Financial Strategy Analysis Report: JetBlue Airways Case Study

VerifiedAdded on 2020/04/29

|18

|4387

|57

Report

AI Summary

This report analyzes the financial strategy of JetBlue Airways Corporation, focusing on its investment plans and funding options for aircraft acquisitions. The report begins with an executive summary outlining the company's goals and challenges, including the need for significant capital expenditure to support growth. It defines the problem JetBlue faces, including the need to finance aircraft purchases and other investments. The report then provides an industry analysis, comparing JetBlue's financial structure to that of other airlines, including both low-cost and traditional carriers. It explores financial alternatives available to JetBlue, such as equity issuance and convertible debentures, and conducts a financial statement analysis to evaluate the impact of these options. The analysis includes calculating the weighted average cost of capital (WACC) and assessing the optimal capital structure for minimizing WACC and maximizing shareholder value. The report concludes with recommendations for JetBlue's financial strategy, emphasizing the issuance of equity as the most feasible alternative for planned investments.

Running head: FINANCIAL STRATEGY

Financial Strategy

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Financial Strategy

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL STRATEGY

Executive Summary:

In the current report, the financial position of JetBlue Airways Corporation is analysed

for providing recommendations to the organisation in relation to its investment plans. It is a low-

cost and low-fare passenger airline group, which serves the US market. By the year 2003, the

organisation has been intending to support its growth by acquiring various new aircrafts over the

next 13 years. This necessitates the need for the organisation for greater capital expenditure in

order to support those acquisitions along with various associated investments. It has been found

that JetBlue would have a financial position, which minimises its overall WACC. As a result, it

maximises the overall value of the stock of the organisation. Hence, from the financial

perspective, it could be stated that the feasible alternative for planned investments is the issuance

of equity for 2003.

Executive Summary:

In the current report, the financial position of JetBlue Airways Corporation is analysed

for providing recommendations to the organisation in relation to its investment plans. It is a low-

cost and low-fare passenger airline group, which serves the US market. By the year 2003, the

organisation has been intending to support its growth by acquiring various new aircrafts over the

next 13 years. This necessitates the need for the organisation for greater capital expenditure in

order to support those acquisitions along with various associated investments. It has been found

that JetBlue would have a financial position, which minimises its overall WACC. As a result, it

maximises the overall value of the stock of the organisation. Hence, from the financial

perspective, it could be stated that the feasible alternative for planned investments is the issuance

of equity for 2003.

2FINANCIAL STRATEGY

Table of Contents

1. Introduction:................................................................................................................................3

2. Problem definition:......................................................................................................................3

3. Industry analysis:.........................................................................................................................4

4. Financial alternatives:..................................................................................................................7

5. Financial statement analysis of the alternatives:.........................................................................8

6. Non-financial analysis:..............................................................................................................11

7. Conclusion:................................................................................................................................14

References and Bibliographies:.....................................................................................................16

Table of Contents

1. Introduction:................................................................................................................................3

2. Problem definition:......................................................................................................................3

3. Industry analysis:.........................................................................................................................4

4. Financial alternatives:..................................................................................................................7

5. Financial statement analysis of the alternatives:.........................................................................8

6. Non-financial analysis:..............................................................................................................11

7. Conclusion:................................................................................................................................14

References and Bibliographies:.....................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL STRATEGY

1. Introduction:

In the current report, the financial position of JetBlue Airways Corporation is analysed

for providing recommendations to the organisation in relation to its investment plans. It is a low-

cost and low-fare passenger airline group, which serves the US market. By the year 2003, the

organisation has been intending to support its growth by acquiring various new aircrafts over the

next 13 years. This necessitates the need for the organisation for greater capital expenditure in

order to support those acquisitions along with various associated investments (Alamdari &

Fagan, 2005).

A background research is carried out for evaluating the ways the other airlines are

funding their aircraft acquisitions and other investments. The various alternatives of funding

available to the organisation are studied in association with the financial position of the same.

Finally, a non-financial evaluation of the debt and equity alternatives is conducted in relation to

all those business areas other than finance.

2. Problem definition:

According to the case study, JetBlue Airways Corporation has finished an initial public

offering (IPO) in 2002 around two years after its establishment. JetBlue has a successful business

model and effective financial outcomes during that timeframe and it has performed well in

contrast to the other US airline firms between 2000 and 2003 (Bhalla, 2004). By July 2003,

JetBlue has been experiencing various opportunities to grow by including new markets and new

flights to the current destinations. For achieving such growth, the organisation has been planning

1. Introduction:

In the current report, the financial position of JetBlue Airways Corporation is analysed

for providing recommendations to the organisation in relation to its investment plans. It is a low-

cost and low-fare passenger airline group, which serves the US market. By the year 2003, the

organisation has been intending to support its growth by acquiring various new aircrafts over the

next 13 years. This necessitates the need for the organisation for greater capital expenditure in

order to support those acquisitions along with various associated investments (Alamdari &

Fagan, 2005).

A background research is carried out for evaluating the ways the other airlines are

funding their aircraft acquisitions and other investments. The various alternatives of funding

available to the organisation are studied in association with the financial position of the same.

Finally, a non-financial evaluation of the debt and equity alternatives is conducted in relation to

all those business areas other than finance.

