Comprehensive Management Accounting Analysis for JOJO Juice Company

VerifiedAdded on 2021/02/20

|14

|4049

|42

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within JOJO Juice, a manufacturing company. It begins by highlighting the need for a management accounting system, emphasizing the role of cost accounting, price optimization, and inventory management. The report then explores various management accounting reporting methods, including budget reports, accounts receivable aging reports, cost managerial accounting reports, and performance reports. A significant portion of the report is dedicated to presenting income statements using both marginal costing and absorption costing methods, providing a comparative analysis of their impact on financial reporting. Furthermore, the report discusses the benefits and limitations of planning tools, such as sales and cash budgets, and outlines ways to address and resolve financial problems within the firm. The analysis covers a wide range of topics from the need for management accounting to the application of different costing methods and planning tools to improve the organization’s functioning.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P 1 Need of MA system in the company....................................................................................1

P 2 different methods of MA reporting system...........................................................................2

LO 2.................................................................................................................................................3

P 3 Presentations of income statement by using the different costing method...........................3

LO 3.................................................................................................................................................6

P 4 Benefits and limitation of various planning tools.................................................................6

LO 4 ................................................................................................................................................8

P 5 Ways to resolve or respond the financial problems of the firm............................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P 1 Need of MA system in the company....................................................................................1

P 2 different methods of MA reporting system...........................................................................2

LO 2.................................................................................................................................................3

P 3 Presentations of income statement by using the different costing method...........................3

LO 3.................................................................................................................................................6

P 4 Benefits and limitation of various planning tools.................................................................6

LO 4 ................................................................................................................................................8

P 5 Ways to resolve or respond the financial problems of the firm............................................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is used to improve the understanding of the financial and non

financial information to take the efficient decision and improve the organisational culture and

environment. It helps to provide the useful information to the stakeholders. JOJO fruit juice is a

manufacturing unit which manufacture juice for all age group. The report highlights the

management accounting role and decision making and various management accounting system

to improve the organisation functioning. It explains the various methods used by MA in

reporting the transaction. It also explains the use of marginal cost and absorption cost in

preparation of income statement. Planning tools such as sales budget, cash budget have various

advantages and disadvantages for budgetary control and the different financial problems and way

to solve these problems.

LO 1

P 1 Need of MA system in the company

Management accounting : It is the process of recording, analysing and maintaining the

accounting information to improve the operation work and prepare the financial reports to inform

the organisation condition to the management and management leaders like Owner, shareholders,

creditors etc. (Kaplan and Atkinson, 2015).

Requirement of Management accounting system

Cost accounting system : It is also known as product costing or costing system. It helps

the JOJO juice manufacturing company to estimate the cost of the product and its ingredients to

analyses the profit, inventory and control the cost of the unit. The firm has to evaluate the each

aspect of the production activity to estimate the accurate cost and profit of the organization. It

also helps them to evaluate the work in process, finished and raw material inventory level in the

company (Schaltegger and Burritt, 2017). There are two main types of cost accounting system :

process costing and job order costing.

Job order costing : It helps the organization to estimate the cost of each job and control

the activity to get the accurate result and find the area of improvement. It mainly used by the

company which produce the unique and special products and services.

Process costing : It helps the company to accumulate the cost of each process separately.

It is widely used in the organization where the production of goods and services can be done by

1

Management accounting is used to improve the understanding of the financial and non

financial information to take the efficient decision and improve the organisational culture and

environment. It helps to provide the useful information to the stakeholders. JOJO fruit juice is a

manufacturing unit which manufacture juice for all age group. The report highlights the

management accounting role and decision making and various management accounting system

to improve the organisation functioning. It explains the various methods used by MA in

reporting the transaction. It also explains the use of marginal cost and absorption cost in

preparation of income statement. Planning tools such as sales budget, cash budget have various

advantages and disadvantages for budgetary control and the different financial problems and way

to solve these problems.

LO 1

P 1 Need of MA system in the company

Management accounting : It is the process of recording, analysing and maintaining the

accounting information to improve the operation work and prepare the financial reports to inform

the organisation condition to the management and management leaders like Owner, shareholders,

creditors etc. (Kaplan and Atkinson, 2015).

Requirement of Management accounting system

Cost accounting system : It is also known as product costing or costing system. It helps

the JOJO juice manufacturing company to estimate the cost of the product and its ingredients to

analyses the profit, inventory and control the cost of the unit. The firm has to evaluate the each

aspect of the production activity to estimate the accurate cost and profit of the organization. It

also helps them to evaluate the work in process, finished and raw material inventory level in the

company (Schaltegger and Burritt, 2017). There are two main types of cost accounting system :

process costing and job order costing.

Job order costing : It helps the organization to estimate the cost of each job and control

the activity to get the accurate result and find the area of improvement. It mainly used by the

company which produce the unique and special products and services.

Process costing : It helps the company to accumulate the cost of each process separately.

It is widely used in the organization where the production of goods and services can be done by

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

department to department or the flow of production is from one department to another

department (Maskell, Baggaley and Grasso, 2017).

