Comprehensive Management Accounting System Report for Jupiter PLC

VerifiedAdded on 2020/10/05

|16

|4568

|71

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within Jupiter PLC, a medium-sized manufacturing company. The report begins by defining management accounting and exploring various system types, including inventory management, cost accounting, and price optimization. It then delves into different reporting methods, such as performance reports, account receivable reports, and inventory management reports, highlighting their benefits and the relationship between accounting systems and reporting. The report further analyzes costing methods, including marginal and absorption costing, and prepares profit and loss statements using these techniques. Planning tools used in management accounting are also examined. Finally, the report assesses how organizations adopt management accounting to address financial challenges and achieve sustainable success, evaluating the effectiveness of planning tools in this context. The analysis includes a detailed breakdown of costs, profit calculations, and the importance of efficient financial management within a business context.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1:Management accounting and types of management accounting system :-...............................3

2:Methods of management accounting reporting .......................................................................4

3:Benefits of management accounting system :-.........................................................................5

4:Relation between management accounting system and reporting :-.........................................6

TASK 2........................................................................................................................................6

1: Calculation by using various costing method..........................................................................6

2: Preparation of profit and loss statement by using techniques..................................................7

3: Preparation of final account after September..........................................................................8

TASK 3........................................................................................................................................9

1:Planning tools used in management accounting ......................................................................9

TASK 4..........................................................................................................................................11

1:Comparison for how organizations are adopting management accounting system to respond

to financial problems:................................................................................................................11

2:Analysis use for solving financial problems for its sustainable success ................................12

3:Evaluation of planning tools for accounting to solve financial problem to lead organization

in sustainable success:................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1:Management accounting and types of management accounting system :-...............................3

2:Methods of management accounting reporting .......................................................................4

3:Benefits of management accounting system :-.........................................................................5

4:Relation between management accounting system and reporting :-.........................................6

TASK 2........................................................................................................................................6

1: Calculation by using various costing method..........................................................................6

2: Preparation of profit and loss statement by using techniques..................................................7

3: Preparation of final account after September..........................................................................8

TASK 3........................................................................................................................................9

1:Planning tools used in management accounting ......................................................................9

TASK 4..........................................................................................................................................11

1:Comparison for how organizations are adopting management accounting system to respond

to financial problems:................................................................................................................11

2:Analysis use for solving financial problems for its sustainable success ................................12

3:Evaluation of planning tools for accounting to solve financial problem to lead organization

in sustainable success:................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES .............................................................................................................................15

INTRODUCTION

In today's competitive word every organisation is working to earn more and more by

increasing in performance that can be in terms of its quality, variety in products and most

important by having a effective management. For this management accounting is done, this helps

to evaluate current position and by considering market conditions future targets are set . Jupiter

PLC is a medium size manufacturing company requires management accounting system to

operate efficiently by managing inventory, row material, production, labour supplies, repairs and

maintenance (Amoako, 2013). In this project description regarding management accounting and

its types, methods of management reporting, advantages of management accounting, relation

between management accounting system and management accounting report, planning tools,

budgets and implementation of these in financial system.

TASK 1

1:Management accounting and types of management accounting system :-

Management Accounting is an internal system in an organisation that is used to measure

or evaluate performance of different departments of organisation by setting targets for

performance, analysing different strategies that will help in achieving targeted goals and helps to

find reasons in deviation from actual goal. In other words management accounting provides

financial and non-financial information to people within an organisation that helps in better

decision making, enhance effectiveness and achieve organisational control.

Types of management accounting system-

Inventory management system- is an ongoing process of managing stocks of a

company in form of row material, work-in-progress, finished goods. This supervision helps in

easy flow of stocks from manufacturing to warehouse and then to sale. Cost of holding extra

material and loss due to shortage in stock is minimised by this. Inventory management have

various methods such as LEFO, FIFO and Average inventory method (Brewer, Sorensen and

Stout, 2014).

LIFO ( Last In First Out ) – Material which is received in last will be released first. This

method holds old material and release new in first.

FIFO ( First In First Out ) - Material which is received first will be released first. Material

which is older removed first this helps to reduce cost due to obsolescence.

In today's competitive word every organisation is working to earn more and more by

increasing in performance that can be in terms of its quality, variety in products and most

important by having a effective management. For this management accounting is done, this helps

to evaluate current position and by considering market conditions future targets are set . Jupiter

PLC is a medium size manufacturing company requires management accounting system to

operate efficiently by managing inventory, row material, production, labour supplies, repairs and

maintenance (Amoako, 2013). In this project description regarding management accounting and

its types, methods of management reporting, advantages of management accounting, relation

between management accounting system and management accounting report, planning tools,

budgets and implementation of these in financial system.

TASK 1

1:Management accounting and types of management accounting system :-

Management Accounting is an internal system in an organisation that is used to measure

or evaluate performance of different departments of organisation by setting targets for

performance, analysing different strategies that will help in achieving targeted goals and helps to

find reasons in deviation from actual goal. In other words management accounting provides

financial and non-financial information to people within an organisation that helps in better

decision making, enhance effectiveness and achieve organisational control.