2. Problem definition:

According to the case study, JetBlue Airways Corporation has finished an initial public

offering (IPO) in 2002 around two years after its establishment. JetBlue has a successful business

model and effective financial outcomes during that timeframe and it has performed well in

contrast to the other US airline firms between 2000 and 2003 (Bhalla, 2004). By July 2003,

JetBlue has been experiencing various opportunities to grow by including new markets and new

flights to the current destinations. For achieving such growth, the organisation has been planning

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL STRATEGY

to buy 65 new Airbus 320 with an alternative of buying extra 50 ones and it is committed to buy

100 Embrarer E190 aircraft with the alternative to buy 100 additional ones.

JetBlue is required to find a way about funding those acquisitions along with other

required investments like spare parts, extra hangars, new engines and a flight-training centre. The

Chief Financial Officer (CFO), John Owen, is entrusted with the responsibility of searching the

best funding scheme for the organisation. The CFO of JetBlue has been confronted with two

problems. Firstly, he is required to fund the acquisitions planned for the second half of 2003.

Indeed, between 1st July to 31st December 2003, the organisation has committed to buy 8 Airbus

A320 aircraft for an overall amount of $305 million to be paid 2003 (Exhibit 8). The

organisation had generated operating cash flows amounting to $129,725,000 for the first quarter

of 2003 and it had already generated $238,989,000 from financing activities (Exhibit 6). This

would constitute for portion of this capital expenditure projected at around $570 million for 2003

(Exhibit 9). Therefore, John Owen is required to fund the remaining portion of such capital

expenditure.

Secondly, John Owen is required to think regarding long-term financial strategy. Indeed,

JetBlue has been committed to the purchase of 207 extra aircraft for an overall amount of $6.86

billion over 8 years. Thus, the personnel needs to think about the effective capital structure for

the organisation and hence, the alternative financial strategy for the investments of the

organisation including the aircraft acquisitions and the associated investments.

3. Industry analysis:

In this section, some background research has been carried out to ascertain the ways the

other airline groups are funding their aircraft acquisitions and other investments. From a broader

to buy 65 new Airbus 320 with an alternative of buying extra 50 ones and it is committed to buy

100 Embrarer E190 aircraft with the alternative to buy 100 additional ones.

JetBlue is required to find a way about funding those acquisitions along with other

required investments like spare parts, extra hangars, new engines and a flight-training centre. The

Chief Financial Officer (CFO), John Owen, is entrusted with the responsibility of searching the

best funding scheme for the organisation. The CFO of JetBlue has been confronted with two

problems. Firstly, he is required to fund the acquisitions planned for the second half of 2003.

Indeed, between 1st July to 31st December 2003, the organisation has committed to buy 8 Airbus

A320 aircraft for an overall amount of $305 million to be paid 2003 (Exhibit 8). The

organisation had generated operating cash flows amounting to $129,725,000 for the first quarter

of 2003 and it had already generated $238,989,000 from financing activities (Exhibit 6). This

would constitute for portion of this capital expenditure projected at around $570 million for 2003

(Exhibit 9). Therefore, John Owen is required to fund the remaining portion of such capital

expenditure.

Secondly, John Owen is required to think regarding long-term financial strategy. Indeed,

JetBlue has been committed to the purchase of 207 extra aircraft for an overall amount of $6.86

billion over 8 years. Thus, the personnel needs to think about the effective capital structure for

the organisation and hence, the alternative financial strategy for the investments of the

organisation including the aircraft acquisitions and the associated investments.

3. Industry analysis:

In this section, some background research has been carried out to ascertain the ways the

other airline groups are funding their aircraft acquisitions and other investments. From a broader

5FINANCIAL STRATEGY

perspective, this section analyses the specificities of their financial structures. Thus, this section

involves few regular and low-cost airline groups.

For instance, British Airways is funding its aircraft acquisitions with the help of debt,

each of which is associated with assets (Bjelicic, 2007).). The airline is using financial leases

principally and contracts of hire purchase for acquiring Aircraft in accordance with its annual

report. On the other hand, Delta Airlines is using pass-through certificates for funding aircraft. In

addition, the organisation has $5.2 billion of loans secured on the part of 287 aircrafts in 2010

(Blaha, 2003).

United Continental Holdings has greater obligations comprising of aircraft leases, debt

and funding. A major portion of the business assets, particularly aircraft, is pledged under

different loans and obligations. In addition, it has been involved in using equipment notes,

secured notes, pass-through certificates and mutual funding ensured on the part of spare parts of

the aircraft, spare engines and aircraft (Cobb, 2005). In addition, it is involved in raising funds by

issuing common stock.

The low-cost airline groups, on the other hand, seem more conservative on their side.

EasyJet has adopted a policy of conservative capital structure having a liquidity target of

£4 million cash each aircraft along with 50% limit on net gearing. The overall debt of the

organisation is associated with assets (Cobbs & Wolf, 2004). It held 62 aircrafts under operating

leases and 8 aircrafts under financial leases out of 196 aircrafts, mainly Airbus.

Another low-cost airline group, Ryonair, has a fleet of 232 Boeing 737-800s. The

organisation makes its purchases related to firm order by combining the bank loans, financial and

operating leases and operational cash flows. Thus, both EasyJet and Ryonair depict a capital

perspective, this section analyses the specificities of their financial structures. Thus, this section

involves few regular and low-cost airline groups.

