ACC200 Project: Connectta Ltd Job Costing System and Overhead Analysis

VerifiedAdded on 2020/10/05

|9

|2463

|188

Project

AI Summary

This project, focusing on ACC200, provides a comprehensive analysis of job costing systems, using Connectta Ltd as a case study. The assignment begins by explaining the appropriateness of job costing for the company, which manufactures computer workstations. It then calculates the work-in-process inventory, determines the cost of finished chairs, and calculates over/under applied overheads. The project delves into the alternative accounting treatments for over-applied and under-applied overhead balances, and finally, explains the importance of activity-based costing in overcoming the limitations of traditional costing systems. The project covers key aspects of cost accounting, including inventory valuation, overhead allocation, and the application of different costing methodologies.

ACC200:

Project

Project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Job costing system records the cost associated with the particular job and it assist in

allocating the cost to the products manufactured by the organisation. This assignment will

include the information regarding the job costing system and it will assist in calculating the work

in progress inventory. Moreover, it will include the information regarding the machine hours. It

will also provide the information regarding the alternative accounting treatment for over applied

and under applied balances when using the job costing system. This assignment will include the

use of the two accounting treatment for the over or under applied overhead. In this case study, it

has provided information regarding Connectta ltd manufactures for computer work stations. This

firm uses the job costing system.

1. Appropriateness of the company to use job cost system

Job costing involves the accumulation of the cost of materials, labor and overhead for a

specific job. The job costing system involves the use of activities such as material, labor,

overhead. The job costing system assist the organisation in identifying the work in process

inventory on the basis of specific job. In the job costing system, the product cost is assigned to

each job. It is appropriate for the companies to use job cost system when they are able to identify

the separate products (Altbach, 2015). The company which is performing its services and

provide the products as per the needs of the customers than they are required to use the job

costing system. As per the job costing system, the cost are first recorded in the work in progress

then they are transferred to the finished goods inventory and after that when the products is being

sold than the cost is being recorded in the income statement as cost of goods sold.

The job costing system can be used by the construction company, manufacturing

company in which the products are being related to the specific job as per the demands of the

customer. Job costing system is assist in identifying the cost of the product by allocating the cost

to specific job regarding the direct material, labour, overhead etc. (Laudon and Laudon, 2016.).

The job costing system is specifically used by those companies which are required to perform the

different job and at the end of the years the profitability is calculated by considering all the jobs

which are being performed by the organisation. The job costing system is useful for those

companies which require to perform their job as per the demand and needs of the customers. The

job costing system involves the use of allocating the cost of material, labour and overhead which

is relate to the specific job in order to determine the profitability associated with each job.

1

Job costing system records the cost associated with the particular job and it assist in

allocating the cost to the products manufactured by the organisation. This assignment will

include the information regarding the job costing system and it will assist in calculating the work

in progress inventory. Moreover, it will include the information regarding the machine hours. It

will also provide the information regarding the alternative accounting treatment for over applied

and under applied balances when using the job costing system. This assignment will include the

use of the two accounting treatment for the over or under applied overhead. In this case study, it

has provided information regarding Connectta ltd manufactures for computer work stations. This

firm uses the job costing system.

1. Appropriateness of the company to use job cost system

Job costing involves the accumulation of the cost of materials, labor and overhead for a

specific job. The job costing system involves the use of activities such as material, labor,

overhead. The job costing system assist the organisation in identifying the work in process

inventory on the basis of specific job. In the job costing system, the product cost is assigned to

each job. It is appropriate for the companies to use job cost system when they are able to identify

the separate products (Altbach, 2015). The company which is performing its services and

provide the products as per the needs of the customers than they are required to use the job

costing system. As per the job costing system, the cost are first recorded in the work in progress

then they are transferred to the finished goods inventory and after that when the products is being

sold than the cost is being recorded in the income statement as cost of goods sold.

