Corporate & Financial Accounting: JKY Limited's Takeover Consolidation

VerifiedAdded on 2023/03/31

|9

|2639

|161

Report

AI Summary

This report provides a scientific outline of various accounting types associated with JKY Limited's takeover decision of FAB Limited, focusing on consolidation and equity bookkeeping differences, intra-group transactions, and disclosures related to non-controlling interests. The consolidation method involves recording assets and liabilities based on the proportion of involvement, while the equity method recognizes income based on equity investment sums. Intra-group transactions, such as inventory sales, require elimination of unrealized profits in consolidated accounts. The report also discusses the separate reporting requirement for non-controlling interests in the consolidation process and alterations needed for accurate group financial statement depiction, referencing AASB standards for guidance. The effect of reporting requirements of developing the group financial statements is also addressed.

Running head: CORPORATE AND FINANCIAL ACCOUNTING

Corporate Takeover Decision Making and the Effects on Consolidation Accounting

Student Name:

Student Number:

Session Number:

Corporate Takeover Decision Making and the Effects on Consolidation Accounting

Student Name:

Student Number:

Session Number:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE AND FINANCIAL ACCOUNTING

Executive Summary:

The aim of this paper is to attain a scientific outline of the variety of "accounting"

types associated with the takeover decision undertaken by JKY Limited. When

subsidiary is involved in sale of goods having non-controlling interest to the group, it

is necessary to eliminate the whole unrecognised profit. This leads to a question of

whether the profit has to be disclosed in relation to non-controlling interest. Firstly,

the non-controlling costs have to be assigned to the unrealised share of profit. This

results in complete removal of the overall profit. The other approach includes no

allocation of unrealised profit to the non-controlling interests and the amount for such

interests reveals the share capital entitlement and reserves related to the subsidiary.

It could be said that the effect of reporting requirements of developing the group

financial statements.

Executive Summary:

The aim of this paper is to attain a scientific outline of the variety of "accounting"

types associated with the takeover decision undertaken by JKY Limited. When

subsidiary is involved in sale of goods having non-controlling interest to the group, it

is necessary to eliminate the whole unrecognised profit. This leads to a question of

whether the profit has to be disclosed in relation to non-controlling interest. Firstly,

the non-controlling costs have to be assigned to the unrealised share of profit. This

results in complete removal of the overall profit. The other approach includes no

allocation of unrealised profit to the non-controlling interests and the amount for such

interests reveals the share capital entitlement and reserves related to the subsidiary.

It could be said that the effect of reporting requirements of developing the group

financial statements.

2CORPORATE AND FINANCIAL ACCOUNTING

Table of Contents

Introduction:..................................................................................................................3

Part A Response:..........................................................................................................3

Part B Response:..........................................................................................................5

Part C Response:.........................................................................................................6

Conclusion:...................................................................................................................7

References:..................................................................................................................9

Table of Contents

Introduction:..................................................................................................................3

Part A Response:..........................................................................................................3

Part B Response:..........................................................................................................5

Part C Response:.........................................................................................................6

Conclusion:...................................................................................................................7

References:..................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE AND FINANCIAL ACCOUNTING

Introduction:

The aim of this paper is to attain a scientific outline of the variety of

"accounting" types associated with decision undertaken by JKY Limited to purchase

FAB Limited. The initial section of this paper would be highlighting the dissimilarities

between the technical diversities in "consolidation book-keeping" and "equity book-

keeping" with precise illustrations. The next section would be discussing the key

ideas of "intra-group transactions" and their evaluation by using treated illustrations.

On the final section, the report would provide a critical discussion on disclosures

associated with non-controlling interests as a particular item in the consolidation

method.

