Journal Entries for Giles Cleaning and Lawn Mowing Service - ACCT 5023

VerifiedAdded on 2022/12/15

|29

|3302

|327

Homework Assignment

AI Summary

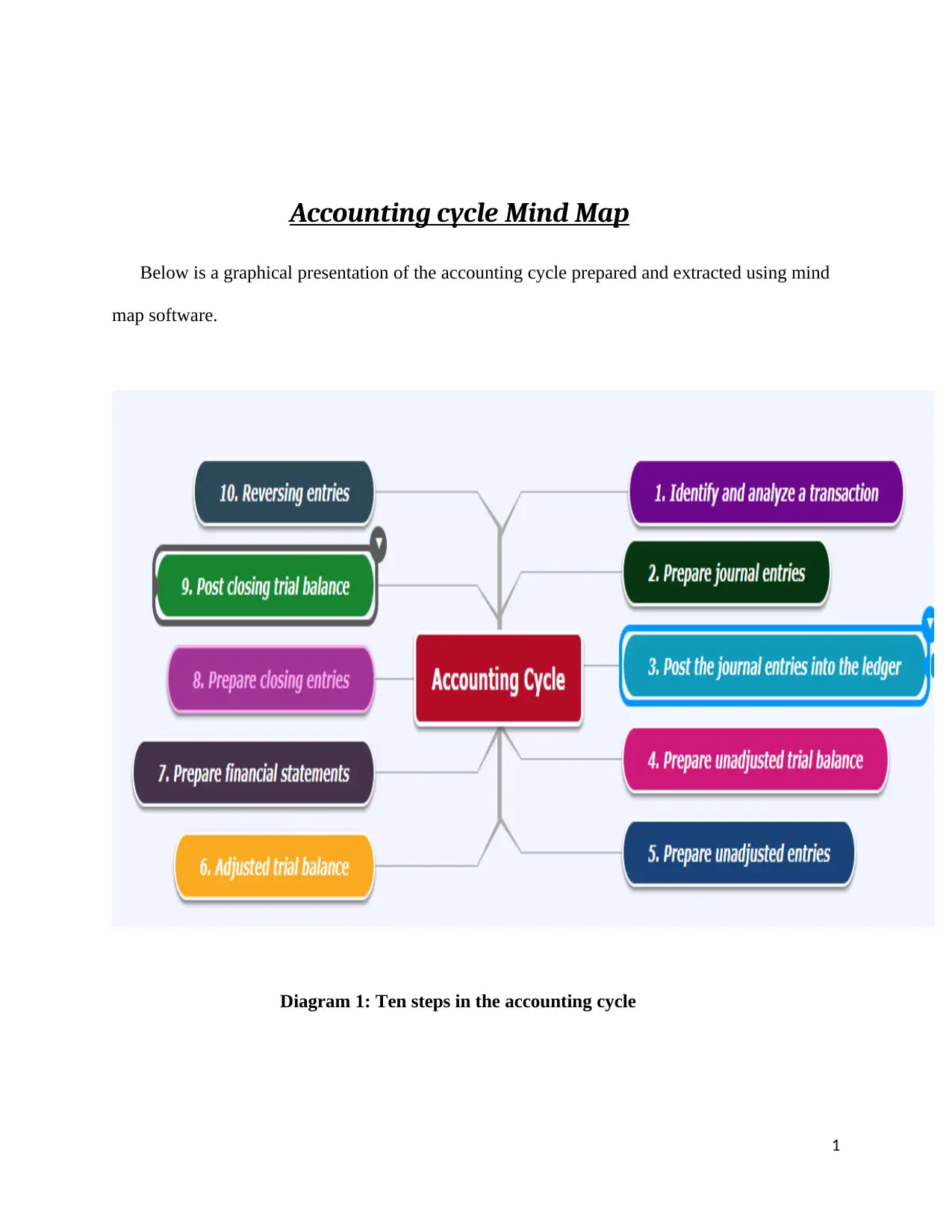