The job costing system can be used by the construction company, manufacturing

company in which the products are being related to the specific job as per the demands of the

customer. Job costing system is assist in identifying the cost of the product by allocating the cost

to specific job regarding the direct material, labour, overhead etc. (Laudon and Laudon, 2016.).

The job costing system is specifically used by those companies which are required to perform the

different job and at the end of the years the profitability is calculated by considering all the jobs

which are being performed by the organisation. The job costing system is useful for those

companies which require to perform their job as per the demand and needs of the customers. The

job costing system involves the use of allocating the cost of material, labour and overhead which

is relate to the specific job in order to determine the profitability associated with each job.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Connectta Ltd uses the job costing system because it is appropriate as this firm is involved in

manufacturing business and have to perform the different jobs as per the needs of the customers.

In this regard, it can be analysed that job costing is an essential costing system for those

business units that produced more than one type of products. Further, it is also useful for those

companies that produces customised products as per the needs of the customers.

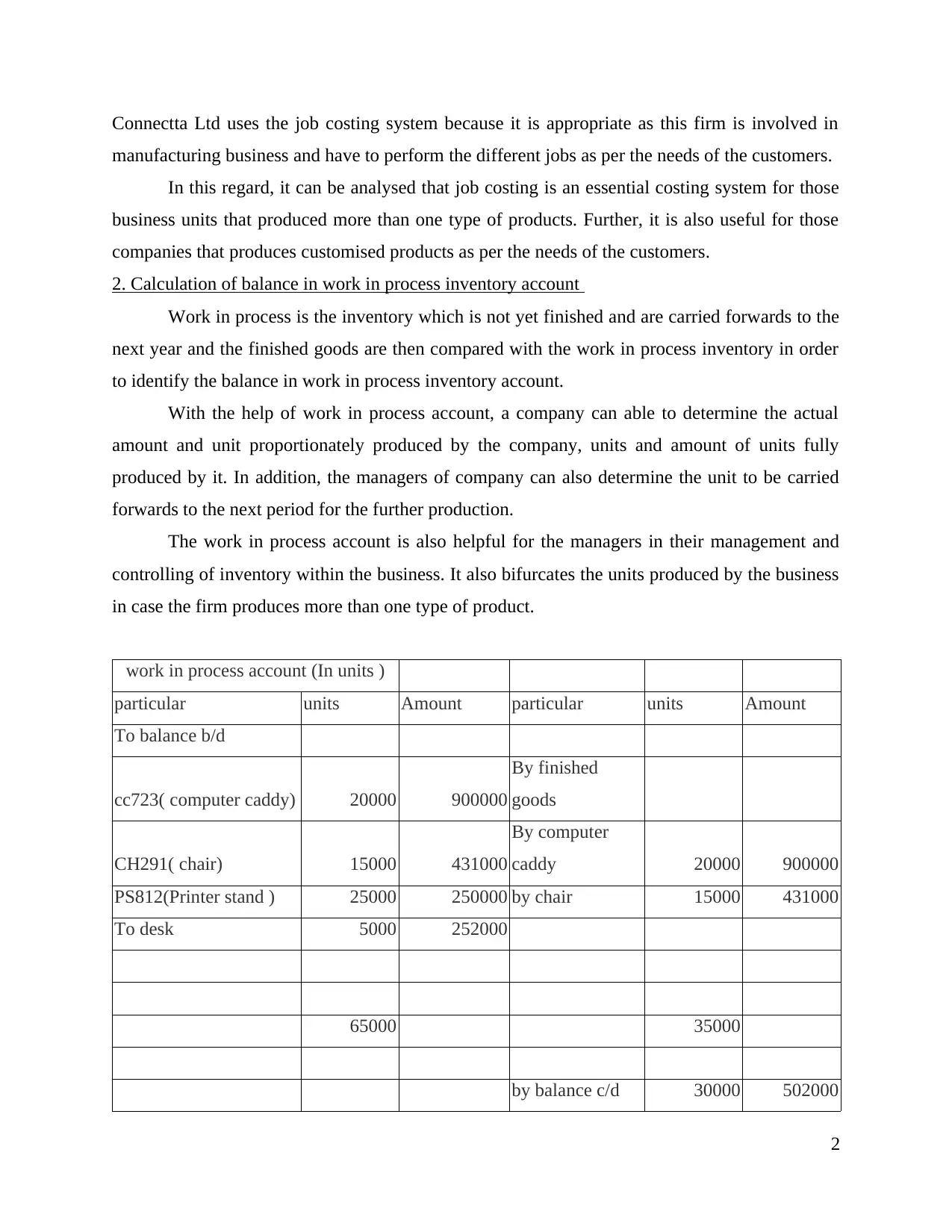

2. Calculation of balance in work in process inventory account

Work in process is the inventory which is not yet finished and are carried forwards to the

next year and the finished goods are then compared with the work in process inventory in order

to identify the balance in work in process inventory account.

With the help of work in process account, a company can able to determine the actual

amount and unit proportionately produced by the company, units and amount of units fully

produced by it. In addition, the managers of company can also determine the unit to be carried

forwards to the next period for the further production.

The work in process account is also helpful for the managers in their management and

controlling of inventory within the business. It also bifurcates the units produced by the business

in case the firm produces more than one type of product.

work in process account (In units )

particular units Amount particular units Amount

To balance b/d

cc723( computer caddy) 20000 900000

By finished

goods

CH291( chair) 15000 431000

By computer

caddy 20000 900000

PS812(Printer stand ) 25000 250000 by chair 15000 431000

To desk 5000 252000

65000 35000

by balance c/d 30000 502000

2

manufacturing business and have to perform the different jobs as per the needs of the customers.

In this regard, it can be analysed that job costing is an essential costing system for those