Types of management accounting system-

Inventory management system- is an ongoing process of managing stocks of a

company in form of row material, work-in-progress, finished goods. This supervision helps in

easy flow of stocks from manufacturing to warehouse and then to sale. Cost of holding extra

material and loss due to shortage in stock is minimised by this. Inventory management have

various methods such as LEFO, FIFO and Average inventory method (Brewer, Sorensen and

Stout, 2014).

LIFO ( Last In First Out ) – Material which is received in last will be released first. This

method holds old material and release new in first.

FIFO ( First In First Out ) - Material which is received first will be released first. Material

which is older removed first this helps to reduce cost due to obsolescence.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average method – No calculation regarding which material needs to be dispatched first,

any material can be dispatched first and calculation is done on average basis.

Jupiter PLC follows FIFO method of inventory as through this old stock is removed first

and any loss due to obsolescence of product because of long duration of storage can be reduced.

Cost accounting system - is used to calculate cost of production of different products by

company in which all cost at different level of production is included together with attributed

fixed cost is also included this helps to calculate total cost of a product and also in profit

calculation. Accounting of cost is done by four methods such as standard costing system,

marginal , activity base costing and lean costing system. Jupiter PLC uses activity base costing

system as this system assigns cost to products that are related to manufacturing.

Job costing system – is method of recording cost of a manufacturing job. This system

helps to assign manufacturing cost to each product and product manager and accountant have

record of cost of each product. Job costing helps to calculate cost of different products when

company produces more then single product which are completely different. Jupiter PLC uses

this costing system to calculate cost of its different products manufactured by the company.

Price optimisation system - This system helps to know how to ultimate consumer will

react to different prices of a product. This helps company to determine price of a product which

helps them to attain their goal of profit maximisation. In this competitive market Jupiter PLC

also uses this system to know optimum price of their product so there is no overpricing for

product (JOSHI and et. al., 20113).

2:Methods of management accounting reporting

Performance report – leads to measuring performance of a organisation as one unit or

on the basis of different segments of organisation, even performance of a particular product can

also be evaluated. All this process is done to measure profitability by good performance of any

division in company and also helps to locate poor performing units. A detail measure regarding

performance is taken and reasons for poor performance is located and necessary steps to be taken

to improve performance. Jupiter PLC will make a performance report to know its performance of

its manufacturing plant so efficiency can be increased.

Account receivable report – Finance system of a organisation must be strong as all

other activities of organisation is very much affected by availability of finance. For this

management of funds must be done and operating revenue is generated from our sales and

any material can be dispatched first and calculation is done on average basis.

Jupiter PLC follows FIFO method of inventory as through this old stock is removed first

and any loss due to obsolescence of product because of long duration of storage can be reduced.

Cost accounting system - is used to calculate cost of production of different products by

company in which all cost at different level of production is included together with attributed

fixed cost is also included this helps to calculate total cost of a product and also in profit

calculation. Accounting of cost is done by four methods such as standard costing system,

marginal , activity base costing and lean costing system. Jupiter PLC uses activity base costing

system as this system assigns cost to products that are related to manufacturing.

Job costing system – is method of recording cost of a manufacturing job. This system

helps to assign manufacturing cost to each product and product manager and accountant have

record of cost of each product. Job costing helps to calculate cost of different products when

company produces more then single product which are completely different. Jupiter PLC uses

this costing system to calculate cost of its different products manufactured by the company.

Price optimisation system - This system helps to know how to ultimate consumer will

react to different prices of a product. This helps company to determine price of a product which

helps them to attain their goal of profit maximisation. In this competitive market Jupiter PLC

also uses this system to know optimum price of their product so there is no overpricing for

product (JOSHI and et. al., 20113).

2:Methods of management accounting reporting

Performance report – leads to measuring performance of a organisation as one unit or

on the basis of different segments of organisation, even performance of a particular product can

also be evaluated. All this process is done to measure profitability by good performance of any

division in company and also helps to locate poor performing units. A detail measure regarding

performance is taken and reasons for poor performance is located and necessary steps to be taken

to improve performance. Jupiter PLC will make a performance report to know its performance of

its manufacturing plant so efficiency can be increased.

Account receivable report – Finance system of a organisation must be strong as all

other activities of organisation is very much affected by availability of finance. For this

management of funds must be done and operating revenue is generated from our sales and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

account receivables get generated. A report of account receivable, unpaid consumers, overdue

payments must be prepared to know financial condition together with that reasons for non

payments and also a system is developed so payments will be received on time and a reminder

prior to due date can be made to debtors. Jupiter PLC will adopt a system in which duration of

credit will be reduced and also a proper system to receive amount from debtors will be followed.

Inventory management report – Inventory is a liquid asset to a company which can be

in any form as raw material, WIP, finished goods. Higher inventory involves more blockage of

funds and liquidity position of company gets affected. This report helps to know different costs

related to inventory such as obtaining cost, storage cost, transportation cost etc. every

organisation wants to be always be available with sufficient demand but for this various methods

are followed so that inventory cost can be minimised without compromising with availability of

stocks. Jupiter PLC is a manufacturing company and cost of holding inventory will be more so a

proper system to be followed to reduce cost due to excess inventory (Klemstine and Maher,

2014).