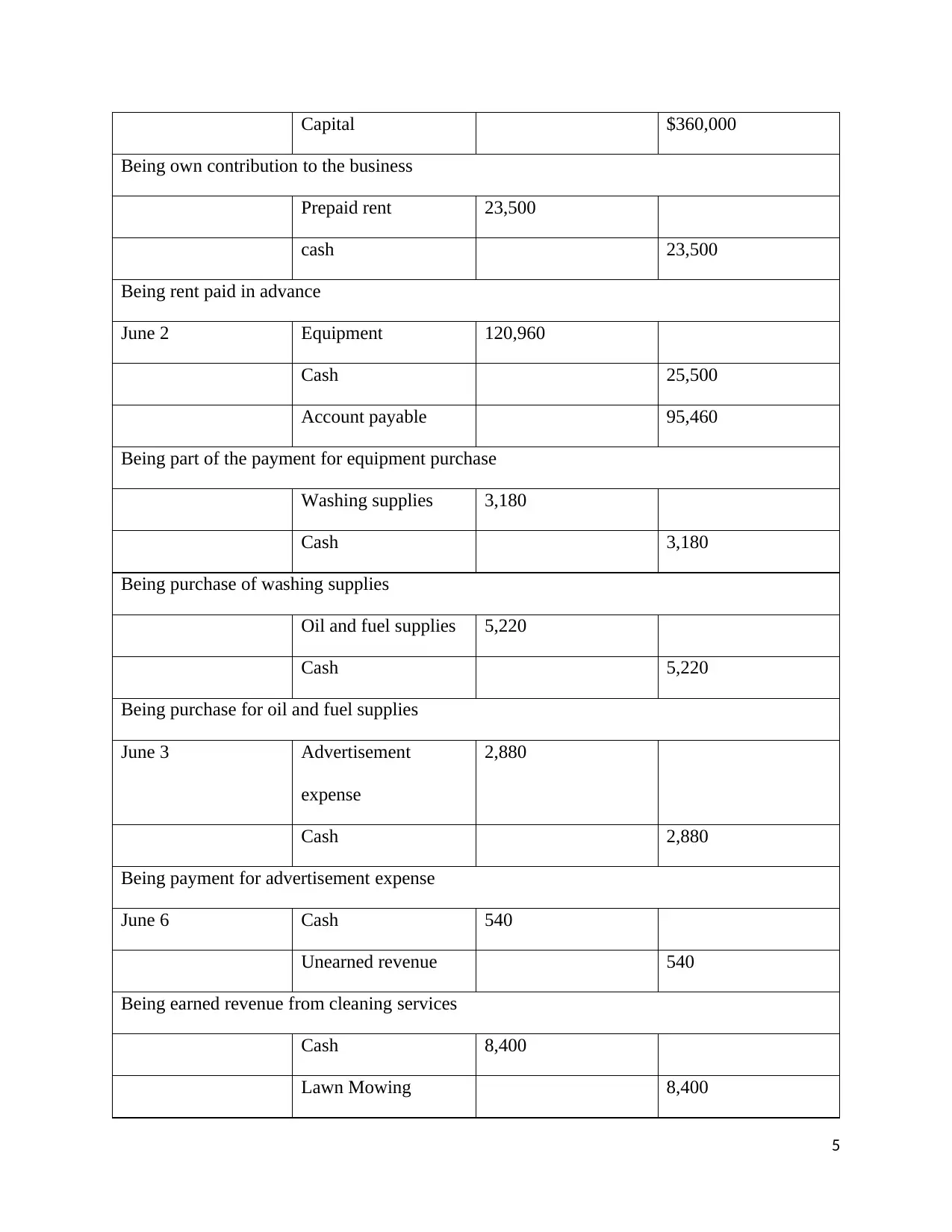

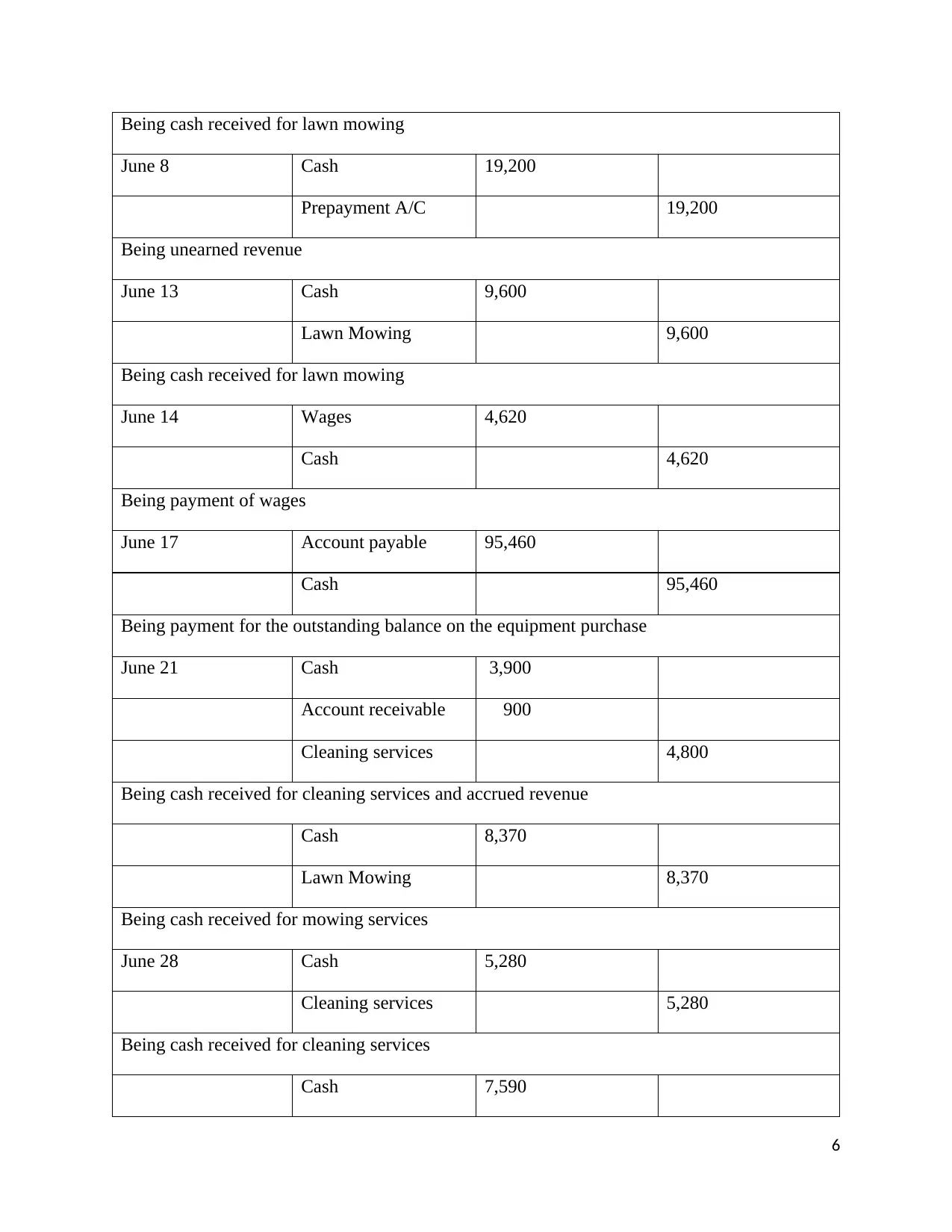

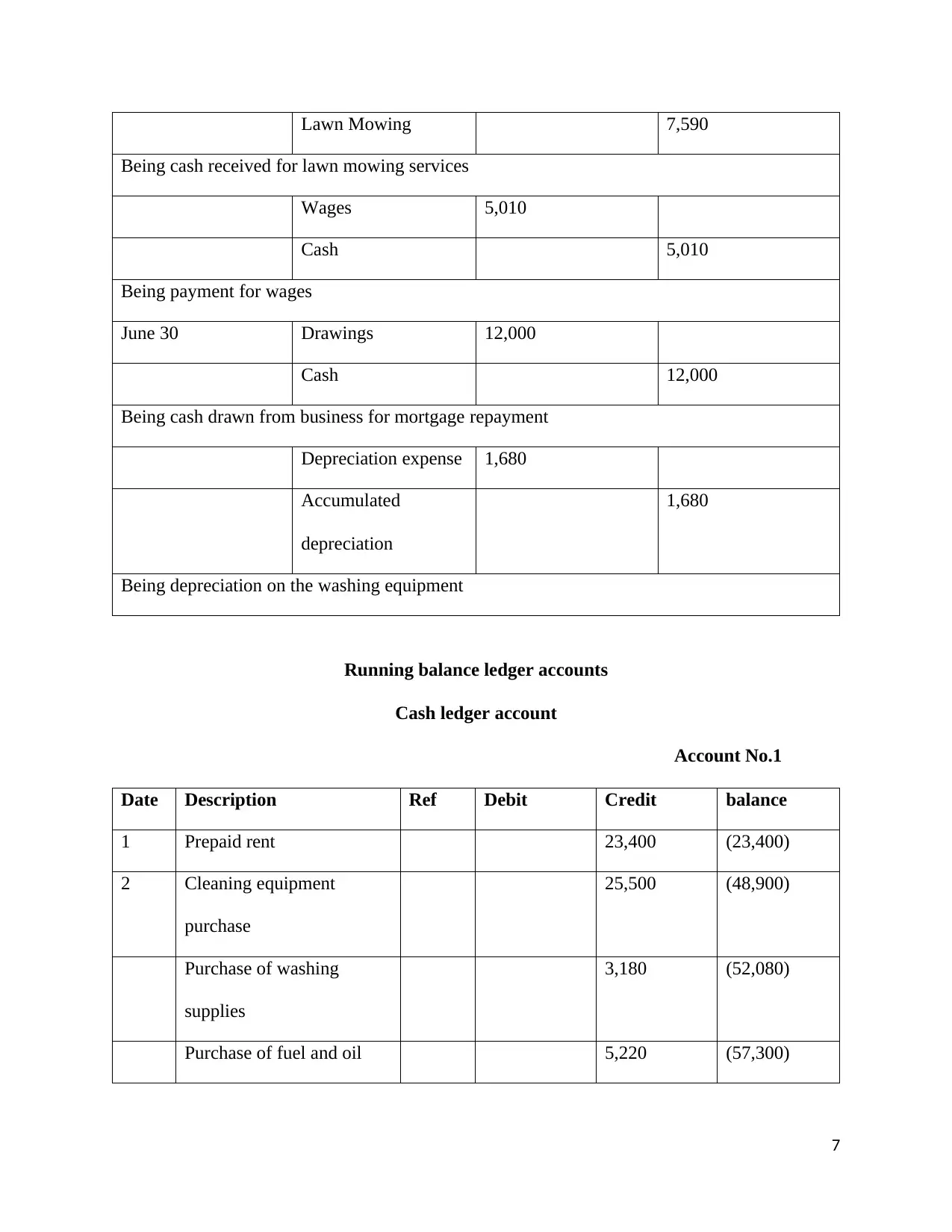

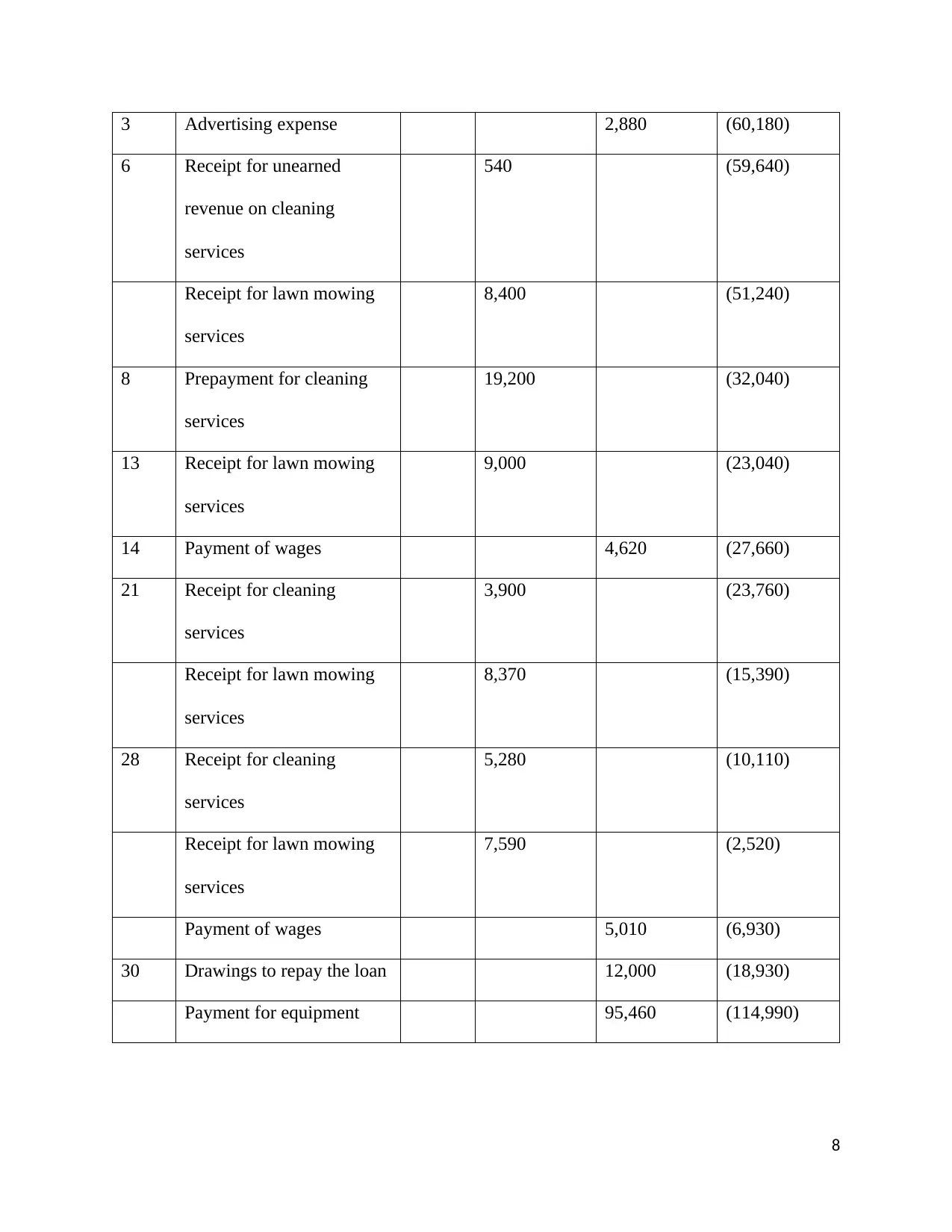