business units that produced more than one type of products. Further, it is also useful for those

companies that produces customised products as per the needs of the customers.

2. Calculation of balance in work in process inventory account

Work in process is the inventory which is not yet finished and are carried forwards to the

next year and the finished goods are then compared with the work in process inventory in order

to identify the balance in work in process inventory account.

With the help of work in process account, a company can able to determine the actual

amount and unit proportionately produced by the company, units and amount of units fully

produced by it. In addition, the managers of company can also determine the unit to be carried

forwards to the next period for the further production.

The work in process account is also helpful for the managers in their management and

controlling of inventory within the business. It also bifurcates the units produced by the business

in case the firm produces more than one type of product.

work in process account (In units )

particular units Amount particular units Amount

To balance b/d

cc723( computer caddy) 20000 900000

By finished

goods

CH291( chair) 15000 431000

By computer

caddy 20000 900000

PS812(Printer stand ) 25000 250000 by chair 15000 431000

To desk 5000 252000

65000 35000

by balance c/d 30000 502000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

printer stand 25000 250000

desk 5000 252000

On the basis of the above calculation it has been understood about the work in process

inventory account which shows the balance of the inventory which are still not finished at the

end of December. The calculation shows that the balance brought down by considering the items

which are in work in process and then comparing them with that of the finished goods in order to

determine the balance at the end of the December.

3. Calculation of cost of chairs in Connectta's finished goods inventory as at 31 December

Total units of chairs produced by the company = 15000

cost per unit incured by business in production of finished charis =431000/15000 = $ 28.73 per

unit

total cost incurred by business in production of chairs = 15000 * 28.73 = $ 430950

Interpretation

From the analysis of above calculation for the total cost incurred by the business in

production of chair, it can be interpret that the company has incurred total amount of $ 28.73

while finishing the single chair. Further, the company has produced total 15000 chairs in the

year. In this regard, the company has incurred a sum of $ 430950 in the production of chair

during the year.

4. Calculation of amount of overheads over applied or under applied for the year

Over applied overheads:

The overheads are said to be over applied in case the actual overhead incurred by the

business comes more than the budgeted overheads. The situation of over applied overhead shows

inefficiency in the business.

