University of Dhaka: JetBlue Airways IPO Valuation Project

VerifiedAdded on 2021/09/08

|20

|4727

|65

Project

AI Summary

This project is a comprehensive analysis of the JetBlue Airways IPO valuation. It begins with an introduction to the company and the scope of the study, followed by an analysis of the economic conditions and industry dynamics, including Porter's Five Forces and PESTEL analysis. The report then delves into a company analysis, including SWOT analysis, ratio analysis (profitability, liquidity, and risk), DuPont analysis, and Z-score calculations to assess financial distress. The core problem statement focuses on determining the optimal IPO offer price. The report explores alternative courses of action, including overpricing and underpricing scenarios, and utilizes discounted cash flow (DCF) and multiple valuation methods to arrive at a recommendation. The project aims to provide a detailed valuation of the JetBlue Airways IPO and suggest an ideal price for the stocks.

1

JetBlue Airways: IPO Valuation

JetBlue Airways: IPO Valuation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

JetBlue Airways: IPO Valuation

Prepared for:

M. Sadiqul Islam

Professor

Department of Finance

Faculty of Business Studies

University of Dhaka

Prepared by:

Group No:

Section: A

BBA 23rd Batch

Serial Name ID Marks

1 Minhajur Rahman Joy 23-106

2 Md. Foyez Alam 23-155

3 H. M. Rahat Fida 23-187

4 Md. Riaj Morshed 23-197

Date of Submission: Aug 16, 2020

JetBlue Airways: IPO Valuation

Prepared for:

M. Sadiqul Islam

Professor

Department of Finance

Faculty of Business Studies

University of Dhaka

Prepared by:

Group No:

Section: A

BBA 23rd Batch

Serial Name ID Marks

1 Minhajur Rahman Joy 23-106

2 Md. Foyez Alam 23-155

3 H. M. Rahat Fida 23-187

4 Md. Riaj Morshed 23-197

Date of Submission: Aug 16, 2020

3

Letter of Transmittal

Aug 16, 2020

M. Sadiqul Islam

Professor

Department of Finance,

Faculty of Business Studies

University of Dhaka.

Subject: Submission of the semester term paper.

Dear Sir:

It is our pleasure to submit the term paper of our 7 th semester course Investment Banking &

Lease Financing (F-403). It has been a privilege for us to have this opportunity to apply our

academic knowledge in real life situations through this case study.

We tried our level best to put sincere effort for the preparation of this term paper. As

undergraduate students, it is usual that inadequacy or error may arise and it may lack

professionalism in some cases. For any unintentional inadequacy in the term paper, your

sympathetic consideration would be highly appreciated. In addition, we will enthusiastically

welcome any clarification and suggestion about any view and conception disseminated in the

report.

We, therefore, pray that you would be kind enough to accept our report for evaluation and

oblige thereby.

Sincerely,

………………………………

Minhajur Rahman Joy

On behalf of Group no.

Section: A

Department of Finance

University of Dhaka

Letter of Transmittal

Aug 16, 2020

M. Sadiqul Islam

Professor

Department of Finance,

Faculty of Business Studies

University of Dhaka.

Subject: Submission of the semester term paper.

Dear Sir:

It is our pleasure to submit the term paper of our 7 th semester course Investment Banking &

Lease Financing (F-403). It has been a privilege for us to have this opportunity to apply our

academic knowledge in real life situations through this case study.

We tried our level best to put sincere effort for the preparation of this term paper. As

undergraduate students, it is usual that inadequacy or error may arise and it may lack

professionalism in some cases. For any unintentional inadequacy in the term paper, your

sympathetic consideration would be highly appreciated. In addition, we will enthusiastically

welcome any clarification and suggestion about any view and conception disseminated in the

report.

We, therefore, pray that you would be kind enough to accept our report for evaluation and

oblige thereby.

Sincerely,

………………………………

Minhajur Rahman Joy

On behalf of Group no.