For instance, British Airways is funding its aircraft acquisitions with the help of debt,

each of which is associated with assets (Bjelicic, 2007).). The airline is using financial leases

principally and contracts of hire purchase for acquiring Aircraft in accordance with its annual

report. On the other hand, Delta Airlines is using pass-through certificates for funding aircraft. In

addition, the organisation has $5.2 billion of loans secured on the part of 287 aircrafts in 2010

(Blaha, 2003).

United Continental Holdings has greater obligations comprising of aircraft leases, debt

and funding. A major portion of the business assets, particularly aircraft, is pledged under

different loans and obligations. In addition, it has been involved in using equipment notes,

secured notes, pass-through certificates and mutual funding ensured on the part of spare parts of

the aircraft, spare engines and aircraft (Cobb, 2005). In addition, it is involved in raising funds by

issuing common stock.

The low-cost airline groups, on the other hand, seem more conservative on their side.

EasyJet has adopted a policy of conservative capital structure having a liquidity target of

£4 million cash each aircraft along with 50% limit on net gearing. The overall debt of the

organisation is associated with assets (Cobbs & Wolf, 2004). It held 62 aircrafts under operating

leases and 8 aircrafts under financial leases out of 196 aircrafts, mainly Airbus.

Another low-cost airline group, Ryonair, has a fleet of 232 Boeing 737-800s. The

organisation makes its purchases related to firm order by combining the bank loans, financial and

operating leases and operational cash flows. Thus, both EasyJet and Ryonair depict a capital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL STRATEGY

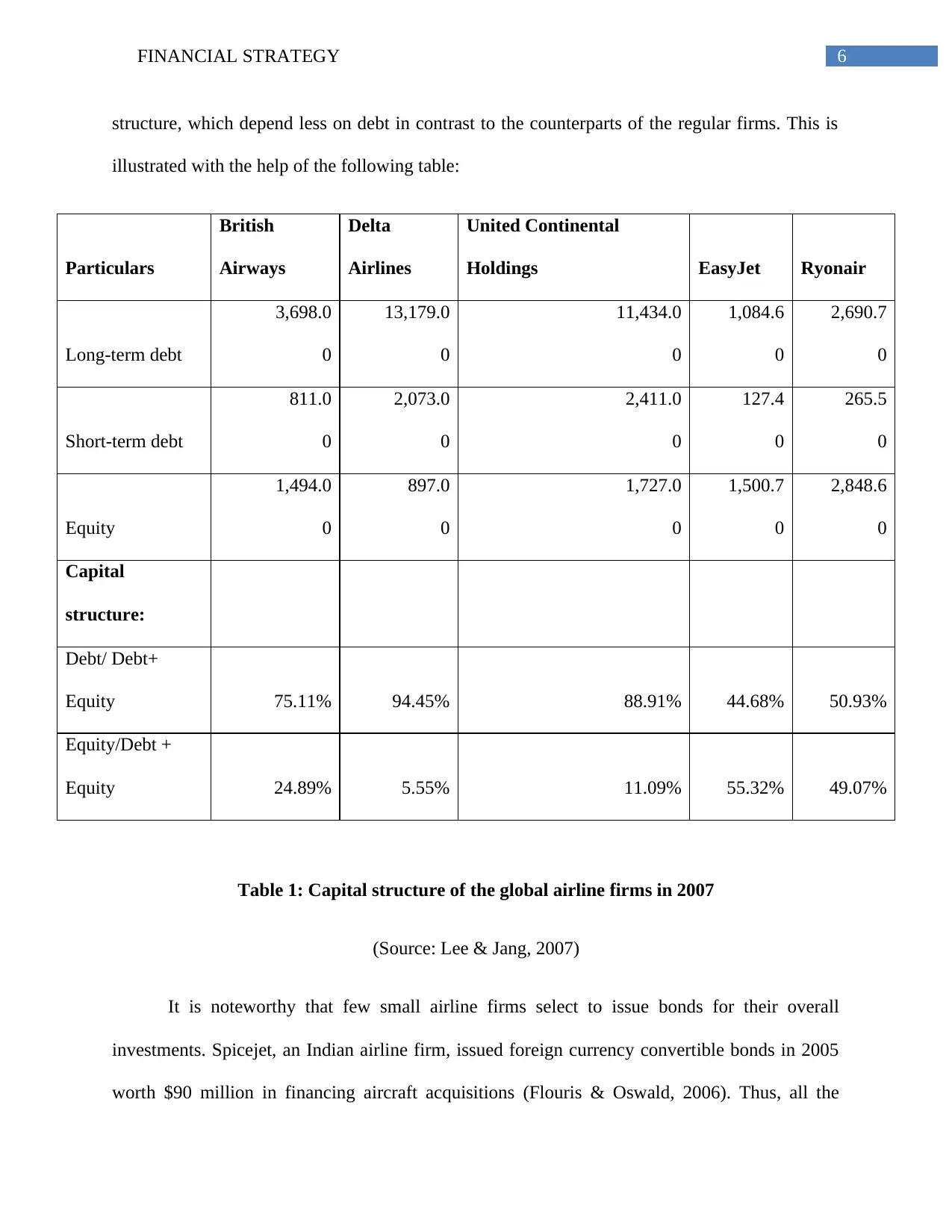

structure, which depend less on debt in contrast to the counterparts of the regular firms. This is

illustrated with the help of the following table:

Particulars

British

Airways

Delta

Airlines

United Continental

Holdings EasyJet Ryonair

Long-term debt

3,698.0

0

13,179.0

0

11,434.0

0

1,084.6

0

2,690.7

0

Short-term debt

811.0

0

2,073.0

0

2,411.0

0

127.4

0

265.5

0

Equity

1,494.0

0

897.0

0

1,727.0

0

1,500.7

0

2,848.6

0

Capital

structure:

Debt/ Debt+

Equity 75.11% 94.45% 88.91% 44.68% 50.93%

Equity/Debt +

Equity 24.89% 5.55% 11.09% 55.32% 49.07%

Table 1: Capital structure of the global airline firms in 2007

(Source: Lee & Jang, 2007)

It is noteworthy that few small airline firms select to issue bonds for their overall

investments. Spicejet, an Indian airline firm, issued foreign currency convertible bonds in 2005

worth $90 million in financing aircraft acquisitions (Flouris & Oswald, 2006). Thus, all the

structure, which depend less on debt in contrast to the counterparts of the regular firms. This is

illustrated with the help of the following table:

Particulars

British

Airways

Delta

Airlines

United Continental

Holdings EasyJet Ryonair

Long-term debt

3,698.0

0

13,179.0

0

11,434.0

0

1,084.6

0

2,690.7

0

Short-term debt

811.0

0

2,073.0

0

2,411.0

0

127.4

0

265.5

0

Equity

1,494.0

0

897.0

0

1,727.0

0

1,500.7

0

2,848.6

0

Capital

structure:

Debt/ Debt+

Equity 75.11% 94.45% 88.91% 44.68% 50.93%

Equity/Debt +

Equity 24.89% 5.55% 11.09% 55.32% 49.07%

Table 1: Capital structure of the global airline firms in 2007

(Source: Lee & Jang, 2007)

It is noteworthy that few small airline firms select to issue bonds for their overall

investments. Spicejet, an Indian airline firm, issued foreign currency convertible bonds in 2005

worth $90 million in financing aircraft acquisitions (Flouris & Oswald, 2006). Thus, all the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STRATEGY

global airline groups are using debt, equity and operating cash flows to raise funds. For instance,

Air-France KLM, Lufthansa, Air Canada, British Airways, Avianca, Australia’s Virgin Blue and

Kingfisher issued bonds in 2009. AMR, on the other hand, used private lenders for borrowing

money. From this study, it has been found out that most of the airlines are funding their aircraft

acquisitions except from using operational cash flows. This either is primarily through debt

secured debt or leases. The other investment requirements are funded through either equity or

debt based on the organisations. However, an inherent trend to low-cost firms appears to be their

conservative financial structures in contrast to larger and regular airline firms.

4. Financial alternatives:

For funding the acquisitions for the leftover part of 2003, JetBlue received two financial

alternatives from the investment banks. The first option is to raise additional 2.6 million shares at

a projected rate of $42.50 per share. JetBlue would be able to fund up to $110.5 million. The

bank fees and commissions for this proposal amount to $3,591,250 and they depict a cost of

3.25%. The second option from the investment banks is to $150 million in a private placement

pertaining to convertible debentures. The debentures would be a convertible debt of 30-year

having a coupon rate of 3.5%. Moreover, the debt would be convertible into JetBlue’s shares at

$63.75 per share and it depicts a conversion rate of 15.6863 shares per $1,000 principal note

amount (Flouris & Walker, 2005). These notes would be unsecured obligations and these would

rank identical in payment right with other unsecured debt. At present, all the debts of JetBlue are

secured. In addition, the airline does not have to incur any additional fees for this option.

There are some other alternatives available for JetBlue as well. Indeed, the organisation

could issue few preferred stocks. Such stocks might be taken into account in the form of equity

global airline groups are using debt, equity and operating cash flows to raise funds. For instance,

Air-France KLM, Lufthansa, Air Canada, British Airways, Avianca, Australia’s Virgin Blue and

Kingfisher issued bonds in 2009. AMR, on the other hand, used private lenders for borrowing

money. From this study, it has been found out that most of the airlines are funding their aircraft

acquisitions except from using operational cash flows. This either is primarily through debt

secured debt or leases. The other investment requirements are funded through either equity or

debt based on the organisations. However, an inherent trend to low-cost firms appears to be their

conservative financial structures in contrast to larger and regular airline firms.

4. Financial alternatives:

For funding the acquisitions for the leftover part of 2003, JetBlue received two financial

alternatives from the investment banks. The first option is to raise additional 2.6 million shares at

a projected rate of $42.50 per share. JetBlue would be able to fund up to $110.5 million. The

bank fees and commissions for this proposal amount to $3,591,250 and they depict a cost of

3.25%. The second option from the investment banks is to $150 million in a private placement

pertaining to convertible debentures. The debentures would be a convertible debt of 30-year

having a coupon rate of 3.5%. Moreover, the debt would be convertible into JetBlue’s shares at

$63.75 per share and it depicts a conversion rate of 15.6863 shares per $1,000 principal note

amount (Flouris & Walker, 2005). These notes would be unsecured obligations and these would

rank identical in payment right with other unsecured debt. At present, all the debts of JetBlue are

secured. In addition, the airline does not have to incur any additional fees for this option.