Under applied overheads:

Under applied overhead arises when the company incurred less amount of overheads than

its budgeted overheads. The situation of under applied overheads shows enhancement of

efficiency in the business organisation.

actual overhead incurred in December (49900

labour hours) 252000

3

desk 5000 252000

On the basis of the above calculation it has been understood about the work in process

inventory account which shows the balance of the inventory which are still not finished at the

end of December. The calculation shows that the balance brought down by considering the items

which are in work in process and then comparing them with that of the finished goods in order to

determine the balance at the end of the December.

3. Calculation of cost of chairs in Connectta's finished goods inventory as at 31 December

Total units of chairs produced by the company = 15000

cost per unit incured by business in production of finished charis =431000/15000 = $ 28.73 per

unit

total cost incurred by business in production of chairs = 15000 * 28.73 = $ 430950

Interpretation

From the analysis of above calculation for the total cost incurred by the business in

production of chair, it can be interpret that the company has incurred total amount of $ 28.73

while finishing the single chair. Further, the company has produced total 15000 chairs in the

year. In this regard, the company has incurred a sum of $ 430950 in the production of chair

during the year.

4. Calculation of amount of overheads over applied or under applied for the year

Over applied overheads:

The overheads are said to be over applied in case the actual overhead incurred by the

business comes more than the budgeted overheads. The situation of over applied overhead shows

inefficiency in the business.

Under applied overheads:

Under applied overhead arises when the company incurred less amount of overheads than

its budgeted overheads. The situation of under applied overheads shows enhancement of

efficiency in the business organisation.