Part A Response:

From the provided thematic analysis, it has been identified that in order to

"acquire" "FAB Ltd", the authorities of "JKY Ltd" is in a predicament regarding the

selection of the "acquisition" plan. The system of "consolidation" and the system of

"equity" are "two" kinds of "acquisition" methodologies utilised while "two" firms are

taking part in a joint project (Balakrishnan, Watts and Zuo 2016). The selection of

any "one" of these systems is dependent on the way the "income statement" and the

"balance sheet statement" of the business "report" the "joint venture". This

appropriately states that the two techniques have significant differences between

each other in techniques, which are stated as follows:

Consolidation method of accounting:

According to this system of "accounting", "assets and liabilities" of a joint

project are recorded in the "balance sheet statement" of business depending on the

proportion of involvement the establishment maintains in the project (Lins, Servaes

and Tamayo 2017). It is necessary to consider all acquisition expenses and income

at the time of calculating assets and liabilities and there should be use of income

statement and balance sheet statement for their recognition. According to

"Paragraph B86 of AASB 10", the combined "financial statements" are connected in

such a manner that all financial statement items are included in them (Aasb.gov.au

2019). However, the combined system of accounting makes elimination

modifications with the target to nullify "inter-business transactions" so that values are

not counted twice at the level of consolidation.

"Paragraph B88 of AASB 10" conducts the calculation requirements of the

varying classes of items of the "operating statements", in it the income and costs of

the auxiliary are based on "asset and liability" amount obtained in the consolidated

statement of profit or loss at acquisition period. Hence, fair values are used for

computing such items at the period of acquisition. "Paragraph 32 of AASB 3", cites a

particular situation in terms of "goodwill" recognition. The claimer has to recognise

"goodwill" at the acquisition period as the higher of the "two" depicted below:

a. The aggregate of-

The measurement and engagement of consideration related to "AASB 3" requiring

"fair value" during the period of "acquisition".

The amount of non-controlling interest held by the organisation purchasing shares of

another organisation with adherence to the standard

Introduction:

The aim of this paper is to attain a scientific outline of the variety of

"accounting" types associated with decision undertaken by JKY Limited to purchase

FAB Limited. The initial section of this paper would be highlighting the dissimilarities

between the technical diversities in "consolidation book-keeping" and "equity book-

keeping" with precise illustrations. The next section would be discussing the key

ideas of "intra-group transactions" and their evaluation by using treated illustrations.

On the final section, the report would provide a critical discussion on disclosures

associated with non-controlling interests as a particular item in the consolidation

method.

Part A Response:

From the provided thematic analysis, it has been identified that in order to

"acquire" "FAB Ltd", the authorities of "JKY Ltd" is in a predicament regarding the

selection of the "acquisition" plan. The system of "consolidation" and the system of

"equity" are "two" kinds of "acquisition" methodologies utilised while "two" firms are

taking part in a joint project (Balakrishnan, Watts and Zuo 2016). The selection of

any "one" of these systems is dependent on the way the "income statement" and the

"balance sheet statement" of the business "report" the "joint venture". This

appropriately states that the two techniques have significant differences between

each other in techniques, which are stated as follows:

Consolidation method of accounting:

According to this system of "accounting", "assets and liabilities" of a joint

project are recorded in the "balance sheet statement" of business depending on the

proportion of involvement the establishment maintains in the project (Lins, Servaes

and Tamayo 2017). It is necessary to consider all acquisition expenses and income

at the time of calculating assets and liabilities and there should be use of income

statement and balance sheet statement for their recognition. According to

"Paragraph B86 of AASB 10", the combined "financial statements" are connected in

such a manner that all financial statement items are included in them (Aasb.gov.au

2019). However, the combined system of accounting makes elimination

modifications with the target to nullify "inter-business transactions" so that values are

not counted twice at the level of consolidation.

"Paragraph B88 of AASB 10" conducts the calculation requirements of the

varying classes of items of the "operating statements", in it the income and costs of

the auxiliary are based on "asset and liability" amount obtained in the consolidated

statement of profit or loss at acquisition period. Hence, fair values are used for

computing such items at the period of acquisition. "Paragraph 32 of AASB 3", cites a

particular situation in terms of "goodwill" recognition. The claimer has to recognise

"goodwill" at the acquisition period as the higher of the "two" depicted below:

a. The aggregate of-

The measurement and engagement of consideration related to "AASB 3" requiring

"fair value" during the period of "acquisition".

