar (2013) cited that the ideal quick ratio in the UK aviation industry is

considered as 1. In this case, the ratio is close; however, below the industrial standard, which

depicts the struggling position of the airline in relation to clearing its short-term obligations and

dues.

Hence, Jet2 has an average liquidity position in the aviation industry of UK, since the

short-term obligations are more compared to the short-term asset base available.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 43

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.