Section: A

Department of Finance

University of Dhaka

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Table of Contents

Executive Summary ................................................................................................................. 5

Chapter 01: Introduction ........................................................................................................ 6

1.1 Scope of the study: ............................................................................................................... 6

1.2 Methodology of the study: ................................................................................................... 6

Primary Data: ......................................................................................................................... 6

Secondary Data: ..................................................................................................................... 6

Chapter 02: Analysis of Economy .......................................................................................... 7

Chapter 03: Industry Analysis ................................................................................................ 8

Porters Five Forces............................................................................................................... 8

PESTEL Analysis ................................................................................................................... 9

Chapter 04: Company Analysis ............................................................................................ 10

SWOT Analysis .................................................................................................................. 10

Ratio Analysis ..................................................................................................................... 10

Profitability Ratio ............................................................................................................. 10

Liquidity Ratio .................................................................................................................. 10

Risk Analysis ....................................................................................................................... 10

Probability of Financial Distress ...................................................................................... 10

DuPont Analysis ................................................................................................................. 11

Decompose ROE ................................................................................................................. 11

Chapter 05: Problem Statement ........................................................................................... 12

Chapter 07: Analysis of Each Alternatives .......................................................................... 14

Alternative Evaluation: Over Pricing....................................................................................... 14

Alternative Evaluation: Under Pricing..................................................................................... 14

Chapter 08: Valuation ........................................................................................................... 15

Discounted Cash Flow Approach ............................................................................................ 15

Multiple Valuation ................................................................................................................... 16

Chapter 09: Recommendation .............................................................................................. 18

Table of Contents

Executive Summary ................................................................................................................. 5

Chapter 01: Introduction ........................................................................................................ 6

1.1 Scope of the study: ............................................................................................................... 6

1.2 Methodology of the study: ................................................................................................... 6

Primary Data: ......................................................................................................................... 6

Secondary Data: ..................................................................................................................... 6

Chapter 02: Analysis of Economy .......................................................................................... 7

Chapter 03: Industry Analysis ................................................................................................ 8

Porters Five Forces............................................................................................................... 8

PESTEL Analysis ................................................................................................................... 9

Chapter 04: Company Analysis ............................................................................................ 10

SWOT Analysis .................................................................................................................. 10

Ratio Analysis ..................................................................................................................... 10

Profitability Ratio ............................................................................................................. 10

Liquidity Ratio .................................................................................................................. 10

Risk Analysis ....................................................................................................................... 10

Probability of Financial Distress ...................................................................................... 10

DuPont Analysis ................................................................................................................. 11

Decompose ROE ................................................................................................................. 11

Chapter 05: Problem Statement ........................................................................................... 12

Chapter 07: Analysis of Each Alternatives .......................................................................... 14

Alternative Evaluation: Over Pricing....................................................................................... 14

Alternative Evaluation: Under Pricing..................................................................................... 14

Chapter 08: Valuation ........................................................................................................... 15

Discounted Cash Flow Approach ............................................................................................ 15

Multiple Valuation ................................................................................................................... 16

Chapter 09: Recommendation .............................................................................................. 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Executive Summary

JetBlue Airways set an extraordinary example the US airline industry by keeping a steady

growth since its first founding in February 1999. It managed to stay profitable even after the

infamous September 11, 2001 event by its affordable point to point comfortable air travel. And

to maintain the growing trend of the management decided to raise capital by offering stocks to

the public.

Though the initial pricing for each stock was ranging from $22 to $ 24. The massive demand

for 5.5 million stock being offered encouraged them to raise the price range to $25 to $26.

But valuating their company and evaluating other alternatives suggest that the pricing for the

stocks is still underpriced. And the suggested price for each stock is around $26 to $29.

Otherwise, they are leaving behind a lot of potential capital to be raised.

Executive Summary

JetBlue Airways set an extraordinary example the US airline industry by keeping a steady

growth since its first founding in February 1999. It managed to stay profitable even after the

infamous September 11, 2001 event by its affordable point to point comfortable air travel. And

to maintain the growing trend of the management decided to raise capital by offering stocks to

the public.

Though the initial pricing for each stock was ranging from $22 to $ 24. The massive demand

for 5.5 million stock being offered encouraged them to raise the price range to $25 to $26.

But valuating their company and evaluating other alternatives suggest that the pricing for the

stocks is still underpriced. And the suggested price for each stock is around $26 to $29.