The amount of non-controlling interest held by the organisation purchasing shares of

another organisation with adherence to the standard

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

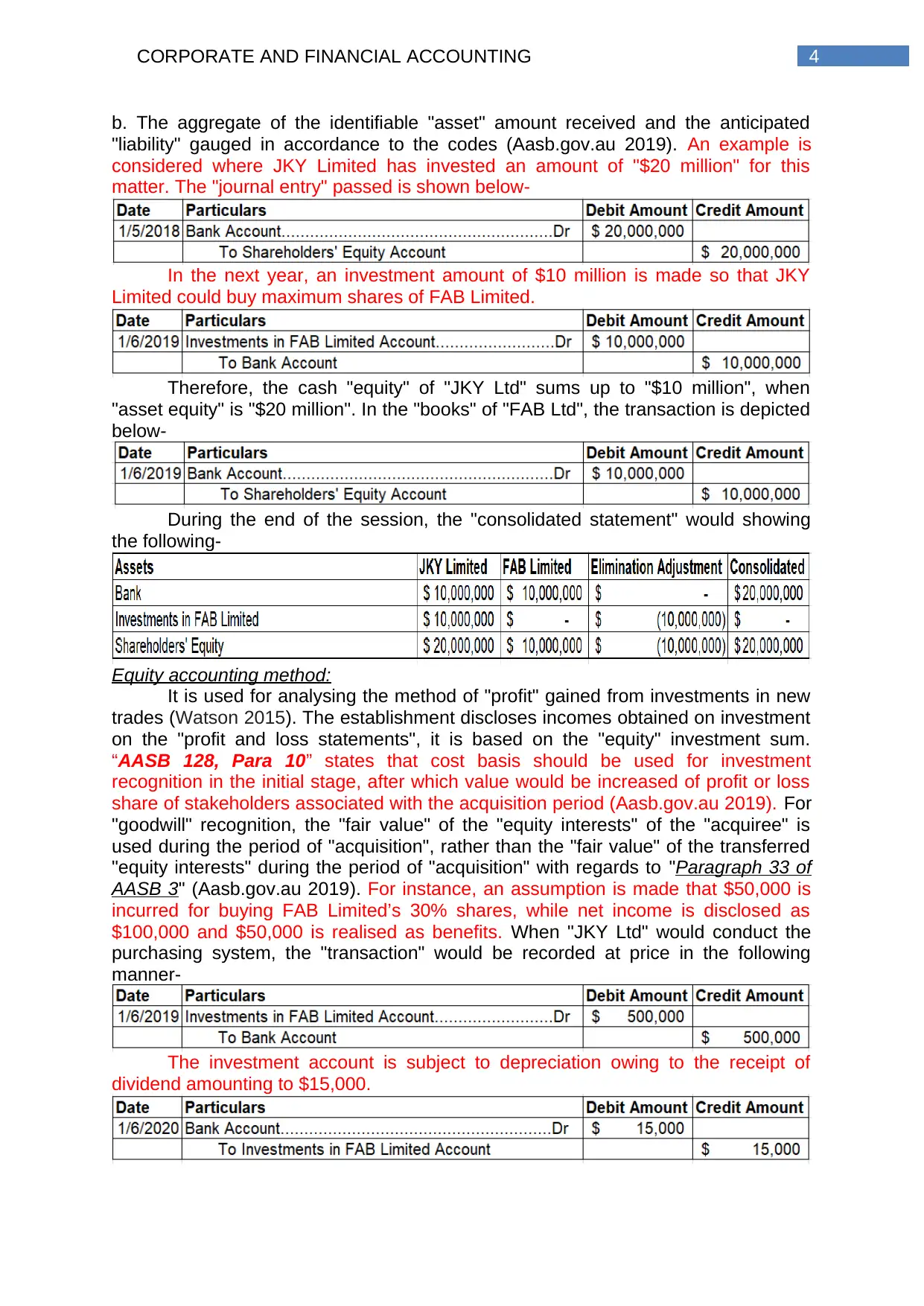

4CORPORATE AND FINANCIAL ACCOUNTING

b. The aggregate of the identifiable "asset" amount received and the anticipated

"liability" gauged in accordance to the codes (Aasb.gov.au 2019). An example is

considered where JKY Limited has invested an amount of "$20 million" for this

matter. The "journal entry" passed is shown below-

In the next year, an investment amount of $10 million is made so that JKY

Limited could buy maximum shares of FAB Limited.