There are some other alternatives available for JetBlue as well. Indeed, the organisation

could issue few preferred stocks. Such stocks might be taken into account in the form of equity

8FINANCIAL STRATEGY

in accenting for strengthening the balance sheet of the organisation; however, it would

accommodate the concern of the board members about dilution (Flouris & Walker, 2005).

However, this option of preferred stock has failed to win the trust and confidence of the

investors.

Another alternative might be to issue simple corporate bonds (Hofer, Dresner & Windle,

2005). However, the coupon rate would be greater than 3.5% of the convertible bonds. Thus, the

cost for this option would be more for JetBlue in contrast to convertible bonds, particularly, if the

share price of the organisation is above $63.75. The issuance of public corporate bonds would

have greater cost for the organisation as well (Jones, 2006). Indeed, few ranking agencies are

required to rank them having greater coupon rates (Exhibit 12). There are two other options

available for JetBlue for funding the aircraft acquisitions, which include operating leases and

secured debt at beneficial conditions. Hence, the alternatives that would be retained for the

remaining part of the evaluation are the secured debt and the operating lease for the acquisitions

of aircraft, the issuance of equity and convertible private bonds for acquisitions and other

investments.

5. Financial statement analysis of the alternatives:

As per June 2003, the short-term debt of JetBlue has been $26,580,000 and long-term

debt has been $731,740,000 along with equity value of $480,594,000 (Exhibit 5a). For

calculation of average interest rate for the organisation, the data from 2002 have been used. The

interest expenses for the year amounted to $10,370,000 (Exhibit 4) for an overall long-term debt

of $690,252,000 (Exhibit 5a) with a rate of interest of 1.5%. The tax expenses in June 2003 have

in accenting for strengthening the balance sheet of the organisation; however, it would

accommodate the concern of the board members about dilution (Flouris & Walker, 2005).

However, this option of preferred stock has failed to win the trust and confidence of the

investors.

Another alternative might be to issue simple corporate bonds (Hofer, Dresner & Windle,

2005). However, the coupon rate would be greater than 3.5% of the convertible bonds. Thus, the

cost for this option would be more for JetBlue in contrast to convertible bonds, particularly, if the

share price of the organisation is above $63.75. The issuance of public corporate bonds would

have greater cost for the organisation as well (Jones, 2006). Indeed, few ranking agencies are

required to rank them having greater coupon rates (Exhibit 12). There are two other options

available for JetBlue for funding the aircraft acquisitions, which include operating leases and

secured debt at beneficial conditions. Hence, the alternatives that would be retained for the

remaining part of the evaluation are the secured debt and the operating lease for the acquisitions

of aircraft, the issuance of equity and convertible private bonds for acquisitions and other

investments.

5. Financial statement analysis of the alternatives:

As per June 2003, the short-term debt of JetBlue has been $26,580,000 and long-term

debt has been $731,740,000 along with equity value of $480,594,000 (Exhibit 5a). For

calculation of average interest rate for the organisation, the data from 2002 have been used. The

interest expenses for the year amounted to $10,370,000 (Exhibit 4) for an overall long-term debt

of $690,252,000 (Exhibit 5a) with a rate of interest of 1.5%. The tax expenses in June 2003 have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL STRATEGY

been $40,188,000 for overall earnings before tax of $95,503,000 (Exhibit 4) with a corporate tax

rate of 42% (Kochan, 2006).