Otherwise, they are leaving behind a lot of potential capital to be raised.

6

Chapter 01: Introduction

This report illustrates the valuation of the IPO of the JetBlue Airways and how it affected the

rest of the US economy. They focused more on the customer experience at a more affordable

cost than others. JetBlue Airways kept their costs low by using only one type of aircraft and

efficient training process. Taking cost cutting measures and online based customer services

helped them to stay profitable in the most challenging times.

1.1 Scope of the study:

JetBlue Airways kept on being profitable even though the rest of the US Airlines were facing

loses due to mishaps during 2001. So, the IPO valuation of JetBlue Airways is a very intriguing

study to learn how the company went about to manage such a feat.

1.2 Methodology of the study:

The report uses data collected from public sources and other related studies done on such

industry. For industry and company analysis the Porter’s Five Forces and Pestel analysis has

been implemented. And alternative courses of action have been evaluated and compared to the

actual decision JetBlue Airways decided to adapt.

Primary Data:

No primary data were used in this study.

Secondary Data:

Data from JetBlue Airway’s prospectus and their financial statements has been referenced as

secondary data for this study.

Chapter 01: Introduction

This report illustrates the valuation of the IPO of the JetBlue Airways and how it affected the

rest of the US economy. They focused more on the customer experience at a more affordable

cost than others. JetBlue Airways kept their costs low by using only one type of aircraft and

efficient training process. Taking cost cutting measures and online based customer services

helped them to stay profitable in the most challenging times.

1.1 Scope of the study:

JetBlue Airways kept on being profitable even though the rest of the US Airlines were facing

loses due to mishaps during 2001. So, the IPO valuation of JetBlue Airways is a very intriguing

study to learn how the company went about to manage such a feat.

1.2 Methodology of the study:

The report uses data collected from public sources and other related studies done on such

industry. For industry and company analysis the Porter’s Five Forces and Pestel analysis has

been implemented. And alternative courses of action have been evaluated and compared to the

actual decision JetBlue Airways decided to adapt.

Primary Data:

No primary data were used in this study.

Secondary Data:

Data from JetBlue Airway’s prospectus and their financial statements has been referenced as

secondary data for this study.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Chapter 02: Analysis of Economy

Highlights:

Stalled US economy for nearly two years in 2002

Lowest interest rate in a generation

The yield of current long-term US Treasuries is 5%

The yield of current short-term US Treasuries is 2%

Market risk premium is 5%

Market experts forecast steady 4% inflation for next 10 years.

This are some of the information available in the case to give us an indication about the

condition of the economy in the near future.

US economy was already stalling up to two years by April of 2002, leading Federal Reserve

to take Expansionary policy to help boost the economy. Meaning, it lowered the interest rate.

Lowest interest in its generation. Current long-term bond yield was 5%, short term bond yield

was 2% and risk premium was 5%.

The goal was to encourage investment in the economy. A lower interest rate meant people

were more likely to have a growth in disposable income and invest more. Also, a rise in

investment lowers unemployment. Lowering of the unemployment rate made the market

experts to forecast a steady 4% inflation for the next 10 years.

Expansionary policies often tend to increase the price of the Bond as the relation between

interest rate and bond is inverse in relation. So, at that point in the economy people were

more likely to shift their investments to Stock market which helped JetBlue Airways in their

capital raising.

Chapter 02: Analysis of Economy

Highlights:

Stalled US economy for nearly two years in 2002

Lowest interest rate in a generation

The yield of current long-term US Treasuries is 5%

The yield of current short-term US Treasuries is 2%

Market risk premium is 5%

Market experts forecast steady 4% inflation for next 10 years.

This are some of the information available in the case to give us an indication about the

condition of the economy in the near future.

US economy was already stalling up to two years by April of 2002, leading Federal Reserve

to take Expansionary policy to help boost the economy. Meaning, it lowered the interest rate.

Lowest interest in its generation. Current long-term bond yield was 5%, short term bond yield

was 2% and risk premium was 5%.

The goal was to encourage investment in the economy. A lower interest rate meant people

were more likely to have a growth in disposable income and invest more. Also, a rise in

investment lowers unemployment. Lowering of the unemployment rate made the market

experts to forecast a steady 4% inflation for the next 10 years.

