University Name: JetBlue Airways Fuel Hedging Case Study Analysis

VerifiedAdded on 2022/08/12

|11

|3506

|30

Case Study

AI Summary

This case study analyzes JetBlue Airways' fuel hedging strategies, focusing on the airline's response to rising fuel costs. The report explores the rationale behind hedging, various hedging instruments like swaps, options, and collars, and the associated risks and costs. It delves into the concept of crack spread, its calculation, and its volatility's impact on hedging. The study examines the price and quantity risks faced by airlines, the extent to which they should hedge, and the shift from WTI to Brent crude oil contracts for hedging. It highlights the importance of integrating hedging strategies with the overall corporate strategy, particularly given the volatile nature of jet fuel prices and the significant portion of operating costs they represent. The case study emphasizes the need for airlines to protect against fuel price fluctuations and the complexities of derivative contracts, ultimately providing insights into the financial risk management practices within the airline industry.

JetBlue Case Study

Student Name

University Name

Student Name

University Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jet Blue Case Study

Contents

Introduction...........................................................................................................................................2

Should Jet blue hedge its fuel cost?.......................................................................................................2

Various strategies used by airlines to hedge fuel price risk...................................................................4

Crack spread..........................................................................................................................................5

What is Crack spread?.......................................................................................................................5

Calculation of the crack spread..........................................................................................................5

Volatility in the crack spread and its effect on the hedging...............................................................6

Hedging strategies by the airlines..........................................................................................................6

What risks are hedged?......................................................................................................................6

Price risk and Quantity risk...............................................................................................................7

To what extent should airlines hedge their fuel risk...........................................................................7

Reason to switch from WTI to Brent hedging.......................................................................................8

Conclusion.............................................................................................................................................9

References.............................................................................................................................................9

1

Contents

Introduction...........................................................................................................................................2

Should Jet blue hedge its fuel cost?.......................................................................................................2

Various strategies used by airlines to hedge fuel price risk...................................................................4

Crack spread..........................................................................................................................................5

What is Crack spread?.......................................................................................................................5

Calculation of the crack spread..........................................................................................................5

Volatility in the crack spread and its effect on the hedging...............................................................6

Hedging strategies by the airlines..........................................................................................................6

What risks are hedged?......................................................................................................................6

Price risk and Quantity risk...............................................................................................................7

To what extent should airlines hedge their fuel risk...........................................................................7

Reason to switch from WTI to Brent hedging.......................................................................................8

Conclusion.............................................................................................................................................9

References.............................................................................................................................................9

1

Jet Blue Case Study

Introduction

This report discusses the hedging strategies used by JetBlue Airways and the related

issues. It is a low-cost airline that was started in 2000. Its business model of providing in-

flight entertainment and other customer centric services at affordable costs helps the

company grow remarkably. It went public in 2002 and experienced high profitability.

But, in 2005 the company’s profits were hit by the rising costs of jet fuel. JetBlue found it

difficult to pass these rising costs as surcharges to the customers as it was not matched by

the other competitors. Hence, the company started hedging its fuel prices to protect its

cost structure and profitability. The company entered into various contracts like swaps,

call options, swaps and collars with underlying as crude oil, jet fuel or heating oil to

hedge its fuel costs. These hedges help airlines to fix the future costs for its jet fuel but

these derivatives contract can be too costly. Also, they can have negative effects if fuel

prices decline drastically. The report first discusses the need for the airlines and JetBlue

in particular to hedge its fuel costs. The advantages of fixing a future price are discussed

along with the negative effects and costs of these contracts. Then the report discusses

various hedging strategies used by the company. The report also talks about the crack

spread and its calculation. It is discussed that basis risk is involved when cross hedging

strategies are used and there is difference between the price of the crude oil and its refined

products. The report further discusses about the price risk and quantity risks. It discusses

which risks need to be hedged and which need to be left unhedged by the company. It

discusses whether airlines should 100% hedge its fuel prices. Finally, the report talks

about the reason to shift from the WTI to Brent crude oil contracts for hedging jet fuel

prices based upon the 2007 to 2011 data.

Should Jet blue hedge its fuel cost?

Hedging refers to the risk management strategy commonly used by the investors in the

stock exchange, with the purpose of reducing or mitigating the risks arising out of price

fluctuations in currencies, commodities, interest rates, securities, weather etc. It can also

be referred as a tactic to transfer risks without having any kind of insurance policies

(Advisorymandi, 2019). It assists companies to maintain their profits during the down

season.

2

Introduction

This report discusses the hedging strategies used by JetBlue Airways and the related

issues. It is a low-cost airline that was started in 2000. Its business model of providing in-

flight entertainment and other customer centric services at affordable costs helps the

company grow remarkably. It went public in 2002 and experienced high profitability.