Therefore, the cash "equity" of "JKY Ltd" sums up to "$10 million", when

"asset equity" is "$20 million". In the "books" of "FAB Ltd", the transaction is depicted

below-

During the end of the session, the "consolidated statement" would showing

the following-

Equity accounting method:

It is used for analysing the method of "profit" gained from investments in new

trades (Watson 2015). The establishment discloses incomes obtained on investment

on the "profit and loss statements", it is based on the "equity" investment sum.

“AASB 128, Para 10” states that cost basis should be used for investment

recognition in the initial stage, after which value would be increased of profit or loss

share of stakeholders associated with the acquisition period (Aasb.gov.au 2019). For

"goodwill" recognition, the "fair value" of the "equity interests" of the "acquiree" is

used during the period of "acquisition", rather than the "fair value" of the transferred

"equity interests" during the period of "acquisition" with regards to "Paragraph 33 of

AASB 3" (Aasb.gov.au 2019). For instance, an assumption is made that $50,000 is

incurred for buying FAB Limited’s 30% shares, while net income is disclosed as

$100,000 and $50,000 is realised as benefits. When "JKY Ltd" would conduct the

purchasing system, the "transaction" would be recorded at price in the following

manner-

The investment account is subject to depreciation owing to the receipt of

dividend amounting to $15,000.

b. The aggregate of the identifiable "asset" amount received and the anticipated

"liability" gauged in accordance to the codes (Aasb.gov.au 2019). An example is

considered where JKY Limited has invested an amount of "$20 million" for this

matter. The "journal entry" passed is shown below-

In the next year, an investment amount of $10 million is made so that JKY

Limited could buy maximum shares of FAB Limited.

Therefore, the cash "equity" of "JKY Ltd" sums up to "$10 million", when

"asset equity" is "$20 million". In the "books" of "FAB Ltd", the transaction is depicted

below-

During the end of the session, the "consolidated statement" would showing

the following-

Equity accounting method:

It is used for analysing the method of "profit" gained from investments in new

trades (Watson 2015). The establishment discloses incomes obtained on investment

on the "profit and loss statements", it is based on the "equity" investment sum.

“AASB 128, Para 10” states that cost basis should be used for investment

recognition in the initial stage, after which value would be increased of profit or loss

share of stakeholders associated with the acquisition period (Aasb.gov.au 2019). For

"goodwill" recognition, the "fair value" of the "equity interests" of the "acquiree" is

used during the period of "acquisition", rather than the "fair value" of the transferred

"equity interests" during the period of "acquisition" with regards to "Paragraph 33 of

AASB 3" (Aasb.gov.au 2019). For instance, an assumption is made that $50,000 is

incurred for buying FAB Limited’s 30% shares, while net income is disclosed as

$100,000 and $50,000 is realised as benefits. When "JKY Ltd" would conduct the

purchasing system, the "transaction" would be recorded at price in the following

manner-

The investment account is subject to depreciation owing to the receipt of

dividend amounting to $15,000.

5CORPORATE AND FINANCIAL ACCOUNTING

Finally, "JKY Ltd" would record the aggregate of "profit" of "FAB Ltd" as a

raise to the "investment account".

Part B Response:

At the time of "financial session", it is natural for a certain legal units within an

"economic" establishment for "transacting" with one another. So, to create

"consolidated accounts", the impact of all the "transactions" between the units within

the establishment is eradicated fully, even at the time the "parent" firm retains only a

part of the "issued equity" (Crowther 2018). As per "Paragraph 29 of AASB 127"

requires "intra-group equities", "transactions", costs and receivables to be eradicated

completely (Legislation.gov.au 2019). A few illustrations of "intra-group transactions"

considerably include the following-

Disbursement of management charges to a representative of the "group".

Disbursement of dividends to members of the "group".

Inventory selling to "intra-group".

"Intra-group" "non-current asset" sells.

Loans to "intra-groups".

