KAP015-3 Advances in Accounting: Risk Management in DBS Bank

VerifiedAdded on 2023/04/21

|11

|2353

|441

Report

AI Summary

This report aims to identify suitable risk management techniques for investors in DBS Bank, focusing on portfolio setting and risk management using Value at Risk (VAR) and the Capital Asset Pricing Model (CAPM). The research explores the effectiveness of CAPM and the impact of VAR on investors, using secondary data from sources like Bloomberg and DBS Bank's annual reports. The methodology involves a quantitative approach, employing CAPM for stability testing of Beta Coefficients and VAR for assessing risk preferences. Ethical considerations, such as privacy and confidentiality, are addressed, and the validity of the analysis is ensured through reliable financial data. The research contributes to understanding the quantitative measurement of anticipated risk for DBS Bank investors, with limitations acknowledged regarding the scope of risk assessment within the banking sector and the specific techniques employed.

Running head: ADVANCES IN ACCOUNTING

Advances in Accounting

Name of the Student

Name of the University

Author’s Note

Advances in Accounting

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCES IN ACCOUNTING

Table of Contents

Introduction..........................................................................................................................3

1.1 Background of the study............................................................................................3

1.2 Research Aim.............................................................................................................3

1.3 Research Objective....................................................................................................3

1.4 Research Question.....................................................................................................3

1.5 Rationale for the research..........................................................................................4

2.0 Literature Review..........................................................................................................4

2.1 Process associated to Risk Management...................................................................4

2.2 Capital Asset Pricing Model......................................................................................4

2.3 Value at Risk (VAR).................................................................................................5

3.0 Research Methodology..................................................................................................5

3.1 Research Approach....................................................................................................5

3.2 Data Collection and Analysis....................................................................................6

3.3 Method of Analysis....................................................................................................6

3.4 Data Analysis.............................................................................................................6

3.5 Planning Horizon.......................................................................................................7

3.6 Ethical Issues.............................................................................................................8

3.7 Validity of Analysis...................................................................................................8

3.8 Limitations of the Research.......................................................................................8

4.0 Conclusion.....................................................................................................................9

References..........................................................................................................................10

Table of Contents

Introduction..........................................................................................................................3

1.1 Background of the study............................................................................................3

1.2 Research Aim.............................................................................................................3

1.3 Research Objective....................................................................................................3

1.4 Research Question.....................................................................................................3

1.5 Rationale for the research..........................................................................................4

2.0 Literature Review..........................................................................................................4

2.1 Process associated to Risk Management...................................................................4

2.2 Capital Asset Pricing Model......................................................................................4

2.3 Value at Risk (VAR).................................................................................................5

3.0 Research Methodology..................................................................................................5

3.1 Research Approach....................................................................................................5

3.2 Data Collection and Analysis....................................................................................6

3.3 Method of Analysis....................................................................................................6

3.4 Data Analysis.............................................................................................................6

3.5 Planning Horizon.......................................................................................................7

3.6 Ethical Issues.............................................................................................................8

3.7 Validity of Analysis...................................................................................................8

3.8 Limitations of the Research.......................................................................................8

4.0 Conclusion.....................................................................................................................9

References..........................................................................................................................10

2ADVANCES IN ACCOUNTING

Introduction

1.1 Background of the study

The decisions pertaining to investments are generally related to initiate specific actions

which will be able to improve the overall strategic position of any company. This is needed to be

related to the analysis which are needed to be related to the various aspects of the basic changes

which are to be brought in the areas of decision making. The determination of the risk factors is

inferred as per considering the relationship of the technological parameters, cost and time (Buyl,

Boone and Wade 2017).

1.2 Research Aim

The aim of the research is to identify the suitable risk management technique for the

investors in DBS Bank.

1.3 Research Objective

The main objectives of the research are listed as follows:

Identification of the most suitable portfolio setting and management of the risk of

investors in DBS Bank

Risk management of investors in DBS Bank by VAR and CPM

1.4 Research Question

The questions for the research are listed as follows:

What is effectiveness of the risk management with the application of CAPM?

What is impact of risk management VAR on the investors?

Introduction

1.1 Background of the study

The decisions pertaining to investments are generally related to initiate specific actions

which will be able to improve the overall strategic position of any company. This is needed to be

related to the analysis which are needed to be related to the various aspects of the basic changes

which are to be brought in the areas of decision making. The determination of the risk factors is

inferred as per considering the relationship of the technological parameters, cost and time (Buyl,

Boone and Wade 2017).