But, in 2005 the company’s profits were hit by the rising costs of jet fuel. JetBlue found it

difficult to pass these rising costs as surcharges to the customers as it was not matched by

the other competitors. Hence, the company started hedging its fuel prices to protect its

cost structure and profitability. The company entered into various contracts like swaps,

call options, swaps and collars with underlying as crude oil, jet fuel or heating oil to

hedge its fuel costs. These hedges help airlines to fix the future costs for its jet fuel but

these derivatives contract can be too costly. Also, they can have negative effects if fuel

prices decline drastically. The report first discusses the need for the airlines and JetBlue

in particular to hedge its fuel costs. The advantages of fixing a future price are discussed

along with the negative effects and costs of these contracts. Then the report discusses

various hedging strategies used by the company. The report also talks about the crack

spread and its calculation. It is discussed that basis risk is involved when cross hedging

strategies are used and there is difference between the price of the crude oil and its refined

products. The report further discusses about the price risk and quantity risks. It discusses

which risks need to be hedged and which need to be left unhedged by the company. It

discusses whether airlines should 100% hedge its fuel prices. Finally, the report talks

about the reason to shift from the WTI to Brent crude oil contracts for hedging jet fuel

prices based upon the 2007 to 2011 data.

Should Jet blue hedge its fuel cost?

Hedging refers to the risk management strategy commonly used by the investors in the

stock exchange, with the purpose of reducing or mitigating the risks arising out of price

fluctuations in currencies, commodities, interest rates, securities, weather etc. It can also

be referred as a tactic to transfer risks without having any kind of insurance policies

(Advisorymandi, 2019). It assists companies to maintain their profits during the down

season.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jet Blue Case Study

There are airline companies which do not choose to hedge with two assumptions in their

mind. First, these companies think that prices of fuel would come down in the near future.

Second, they develop the thought of passing inflation of jet fuel prices onto the fliers or

consumers. However, both assumptions are extremely dangerous because of the highly

volatile fuel prices and competition posing a downward pressure over the profit margins.

Therefore, it is always better for the airline companies to focus more on hedging fuel

prices to avoid price shocks in future instead of putting an effort to outperform the

market.

However, there are many derivative instruments which are used for hedging purpose but

most of the financiers fail to understand the uses of these instruments. At the end, airline

companies have to take the support of banks and other hedge fund managers to hedge

their position. However, these banks and hedge fund managers may not have the best

interest of these airline companies in their heart (Kholeif, 2017). In order to form a

perfect and useful hedging strategy it is required for the airline companies to integrate it

with the entire corporate strategy for matching strategic investments.

If we talk about the airlines industry then hedging of fuel prices have become a common

practice. It has been seen that cost of jet fuel accounts for 30%-40% of entire operating

costs of the airline companies. In the same way, Jet Blue Airways accounts for 40% of the

company’s total cost and therefore it treats the process of fuel hedging as an insurance

policy. Prices of fuel are highly volatile in nature when compared to any other type of

operational cost incurred by the airline companies. Therefore, it is always safe for the

airline companies to hedge its fuel prices to avoid any type of loss in future due to sudden

change in fuel price. These airline companies hedge the fuel prices by buying or selling

crude oil at a price expected in future using different instruments like options, forwards,

future, swaps etc. which are known as hedging instruments or derivative instruments.

Derivatives are costly affairs sometimes hedging fuel prices poses a great risk for the

company. It happens that prices of fuel decline sharply in future and at the end airline

companies bear a heavy loss.

At present, Jet Blue airways has entered into number of hedging contracts like call

options, swaps and collar contracts to hedge fuel risk. These contracts cost millions of

3

There are airline companies which do not choose to hedge with two assumptions in their

mind. First, these companies think that prices of fuel would come down in the near future.

Second, they develop the thought of passing inflation of jet fuel prices onto the fliers or

consumers. However, both assumptions are extremely dangerous because of the highly

volatile fuel prices and competition posing a downward pressure over the profit margins.

Therefore, it is always better for the airline companies to focus more on hedging fuel

prices to avoid price shocks in future instead of putting an effort to outperform the

market.

However, there are many derivative instruments which are used for hedging purpose but

most of the financiers fail to understand the uses of these instruments. At the end, airline

companies have to take the support of banks and other hedge fund managers to hedge

their position. However, these banks and hedge fund managers may not have the best

interest of these airline companies in their heart (Kholeif, 2017). In order to form a

perfect and useful hedging strategy it is required for the airline companies to integrate it

with the entire corporate strategy for matching strategic investments.

If we talk about the airlines industry then hedging of fuel prices have become a common

practice. It has been seen that cost of jet fuel accounts for 30%-40% of entire operating

costs of the airline companies. In the same way, Jet Blue Airways accounts for 40% of the

company’s total cost and therefore it treats the process of fuel hedging as an insurance

policy. Prices of fuel are highly volatile in nature when compared to any other type of

operational cost incurred by the airline companies. Therefore, it is always safe for the

airline companies to hedge its fuel prices to avoid any type of loss in future due to sudden

change in fuel price. These airline companies hedge the fuel prices by buying or selling

crude oil at a price expected in future using different instruments like options, forwards,

future, swaps etc. which are known as hedging instruments or derivative instruments.

