Detailed Financial Analysis of JP Morgan Chase: Basel III and Crisis

VerifiedAdded on 2020/04/15

|21

|6076

|61

Report

AI Summary

This report offers a detailed analysis of JP Morgan Chase, examining its key contributions to the US financial system. It delves into the problems associated with debt financing, particularly the challenges faced by financial surplus units. The report provides a comprehensive overview of the changes introduced by Basel III regarding capital adequacy, liquidity, and leverage requirements, and assesses their impact on JP Morgan Chase's financial condition. Furthermore, it explores the process of asset securitization and the bank's motivations for engaging in it. Finally, the report analyzes the implications of the 2008 financial crisis on JP Morgan Chase's financial performance, including the measures implemented by the US government to stabilize the markets. The analysis covers critical aspects such as maturity mismatch, size mismatch and high interest rates.

JP Morgan Chase Analysis 1

JP Morgan Chase Analysis

JP Morgan Chase Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

JP Morgan Chase Analysis 2

Table of Contents

Introduction................................................................................................................................3

1. Background of JP Morgan Chase and its two key roles in terms of its contributions to the

US financial system....................................................................................................................3

2. Problems of Debt Finance Provided By Financial Surplus Unit In Comparison to Financial

Deficit Unit.................................................................................................................................4

3. Main Changes to the Capital Adequacy, Liquidity and Leverage Requirements as

Stipulated by Basel III and Impact of such Changes on JP Morgan’s Financial Conditions.....6

4. Asset Securitization and the Reasons Why Different Financial or Banking Institutions

Might Wish to Securitize.........................................................................................................10

5. Implications of the 2008 financial crisis on JP Morgan’s financial performances shortly

after the crisis...........................................................................................................................13

Conclusion................................................................................................................................16

REFERENCES.........................................................................................................................18

Table of Contents

Introduction................................................................................................................................3

1. Background of JP Morgan Chase and its two key roles in terms of its contributions to the

US financial system....................................................................................................................3

2. Problems of Debt Finance Provided By Financial Surplus Unit In Comparison to Financial

Deficit Unit.................................................................................................................................4

3. Main Changes to the Capital Adequacy, Liquidity and Leverage Requirements as

Stipulated by Basel III and Impact of such Changes on JP Morgan’s Financial Conditions.....6

4. Asset Securitization and the Reasons Why Different Financial or Banking Institutions

Might Wish to Securitize.........................................................................................................10

5. Implications of the 2008 financial crisis on JP Morgan’s financial performances shortly

after the crisis...........................................................................................................................13

Conclusion................................................................................................................................16

REFERENCES.........................................................................................................................18

JP Morgan Chase Analysis 3

JP Morgan Chase Analysis

Introduction

The report is about a detailed analysis of JP Morgan Chase. It comprises of a critical

discussion of the key roles this banks plays in contributing to the nation’s financial system. In

addition, it presents some of the problems associated with relying on debt financing provided

by financial institution that is financially surplus compared to the one that is financially

deficit. The report also presents explanations of the main changes to the capital adequacy,

liquidity and leverage requirements as stipulated by Basel III as well as some of the likely

impact of these changes on JP Morgan Chase’s financial conditions. Besides, it presents

explanation of asset securitization process and the reason the bank would wish to securitize.

Finally, it present a detailed discussion of the main implications of the 2008 financial crisis

on JP Morgan Chase’s financial performance shortly after the crisis as well as some of the

measures implemented by the US government to calm its financial markets during that time.

1. Background of JP Morgan Chase and its two key roles in terms of its contributions to

the US financial system

JP Morgan Chase is one of the American multinational financial and banking services firm

based in the New York (JP Morgan, 2016). It is usually amongst the largest financial or

banking institutions across US and sixth largest across the globes by assets with a total assets

of around $2.5 trillion. It is also the second most valuable firm across the world by market

capitalization after commercial and Industrial banks of China (JP Morgan, 2016). In other

words, JP Morgan Chase is one of the main providers of the financial and banking service (JP

Morgan, 2016).

JP Morgan Chase Analysis

Introduction

The report is about a detailed analysis of JP Morgan Chase. It comprises of a critical

discussion of the key roles this banks plays in contributing to the nation’s financial system. In

addition, it presents some of the problems associated with relying on debt financing provided

by financial institution that is financially surplus compared to the one that is financially

deficit. The report also presents explanations of the main changes to the capital adequacy,

liquidity and leverage requirements as stipulated by Basel III as well as some of the likely

impact of these changes on JP Morgan Chase’s financial conditions. Besides, it presents

explanation of asset securitization process and the reason the bank would wish to securitize.

Finally, it present a detailed discussion of the main implications of the 2008 financial crisis

on JP Morgan Chase’s financial performance shortly after the crisis as well as some of the

measures implemented by the US government to calm its financial markets during that time.

