COVID-19 Impact: JPMorgan's Accelerated Digital Transformation

VerifiedAdded on 2023/06/12

|73

|19249

|495

Report

AI Summary

This report investigates the accelerated digital transformation in the banking sector, focusing on JPMorgan Chase's response to the COVID-19 pandemic. It examines the impact of digital technologies on banking processes, customer experiences, and organizational strategies. The study adopts a positivist research philosophy and qualitative methods, drawing data from books, articles, and online resources. Key findings highlight the challenges posed by the pandemic and JPMorgan's successful implementation of digital solutions to maintain efficiency and customer loyalty. The report recommends that banks invest in technology, innovation, and data-driven strategies, while also embracing emerging technologies like AI, machine learning, and cloud computing. Emphasis is placed on security best practices to ensure continuous and secure business outcomes, ultimately enhancing digital customer experiences and competitive advantage. Desklib provides access to similar reports and study tools.

An Accelerated Digital Transformation in the Banking

Sector: Propelled by COVID 19

- A Study on JPMorgan

Master of Science in Digital Business

PLAGIARISM STATEMENT

Based on my study and research, I certify that this project is my work. I have

acknowledged all materials and sources used in its preparation, whether books, articles, reports,

lecture notes, and all other kind of documents, electronic or personal communication. I also

certify that this project has not previously been submitted for assessment in any other unit,

except where specific permission has been granted from all unit coordinators involved, or at any

1

Sector: Propelled by COVID 19

- A Study on JPMorgan

Master of Science in Digital Business

PLAGIARISM STATEMENT

Based on my study and research, I certify that this project is my work. I have

acknowledged all materials and sources used in its preparation, whether books, articles, reports,

lecture notes, and all other kind of documents, electronic or personal communication. I also

certify that this project has not previously been submitted for assessment in any other unit,

except where specific permission has been granted from all unit coordinators involved, or at any

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

additional time in this unit, and that I have not copied in part or whole or otherwise plagiarized

the works of other students or persons.

Name: David Sodeinde Date:

Signature:

ABSTRACT

Globalization and rapid technological advancement have altered a lot of processes and

services across the world. Increasingly, in many sectors of the state, traditional processes are

giving way to digital processes and transformation in production cycle and customer

relationship, particularly in service delivery. This research was conducted to investigate the

2

the works of other students or persons.

Name: David Sodeinde Date:

Signature:

ABSTRACT

Globalization and rapid technological advancement have altered a lot of processes and

services across the world. Increasingly, in many sectors of the state, traditional processes are

giving way to digital processes and transformation in production cycle and customer

relationship, particularly in service delivery. This research was conducted to investigate the

2

effectiveness of digital transformation and how this can assist banks in making further decisions

that drive transformational changes for efficient services on both customers and banks.

The positivist research philosophy was adopted because the study used the qualitative

method to provide theoretical and reliable information related to a particular subject area. Data

for the study was generated from information on relevant topics around the subject through

sources such as books, articles, journals, and relevant online materials.

The study found that the global COVID-19 pandemic created a challenge for the banking

sector especially in carrying out efficient services to customers. It was also found that JPMorgan

Chase Bank underwent a significant level of digital transformation of its services to its customers

in order to remain efficient and retain customers’ trust and loyalty. The study therefore

recommended that businesses should invest in technologies, innovations, processes, data,

applications, and workforce as well as customers. Banks should be committed to digital

strategies through projects, planning, innovations, optimization, directing, adoption of

business/technology models, and communication between business and IT stakeholders, which

would improve efficiency and boast service delivery.

It was recommended that JPMorgan Chase Bank, alongside other banks should explore

more IT-driven innovative technologies such as AI, orchestration, machine learning, mobility,

integration, analytics and intelligence, open banking APIs, cloud computing, robotics, and

automation. In addition, the adoption of security best practices, frameworks, and standards from

National Institute of Standards and Technology (NIST) and ISO 27001, amongst others, should

continually be matured to operationalise a continuous, successful, predictive, and secured

business outcome. These capabilities will elevate digital customer experiences at a speed and

scale, and distinctions will be made amongst banks during and beyond the covid-19 pandemic.

TABLE OF CONTENT

CHAPTER ONE: INTRODUCTION...................................................................................................................5

1.1 Research Background........................................................................................................................5

1.2 Research Rationale............................................................................................................................7

1.3 Research Aim.....................................................................................................................................8

1.4 Research Objectives...........................................................................................................................8

3

that drive transformational changes for efficient services on both customers and banks.