Derivatives are costly affairs sometimes hedging fuel prices poses a great risk for the

company. It happens that prices of fuel decline sharply in future and at the end airline

companies bear a heavy loss.

At present, Jet Blue airways has entered into number of hedging contracts like call

options, swaps and collar contracts to hedge fuel risk. These contracts cost millions of

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jet Blue Case Study

dollars to the company and probability to incur loss due to heavy fall in fuel prices exist.

However, it is advisable for Jet Blue to hedge its fuel cost as the prices of jet fuel are

highly volatile in nature and it is necessary to protect the company from any losses arising

out of this price volatility as the same happened in 2005 when Jet Blue suffered a heavy

loss due to increased jet fuel price.

Various strategies used by airlines to hedge fuel price risk.

Airline companies use hedging strategies to avoid the situation of loss in future due to

price fluctuation of jet fuel. It is basically used as a protection tool against unforeseen

condition.

Now, when airline companies know that price of jet fuel oil would rise in future, they try

to mitigate these risks and purchases current oil contract for meeting the future needs.

Companies also buy call options for hedging against increasing jet fuel cost. It gives

airline companies the right to purchase jet fuel oil on pre-decided future date at an agreed

price (Zacks Equity Research, 2015).

Airline companies also uses collar hedge strategy for hedging against the rising jet fuel

cost. Here, companies purchase both call option and put option. One side company

purchases a call option where it gets the right to purchase jet fuel oil on pre-decided date

at an agreed price. On the other side, company purchases a put option where it gets right

to sell jet fuel oil on pre-decided date at an agreed price. When airline company expect a

rise in the fuel prices then put option help that company from the loss of declining fuel

price and if fuel price goes up then it would lose some amount per call option contract say

$5. Here, collar hedge helps the company from incurring this loss (Tarver, 2015).

Companies operating the airline industry often employs swap strategy to hedge its risk

against fuel price fluctuation. Unlike call option, when a company purchases a swap it

becomes an obligation for it to exercise the contract. Like, even if there is a decline in jet

fuel prices, airline company has to exercise the swap contract at a pre- specified rate and

date and incur loss (Gosai, 2017).

Airlines like JetBlue have to cross hedge the jet fuel risk as the derivatives contract based

upon the crude oil have higher trading volume that leads to lower costs and better

4

dollars to the company and probability to incur loss due to heavy fall in fuel prices exist.

However, it is advisable for Jet Blue to hedge its fuel cost as the prices of jet fuel are

highly volatile in nature and it is necessary to protect the company from any losses arising

out of this price volatility as the same happened in 2005 when Jet Blue suffered a heavy

loss due to increased jet fuel price.

Various strategies used by airlines to hedge fuel price risk.

Airline companies use hedging strategies to avoid the situation of loss in future due to

price fluctuation of jet fuel. It is basically used as a protection tool against unforeseen

condition.

Now, when airline companies know that price of jet fuel oil would rise in future, they try

to mitigate these risks and purchases current oil contract for meeting the future needs.

Companies also buy call options for hedging against increasing jet fuel cost. It gives

airline companies the right to purchase jet fuel oil on pre-decided future date at an agreed

price (Zacks Equity Research, 2015).

Airline companies also uses collar hedge strategy for hedging against the rising jet fuel

cost. Here, companies purchase both call option and put option. One side company

purchases a call option where it gets the right to purchase jet fuel oil on pre-decided date

at an agreed price. On the other side, company purchases a put option where it gets right

to sell jet fuel oil on pre-decided date at an agreed price. When airline company expect a

rise in the fuel prices then put option help that company from the loss of declining fuel

price and if fuel price goes up then it would lose some amount per call option contract say

$5. Here, collar hedge helps the company from incurring this loss (Tarver, 2015).

Companies operating the airline industry often employs swap strategy to hedge its risk

against fuel price fluctuation. Unlike call option, when a company purchases a swap it

becomes an obligation for it to exercise the contract. Like, even if there is a decline in jet

fuel prices, airline company has to exercise the swap contract at a pre- specified rate and

date and incur loss (Gosai, 2017).

Airlines like JetBlue have to cross hedge the jet fuel risk as the derivatives contract based

upon the crude oil have higher trading volume that leads to lower costs and better

4

Jet Blue Case Study

liquidity. The prices of these underlying products like crude oil have high correlation with

jet fuel prices as jet fuel is produced from the distillation of crude oil. SO. It makes sense

to use cross hedging.