1. Background of JP Morgan Chase and its two key roles in terms of its contributions to

the US financial system

JP Morgan Chase is one of the American multinational financial and banking services firm

based in the New York (JP Morgan, 2016). It is usually amongst the largest financial or

banking institutions across US and sixth largest across the globes by assets with a total assets

of around $2.5 trillion. It is also the second most valuable firm across the world by market

capitalization after commercial and Industrial banks of China (JP Morgan, 2016). In other

words, JP Morgan Chase is one of the main providers of the financial and banking service (JP

Morgan, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

JP Morgan Chase Analysis 4

It provides numerous financial and banking services to governmental, institutional and

corporate customers within the US and internationally. Further, it provides non-interest

bearing deposits, savings accounts, interest-bearing time deposits as well as market deposits

(JP Morgan, 2016). In addition, it offers clients loans such as home equity loans, lines of

credits, residential mortgages, business banking loans, auto loans, as well as other loans. In

other words it offers prime mortgage loans, credit card loans, payment option loans as well as

wholesale loans to numerous clients (JP Morgan, 2016).

To be more specific, JP Morgan Chase is the world leader in banking and financial services,

providing solutions to the global most significant governments, institutions and corporations

in over 100 nations (JP Morgan, 2016). In other words, JP Morgan Chase is the largest bank

and chief provider of financial and banking services across US by profit, market value, sales

and assets. It serves over 1 million clients, small enterprises, and many prominent

institutional, governmental and corporate customers (JP Morgan, 2016). It gives around $200

million every year to the non-profit firms across the globe. It also leads volunteer services

events for the personnel in the local communities by using numerous resources including the

one that stem from the access to capital, global reach, economies of scale and expertise. JP

Morgan Chase invests in its partners and communities with the local firms to offer creative

solutions which are said to respond to the neighbourhood development needs. Its leading

expertise and scale assist in reducing environmental risks while producing new opportunities

in order to make more sustainable worldwide economy (JP Morgan, 2016).

2. Critically explained the Problems of Debt Finance Provided by JP Morgan Chase

with those parties who are a Financial Surplus Unit in Comparison to Financial Deficit

Unit

It provides numerous financial and banking services to governmental, institutional and

corporate customers within the US and internationally. Further, it provides non-interest

bearing deposits, savings accounts, interest-bearing time deposits as well as market deposits

(JP Morgan, 2016). In addition, it offers clients loans such as home equity loans, lines of

credits, residential mortgages, business banking loans, auto loans, as well as other loans. In

other words it offers prime mortgage loans, credit card loans, payment option loans as well as

wholesale loans to numerous clients (JP Morgan, 2016).

To be more specific, JP Morgan Chase is the world leader in banking and financial services,

providing solutions to the global most significant governments, institutions and corporations

in over 100 nations (JP Morgan, 2016). In other words, JP Morgan Chase is the largest bank

and chief provider of financial and banking services across US by profit, market value, sales

and assets. It serves over 1 million clients, small enterprises, and many prominent

institutional, governmental and corporate customers (JP Morgan, 2016). It gives around $200

million every year to the non-profit firms across the globe. It also leads volunteer services

events for the personnel in the local communities by using numerous resources including the

one that stem from the access to capital, global reach, economies of scale and expertise. JP

Morgan Chase invests in its partners and communities with the local firms to offer creative

solutions which are said to respond to the neighbourhood development needs. Its leading

expertise and scale assist in reducing environmental risks while producing new opportunities

in order to make more sustainable worldwide economy (JP Morgan, 2016).

2. Critically explained the Problems of Debt Finance Provided by JP Morgan Chase

with those parties who are a Financial Surplus Unit in Comparison to Financial Deficit

Unit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

JP Morgan Chase Analysis 5

Provision of debt finance by JP Morgan Chase to the surplus units as well as deficit units

poses some problems to the bank (Bohn, 1998). For instance, the act of providing debt

finance to financial surplus unit posed numerous issues on maturity mismatch where by it is

forced to provide a loan with minimal or short maturity period. This was hectic to the bank

since given the fact that financial surplus units was having some leverage issues due to the

2008 financial crisis, these units would struggle to meet their short maturity debts obligations

provided by JP Morgan Chase. Such would not occur if the JP Morgan Chase decides to

provide debt to the financial deficit unit that offers long maturity debts (Demetriades &

Andrianova, 2004). In addition, JP Morgan Chase provision of debt finance to financial

surplus unit would be challenging due to size mismatch whereby there are only small funds

available being offered to these banks. For instance, JP Morgan Chase action in providing a

loan to one of the banks in US posed a major problem since it was hectic to get the actual

amount it required to finance its operations as compared to the amount it provided to

financial deficit unit that are large (Demetriades & Andrianova, 2004). In addition, JP

Morgan Chase providing debt finance to units with those parties who are a financial surplus

unit would be hectic since it demands the bank to have as high return as possible (Bohn,

1998). Further, providing debt finance to parties that are financial surplus would be

challenging since it would necessitate the bank to charge relatively high interest rates which

would make the deficit units unable to repay the loans (Bohn, 1998). This would force JP

Morgan Chase to get some collaterals in order to safeguard its loans. Nonetheless, where such

risks are of greater concern, there are other risks involved such as risk of bankruptcy. This

means that if the loans are on fixed rates, the US Fed act of imposing high interest rates

would benefit the depositors but JP Morgan Chase would be forced to strike the balance in

between the returns and risks to remain competitive (Petersen & Wiegelmann, 2014).