Expansionary policies often tend to increase the price of the Bond as the relation between

interest rate and bond is inverse in relation. So, at that point in the economy people were

more likely to shift their investments to Stock market which helped JetBlue Airways in their

capital raising.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

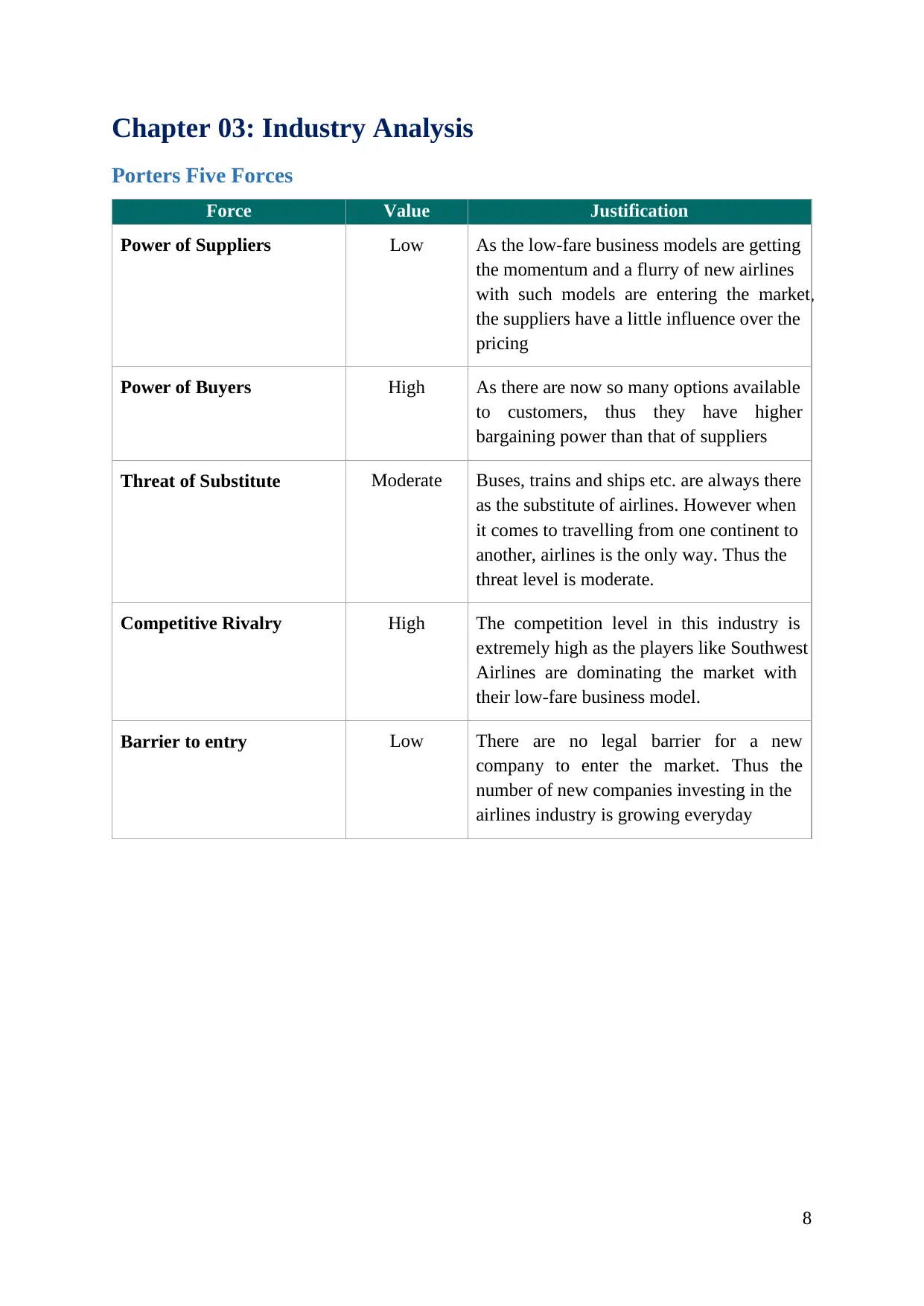

Chapter 03: Industry Analysis

Porters Five Forces

Force Value Justification

Power of Suppliers Low As the low-fare business models are getting

the momentum and a flurry of new airlines

with such models are entering the market,

the suppliers have a little influence over the

pricing

Power of Buyers High As there are now so many options available

to customers, thus they have higher

bargaining power than that of suppliers

Threat of Substitute Moderate Buses, trains and ships etc. are always there

as the substitute of airlines. However when

it comes to travelling from one continent to

another, airlines is the only way. Thus the

threat level is moderate.

Competitive Rivalry High The competition level in this industry is

extremely high as the players like Southwest

Airlines are dominating the market with

their low-fare business model.

Barrier to entry Low There are no legal barrier for a new

company to enter the market. Thus the

number of new companies investing in the

airlines industry is growing everyday

Chapter 03: Industry Analysis

Porters Five Forces

Force Value Justification

Power of Suppliers Low As the low-fare business models are getting

the momentum and a flurry of new airlines

with such models are entering the market,

the suppliers have a little influence over the

pricing

Power of Buyers High As there are now so many options available

to customers, thus they have higher

bargaining power than that of suppliers

Threat of Substitute Moderate Buses, trains and ships etc. are always there

as the substitute of airlines. However when

it comes to travelling from one continent to

another, airlines is the only way. Thus the

threat level is moderate.

Competitive Rivalry High The competition level in this industry is

extremely high as the players like Southwest

Airlines are dominating the market with

their low-fare business model.