The positivist research philosophy was adopted because the study used the qualitative

method to provide theoretical and reliable information related to a particular subject area. Data

for the study was generated from information on relevant topics around the subject through

sources such as books, articles, journals, and relevant online materials.

The study found that the global COVID-19 pandemic created a challenge for the banking

sector especially in carrying out efficient services to customers. It was also found that JPMorgan

Chase Bank underwent a significant level of digital transformation of its services to its customers

in order to remain efficient and retain customers’ trust and loyalty. The study therefore

recommended that businesses should invest in technologies, innovations, processes, data,

applications, and workforce as well as customers. Banks should be committed to digital

strategies through projects, planning, innovations, optimization, directing, adoption of

business/technology models, and communication between business and IT stakeholders, which

would improve efficiency and boast service delivery.

It was recommended that JPMorgan Chase Bank, alongside other banks should explore

more IT-driven innovative technologies such as AI, orchestration, machine learning, mobility,

integration, analytics and intelligence, open banking APIs, cloud computing, robotics, and

automation. In addition, the adoption of security best practices, frameworks, and standards from

National Institute of Standards and Technology (NIST) and ISO 27001, amongst others, should

continually be matured to operationalise a continuous, successful, predictive, and secured

business outcome. These capabilities will elevate digital customer experiences at a speed and

scale, and distinctions will be made amongst banks during and beyond the covid-19 pandemic.

TABLE OF CONTENT

CHAPTER ONE: INTRODUCTION...................................................................................................................5

1.1 Research Background........................................................................................................................5

1.2 Research Rationale............................................................................................................................7

1.3 Research Aim.....................................................................................................................................8

1.4 Research Objectives...........................................................................................................................8

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.5 Research Questions...........................................................................................................................8

CHAPTER TWO: LITERATURE REVIEW..........................................................................................................9

2.1 Impact of the Digital Transformation on the Banks and People during COVID-19 Pandemic............9

2.2 Different Perceptions of Banking Organizations regarding the Shift toward Digital Transformation

...............................................................................................................................................................17

2.3 Effective Ways to Implement Features of Digital Transformation in the Financial Sector...............24

CHAPTER THREE: METHODOLOGY.............................................................................................................28

3.1 Introduction.....................................................................................................................................28

3.2 Research Philosophy........................................................................................................................28

3.3 Research Approach..........................................................................................................................29

3.4 Research Choice...............................................................................................................................29

3.5 Research Strategy............................................................................................................................29

3.6 Data collection methods..................................................................................................................30

3.7 Sampling..........................................................................................................................................32

3.8 Data Analysis....................................................................................................................................33

3.10 Ethical Considerations....................................................................................................................34

CHAPTER FOUR: RESULT AND DISCUSSION...............................................................................................35

4.1 Introduction.....................................................................................................................................35

4.2 Statistical analysis of closed-ended questions.................................................................................35

4.2.1 Frequency Table........................................................................................................................35

4.2.2 non-statistical analysis of open-ended questions.....................................................................43

4.3 Discussion........................................................................................................................................44

4.3.1 Impact of digital transformation on banks and people during COVID-19.................................44

4.3.2 Different perceptions of banking organizations towards digital transformation......................46

4.3.3 Effective ways to implement the features of digital transformation in the financial sector.....47

CHAPTER FIVE: CONCLUSION AND RECOMMENDATION...........................................................................50

5.1 Conclusion.......................................................................................................................................50

5.2 Recommendations...........................................................................................................................52

5.3 Evaluation of study and scope.........................................................................................................55

5.4 Further Research Areas....................................................................................................................56

REFERENCES..............................................................................................................................................57

APPENDIX..................................................................................................................................................63

Ethics form Taught-Ethics-Application-Form-SBS..................................................................................63

Close-ended questions...........................................................................................................................71

4

CHAPTER TWO: LITERATURE REVIEW..........................................................................................................9

2.1 Impact of the Digital Transformation on the Banks and People during COVID-19 Pandemic............9

2.2 Different Perceptions of Banking Organizations regarding the Shift toward Digital Transformation

...............................................................................................................................................................17

2.3 Effective Ways to Implement Features of Digital Transformation in the Financial Sector...............24

CHAPTER THREE: METHODOLOGY.............................................................................................................28