Provision of debt finance by JP Morgan Chase to the surplus units as well as deficit units

poses some problems to the bank (Bohn, 1998). For instance, the act of providing debt

finance to financial surplus unit posed numerous issues on maturity mismatch where by it is

forced to provide a loan with minimal or short maturity period. This was hectic to the bank

since given the fact that financial surplus units was having some leverage issues due to the

2008 financial crisis, these units would struggle to meet their short maturity debts obligations

provided by JP Morgan Chase. Such would not occur if the JP Morgan Chase decides to

provide debt to the financial deficit unit that offers long maturity debts (Demetriades &

Andrianova, 2004). In addition, JP Morgan Chase provision of debt finance to financial

surplus unit would be challenging due to size mismatch whereby there are only small funds

available being offered to these banks. For instance, JP Morgan Chase action in providing a

loan to one of the banks in US posed a major problem since it was hectic to get the actual

amount it required to finance its operations as compared to the amount it provided to

financial deficit unit that are large (Demetriades & Andrianova, 2004). In addition, JP

Morgan Chase providing debt finance to units with those parties who are a financial surplus

unit would be hectic since it demands the bank to have as high return as possible (Bohn,

1998). Further, providing debt finance to parties that are financial surplus would be

challenging since it would necessitate the bank to charge relatively high interest rates which

would make the deficit units unable to repay the loans (Bohn, 1998). This would force JP

Morgan Chase to get some collaterals in order to safeguard its loans. Nonetheless, where such

risks are of greater concern, there are other risks involved such as risk of bankruptcy. This

means that if the loans are on fixed rates, the US Fed act of imposing high interest rates

would benefit the depositors but JP Morgan Chase would be forced to strike the balance in

between the returns and risks to remain competitive (Petersen & Wiegelmann, 2014).

JP Morgan Chase Analysis 6

3. Main Changes to the Capital Adequacy, Liquidity and Leverage Requirements as

Stipulated by Basel III and Impact of such Changes on JP Morgan’s Financial

Conditions

Basel III is usually a sequence of measures designed in repairing and augmenting Basel II

accord (Ojo, 2013). This adjunct addresses the issues of the economic pro-cyclicality and

gives suggestions on the means of mitigating such issues through increase in capital charges

when country’s economies overheat as well as when capital charge reduces in the economic

contractions (Kasekende, Bagyenda & Brownbridge, 2011). Basically, the Basel III is far

much stricter and complete than the Basel II. Some of the reforms recommended in the Basel

III include the five facets for enhancing capital, raising quality, transparency and consistency

of capital base, enhancing risk-based capital needs with leverage ratio, enhancing risk

coverage, promoting country-cyclical buffers and reducing pro-cyclicality as well as

addressing interconnectedness and systematic risks (Ojo, 2013). The Basel III comprised of

some measures that are mainly targeted at improving the value and capacity of capital within

the economy, aimed at refining loss-absorption ability in both the liquidation and going

concerns setups. By retaining a minimum capital competence of 8%, Tier 1 was increased to

6% with equity postulated at 4.5% (Jayadev, 2013). These new concepts are for

countercyclical capital bumper and capital conversion bumper which ensured that financial

institutions are capable of absorbing the losses without any breach to the minimum capital

requirements and were capable of carrying their operations even during economic crisis

without deleveraging (Bhowmik, 2014).

