Detailed Analysis of Joe Harper's Taxation Law and Tax Return

VerifiedAdded on 2021/02/19

|8

|2184

|326

Report

AI Summary

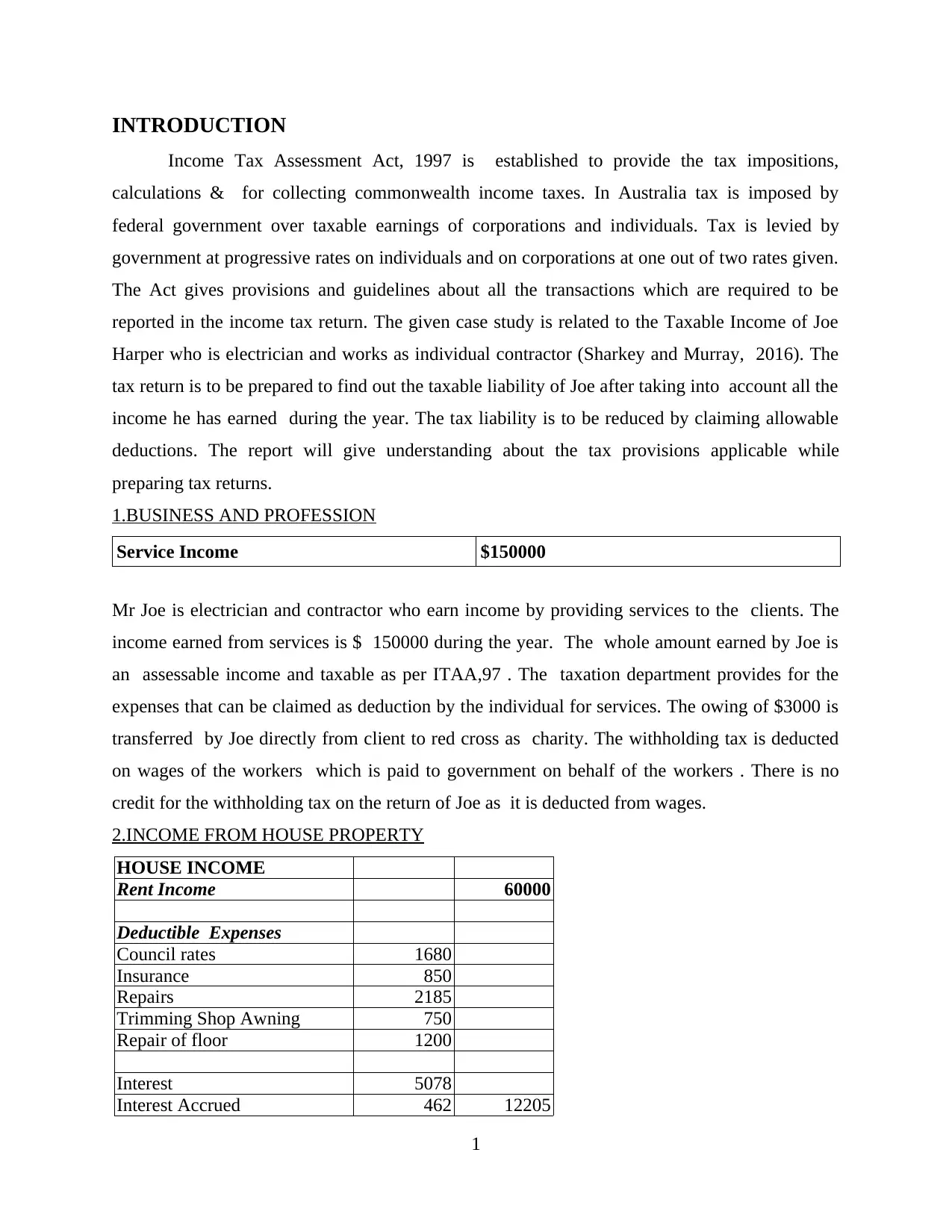

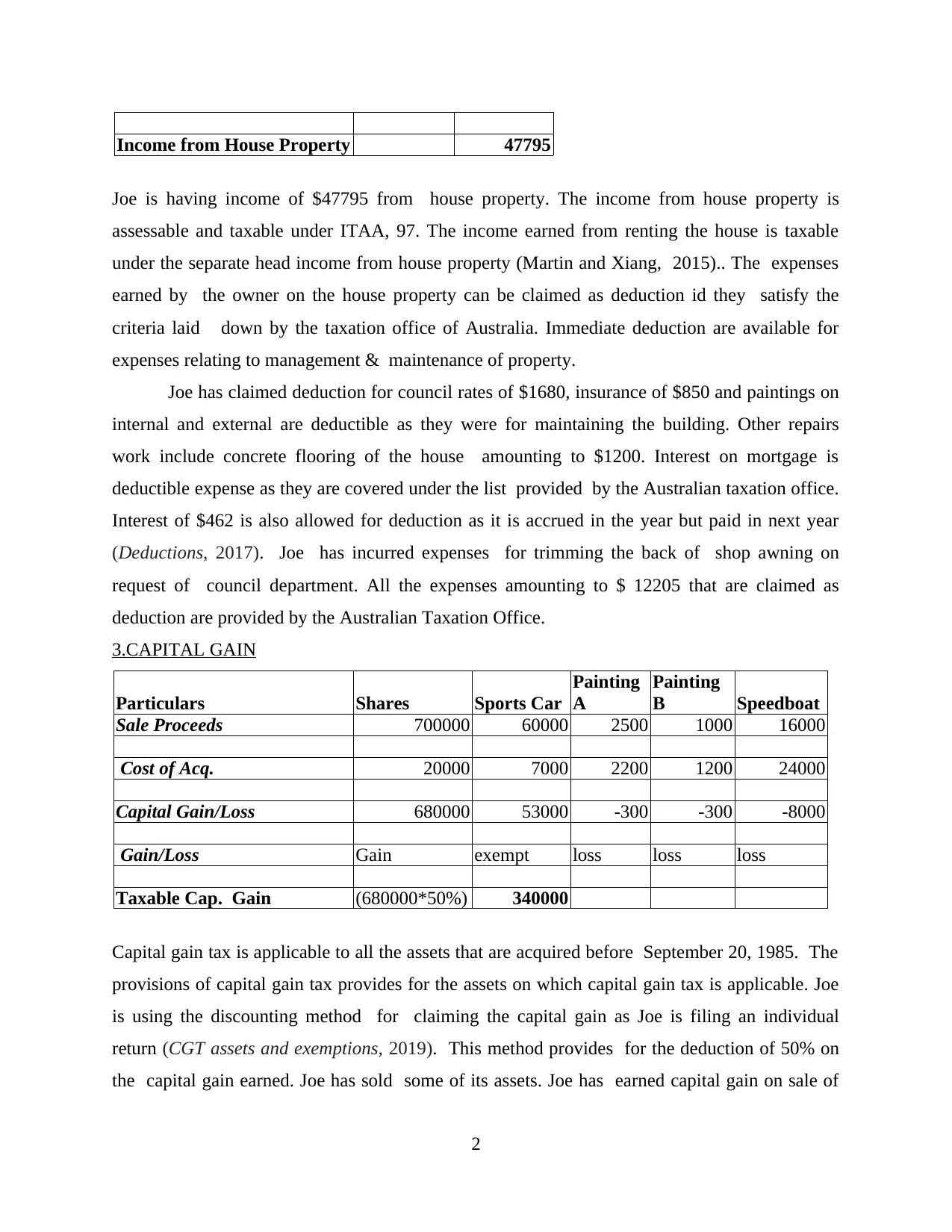

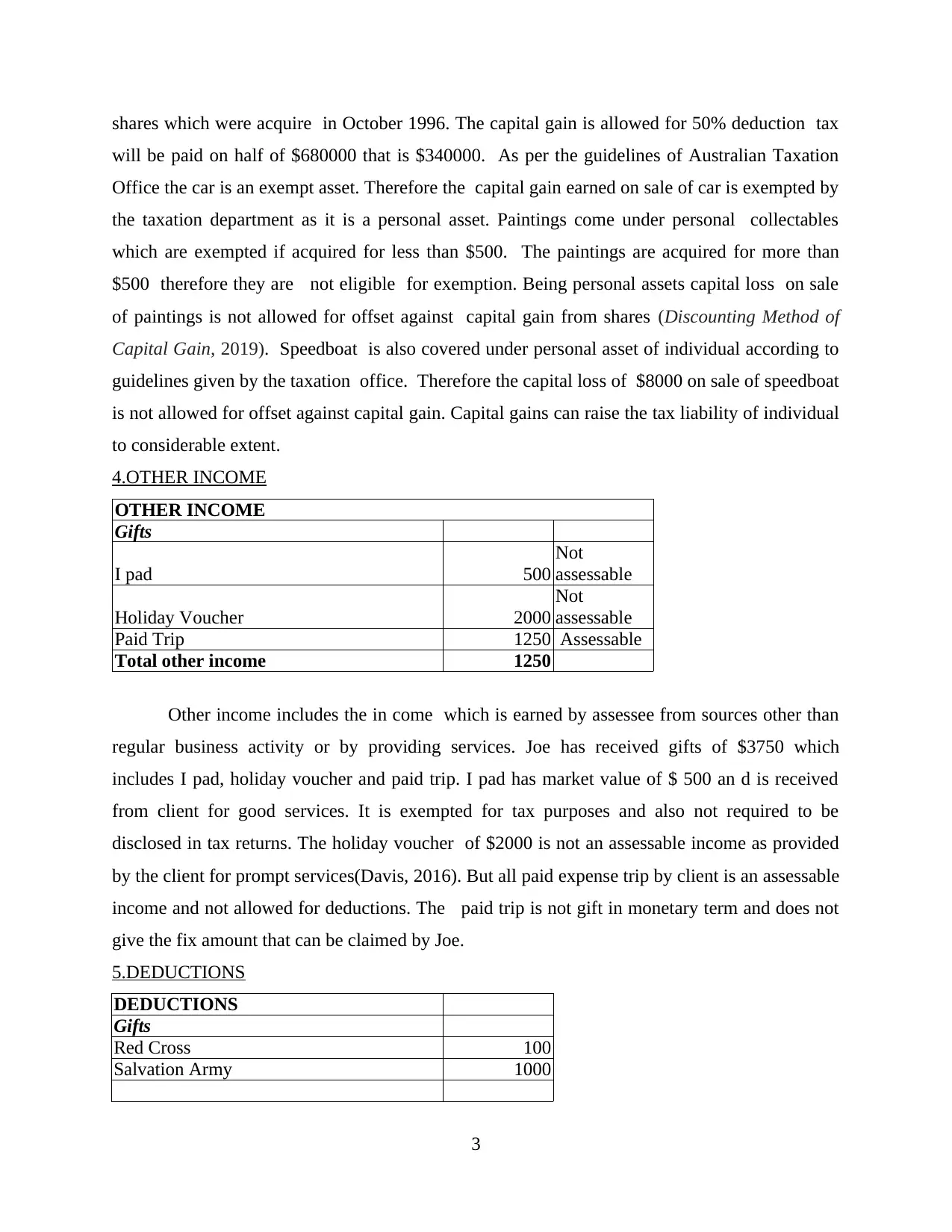