3.1 Introduction.....................................................................................................................................28

3.2 Research Philosophy........................................................................................................................28

3.3 Research Approach..........................................................................................................................29

3.4 Research Choice...............................................................................................................................29

3.5 Research Strategy............................................................................................................................29

3.6 Data collection methods..................................................................................................................30

3.7 Sampling..........................................................................................................................................32

3.8 Data Analysis....................................................................................................................................33

3.10 Ethical Considerations....................................................................................................................34

CHAPTER FOUR: RESULT AND DISCUSSION...............................................................................................35

4.1 Introduction.....................................................................................................................................35

4.2 Statistical analysis of closed-ended questions.................................................................................35

4.2.1 Frequency Table........................................................................................................................35

4.2.2 non-statistical analysis of open-ended questions.....................................................................43

4.3 Discussion........................................................................................................................................44

4.3.1 Impact of digital transformation on banks and people during COVID-19.................................44

4.3.2 Different perceptions of banking organizations towards digital transformation......................46

4.3.3 Effective ways to implement the features of digital transformation in the financial sector.....47

CHAPTER FIVE: CONCLUSION AND RECOMMENDATION...........................................................................50

5.1 Conclusion.......................................................................................................................................50

5.2 Recommendations...........................................................................................................................52

5.3 Evaluation of study and scope.........................................................................................................55

5.4 Further Research Areas....................................................................................................................56

REFERENCES..............................................................................................................................................57

APPENDIX..................................................................................................................................................63

Ethics form Taught-Ethics-Application-Form-SBS..................................................................................63

Close-ended questions...........................................................................................................................71

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CHAPTER ONE: INTRODUCTION

1.1 Research Background

Digital transformation is fundamentally the process of leveraging digital technologies to

develop or change existing cultures, processes, and customer experiences (Haralayya, 2021). It

helps in modifying businesses and meeting the needs of the market. Digital transformation is

directly linked with the implementation of digital technology within an organization to improve

business and innovation and create value for the consumers (Nguyen, 2020). It is all about

evolving the industry through experimenting with advanced technologies and rethinking the

existing problem-solving approaches (Ananda, Devesh, and Al Lawati, 2020). Organizations use

digital technologies to improve their end-user experience (Czerwińska et al., 2021) by leveraging

artificial intelligence (AI), improving on-demand services among others.

5

1.1 Research Background

Digital transformation is fundamentally the process of leveraging digital technologies to

develop or change existing cultures, processes, and customer experiences (Haralayya, 2021). It

helps in modifying businesses and meeting the needs of the market. Digital transformation is

directly linked with the implementation of digital technology within an organization to improve

business and innovation and create value for the consumers (Nguyen, 2020). It is all about

evolving the industry through experimenting with advanced technologies and rethinking the

existing problem-solving approaches (Ananda, Devesh, and Al Lawati, 2020). Organizations use

digital technologies to improve their end-user experience (Czerwińska et al., 2021) by leveraging

artificial intelligence (AI), improving on-demand services among others.

5

The financial sector is essential as it mobilizes savings and allots credit across time and

space (Kaur et al., 2021). Moreover, it reduces the risks and costs of developing services and

products and makes necessary contributions for enhancing the living standards. Development in

the financial industry extends beyond financial intermediation and infrastructures, requiring

comprehensive regulatory and supervisory procedures for all the major businesses. Recently,

financial institutions have had to monitor and deal with the impact of the COVID-19 pandemic

focusing on understanding the challenges to economies and societies and their long-term

influence on the financial system. They have mainly considered experts to assist them regarding

banking for making better decisions. (Das, 2020).

In the financial sector, digital transformation is simply a conception that has successfully

become a part of business strategy. It is helpful in financial management, accounting, and

compliance management to reduce human errors involved in the financial sector's risk

management by introducing robust digital strategies (Haralayya, 2021). In the financial industry,

digital transformation has improved the customer's and employees' experiences by helping meet

the deadlines and conducting cost-effective operations. From branch offices to mobile

applications and ATMs, digital transformation provides more convenience and a better

experience; in fact, consumers are gravitating more and more towards obtaining a compelling

digital experience (Dermine, 2016).

COVID-19 pandemic has reshaped the way banks interact with their customers, most

notably in the United States. With more financial institutions than any other country in the

European Union and total market size, most banks in the US are continually innovating to meet

digitization expectations for their customers (Demirgüç-Kunt, Pedraza, and Ruiz-Ortega, 2021).

