Comprehensive Management Accounting Report for KEF Limited Analysis

VerifiedAdded on 2021/02/21

|17

|3565

|317

Report

AI Summary

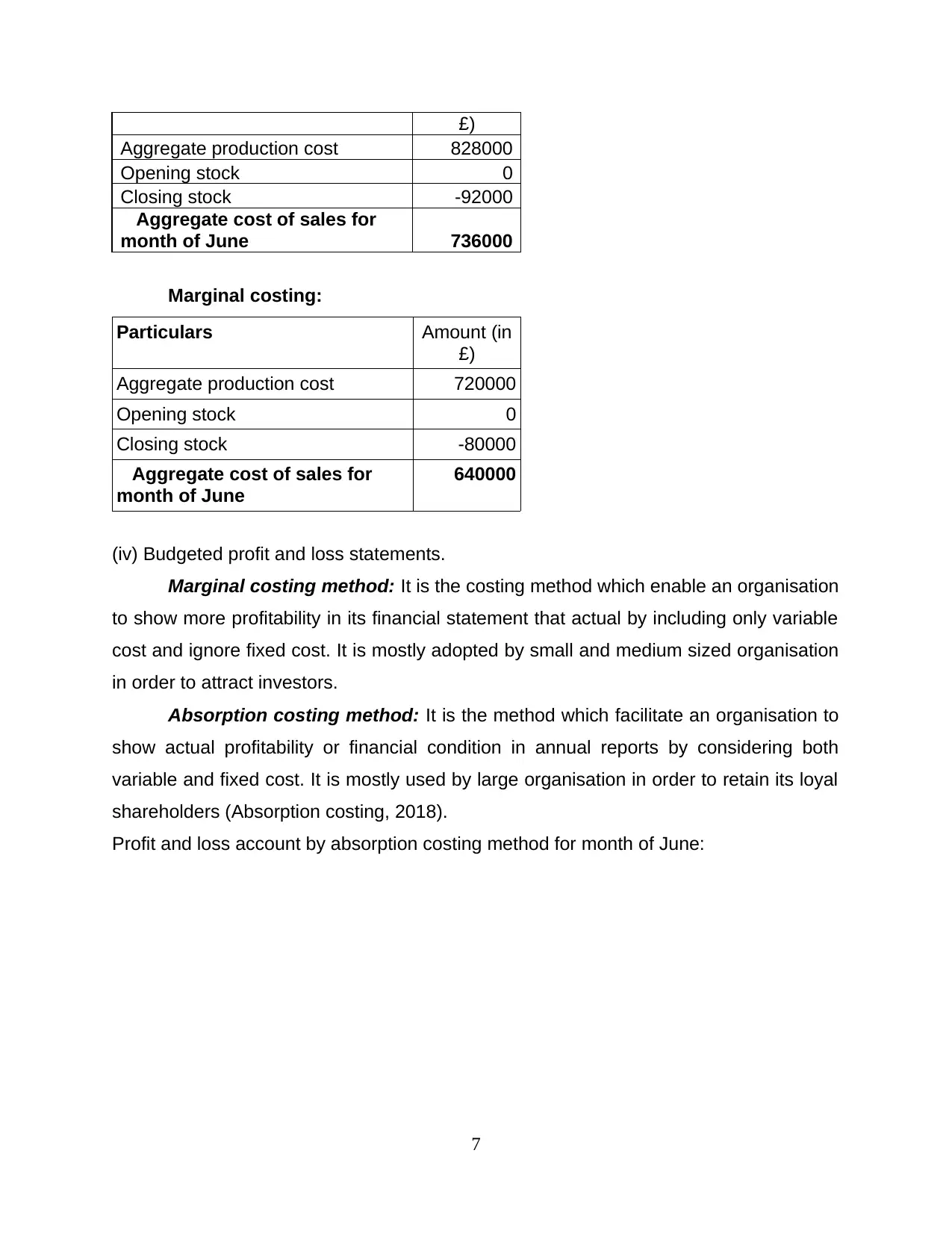

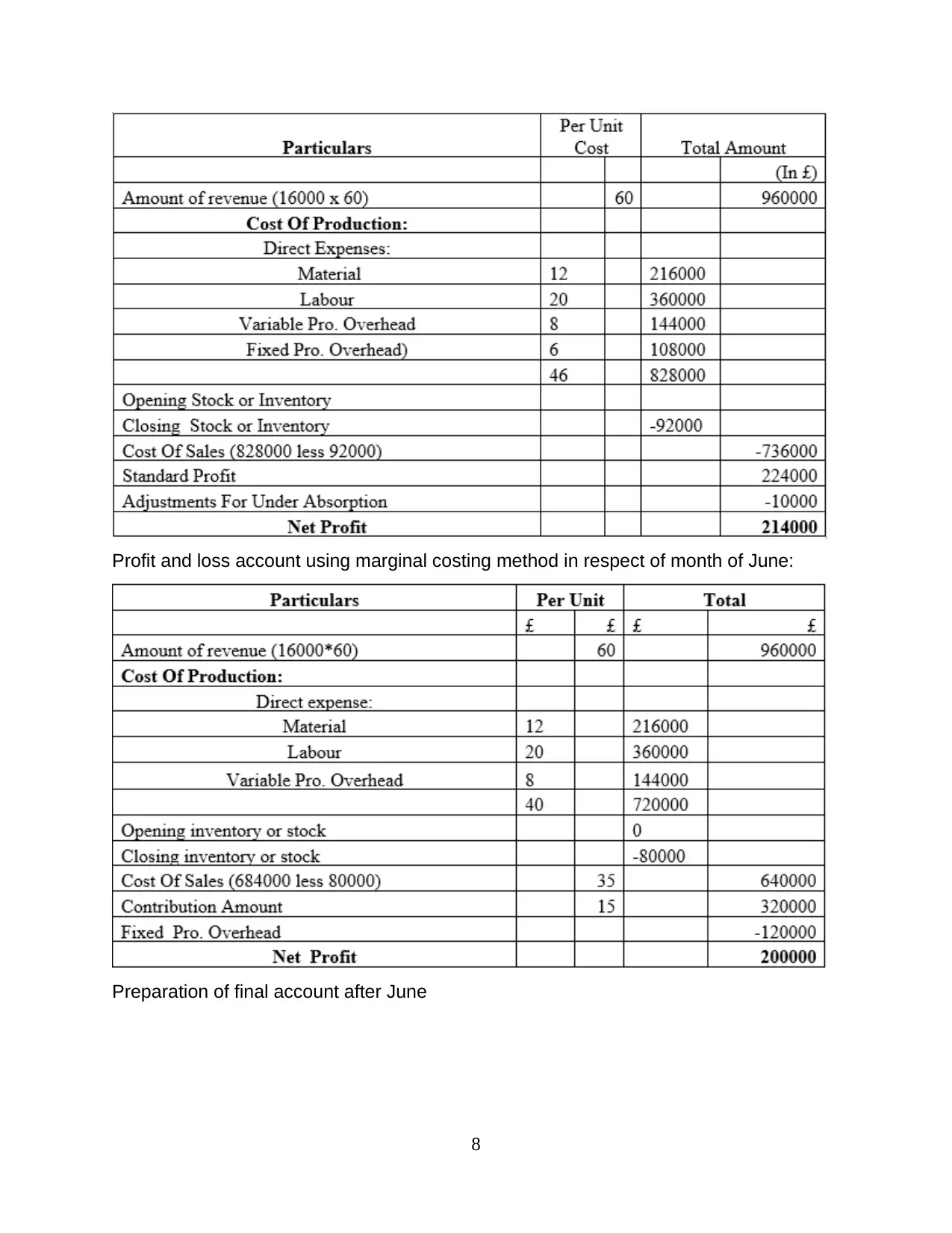

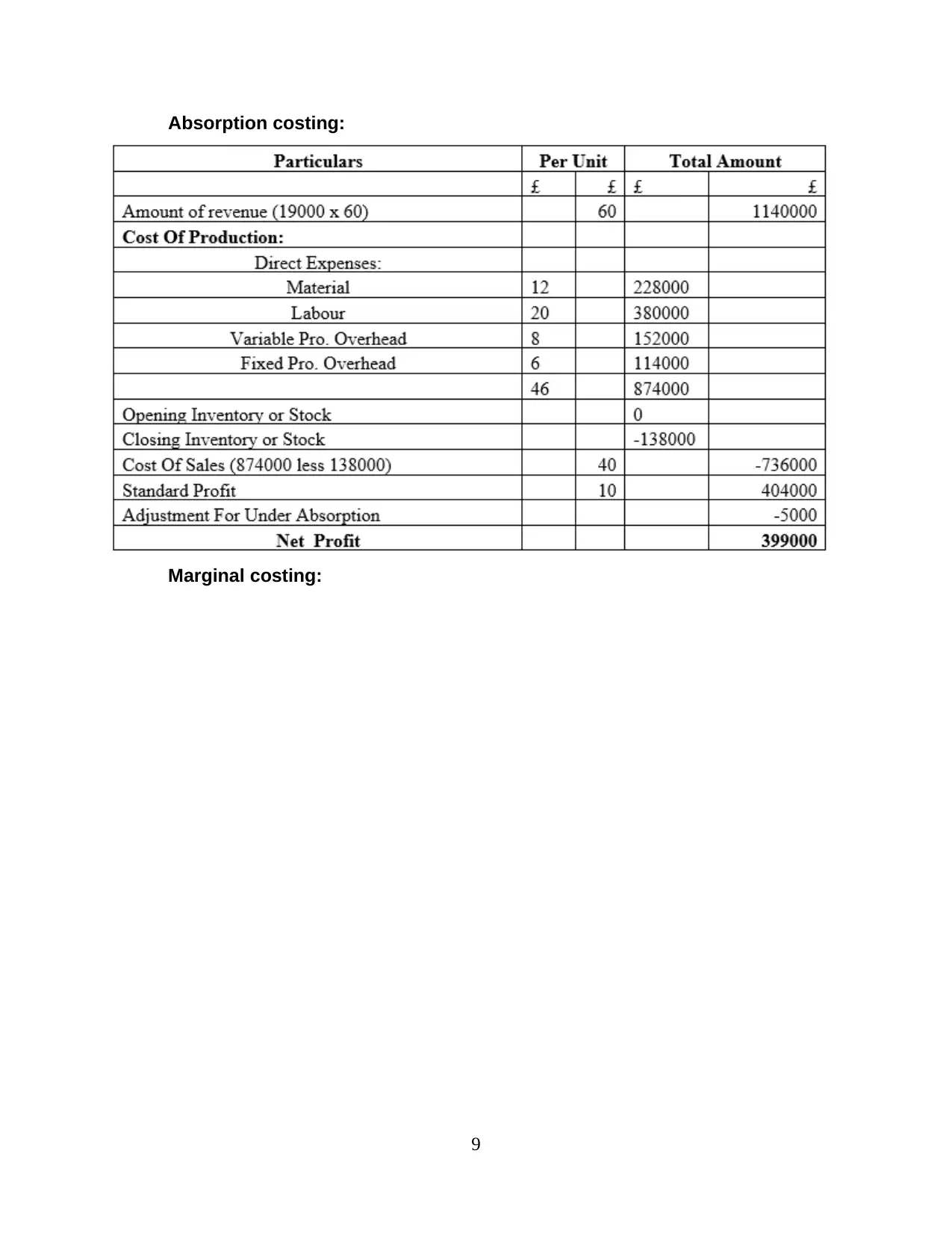

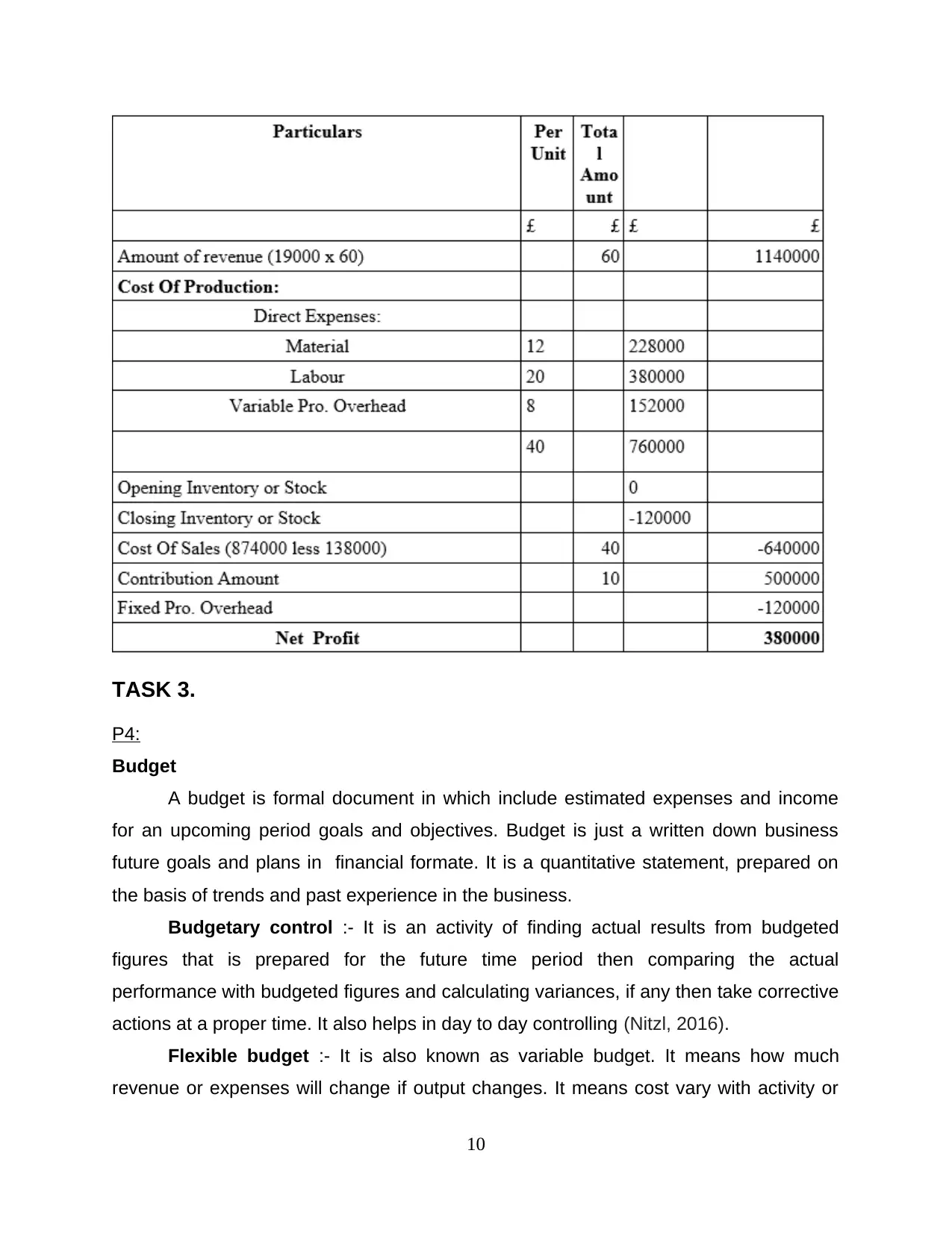

This report provides a comprehensive analysis of management accounting practices at KEF Limited. It begins with an introduction to management accounting and its role in organizational success, emphasizing the importance of financial statements and the responsibilities of accounting and finance managers. The report then delves into various management accounting systems, including cost accounting, price optimization, job costing, and inventory management systems, detailing their applications and benefits for KEF Limited. It further explores the significance of budget reports, accounts receivable reports, cost managerial accounting reports, and performance reports. The report also examines the integration between management accounting systems and reporting, using examples to illustrate their interconnectedness. Finally, it analyzes costing methods, specifically marginal and absorption costing, including detailed calculations of production costs, cost of sales, and budgeted profit and loss statements, providing a comparative analysis of the two methods and their impact on financial reporting.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.