Taxation Return Analysis: Applying ATO Laws for Jez Morgan's Return

VerifiedAdded on 2020/01/07

|26

|5155

|149

Homework Assignment

AI Summary

This assignment analyzes the tax return of Jez Morgan for the 2015/16 financial year, applying Australian Taxation Office (ATO) laws and principles. It examines various income sources, including salary and wages, allowances, interest, dividends, and capital gains. The analysis categorizes income as assessable or non-assessable, providing justifications based on ATO regulations. Specific items like salary from Brisbane Secondary College, annual leave pay, and PAYG tax withheld are assessed. The report also covers allowances such as the stationery allowance, gifts, and awards. Furthermore, it delves into interest income from Suncorp and Macquarie, and dividends from CBA and BHP shares, detailing franking credits and dividend reinvestment plans. Capital gains from the sale of inherited shares are also considered. The report follows the step-by-step process of calculating capital gains or losses. The goal is to construct an accurate tax return for Morgan, demonstrating a thorough understanding of Australian taxation laws.

7106AFE Assignment, Semester 3, 2016

INTRODUCTION

Tax refers to a compulsory payment made by assesses following the principles & tax regulations of the country. In Australia, Australian Taxation

Officer (ATO) set policies, tax rules, regulations & provisions whereby all the individuals are who falls in the taxation category are liable to pay taxation as per

due dates to the regulatory bodies. ATO regulates the imposing of taxation obligations & its collections in a proper manner so as to gather money for the

governmental budget. It is the liability of every individual to pay taxes at per prevailing rates and duties and meet out their liabilities timely. If any person fails

to comply with their taxation obligations than, he or she will be penalised by the authority for the same. The aim of present project report is to apply various

laws & principles of ATO for the preparation of taxation return for the Jez Morgan. On the basis of it, it will be identified that what kind of individual receipts

are assessable or not under the taxation framework so as to construct the actual tax return of Morgan for the reporting year 2015/16. All the arguments &

discussion will be supported with the proper evidences of ATO regulations for thoroughly & accurate analysis.

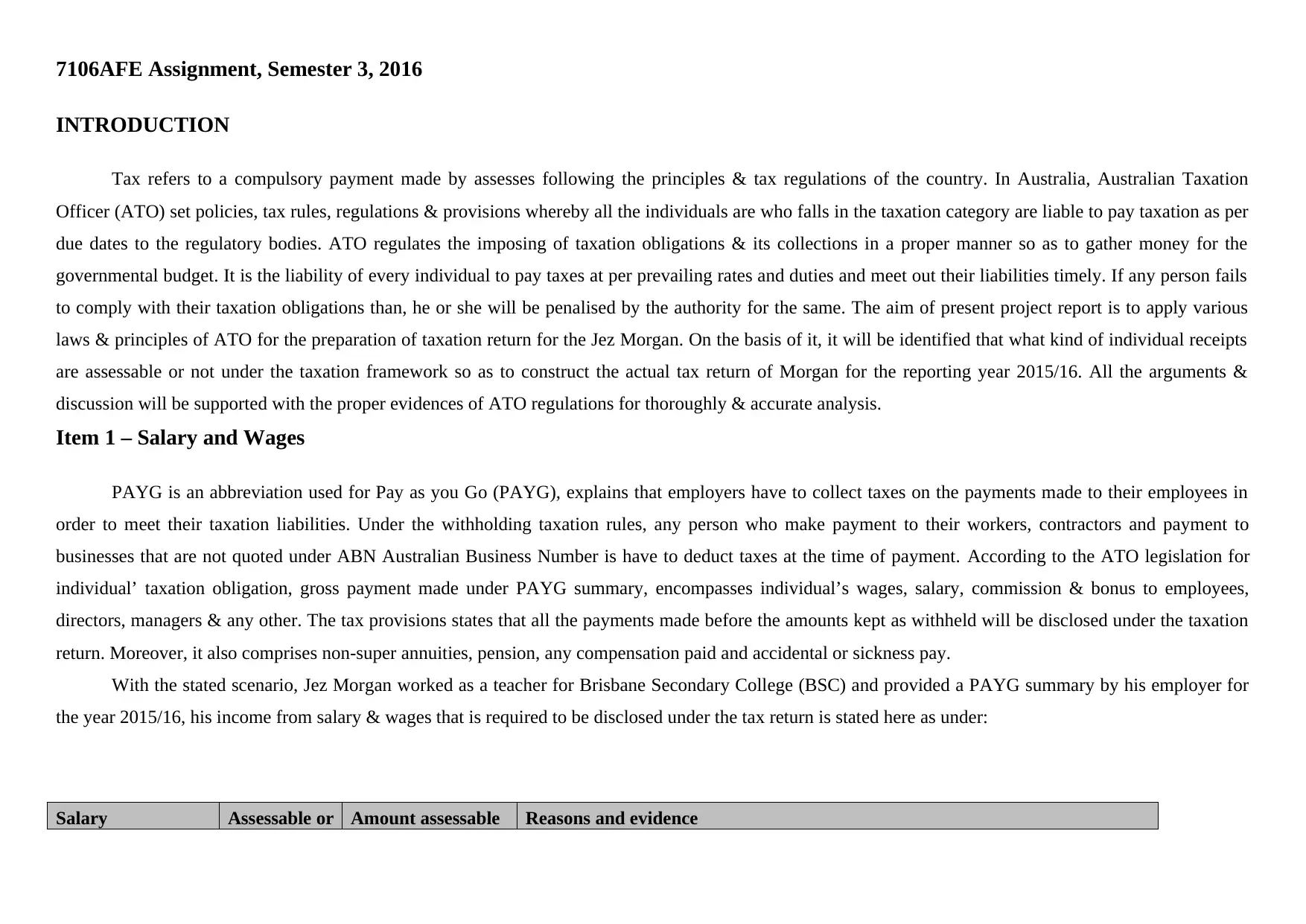

Item 1 – Salary and Wages

PAYG is an abbreviation used for Pay as you Go (PAYG), explains that employers have to collect taxes on the payments made to their employees in

order to meet their taxation liabilities. Under the withholding taxation rules, any person who make payment to their workers, contractors and payment to

businesses that are not quoted under ABN Australian Business Number is have to deduct taxes at the time of payment. According to the ATO legislation for

individual’ taxation obligation, gross payment made under PAYG summary, encompasses individual’s wages, salary, commission & bonus to employees,

directors, managers & any other. The tax provisions states that all the payments made before the amounts kept as withheld will be disclosed under the taxation

return. Moreover, it also comprises non-super annuities, pension, any compensation paid and accidental or sickness pay.

With the stated scenario, Jez Morgan worked as a teacher for Brisbane Secondary College (BSC) and provided a PAYG summary by his employer for

the year 2015/16, his income from salary & wages that is required to be disclosed under the tax return is stated here as under:

Salary Assessable or Amount assessable Reasons and evidence

INTRODUCTION

Tax refers to a compulsory payment made by assesses following the principles & tax regulations of the country. In Australia, Australian Taxation

Officer (ATO) set policies, tax rules, regulations & provisions whereby all the individuals are who falls in the taxation category are liable to pay taxation as per

due dates to the regulatory bodies. ATO regulates the imposing of taxation obligations & its collections in a proper manner so as to gather money for the

governmental budget. It is the liability of every individual to pay taxes at per prevailing rates and duties and meet out their liabilities timely. If any person fails

to comply with their taxation obligations than, he or she will be penalised by the authority for the same. The aim of present project report is to apply various

laws & principles of ATO for the preparation of taxation return for the Jez Morgan. On the basis of it, it will be identified that what kind of individual receipts

are assessable or not under the taxation framework so as to construct the actual tax return of Morgan for the reporting year 2015/16. All the arguments &

discussion will be supported with the proper evidences of ATO regulations for thoroughly & accurate analysis.