The result is an enhanced banking experience, accelerating day by day due to the closing down

of bank branches during the pandemic. Although this was evident in banking even before the

epidemic hit, new and more effective innovating strategies were highly required due to COVID-

19 restrictions, lockdown and other social distancing regulations (Kaur et al., 2021).

Clients’ banking expectations were notably accelerated during the development of these

innovative and even disruptive technologies, with the growth of customized services of

significant technology companies (Melnychenko, Volosovych, and Baraniuk, 2020). On the

6

space (Kaur et al., 2021). Moreover, it reduces the risks and costs of developing services and

products and makes necessary contributions for enhancing the living standards. Development in

the financial industry extends beyond financial intermediation and infrastructures, requiring

comprehensive regulatory and supervisory procedures for all the major businesses. Recently,

financial institutions have had to monitor and deal with the impact of the COVID-19 pandemic

focusing on understanding the challenges to economies and societies and their long-term

influence on the financial system. They have mainly considered experts to assist them regarding

banking for making better decisions. (Das, 2020).

In the financial sector, digital transformation is simply a conception that has successfully

become a part of business strategy. It is helpful in financial management, accounting, and

compliance management to reduce human errors involved in the financial sector's risk

management by introducing robust digital strategies (Haralayya, 2021). In the financial industry,

digital transformation has improved the customer's and employees' experiences by helping meet

the deadlines and conducting cost-effective operations. From branch offices to mobile

applications and ATMs, digital transformation provides more convenience and a better

experience; in fact, consumers are gravitating more and more towards obtaining a compelling

digital experience (Dermine, 2016).

COVID-19 pandemic has reshaped the way banks interact with their customers, most

notably in the United States. With more financial institutions than any other country in the

European Union and total market size, most banks in the US are continually innovating to meet

digitization expectations for their customers (Demirgüç-Kunt, Pedraza, and Ruiz-Ortega, 2021).

The result is an enhanced banking experience, accelerating day by day due to the closing down

of bank branches during the pandemic. Although this was evident in banking even before the

epidemic hit, new and more effective innovating strategies were highly required due to COVID-

19 restrictions, lockdown and other social distancing regulations (Kaur et al., 2021).

Clients’ banking expectations were notably accelerated during the development of these

innovative and even disruptive technologies, with the growth of customized services of

significant technology companies (Melnychenko, Volosovych, and Baraniuk, 2020). On the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

other hand, the extent to which all the banks are offering effective services and maintaining

relevance to the consumers is vital (Etembekov, 2021).

The digitalizing process of banking is also prone to a few system errors, where high

response rates to customer service inquiries are also of great concern and quick loan

distributions. Providing a faultless payment system is necessary as the COVID-19 pandemic has

accelerated branchless banking, mobile banking, and the need to make society cashless (Sonand

et al., 2020). All over the world, more than 55% of the banks are getting into partnerships with

Fintech to provide additional and better services to the clients, such as facilitating on-boarding,

spending on analytics, and others (Disemadi and Shaleh, 2020).

Digitalization mainly tends towards using the overarching term that spans different

dimensions and bank value chain activities (Nguyen, Nguyen, and Nguyen, 2020). The digital

transformation in banking effectively provides a better and timesaving banking experience to

customers, as they can make safe and more accessible payment transactions anywhere and

anytime (Fairooz and Wickramasinghe, 2019).

1.2 Research Rationale

The rationale behind conducting this investigation is to examine the effectiveness of

digital transformation and how this can assist people and all other commercial paradigms,

especially the financial sector during this global pandemic.

Due to the COVID-19 pandemic, people faced the issue of making payments and

transferring money remotely (Harvey, 2016). In banking, digital transformation has been

embraced by banks of all sizes scrambling to implement advanced technologies, entailing

cutting-edge innovations such as AI integration in customer support helplines and broader

spectrums and platforms for sending and receiving money within seconds; a shift that has led to

the provision of digital and online services through several backend modifications needed to

support the transformation.

This investigation has therefore been conducted in both personal and professional

contexts. In the personal context, the study critically examines the digital transformation

employed in the banking sector during the pandemic to help enhance researchers' knowledge

7

relevance to the consumers is vital (Etembekov, 2021).