Batch cost report – when a group of products and service are produced and cost of

which cannot be divided according to product then whole cost incurred will be divided in

number of units produced in a batch. Jupiter PLC uses batch cost reporting so that cost of goods

that are produced in a batch and whose cost cannot be determine by other method can be

determined.

3:Benefits of management accounting system :-

Management accounting is introduced with various advantages and enhancing overall

performance of a organisation is one of them. Lets know various advantages of management

accounting -

Simplifies decision making : managerial decisions requires some basis on which

decisions can be made and accounting provides that basis by evaluating current and past

performance of organisation. In Jupiter PLC decisions on every level needs to be taken and also

these must be on some reasonable basis and management accounting provides that basis.

Increase efficiency of the company : companies opt for management accounting as this

helps in increasing efficiency by evaluating and comparing performance of organisation. It

indirectly motivates employees to perform better to and grow more. Medium size company like

Jupiter PLC by increasing efficiency generate more profits and grow more rapidly.

payments must be prepared to know financial condition together with that reasons for non

payments and also a system is developed so payments will be received on time and a reminder

prior to due date can be made to debtors. Jupiter PLC will adopt a system in which duration of

credit will be reduced and also a proper system to receive amount from debtors will be followed.

Inventory management report – Inventory is a liquid asset to a company which can be

in any form as raw material, WIP, finished goods. Higher inventory involves more blockage of

funds and liquidity position of company gets affected. This report helps to know different costs

related to inventory such as obtaining cost, storage cost, transportation cost etc. every

organisation wants to be always be available with sufficient demand but for this various methods

are followed so that inventory cost can be minimised without compromising with availability of

stocks. Jupiter PLC is a manufacturing company and cost of holding inventory will be more so a

proper system to be followed to reduce cost due to excess inventory (Klemstine and Maher,

2014).

Batch cost report – when a group of products and service are produced and cost of

which cannot be divided according to product then whole cost incurred will be divided in

number of units produced in a batch. Jupiter PLC uses batch cost reporting so that cost of goods

that are produced in a batch and whose cost cannot be determine by other method can be

determined.

3:Benefits of management accounting system :-

Management accounting is introduced with various advantages and enhancing overall

performance of a organisation is one of them. Lets know various advantages of management

accounting -

Simplifies decision making : managerial decisions requires some basis on which

decisions can be made and accounting provides that basis by evaluating current and past

performance of organisation. In Jupiter PLC decisions on every level needs to be taken and also

these must be on some reasonable basis and management accounting provides that basis.

Increase efficiency of the company : companies opt for management accounting as this

helps in increasing efficiency by evaluating and comparing performance of organisation. It

indirectly motivates employees to perform better to and grow more. Medium size company like

Jupiter PLC by increasing efficiency generate more profits and grow more rapidly.

Provides freedom and flexibility : management accounting report is not required to be

prepared on any fixed intervals as this provides a enough time to prepare a good report and those

who makes report may have different opinion on some issues that provides them with freedom to

express views . Having freedom and flexibility in Jupiter PLC helps to provide them with more

honest opinions and also with a clear cut solutions to them (Lim, M., 2011).

4:Relation between management accounting system and reporting :-

Management accounting system and management reporting system both moves hand in

hand as accounting is a core on the basis of which reporting is done. Accounting involves all the

process to brings out an effective result from available data. While accounting is done various

methods are followed so a decision regarding different activities in business can be made. When

accounting is made correctly by taking real numbers as a base and getting every circumstances

evaluated correctly then only a effective report can be prepared. Reporting gives a critical

analysis of a particular activity in an organisation but this analysis is correctly done when

accounting is done right. Jupiter PLC to evolve as a better manufacturing have to work on

increasing in quality of accounting so that reporting can be done better and decisions for benefits

of organisation can be taken on time.

TASK 2

Cost is said to be value that we have to spend to get something in return. Having

planning regarding cost helps to arrange resources on time to Jupiter PLC. There are various

methods to calculating costing of a product and on the basis of cost net profits of Jupiter plc will

be calculated (Tessier and Otley, 2012). Methods of costing are-

Marginal costing : marginal means extra, it refers to that cost which is incurred to

produce an extra unit of output. Marginal costing only considers variable cost as fixed cost is

already incurred and is written off against contribution.

Absorption costing : absorption means to acquire, this system of costing acquires all cost

that is incurred in manufacturing a particular unit of a product (Absorption costing, 2018). This

costing system gives details regarding total cost but do not have much relevance in decision

making.