1.2 Research Aim

The aim of the research is to identify the suitable risk management technique for the

investors in DBS Bank.

1.3 Research Objective

The main objectives of the research are listed as follows:

Identification of the most suitable portfolio setting and management of the risk of

investors in DBS Bank

Risk management of investors in DBS Bank by VAR and CPM

1.4 Research Question

The questions for the research are listed as follows:

What is effectiveness of the risk management with the application of CAPM?

What is impact of risk management VAR on the investors?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCES IN ACCOUNTING

1.5 Rationale for the research

The risk of the investment decision is understood in terms of quantitatively measuring the

anticipated risk associated to the risk of the investors in the shares of DBS Bank. In various ways

the risks are depicted with the identification of the best portfolio setting and also the method to

manage the risks in portfolio which are considered among the investors of the bank.

2.0 Literature Review

2.1 Process associated to Risk Management

The risk management process begins with identifying the potential factors of risk among

the investors. These are significantly ranging in term of sourcing the issues associated with

changes in the return in portfolio of the bank. The implementation of the risk management is

inferred in terms of commencement of the different types of the strategies associated to

definition of risk used with the decision-making factors (Schanzenbach and Sitkoff 2017).

2.2 Capital Asset Pricing Model

The CAPM is set on the model of portfolio designed by Harry Markowitz in 1959. This

particular model is seen to be based on the use “mean-variance of the efficient portfolio”. The

risk management procedure in general inferred with ideal systematic management of the

investor’s risk. The systematic risk is referred as the related investment risks. In case the interest

rate is considerably high then an individual can consider the rate of inflation for resistant factors

(Greenwood, Landier and Thesmar 2015). The CAPM model is also considered with the mean-

variance of two more assumptions which were seen to be added in the assumptions proposed by

Markowitz. The vast degree of practical application is seen to be ideal for the estimation of cost

of capital which is necessary for the evaluation of the effectiveness of managing the portfolio.

The important assumptions for this model as per the investors is seen to be based on attaining the

1.5 Rationale for the research

The risk of the investment decision is understood in terms of quantitatively measuring the

anticipated risk associated to the risk of the investors in the shares of DBS Bank. In various ways

the risks are depicted with the identification of the best portfolio setting and also the method to

manage the risks in portfolio which are considered among the investors of the bank.

2.0 Literature Review

2.1 Process associated to Risk Management

The risk management process begins with identifying the potential factors of risk among

the investors. These are significantly ranging in term of sourcing the issues associated with

changes in the return in portfolio of the bank. The implementation of the risk management is

inferred in terms of commencement of the different types of the strategies associated to

definition of risk used with the decision-making factors (Schanzenbach and Sitkoff 2017).

2.2 Capital Asset Pricing Model

The CAPM is set on the model of portfolio designed by Harry Markowitz in 1959. This

particular model is seen to be based on the use “mean-variance of the efficient portfolio”. The

risk management procedure in general inferred with ideal systematic management of the

investor’s risk. The systematic risk is referred as the related investment risks. In case the interest

rate is considerably high then an individual can consider the rate of inflation for resistant factors

(Greenwood, Landier and Thesmar 2015). The CAPM model is also considered with the mean-

variance of two more assumptions which were seen to be added in the assumptions proposed by

Markowitz. The vast degree of practical application is seen to be ideal for the estimation of cost

of capital which is necessary for the evaluation of the effectiveness of managing the portfolio.

The important assumptions for this model as per the investors is seen to be based on attaining the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCES IN ACCOUNTING

target point of the effective frontier in which the return may be capitalized as per similar risk

level (Yet et al. 2016).

2.3 Value at Risk (VAR)

The depictions of the VAR are further seen to be largest pertaining to the reduction in the

value in a specific period for a certain degree of confidence. This particular technique will be

applied in consideration with the historical data as per non-parametric data. The computation of

the VAR is seen to be done as per the use of the percentile technique as per the desired

confidence interval. The application of the non-parametric VAR is regardless of the distribution

type (Arnold and Yildiz 2015).

3.0 Research Methodology

3.1 Research Approach

The main approach of the research is seen to be used with the use of suitable setting of

portfolio for the investors of DBS Bank. The contributing elements of the research is related to

the identification of the portfolio risk management among the investors in the bank. In addition

to this, the research horizon will be inferred in five stages. The first stage relates to ideation of

the research study (Karneyeva and Wüstenhagen 2017). This will be followed with stages such

as designing of the research, collection of data, publication of the data and analysis of the same.