actual overhead incurred in December (49900

labour hours) 252000

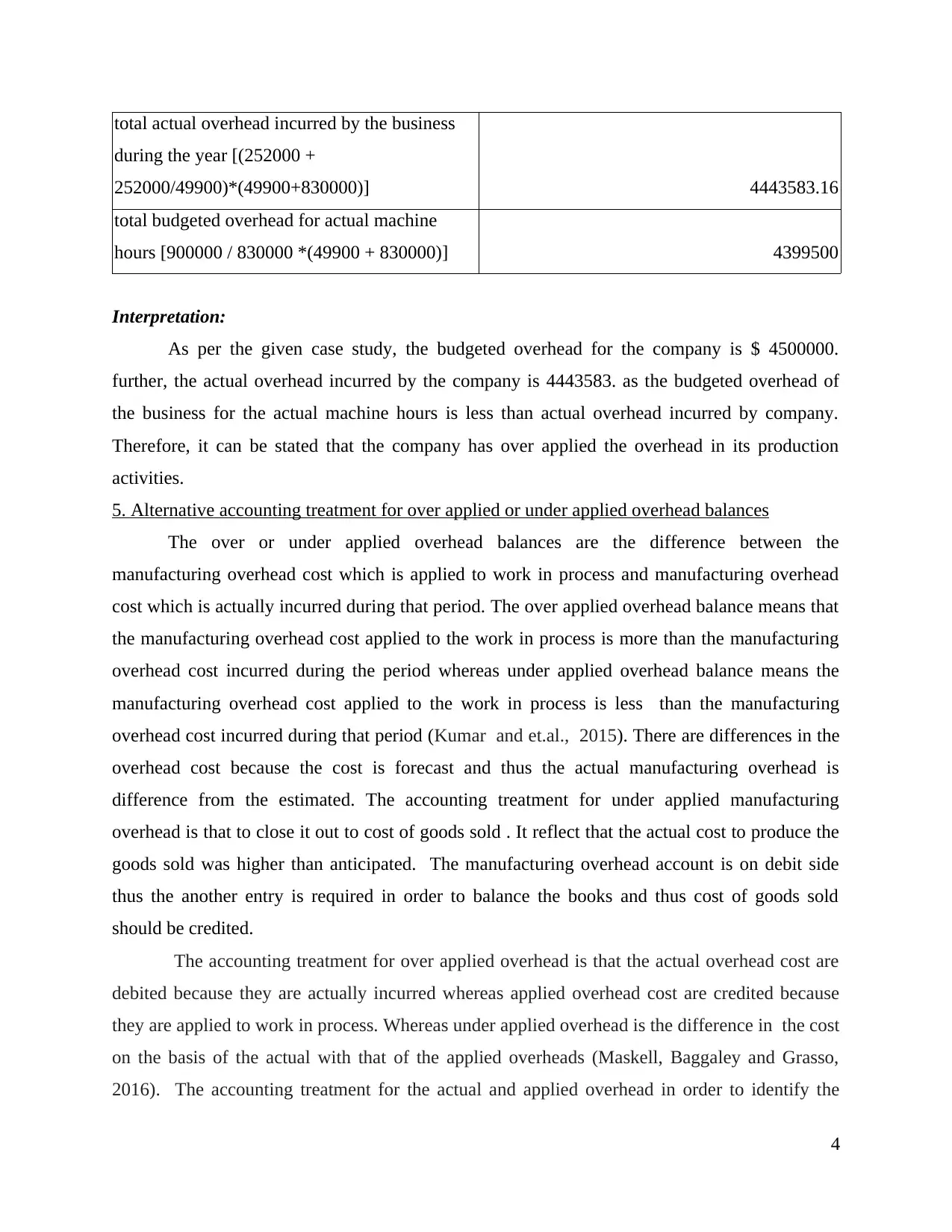

3

total actual overhead incurred by the business

during the year [(252000 +

252000/49900)*(49900+830000)] 4443583.16

total budgeted overhead for actual machine

hours [900000 / 830000 *(49900 + 830000)] 4399500

Interpretation:

As per the given case study, the budgeted overhead for the company is $ 4500000.

further, the actual overhead incurred by the company is 4443583. as the budgeted overhead of

the business for the actual machine hours is less than actual overhead incurred by company.

Therefore, it can be stated that the company has over applied the overhead in its production

activities.

5. Alternative accounting treatment for over applied or under applied overhead balances

The over or under applied overhead balances are the difference between the

manufacturing overhead cost which is applied to work in process and manufacturing overhead

cost which is actually incurred during that period. The over applied overhead balance means that

the manufacturing overhead cost applied to the work in process is more than the manufacturing

overhead cost incurred during the period whereas under applied overhead balance means the

manufacturing overhead cost applied to the work in process is less than the manufacturing

overhead cost incurred during that period (Kumar and et.al., 2015). There are differences in the

overhead cost because the cost is forecast and thus the actual manufacturing overhead is

difference from the estimated. The accounting treatment for under applied manufacturing

overhead is that to close it out to cost of goods sold . It reflect that the actual cost to produce the

goods sold was higher than anticipated. The manufacturing overhead account is on debit side

thus the another entry is required in order to balance the books and thus cost of goods sold

should be credited.

The accounting treatment for over applied overhead is that the actual overhead cost are

debited because they are actually incurred whereas applied overhead cost are credited because

they are applied to work in process. Whereas under applied overhead is the difference in the cost

on the basis of the actual with that of the applied overheads (Maskell, Baggaley and Grasso,

2016). The accounting treatment for the actual and applied overhead in order to identify the

4

during the year [(252000 +

252000/49900)*(49900+830000)] 4443583.16

total budgeted overhead for actual machine

hours [900000 / 830000 *(49900 + 830000)] 4399500

Interpretation:

As per the given case study, the budgeted overhead for the company is $ 4500000.

further, the actual overhead incurred by the company is 4443583. as the budgeted overhead of

the business for the actual machine hours is less than actual overhead incurred by company.

Therefore, it can be stated that the company has over applied the overhead in its production

activities.