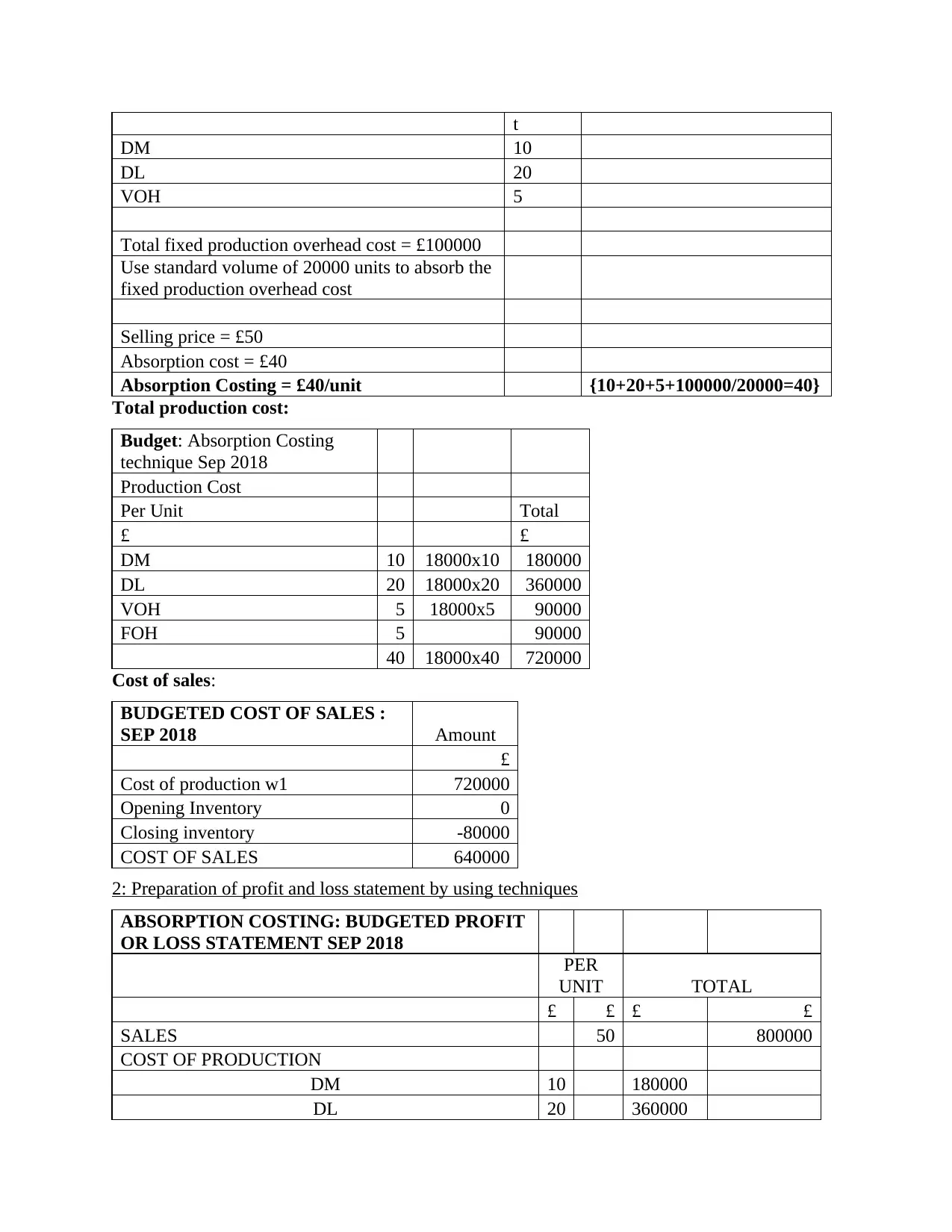

1: Calculation by using various costing method

Production cost per unit Amoun Details

prepared on any fixed intervals as this provides a enough time to prepare a good report and those

who makes report may have different opinion on some issues that provides them with freedom to

express views . Having freedom and flexibility in Jupiter PLC helps to provide them with more

honest opinions and also with a clear cut solutions to them (Lim, M., 2011).

4:Relation between management accounting system and reporting :-

Management accounting system and management reporting system both moves hand in

hand as accounting is a core on the basis of which reporting is done. Accounting involves all the

process to brings out an effective result from available data. While accounting is done various

methods are followed so a decision regarding different activities in business can be made. When

accounting is made correctly by taking real numbers as a base and getting every circumstances

evaluated correctly then only a effective report can be prepared. Reporting gives a critical

analysis of a particular activity in an organisation but this analysis is correctly done when

accounting is done right. Jupiter PLC to evolve as a better manufacturing have to work on

increasing in quality of accounting so that reporting can be done better and decisions for benefits

of organisation can be taken on time.

TASK 2

Cost is said to be value that we have to spend to get something in return. Having

planning regarding cost helps to arrange resources on time to Jupiter PLC. There are various

methods to calculating costing of a product and on the basis of cost net profits of Jupiter plc will

be calculated (Tessier and Otley, 2012). Methods of costing are-

Marginal costing : marginal means extra, it refers to that cost which is incurred to

produce an extra unit of output. Marginal costing only considers variable cost as fixed cost is

already incurred and is written off against contribution.

Absorption costing : absorption means to acquire, this system of costing acquires all cost

that is incurred in manufacturing a particular unit of a product (Absorption costing, 2018). This

costing system gives details regarding total cost but do not have much relevance in decision

making.