It is seen to be important for understanding the research process which are formulated as per

important methods necessary for the process of risk management. The risk management process

will be further able to reveal about the information associated to the secondary resources (Brink

2017).

target point of the effective frontier in which the return may be capitalized as per similar risk

level (Yet et al. 2016).

2.3 Value at Risk (VAR)

The depictions of the VAR are further seen to be largest pertaining to the reduction in the

value in a specific period for a certain degree of confidence. This particular technique will be

applied in consideration with the historical data as per non-parametric data. The computation of

the VAR is seen to be done as per the use of the percentile technique as per the desired

confidence interval. The application of the non-parametric VAR is regardless of the distribution

type (Arnold and Yildiz 2015).

3.0 Research Methodology

3.1 Research Approach

The main approach of the research is seen to be used with the use of suitable setting of

portfolio for the investors of DBS Bank. The contributing elements of the research is related to

the identification of the portfolio risk management among the investors in the bank. In addition

to this, the research horizon will be inferred in five stages. The first stage relates to ideation of

the research study (Karneyeva and Wüstenhagen 2017). This will be followed with stages such

as designing of the research, collection of data, publication of the data and analysis of the same.

It is seen to be important for understanding the research process which are formulated as per

important methods necessary for the process of risk management. The risk management process

will be further able to reveal about the information associated to the secondary resources (Brink

2017).

5ADVANCES IN ACCOUNTING

3.2 Data Collection and Analysis

The process of collection of the information will be taken into account with the depiction

of the secondary information. The secondary information will also include the value in returns

pertaining to the portfolio available website like Bloomberg and annual report of the company.

The information available as per the return of the portfolio is seen to be useful as per the

financial health of the company (Adhikari and Agrawal 2016). This information may be used by

the investors pertaining to the risk management process based on the identification of the

available information like risk mitigation and risk identification with CAPM and VAR. The

information collected from the annual report will be related to inferring the financial health of a

company. This information needs to be considered as per risk management process and use of

available information such as liquidity position. The financial position of the company will be

also inferred in terms of extracting information such as efficiency ratio and leverage ratio

(Calomiris and Carlson 2016).

3.3 Method of Analysis

The interpretation of the data will be further used as per quantitative research technique.

The analysis technique of the research will be inferred with the use of CAPM and VAR. The

CAPM will include the Stability of test for the Beta Coefficients. The portfolio effectiveness is

further seen with measurement pertaining to managing the portfolio. The assumption of the

CAPM will be depicted as frontier in which the return will be capitalized as per similar level of

risk (Kumar et al. 2016).

3.4 Data Analysis

The analysis with the use of mean variance shall be considered with specific aspects of

the risk. The research results will be analysed with the grouping of data within 50 investors who

will be able to provide a rationale on the use of definite method for the risk management in DBS

3.2 Data Collection and Analysis

The process of collection of the information will be taken into account with the depiction

of the secondary information. The secondary information will also include the value in returns

pertaining to the portfolio available website like Bloomberg and annual report of the company.

The information available as per the return of the portfolio is seen to be useful as per the

financial health of the company (Adhikari and Agrawal 2016). This information may be used by

the investors pertaining to the risk management process based on the identification of the

available information like risk mitigation and risk identification with CAPM and VAR. The

information collected from the annual report will be related to inferring the financial health of a

company. This information needs to be considered as per risk management process and use of

available information such as liquidity position. The financial position of the company will be

also inferred in terms of extracting information such as efficiency ratio and leverage ratio

(Calomiris and Carlson 2016).

3.3 Method of Analysis

The interpretation of the data will be further used as per quantitative research technique.

The analysis technique of the research will be inferred with the use of CAPM and VAR. The

CAPM will include the Stability of test for the Beta Coefficients. The portfolio effectiveness is

further seen with measurement pertaining to managing the portfolio. The assumption of the

CAPM will be depicted as frontier in which the return will be capitalized as per similar level of

risk (Kumar et al. 2016).

3.4 Data Analysis

The analysis with the use of mean variance shall be considered with specific aspects of

the risk. The research results will be analysed with the grouping of data within 50 investors who

will be able to provide a rationale on the use of definite method for the risk management in DBS

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCES IN ACCOUNTING

Bank (Baker and Wurgler 2015). The VAR will be inferred with the indicator returns. This will

be able to provide a considerable amount of information which will be based on lower risk

preference. The Coefficient of Variation will be considered with the particular focus on the risk

taker as pe the matter associated to the investors who are seen to eb having a similar value when

it is compared with lower risk preference (Aven 2015).