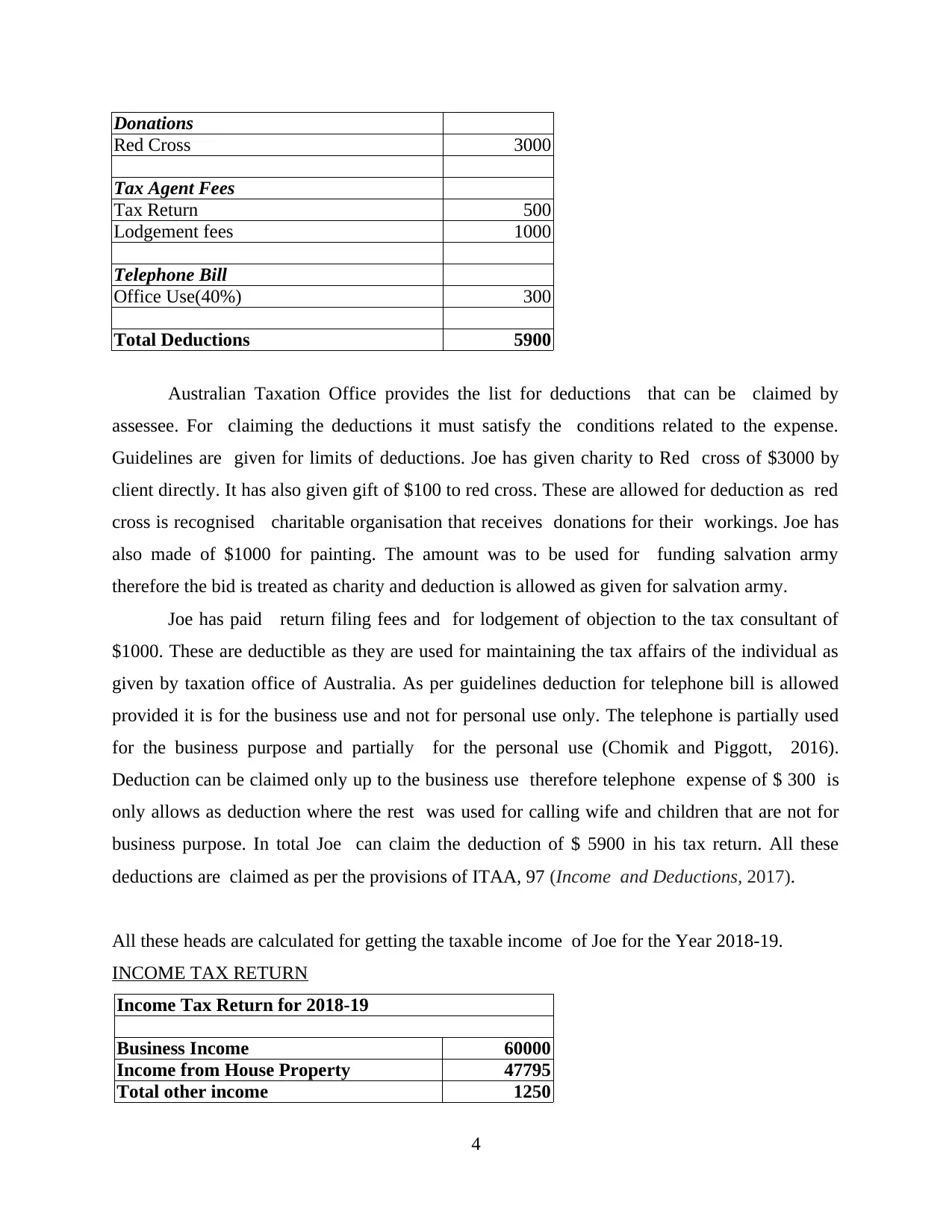

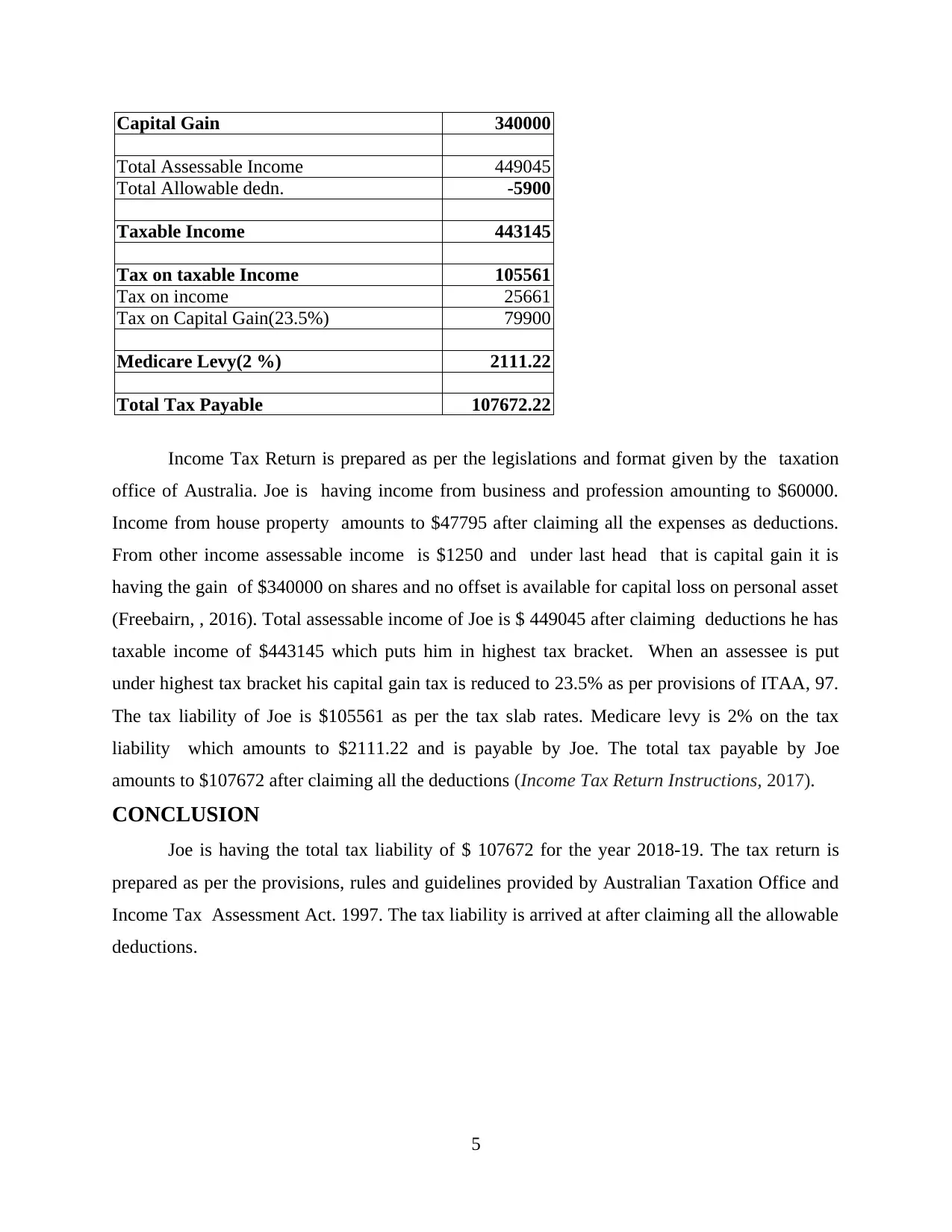

This report analyzes the income tax return of Joe Harper, an electrician and contractor, for the year 2018-19, focusing on Australian taxation law and the Income Tax Assessment Act 1997. It details the calculation of Joe's taxable income, including income from business and profession ($150,000), house property ($47,795), and other income ($1,250), along with capital gains. The report examines allowable deductions such as council rates, insurance, repairs, and charitable donations, totaling $5,900. Capital gains tax implications are discussed, considering the sale of shares, personal assets like a car and speedboat, and paintings. The final income tax return shows a total assessable income of $449,045, a taxable income of $443,145, and a total tax payable of $107,672.22, including Medicare levy. The report provides a comprehensive overview of the tax provisions and calculations relevant to Joe Harper's financial situation.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.