Barrier to entry Low There are no legal barrier for a new

company to enter the market. Thus the

number of new companies investing in the

airlines industry is growing everyday

9

PESTEL Analysis

Economic

Low fare business model started to disrupt the

industry since 2002

Social

Low level of motivation to travel via airlines

after the 9/11 attack

Environmental

No data was available in the case regarding

the environmental impact of the industry

Political

The government is showing dedicated support to

the airlines industry after 9/11 attack

Technological

Increasing use of technologies such as laptop

computers, bulletproof Kevlar doors and security

cameras

Legal

The SEC required firms selling equity in public

markets solicit the commission’s approval

PESTEL Analysis

Economic

Low fare business model started to disrupt the

industry since 2002

Social

Low level of motivation to travel via airlines

after the 9/11 attack

Environmental

No data was available in the case regarding

the environmental impact of the industry

Political

The government is showing dedicated support to

the airlines industry after 9/11 attack

Technological

Increasing use of technologies such as laptop

computers, bulletproof Kevlar doors and security

cameras

Legal

The SEC required firms selling equity in public

markets solicit the commission’s approval

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

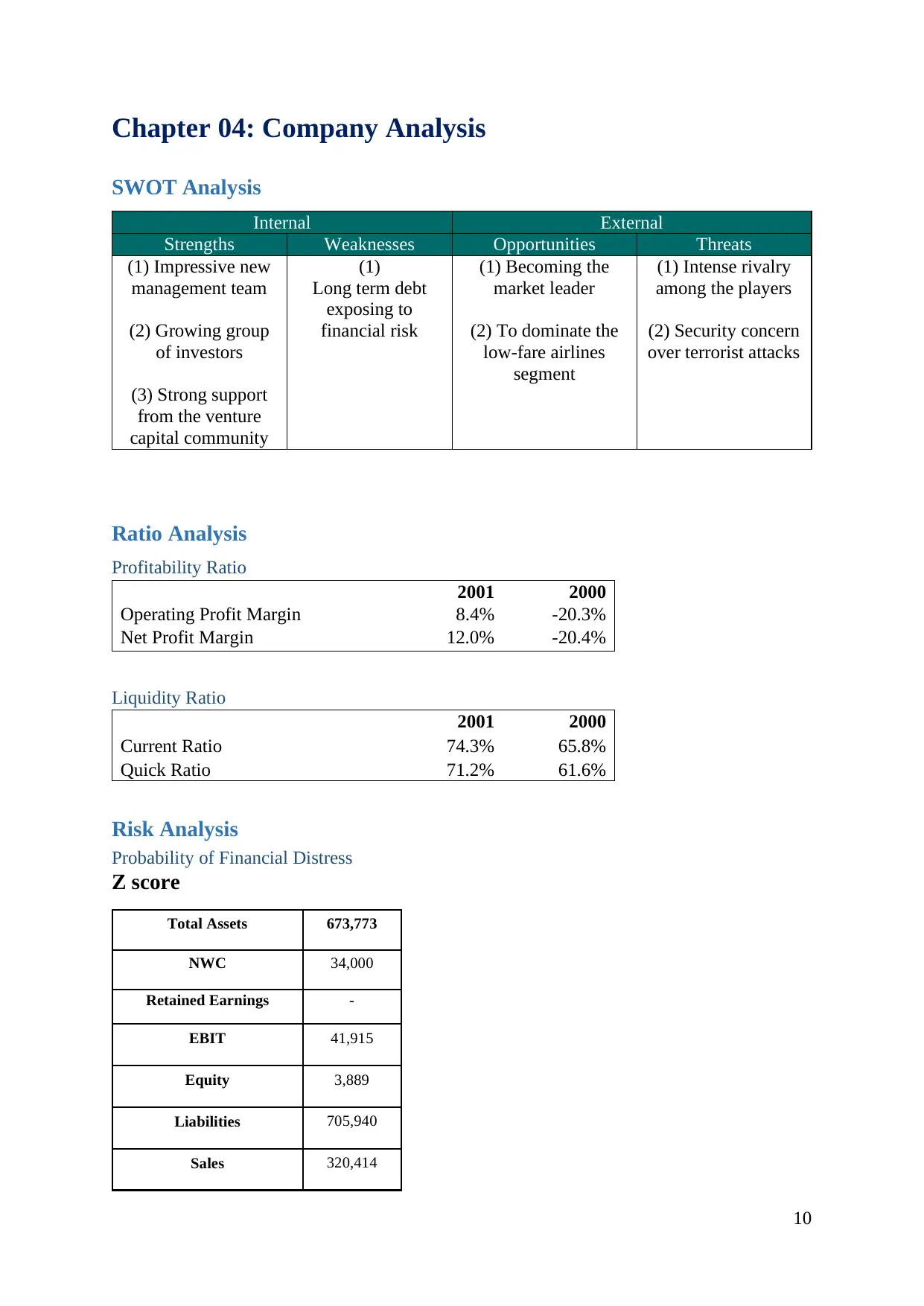

Chapter 04: Company Analysis

SWOT Analysis

Internal External

Strengths Weaknesses Opportunities Threats

(1) Impressive new

management team

(2) Growing group

of investors

(3) Strong support

from the venture

capital community

(1)

Long term debt

exposing to

financial risk

(1) Becoming the

market leader

(2) To dominate the

low-fare airlines

segment

(1) Intense rivalry

among the players

(2) Security concern

over terrorist attacks

Ratio Analysis

Profitability Ratio

2001 2000

Operating Profit Margin 8.4% -20.3%

Net Profit Margin 12.0% -20.4%

Liquidity Ratio

2001 2000

Current Ratio 74.3% 65.8%

Quick Ratio 71.2% 61.6%

Risk Analysis

Probability of Financial Distress

Z score

Total Assets 673,773

NWC 34,000

Retained Earnings -

EBIT 41,915

Equity 3,889

Liabilities 705,940

Sales 320,414

Chapter 04: Company Analysis

SWOT Analysis

Internal External

Strengths Weaknesses Opportunities Threats

(1) Impressive new

management team

(2) Growing group

of investors

(3) Strong support

from the venture

capital community

(1)