1: Calculation by using various costing method

Production cost per unit Amoun Details

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

t

DM 10

DL 20

VOH 5

Total fixed production overhead cost = £100000

Use standard volume of 20000 units to absorb the

fixed production overhead cost

Selling price = £50

Absorption cost = £40

Absorption Costing = £40/unit {10+20+5+100000/20000=40}

Total production cost:

Budget: Absorption Costing

technique Sep 2018

Production Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000

Cost of sales:

BUDGETED COST OF SALES :

SEP 2018 Amount

£

Cost of production w1 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

2: Preparation of profit and loss statement by using techniques

ABSORPTION COSTING: BUDGETED PROFIT

OR LOSS STATEMENT SEP 2018

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

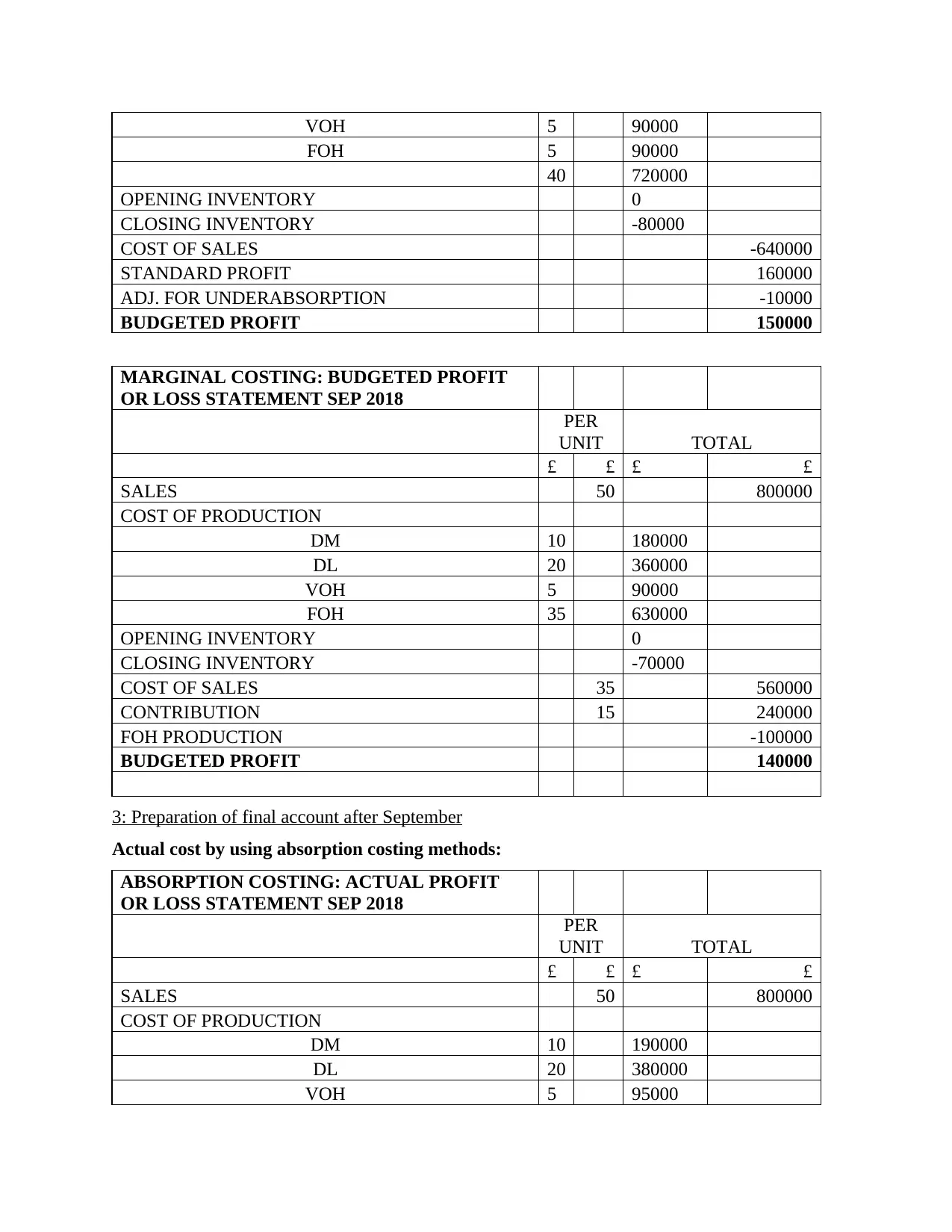

DM 10

DL 20

VOH 5

Total fixed production overhead cost = £100000

Use standard volume of 20000 units to absorb the

fixed production overhead cost

Selling price = £50

Absorption cost = £40

Absorption Costing = £40/unit {10+20+5+100000/20000=40}

Total production cost:

Budget: Absorption Costing

technique Sep 2018

Production Cost

Per Unit Total

£ £

DM 10 18000x10 180000

DL 20 18000x20 360000

VOH 5 18000x5 90000

FOH 5 90000

40 18000x40 720000

Cost of sales:

BUDGETED COST OF SALES :

SEP 2018 Amount

£

Cost of production w1 720000

Opening Inventory 0

Closing inventory -80000

COST OF SALES 640000

2: Preparation of profit and loss statement by using techniques

ABSORPTION COSTING: BUDGETED PROFIT

OR LOSS STATEMENT SEP 2018

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VOH 5 90000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