The "consolidation" alterations incorporated with "intra-group" "transactions"

eliminates this kind of "transactions" through annulments of the actual "book-

keeping" entries made for recognition of the "transactions" in particular legal

establishments (Kothari 2019).

Based on the provided information, it could be witnessed that there has been

inventory purchase by JKY Limited from a subsidiary. Based on the group

perspective, revenue could not be recognised until inventory is sold to the other

parties. Hence, the profits that are not realised have to be removed from the

consolidated accounts. The sale of inventory results in unrecognised profit within the

group held at the end of the year. As per “AASB 127, Para 5”, the losses or gains

obtained from transactions within the group that are realised in inventories and non-

current assets have to be removed fully (Kothari 2019).

In the given case, the subsidiary has disposed off a part of its inventory to

JKY Limited, which includes a mark-up in cost. At the time JKY Limited is involved in

selling inventories to the other parties, no issues would occur when it comes to the

transaction point of the group. However, until the time inventory is sold to the outside

customers, the profit made by the subsidiary would be classified as unrealised

resulting in undue increase in group profit. Hence, the unrecognised profit has to be

eliminated fully. If it assumed that inventory was purchased by JKY Limited from a

subsidiary valuing $10,000 with 25% mark-up, gain on inventory would be $2,000.

This would lead to overstated consolidated profit by $2,00, which needs to be

adjusted by passing the entry below:

Dr Consolidated Profit $2,000

Cr Consolidated Inventory $2,000

When subsidiary is involved in sale of goods having non-controlling interest to

the group, it is necessary to eliminate the whole unrecognised profit. This leads to a

question of whether the profit has to be disclosed in relation to non-controlling

interest. Firstly, the non-controlling costs have to be assigned to the unrealised share

Finally, "JKY Ltd" would record the aggregate of "profit" of "FAB Ltd" as a

raise to the "investment account".

Part B Response:

At the time of "financial session", it is natural for a certain legal units within an

"economic" establishment for "transacting" with one another. So, to create

"consolidated accounts", the impact of all the "transactions" between the units within

the establishment is eradicated fully, even at the time the "parent" firm retains only a

part of the "issued equity" (Crowther 2018). As per "Paragraph 29 of AASB 127"

requires "intra-group equities", "transactions", costs and receivables to be eradicated

completely (Legislation.gov.au 2019). A few illustrations of "intra-group transactions"

considerably include the following-

Disbursement of management charges to a representative of the "group".

Disbursement of dividends to members of the "group".

Inventory selling to "intra-group".

"Intra-group" "non-current asset" sells.

Loans to "intra-groups".

The "consolidation" alterations incorporated with "intra-group" "transactions"

eliminates this kind of "transactions" through annulments of the actual "book-

keeping" entries made for recognition of the "transactions" in particular legal

establishments (Kothari 2019).

Based on the provided information, it could be witnessed that there has been

inventory purchase by JKY Limited from a subsidiary. Based on the group

perspective, revenue could not be recognised until inventory is sold to the other

parties. Hence, the profits that are not realised have to be removed from the

consolidated accounts. The sale of inventory results in unrecognised profit within the

group held at the end of the year. As per “AASB 127, Para 5”, the losses or gains

obtained from transactions within the group that are realised in inventories and non-

current assets have to be removed fully (Kothari 2019).

In the given case, the subsidiary has disposed off a part of its inventory to

JKY Limited, which includes a mark-up in cost. At the time JKY Limited is involved in

selling inventories to the other parties, no issues would occur when it comes to the

transaction point of the group. However, until the time inventory is sold to the outside

customers, the profit made by the subsidiary would be classified as unrealised

resulting in undue increase in group profit. Hence, the unrecognised profit has to be

eliminated fully. If it assumed that inventory was purchased by JKY Limited from a

subsidiary valuing $10,000 with 25% mark-up, gain on inventory would be $2,000.