JetBlue reduced its hedging in 2009 because of the low fuel prices during that period. The

company wanted to take advantage of the declining fuel prices at that time without fixing

the future prices of its jet fuel. The company had switched from one underlying to other

due to the better trackability of the different products which reduced its basis risk, which

arises from the lack of correlation between the hedged commodity and the underlying of

the derivative contract.

Crack spread.

What is Crack spread?

Various products are generated from crude oil via the distillation process. The prices of

refined petroleum products and crude oil are highly correlated but there is difference in

these prices due to various factors. The crack spread is the difference between the price of

the input and the price of the output of the process (Ramkumar, 2019).

The most basic crack spread is just a simple 1-1 spread. For example, the difference

between the price of jet fuel (refined product) and the price of crude oil (input). The

crack-spread is quoted in terms of dollars-per-barrel. In the case of jet fuel and crude oil

1-1 crack spread, crude oil is quoted in per barrel terms but the jet fuel is quoted in ger

gallon terms. As there are 42 gallons in a barrel so jet fuel prices need to be multiplied by

42 to convert these from per gallon to per barrel terms.

Calculation of the crack spread.

Calculation of crack spread is simply the difference between the price of total output

products and the price of total input divided by the number of barrels. So, to calculate the

1-1 crack spread of crude oil and jet fuel, the price of one barrel of crude oil is subtracted

from the price of one barrel of the jet fuel and the resulting value is divided by 1 (CME

Group, n.d.).

5

liquidity. The prices of these underlying products like crude oil have high correlation with

jet fuel prices as jet fuel is produced from the distillation of crude oil. SO. It makes sense

to use cross hedging.

JetBlue reduced its hedging in 2009 because of the low fuel prices during that period. The

company wanted to take advantage of the declining fuel prices at that time without fixing

the future prices of its jet fuel. The company had switched from one underlying to other

due to the better trackability of the different products which reduced its basis risk, which

arises from the lack of correlation between the hedged commodity and the underlying of

the derivative contract.

Crack spread.

What is Crack spread?

Various products are generated from crude oil via the distillation process. The prices of

refined petroleum products and crude oil are highly correlated but there is difference in

these prices due to various factors. The crack spread is the difference between the price of

the input and the price of the output of the process (Ramkumar, 2019).

The most basic crack spread is just a simple 1-1 spread. For example, the difference

between the price of jet fuel (refined product) and the price of crude oil (input). The

crack-spread is quoted in terms of dollars-per-barrel. In the case of jet fuel and crude oil

1-1 crack spread, crude oil is quoted in per barrel terms but the jet fuel is quoted in ger

gallon terms. As there are 42 gallons in a barrel so jet fuel prices need to be multiplied by

42 to convert these from per gallon to per barrel terms.

Calculation of the crack spread.

Calculation of crack spread is simply the difference between the price of total output

products and the price of total input divided by the number of barrels. So, to calculate the

1-1 crack spread of crude oil and jet fuel, the price of one barrel of crude oil is subtracted

from the price of one barrel of the jet fuel and the resulting value is divided by 1 (CME

Group, n.d.).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jet Blue Case Study

As given in the case study, at the end of December 2011 the price of WTI Crude oil was

$98.83 per barrel and the price of jet fuel was $2.917 per gallon. Multiplying $2.917 with

42 to find jet fuel price in per barrel terms of $122.514. So, the 1-1 crude oil-jet fuel crack

spread was ($122.514 - $98.83)/1 = $23.684 per barrel.

Volatility in the crack spread and its effect on the hedging.

As the commodity prices are very volatile so the crack spread that depends on the prices

of various commodities (jet fuel, crude oil etc.) can be incredibly volatile. As observed in

the case study, the 1-1 crack spread of crude oil and jet fuel had oscillated between $3.9

per barrel to $41.9 per barrel from 2007 to 2011.

There is the issue of basis risk between the hedged commodity (jet fuel) and the hedging

derivative (crude oil) prices as the crack spread fluctuates and this adds to the airline

costs.

Following are the factors that affect value of the Crack Spread (CME Group, 2017):

Geopolitical issue: Politics, geography and foreign policies can affect the supply of crude

oil. If supply is reduced then crack-spread will weaken initially due to the higher crude oil

prices in comparison to the refined products but later on the spread will strengthen as

refineries reduce the product outputs in response to tighter crude oil supply.

Strong sustained product demand: Prices of the refined output products increase with the

strong sustained demand of particular product which strengthen the crack spread.

Environmental regulation on tighter product specifications: Tightening of product supply

can lead to higher product prices that strengthen the spread.

Hedging strategies by the airlines.

What risks are hedged?

There are various uncertainties involved in every business operation and businesses can

hedge these risks to avoid losses. But some of the uncertainties are left unhedged to avoid

6

As given in the case study, at the end of December 2011 the price of WTI Crude oil was

$98.83 per barrel and the price of jet fuel was $2.917 per gallon. Multiplying $2.917 with

42 to find jet fuel price in per barrel terms of $122.514. So, the 1-1 crude oil-jet fuel crack

spread was ($122.514 - $98.83)/1 = $23.684 per barrel.