Item 1 – Salary and Wages

PAYG is an abbreviation used for Pay as you Go (PAYG), explains that employers have to collect taxes on the payments made to their employees in

order to meet their taxation liabilities. Under the withholding taxation rules, any person who make payment to their workers, contractors and payment to

businesses that are not quoted under ABN Australian Business Number is have to deduct taxes at the time of payment. According to the ATO legislation for

individual’ taxation obligation, gross payment made under PAYG summary, encompasses individual’s wages, salary, commission & bonus to employees,

directors, managers & any other. The tax provisions states that all the payments made before the amounts kept as withheld will be disclosed under the taxation

return. Moreover, it also comprises non-super annuities, pension, any compensation paid and accidental or sickness pay.

With the stated scenario, Jez Morgan worked as a teacher for Brisbane Secondary College (BSC) and provided a PAYG summary by his employer for

the year 2015/16, his income from salary & wages that is required to be disclosed under the tax return is stated here as under:

Salary Assessable or Amount assessable Reasons and evidence

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not?

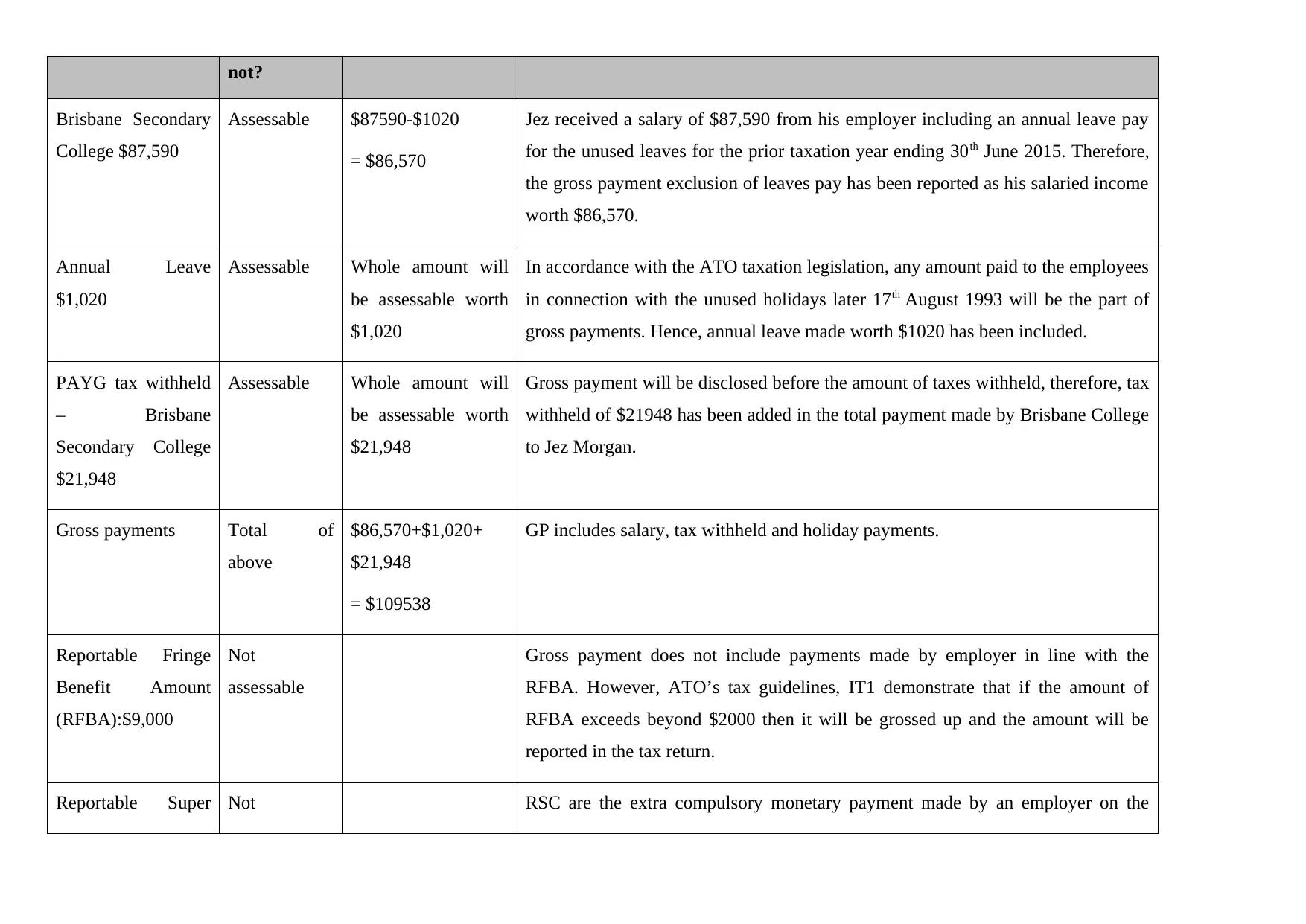

Brisbane Secondary

College $87,590

Assessable $87590-$1020

= $86,570

Jez received a salary of $87,590 from his employer including an annual leave pay

for the unused leaves for the prior taxation year ending 30th June 2015. Therefore,

the gross payment exclusion of leaves pay has been reported as his salaried income

worth $86,570.

Annual Leave

$1,020

Assessable Whole amount will

be assessable worth

$1,020

In accordance with the ATO taxation legislation, any amount paid to the employees

in connection with the unused holidays later 17th August 1993 will be the part of

gross payments. Hence, annual leave made worth $1020 has been included.

PAYG tax withheld

– Brisbane

Secondary College

$21,948

Assessable Whole amount will

be assessable worth

$21,948

Gross payment will be disclosed before the amount of taxes withheld, therefore, tax

withheld of $21948 has been added in the total payment made by Brisbane College

to Jez Morgan.

Gross payments Total of

above

$86,570+$1,020+

$21,948

= $109538

GP includes salary, tax withheld and holiday payments.

Reportable Fringe

Benefit Amount

(RFBA):$9,000

Not

assessable

Gross payment does not include payments made by employer in line with the

RFBA. However, ATO’s tax guidelines, IT1 demonstrate that if the amount of

RFBA exceeds beyond $2000 then it will be grossed up and the amount will be

reported in the tax return.

Reportable Super Not RSC are the extra compulsory monetary payment made by an employer on the

Brisbane Secondary

College $87,590

Assessable $87590-$1020

= $86,570

Jez received a salary of $87,590 from his employer including an annual leave pay

for the unused leaves for the prior taxation year ending 30th June 2015. Therefore,

the gross payment exclusion of leaves pay has been reported as his salaried income

worth $86,570.

Annual Leave

$1,020

Assessable Whole amount will

be assessable worth

$1,020

In accordance with the ATO taxation legislation, any amount paid to the employees

in connection with the unused holidays later 17th August 1993 will be the part of

gross payments. Hence, annual leave made worth $1020 has been included.

PAYG tax withheld

– Brisbane

Secondary College

$21,948

Assessable Whole amount will

be assessable worth

$21,948

Gross payment will be disclosed before the amount of taxes withheld, therefore, tax

withheld of $21948 has been added in the total payment made by Brisbane College

to Jez Morgan.

Gross payments Total of

above

$86,570+$1,020+

$21,948

= $109538

GP includes salary, tax withheld and holiday payments.

Reportable Fringe

Benefit Amount

(RFBA):$9,000

Not

assessable

Gross payment does not include payments made by employer in line with the

RFBA. However, ATO’s tax guidelines, IT1 demonstrate that if the amount of

RFBA exceeds beyond $2000 then it will be grossed up and the amount will be

reported in the tax return.

Reportable Super Not RSC are the extra compulsory monetary payment made by an employer on the

Contribution (RSC):

$3,000

assessable behalf of employee’s salary sacrifice. In accordance with the IT2, If employer

Brisbane College contributed to super fund at employee, Jez’s request, then it will

not be taxed but here is a condition attached that the payment must not exceed the

law requirement. However, in the absence of maximum permissible contribution, it

has been assumed that RSC amount is under the limit hence, not assessable.