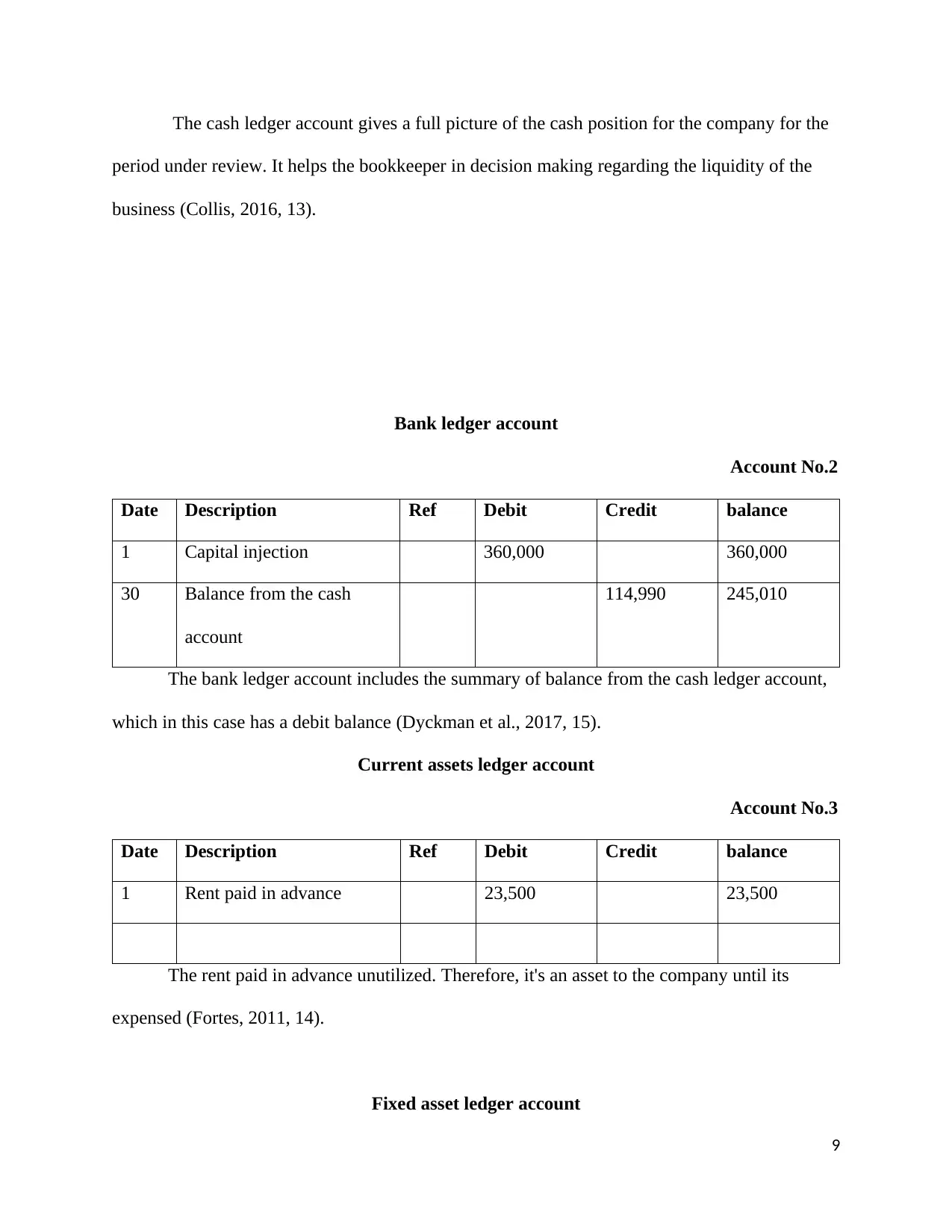

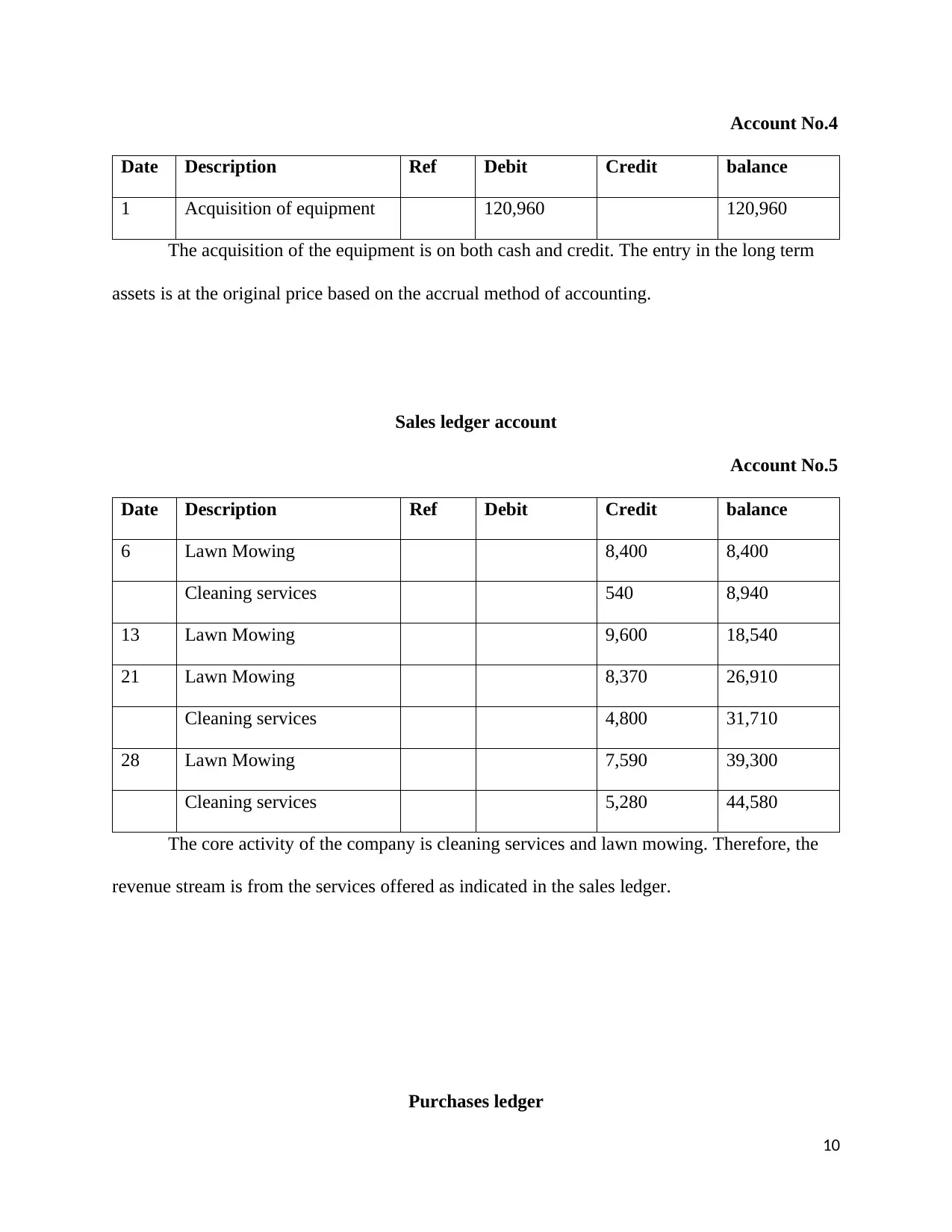

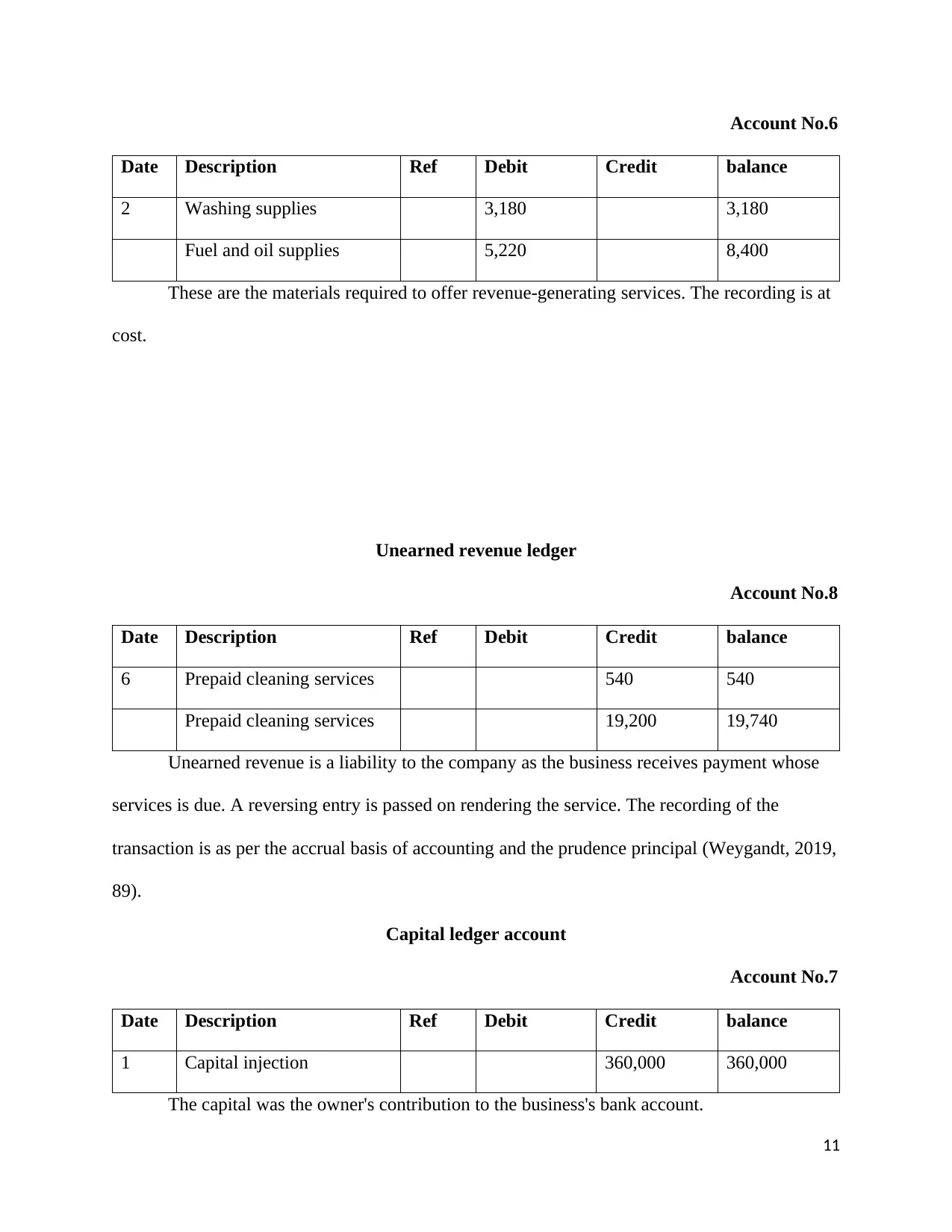

This assignment provides a comprehensive analysis of the accounting cycle for Giles Cleaning and Lawn Mowing Service for June 2019. It meticulously details the journal entries for various transactions, including initial capital contributions, purchases of equipment and supplies, advertising expenses, revenue from cleaning and lawn mowing services, wage payments, and owner drawings. The assignment includes the preparation of cash, bank, current assets, fixed assets, sales, purchases, unearned revenue, and capital ledger accounts. Furthermore, it presents an unadjusted trial balance, adjusting entries for accrued wages, closing stock, and accrued revenues, and an adjusted trial balance. The document also includes closing journal entries, a post-closing trial balance, and a profit and loss account, demonstrating a complete understanding of the accounting cycle.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.