ABC costing : Activity based costing is used to estimate the cost of each activity and

assign the related expenses. It describes the relation between cost, overhead and manufacturing

activity. But some cost are unable to estimate by using the ABC costing system such as indirect

cost : office staff and workers salary.

Price optimization system : The system helps the company to determine the response

and behavior towards the price of the product and services. Customer is the end users of the

goods. They play major role in setting in the price to influencing manufacturers by their

activities. Organization uses various methods or tools to estimate the behavior of customer. It

also helps the JOJO juice manufacturing company to decide that whether the price set by them is

able to achieve the organization objective or not and the customer are able to reach the product

or not.

Inventory management system : It is a software system which provided the information

and support the company to record and measure the inventory lever, order quantity and sales of

the company in particular time period. Inventory management system is used to maintain the

inventory level and reduces the waste of inventory (Chenhall and Moers, 2015). It also helps the

company to minimize the over and under production of goods. JOJO manufacturing company

use the system to manage the demand and supply level and deliver the juice to the customer on

time. It is tool which record all the data related to the inventory in computer based system which

was prior done manually. It helps them to get the required stock on time by recording all the

sales and arrival of the products.

P 2 different methods of MA reporting system

The aim of MA reporting is to collect the data form the financial accounting a use them

to prepare the report by recording the transaction in different accounts to inform the stakeholders

about the financial position of the company. There are different management accounting report

such as :

Budget report : one of the role of management accounting is to plan the requirement of

finance by preparing budget for the different activities and ascertain the requirement of resource

to accomplish the goal and objectives (Maas, Schaltegger, and Crutzen, 2016). Budget are

prepared by the manager by using the past year data and add the inflation rate and estimate

2

department (Maskell, Baggaley and Grasso, 2017).

ABC costing : Activity based costing is used to estimate the cost of each activity and

assign the related expenses. It describes the relation between cost, overhead and manufacturing

activity. But some cost are unable to estimate by using the ABC costing system such as indirect

cost : office staff and workers salary.

Price optimization system : The system helps the company to determine the response

and behavior towards the price of the product and services. Customer is the end users of the

goods. They play major role in setting in the price to influencing manufacturers by their

activities. Organization uses various methods or tools to estimate the behavior of customer. It

also helps the JOJO juice manufacturing company to decide that whether the price set by them is

able to achieve the organization objective or not and the customer are able to reach the product

or not.

Inventory management system : It is a software system which provided the information

and support the company to record and measure the inventory lever, order quantity and sales of

the company in particular time period. Inventory management system is used to maintain the

inventory level and reduces the waste of inventory (Chenhall and Moers, 2015). It also helps the

company to minimize the over and under production of goods. JOJO manufacturing company

use the system to manage the demand and supply level and deliver the juice to the customer on

time. It is tool which record all the data related to the inventory in computer based system which

was prior done manually. It helps them to get the required stock on time by recording all the

sales and arrival of the products.

P 2 different methods of MA reporting system

The aim of MA reporting is to collect the data form the financial accounting a use them

to prepare the report by recording the transaction in different accounts to inform the stakeholders

about the financial position of the company. There are different management accounting report

such as :

Budget report : one of the role of management accounting is to plan the requirement of

finance by preparing budget for the different activities and ascertain the requirement of resource

to accomplish the goal and objectives (Maas, Schaltegger, and Crutzen, 2016). Budget are

prepared by the manager by using the past year data and add the inflation rate and estimate

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses to the company performance in the future. Budget report help the company to get the

current state of the company and control the limit of expending of organisation by setting the

criteria and associate the cost of each activity. It provides an estimation of all the income and

expenses in particular accounting period and done the activity according to the set of activities.

Account receivable aging report : It helps the company to ascertain the debt of the

organization and the time period of owning the debt. Manager uses the A/R report to estimate the

defaulters of the company and find the problems in collection of the debt from the debtors

(Methods of Management Accounting Report, 2019). It helps them to renovate and improve the

policies and rules regarding the collection of debt of the organization. It breaks down the

remaining balances of the debtor so the company can estimate the time period of collection of

debt and write off the debt of the company which was about to unrecoverable.

Cost managerial accounting report : It is estimated by the company by adding all the

cost such as material cost, overhead cost, direct and indirect cost and divided by the total number

of production. It helps the JOJO juice manufacturing company to set the profit margins and

estimate the cost and price of the items (Stacchezzini, Melloni and Lai, 2016.). It is used by the

company to manage the wastage of inventory, products and labour. The treatment of wastage of

JOJO juice manufacturing company help them to minimize the cost and time in the production

activity and also increases the profit margin to get the higher profit.

Performance report : The report are prepared to analyse and reviewed the performance

of the company and its employees. It helps to manage the activities of the employees and prepare

report to analyse their growth and work in the company to provide the wages and incentives

according to their performance. JOJO juice manufacturing company use the performance report

to record the activities of each department and take the major actions on the basis of activities

growth and output and find the ways to improve performance. It helps the company to present

the financial information to the different users of the company so they can take the decision of

investing in the companies' production or manufacturing activities or not.