This would lead to overstated consolidated profit by $2,00, which needs to be

adjusted by passing the entry below:

Dr Consolidated Profit $2,000

Cr Consolidated Inventory $2,000

When subsidiary is involved in sale of goods having non-controlling interest to

the group, it is necessary to eliminate the whole unrecognised profit. This leads to a

question of whether the profit has to be disclosed in relation to non-controlling

interest. Firstly, the non-controlling costs have to be assigned to the unrealised share

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE AND FINANCIAL ACCOUNTING

of profit. This results in complete removal of the overall profit. The other approach

includes no allocation of unrealised profit to the non-controlling interests and the

amount for such interests reveals the share capital entitlement and reserves related

to the subsidiary (Kothari 2019).

An example is considered where interest of JKY Limited is 80% in A and 75%

in B. A has sold products valuing $70,000 in lieu of $100,000 to B and B has

managed to sell only 50% of the products. During the development of the group

financial statements, the elimination of unrealised inventory profit is necessary. Profit

is transferred to B at $50,000 and the cost of the group would be $35,000. As a

result, intra-group profit requires elimination of inventory by $15,000. In case of the

application of the first method, as JKY Limited has only 20% non-controlling interest,

the total amount would stand at $3,000, which is obtained by multiplying $15,000

with 20%.

Part C Response:

NCI reporting requirement in the form of separate item in the consolidation

process:

As per “AASB 127, Para 6”, non-controlling interests have to be developed

separately from the equity of the parent entity in the balance sheet (Aasb.gov.au

2019). A part of equity in the subsidiary is non-controlling interest and the attribution

could not be made to the parent, be it direct or indirect. The standard has helped in

enhanced reporting and accounting in relation to non-controlling interest in the

financial reports. The consolidation process requires separate reporting of non-

controlling interest, as the shareholders’ equity have to be reconciled for highlighting

the modifications made in the parent and non-controlling interest, which is specifies

in “AASB 101, Para 106 (a)”. The distinct non-controlling interest value has to be

labelled and identified distinctively so that excess clarifications could be provided to

the shareholders of the parent, as they have claims on the net assets. In addition,

fair representation is made at the time any subsidiary has either direct or indirect NCI

(Kothari 2019).

The equity transactions are identified as the alterations in ownership interest

of the parent entity in any subsidiary that does not happen if the subsidiary is no

more controlled by the parent. When there are alterations in the equity portion held

by non-controlling interest, adjustments are necessary for the relative interest of the

subsidiary in the carrying amounts of controlling as well as non-controlling interests.

There has to be direct realisation of the fair value related to payment for

consideration and adjustments pertaining to non-controlling interest and therefore,

the group shareholders are attributed to them (Kothari 2019).

Alterations required assuring correct depiction of the group financial

statements:

To assure that the consolidated financial statements are presented

accurately, AASB 101 has specified different changes, The group financial

statements are not needed to be prepared at the identical reporting date and it is

necessary to carry out adjustments to represent the impact on major transactions or

events taking place between the subsidiary dates and the financial statements of the

group.

The losses from impairment of the related assets need to be recognised,

which could be detected from the losses within the group. Besides, intra-group

transactions, expenses, income and balances require elimination. The financial

of profit. This results in complete removal of the overall profit. The other approach

includes no allocation of unrealised profit to the non-controlling interests and the

amount for such interests reveals the share capital entitlement and reserves related

to the subsidiary (Kothari 2019).

An example is considered where interest of JKY Limited is 80% in A and 75%

in B. A has sold products valuing $70,000 in lieu of $100,000 to B and B has

managed to sell only 50% of the products. During the development of the group

financial statements, the elimination of unrealised inventory profit is necessary. Profit

is transferred to B at $50,000 and the cost of the group would be $35,000. As a

result, intra-group profit requires elimination of inventory by $15,000. In case of the

application of the first method, as JKY Limited has only 20% non-controlling interest,

the total amount would stand at $3,000, which is obtained by multiplying $15,000

with 20%.