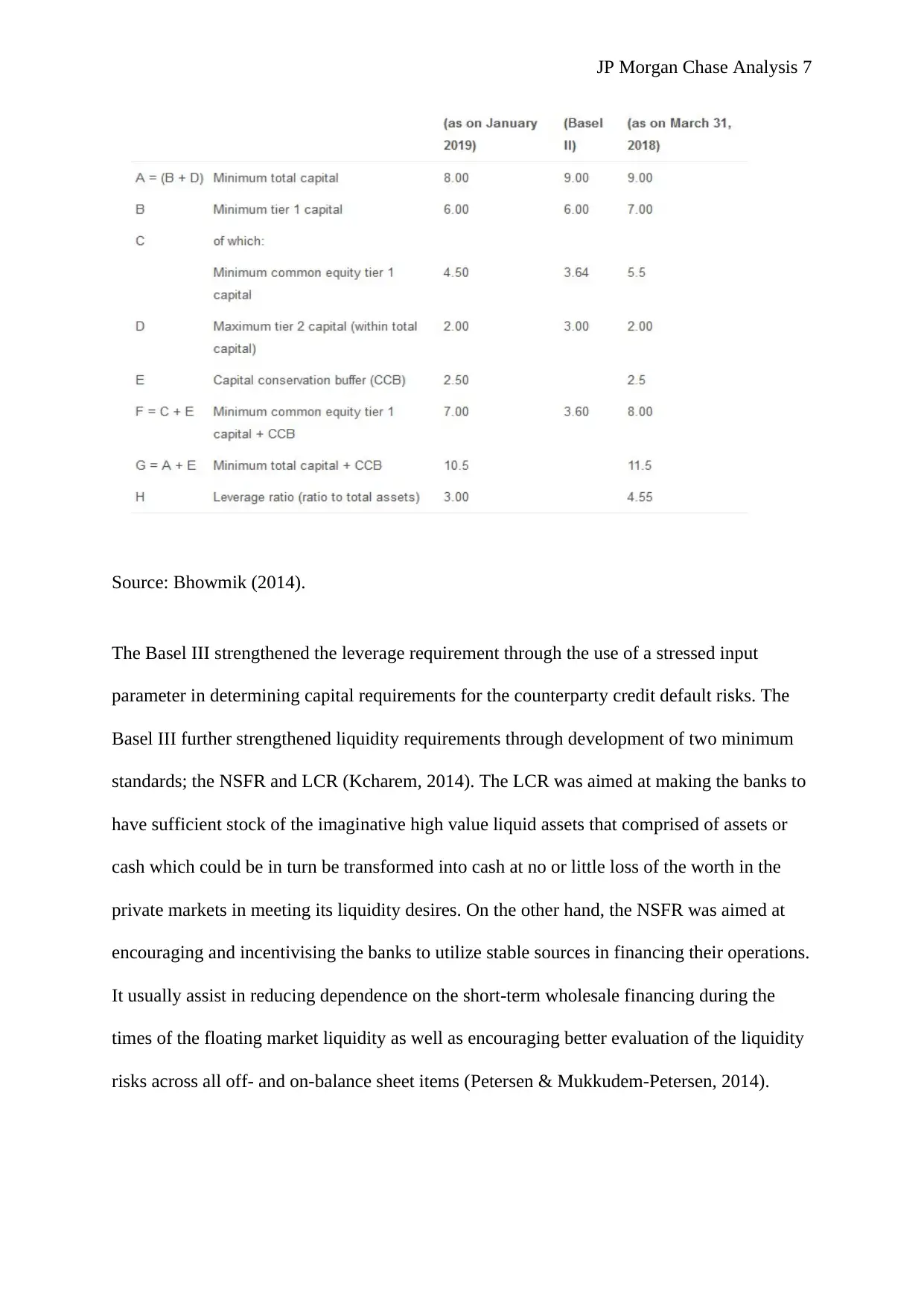

Table 1: Regulatory Capital prescriptions under Basel III

3. Main Changes to the Capital Adequacy, Liquidity and Leverage Requirements as

Stipulated by Basel III and Impact of such Changes on JP Morgan’s Financial

Conditions

Basel III is usually a sequence of measures designed in repairing and augmenting Basel II

accord (Ojo, 2013). This adjunct addresses the issues of the economic pro-cyclicality and

gives suggestions on the means of mitigating such issues through increase in capital charges

when country’s economies overheat as well as when capital charge reduces in the economic

contractions (Kasekende, Bagyenda & Brownbridge, 2011). Basically, the Basel III is far

much stricter and complete than the Basel II. Some of the reforms recommended in the Basel

III include the five facets for enhancing capital, raising quality, transparency and consistency

of capital base, enhancing risk-based capital needs with leverage ratio, enhancing risk

coverage, promoting country-cyclical buffers and reducing pro-cyclicality as well as

addressing interconnectedness and systematic risks (Ojo, 2013). The Basel III comprised of

some measures that are mainly targeted at improving the value and capacity of capital within

the economy, aimed at refining loss-absorption ability in both the liquidation and going

concerns setups. By retaining a minimum capital competence of 8%, Tier 1 was increased to

6% with equity postulated at 4.5% (Jayadev, 2013). These new concepts are for

countercyclical capital bumper and capital conversion bumper which ensured that financial

institutions are capable of absorbing the losses without any breach to the minimum capital

requirements and were capable of carrying their operations even during economic crisis

without deleveraging (Bhowmik, 2014).

Table 1: Regulatory Capital prescriptions under Basel III

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

JP Morgan Chase Analysis 7

Source: Bhowmik (2014).

The Basel III strengthened the leverage requirement through the use of a stressed input

parameter in determining capital requirements for the counterparty credit default risks. The

Basel III further strengthened liquidity requirements through development of two minimum

standards; the NSFR and LCR (Kcharem, 2014). The LCR was aimed at making the banks to

have sufficient stock of the imaginative high value liquid assets that comprised of assets or

cash which could be in turn be transformed into cash at no or little loss of the worth in the

private markets in meeting its liquidity desires. On the other hand, the NSFR was aimed at

encouraging and incentivising the banks to utilize stable sources in financing their operations.

It usually assist in reducing dependence on the short-term wholesale financing during the

times of the floating market liquidity as well as encouraging better evaluation of the liquidity

risks across all off- and on-balance sheet items (Petersen & Mukkudem-Petersen, 2014).

Source: Bhowmik (2014).

The Basel III strengthened the leverage requirement through the use of a stressed input

parameter in determining capital requirements for the counterparty credit default risks. The

Basel III further strengthened liquidity requirements through development of two minimum

standards; the NSFR and LCR (Kcharem, 2014). The LCR was aimed at making the banks to

have sufficient stock of the imaginative high value liquid assets that comprised of assets or

cash which could be in turn be transformed into cash at no or little loss of the worth in the

private markets in meeting its liquidity desires. On the other hand, the NSFR was aimed at

encouraging and incentivising the banks to utilize stable sources in financing their operations.