LO 2

P 3 Presentations of income statement by using the different costing method

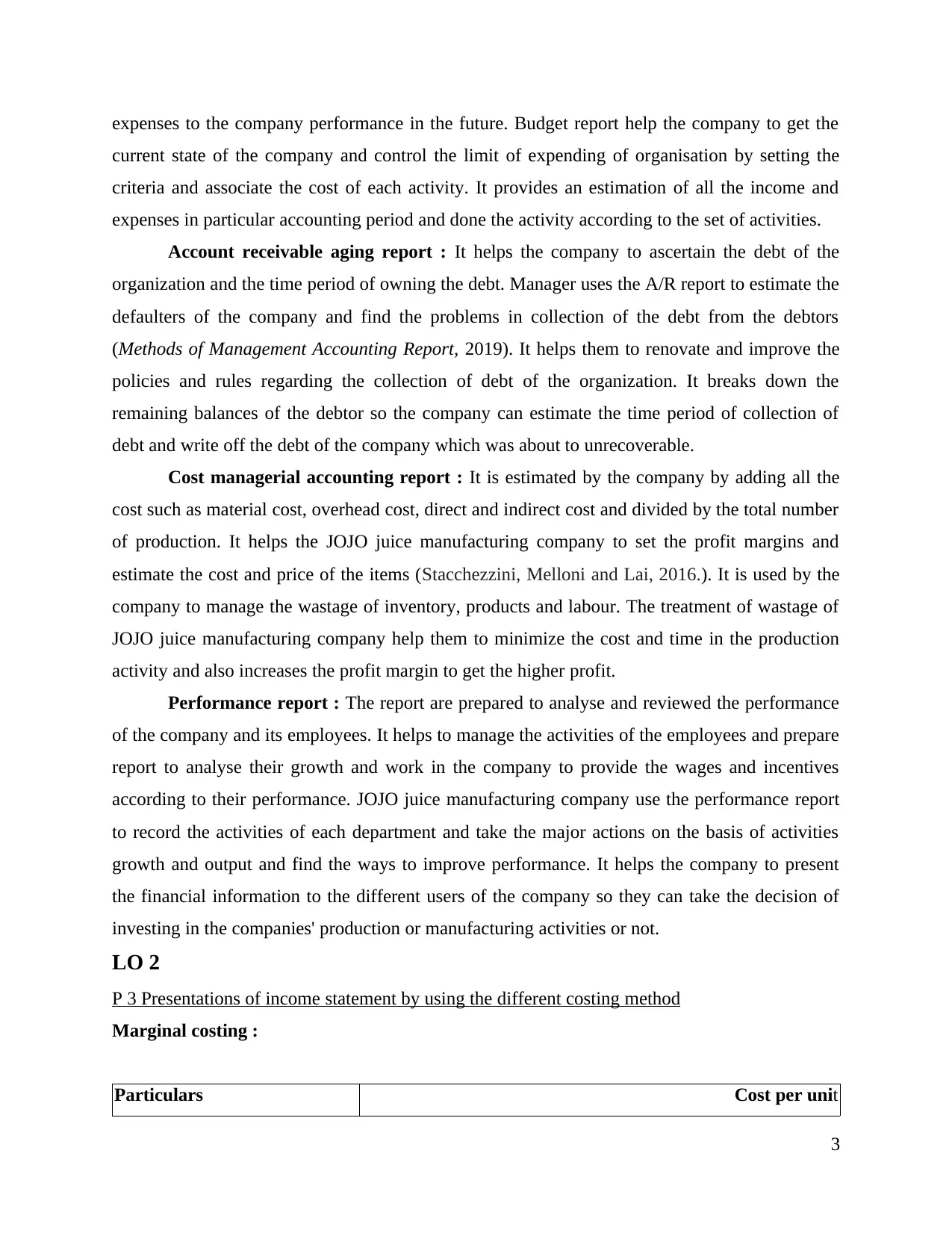

Marginal costing :

Particulars Cost per unit

3

current state of the company and control the limit of expending of organisation by setting the

criteria and associate the cost of each activity. It provides an estimation of all the income and

expenses in particular accounting period and done the activity according to the set of activities.

Account receivable aging report : It helps the company to ascertain the debt of the

organization and the time period of owning the debt. Manager uses the A/R report to estimate the

defaulters of the company and find the problems in collection of the debt from the debtors

(Methods of Management Accounting Report, 2019). It helps them to renovate and improve the

policies and rules regarding the collection of debt of the organization. It breaks down the

remaining balances of the debtor so the company can estimate the time period of collection of

debt and write off the debt of the company which was about to unrecoverable.

Cost managerial accounting report : It is estimated by the company by adding all the

cost such as material cost, overhead cost, direct and indirect cost and divided by the total number

of production. It helps the JOJO juice manufacturing company to set the profit margins and

estimate the cost and price of the items (Stacchezzini, Melloni and Lai, 2016.). It is used by the

company to manage the wastage of inventory, products and labour. The treatment of wastage of

JOJO juice manufacturing company help them to minimize the cost and time in the production

activity and also increases the profit margin to get the higher profit.

Performance report : The report are prepared to analyse and reviewed the performance

of the company and its employees. It helps to manage the activities of the employees and prepare

report to analyse their growth and work in the company to provide the wages and incentives

according to their performance. JOJO juice manufacturing company use the performance report

to record the activities of each department and take the major actions on the basis of activities

growth and output and find the ways to improve performance. It helps the company to present

the financial information to the different users of the company so they can take the decision of

investing in the companies' production or manufacturing activities or not.