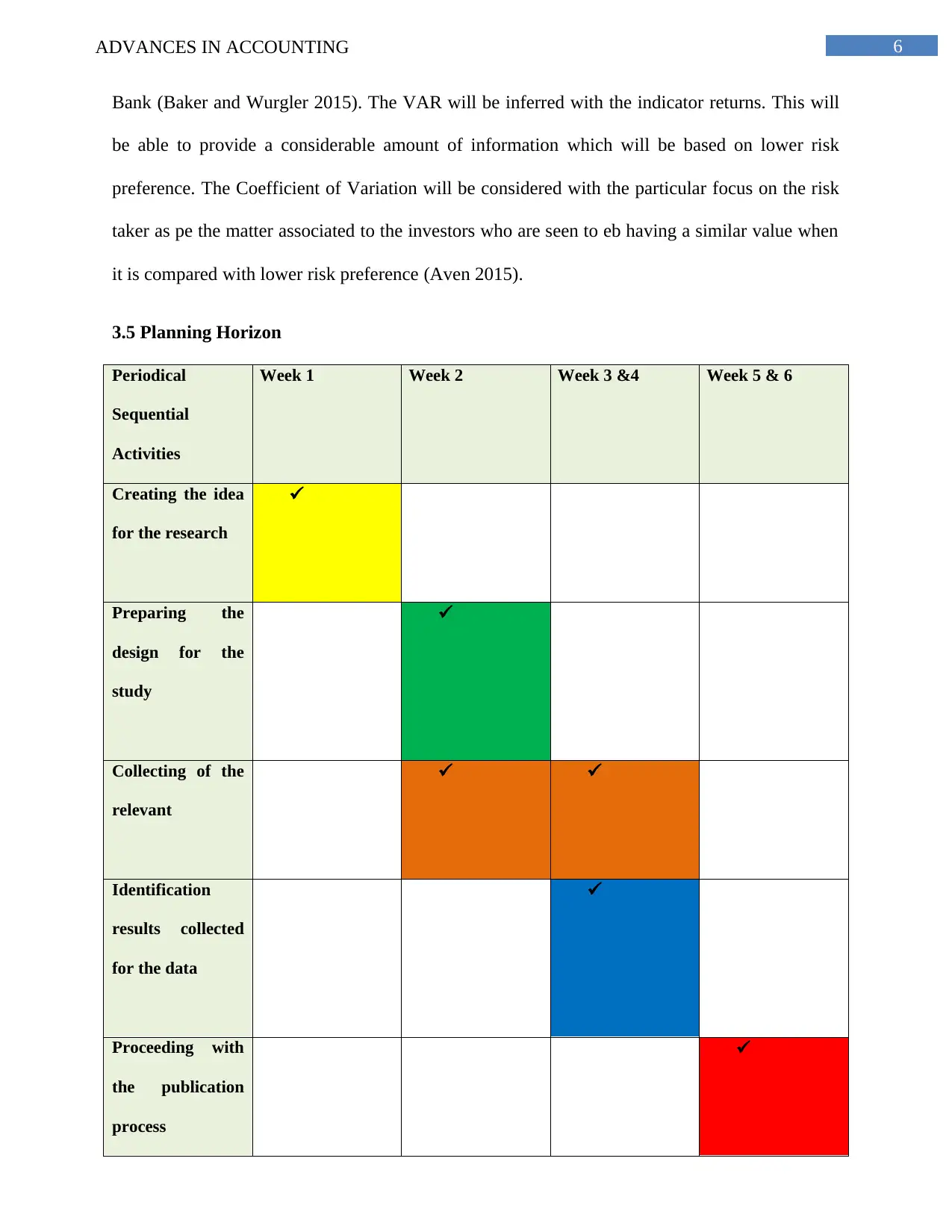

3.5 Planning Horizon

Periodical

Sequential

Activities

Week 1 Week 2 Week 3 &4 Week 5 & 6

Creating the idea

for the research

Preparing the

design for the

study

Collecting of the

relevant

Identification

results collected

for the data

Proceeding with

the publication

process

Bank (Baker and Wurgler 2015). The VAR will be inferred with the indicator returns. This will

be able to provide a considerable amount of information which will be based on lower risk

preference. The Coefficient of Variation will be considered with the particular focus on the risk

taker as pe the matter associated to the investors who are seen to eb having a similar value when

it is compared with lower risk preference (Aven 2015).

