Accounting Journal Entries: Depreciation, Impairment, and Revaluation

VerifiedAdded on 2023/01/06

|4

|367

|97

Homework Assignment

AI Summary

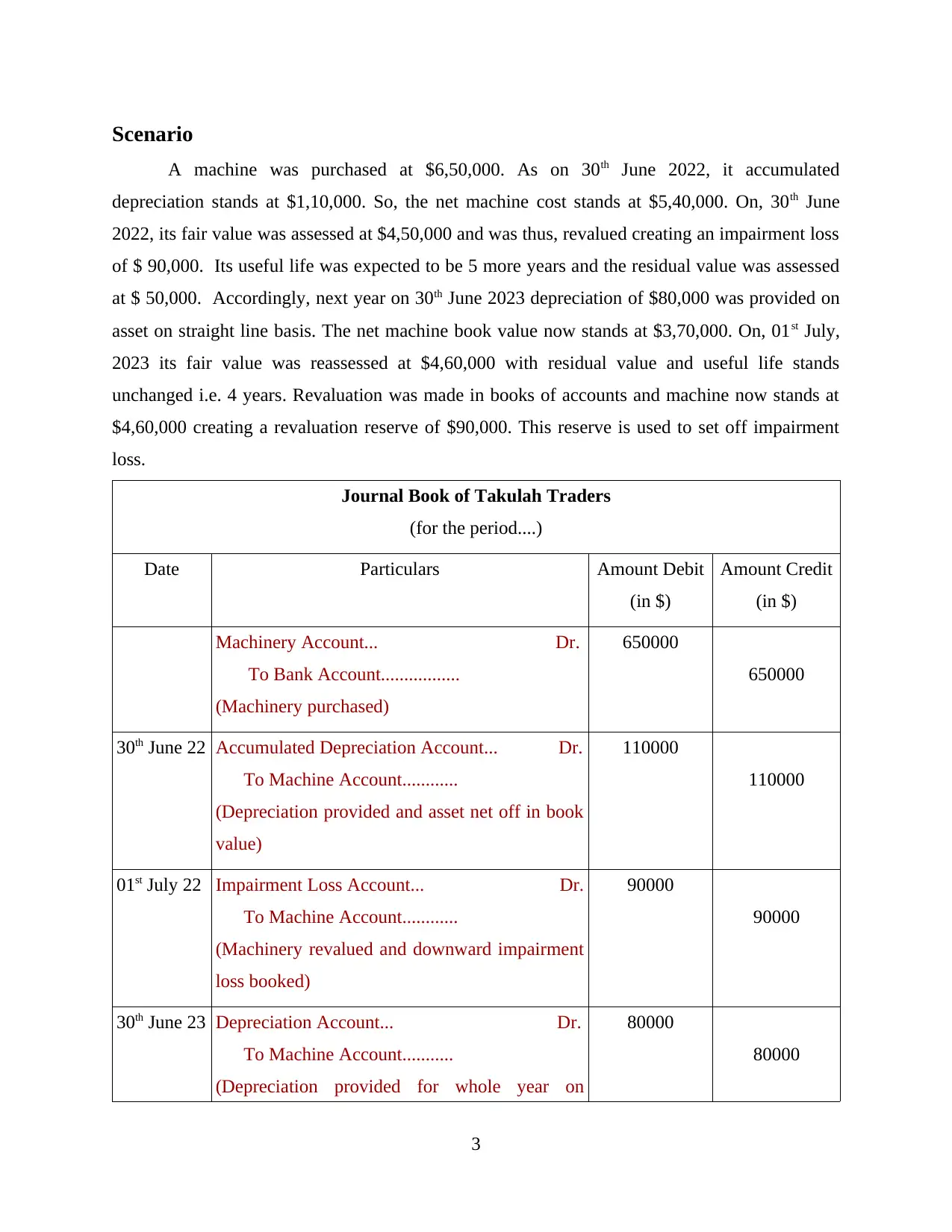

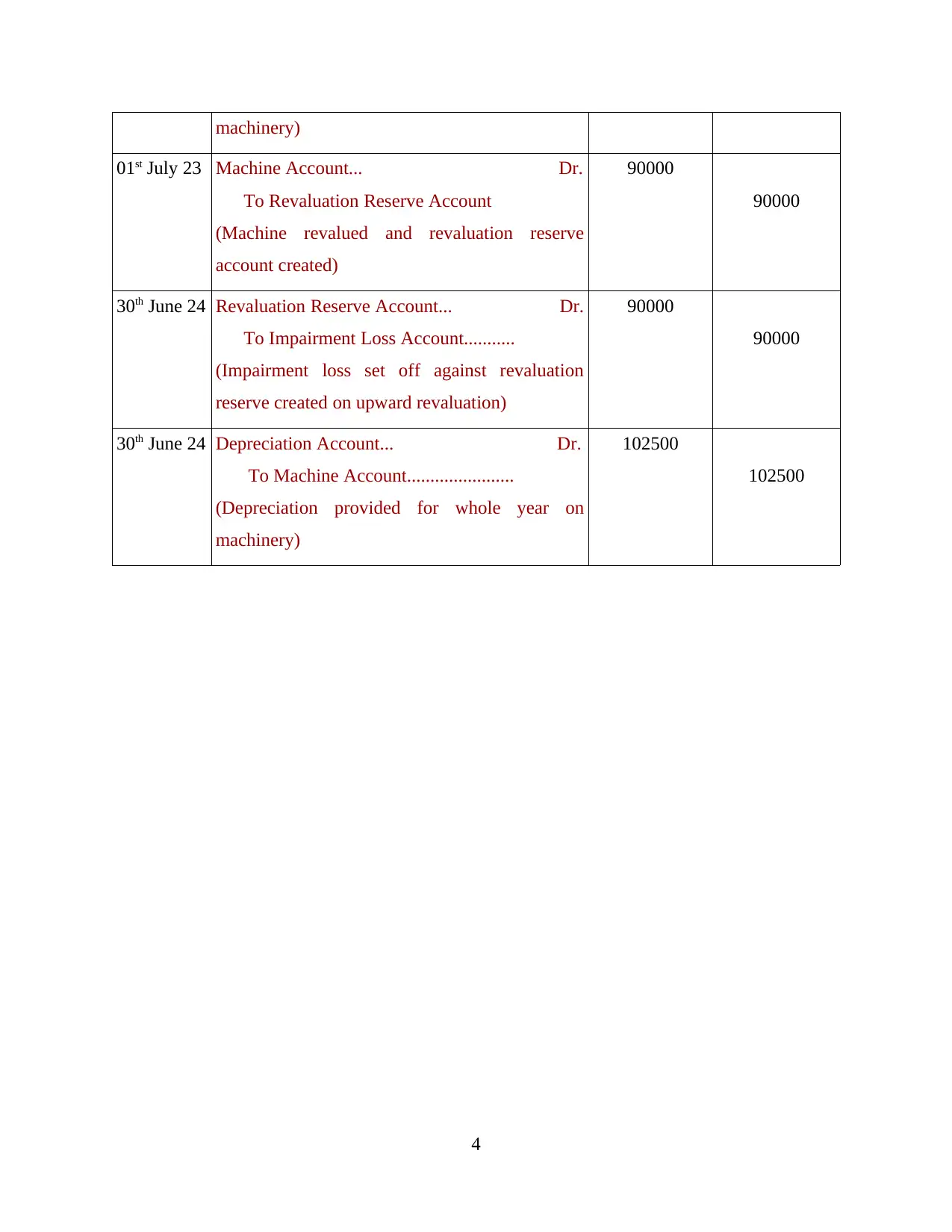

This assignment focuses on the accounting treatment of asset valuation, specifically covering journal entries for depreciation, impairment losses, and revaluation. The solution begins with the initial purchase of a machine and the subsequent recording of accumulated depreciation. It then addresses an impairment loss, followed by the calculation and recording of annual depreciation using the straight-line method. The assignment further illustrates the revaluation of the asset, creating a revaluation reserve. The solution details the process of setting off the impairment loss against the revaluation reserve, and finally, the calculation and recording of depreciation expense for a subsequent year is provided. The journal entries are clearly presented with debit and credit entries, providing a step-by-step guide to the accounting process.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.