Comparative Ratio Analysis: Kathmandu Ltd and OrotonGroup

VerifiedAdded on 2020/03/02

|7

|1772

|98

Report

AI Summary

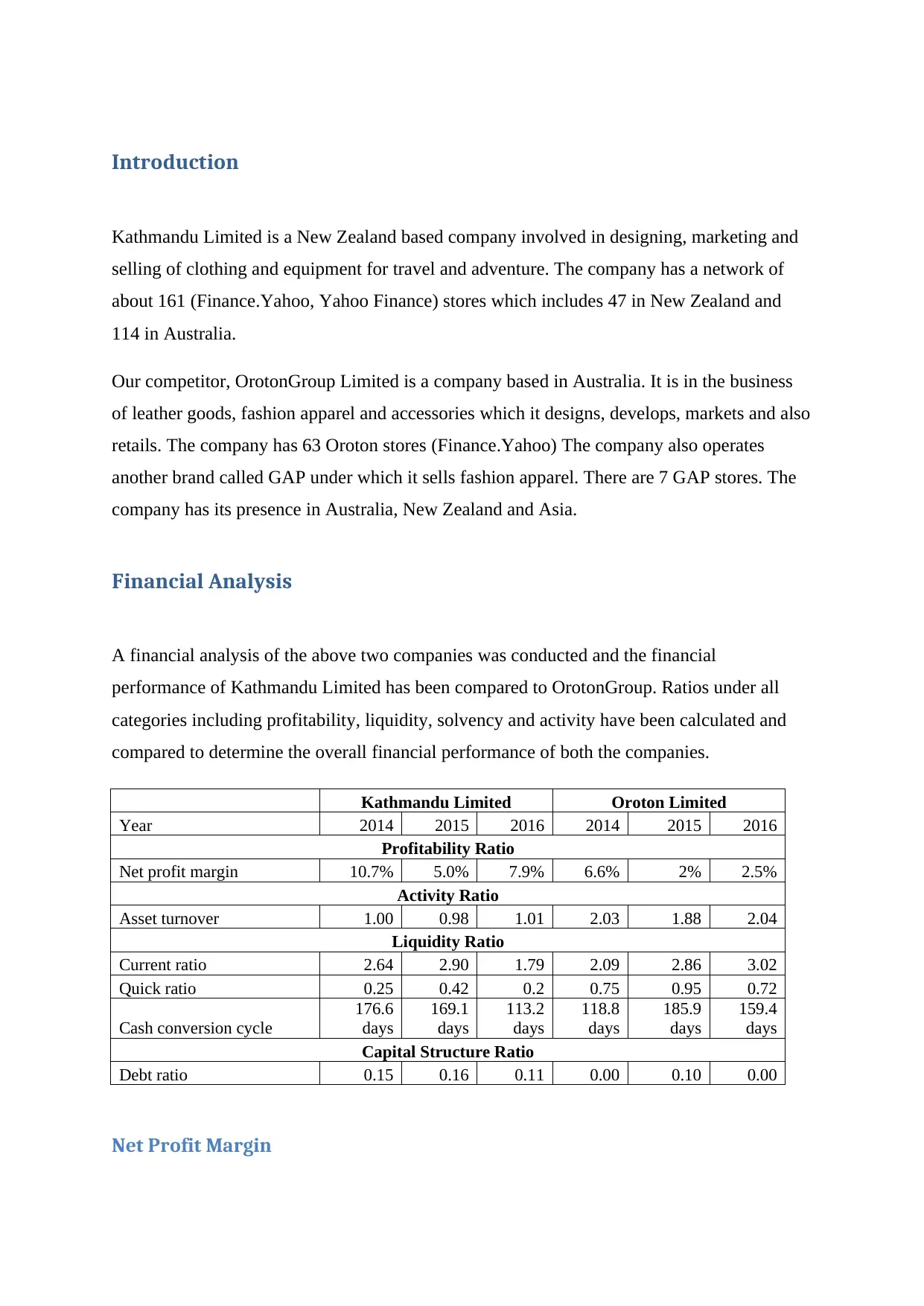

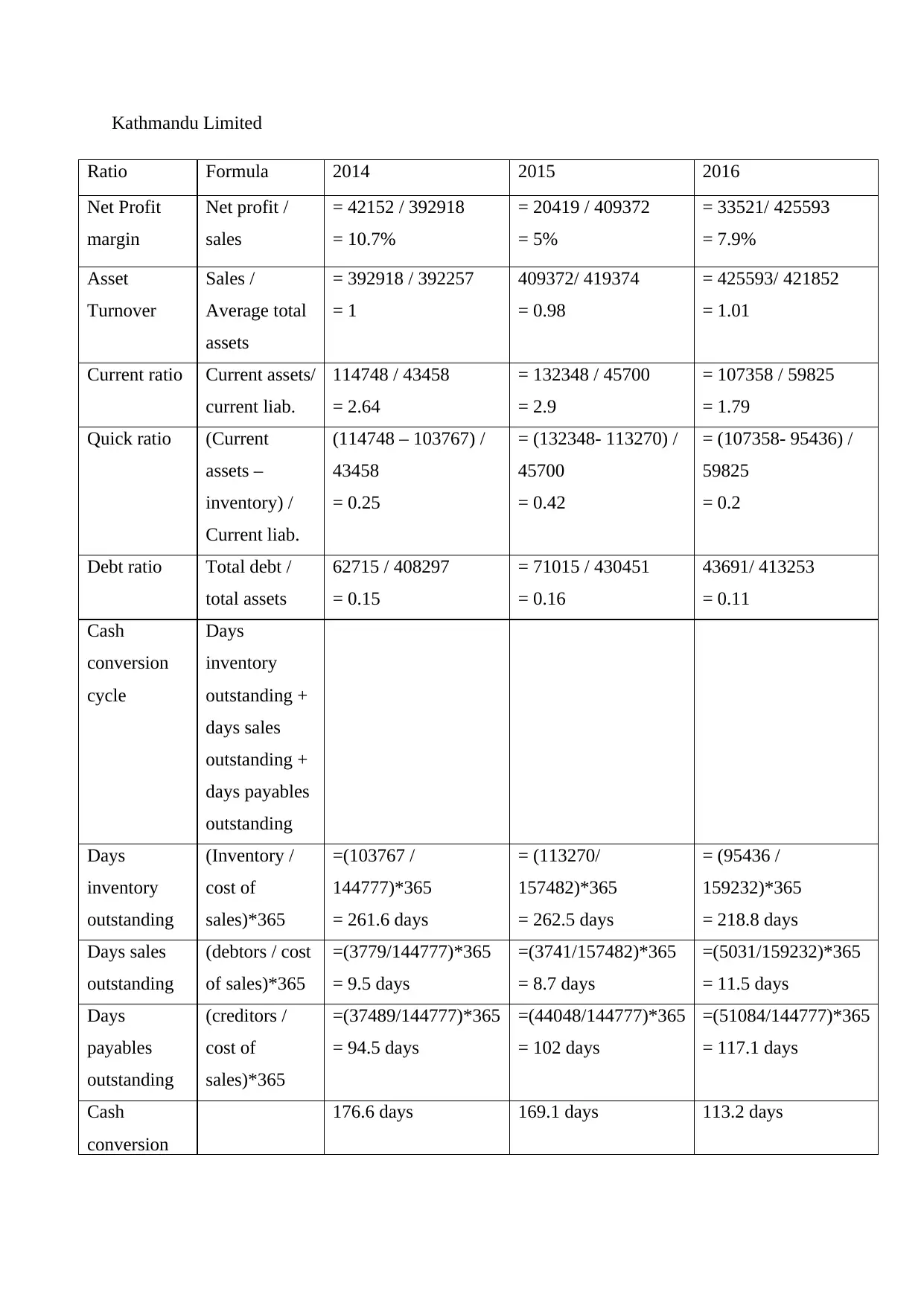

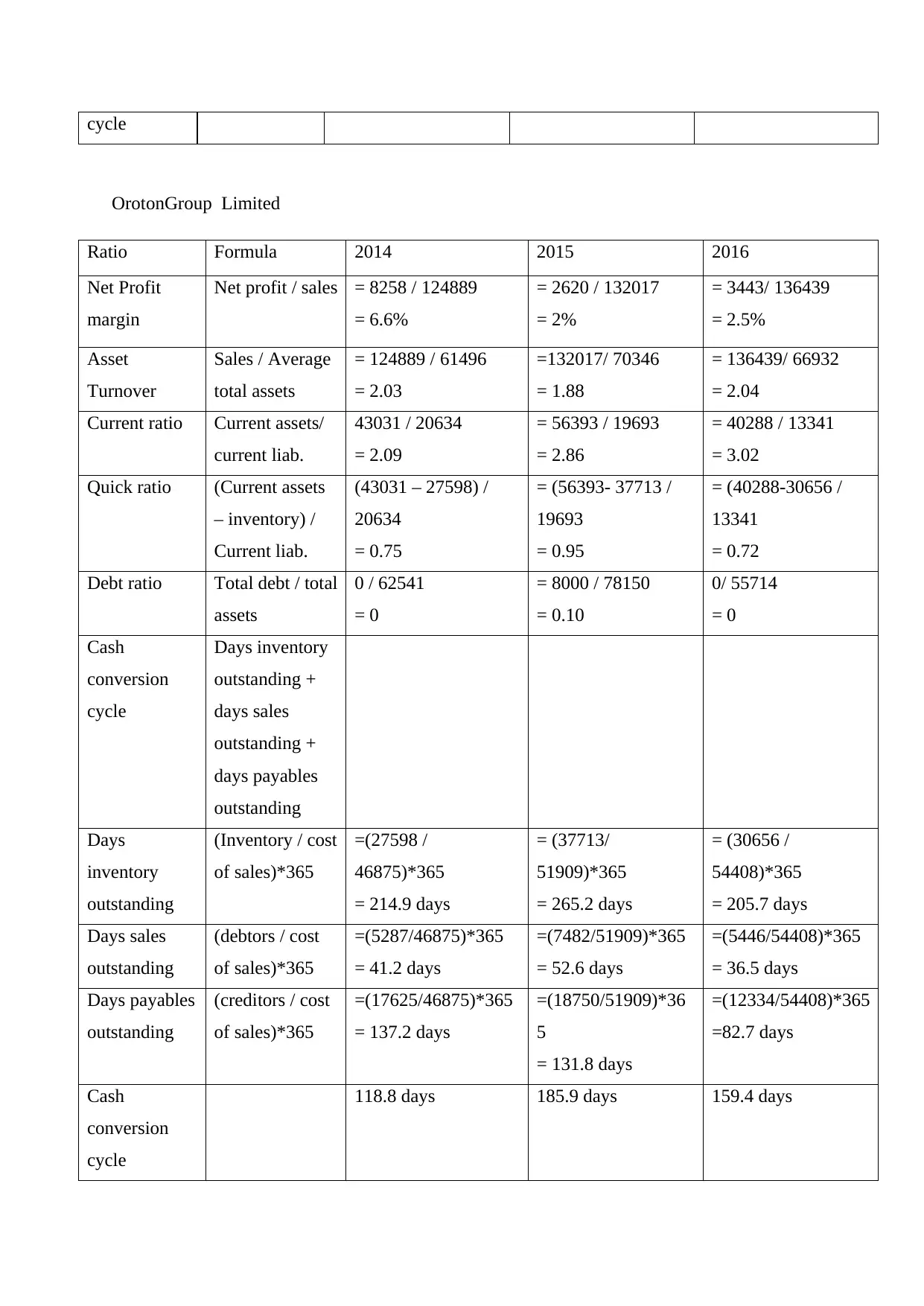

This report presents a comparative financial analysis of Kathmandu Limited and OrotonGroup, two companies operating in the retail and fashion industries. The analysis employs various financial ratios, including profitability (net profit margin), activity (asset turnover), liquidity (current and quick ratios), and capital structure (debt ratio), to assess and compare their financial performance over the period from 2014 to 2016. The report calculates and interprets these ratios, highlighting key trends and differences between the two companies. Kathmandu Limited demonstrates stronger profit margins, while OrotonGroup exhibits better asset utilization. The report also examines liquidity and solvency, revealing OrotonGroup's stronger position in these areas. Furthermore, the analysis includes a discussion of the cash conversion cycle and offers recommendations to potential investors, concluding that Kathmandu Limited is the more favorable investment due to its superior profit margins and potential for improved liquidity.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.