LO 2

P 3 Presentations of income statement by using the different costing method

Marginal costing :

Particulars Cost per unit

3

Direct Material 18

Direct Labour 4

Variable O/H 3

Marginal cost per unit 25

Selling price 50

-Marginal cost per unit -25

-variable selling price -5.00

Contribution per unit 20.00

profit and loss statement by using marginal costing method

November December

particula

rs

unit

price unit amount

Net

amount

unit

price unit amount

net

amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales 25 2000 50000

variable

cost of

productio

n 25 12000 300000 25 10000 250000 300000

Less

closing

stock 25 2000 50000 250000

less

variable

cost of

productio

n 5 10000 50000 50000 5 12000 60000 60000

4

Direct Labour 4

Variable O/H 3

Marginal cost per unit 25

Selling price 50

-Marginal cost per unit -25

-variable selling price -5.00

Contribution per unit 20.00

profit and loss statement by using marginal costing method

November December

particula

rs

unit

price unit amount

Net

amount

unit

price unit amount

net

amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales 25 2000 50000

variable

cost of

productio

n 25 12000 300000 25 10000 250000 300000

Less

closing

stock 25 2000 50000 250000

less

variable

cost of

productio

n 5 10000 50000 50000 5 12000 60000 60000

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

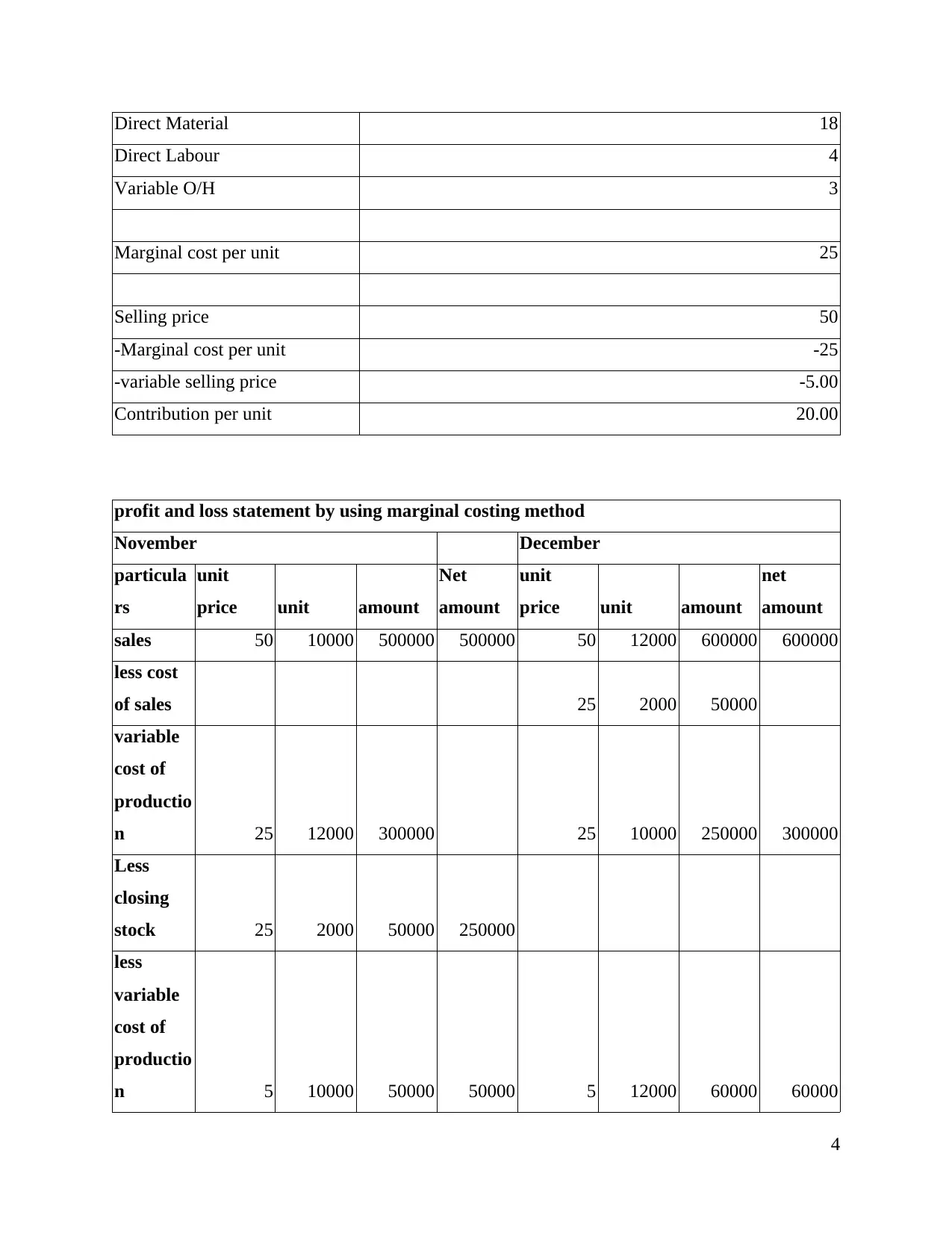

200000 240000

less fixed

variable

productio

n cost

productio

n 99000 99000