MARGINAL COSTING: BUDGETED PROFIT

OR LOSS STATEMENT SEP 2018

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

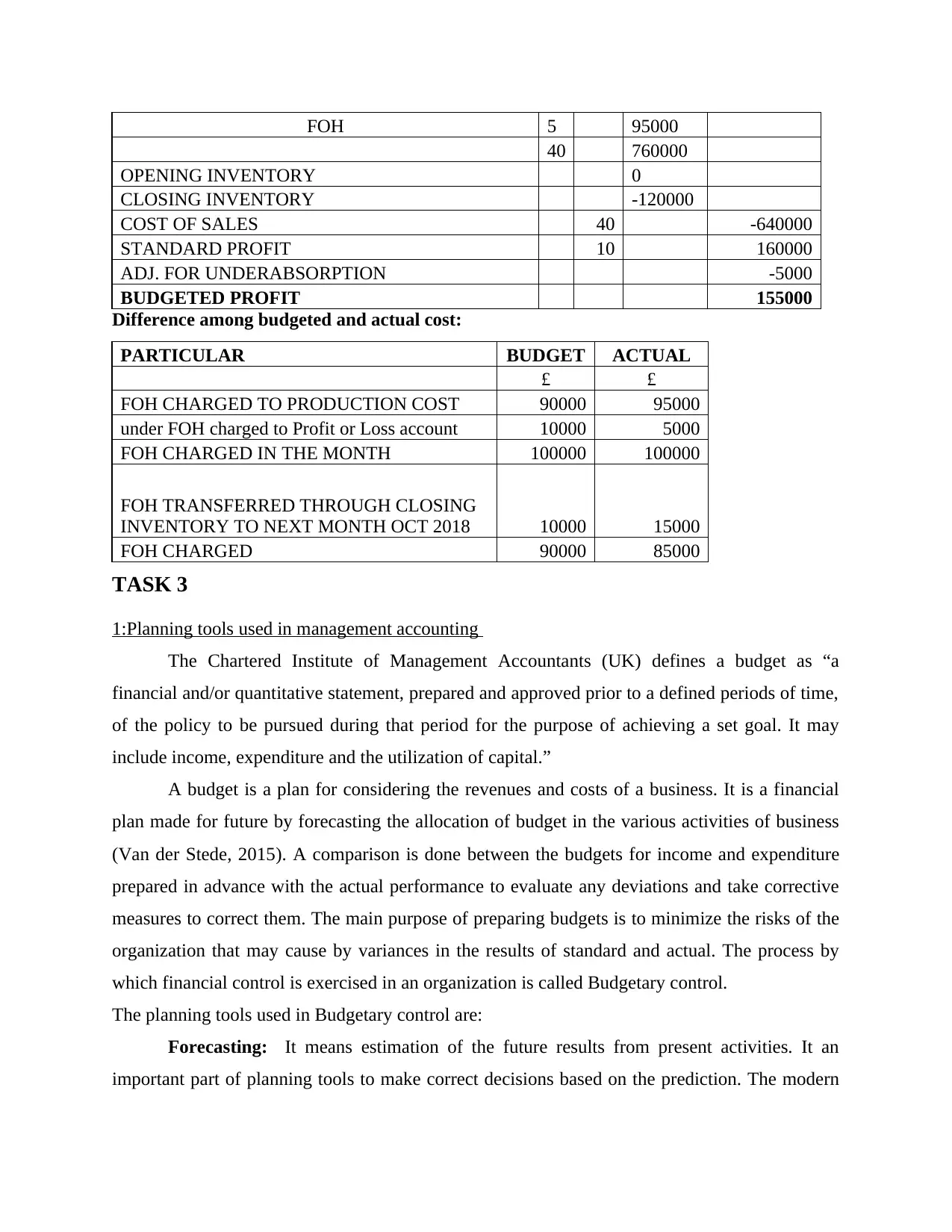

3: Preparation of final account after September

Actual cost by using absorption costing methods:

ABSORPTION COSTING: ACTUAL PROFIT

OR LOSS STATEMENT SEP 2018

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 90000

40 720000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES -640000

STANDARD PROFIT 160000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 150000

MARGINAL COSTING: BUDGETED PROFIT

OR LOSS STATEMENT SEP 2018

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 180000

DL 20 360000

VOH 5 90000

FOH 35 630000

OPENING INVENTORY 0

CLOSING INVENTORY -70000

COST OF SALES 35 560000

CONTRIBUTION 15 240000

FOH PRODUCTION -100000

BUDGETED PROFIT 140000

3: Preparation of final account after September

Actual cost by using absorption costing methods:

ABSORPTION COSTING: ACTUAL PROFIT

OR LOSS STATEMENT SEP 2018

PER

UNIT TOTAL

£ £ £ £

SALES 50 800000

COST OF PRODUCTION

DM 10 190000

DL 20 380000

VOH 5 95000

FOH 5 95000

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

Difference among budgeted and actual cost:

PARTICULAR BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

TASK 3

1:Planning tools used in management accounting

The Chartered Institute of Management Accountants (UK) defines a budget as “a

financial and/or quantitative statement, prepared and approved prior to a defined periods of time,

of the policy to be pursued during that period for the purpose of achieving a set goal. It may

include income, expenditure and the utilization of capital.”

A budget is a plan for considering the revenues and costs of a business. It is a financial

plan made for future by forecasting the allocation of budget in the various activities of business

(Van der Stede, 2015). A comparison is done between the budgets for income and expenditure

prepared in advance with the actual performance to evaluate any deviations and take corrective

measures to correct them. The main purpose of preparing budgets is to minimize the risks of the

organization that may cause by variances in the results of standard and actual. The process by

which financial control is exercised in an organization is called Budgetary control.