Total assessable income $ 109538

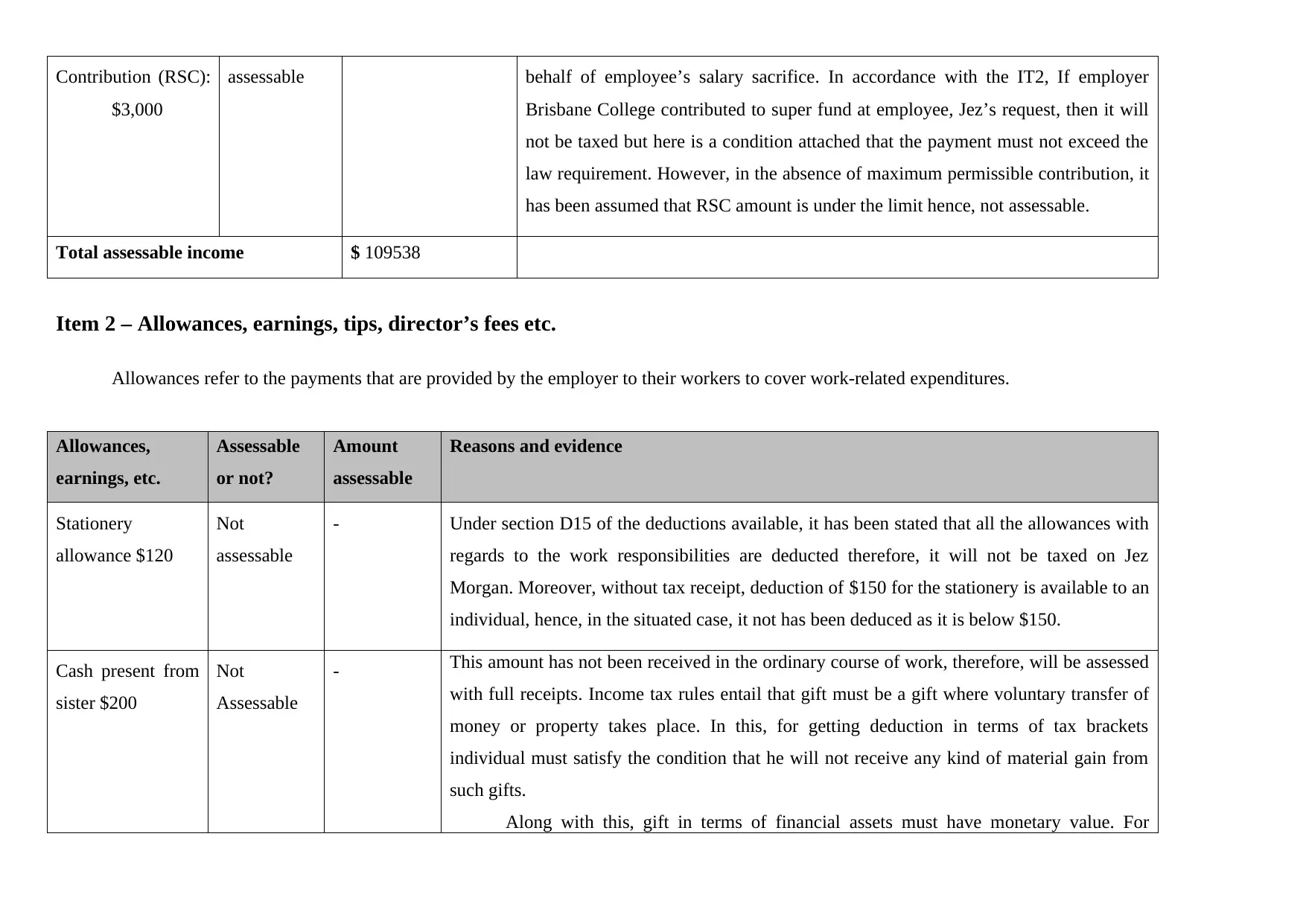

Item 2 – Allowances, earnings, tips, director’s fees etc.

Allowances refer to the payments that are provided by the employer to their workers to cover work-related expenditures.

Allowances,

earnings, etc.

Assessable

or not?

Amount

assessable

Reasons and evidence

Stationery

allowance $120

Not

assessable

- Under section D15 of the deductions available, it has been stated that all the allowances with

regards to the work responsibilities are deducted therefore, it will not be taxed on Jez

Morgan. Moreover, without tax receipt, deduction of $150 for the stationery is available to an

individual, hence, in the situated case, it not has been deduced as it is below $150.

Cash present from

sister $200

Not

Assessable

- This amount has not been received in the ordinary course of work, therefore, will be assessed

with full receipts. Income tax rules entail that gift must be a gift where voluntary transfer of

money or property takes place. In this, for getting deduction in terms of tax brackets

individual must satisfy the condition that he will not receive any kind of material gain from

such gifts.

Along with this, gift in terms of financial assets must have monetary value. For

$3,000

assessable behalf of employee’s salary sacrifice. In accordance with the IT2, If employer

Brisbane College contributed to super fund at employee, Jez’s request, then it will

not be taxed but here is a condition attached that the payment must not exceed the

law requirement. However, in the absence of maximum permissible contribution, it

has been assumed that RSC amount is under the limit hence, not assessable.

Total assessable income $ 109538

Item 2 – Allowances, earnings, tips, director’s fees etc.

Allowances refer to the payments that are provided by the employer to their workers to cover work-related expenditures.

Allowances,

earnings, etc.

Assessable

or not?

Amount

assessable

Reasons and evidence

Stationery

allowance $120

Not

assessable

- Under section D15 of the deductions available, it has been stated that all the allowances with

regards to the work responsibilities are deducted therefore, it will not be taxed on Jez

Morgan. Moreover, without tax receipt, deduction of $150 for the stationery is available to an

individual, hence, in the situated case, it not has been deduced as it is below $150.

Cash present from

sister $200

Not

Assessable

- This amount has not been received in the ordinary course of work, therefore, will be assessed

with full receipts. Income tax rules entail that gift must be a gift where voluntary transfer of

money or property takes place. In this, for getting deduction in terms of tax brackets

individual must satisfy the condition that he will not receive any kind of material gain from

such gifts.