Part C Response:

NCI reporting requirement in the form of separate item in the consolidation

process:

As per “AASB 127, Para 6”, non-controlling interests have to be developed

separately from the equity of the parent entity in the balance sheet (Aasb.gov.au

2019). A part of equity in the subsidiary is non-controlling interest and the attribution

could not be made to the parent, be it direct or indirect. The standard has helped in

enhanced reporting and accounting in relation to non-controlling interest in the

financial reports. The consolidation process requires separate reporting of non-

controlling interest, as the shareholders’ equity have to be reconciled for highlighting

the modifications made in the parent and non-controlling interest, which is specifies

in “AASB 101, Para 106 (a)”. The distinct non-controlling interest value has to be

labelled and identified distinctively so that excess clarifications could be provided to

the shareholders of the parent, as they have claims on the net assets. In addition,

fair representation is made at the time any subsidiary has either direct or indirect NCI

(Kothari 2019).

The equity transactions are identified as the alterations in ownership interest

of the parent entity in any subsidiary that does not happen if the subsidiary is no

more controlled by the parent. When there are alterations in the equity portion held

by non-controlling interest, adjustments are necessary for the relative interest of the

subsidiary in the carrying amounts of controlling as well as non-controlling interests.

There has to be direct realisation of the fair value related to payment for

consideration and adjustments pertaining to non-controlling interest and therefore,

the group shareholders are attributed to them (Kothari 2019).

Alterations required assuring correct depiction of the group financial

statements:

To assure that the consolidated financial statements are presented

accurately, AASB 101 has specified different changes, The group financial

statements are not needed to be prepared at the identical reporting date and it is

necessary to carry out adjustments to represent the impact on major transactions or

events taking place between the subsidiary dates and the financial statements of the

group.

The losses from impairment of the related assets need to be recognised,

which could be detected from the losses within the group. Besides, intra-group

transactions, expenses, income and balances require elimination. The financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE AND FINANCIAL ACCOUNTING

statements of the group have to take into account various cash flow items, assets,

expenses and liabilities of the parent entity and its subsidiaries. It is crucial to ensure

that the group accounting policies need to be uniform for undertaking appropriate

adjustments to the financial reports of the group member when preparing the group

financial statements in a situation that any group member uses varying accounting

policies for different transactions (Kothari 2019).

The total comprehensive income has to be attributed to the parent

management along with non-controlling interest despite any chance of the treatment

to result in negative balance pertaining to non-controlling interest. Impact of the

mandatory alternations on reporting requirements in the annual report:

“AASB 127, Para 10” states that at the time separate financial reports are

prepared by an entity, investments have to be accounted for incurred in joint

ventures, subsidiaries and associates either as per AASB 9 or at cost (Aasb.gov.au

2019). This allows the scope of relaxation for the consolidated financial reports.

Hence, it is necessary to mention the degree and nature of any significant

drawbacks owing to the regulation requirements on the subsidiary’s ability to transfer

to the parent either through advances, loan repayment and cash dividends (Kothari

2019).

Moreover, when the group financial statements are prepared, the statements

of the subsidiaries are needed at the end of the reporting year and if there is

difference in the date of reporting between the parent firm and the subsidiaries, there

have to be pertinent disclosures of the same. Besides, if the voting rights of the

parent are below 50%, it is essential to report the same explaining the sort of

association between the two firms. Therefore, it could be said that the effect of

reporting requirements of developing the group financial statements.

Conclusion:

Based on the above analysis, it could be cited that For "goodwill" recognition,

the "fair value" of the "equity interests" of the "acquiree" is used during the period of

"acquisition", rather than the "fair value" of the transferred "equity interests" during

the period of "acquisition" with regards to "Paragraph 33 of AASB 3". When

subsidiary is involved in sale of goods having non-controlling interest to the group, it

is necessary to eliminate the whole unrecognised profit. This leads to a question of

whether the profit has to be disclosed in relation to non-controlling interest. Firstly,

the non-controlling costs have to be assigned to the unrealised share of profit. This

results in complete removal of the overall profit. The other approach includes no

allocation of unrealised profit to the non-controlling interests and the amount for such

interests reveals the share capital entitlement and reserves related to the subsidiary.

It could be said that the effect of reporting requirements of developing the group

financial statements.

statements of the group have to take into account various cash flow items, assets,

expenses and liabilities of the parent entity and its subsidiaries. It is crucial to ensure

that the group accounting policies need to be uniform for undertaking appropriate

adjustments to the financial reports of the group member when preparing the group

financial statements in a situation that any group member uses varying accounting

policies for different transactions (Kothari 2019).