It usually assist in reducing dependence on the short-term wholesale financing during the

times of the floating market liquidity as well as encouraging better evaluation of the liquidity

risks across all off- and on-balance sheet items (Petersen & Mukkudem-Petersen, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

JP Morgan Chase Analysis 8

The Basel III also introduced the leverage acts as the non-risk sensitive backstop

measurement in reducing risks of the build-up of extreme leverage in the banks and within

the financial system (Kcharem, 2014). This prerequisite would establish an all-inclusive floor

to a minimum capital requirement that would in turn minimizes the probable erosive impact

of the gaming as well as model risk on the capital alongside the true risks. In essence, the

Basel III necessitated financial and banking institutions to gradually increase their capital

ratios and reaching a high capital ratio (Ojo, 2013). Furthermore, Basel III mainly focused on

funding and capital. It specified the new capital ratios. It also set some new standards for the

short-term financing and sketches out needs for the long-term financing. In strengthening

minimum capital needs, Basel III necessitates financial institutions to make adequate high-

quality capital by increasing it common equity tier, introducing qualifying criteria as well as

enlarging the scope of reduction for the goodwill, treasury stock as well as deferred assets

(Kcharem, 2014). Moreover, it mandates enhanced disclosure which in turn affects reporting

on the securitization exposures, components of the regulatory capital ratio and off-balance

sheet vehicles. The Basel III was mainly established to reduce probability of any recurrence

of the global financial crisis (Kcharem, 2014). In essence, it main objectives was to improve s

absorbing capacity of every individual banks. It has some measures in ensuring that financial

institutions system do not crumble and some of its spill-over effect on the economy is

reduced (Raman, 2012).

Furthermore, the change in capital requirements under Basel III, are more likely to enable the

company raise capital set against certain exposures, provide extra incentive to move the OTC

derivatives, contracts to the central counterparties as well as minimize pro-cyclicality; hence,

assisting it reduce the systemic risks across its operations (Petersen & Mukkudem-Petersen,

2014). The change is also more likely to provide some incentives to JP Morgan Chase in

strengthening its risk management of the counterparty credit exposures (Ojo, 2016). To be

The Basel III also introduced the leverage acts as the non-risk sensitive backstop

measurement in reducing risks of the build-up of extreme leverage in the banks and within

the financial system (Kcharem, 2014). This prerequisite would establish an all-inclusive floor

to a minimum capital requirement that would in turn minimizes the probable erosive impact

of the gaming as well as model risk on the capital alongside the true risks. In essence, the

Basel III necessitated financial and banking institutions to gradually increase their capital

ratios and reaching a high capital ratio (Ojo, 2013). Furthermore, Basel III mainly focused on

funding and capital. It specified the new capital ratios. It also set some new standards for the

short-term financing and sketches out needs for the long-term financing. In strengthening

minimum capital needs, Basel III necessitates financial institutions to make adequate high-

quality capital by increasing it common equity tier, introducing qualifying criteria as well as

enlarging the scope of reduction for the goodwill, treasury stock as well as deferred assets

(Kcharem, 2014). Moreover, it mandates enhanced disclosure which in turn affects reporting

on the securitization exposures, components of the regulatory capital ratio and off-balance

sheet vehicles. The Basel III was mainly established to reduce probability of any recurrence

of the global financial crisis (Kcharem, 2014). In essence, it main objectives was to improve s

absorbing capacity of every individual banks. It has some measures in ensuring that financial

institutions system do not crumble and some of its spill-over effect on the economy is

reduced (Raman, 2012).

Furthermore, the change in capital requirements under Basel III, are more likely to enable the

company raise capital set against certain exposures, provide extra incentive to move the OTC

derivatives, contracts to the central counterparties as well as minimize pro-cyclicality; hence,

assisting it reduce the systemic risks across its operations (Petersen & Mukkudem-Petersen,

2014). The change is also more likely to provide some incentives to JP Morgan Chase in

strengthening its risk management of the counterparty credit exposures (Ojo, 2016). To be

JP Morgan Chase Analysis 9

more specific, the change in capital requirements under the Basel III would expose the bank

books to attract some enhanced capital charges. Therefore, JP Morgan Chase would have

common equity capital under the Basel III which would stand it in good stead (Raman, 2012).

Basel III also introduced new liquidity policies aimed at improving resilience of the financial

and banking institutions to liquidity shocks (Ojo, 2013). This necessitated financial

institutions to maintain buffer of extremely liquid securities commonly measured by liquidity

coverage ratio. The buffer is usually aimed at promoting resilience to probable liquidity

disruptions over the month (Petersen & Mukkudem-Petersen, 2014). These standards are

likely to affect JP Morgan Chase financial conditions by ensuring that this bank has adequate

unencumbered, as well as high-liquid assets in offsetting its net cash outflows encountered

under its acute short-term operations. In addition, the new liquidity standards is more likely to

cause a significant downgrade in JP Morgan Chase’s public credit rating, a loss of the

unsecured wholesale financing, increase in derivative substantial and collateral calls on the

non-contractual as well as contractual off-balance sheet revelations, partial loss of deposits as

well as increase in the secured funding haircuts (Raman, 2012).

Another liquidity measure under the Basel III is the net stable financing ratio (Ojo, 2016).