Along with this, gift in terms of financial assets must have monetary value. For

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

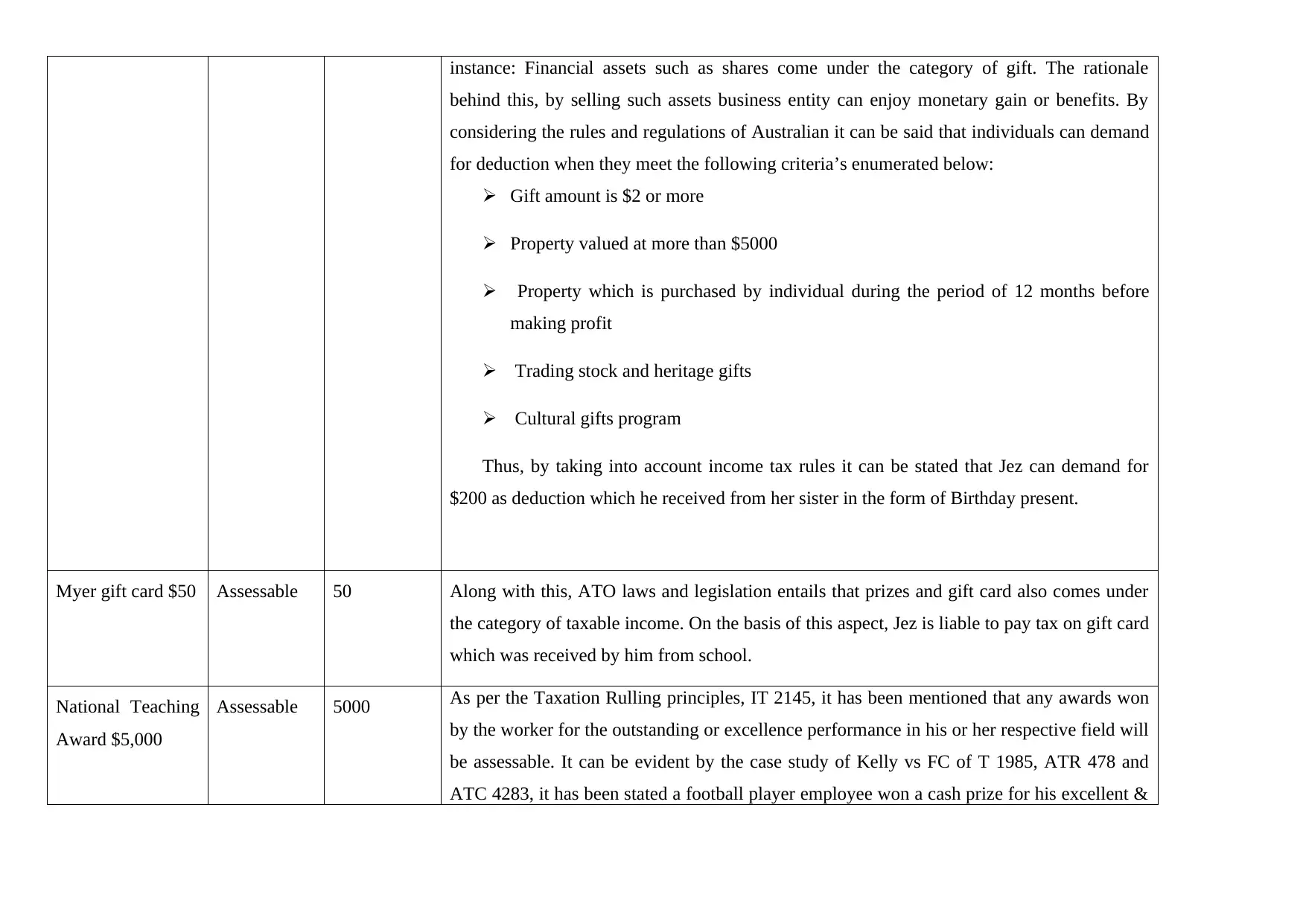

instance: Financial assets such as shares come under the category of gift. The rationale

behind this, by selling such assets business entity can enjoy monetary gain or benefits. By

considering the rules and regulations of Australian it can be said that individuals can demand

for deduction when they meet the following criteria’s enumerated below:

Gift amount is $2 or more

Property valued at more than $5000

Property which is purchased by individual during the period of 12 months before

making profit

Trading stock and heritage gifts

Cultural gifts program

Thus, by taking into account income tax rules it can be stated that Jez can demand for

$200 as deduction which he received from her sister in the form of Birthday present.

Myer gift card $50 Assessable 50 Along with this, ATO laws and legislation entails that prizes and gift card also comes under

the category of taxable income. On the basis of this aspect, Jez is liable to pay tax on gift card

which was received by him from school.

National Teaching

Award $5,000

Assessable 5000 As per the Taxation Rulling principles, IT 2145, it has been mentioned that any awards won

by the worker for the outstanding or excellence performance in his or her respective field will

be assessable. It can be evident by the case study of Kelly vs FC of T 1985, ATR 478 and

ATC 4283, it has been stated a football player employee won a cash prize for his excellent &

behind this, by selling such assets business entity can enjoy monetary gain or benefits. By

considering the rules and regulations of Australian it can be said that individuals can demand

for deduction when they meet the following criteria’s enumerated below:

Gift amount is $2 or more

Property valued at more than $5000

Property which is purchased by individual during the period of 12 months before

making profit

Trading stock and heritage gifts

Cultural gifts program

Thus, by taking into account income tax rules it can be stated that Jez can demand for

$200 as deduction which he received from her sister in the form of Birthday present.

Myer gift card $50 Assessable 50 Along with this, ATO laws and legislation entails that prizes and gift card also comes under

the category of taxable income. On the basis of this aspect, Jez is liable to pay tax on gift card

which was received by him from school.

National Teaching

Award $5,000

Assessable 5000 As per the Taxation Rulling principles, IT 2145, it has been mentioned that any awards won

by the worker for the outstanding or excellence performance in his or her respective field will

be assessable. It can be evident by the case study of Kelly vs FC of T 1985, ATR 478 and

ATC 4283, it has been stated a football player employee won a cash prize for his excellent &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

remarkable playing in the football match. In this, court declared that it is an incidental

payment and received as a virtue of the employment, hence, it has been considered as an

normal incident relation with his job. Further, in accordance with ATO, Jez also received

money such as $5000 as a National Teaching Award. Thus, in accordance with ATO, both

the above mentioned amounts are the part of tax liability.

Total assessable income $5050

Item 10 – Gross Interest

Interest Assessabl

e or not?

Amount

assessable

Reasons and evidence

Suncorp $219

Suncorp $211 Not

Assessable Same as below mentioned reasons.

Macquarie $1,110 Not

Assessable

According to Income Tax Act of Australia income which is earned by the individual through

the means of fixed deposit is come under the tax category. Moreover, such income is also

considered as the one which is earned by the firm from other sources. TDS is one the main

ways of automatic tax collection undertaken by Income Tax departments. In this way,

payment and received as a virtue of the employment, hence, it has been considered as an

normal incident relation with his job. Further, in accordance with ATO, Jez also received

money such as $5000 as a National Teaching Award. Thus, in accordance with ATO, both

the above mentioned amounts are the part of tax liability.

Total assessable income $5050

Item 10 – Gross Interest

Interest Assessabl

e or not?

Amount

assessable

Reasons and evidence

Suncorp $219

Suncorp $211 Not

Assessable Same as below mentioned reasons.

Macquarie $1,110 Not

Assessable

According to Income Tax Act of Australia income which is earned by the individual through

the means of fixed deposit is come under the tax category. Moreover, such income is also

considered as the one which is earned by the firm from other sources. TDS is one the main

ways of automatic tax collection undertaken by Income Tax departments. In this way,

interest received from TDS is partially paid by the bank and the rest is considered for self

assessment tax paid by the individual. On the basis of laws as well as legal regulations bank

can deduct TDS from interest only when the interest amount is greater than $200 per annum.

In this case, TDS is deducted by the banking institution with the rate of 20%.

Given case situation presents that gross interest which was earned by Jez during the

period of 2015-16 from fixed or term deposit accounts for $1110. As per the laws, amount

which is higher than $200 is subject to TDS of 20%. On the basis of this aspect, Macquarie

bank charges 222 in the form of TDS and provided Jez with the amount of $888. Hence, net

income earned by Jez from interest is $888. However, such income is not includes in the tax

category or brackets.

Total interest assessable $ x Label L

TFN withheld $ y Label M

assessment tax paid by the individual. On the basis of laws as well as legal regulations bank

can deduct TDS from interest only when the interest amount is greater than $200 per annum.

In this case, TDS is deducted by the banking institution with the rate of 20%.

Given case situation presents that gross interest which was earned by Jez during the

period of 2015-16 from fixed or term deposit accounts for $1110. As per the laws, amount

which is higher than $200 is subject to TDS of 20%. On the basis of this aspect, Macquarie

bank charges 222 in the form of TDS and provided Jez with the amount of $888. Hence, net

income earned by Jez from interest is $888. However, such income is not includes in the tax

category or brackets.