The total comprehensive income has to be attributed to the parent

management along with non-controlling interest despite any chance of the treatment

to result in negative balance pertaining to non-controlling interest. Impact of the

mandatory alternations on reporting requirements in the annual report:

“AASB 127, Para 10” states that at the time separate financial reports are

prepared by an entity, investments have to be accounted for incurred in joint

ventures, subsidiaries and associates either as per AASB 9 or at cost (Aasb.gov.au

2019). This allows the scope of relaxation for the consolidated financial reports.

Hence, it is necessary to mention the degree and nature of any significant

drawbacks owing to the regulation requirements on the subsidiary’s ability to transfer

to the parent either through advances, loan repayment and cash dividends (Kothari

2019).

Moreover, when the group financial statements are prepared, the statements

of the subsidiaries are needed at the end of the reporting year and if there is

difference in the date of reporting between the parent firm and the subsidiaries, there

have to be pertinent disclosures of the same. Besides, if the voting rights of the

parent are below 50%, it is essential to report the same explaining the sort of

association between the two firms. Therefore, it could be said that the effect of

reporting requirements of developing the group financial statements.

Conclusion:

Based on the above analysis, it could be cited that For "goodwill" recognition,

the "fair value" of the "equity interests" of the "acquiree" is used during the period of

"acquisition", rather than the "fair value" of the transferred "equity interests" during

the period of "acquisition" with regards to "Paragraph 33 of AASB 3". When

subsidiary is involved in sale of goods having non-controlling interest to the group, it

is necessary to eliminate the whole unrecognised profit. This leads to a question of

whether the profit has to be disclosed in relation to non-controlling interest. Firstly,

the non-controlling costs have to be assigned to the unrealised share of profit. This

results in complete removal of the overall profit. The other approach includes no

allocation of unrealised profit to the non-controlling interests and the amount for such

interests reveals the share capital entitlement and reserves related to the subsidiary.

It could be said that the effect of reporting requirements of developing the group

financial statements.

8CORPORATE AND FINANCIAL ACCOUNTING

References:

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Legislation.gov.au., 2019. AASB 127 - Consolidated and Separate Financial

Statements - July 2004. [online] Available at:

https://www.legislation.gov.au/Details/F2009C01112 [Accessed 4 May 2019].

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism

on corporate investment during the global financial crisis. Journal of Business

Finance & Accounting, 43(5-6), pp.513-542.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting. Routledge.

Kothari, S.P., 2019. Accounting Information in Corporate Governance: Implications

for Standard Setting. The Accounting Review, 94(2), pp.357-361.

Lins, K.V., Servaes, H. and Tamayo, A., 2017. Social capital, trust, and firm

performance: The value of corporate social responsibility during the financial

crisis. The Journal of Finance, 72(4), pp.1785-1824.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

References:

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB3_08-15.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB128_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB10_08-11.pdf [Accessed 3

May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB127_08-

11_COMPjan15_07-15.pdf [Accessed 3 May 2019].

Aasb.gov.au., 2019. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB101_07-15.pdf [Accessed 3

May 2019].

Legislation.gov.au., 2019. AASB 127 - Consolidated and Separate Financial

Statements - July 2004. [online] Available at:

https://www.legislation.gov.au/Details/F2009C01112 [Accessed 4 May 2019].

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism

on corporate investment during the global financial crisis. Journal of Business

Finance & Accounting, 43(5-6), pp.513-542.

Crowther, D., 2018. A Social Critique of Corporate Reporting: A Semiotic Analysis of

Corporate Financial and Environmental Reporting: A Semiotic Analysis of Corporate

Financial and Environmental Reporting. Routledge.

Kothari, S.P., 2019. Accounting Information in Corporate Governance: Implications

for Standard Setting. The Accounting Review, 94(2), pp.357-361.

Lins, K.V., Servaes, H. and Tamayo, A., 2017. Social capital, trust, and firm

performance: The value of corporate social responsibility during the financial

crisis. The Journal of Finance, 72(4), pp.1785-1824.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.