ITAA 36 Analysis: Determining Mr. Johnson's Residency for Taxation

VerifiedAdded on 2023/03/30

|7

|1151

|115

Report

AI Summary

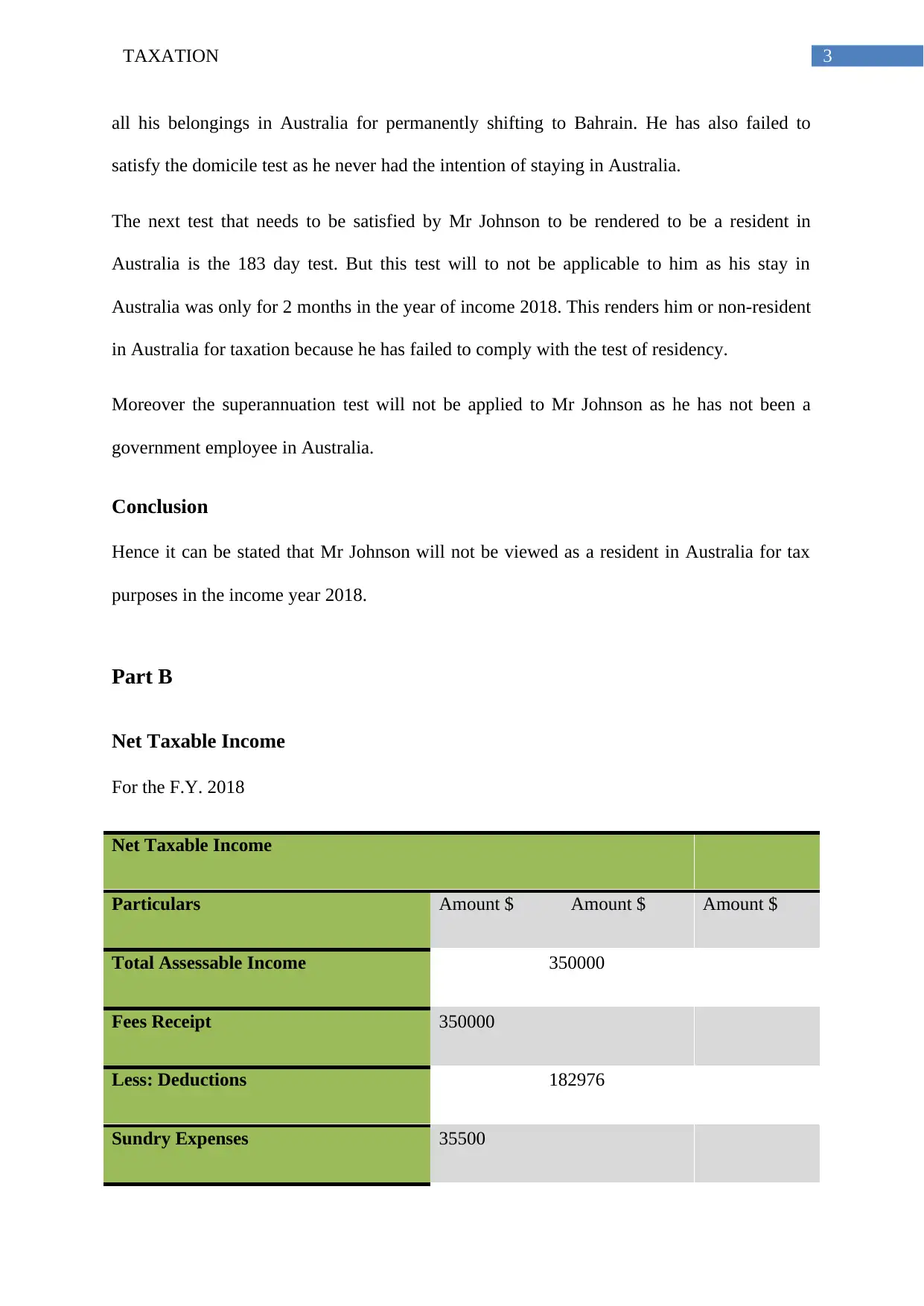

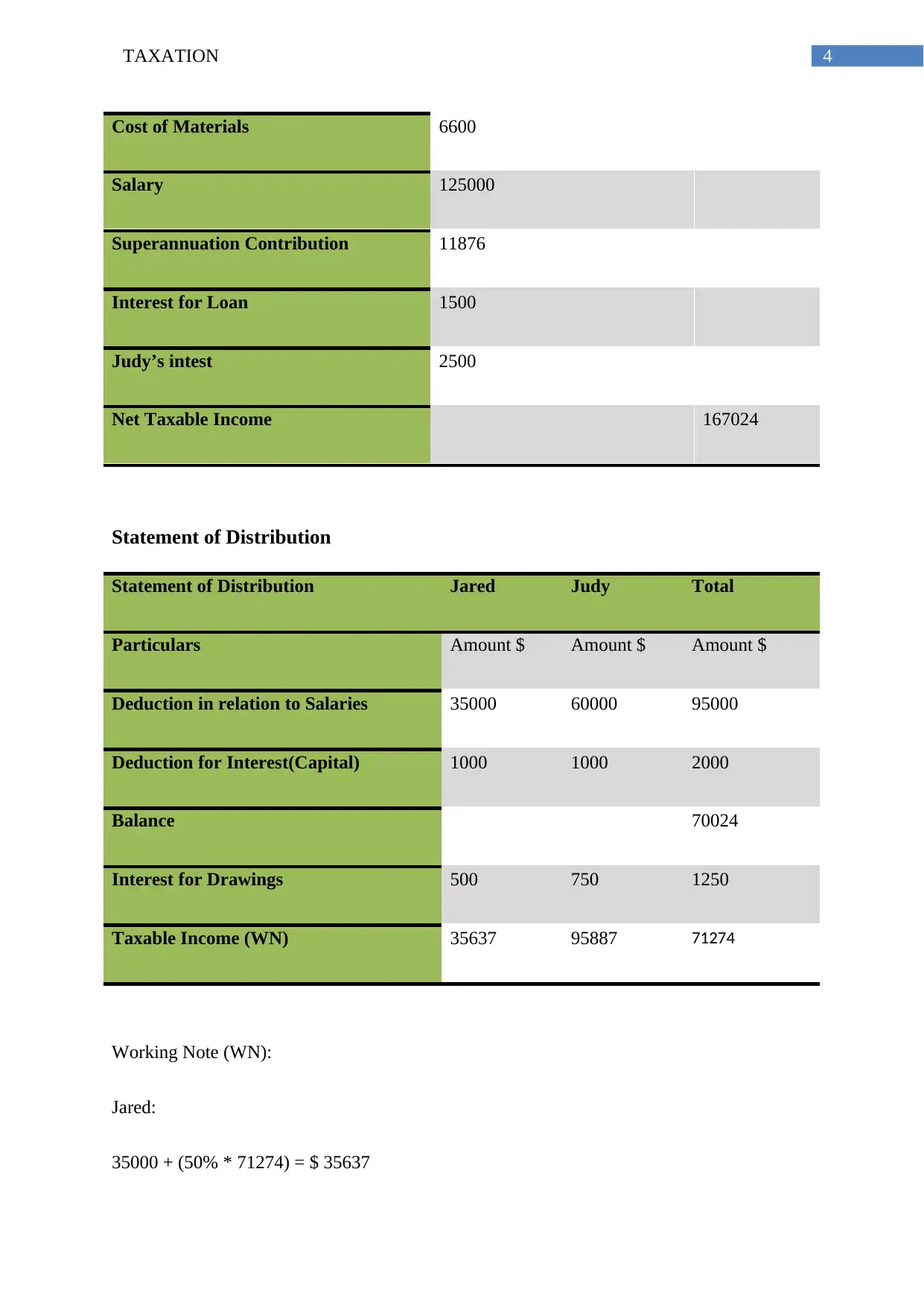

This report provides a legal analysis of Mr. Johnson's residency status for Australian taxation purposes in the income year 2018, based on the Income Tax Assessment Act 1936 (ITAA 36). It examines the resides test, domicile test, and the 183-day test to determine whether Mr. Johnson should be considered an Australian resident for tax purposes, considering his employment in Bahrain and visits to Australia. Additionally, the report includes a calculation of net taxable income for a partnership, detailing income, deductions, and a statement of distribution among partners, Jared and Judy. The conclusion states that Mr. Johnson is not a resident for tax purposes and provides the net income calculation and distribution.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.