The planning tools used in Budgetary control are:

Forecasting: It means estimation of the future results from present activities. It an

important part of planning tools to make correct decisions based on the prediction. The modern

40 760000

OPENING INVENTORY 0

CLOSING INVENTORY -120000

COST OF SALES 40 -640000

STANDARD PROFIT 10 160000

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 155000

Difference among budgeted and actual cost:

PARTICULAR BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 90000 95000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

TASK 3

1:Planning tools used in management accounting

The Chartered Institute of Management Accountants (UK) defines a budget as “a

financial and/or quantitative statement, prepared and approved prior to a defined periods of time,

of the policy to be pursued during that period for the purpose of achieving a set goal. It may

include income, expenditure and the utilization of capital.”

A budget is a plan for considering the revenues and costs of a business. It is a financial

plan made for future by forecasting the allocation of budget in the various activities of business

(Van der Stede, 2015). A comparison is done between the budgets for income and expenditure

prepared in advance with the actual performance to evaluate any deviations and take corrective

measures to correct them. The main purpose of preparing budgets is to minimize the risks of the

organization that may cause by variances in the results of standard and actual. The process by

which financial control is exercised in an organization is called Budgetary control.

The planning tools used in Budgetary control are:

Forecasting: It means estimation of the future results from present activities. It an

important part of planning tools to make correct decisions based on the prediction. The modern

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and scientific forecasting uses mathematical models, historical data and statistical analysis to

predict the future outcomes. There are two types of forecasting short-term and long-term.

Advantage: It helps in providing an idea about the required budgets to minimize the risks

associated with the activities and to compare the actual with standard to analyse the

variance and correct it (Zoni, Dossi and Morelli, 2012).

Disadvantage: The forecasting is not always correct as the future is uncertain.

Scenario Planning: The planning is done in a structured way for evaluation of various

outcomes in future in respect to strategic, operational and financial planning.

Advantage: The main advantage is that the planning is done by covering political,

economic, social and technological areas. All these provide a better insight about the

requirement and control of budgets.

Disadvantage: It involves various future alternatives of a situation there for decision

making becomes confusing. Absorption costing. 2018

Contingency plan: The contingency plan is prepared to handle emergency situations

which are beyond control and expectations. These are the back-up plans for future contingencies.

Advantage: Planning for contingencies can save the company from major financial

problems and risks.

Disadvantage: The amount and time used for planning contingencies will be a huge

wastage if no such contingency occurs in future.

From the above-mentioned tools, the use of forecasting tool is to predict the future, make

budgets, and control the variances between the actual and standard. This planning helps the

company to predict what will happen in future from the past data. The actual results are

measured with the standard to find out the variance. The variance is corrected by corrective

measure and enables the company to control in a better way.

The use of scenario tool is that it provide a detail planning about the various outcomes

that may happen in future. The company may decide a task and do the planning according to the

particular task by considering the overall aspects of the organization. This gives a whole picture

of how to plan so that all the company can control the budgets allocated to different departments.

The use of contingency planning is to prepare for unexpected yet possible situations in future. If

this planning is done rightly it can save company from the unexpected financial losses (Lavia

López and Hiebl, 2014).

predict the future outcomes. There are two types of forecasting short-term and long-term.

Advantage: It helps in providing an idea about the required budgets to minimize the risks

associated with the activities and to compare the actual with standard to analyse the

variance and correct it (Zoni, Dossi and Morelli, 2012).

Disadvantage: The forecasting is not always correct as the future is uncertain.

Scenario Planning: The planning is done in a structured way for evaluation of various

outcomes in future in respect to strategic, operational and financial planning.

Advantage: The main advantage is that the planning is done by covering political,

economic, social and technological areas. All these provide a better insight about the

requirement and control of budgets.

Disadvantage: It involves various future alternatives of a situation there for decision

making becomes confusing. Absorption costing. 2018

Contingency plan: The contingency plan is prepared to handle emergency situations

which are beyond control and expectations. These are the back-up plans for future contingencies.

Advantage: Planning for contingencies can save the company from major financial

problems and risks.

Disadvantage: The amount and time used for planning contingencies will be a huge

wastage if no such contingency occurs in future.

From the above-mentioned tools, the use of forecasting tool is to predict the future, make

budgets, and control the variances between the actual and standard. This planning helps the

company to predict what will happen in future from the past data. The actual results are

measured with the standard to find out the variance. The variance is corrected by corrective

measure and enables the company to control in a better way.

The use of scenario tool is that it provide a detail planning about the various outcomes

that may happen in future. The company may decide a task and do the planning according to the

particular task by considering the overall aspects of the organization. This gives a whole picture

of how to plan so that all the company can control the budgets allocated to different departments.

The use of contingency planning is to prepare for unexpected yet possible situations in future. If

this planning is done rightly it can save company from the unexpected financial losses (Lavia

López and Hiebl, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

1:Comparison for how organizations are adopting management accounting system to respond to

financial problems:

Management accounting: A process of preparation of accounts and management reports

to make available the important financial and operational information required by managers

whereas Financial accounting is basically associated with producing the reports on annual basis

for external parties like stakeholders. Most of the enterprises use the financial and non financial

information for revealing their success in accomplishing the long term goals.