The digitalizing process of banking is also prone to a few system errors, where high

response rates to customer service inquiries are also of great concern and quick loan

distributions. Providing a faultless payment system is necessary as the COVID-19 pandemic has

accelerated branchless banking, mobile banking, and the need to make society cashless (Sonand

et al., 2020). All over the world, more than 55% of the banks are getting into partnerships with

Fintech to provide additional and better services to the clients, such as facilitating on-boarding,

spending on analytics, and others (Disemadi and Shaleh, 2020).

Digitalization mainly tends towards using the overarching term that spans different

dimensions and bank value chain activities (Nguyen, Nguyen, and Nguyen, 2020). The digital

transformation in banking effectively provides a better and timesaving banking experience to

customers, as they can make safe and more accessible payment transactions anywhere and

anytime (Fairooz and Wickramasinghe, 2019).

1.2 Research Rationale

The rationale behind conducting this investigation is to examine the effectiveness of

digital transformation and how this can assist people and all other commercial paradigms,

especially the financial sector during this global pandemic.

Due to the COVID-19 pandemic, people faced the issue of making payments and

transferring money remotely (Harvey, 2016). In banking, digital transformation has been

embraced by banks of all sizes scrambling to implement advanced technologies, entailing

cutting-edge innovations such as AI integration in customer support helplines and broader

spectrums and platforms for sending and receiving money within seconds; a shift that has led to

the provision of digital and online services through several backend modifications needed to

support the transformation.

This investigation has therefore been conducted in both personal and professional

contexts. In the personal context, the study critically examines the digital transformation

employed in the banking sector during the pandemic to help enhance researchers' knowledge

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

regarding digital transformation (Baicu et al., 2020). In the professional context, the study can

help improve an investigator's analytical and research skills.

1.3 Research Aim

This research aims to investigate the effectiveness of digital transformation and how it

can assist people and all other commercial paradigms, especially the financial sector, throughout

this global pandemic.

1.4 Research Objectives

The objectives of this study are to:

Critically evaluate the impact of the digital transformation on banks and people during

the COVID-19 pandemic in the context of the US banking sector.

Investigate different perceptions of banking organizations in terms of the shift towards

digital transformation in the US banking sector.

Identify the challenges of the banks in implementing and aligning with digital

transformations.

Recommend effective ways to implement digital transformation features in the financial

sector in the context of the US banking sector.

1.5 Research Questions

RQ1: What are the benefits of digital transformation for the users?

RQ2: What are the perceptions of banking organizations in the U.S about the shift

towards digital transformation?

RQ3: How is digital transformation of the banking sector in the U.D challenged?

RQ4: In what ways can digital transformation features be more effectively implemented?

1.6 Research Structure

The dissertation is structured as follows:

8

help improve an investigator's analytical and research skills.

1.3 Research Aim

This research aims to investigate the effectiveness of digital transformation and how it

can assist people and all other commercial paradigms, especially the financial sector, throughout

this global pandemic.

1.4 Research Objectives

The objectives of this study are to:

Critically evaluate the impact of the digital transformation on banks and people during

the COVID-19 pandemic in the context of the US banking sector.

Investigate different perceptions of banking organizations in terms of the shift towards

digital transformation in the US banking sector.

Identify the challenges of the banks in implementing and aligning with digital

transformations.

Recommend effective ways to implement digital transformation features in the financial

sector in the context of the US banking sector.

1.5 Research Questions

RQ1: What are the benefits of digital transformation for the users?

RQ2: What are the perceptions of banking organizations in the U.S about the shift

towards digital transformation?

RQ3: How is digital transformation of the banking sector in the U.D challenged?

RQ4: In what ways can digital transformation features be more effectively implemented?

1.6 Research Structure

The dissertation is structured as follows:

8

Introduction: It is the first chapter in the dissertation, containing the background of the study,

the rationale of the research, research aim, research objectives, research questions, and proposed

methodology.

Literature Review: It is the second chapter highlighting the research objectives by considering

secondary sources such as books, journals, articles, as well as scholars. It also involves analysing

the viewpoints of the authors and making critical evaluations.

Methodology: It is the third chapter and contains the different methods such as research

philosophy, research approach, research method, research strategy, data collection method,

sampling, data analysis, and ethical considerations.

Results and Discussion: This chapter is mainly presented logically by considering the figures

and tables, making graphs and forming interpretations to analyse the primary data. The results

are linked to the research objectives and literature review.

Conclusions and Recommendations: This chapter consists of a decision based on the whole

investigation. The determination depends on the outcome. The recommendations are related to

giving suggestions to improve the business in the future. It also consists of the aims, execution

strategies, cost of resources, and benefits.