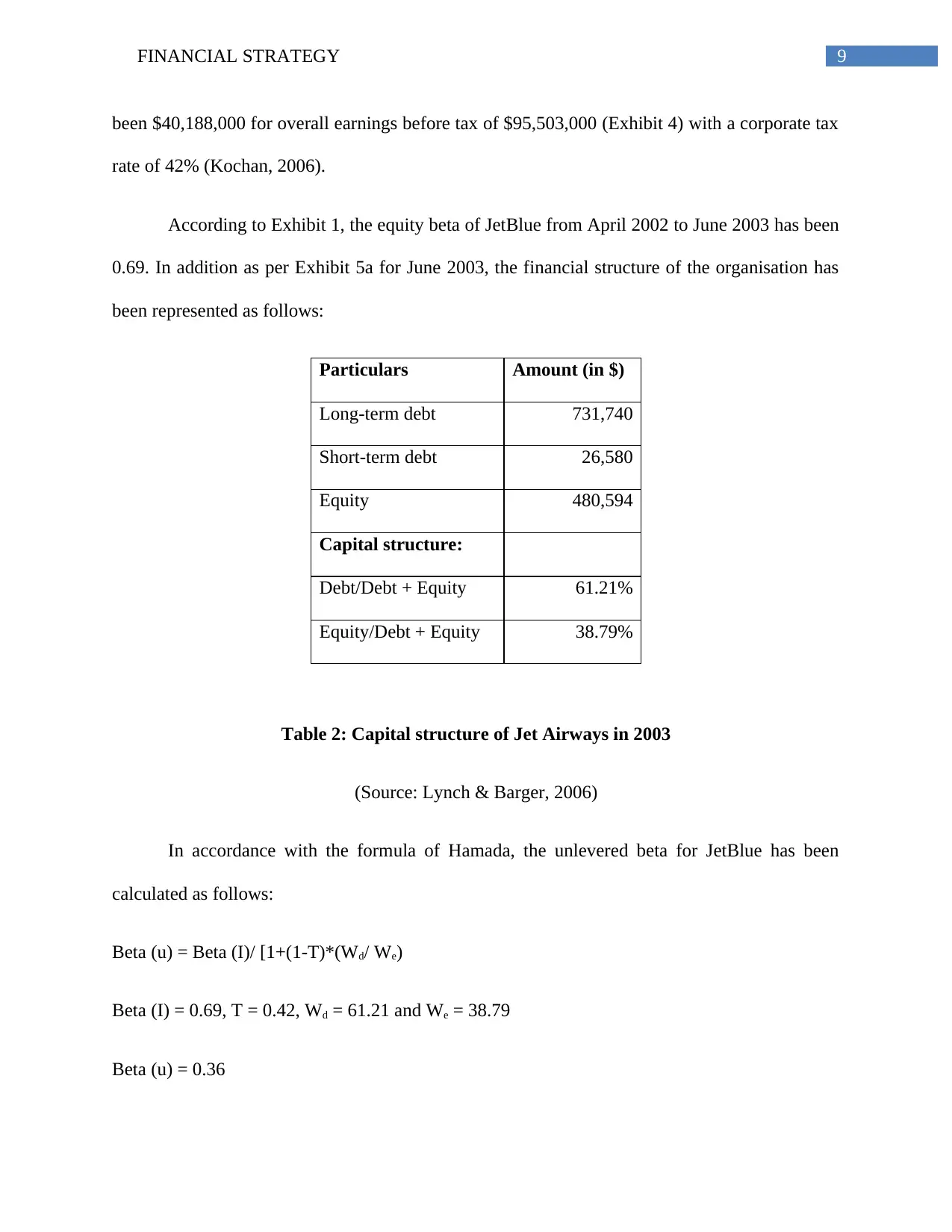

According to Exhibit 1, the equity beta of JetBlue from April 2002 to June 2003 has been

0.69. In addition as per Exhibit 5a for June 2003, the financial structure of the organisation has

been represented as follows:

Particulars Amount (in $)

Long-term debt 731,740

Short-term debt 26,580

Equity 480,594

Capital structure:

Debt/Debt + Equity 61.21%

Equity/Debt + Equity 38.79%

Table 2: Capital structure of Jet Airways in 2003

(Source: Lynch & Barger, 2006)

In accordance with the formula of Hamada, the unlevered beta for JetBlue has been

calculated as follows:

Beta (u) = Beta (I)/ [1+(1-T)*(Wd/ We)

Beta (I) = 0.69, T = 0.42, Wd = 61.21 and We = 38.79

Beta (u) = 0.36

been $40,188,000 for overall earnings before tax of $95,503,000 (Exhibit 4) with a corporate tax

rate of 42% (Kochan, 2006).

According to Exhibit 1, the equity beta of JetBlue from April 2002 to June 2003 has been

0.69. In addition as per Exhibit 5a for June 2003, the financial structure of the organisation has

been represented as follows:

Particulars Amount (in $)

Long-term debt 731,740

Short-term debt 26,580

Equity 480,594

Capital structure:

Debt/Debt + Equity 61.21%

Equity/Debt + Equity 38.79%

Table 2: Capital structure of Jet Airways in 2003

(Source: Lynch & Barger, 2006)

In accordance with the formula of Hamada, the unlevered beta for JetBlue has been

calculated as follows:

Beta (u) = Beta (I)/ [1+(1-T)*(Wd/ We)