3.5 Planning Horizon

Periodical

Sequential

Activities

Week 1 Week 2 Week 3 &4 Week 5 & 6

Creating the idea

for the research

Preparing the

design for the

study

Collecting of the

relevant

Identification

results collected

for the data

Proceeding with

the publication

process

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCES IN ACCOUNTING

3.6 Ethical Issues

The ethical issues of the study will be evaluated with respect for privacy of confidential

information of DBS Bank. The increased concern for the vulnerable group is seen to be based on

the various types of the considerations pertaining to the vulnerability and welfare of the

individuals. The ethical aspect of the research will be also ensured with the principle of

Beneficence- Do not harm. This aspect will be able to make sure that research will consider all

the possible consequence for the research and at the same time balance the risks pertaining to the

proportionate benefit (Bromiley et al. 2015).

3.7 Validity of Analysis

The validity of the research analysis will be ensured with including relevant financial

information only as per annual report of the company. In addition to this, information about the

stock of the company will be seen to inferred as per the use of website such as Yahoo Finance

and Bloomberg.

3.8 Limitations of the Research

The main limitation of the research shall be considered only as per the risk assessment in

the banking sectors. Therefore, the use of the different types of the research techniques may be

differing in other form of research process. The limitation of the risk is also inferred as per

effectiveness of the risk management with the application of CAPM and impact of risk

management VAR on the investors. Therefore, different types of the other factors shall be

inferred as per use of only these techniques (Guiso, Sapienza and Zingales 2018).

3.6 Ethical Issues

The ethical issues of the study will be evaluated with respect for privacy of confidential

information of DBS Bank. The increased concern for the vulnerable group is seen to be based on

the various types of the considerations pertaining to the vulnerability and welfare of the

individuals. The ethical aspect of the research will be also ensured with the principle of

Beneficence- Do not harm. This aspect will be able to make sure that research will consider all

the possible consequence for the research and at the same time balance the risks pertaining to the

proportionate benefit (Bromiley et al. 2015).

3.7 Validity of Analysis

The validity of the research analysis will be ensured with including relevant financial

information only as per annual report of the company. In addition to this, information about the

stock of the company will be seen to inferred as per the use of website such as Yahoo Finance

and Bloomberg.

3.8 Limitations of the Research

The main limitation of the research shall be considered only as per the risk assessment in

the banking sectors. Therefore, the use of the different types of the research techniques may be

differing in other form of research process. The limitation of the risk is also inferred as per

effectiveness of the risk management with the application of CAPM and impact of risk

management VAR on the investors. Therefore, different types of the other factors shall be

inferred as per use of only these techniques (Guiso, Sapienza and Zingales 2018).

8ADVANCES IN ACCOUNTING

4.0 Conclusion

The research will be essential in understanding the of quantitatively measuring the

anticipated risk of the investors in the shares of DBS Bank. In various ways the risks are depicted

with the identification of the best portfolio setting and also the method to manage the risks in

portfolio among the investors of the bank. The main method for the research will be based on

designing of the research, collection of data, publication of the data and analysis of the same.

The analysis and collection of the data will be considered as per risk identification with CAPM

and VAR. Furthermore, the ethical issues of the study will be evaluated with respect for privacy

of confidential information of DBS Bank.

4.0 Conclusion

The research will be essential in understanding the of quantitatively measuring the

anticipated risk of the investors in the shares of DBS Bank. In various ways the risks are depicted

with the identification of the best portfolio setting and also the method to manage the risks in

portfolio among the investors of the bank. The main method for the research will be based on

designing of the research, collection of data, publication of the data and analysis of the same.

The analysis and collection of the data will be considered as per risk identification with CAPM

and VAR. Furthermore, the ethical issues of the study will be evaluated with respect for privacy

of confidential information of DBS Bank.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCES IN ACCOUNTING

References

Adhikari, B.K. and Agrawal, A., 2016. Does local religiosity matter for bank risk-

taking?. Journal of Corporate Finance, 38, pp.272-293.

Arnold, U. and Yildiz, Ö., 2015. Economic risk analysis of decentralized renewable energy

infrastructures–A Monte Carlo Simulation approach. Renewable Energy, 77, pp.227-239.

Aven, T., 2015. Risk analysis. John Wiley & Sons.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Brink, C.H., 2017. Measuring political risk: risks to foreign investment. Routledge.