CHAPTER TWO: LITERATURE REVIEW

2.1 Impact of the Digital Transformation on the Banks and People during COVID-19

Pandemic.

According to Shubenok (2021), digital transformation is described as the up gradation of

the existing processes or introducing new ways of performing business activities that enhance

customers' experience.

In banking, digital transformation is related to several changes performed through the

banks, which are integrated with different Fintech solutions to automate, digitize, and optimize

the process and enhance data safety. It is a phenomenon that arose from information

development and communication technologies (Egala, Boateng & Mensah, 2021).

9

the rationale of the research, research aim, research objectives, research questions, and proposed

methodology.

Literature Review: It is the second chapter highlighting the research objectives by considering

secondary sources such as books, journals, articles, as well as scholars. It also involves analysing

the viewpoints of the authors and making critical evaluations.

Methodology: It is the third chapter and contains the different methods such as research

philosophy, research approach, research method, research strategy, data collection method,

sampling, data analysis, and ethical considerations.

Results and Discussion: This chapter is mainly presented logically by considering the figures

and tables, making graphs and forming interpretations to analyse the primary data. The results

are linked to the research objectives and literature review.

Conclusions and Recommendations: This chapter consists of a decision based on the whole

investigation. The determination depends on the outcome. The recommendations are related to

giving suggestions to improve the business in the future. It also consists of the aims, execution

strategies, cost of resources, and benefits.

CHAPTER TWO: LITERATURE REVIEW

2.1 Impact of the Digital Transformation on the Banks and People during COVID-19

Pandemic.

According to Shubenok (2021), digital transformation is described as the up gradation of

the existing processes or introducing new ways of performing business activities that enhance

customers' experience.

In banking, digital transformation is related to several changes performed through the

banks, which are integrated with different Fintech solutions to automate, digitize, and optimize

the process and enhance data safety. It is a phenomenon that arose from information

development and communication technologies (Egala, Boateng & Mensah, 2021).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Banks are at a competitive edge in digital transformation as digital capacity has

increased, client travel has developed further, and the central banking methods have surpassed

branch offices with mobile services (Kitsios, Giatsidis, and Kamariotou, 2021).

For the banks, digital transformation can be understood as a shift to digitalizing services,

products, and communication channels. Due to the increasing expansion of mobile technologies,

the banking business is now more technologically knowledgeable (Das, 2020).

Although some banking firms have previously delayed mobile app development, this step

has become virtually obligatory especially in the aftermath of the COVID19 pandemic.

The COVID-19 pandemic forced customers and banks to use digital processes and tools

to compensate for the office workspace, call centres, and branch closures. Because of the

closures of physical bank branches due to local and national lockdowns, mobile and online

banking became the primary channels for individuals to interact with banks.

(Disemadi&Shaleh,2020).

With the rise of digital capabilities, customers' journeys have evolved, with mobile

services overtaking the routine visit to bank branches and redefining traditional banking. Banks

use digital technologies to minimize costs in the US and provide better services to customers

(Wewege, Lee and Thomsett, 2020).

Top banks in America have decided not to let global COVID-19 pandemic potential

interfere negatively on their service quality. At the beginning of the pandemic, banks capitalized

on the escalated willingness of customers to consider digital financial services, which was

positive compared to before the pandemic when some banks were providing bafflingly archaic

financial services (Luhach, Jha, and Luhach, 2018).

It is arguable that banks played a vital role in slowing the spread of COVID-19 by

assisting clients in making better and more effective use of remote channels and existing digital

media in managing their budgets, transferring money across bank accounts, making digital

payments, and using government programs. With the spread of the economic fallouts, retail

banks had to deal with more overwhelming and fluid priorities, making repositioning a critical

step to be taken at present and recalibration essential for the future.

10

increased, client travel has developed further, and the central banking methods have surpassed

branch offices with mobile services (Kitsios, Giatsidis, and Kamariotou, 2021).

For the banks, digital transformation can be understood as a shift to digitalizing services,

products, and communication channels. Due to the increasing expansion of mobile technologies,

the banking business is now more technologically knowledgeable (Das, 2020).

Although some banking firms have previously delayed mobile app development, this step

has become virtually obligatory especially in the aftermath of the COVID19 pandemic.