This standard necessitates minimum value of the stable bases of financing at the institutions

in relation to liquidity profile of assets and potential for the provisional liquidity requirements

emerging from the off-balance sheet pledges, over the period. This standard would assist JP

Morgan Chase to border its over-dependence on temporary financing throughout times of the

floating arcade liquidity and would also hearten it to better evaluate its liquidity risk

diagonally through all the off- and on-balance sheet objects (Kcharem, 2014). Such measures

would promote resilience of the bank over the long-term by creating extra incentives for JP

more specific, the change in capital requirements under the Basel III would expose the bank

books to attract some enhanced capital charges. Therefore, JP Morgan Chase would have

common equity capital under the Basel III which would stand it in good stead (Raman, 2012).

Basel III also introduced new liquidity policies aimed at improving resilience of the financial

and banking institutions to liquidity shocks (Ojo, 2013). This necessitated financial

institutions to maintain buffer of extremely liquid securities commonly measured by liquidity

coverage ratio. The buffer is usually aimed at promoting resilience to probable liquidity

disruptions over the month (Petersen & Mukkudem-Petersen, 2014). These standards are

likely to affect JP Morgan Chase financial conditions by ensuring that this bank has adequate

unencumbered, as well as high-liquid assets in offsetting its net cash outflows encountered

under its acute short-term operations. In addition, the new liquidity standards is more likely to

cause a significant downgrade in JP Morgan Chase’s public credit rating, a loss of the

unsecured wholesale financing, increase in derivative substantial and collateral calls on the

non-contractual as well as contractual off-balance sheet revelations, partial loss of deposits as

well as increase in the secured funding haircuts (Raman, 2012).

Another liquidity measure under the Basel III is the net stable financing ratio (Ojo, 2016).

This standard necessitates minimum value of the stable bases of financing at the institutions

in relation to liquidity profile of assets and potential for the provisional liquidity requirements

emerging from the off-balance sheet pledges, over the period. This standard would assist JP

Morgan Chase to border its over-dependence on temporary financing throughout times of the

floating arcade liquidity and would also hearten it to better evaluate its liquidity risk

diagonally through all the off- and on-balance sheet objects (Kcharem, 2014). Such measures

would promote resilience of the bank over the long-term by creating extra incentives for JP

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

JP Morgan Chase Analysis 10

Morgan Chase to funds its operations with more steady sources of finance on a continuing

basis (Saleuddin, 2015).

The changes in leverage requirements on the other hand would enable the bank to protect

itself against system-wide build-up of the leverage which would in turn cause some

destabilization unwinding process in times of financial stress (Waithaka, 2013). In addition,

the change would protect JP Morgan Chase against the perverse incentive in piling on the

low-risk assets, which might not remain stable under extreme conditions producing some

systemic risks (Petersen & Mukkudem-Petersen, 2014). Furthermore, with introduction of a

more transparent, simple and non-risk-based leverage as the supplementary backstop measure

to capital requirements, JP Morgan Chase would be able to contain excessive risk. Further,

the change in leverage requirements under Basel III would have substantial impact on JP

Morgan Chase’s profitability. In essence, the change would reduce the bank’s return on

equity by around 3% (Kcharem, 2014). Its numerous core operations would also be

profoundly affected, especially securitization and trading businesses (Raman, 2012).

4. Asset Securitization and the Reasons Why Different Financial or Banking Institutions

Might Wish to Securitize

Asset securitization is usually the process of taking illiquid assets and through financial

engineering, transforming these assets into securities (Thakor, 2015).. In other words, asset

securitization is the financial prearrangement that comprises of issues the securities funded by

several assets, in most scenarios debt. In this scenario, the basic assets are usually converted

into securities, therefore the securitization (Giddy, 2001). In essence, securitization is a