Selling

price 14000 14000

administr

ative 26000 139000 139000 26000 139000 139000

61000 101000

Absorption costing

Income statement

using absorption

costing method

particulars Amount Per unit

Normal level of

production 11000

Fixed overhead cost 99000

Fixed production

overhead 9

Total production cost

variable cost 25

Fixed cost 9

Total 34

profit and loss statement by using absorption costing method

5

less fixed

variable

productio

n cost

productio

n 99000 99000

Selling

price 14000 14000

administr

ative 26000 139000 139000 26000 139000 139000

61000 101000

Absorption costing

Income statement

using absorption

costing method

particulars Amount Per unit

Normal level of

production 11000

Fixed overhead cost 99000

Fixed production

overhead 9

Total production cost

variable cost 25

Fixed cost 9

Total 34

profit and loss statement by using absorption costing method

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

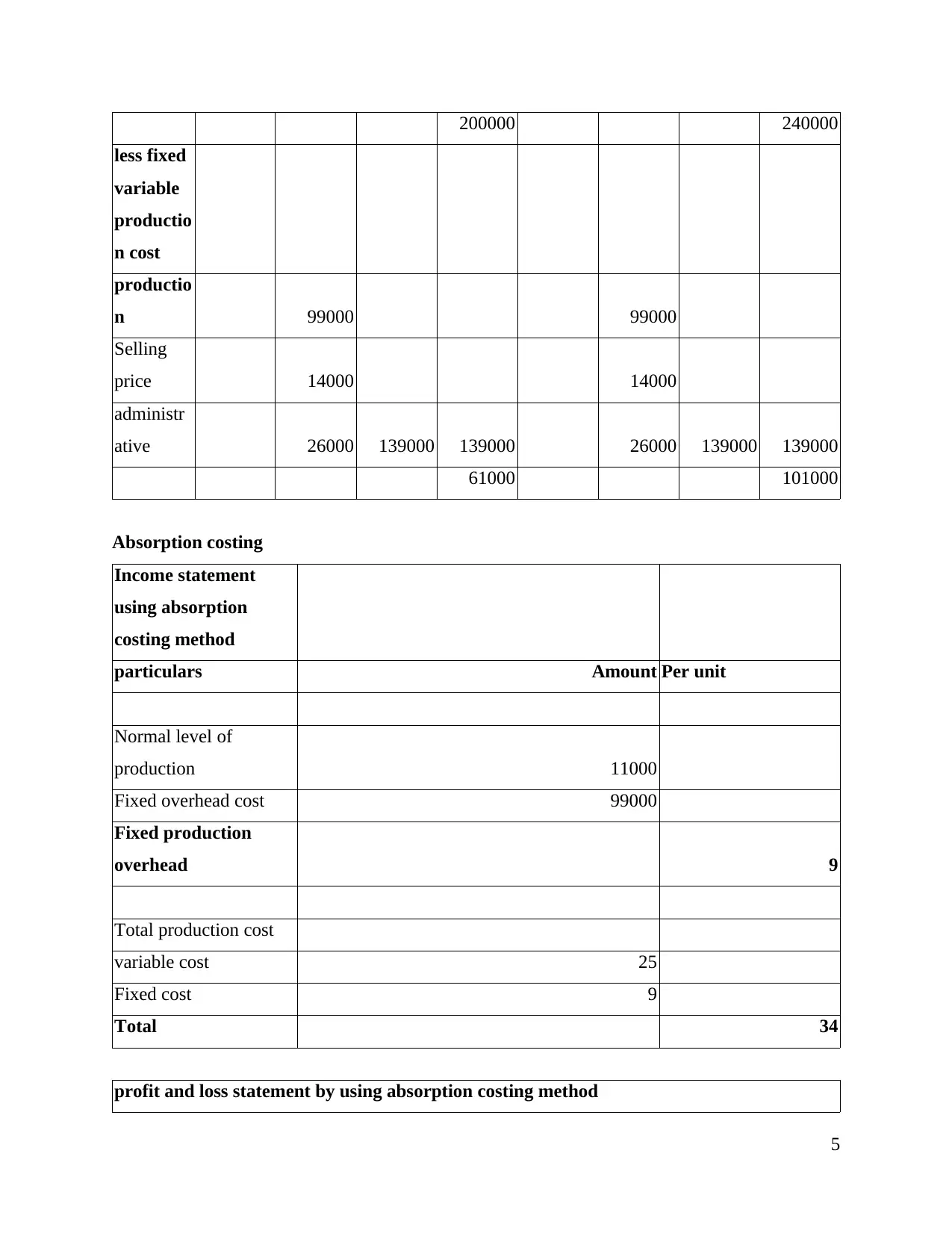

unit

price unit amount

unit

price unit amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales

opening

stock 34 2000 68000

productio

n cost 34 12000 408000 34 10000 340000 408000

34 2000 68000 340000

gross

profit 160000 192000

adjustmen

t for fixed

and under

absorptio

n 9000 9000

169000 183000

less

overhead

cost

variable

selling

O/H 50000 60000

fixed

selling

O/H 14000 14000

fixed

administr

ative O/H 26000 90000 26000 100000 100000

net profit 79000 83000

6

price unit amount

unit