Total interest assessable $ x Label L

TFN withheld $ y Label M

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

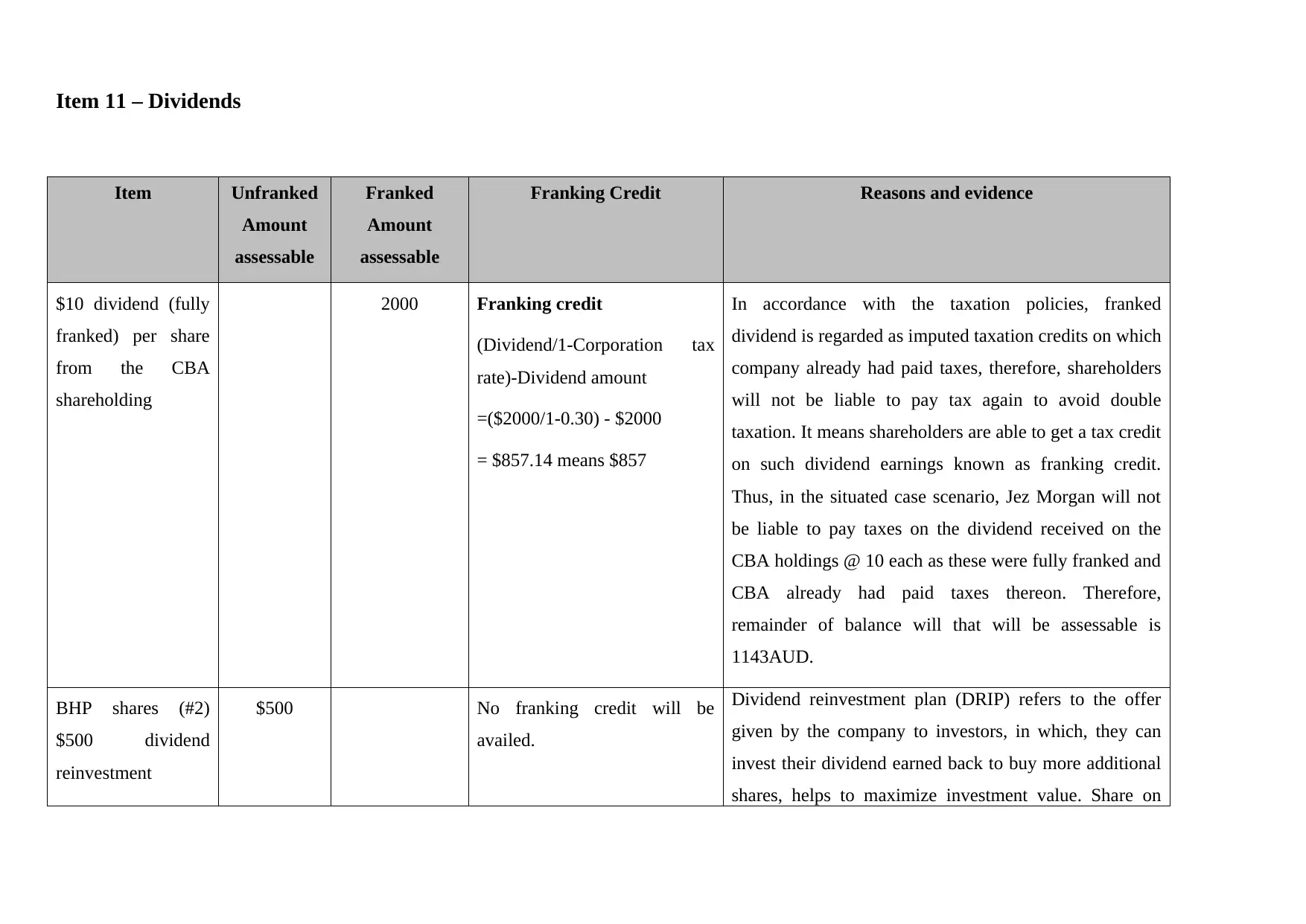

Item 11 – Dividends

Item Unfranked

Amount

assessable

Franked

Amount

assessable

Franking Credit Reasons and evidence

$10 dividend (fully

franked) per share

from the CBA

shareholding

2000 Franking credit

(Dividend/1-Corporation tax

rate)-Dividend amount

=($2000/1-0.30) - $2000

= $857.14 means $857

In accordance with the taxation policies, franked

dividend is regarded as imputed taxation credits on which

company already had paid taxes, therefore, shareholders

will not be liable to pay tax again to avoid double

taxation. It means shareholders are able to get a tax credit

on such dividend earnings known as franking credit.

Thus, in the situated case scenario, Jez Morgan will not

be liable to pay taxes on the dividend received on the

CBA holdings @ 10 each as these were fully franked and

CBA already had paid taxes thereon. Therefore,

remainder of balance will that will be assessable is

1143AUD.

BHP shares (#2)

$500 dividend

reinvestment

$500 No franking credit will be

availed.

Dividend reinvestment plan (DRIP) refers to the offer

given by the company to investors, in which, they can

invest their dividend earned back to buy more additional

shares, helps to maximize investment value. Share on

Item Unfranked

Amount

assessable

Franked

Amount

assessable

Franking Credit Reasons and evidence

$10 dividend (fully

franked) per share

from the CBA

shareholding

2000 Franking credit

(Dividend/1-Corporation tax

rate)-Dividend amount

=($2000/1-0.30) - $2000

= $857.14 means $857

In accordance with the taxation policies, franked

dividend is regarded as imputed taxation credits on which

company already had paid taxes, therefore, shareholders

will not be liable to pay tax again to avoid double

taxation. It means shareholders are able to get a tax credit

on such dividend earnings known as franking credit.

Thus, in the situated case scenario, Jez Morgan will not

be liable to pay taxes on the dividend received on the

CBA holdings @ 10 each as these were fully franked and

CBA already had paid taxes thereon. Therefore,

remainder of balance will that will be assessable is

1143AUD.

BHP shares (#2)

$500 dividend

reinvestment

$500 No franking credit will be

availed.

Dividend reinvestment plan (DRIP) refers to the offer

given by the company to investors, in which, they can

invest their dividend earned back to buy more additional

shares, helps to maximize investment value. Share on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

which company did not pay dividend is called unfranked

dividend, and on the same, no franking credit will be

available to assess (Dividend Reinvestment Plans. n.d.).

TOTAL $x 500

Label S

$x 2000

Label T

$x 857

Label U

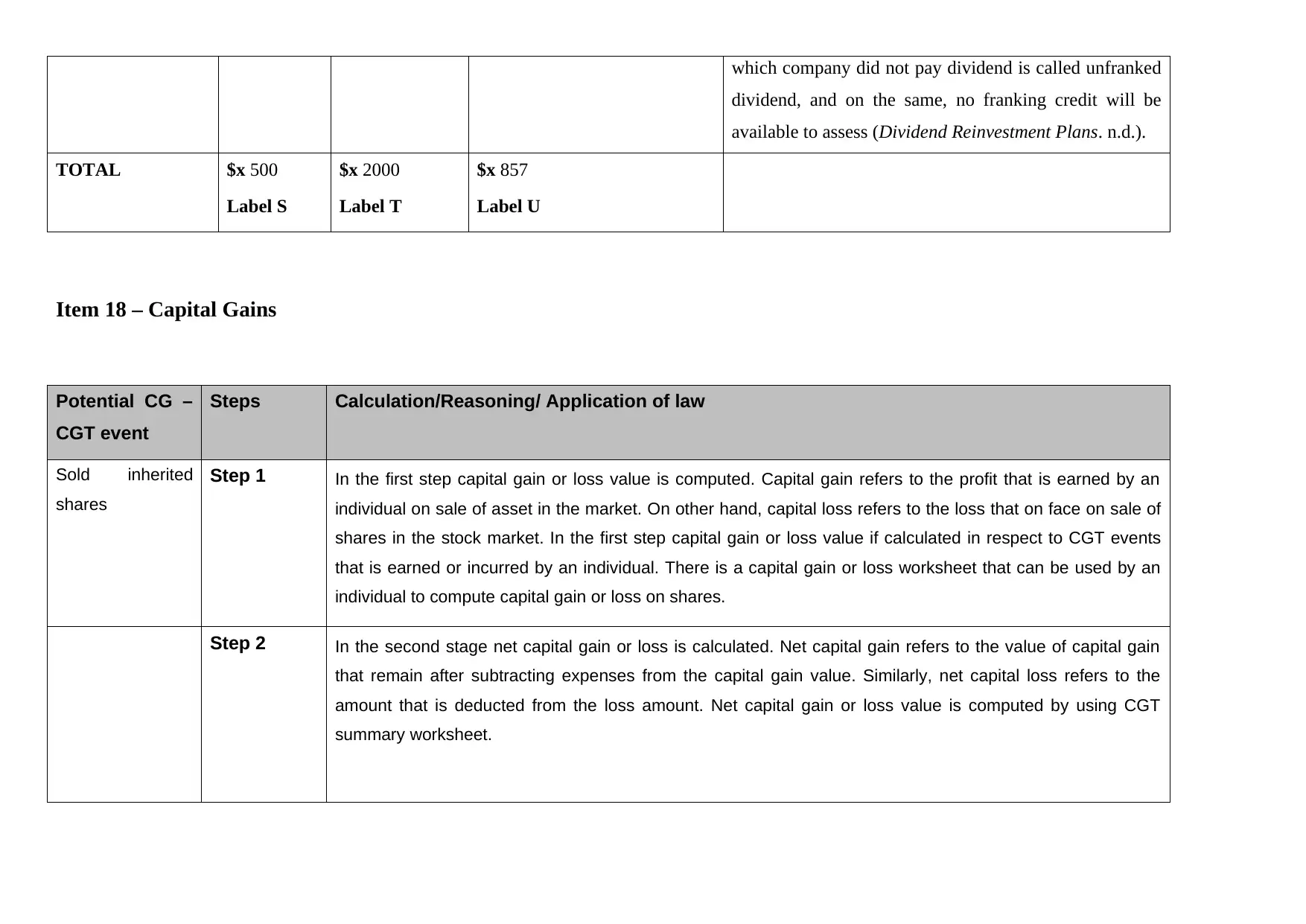

Item 18 – Capital Gains

Potential CG –

CGT event

Steps Calculation/Reasoning/ Application of law

Sold inherited

shares

Step 1 In the first step capital gain or loss value is computed. Capital gain refers to the profit that is earned by an

individual on sale of asset in the market. On other hand, capital loss refers to the loss that on face on sale of

shares in the stock market. In the first step capital gain or loss value if calculated in respect to CGT events

that is earned or incurred by an individual. There is a capital gain or loss worksheet that can be used by an

individual to compute capital gain or loss on shares.