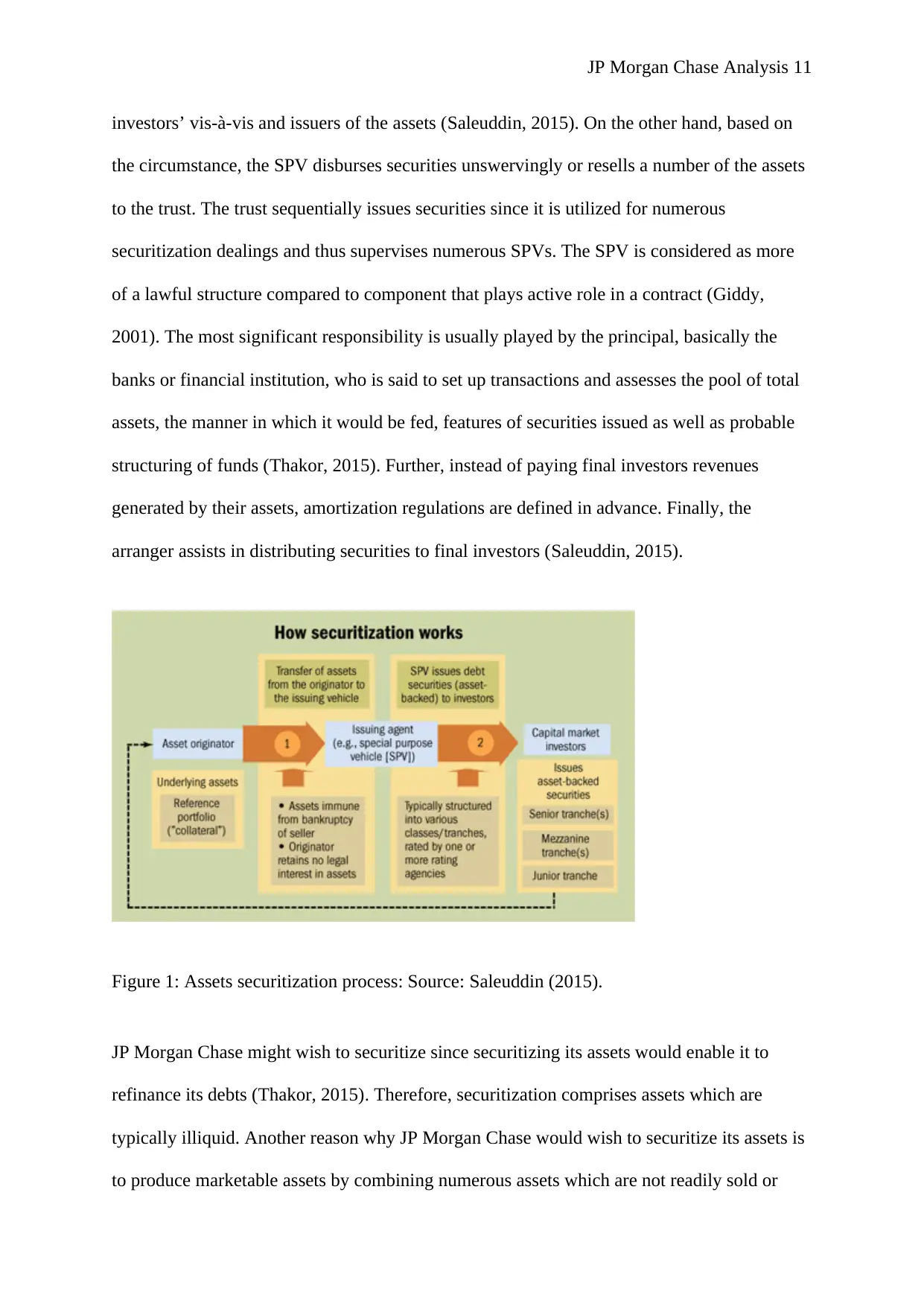

complicated procedure that entails several actors as shown in Figure 1 below. Under the

diagram, the firm originally holding the assets usually starts the progression by selling its

assets to lawful entities. The Special Purpose Vehicle helps in limiting the risk of final

Morgan Chase to funds its operations with more steady sources of finance on a continuing

basis (Saleuddin, 2015).

The changes in leverage requirements on the other hand would enable the bank to protect

itself against system-wide build-up of the leverage which would in turn cause some

destabilization unwinding process in times of financial stress (Waithaka, 2013). In addition,

the change would protect JP Morgan Chase against the perverse incentive in piling on the

low-risk assets, which might not remain stable under extreme conditions producing some

systemic risks (Petersen & Mukkudem-Petersen, 2014). Furthermore, with introduction of a

more transparent, simple and non-risk-based leverage as the supplementary backstop measure

to capital requirements, JP Morgan Chase would be able to contain excessive risk. Further,

the change in leverage requirements under Basel III would have substantial impact on JP

Morgan Chase’s profitability. In essence, the change would reduce the bank’s return on

equity by around 3% (Kcharem, 2014). Its numerous core operations would also be

profoundly affected, especially securitization and trading businesses (Raman, 2012).

4. Asset Securitization and the Reasons Why Different Financial or Banking Institutions

Might Wish to Securitize

Asset securitization is usually the process of taking illiquid assets and through financial

engineering, transforming these assets into securities (Thakor, 2015).. In other words, asset

securitization is the financial prearrangement that comprises of issues the securities funded by

several assets, in most scenarios debt. In this scenario, the basic assets are usually converted

into securities, therefore the securitization (Giddy, 2001). In essence, securitization is a

complicated procedure that entails several actors as shown in Figure 1 below. Under the

diagram, the firm originally holding the assets usually starts the progression by selling its

assets to lawful entities. The Special Purpose Vehicle helps in limiting the risk of final

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

JP Morgan Chase Analysis 11

investors’ vis-à-vis and issuers of the assets (Saleuddin, 2015). On the other hand, based on

the circumstance, the SPV disburses securities unswervingly or resells a number of the assets

to the trust. The trust sequentially issues securities since it is utilized for numerous

securitization dealings and thus supervises numerous SPVs. The SPV is considered as more

of a lawful structure compared to component that plays active role in a contract (Giddy,

2001). The most significant responsibility is usually played by the principal, basically the

banks or financial institution, who is said to set up transactions and assesses the pool of total

assets, the manner in which it would be fed, features of securities issued as well as probable

structuring of funds (Thakor, 2015). Further, instead of paying final investors revenues

generated by their assets, amortization regulations are defined in advance. Finally, the

arranger assists in distributing securities to final investors (Saleuddin, 2015).