Volatility in the crack spread and its effect on the hedging.

As the commodity prices are very volatile so the crack spread that depends on the prices

of various commodities (jet fuel, crude oil etc.) can be incredibly volatile. As observed in

the case study, the 1-1 crack spread of crude oil and jet fuel had oscillated between $3.9

per barrel to $41.9 per barrel from 2007 to 2011.

There is the issue of basis risk between the hedged commodity (jet fuel) and the hedging

derivative (crude oil) prices as the crack spread fluctuates and this adds to the airline

costs.

Following are the factors that affect value of the Crack Spread (CME Group, 2017):

Geopolitical issue: Politics, geography and foreign policies can affect the supply of crude

oil. If supply is reduced then crack-spread will weaken initially due to the higher crude oil

prices in comparison to the refined products but later on the spread will strengthen as

refineries reduce the product outputs in response to tighter crude oil supply.

Strong sustained product demand: Prices of the refined output products increase with the

strong sustained demand of particular product which strengthen the crack spread.

Environmental regulation on tighter product specifications: Tightening of product supply

can lead to higher product prices that strengthen the spread.

Hedging strategies by the airlines.

What risks are hedged?

There are various uncertainties involved in every business operation and businesses can

hedge these risks to avoid losses. But some of the uncertainties are left unhedged to avoid

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jet Blue Case Study

making losses if market moves in opposite direction or if the actual quantity required is

different than the quantity earlier estimated while making hedging decision.

Price risk and Quantity risk.

Price risk is related to the unfavourable movement of the prices of the product. For

example, airlines face huge risk from the upward movement in the prices of jet fuel. From

the case study it can be seen that fuel represented approximately 40% of JetBlue’s

operational costs. So, the airline hedged some of its fuel price risk as it found difficult to

pass increase in fuel prices to customers via surcharges if this was not matched by other

players. Due to this limited ability to pass through the increased costs to customers,

hedging the fuel price risk protected its cost structure.

Quantity risk is the unfavourable change in the quantity of the product that is being

hedged. Airlines faces quantity risk as if the demand is lower in future and hence the

required quantity of fuel in this scenario will be lower than earlier estimated quantity. If

the fuel prices decline then company will lose due to lower spot prices and due to higher

quantity hedged using derivatives. Opposite of this can also happen if demand turns out to

be higher and fuel required is higher than the hedged quantity. Then, if price of fuel

increases in spot market then airline will have to pay more for increased quantity.

As given in the case study, JetBlue’s entered into hedges on discretionary basis without

setting particular targets. In 2009, the company hedged less but it increased the

percentage of the fuel hedged in 2010 and 2011. Dynamic strategy was based on the

mean-reverting oil prices as airlines wanted to lock future oil prices at the low point in the

cycle but taking advantage of the eventual decline in prices by adjusting the quantities

that are hedged (Jaganathan & Bryan, 2015).

To what extent should airlines hedge their fuel risk.

Airlines used the hedging of its fuel costs as an insurance to protect them from rising fuel

price and to protect their profitability. But purchasing of these derivatives contracts for

hedging purposes could be a costly affair. There is an additional basis risk issue because

of the cross hedging involved that adds extra risk to the hedging process. Also, if there is

a sharp decline in the fuel prices that will lead to huge losses for the airline. Due to the

7

making losses if market moves in opposite direction or if the actual quantity required is

different than the quantity earlier estimated while making hedging decision.

Price risk and Quantity risk.

Price risk is related to the unfavourable movement of the prices of the product. For

example, airlines face huge risk from the upward movement in the prices of jet fuel. From

the case study it can be seen that fuel represented approximately 40% of JetBlue’s

operational costs. So, the airline hedged some of its fuel price risk as it found difficult to

pass increase in fuel prices to customers via surcharges if this was not matched by other

players. Due to this limited ability to pass through the increased costs to customers,

hedging the fuel price risk protected its cost structure.

Quantity risk is the unfavourable change in the quantity of the product that is being

hedged. Airlines faces quantity risk as if the demand is lower in future and hence the

required quantity of fuel in this scenario will be lower than earlier estimated quantity. If

the fuel prices decline then company will lose due to lower spot prices and due to higher

quantity hedged using derivatives. Opposite of this can also happen if demand turns out to

be higher and fuel required is higher than the hedged quantity. Then, if price of fuel

increases in spot market then airline will have to pay more for increased quantity.

As given in the case study, JetBlue’s entered into hedges on discretionary basis without

setting particular targets. In 2009, the company hedged less but it increased the

percentage of the fuel hedged in 2010 and 2011. Dynamic strategy was based on the

mean-reverting oil prices as airlines wanted to lock future oil prices at the low point in the

cycle but taking advantage of the eventual decline in prices by adjusting the quantities

that are hedged (Jaganathan & Bryan, 2015).