Financial Indicators: There are various ratios available to determine the sustainability

and success of the company in the market (DRURY, 2013).

Basis KPI Interpretation

Liquidity, solvency and debt

ratio

- Current ratio

- Quick ratio

- Woking capital

-Debt to equity

-Accounts payable to

inventory

Indicates the ability to pay

short term obligations.

Availability of liquid assets to

meet out short-term debt.

Sufficiency of the amount to

meet out day-to-day

requirements.

Indicates the proportion of

debt to equity utilized for

financing of assets.

Amount of the accounts

payable outstanding to the

inventory level.

Profitability ratios - Gross profit margin

-Net profit margin

A percentage of sales which is

used in paying operating cost

by making profit.

Indicates net profit earned by

the company.

1:Comparison for how organizations are adopting management accounting system to respond to

financial problems:

Management accounting: A process of preparation of accounts and management reports

to make available the important financial and operational information required by managers

whereas Financial accounting is basically associated with producing the reports on annual basis

for external parties like stakeholders. Most of the enterprises use the financial and non financial

information for revealing their success in accomplishing the long term goals.

Financial Indicators: There are various ratios available to determine the sustainability

and success of the company in the market (DRURY, 2013).

Basis KPI Interpretation

Liquidity, solvency and debt

ratio

- Current ratio

- Quick ratio

- Woking capital

-Debt to equity

-Accounts payable to

inventory

Indicates the ability to pay

short term obligations.

Availability of liquid assets to

meet out short-term debt.

Sufficiency of the amount to

meet out day-to-day

requirements.

Indicates the proportion of

debt to equity utilized for

financing of assets.

Amount of the accounts

payable outstanding to the

inventory level.

Profitability ratios - Gross profit margin

-Net profit margin

A percentage of sales which is

used in paying operating cost

by making profit.

Indicates net profit earned by

the company.

Non- financial Indicators:

Management of human resources : Employees are the most important assets of the

company. Employees contribute to the success of the business. The elements that are

included in human resource are staff turnover, % of jobs offers accepted etc.

Product and service quality: Quality is what makes the goodwill of a business. People

are willing to pay any price if the business serves good quality products. The quality of

products and service helps the company to sustain in the long- run and by providing

quality that company can grab a huge market share. The company should make sure it

fulfils the customer needs and considered customer's satisfaction a basis for evaluating

the success (Boyns and Edwards, 2011).

Brand awareness and company profile: A company can assess the growth by

measuring the brand value. Brand value reflects the future growth and development of the

company. It includes aspects like high loyalty, name awareness, quality, patents,

trademarks etc.

2:Analysis use for solving financial problems for its sustainable success

Sensitivity Analysis: This analysis is used to evaluate various scenarios that may happen

in future and their respective impacts. The analysis is done by taking into account different

assumptions about the expected situations. This analysis helps the company to determine the

level of profitability according to changes in the future.

Scenario Analysis: Under this analysis, the risk associated with the securities of the

company is estimated. The calculation is done to determine the cash flows and assets value under

various circumstances based on the risk factor. This analysis identifies the potential future

problems, the remedies to reduce the impact of the problems.

Stimulation analysis: It is used to calculate the financial and operational risks associated

with the company. These risks can influenced the overall profitability and success of the

company therefore are needed to be calculated for minimizing the risk. It is an research analysis

of the risk trend going on. By analysis , company can prepare the policies to reduce the risk and

maximize the profits.

Other than these analysis there are some other points which can contribute to the

sustainable success of the organization:

Management of human resources : Employees are the most important assets of the

company. Employees contribute to the success of the business. The elements that are

included in human resource are staff turnover, % of jobs offers accepted etc.

Product and service quality: Quality is what makes the goodwill of a business. People

are willing to pay any price if the business serves good quality products. The quality of

products and service helps the company to sustain in the long- run and by providing

quality that company can grab a huge market share. The company should make sure it

fulfils the customer needs and considered customer's satisfaction a basis for evaluating

the success (Boyns and Edwards, 2011).

Brand awareness and company profile: A company can assess the growth by

measuring the brand value. Brand value reflects the future growth and development of the

company. It includes aspects like high loyalty, name awareness, quality, patents,

trademarks etc.

2:Analysis use for solving financial problems for its sustainable success

Sensitivity Analysis: This analysis is used to evaluate various scenarios that may happen

in future and their respective impacts. The analysis is done by taking into account different

assumptions about the expected situations. This analysis helps the company to determine the

level of profitability according to changes in the future.

Scenario Analysis: Under this analysis, the risk associated with the securities of the

company is estimated. The calculation is done to determine the cash flows and assets value under

various circumstances based on the risk factor. This analysis identifies the potential future

problems, the remedies to reduce the impact of the problems.

Stimulation analysis: It is used to calculate the financial and operational risks associated

with the company. These risks can influenced the overall profitability and success of the

company therefore are needed to be calculated for minimizing the risk. It is an research analysis

of the risk trend going on. By analysis , company can prepare the policies to reduce the risk and

maximize the profits.

Other than these analysis there are some other points which can contribute to the

sustainable success of the organization:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.