Beta (I) = 0.69, T = 0.42, Wd = 61.21 and We = 38.79

Beta (u) = 0.36

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL STRATEGY

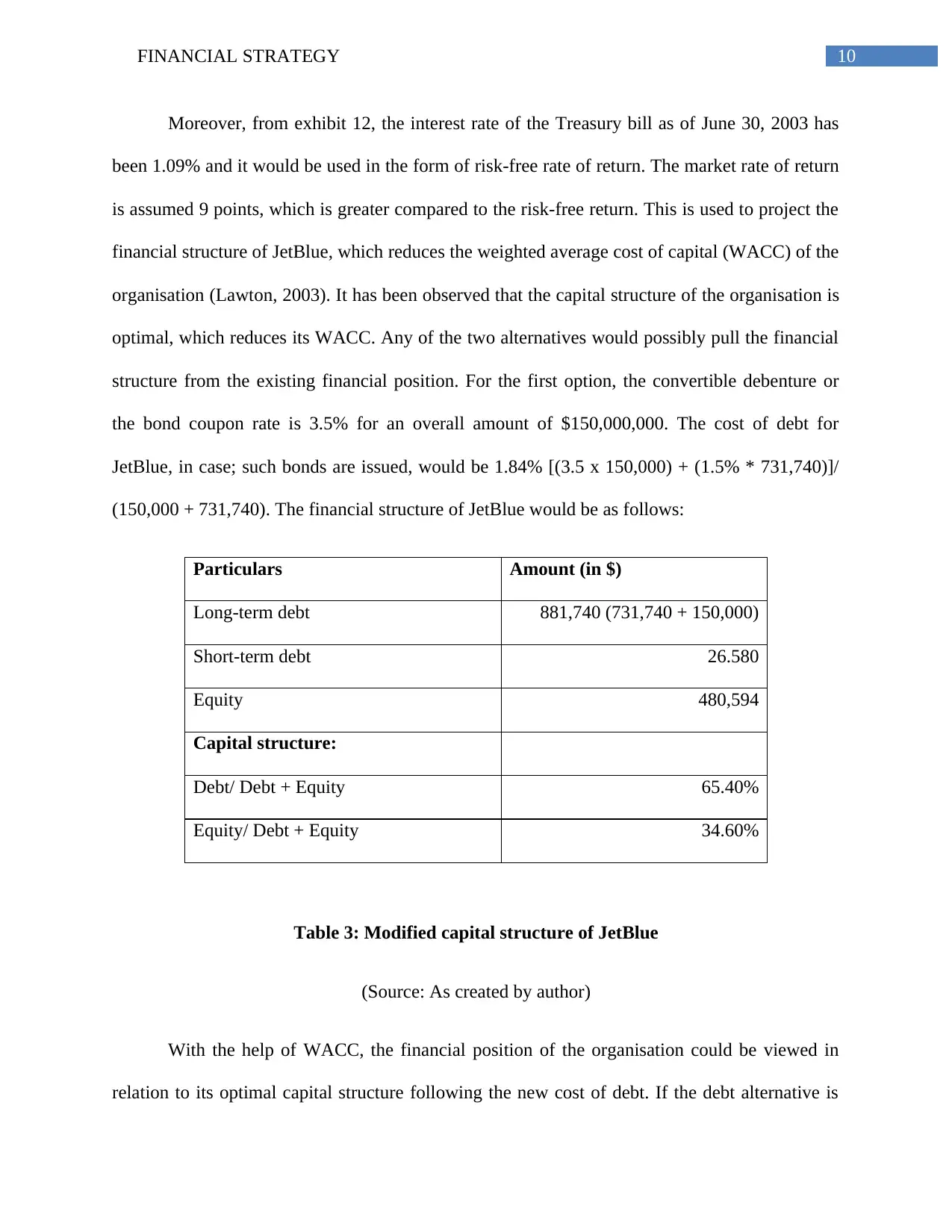

Moreover, from exhibit 12, the interest rate of the Treasury bill as of June 30, 2003 has

been 1.09% and it would be used in the form of risk-free rate of return. The market rate of return

is assumed 9 points, which is greater compared to the risk-free return. This is used to project the

financial structure of JetBlue, which reduces the weighted average cost of capital (WACC) of the

organisation (Lawton, 2003). It has been observed that the capital structure of the organisation is

optimal, which reduces its WACC. Any of the two alternatives would possibly pull the financial

structure from the existing financial position. For the first option, the convertible debenture or

the bond coupon rate is 3.5% for an overall amount of $150,000,000. The cost of debt for

JetBlue, in case; such bonds are issued, would be 1.84% [(3.5 x 150,000) + (1.5% * 731,740)]/

(150,000 + 731,740). The financial structure of JetBlue would be as follows:

Particulars Amount (in $)

Long-term debt 881,740 (731,740 + 150,000)

Short-term debt 26.580

Equity 480,594

Capital structure:

Debt/ Debt + Equity 65.40%

Equity/ Debt + Equity 34.60%

Table 3: Modified capital structure of JetBlue

(Source: As created by author)

With the help of WACC, the financial position of the organisation could be viewed in

relation to its optimal capital structure following the new cost of debt. If the debt alternative is

Moreover, from exhibit 12, the interest rate of the Treasury bill as of June 30, 2003 has

been 1.09% and it would be used in the form of risk-free rate of return. The market rate of return

is assumed 9 points, which is greater compared to the risk-free return. This is used to project the

financial structure of JetBlue, which reduces the weighted average cost of capital (WACC) of the

organisation (Lawton, 2003). It has been observed that the capital structure of the organisation is

optimal, which reduces its WACC. Any of the two alternatives would possibly pull the financial

structure from the existing financial position. For the first option, the convertible debenture or

the bond coupon rate is 3.5% for an overall amount of $150,000,000. The cost of debt for

JetBlue, in case; such bonds are issued, would be 1.84% [(3.5 x 150,000) + (1.5% * 731,740)]/

(150,000 + 731,740). The financial structure of JetBlue would be as follows:

Particulars Amount (in $)

Long-term debt 881,740 (731,740 + 150,000)

Short-term debt 26.580

Equity 480,594

Capital structure:

Debt/ Debt + Equity 65.40%

Equity/ Debt + Equity 34.60%

Table 3: Modified capital structure of JetBlue

(Source: As created by author)

With the help of WACC, the financial position of the organisation could be viewed in

relation to its optimal capital structure following the new cost of debt. If the debt alternative is