To what extent should airlines hedge their fuel risk.

Airlines used the hedging of its fuel costs as an insurance to protect them from rising fuel

price and to protect their profitability. But purchasing of these derivatives contracts for

hedging purposes could be a costly affair. There is an additional basis risk issue because

of the cross hedging involved that adds extra risk to the hedging process. Also, if there is

a sharp decline in the fuel prices that will lead to huge losses for the airline. Due to the

7

Jet Blue Case Study

high volatility in fuel prices, airlines do not go for 100% hedge or over hedging as that

can lead to huge losses if fuel prices decline (Leff, 2018).

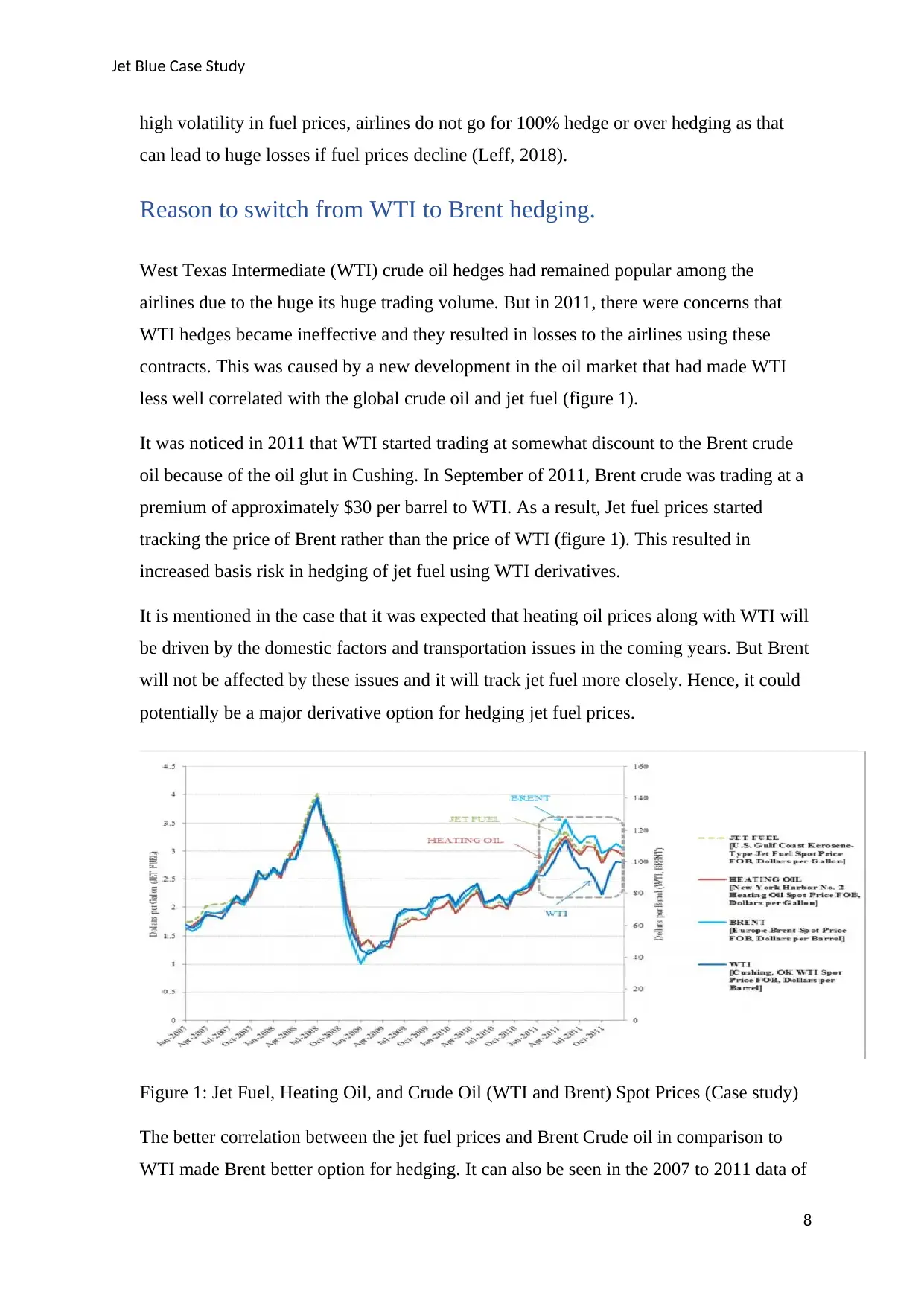

Reason to switch from WTI to Brent hedging.

West Texas Intermediate (WTI) crude oil hedges had remained popular among the

airlines due to the huge its huge trading volume. But in 2011, there were concerns that

WTI hedges became ineffective and they resulted in losses to the airlines using these

contracts. This was caused by a new development in the oil market that had made WTI

less well correlated with the global crude oil and jet fuel (figure 1).