5. Alternative accounting treatment for over applied or under applied overhead balances

The over or under applied overhead balances are the difference between the

manufacturing overhead cost which is applied to work in process and manufacturing overhead

cost which is actually incurred during that period. The over applied overhead balance means that

the manufacturing overhead cost applied to the work in process is more than the manufacturing

overhead cost incurred during the period whereas under applied overhead balance means the

manufacturing overhead cost applied to the work in process is less than the manufacturing

overhead cost incurred during that period (Kumar and et.al., 2015). There are differences in the

overhead cost because the cost is forecast and thus the actual manufacturing overhead is

difference from the estimated. The accounting treatment for under applied manufacturing

overhead is that to close it out to cost of goods sold . It reflect that the actual cost to produce the

goods sold was higher than anticipated. The manufacturing overhead account is on debit side

thus the another entry is required in order to balance the books and thus cost of goods sold

should be credited.

The accounting treatment for over applied overhead is that the actual overhead cost are

debited because they are actually incurred whereas applied overhead cost are credited because

they are applied to work in process. Whereas under applied overhead is the difference in the cost

on the basis of the actual with that of the applied overheads (Maskell, Baggaley and Grasso,

2016). The accounting treatment for the actual and applied overhead in order to identify the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

under or over applied cost through the help of manufacturing account. Moreover, allocation of

the cost to work-in process, finished goods and cost of goods sold. It assist in identifying the cost

of the manufacturing overhead by comparing the actual with that of the applied in order to

identify the overhead balances (Monden, 2018). The two alternative treatment for the over or

under applied overhead is that through the help of allocating the cost to cost of goods sold and to

take the balance to the manufacturing account.

The alternative accounting treatment are as follows :

Adjusting the over or under applied overhead with that of cost of goods sold.

The allocation method can also use uses in which the overheads which is over or under

applied is allocated to work - in process, finished goods of cos of goods sold.

Recording the actual and overhead applied in manufacturing overhead account.

6. Explaining the importance of activity based costing to overcome the inherent deficiencies in

the existing costing system

Activity based costing

The activity based costing is a system of costing that helps the managers in improving

their cost control system. It helps them in involving flexibility in their controlling and

management system of costing (Monden, 2018). The activity based costing also helps in

providing flexibility to customers and development of product or services as well. In this regard,

adoption of this system helps in enhancement of effectiveness of the business organisation.

The present costing system suggest the management that they should consider the all the

contingent variables while managing various business activities related to the cost control

system. As per the activity based costing system, the managers can determine the cost to be

incurred by the business while producing different level of production. It also enables the

managers to determine various issues that can be suffered by the business at the time of

producing a specific level of production.

On the other hand, the job costing system, provides rigidity to the business operations

(Mazzucco and et.al., 2015). It provides some specific controlling measures through which they

need to perform their managerial functions and control the costing system of the company.

In addition, various job costing systems like budgeting, standard costing, etc. results in

development of rigidity of controlling measures. As in case the business wants to produce at

5

the cost to work-in process, finished goods and cost of goods sold. It assist in identifying the cost

of the manufacturing overhead by comparing the actual with that of the applied in order to

identify the overhead balances (Monden, 2018). The two alternative treatment for the over or

under applied overhead is that through the help of allocating the cost to cost of goods sold and to

take the balance to the manufacturing account.

The alternative accounting treatment are as follows :

Adjusting the over or under applied overhead with that of cost of goods sold.

The allocation method can also use uses in which the overheads which is over or under

applied is allocated to work - in process, finished goods of cos of goods sold.

Recording the actual and overhead applied in manufacturing overhead account.

6. Explaining the importance of activity based costing to overcome the inherent deficiencies in

the existing costing system

Activity based costing

The activity based costing is a system of costing that helps the managers in improving

their cost control system. It helps them in involving flexibility in their controlling and

management system of costing (Monden, 2018). The activity based costing also helps in

providing flexibility to customers and development of product or services as well. In this regard,

adoption of this system helps in enhancement of effectiveness of the business organisation.