Bromiley, P., McShane, M., Nair, A. and Rustambekov, E., 2015. Enterprise risk management:

Review, critique, and research directions. Long range planning, 48(4), pp.265-276.

Buyl, T., Boone, C. and Wade, J.B., 2017. CEO narcissism, risk-taking, and resilience: An

empirical analysis in US commercial banks. Journal of Management, p.0149206317699521.

Calomiris, C.W. and Carlson, M., 2016. Corporate governance and risk management at

unprotected banks: National banks in the 1890s. Journal of Financial Economics, 119(3),

pp.512-532.

Greenwood, R., Landier, A. and Thesmar, D., 2015. Vulnerable banks. Journal of Financial

Economics, 115(3), pp.471-485.

Guiso, L., Sapienza, P. and Zingales, L., 2018. Time varying risk aversion. Journal of Financial

Economics, 128(3), pp.403-421.

References

Adhikari, B.K. and Agrawal, A., 2016. Does local religiosity matter for bank risk-

taking?. Journal of Corporate Finance, 38, pp.272-293.

Arnold, U. and Yildiz, Ö., 2015. Economic risk analysis of decentralized renewable energy

infrastructures–A Monte Carlo Simulation approach. Renewable Energy, 77, pp.227-239.

Aven, T., 2015. Risk analysis. John Wiley & Sons.

Baker, M. and Wurgler, J., 2015. Do strict capital requirements raise the cost of capital? Bank

regulation, capital structure, and the low-risk anomaly. American Economic Review, 105(5),

pp.315-20.

Brink, C.H., 2017. Measuring political risk: risks to foreign investment. Routledge.

Bromiley, P., McShane, M., Nair, A. and Rustambekov, E., 2015. Enterprise risk management:

Review, critique, and research directions. Long range planning, 48(4), pp.265-276.

Buyl, T., Boone, C. and Wade, J.B., 2017. CEO narcissism, risk-taking, and resilience: An

empirical analysis in US commercial banks. Journal of Management, p.0149206317699521.

Calomiris, C.W. and Carlson, M., 2016. Corporate governance and risk management at

unprotected banks: National banks in the 1890s. Journal of Financial Economics, 119(3),

pp.512-532.

Greenwood, R., Landier, A. and Thesmar, D., 2015. Vulnerable banks. Journal of Financial

Economics, 115(3), pp.471-485.

Guiso, L., Sapienza, P. and Zingales, L., 2018. Time varying risk aversion. Journal of Financial

Economics, 128(3), pp.403-421.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCES IN ACCOUNTING

Karneyeva, Y. and Wüstenhagen, R., 2017. Solar feed-in tariffs in a post-grid parity world: The

role of risk, investor diversity and business models. Energy Policy, 106, pp.445-456.

Kumar, V., Natarajan, S., Keerthana, S., Chinmayi, K.M. and Lakshmi, N., 2016, September.

Credit risk analysis in peer-to-peer lending system. In Knowledge Engineering and Applications

(ICKEA), IEEE International Conference on (pp. 193-196). IEEE.

Schanzenbach, M.M. and Sitkoff, R.H., 2017. The prudent investor rule and market risk: an

empirical analysis. Journal of Empirical Legal Studies, 14(1), pp.129-168.

Yet, B., Constantinou, A., Fenton, N., Neil, M., Luedeling, E. and Shepherd, K., 2016. A

Bayesian network framework for project cost, benefit and risk analysis with an agricultural

development case study. Expert Systems with Applications, 60, pp.141-155.

Karneyeva, Y. and Wüstenhagen, R., 2017. Solar feed-in tariffs in a post-grid parity world: The

role of risk, investor diversity and business models. Energy Policy, 106, pp.445-456.

Kumar, V., Natarajan, S., Keerthana, S., Chinmayi, K.M. and Lakshmi, N., 2016, September.

Credit risk analysis in peer-to-peer lending system. In Knowledge Engineering and Applications

(ICKEA), IEEE International Conference on (pp. 193-196). IEEE.

Schanzenbach, M.M. and Sitkoff, R.H., 2017. The prudent investor rule and market risk: an

empirical analysis. Journal of Empirical Legal Studies, 14(1), pp.129-168.

Yet, B., Constantinou, A., Fenton, N., Neil, M., Luedeling, E. and Shepherd, K., 2016. A

Bayesian network framework for project cost, benefit and risk analysis with an agricultural

development case study. Expert Systems with Applications, 60, pp.141-155.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.