Long term debt

exposing to

financial risk

(1) Becoming the

market leader

(2) To dominate the

low-fare airlines

segment

(1) Intense rivalry

among the players

(2) Security concern

over terrorist attacks

Ratio Analysis

Profitability Ratio

2001 2000

Operating Profit Margin 8.4% -20.3%

Net Profit Margin 12.0% -20.4%

Liquidity Ratio

2001 2000

Current Ratio 74.3% 65.8%

Quick Ratio 71.2% 61.6%

Risk Analysis

Probability of Financial Distress

Z score

Total Assets 673,773

NWC 34,000

Retained Earnings -

EBIT 41,915

Equity 3,889

Liabilities 705,940

Sales 320,414

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

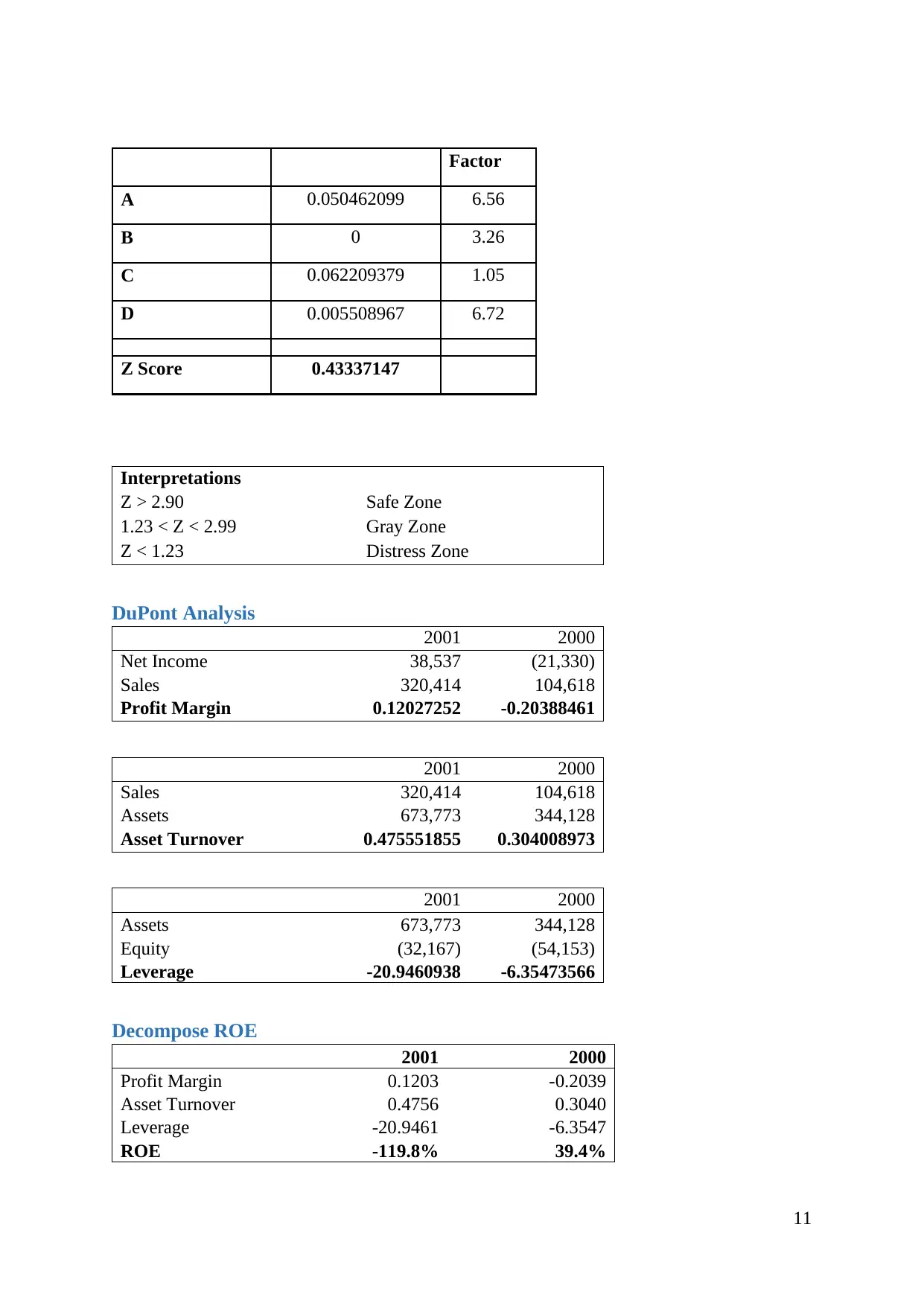

Factor

A 0.050462099 6.56

B 0 3.26

C 0.062209379 1.05

D 0.005508967 6.72

Z Score 0.43337147

Interpretations

Z > 2.90 Safe Zone

1.23 < Z < 2.99 Gray Zone

Z < 1.23 Distress Zone

DuPont Analysis

2001 2000

Net Income 38,537 (21,330)