price unit amount

sales 50 10000 500000 500000 50 12000 600000 600000

less cost

of sales

opening

stock 34 2000 68000

productio

n cost 34 12000 408000 34 10000 340000 408000

34 2000 68000 340000

gross

profit 160000 192000

adjustmen

t for fixed

and under

absorptio

n 9000 9000

169000 183000

less

overhead

cost

variable

selling

O/H 50000 60000

fixed

selling

O/H 14000 14000

fixed

administr

ative O/H 26000 90000 26000 100000 100000

net profit 79000 83000

6

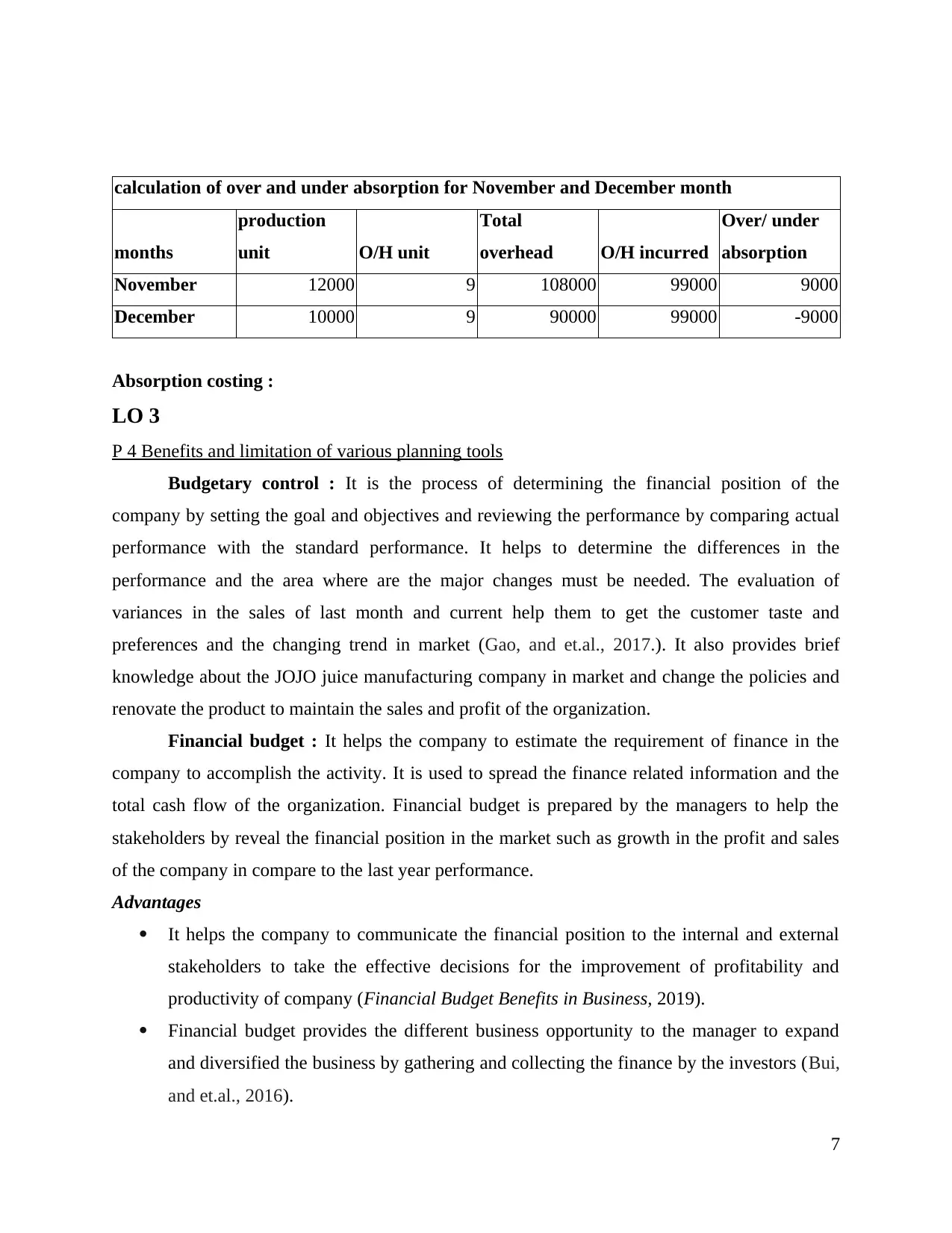

calculation of over and under absorption for November and December month

months

production

unit O/H unit

Total

overhead O/H incurred

Over/ under

absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Absorption costing :

LO 3

P 4 Benefits and limitation of various planning tools

Budgetary control : It is the process of determining the financial position of the

company by setting the goal and objectives and reviewing the performance by comparing actual

performance with the standard performance. It helps to determine the differences in the

performance and the area where are the major changes must be needed. The evaluation of

variances in the sales of last month and current help them to get the customer taste and

preferences and the changing trend in market (Gao, and et.al., 2017.). It also provides brief

knowledge about the JOJO juice manufacturing company in market and change the policies and

renovate the product to maintain the sales and profit of the organization.