Step 2 In the second stage net capital gain or loss is calculated. Net capital gain refers to the value of capital gain

that remain after subtracting expenses from the capital gain value. Similarly, net capital loss refers to the

amount that is deducted from the loss amount. Net capital gain or loss value is computed by using CGT

summary worksheet.

dividend, and on the same, no franking credit will be

available to assess (Dividend Reinvestment Plans. n.d.).

TOTAL $x 500

Label S

$x 2000

Label T

$x 857

Label U

Item 18 – Capital Gains

Potential CG –

CGT event

Steps Calculation/Reasoning/ Application of law

Sold inherited

shares

Step 1 In the first step capital gain or loss value is computed. Capital gain refers to the profit that is earned by an

individual on sale of asset in the market. On other hand, capital loss refers to the loss that on face on sale of

shares in the stock market. In the first step capital gain or loss value if calculated in respect to CGT events

that is earned or incurred by an individual. There is a capital gain or loss worksheet that can be used by an

individual to compute capital gain or loss on shares.

Step 2 In the second stage net capital gain or loss is calculated. Net capital gain refers to the value of capital gain

that remain after subtracting expenses from the capital gain value. Similarly, net capital loss refers to the

amount that is deducted from the loss amount. Net capital gain or loss value is computed by using CGT

summary worksheet.

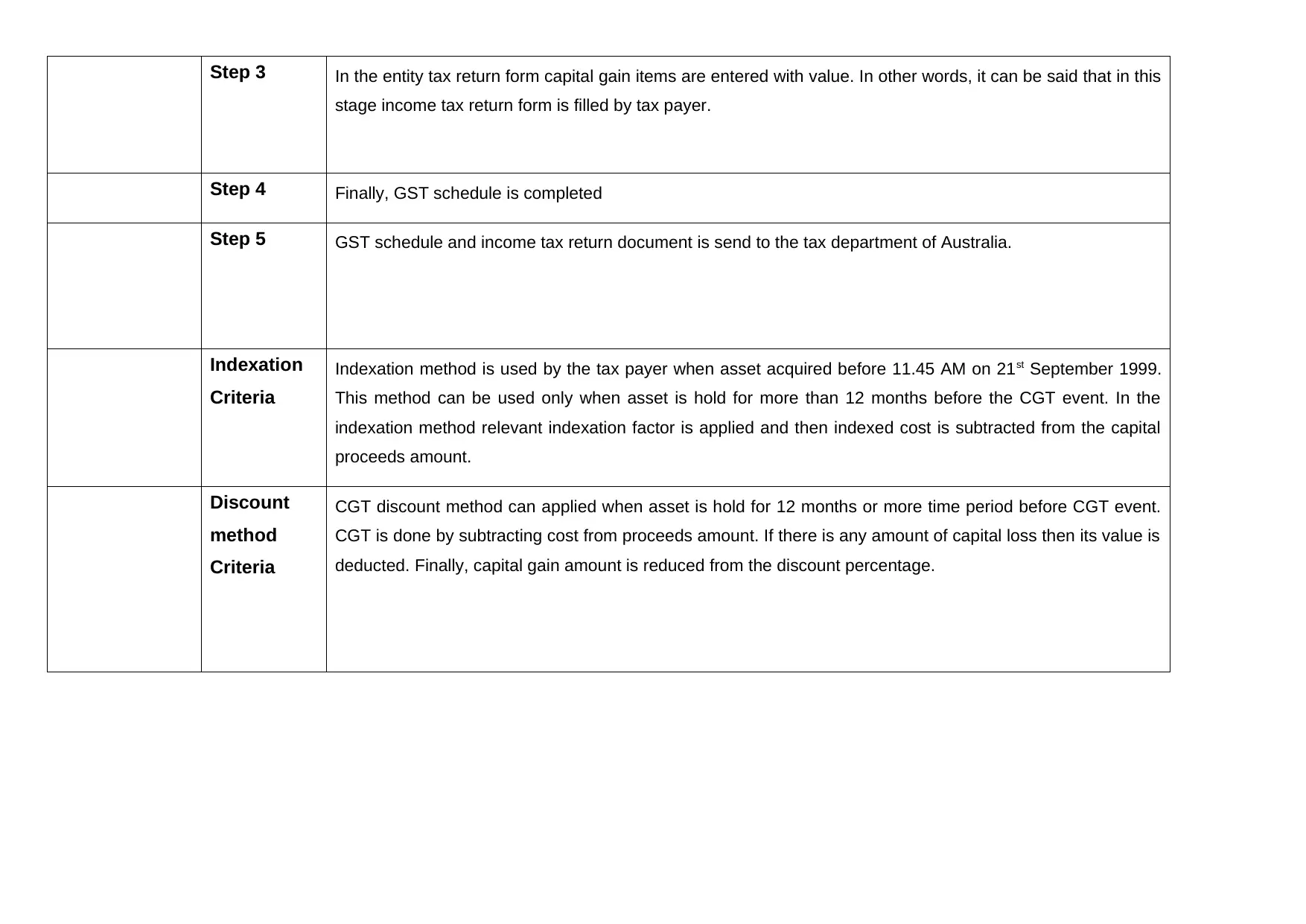

Step 3 In the entity tax return form capital gain items are entered with value. In other words, it can be said that in this

stage income tax return form is filled by tax payer.

Step 4 Finally, GST schedule is completed

Step 5 GST schedule and income tax return document is send to the tax department of Australia.

Indexation

Criteria

Indexation method is used by the tax payer when asset acquired before 11.45 AM on 21st September 1999.

This method can be used only when asset is hold for more than 12 months before the CGT event. In the

indexation method relevant indexation factor is applied and then indexed cost is subtracted from the capital

proceeds amount.

Discount

method

Criteria

CGT discount method can applied when asset is hold for 12 months or more time period before CGT event.

CGT is done by subtracting cost from proceeds amount. If there is any amount of capital loss then its value is

deducted. Finally, capital gain amount is reduced from the discount percentage.

stage income tax return form is filled by tax payer.

Step 4 Finally, GST schedule is completed

Step 5 GST schedule and income tax return document is send to the tax department of Australia.

Indexation

Criteria

Indexation method is used by the tax payer when asset acquired before 11.45 AM on 21st September 1999.

This method can be used only when asset is hold for more than 12 months before the CGT event. In the

indexation method relevant indexation factor is applied and then indexed cost is subtracted from the capital

proceeds amount.

Discount

method

Criteria

CGT discount method can applied when asset is hold for 12 months or more time period before CGT event.