11FINANCIAL STRATEGY

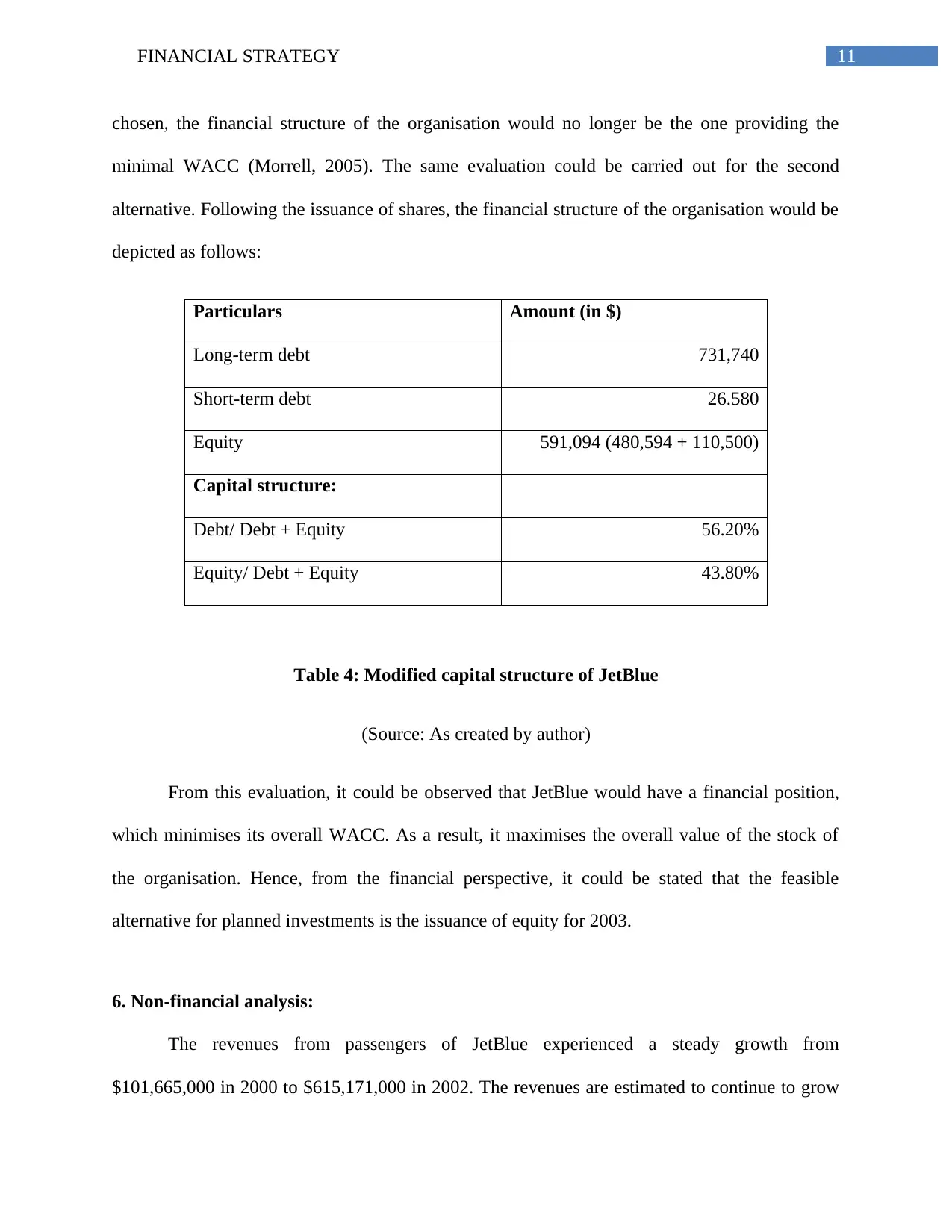

chosen, the financial structure of the organisation would no longer be the one providing the

minimal WACC (Morrell, 2005). The same evaluation could be carried out for the second

alternative. Following the issuance of shares, the financial structure of the organisation would be

depicted as follows:

Particulars Amount (in $)

Long-term debt 731,740

Short-term debt 26.580

Equity 591,094 (480,594 + 110,500)

Capital structure:

Debt/ Debt + Equity 56.20%

Equity/ Debt + Equity 43.80%

Table 4: Modified capital structure of JetBlue

(Source: As created by author)

From this evaluation, it could be observed that JetBlue would have a financial position,

which minimises its overall WACC. As a result, it maximises the overall value of the stock of

the organisation. Hence, from the financial perspective, it could be stated that the feasible

alternative for planned investments is the issuance of equity for 2003.

6. Non-financial analysis:

The revenues from passengers of JetBlue experienced a steady growth from

$101,665,000 in 2000 to $615,171,000 in 2002. The revenues are estimated to continue to grow

chosen, the financial structure of the organisation would no longer be the one providing the

minimal WACC (Morrell, 2005). The same evaluation could be carried out for the second

alternative. Following the issuance of shares, the financial structure of the organisation would be

depicted as follows:

Particulars Amount (in $)

Long-term debt 731,740

Short-term debt 26.580

Equity 591,094 (480,594 + 110,500)

Capital structure:

Debt/ Debt + Equity 56.20%

Equity/ Debt + Equity 43.80%

Table 4: Modified capital structure of JetBlue

(Source: As created by author)

From this evaluation, it could be observed that JetBlue would have a financial position,

which minimises its overall WACC. As a result, it maximises the overall value of the stock of

the organisation. Hence, from the financial perspective, it could be stated that the feasible

alternative for planned investments is the issuance of equity for 2003.

6. Non-financial analysis:

The revenues from passengers of JetBlue experienced a steady growth from

$101,665,000 in 2000 to $615,171,000 in 2002. The revenues are estimated to continue to grow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.