Kedison Plc & Chocco Plc: A Comprehensive Financial Analysis Report

VerifiedAdded on 2023/06/14

|11

|1668

|353

Homework Assignment

AI Summary

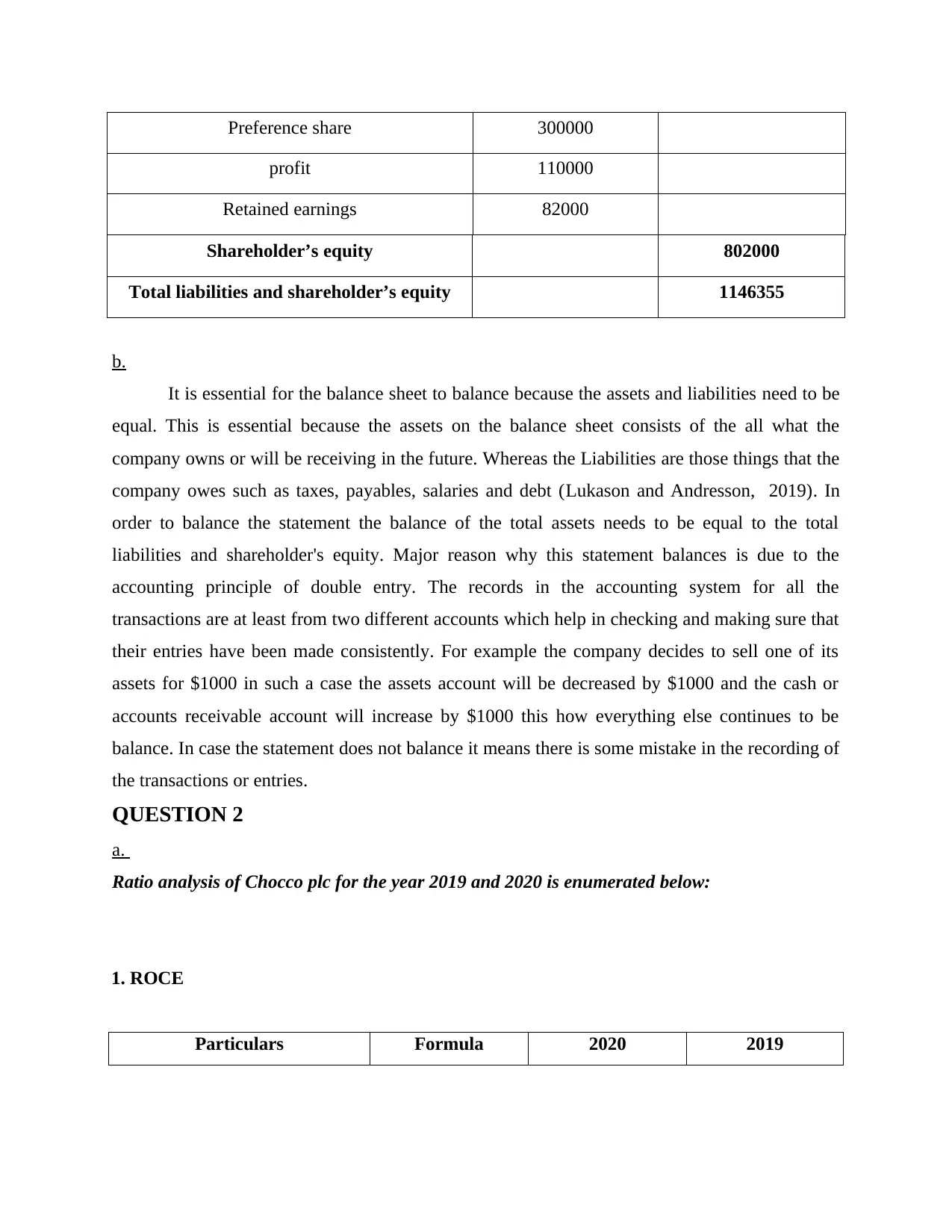

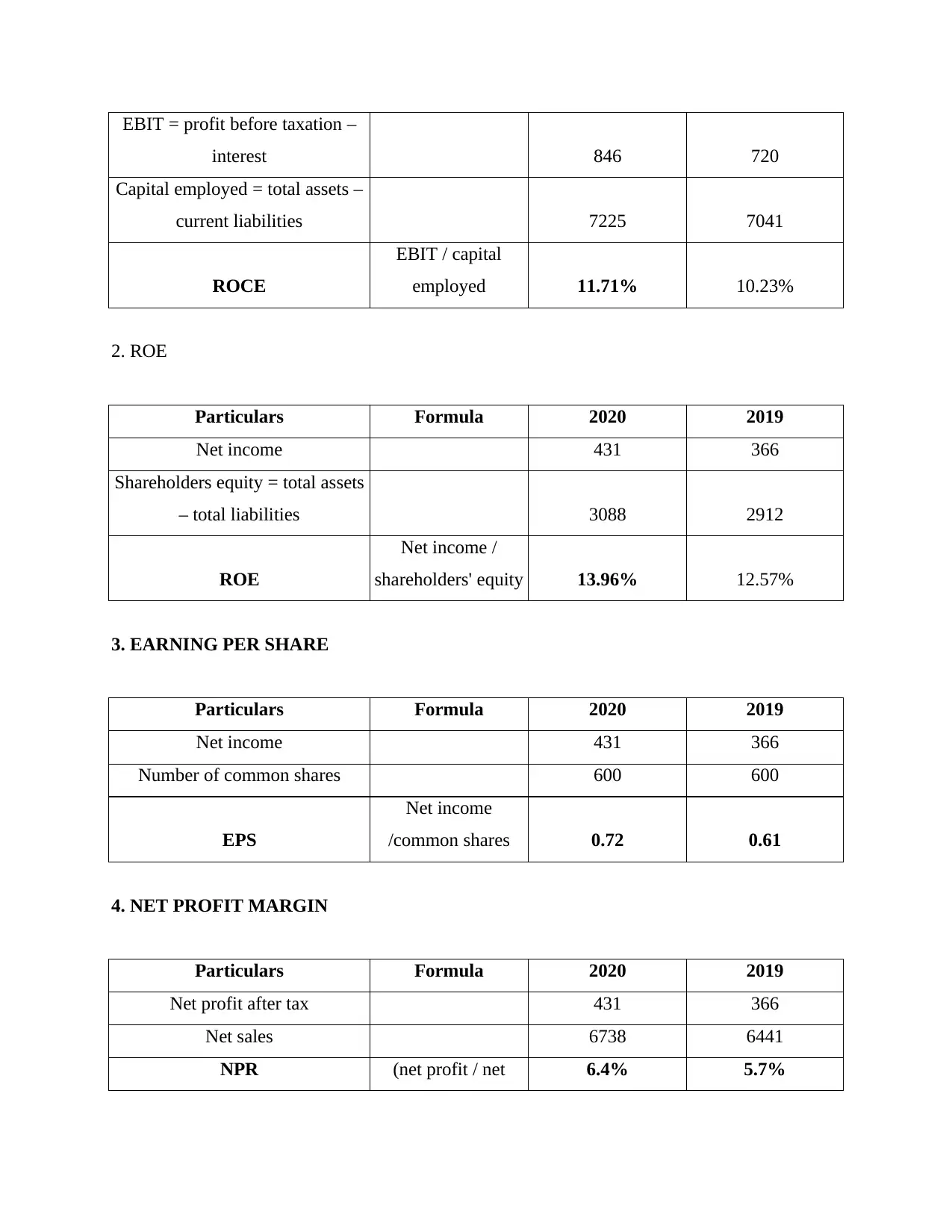

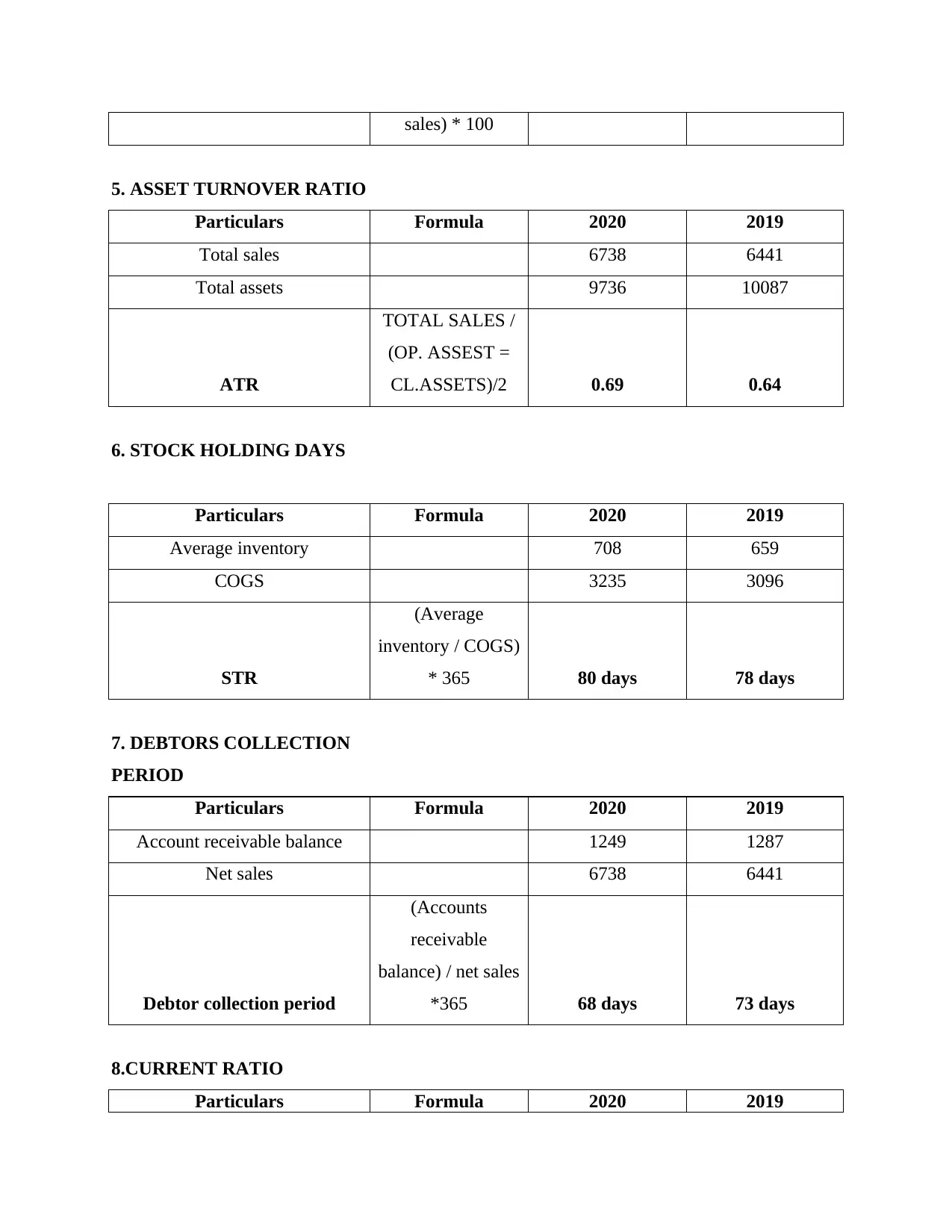

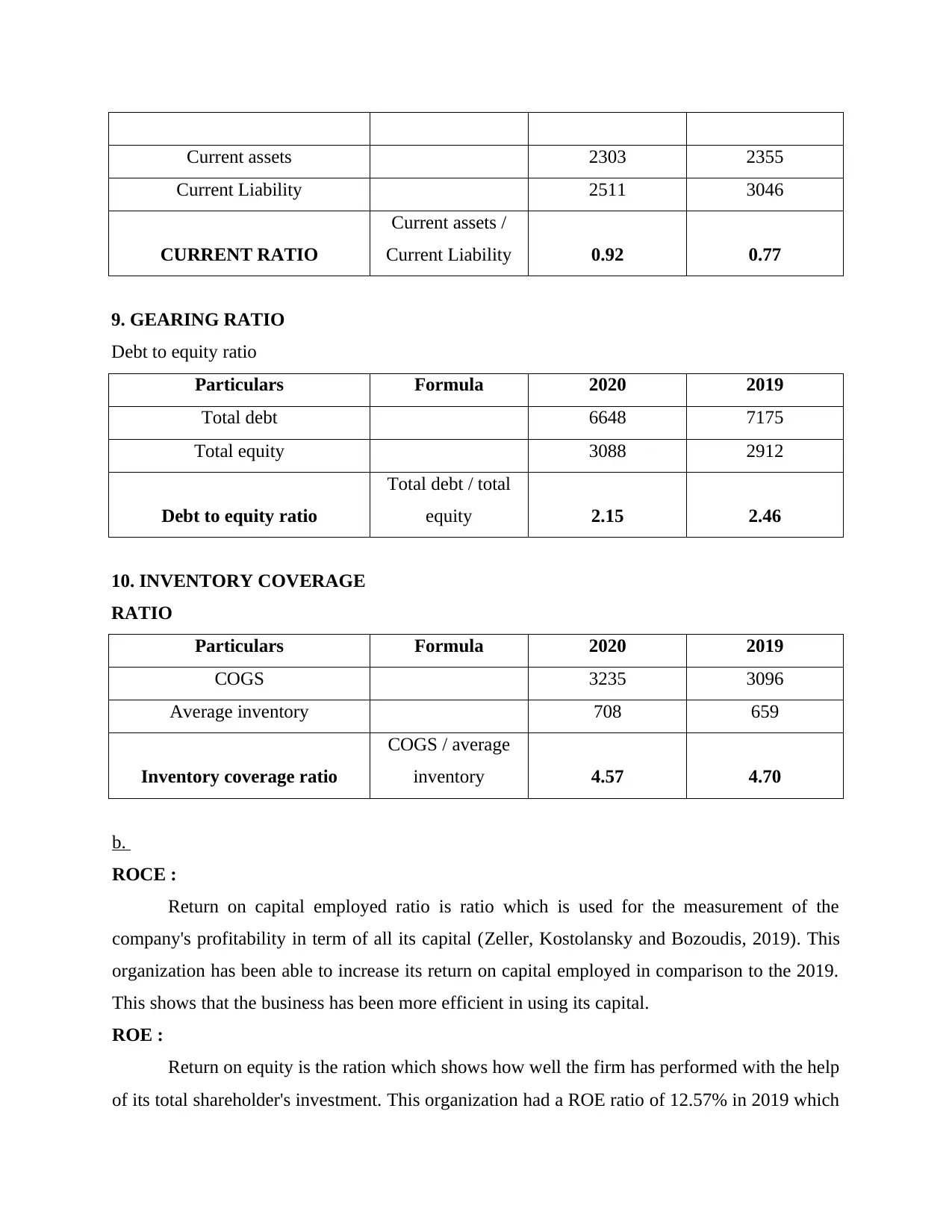

This assignment provides a comprehensive financial analysis of Kedison Plc and Chocco Plc. It includes the preparation of an income statement and balance sheet for Kedison Plc, along with an explanation of the importance of a balanced balance sheet. Furthermore, it conducts a detailed ratio analysis for Chocco Plc, covering key metrics such as ROCE, ROE, EPS, net profit margin, asset turnover ratio, stock holding days, debtors' collection period, current ratio, gearing ratio, and inventory coverage ratio. The analysis interprets these ratios to assess Chocco Plc's financial performance, highlighting areas of improvement and strengths. The assignment concludes with recommendations for enhancing the company's financial health, particularly focusing on inventory management to improve profitability and liquidity. Desklib provides access to similar solved assignments and past papers for students.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.