The COVID-19 pandemic forced customers and banks to use digital processes and tools

to compensate for the office workspace, call centres, and branch closures. Because of the

closures of physical bank branches due to local and national lockdowns, mobile and online

banking became the primary channels for individuals to interact with banks.

(Disemadi&Shaleh,2020).

With the rise of digital capabilities, customers' journeys have evolved, with mobile

services overtaking the routine visit to bank branches and redefining traditional banking. Banks

use digital technologies to minimize costs in the US and provide better services to customers

(Wewege, Lee and Thomsett, 2020).

Top banks in America have decided not to let global COVID-19 pandemic potential

interfere negatively on their service quality. At the beginning of the pandemic, banks capitalized

on the escalated willingness of customers to consider digital financial services, which was

positive compared to before the pandemic when some banks were providing bafflingly archaic

financial services (Luhach, Jha, and Luhach, 2018).

It is arguable that banks played a vital role in slowing the spread of COVID-19 by

assisting clients in making better and more effective use of remote channels and existing digital

media in managing their budgets, transferring money across bank accounts, making digital

payments, and using government programs. With the spread of the economic fallouts, retail

banks had to deal with more overwhelming and fluid priorities, making repositioning a critical

step to be taken at present and recalibration essential for the future.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

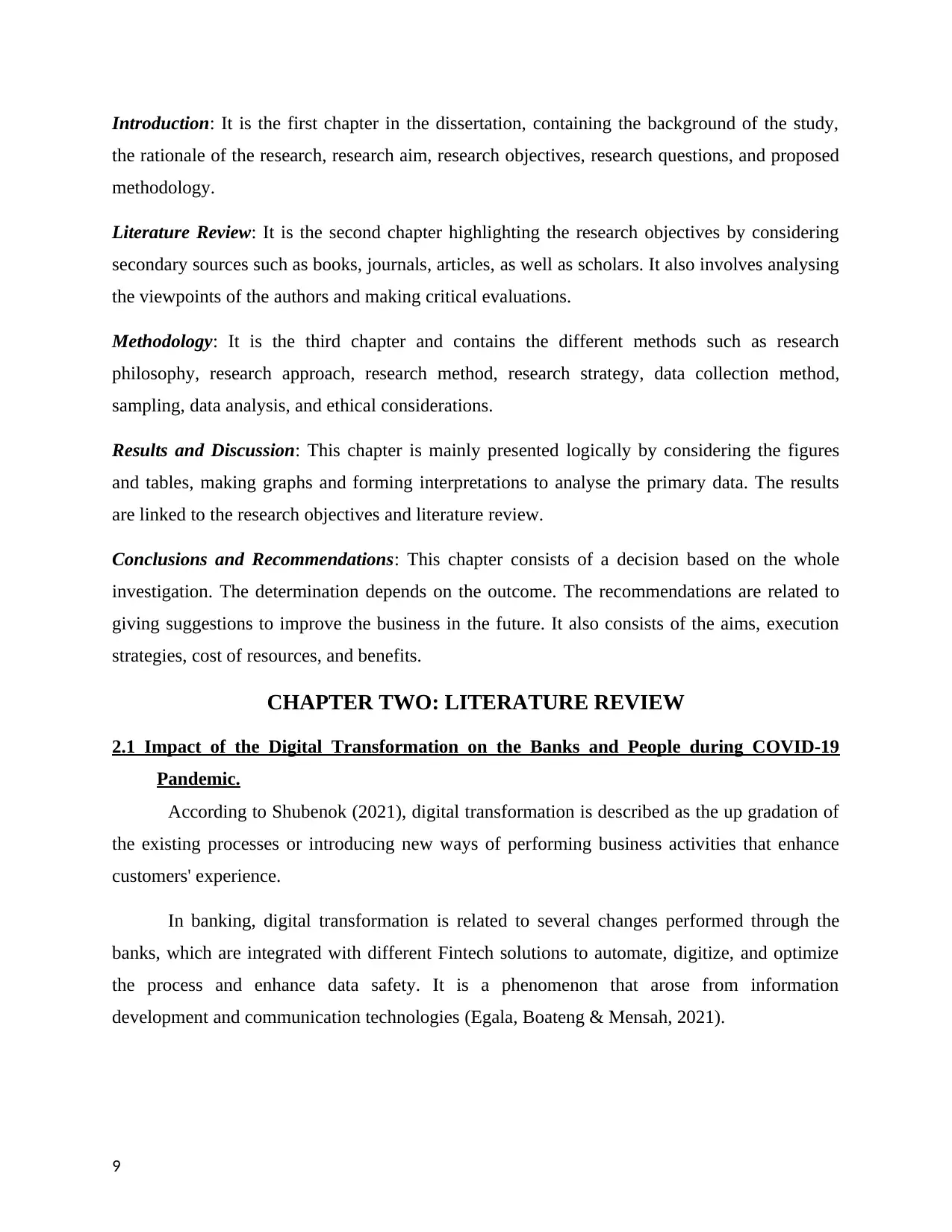

Concerning this, bank operations have continuously monitored circumstances daily while