CGT is done by subtracting cost from proceeds amount. If there is any amount of capital loss then its value is

deducted. Finally, capital gain amount is reduced from the discount percentage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

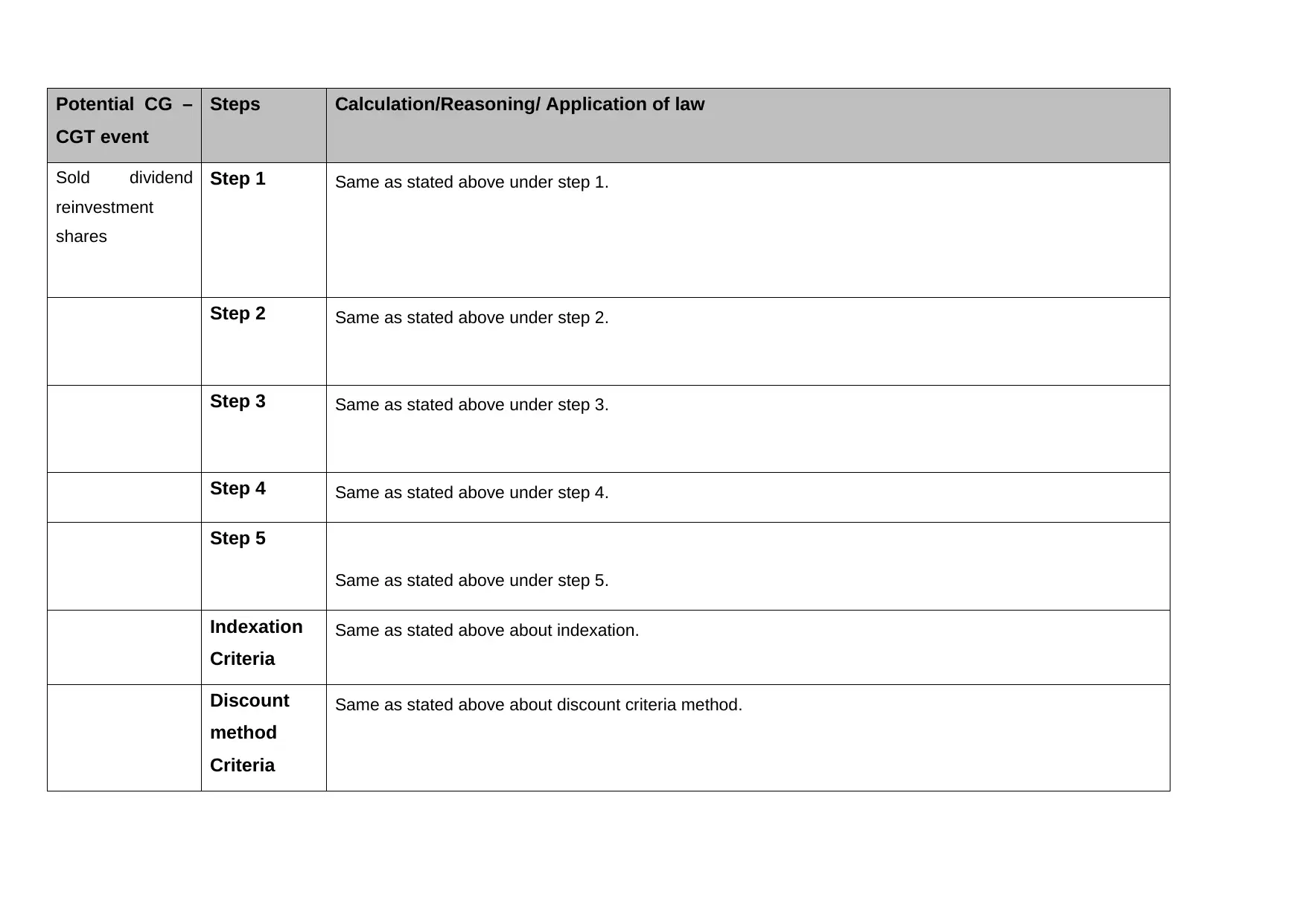

Potential CG –

CGT event

Steps Calculation/Reasoning/ Application of law

Sold dividend

reinvestment

shares

Step 1 Same as stated above under step 1.

Step 2 Same as stated above under step 2.

Step 3 Same as stated above under step 3.

Step 4 Same as stated above under step 4.

Step 5

Same as stated above under step 5.

Indexation

Criteria

Same as stated above about indexation.

Discount

method

Criteria

Same as stated above about discount criteria method.

CGT event

Steps Calculation/Reasoning/ Application of law

Sold dividend

reinvestment

shares

Step 1 Same as stated above under step 1.

Step 2 Same as stated above under step 2.

Step 3 Same as stated above under step 3.

Step 4 Same as stated above under step 4.

Step 5

Same as stated above under step 5.

Indexation

Criteria

Same as stated above about indexation.

Discount

method

Criteria

Same as stated above about discount criteria method.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

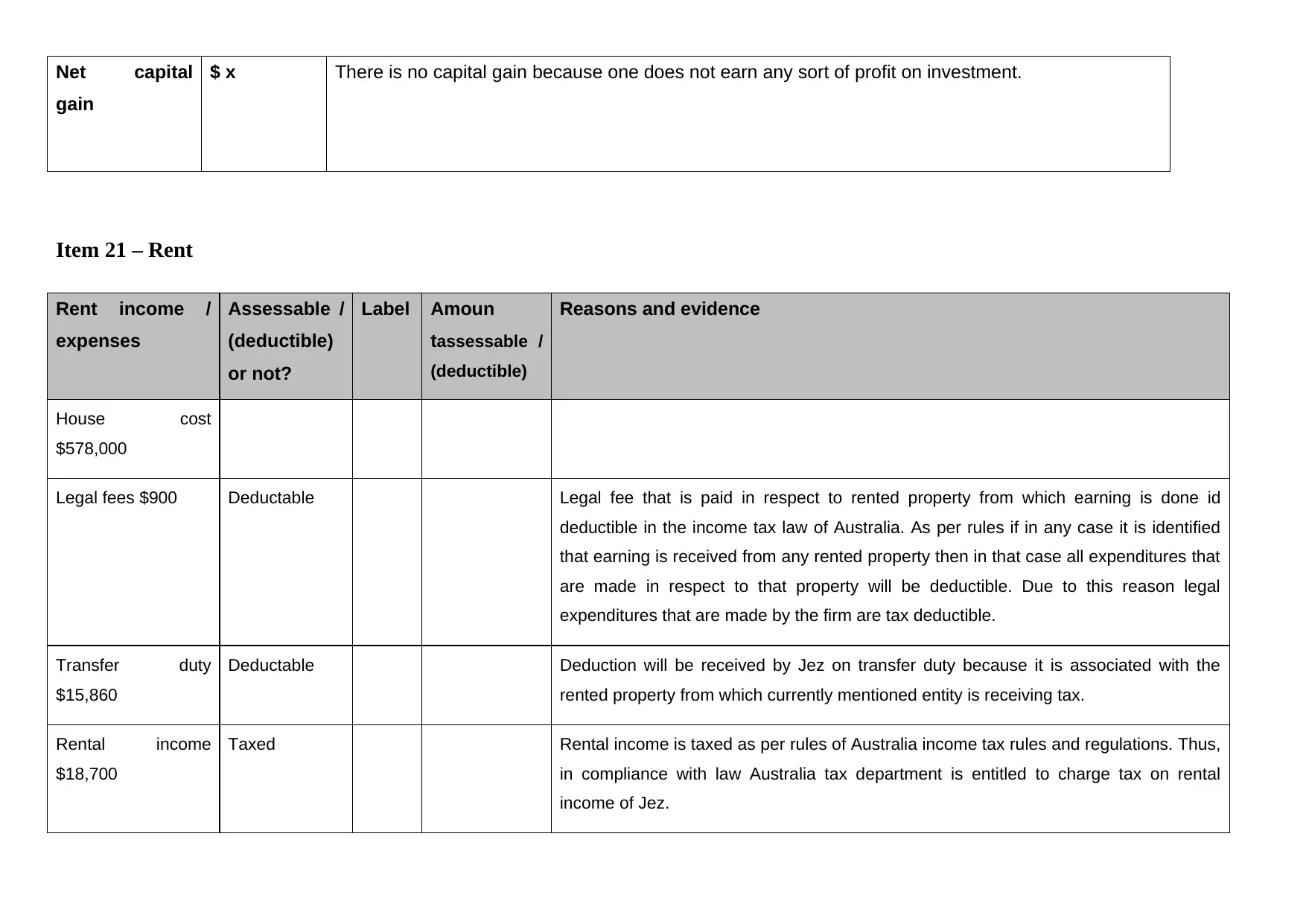

Net capital

gain

$ x There is no capital gain because one does not earn any sort of profit on investment.