Sales 320,414 104,618

Profit Margin 0.12027252 -0.20388461

2001 2000

Sales 320,414 104,618

Assets 673,773 344,128

Asset Turnover 0.475551855 0.304008973

2001 2000

Assets 673,773 344,128

Equity (32,167) (54,153)

Leverage -20.9460938 -6.35473566

Decompose ROE

2001 2000

Profit Margin 0.1203 -0.2039

Asset Turnover 0.4756 0.3040

Leverage -20.9461 -6.3547

ROE -119.8% 39.4%

Factor

A 0.050462099 6.56

B 0 3.26

C 0.062209379 1.05

D 0.005508967 6.72

Z Score 0.43337147

Interpretations

Z > 2.90 Safe Zone

1.23 < Z < 2.99 Gray Zone

Z < 1.23 Distress Zone

DuPont Analysis

2001 2000

Net Income 38,537 (21,330)

Sales 320,414 104,618

Profit Margin 0.12027252 -0.20388461

2001 2000

Sales 320,414 104,618

Assets 673,773 344,128

Asset Turnover 0.475551855 0.304008973

2001 2000

Assets 673,773 344,128

Equity (32,167) (54,153)

Leverage -20.9460938 -6.35473566

Decompose ROE

2001 2000

Profit Margin 0.1203 -0.2039

Asset Turnover 0.4756 0.3040

Leverage -20.9461 -6.3547

ROE -119.8% 39.4%

12

Chapter 05: Problem Statement

The core issue of this case can be summarized in the following statement:

Finding the ideal offer price that ensures the firm can avail the optimum benefit from

this opportunity without jeopardizing the success of a fully sold out IPO launch.

Our comprehensive analysis of the JetBlue Airways IPO Valuation case has provided us a

number of issues based on the current scenario which we believe to have a large impact on the

outcome of this offering. Our findings have been discussed below with proper reasoning:

(1) The aftermaths of September 11: The terrorist attack on World Trade Centre has

obviously slowed down the growth of airlines industry. People are showing lack of

motivation on travelling via airlines which is leading towards the small companies

being bankrupt. Also it has shown the industry how important it is to invest in

technologies to ensure the safety of passengers.

(2) The low-fare business model: The low-fare business models started to disrupt the

industry in 2002. One of the dominant player with such business model is Southwest

Airlines. In fact, Southwest’s market capitalization was larger than all other airlines

companies of U.S. combined.

(3) New players entering the market: Following the success of Southwest Airlines a

flurry of new players with low-fare business models are entering the market. AirTran,

America West, ATA and Frontier etc. are the player that are following the model of

Southwest.

Chapter 05: Problem Statement

The core issue of this case can be summarized in the following statement:

Finding the ideal offer price that ensures the firm can avail the optimum benefit from

this opportunity without jeopardizing the success of a fully sold out IPO launch.

Our comprehensive analysis of the JetBlue Airways IPO Valuation case has provided us a

number of issues based on the current scenario which we believe to have a large impact on the

outcome of this offering. Our findings have been discussed below with proper reasoning:

(1) The aftermaths of September 11: The terrorist attack on World Trade Centre has

obviously slowed down the growth of airlines industry. People are showing lack of

motivation on travelling via airlines which is leading towards the small companies

being bankrupt. Also it has shown the industry how important it is to invest in

technologies to ensure the safety of passengers.

(2) The low-fare business model: The low-fare business models started to disrupt the

industry in 2002. One of the dominant player with such business model is Southwest

Airlines. In fact, Southwest’s market capitalization was larger than all other airlines

companies of U.S. combined.

(3) New players entering the market: Following the success of Southwest Airlines a

flurry of new players with low-fare business models are entering the market. AirTran,

America West, ATA and Frontier etc. are the player that are following the model of

Southwest.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.