It was noticed in 2011 that WTI started trading at somewhat discount to the Brent crude

oil because of the oil glut in Cushing. In September of 2011, Brent crude was trading at a

premium of approximately $30 per barrel to WTI. As a result, Jet fuel prices started

tracking the price of Brent rather than the price of WTI (figure 1). This resulted in

increased basis risk in hedging of jet fuel using WTI derivatives.

It is mentioned in the case that it was expected that heating oil prices along with WTI will

be driven by the domestic factors and transportation issues in the coming years. But Brent

will not be affected by these issues and it will track jet fuel more closely. Hence, it could

potentially be a major derivative option for hedging jet fuel prices.

Figure 1: Jet Fuel, Heating Oil, and Crude Oil (WTI and Brent) Spot Prices (Case study)

The better correlation between the jet fuel prices and Brent Crude oil in comparison to

WTI made Brent better option for hedging. It can also be seen in the 2007 to 2011 data of

8

high volatility in fuel prices, airlines do not go for 100% hedge or over hedging as that

can lead to huge losses if fuel prices decline (Leff, 2018).

Reason to switch from WTI to Brent hedging.

West Texas Intermediate (WTI) crude oil hedges had remained popular among the

airlines due to the huge its huge trading volume. But in 2011, there were concerns that

WTI hedges became ineffective and they resulted in losses to the airlines using these

contracts. This was caused by a new development in the oil market that had made WTI

less well correlated with the global crude oil and jet fuel (figure 1).

It was noticed in 2011 that WTI started trading at somewhat discount to the Brent crude

oil because of the oil glut in Cushing. In September of 2011, Brent crude was trading at a

premium of approximately $30 per barrel to WTI. As a result, Jet fuel prices started

tracking the price of Brent rather than the price of WTI (figure 1). This resulted in

increased basis risk in hedging of jet fuel using WTI derivatives.

It is mentioned in the case that it was expected that heating oil prices along with WTI will

be driven by the domestic factors and transportation issues in the coming years. But Brent

will not be affected by these issues and it will track jet fuel more closely. Hence, it could

potentially be a major derivative option for hedging jet fuel prices.

Figure 1: Jet Fuel, Heating Oil, and Crude Oil (WTI and Brent) Spot Prices (Case study)

The better correlation between the jet fuel prices and Brent Crude oil in comparison to

WTI made Brent better option for hedging. It can also be seen in the 2007 to 2011 data of

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Jet Blue Case Study

the spot prices of jet fuel, WTI and Brent and their regression analysis that Brent prices

rather than WTI moved in tandem with the jet fuel.

Conclusion

The report discussed various hedging strategies and related issues for the JetBlue

Airways. It discussed that hedging allowed the company to fix the costs of its jet fuel to

protect it profitability. But there are some risks involved in the hedging due to the high

costs of the derivatives contracts and negative effects due to declining fuel prices. It

discussed the use of over the counter products like swaps contacts, call options and collar

to fix the future price of jet fuel. These over the counter products are customizable as

compared to exchange traded products so it reduced basis risk. It is further discussed that

the difference in prices of the crude oil that is the input of the distillation process and jet

fuel that is the output or refined product gives rise to crack spread. It is further discussed

that airlines faces both the price risk and quantity risk. It is advisable for the airlines to

not fully hedge its fuel costs as there can be negative effect of declining fuel prices

because of the volatile nature of commodity products. Finally, the report discussed that

due to the better correlation of Brent crude oil as compared to WTI with the jet fuel due to

changing structure of the oil market made Brent better option for hedging.

References

Advisorymandi. (2019). What Is Hedging? Advantages And Disadvantages. Retrieved

February 16, 2020 from http://www.advisorymandi.com/blog/what-is-hedging-

advantages-and-disadvantages/.

CME Group. (n.d.). UNDERSTANDING FUTURES SPREADS: Learn about the 1:1

Crack Spread. Retrieved February 16, 2020 from

https://www.cmegroup.com/education/courses/understanding-futures-spreads/

learn-about-the-1-1-crack-spread.html.

CME Group. (2017). Introduction to Crack Spreads. Retrieved February 16, 2020 from

https://www.cmegroup.com/education/articles-and-reports/introduction-to-crack-

spreads.html.

Gosai, H. (2017). Part One: An Introduction to Airline Fuel Hedging. Retrieved February

16, 2020 from https://airlinegeeks.com/2017/09/02/part-one-an-introduction-to-

airline-fuel-hedging/.

9

the spot prices of jet fuel, WTI and Brent and their regression analysis that Brent prices

rather than WTI moved in tandem with the jet fuel.