Figure 1: Assets securitization process: Source: Saleuddin (2015).

JP Morgan Chase might wish to securitize since securitizing its assets would enable it to

refinance its debts (Thakor, 2015). Therefore, securitization comprises assets which are

typically illiquid. Another reason why JP Morgan Chase would wish to securitize its assets is

to produce marketable assets by combining numerous assets which are not readily sold or

investors’ vis-à-vis and issuers of the assets (Saleuddin, 2015). On the other hand, based on

the circumstance, the SPV disburses securities unswervingly or resells a number of the assets

to the trust. The trust sequentially issues securities since it is utilized for numerous

securitization dealings and thus supervises numerous SPVs. The SPV is considered as more

of a lawful structure compared to component that plays active role in a contract (Giddy,

2001). The most significant responsibility is usually played by the principal, basically the

banks or financial institution, who is said to set up transactions and assesses the pool of total

assets, the manner in which it would be fed, features of securities issued as well as probable

structuring of funds (Thakor, 2015). Further, instead of paying final investors revenues

generated by their assets, amortization regulations are defined in advance. Finally, the

arranger assists in distributing securities to final investors (Saleuddin, 2015).

Figure 1: Assets securitization process: Source: Saleuddin (2015).

JP Morgan Chase might wish to securitize since securitizing its assets would enable it to

refinance its debts (Thakor, 2015). Therefore, securitization comprises assets which are

typically illiquid. Another reason why JP Morgan Chase would wish to securitize its assets is

to produce marketable assets by combining numerous assets which are not readily sold or

JP Morgan Chase Analysis 12

bought in order to generate a significant market for such assets and help it in making up more

valuable pools. Further, JP Morgan Chase would wish to securitize its assets in lessening the

total amount assigned to debt from its balance sheet, which in turn results in corresponding

decrease in its regulatory capital requirements and enables its bring in extra liquidity which

could be utilized in making new loans (Giddy, 2001).

In addition, JP Morgan Chase might securitize for risk management, greater leverage of the

capital, balance sheet issues as well as profiting from the origination fees. In essence, by

securitize their assets, JP Morgan Chases might benefit from moving default risks linked with

securitized debts from their balance sheets allowing for more leverage (Wæver, 2011). As

such, this results in reduced debt risk and loads, whereby JP Morgan Chase could utilize its

capital more effectively. Also, JP Morgan Chase might securitize to reduce asset-liability

mismatch since based on the structure selected, securitization could provide perfect matched

financing by removing the funding exposure in both pricing and duration basis. In essence, JP

Morgan Chase might securitize in order to be in a position to cater for the credit boom since

they securitize their loans and utilize the money to give more credits. JP Morgan Chase might

also securitize with the aim of increasing its profits (Martín-Oliver & Saurina, 2007). This is

based on the notion that securitization provides the bank numerous options for financing its

major activities and managing the risk profile which would in turn result in greater expected

profits. Banks might also securitize for funding motives. In essence, by securitizing its loans,

JP Morgan Chase is said to broaden its source of finances as the past sceptical investors could

no longer have to venture in a bank they do not like, but just portfolio of the securities the

bank originated which investors might consider worth investing. In other words,

securitization permits for segment funding, produced by pooling of the assets so as the bank

could borrow cash from numerous sources at numerous rates, which in turn result in decrease

in marginal costs of the funding (Fabozzi & Kothari, 2008).

bought in order to generate a significant market for such assets and help it in making up more

valuable pools. Further, JP Morgan Chase would wish to securitize its assets in lessening the

total amount assigned to debt from its balance sheet, which in turn results in corresponding

decrease in its regulatory capital requirements and enables its bring in extra liquidity which

could be utilized in making new loans (Giddy, 2001).

In addition, JP Morgan Chase might securitize for risk management, greater leverage of the

capital, balance sheet issues as well as profiting from the origination fees. In essence, by

securitize their assets, JP Morgan Chases might benefit from moving default risks linked with

securitized debts from their balance sheets allowing for more leverage (Wæver, 2011). As

such, this results in reduced debt risk and loads, whereby JP Morgan Chase could utilize its

capital more effectively. Also, JP Morgan Chase might securitize to reduce asset-liability

mismatch since based on the structure selected, securitization could provide perfect matched

financing by removing the funding exposure in both pricing and duration basis. In essence, JP

Morgan Chase might securitize in order to be in a position to cater for the credit boom since

they securitize their loans and utilize the money to give more credits. JP Morgan Chase might

also securitize with the aim of increasing its profits (Martín-Oliver & Saurina, 2007). This is

based on the notion that securitization provides the bank numerous options for financing its

major activities and managing the risk profile which would in turn result in greater expected

profits. Banks might also securitize for funding motives. In essence, by securitizing its loans,

JP Morgan Chase is said to broaden its source of finances as the past sceptical investors could

no longer have to venture in a bank they do not like, but just portfolio of the securities the

bank originated which investors might consider worth investing. In other words,

securitization permits for segment funding, produced by pooling of the assets so as the bank

could borrow cash from numerous sources at numerous rates, which in turn result in decrease

in marginal costs of the funding (Fabozzi & Kothari, 2008).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.