The present costing system suggest the management that they should consider the all the

contingent variables while managing various business activities related to the cost control

system. As per the activity based costing system, the managers can determine the cost to be

incurred by the business while producing different level of production. It also enables the

managers to determine various issues that can be suffered by the business at the time of

producing a specific level of production.

On the other hand, the job costing system, provides rigidity to the business operations

(Mazzucco and et.al., 2015). It provides some specific controlling measures through which they

need to perform their managerial functions and control the costing system of the company.

In addition, various job costing systems like budgeting, standard costing, etc. results in

development of rigidity of controlling measures. As in case the business wants to produce at

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

another level of production, or it decides to produce the managers would need to develop their

new measures for the controlling and management purpose (Fisher and et.al., 2016). All these

deficiencies can be removed by adoption of activity based costing as it provides flexibility to the

managers. With the help of this flexibility, the managers can control and monitor various types

of business, through which the efficiency of performing business activities can be enhanced.

CONCLUSION

From the analysis of this project report, it can be concluded that the job costing system

helps the business organisation in enhancing the efficiency of cost controlling system of the

company. Further, it is helpful for those organisations that develops customised products for the

customers. With the help of work in process inventory account, managers can determine the

amount as well as unit of the inventory partially produced, inventory of finished products and

amount and unit of inventory to be carry forward to the next period for further production, as

well.

Further, the study as also concluded that with the help of over applied or under applied

overheads, company's efficiency in the cost control system can be determined. In addition,

adoption of activity based costing enables the company in elimination of various deficiencies in

the existing cost controlling system of the business.

6

new measures for the controlling and management purpose (Fisher and et.al., 2016). All these

deficiencies can be removed by adoption of activity based costing as it provides flexibility to the

managers. With the help of this flexibility, the managers can control and monitor various types

of business, through which the efficiency of performing business activities can be enhanced.

CONCLUSION

From the analysis of this project report, it can be concluded that the job costing system

helps the business organisation in enhancing the efficiency of cost controlling system of the

company. Further, it is helpful for those organisations that develops customised products for the

customers. With the help of work in process inventory account, managers can determine the

amount as well as unit of the inventory partially produced, inventory of finished products and

amount and unit of inventory to be carry forward to the next period for further production, as

well.

Further, the study as also concluded that with the help of over applied or under applied

overheads, company's efficiency in the cost control system can be determined. In addition,

adoption of activity based costing enables the company in elimination of various deficiencies in

the existing cost controlling system of the business.

6

REFERENCES

Books and Journals

Maskell, B. H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Kumar, R. and et.al., 2015. Method and system using admission control in interactive grid

computing systems. U.S. Patent 8. 935.401.

Laudon, K. C. and Laudon, J. P., 2016. Management information system. Pearson Education

India.

Altbach, P., 2015. The costs and benefits of world-class universities. International Higher

Education. (33).

Monden, Y., 2018. Toyota management system: Linking the seven key functional areas.

Mazzucco, M. and et.al., 2015. Distributed data processing system. U.S. Patent 9,015,227.

Fisher, E. S. and et.al., 2016. Implementation science: a potential catalyst for delivery system

reform. Jama. 315(4). pp.339-340.

7

Books and Journals

Maskell, B. H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Kumar, R. and et.al., 2015. Method and system using admission control in interactive grid

computing systems. U.S. Patent 8. 935.401.

Laudon, K. C. and Laudon, J. P., 2016. Management information system. Pearson Education

India.

Altbach, P., 2015. The costs and benefits of world-class universities. International Higher

Education. (33).

Monden, Y., 2018. Toyota management system: Linking the seven key functional areas.

Mazzucco, M. and et.al., 2015. Distributed data processing system. U.S. Patent 9,015,227.

Fisher, E. S. and et.al., 2016. Implementation science: a potential catalyst for delivery system

reform. Jama. 315(4). pp.339-340.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.