also focusing on the changing working hours of branches’ operations and closures (Kaur et al.,

2020).

For instance, JPMorgan Chase Bank has temporarily closed around 20% of its

components and minimized staff, only operating their branches in the morning.

Figure 1: Frequency of mobile app usage for deposit product in the year 2019 (%)

(Source: McKinsey Banking Journey Pulse Benchmark)

From the above graph, it is evident that even in the current crisis, there are some actions

that banks can take to assist retail customers as well as some other businesses by using digital

channels so that consumers can make bank-related transactions from home.

In the COVID-19 pandemic, banks in the US focused on developing proactive measures

and strategies to prevent mortality within their workforce due to the COVID-19 virus infections

(Dermine,2016).

Actions taken to reduce the spread of the virus included visiting only through

appointments, maintaining social distancing, keeping doors locked to limit the number of

customers inside, and having no higher than the prescribed number of workers on premises

(Etembekov, 2021).

Digital banking helped in easier transactions, checking account balances, and other

digital devices (Fedotova et al., 2018).

11

also focusing on the changing working hours of branches’ operations and closures (Kaur et al.,

2020).

For instance, JPMorgan Chase Bank has temporarily closed around 20% of its

components and minimized staff, only operating their branches in the morning.

Figure 1: Frequency of mobile app usage for deposit product in the year 2019 (%)

(Source: McKinsey Banking Journey Pulse Benchmark)

From the above graph, it is evident that even in the current crisis, there are some actions

that banks can take to assist retail customers as well as some other businesses by using digital

channels so that consumers can make bank-related transactions from home.

In the COVID-19 pandemic, banks in the US focused on developing proactive measures

and strategies to prevent mortality within their workforce due to the COVID-19 virus infections

(Dermine,2016).

Actions taken to reduce the spread of the virus included visiting only through

appointments, maintaining social distancing, keeping doors locked to limit the number of

customers inside, and having no higher than the prescribed number of workers on premises

(Etembekov, 2021).

Digital banking helped in easier transactions, checking account balances, and other

digital devices (Fedotova et al., 2018).

11

Figure 2: US banks by branches

(Source: COVID nudges US bank customers into digital era)

The pandemic has had a substantial impact on the way individuals make purchases.

Contactless payments rose by 40% globally (Dermine,2016).

The pandemic also motivated the retail banks to speed up digital transformation plans

and promote awareness in the people for using digital banking to make the transactions easily,

transfer money and other bank-related transactions without going to a bank branch. This

exponential trend of a rise in digital activities has opened new and harmonious relationships,

registrations, contactless payments, and mobile applications for payments.

On the other hand, banks can also successfully apply fraud prevention measures for credit

card transactions using AI, real-time data analytics, and User Behaviour analytics (UBA) as

warning systems (Disemadi and Shaleh,2020).

The development of the new innovative technology permits the banks to enhance

customer engagement and offer personalized experiences (Omarini, 2017).

12

(Source: COVID nudges US bank customers into digital era)

The pandemic has had a substantial impact on the way individuals make purchases.

Contactless payments rose by 40% globally (Dermine,2016).

The pandemic also motivated the retail banks to speed up digital transformation plans

and promote awareness in the people for using digital banking to make the transactions easily,

transfer money and other bank-related transactions without going to a bank branch. This

exponential trend of a rise in digital activities has opened new and harmonious relationships,

registrations, contactless payments, and mobile applications for payments.

On the other hand, banks can also successfully apply fraud prevention measures for credit

card transactions using AI, real-time data analytics, and User Behaviour analytics (UBA) as

warning systems (Disemadi and Shaleh,2020).

The development of the new innovative technology permits the banks to enhance

customer engagement and offer personalized experiences (Omarini, 2017).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 73

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.