Financial budget : It helps the company to estimate the requirement of finance in the

company to accomplish the activity. It is used to spread the finance related information and the

total cash flow of the organization. Financial budget is prepared by the managers to help the

stakeholders by reveal the financial position in the market such as growth in the profit and sales

of the company in compare to the last year performance.

Advantages

It helps the company to communicate the financial position to the internal and external

stakeholders to take the effective decisions for the improvement of profitability and

productivity of company (Financial Budget Benefits in Business, 2019).

Financial budget provides the different business opportunity to the manager to expand

and diversified the business by gathering and collecting the finance by the investors (Bui,

and et.al., 2016).

7

months

production

unit O/H unit

Total

overhead O/H incurred

Over/ under

absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Absorption costing :

LO 3

P 4 Benefits and limitation of various planning tools

Budgetary control : It is the process of determining the financial position of the

company by setting the goal and objectives and reviewing the performance by comparing actual

performance with the standard performance. It helps to determine the differences in the

performance and the area where are the major changes must be needed. The evaluation of

variances in the sales of last month and current help them to get the customer taste and

preferences and the changing trend in market (Gao, and et.al., 2017.). It also provides brief

knowledge about the JOJO juice manufacturing company in market and change the policies and

renovate the product to maintain the sales and profit of the organization.

Financial budget : It helps the company to estimate the requirement of finance in the

company to accomplish the activity. It is used to spread the finance related information and the

total cash flow of the organization. Financial budget is prepared by the managers to help the

stakeholders by reveal the financial position in the market such as growth in the profit and sales

of the company in compare to the last year performance.

Advantages

It helps the company to communicate the financial position to the internal and external

stakeholders to take the effective decisions for the improvement of profitability and

productivity of company (Financial Budget Benefits in Business, 2019).

Financial budget provides the different business opportunity to the manager to expand

and diversified the business by gathering and collecting the finance by the investors (Bui,

and et.al., 2016).

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It also helps to prepare the plan for ascertain the various sources of finance and manage

the assets and liability of the organization to paid the loan and debt within the time

period.

Disadvantage

It only provides the estimation of requirement of finance and not present the true and

accurate position of the company.

Manager also want to show the high profit in the balance sheet to attract the customer so

the manipulation of data is high in the financial budget.

Operating budget : It was used by the firm to plan or scheduled the requirement of

resources for the day to day operational activity. It helps to estimate the expenses, overhead and

requirement of resources by comparing it with the actual expenses.

Advantages

It helps to manage the current expenses and cost of the product and services such as the

rent, staff salaries, overhead etc.

Operational budget help to estimate the future expenses and resolve the last year

problems. The variance analysis help the company to manage the area of deficiency and

improve the performance. The estimation and presentation of operational budget increases the accountability of the

data and helps to gather the attention of stakeholders towards the company.

Disadvantage

The estimation of the cost require huge time to interpret each and every activity and the

cost of the previous year.

Operational budget also require the experts which have the knowledge about the market

and each area to accurately estimate the cost of the company.

Incremental budget : It is prepared by the company on the basis of previous year

budgets and add the incremental amount to get the new budget of the company (McCrory, and

et.al., 2015.). It helps the company to prepare the budget and control and monitor the activities of

company to reduce the wastage and improve the quality of work.

Advantages

8

the assets and liability of the organization to paid the loan and debt within the time

period.

Disadvantage

It only provides the estimation of requirement of finance and not present the true and

accurate position of the company.

Manager also want to show the high profit in the balance sheet to attract the customer so

the manipulation of data is high in the financial budget.

Operating budget : It was used by the firm to plan or scheduled the requirement of

resources for the day to day operational activity. It helps to estimate the expenses, overhead and

requirement of resources by comparing it with the actual expenses.

Advantages

It helps to manage the current expenses and cost of the product and services such as the

rent, staff salaries, overhead etc.

Operational budget help to estimate the future expenses and resolve the last year

problems. The variance analysis help the company to manage the area of deficiency and

improve the performance. The estimation and presentation of operational budget increases the accountability of the

data and helps to gather the attention of stakeholders towards the company.

Disadvantage

The estimation of the cost require huge time to interpret each and every activity and the

cost of the previous year.

Operational budget also require the experts which have the knowledge about the market

and each area to accurately estimate the cost of the company.

Incremental budget : It is prepared by the company on the basis of previous year

budgets and add the incremental amount to get the new budget of the company (McCrory, and

et.al., 2015.). It helps the company to prepare the budget and control and monitor the activities of

company to reduce the wastage and improve the quality of work.

Advantages

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is easy to prepared and manage in the company because it is based on the previous year

budget so the employees and manager can easily understand the estimation of budget and

organise the task according to the budget. Incremental budget are prepared at multi department level which help the company to

evaluate the funding of each department.

Disadvantage

The budget is based on the previous year budget but the market condition and investment

from the investor are fluctuating every year which did not present the true position.

The actual expenses and revenue of the company may different from the estimated

budget because of the development of budget on the prior year data.