Item 21 – Rent

Rent income /

expenses

Assessable /

(deductible)

or not?

Label Amoun

tassessable /

(deductible)

Reasons and evidence

House cost

$578,000

Legal fees $900 Deductable Legal fee that is paid in respect to rented property from which earning is done id

deductible in the income tax law of Australia. As per rules if in any case it is identified

that earning is received from any rented property then in that case all expenditures that

are made in respect to that property will be deductible. Due to this reason legal

expenditures that are made by the firm are tax deductible.

Transfer duty

$15,860

Deductable Deduction will be received by Jez on transfer duty because it is associated with the

rented property from which currently mentioned entity is receiving tax.

Rental income

$18,700

Taxed Rental income is taxed as per rules of Australia income tax rules and regulations. Thus,

in compliance with law Australia tax department is entitled to charge tax on rental

income of Jez.

gain

$ x There is no capital gain because one does not earn any sort of profit on investment.

Item 21 – Rent

Rent income /

expenses

Assessable /

(deductible)

or not?

Label Amoun

tassessable /

(deductible)

Reasons and evidence

House cost

$578,000

Legal fees $900 Deductable Legal fee that is paid in respect to rented property from which earning is done id

deductible in the income tax law of Australia. As per rules if in any case it is identified

that earning is received from any rented property then in that case all expenditures that

are made in respect to that property will be deductible. Due to this reason legal

expenditures that are made by the firm are tax deductible.

Transfer duty

$15,860

Deductable Deduction will be received by Jez on transfer duty because it is associated with the

rented property from which currently mentioned entity is receiving tax.

Rental income

$18,700

Taxed Rental income is taxed as per rules of Australia income tax rules and regulations. Thus,

in compliance with law Australia tax department is entitled to charge tax on rental

income of Jez.

Rent income /

expenses

Assessable /

(deductible)

or not?

Label Amoun

tassessable /

(deductible)

Reasons and evidence

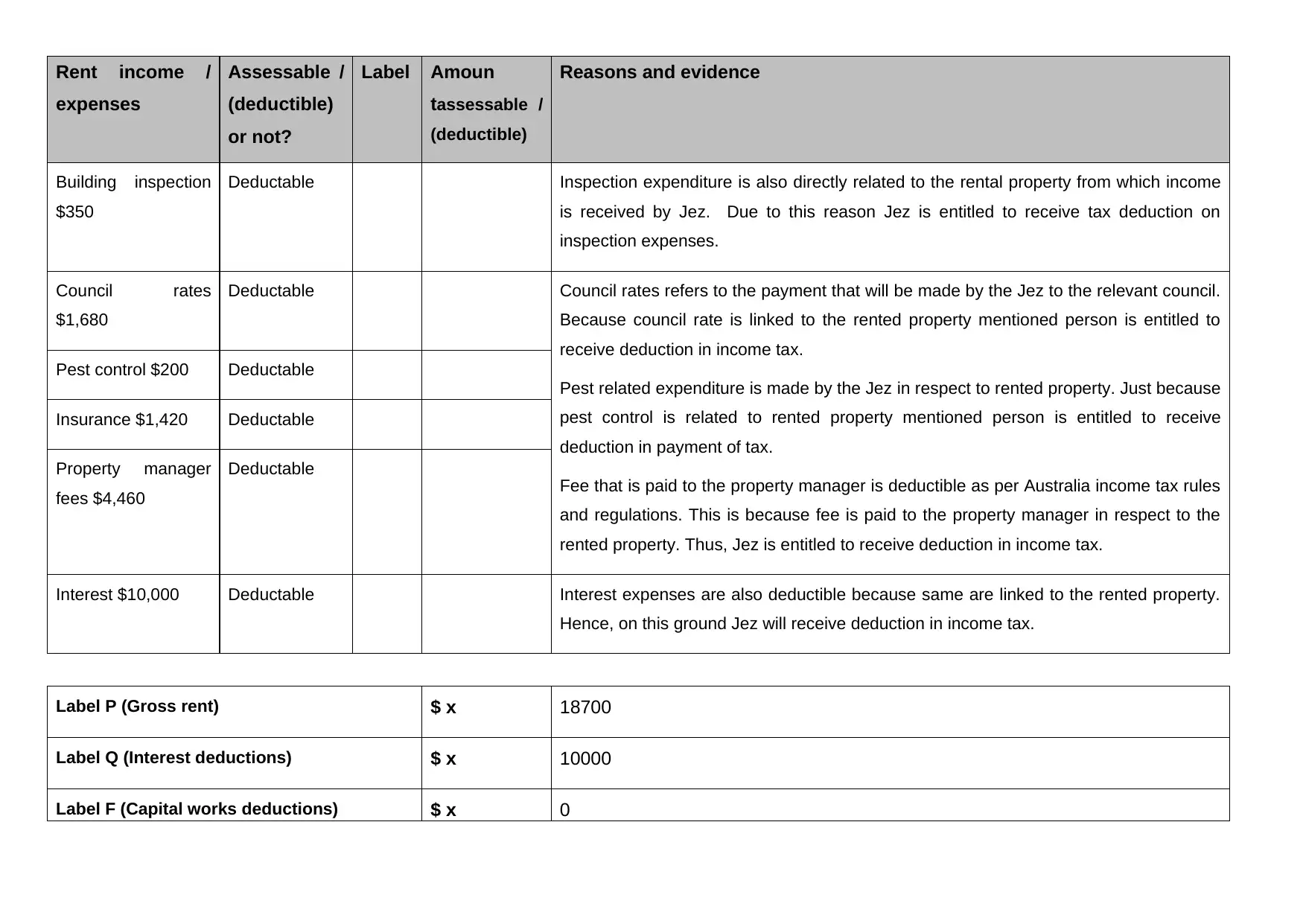

Building inspection

$350

Deductable Inspection expenditure is also directly related to the rental property from which income

is received by Jez. Due to this reason Jez is entitled to receive tax deduction on

inspection expenses.

Council rates

$1,680

Deductable Council rates refers to the payment that will be made by the Jez to the relevant council.

Because council rate is linked to the rented property mentioned person is entitled to

receive deduction in income tax.

Pest related expenditure is made by the Jez in respect to rented property. Just because

pest control is related to rented property mentioned person is entitled to receive

deduction in payment of tax.

Fee that is paid to the property manager is deductible as per Australia income tax rules

and regulations. This is because fee is paid to the property manager in respect to the

rented property. Thus, Jez is entitled to receive deduction in income tax.

Pest control $200 Deductable

Insurance $1,420 Deductable

Property manager

fees $4,460

Deductable

Interest $10,000 Deductable Interest expenses are also deductible because same are linked to the rented property.

Hence, on this ground Jez will receive deduction in income tax.

Label P (Gross rent) $ x 18700

Label Q (Interest deductions) $ x 10000

Label F (Capital works deductions) $ x 0

expenses

Assessable /

(deductible)

or not?

Label Amoun

tassessable /

(deductible)

Reasons and evidence

Building inspection

$350

Deductable Inspection expenditure is also directly related to the rental property from which income

is received by Jez. Due to this reason Jez is entitled to receive tax deduction on

inspection expenses.

Council rates

$1,680

Deductable Council rates refers to the payment that will be made by the Jez to the relevant council.

Because council rate is linked to the rented property mentioned person is entitled to

receive deduction in income tax.

Pest related expenditure is made by the Jez in respect to rented property. Just because

pest control is related to rented property mentioned person is entitled to receive

deduction in payment of tax.

Fee that is paid to the property manager is deductible as per Australia income tax rules

and regulations. This is because fee is paid to the property manager in respect to the

rented property. Thus, Jez is entitled to receive deduction in income tax.

Pest control $200 Deductable

Insurance $1,420 Deductable

Property manager

fees $4,460

Deductable

Interest $10,000 Deductable Interest expenses are also deductible because same are linked to the rented property.

Hence, on this ground Jez will receive deduction in income tax.

Label P (Gross rent) $ x 18700

Label Q (Interest deductions) $ x 10000

Label F (Capital works deductions) $ x 0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.