Conclusion

The report discussed various hedging strategies and related issues for the JetBlue

Airways. It discussed that hedging allowed the company to fix the costs of its jet fuel to

protect it profitability. But there are some risks involved in the hedging due to the high

costs of the derivatives contracts and negative effects due to declining fuel prices. It

discussed the use of over the counter products like swaps contacts, call options and collar

to fix the future price of jet fuel. These over the counter products are customizable as

compared to exchange traded products so it reduced basis risk. It is further discussed that

the difference in prices of the crude oil that is the input of the distillation process and jet

fuel that is the output or refined product gives rise to crack spread. It is further discussed

that airlines faces both the price risk and quantity risk. It is advisable for the airlines to

not fully hedge its fuel costs as there can be negative effect of declining fuel prices

because of the volatile nature of commodity products. Finally, the report discussed that

due to the better correlation of Brent crude oil as compared to WTI with the jet fuel due to

changing structure of the oil market made Brent better option for hedging.

References

Advisorymandi. (2019). What Is Hedging? Advantages And Disadvantages. Retrieved

February 16, 2020 from http://www.advisorymandi.com/blog/what-is-hedging-

advantages-and-disadvantages/.

CME Group. (n.d.). UNDERSTANDING FUTURES SPREADS: Learn about the 1:1

Crack Spread. Retrieved February 16, 2020 from

https://www.cmegroup.com/education/courses/understanding-futures-spreads/

learn-about-the-1-1-crack-spread.html.

CME Group. (2017). Introduction to Crack Spreads. Retrieved February 16, 2020 from

https://www.cmegroup.com/education/articles-and-reports/introduction-to-crack-

spreads.html.

Gosai, H. (2017). Part One: An Introduction to Airline Fuel Hedging. Retrieved February

16, 2020 from https://airlinegeeks.com/2017/09/02/part-one-an-introduction-to-

airline-fuel-hedging/.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Jet Blue Case Study

Jaganathan, J. & Bryan, V. (2015). Airlines prepare to hedge more jet fuel to lock in huge

savings. Retrieved February 16, 2020 from https://www.reuters.com/article/asia-

airlines-hedging/airlines-prepare-to-hedge-more-jet-fuel-to-lock-in-huge-savings-

idUSKBN0KN0RM20150114.

Kholeif, Y. (2017). Should airlines hedge their fuel costs?. Retrieved February 16, 2020

from https://www.linkedin.com/pulse/should-airlines-hedge-fuel-costs-youssef-

kholeif/.

Leff, G. (2018). Why American Airlines is Brilliant Not to Hedge Fuel. Retrieved

February 16, 2020 from https://viewfromthewing.com/american-airlines-brilliant-

not-hedge-fuel/.

Ramkumar, M. (2019). Refining Crack Spread Overview: All You Ever Wanted to Know.

Retrieved February 16, 2020 from https://marketrealist.com/2019/09/refining-

crack-spread-overview-you-ever-wanted-know/.

Tarver, E. (2015). 4 Ways Airlines Hedge Against Oil. Retrieved February 16, 2020 from

https://www.investopedia.com/articles/investing/081415/4-ways-airlines-hedge-

against-oil.asp.

Zacks Equity Research. (2015). How Do Airlines Hedge Against Rising Fuel Prices?.

Retrieved February 16, 2020 from https://www.nasdaq.com/articles/how-do-

airlines-hedge-against-rising-fuel-prices-2015-08-31.

10

Jaganathan, J. & Bryan, V. (2015). Airlines prepare to hedge more jet fuel to lock in huge

savings. Retrieved February 16, 2020 from https://www.reuters.com/article/asia-

airlines-hedging/airlines-prepare-to-hedge-more-jet-fuel-to-lock-in-huge-savings-

idUSKBN0KN0RM20150114.

Kholeif, Y. (2017). Should airlines hedge their fuel costs?. Retrieved February 16, 2020

from https://www.linkedin.com/pulse/should-airlines-hedge-fuel-costs-youssef-

kholeif/.

Leff, G. (2018). Why American Airlines is Brilliant Not to Hedge Fuel. Retrieved

February 16, 2020 from https://viewfromthewing.com/american-airlines-brilliant-

not-hedge-fuel/.

Ramkumar, M. (2019). Refining Crack Spread Overview: All You Ever Wanted to Know.

Retrieved February 16, 2020 from https://marketrealist.com/2019/09/refining-

crack-spread-overview-you-ever-wanted-know/.

Tarver, E. (2015). 4 Ways Airlines Hedge Against Oil. Retrieved February 16, 2020 from

https://www.investopedia.com/articles/investing/081415/4-ways-airlines-hedge-

against-oil.asp.

Zacks Equity Research. (2015). How Do Airlines Hedge Against Rising Fuel Prices?.

Retrieved February 16, 2020 from https://www.nasdaq.com/articles/how-do-

airlines-hedge-against-rising-fuel-prices-2015-08-31.

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.