LO 4

P 5 Ways to resolve or respond the financial problems of the firm

Benchmarking : It is used as the measure of reviewing the performance of the product

and services in the organization by comparing the performance with the pre setted benchmark of

the company or evaluate it with the competitors' performance in the market. It helps to get the

differences in the output of the company and find the area of variation to resolve the financial

problems. It used to reviewing the revenue of the JOJO juice manufacturing company with the

last year revenue and find the reason behind increasing or decreasing the revenue (Parmenter,

2015). The benchmark system can also be used by the each department to get the financial

position of each department and analyse the problem associated with the departments output.

Benchmarking system helps to improve the understanding of the employees towards the cost and

internal process of the firm.

Key performance indicators : It is used to evaluate that how effectively a company is

able to get the target and objectives of the company. The company used the KPI system at multi

level (Chambers, Freeny and Heiberger, 2017). At high level it was used to measure the overall

performance of the company and at lower level KPI was used to evaluate the performance of

each department and measure the monetary and on monetary problems of the company.

Variance analysis : It is used to evaluate the difference between the actual performance

and estimated performance of the firm. The difference in their performance is known as

variances. It helps to get the variation in different area by evaluating each and every task and

9

budget so the employees and manager can easily understand the estimation of budget and

organise the task according to the budget. Incremental budget are prepared at multi department level which help the company to

evaluate the funding of each department.

Disadvantage

The budget is based on the previous year budget but the market condition and investment

from the investor are fluctuating every year which did not present the true position.

The actual expenses and revenue of the company may different from the estimated

budget because of the development of budget on the prior year data.

LO 4

P 5 Ways to resolve or respond the financial problems of the firm

Benchmarking : It is used as the measure of reviewing the performance of the product

and services in the organization by comparing the performance with the pre setted benchmark of

the company or evaluate it with the competitors' performance in the market. It helps to get the

differences in the output of the company and find the area of variation to resolve the financial

problems. It used to reviewing the revenue of the JOJO juice manufacturing company with the

last year revenue and find the reason behind increasing or decreasing the revenue (Parmenter,

2015). The benchmark system can also be used by the each department to get the financial

position of each department and analyse the problem associated with the departments output.

Benchmarking system helps to improve the understanding of the employees towards the cost and

internal process of the firm.

Key performance indicators : It is used to evaluate that how effectively a company is

able to get the target and objectives of the company. The company used the KPI system at multi

level (Chambers, Freeny and Heiberger, 2017). At high level it was used to measure the overall

performance of the company and at lower level KPI was used to evaluate the performance of

each department and measure the monetary and on monetary problems of the company.

Variance analysis : It is used to evaluate the difference between the actual performance

and estimated performance of the firm. The difference in their performance is known as

variances. It helps to get the variation in different area by evaluating each and every task and

9

project to get the financial problems (Samra, 2016). It also used by the company to control and

manage the activities, inventories and cost of the firm to get the successful results.

Resolve financial problems

Financial governance : It refers to the process of collecting, monitoring, managing and

controlling the financial problems. Financial governance provide a framework to resolve the

financial problems by collecting all the necessary data and information and interpret them to get

the effective result. It is used by the organization to track the company transaction and manage

them to get effective result. A good financial governance reflects that the company used the data

and information according to the government rules and regulations (Berger, Imbierowicz and

Rauch, 2016). A sound financial governance help to prepare the effective budget plan, models

and help to forecast the financial position to take effective measures. It helps to ensure that the

collected data and information are accurate and accountable.

CONCLUSION

The study on management accounting summarizes the impact and role of MA in the

company and the requirement of various types of accounting system to monitor and control the

accounting activities. Different management accounting reports are used to record the financial

and non financial data to keep the information in accounts and provide the information to the

users to take the decision which are beneficial to the firm. It can also be concluded that the

different planning tools help the company to control the budget and take effective advantages.

KPI, benchmarking system and variance analysis is used to measure the financial problems and

financial governance is used to resolve the financial problem related to the revenue, profit and

expenses of the company.

10

manage the activities, inventories and cost of the firm to get the successful results.

Resolve financial problems

Financial governance : It refers to the process of collecting, monitoring, managing and

controlling the financial problems. Financial governance provide a framework to resolve the

financial problems by collecting all the necessary data and information and interpret them to get

the effective result. It is used by the organization to track the company transaction and manage

them to get effective result. A good financial governance reflects that the company used the data

and information according to the government rules and regulations (Berger, Imbierowicz and

Rauch, 2016). A sound financial governance help to prepare the effective budget plan, models

and help to forecast the financial position to take effective measures. It helps to ensure that the

collected data and information are accurate and accountable.

CONCLUSION

The study on management accounting summarizes the impact and role of MA in the

company and the requirement of various types of accounting system to monitor and control the

accounting activities. Different management accounting reports are used to record the financial

and non financial data to keep the information in accounts and provide the information to the

users to take the decision which are beneficial to the firm. It can also be concluded that the

different planning tools help the company to control the budget and take effective advantages.

KPI, benchmarking system and variance analysis is used to measure the financial problems and

financial governance is used to resolve the financial problem related to the revenue, profit and

expenses of the company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.