KEF Limited: Management Accounting Systems and Applications Project

VerifiedAdded on 2023/01/18

|19

|3847

|34

Project

AI Summary

This project report delves into the realm of management accounting, focusing on its importance for companies, particularly KEF Limited, a manufacturing sector entity. The report meticulously covers various aspects, including different types of Management Accounting Systems (MAS) like inventory management, cost accounting, and price optimization systems. It further examines Management Accounting (MA) reports, such as accounts receivable aging reports, budget reports, and performance reports, along with their benefits. The project includes detailed calculations of production costs using absorption and marginal costing methods, alongside the preparation of income statements. Additionally, it explores the benefits and drawbacks of planning tools like budgetary control and capital budgeting, and provides suggestions for enhancing the company's financial strategies. The report emphasizes the integration of MAS and MA reports with organizational processes, offering a comprehensive analysis of management accounting principles and their practical applications.

MANAGEMENT

ACCOUNTING

SYSTEMS AND ITS

APPLICATIONS

ACCOUNTING

SYSTEMS AND ITS

APPLICATIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...............................................................................................................3

MAIN BODY.......................................................................................................................3

Task 1............................................................................................................................3

Task 2............................................................................................................................6

Task 3..........................................................................................................................11

Task 4..........................................................................................................................13

CONCLUSION.................................................................................................................16

REFERENCES................................................................................................................17

REFERENCES................................................................................................................18

INTRODUCTION...............................................................................................................3

MAIN BODY.......................................................................................................................3

Task 1............................................................................................................................3

Task 2............................................................................................................................6

Task 3..........................................................................................................................11

Task 4..........................................................................................................................13

CONCLUSION.................................................................................................................16

REFERENCES................................................................................................................17

REFERENCES................................................................................................................18

INTRODUCTION

Management accounting is an act of taking relevant monetary & costing data and

turning the data into valuable information for administrators and managers within a

company. This is also known as managerial accounting, in other words it can be defined

as a method of analysing costs of doing business and procedures to prepare inner

financial reports, records to help managers for making decisions to achieve business

objectives (Crosson and Needles, 2013). The objective of project report is to evaluating

importance of MA for companies. In the project report, KEF limited company has been

chosen which operates in manufacturing sector.

The report covers detailed information about types of MAS, MA reports, costing

techniques and planning tools. In the end part of report role of MA in sorting monetary

issues is covered.

MAIN BODY

Task 1.

Meaning of management accounting and requirements of various MAS.

MA- Management accounting is the practice of preparing management statements and

accounts which provide reliable and appropriate numerical and qualitative information to

executives. This information is needed to make brief-term and lengthy-term judgements.

There are various types of MAS:

Inventory management system - The inventory management system is intended

to improve the work of producers who need to constantly monitor the flow of

stock across different manufacturing stages (Hart, Wilson and Fergus, 2012).

Essentially, even before the manufacturing process starts, a business uses the

inventory management system to identify the materials. Such raw materials

gradually transform in real-time to finished products. It is essential for companies

in order to track movement of material in entire production process. In the KEF

limited company, their manufacturing department implies this system which helps

in managing overall value of stock and for minimising cost.

Management accounting is an act of taking relevant monetary & costing data and

turning the data into valuable information for administrators and managers within a

company. This is also known as managerial accounting, in other words it can be defined

as a method of analysing costs of doing business and procedures to prepare inner

financial reports, records to help managers for making decisions to achieve business

objectives (Crosson and Needles, 2013). The objective of project report is to evaluating

importance of MA for companies. In the project report, KEF limited company has been

chosen which operates in manufacturing sector.

The report covers detailed information about types of MAS, MA reports, costing

techniques and planning tools. In the end part of report role of MA in sorting monetary

issues is covered.

MAIN BODY

Task 1.

Meaning of management accounting and requirements of various MAS.

MA- Management accounting is the practice of preparing management statements and

accounts which provide reliable and appropriate numerical and qualitative information to

executives. This information is needed to make brief-term and lengthy-term judgements.

There are various types of MAS:

Inventory management system - The inventory management system is intended

to improve the work of producers who need to constantly monitor the flow of

stock across different manufacturing stages (Hart, Wilson and Fergus, 2012).

Essentially, even before the manufacturing process starts, a business uses the

inventory management system to identify the materials. Such raw materials

gradually transform in real-time to finished products. It is essential for companies

in order to track movement of material in entire production process. In the KEF

limited company, their manufacturing department implies this system which helps

in managing overall value of stock and for minimising cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system - It is a method that businesses use to determine the

cost of their goods for the study of productivity, stock assessment and controlling

costs. It is important for successful operations to determine the exact cost of

products. A business must know that goods are competitive and which ones are

not, and this can only be calculated if the appropriate cost of the product has

been measured. Hence, it is essential for companies for accurate estimation of

costs and for reducing total expenditures. In the KEF limited company, their

finance department applies this system for managing cost of overall operations

and activities.

Price optimisation system – It is a type of accounting system which is aligned to

process of assessing how demand fluctuates at various price segments and after

that combining that data with information on costs to suggest prices which will

enhance profitability. This accounting system plays a key role for those

companies who want to make focus on targeted customers. In the aspect of KEF

limited company, they apply this accounting system which contributes them in

setting prices of products and services.

Job order costing system- Job order costing system is a cost accounting process

which accumulates manufacturing costs of each job individually. This accounting

system is applied in those businesses which manufacture products and services

in accordance of order of any party. As well as it is essential for companies in

computing cost of job which involves in process of operations.

In the KEF limited company, they apply this accounting system for better

management of cost of job.

Different method of MA reports.

MA reports- Management accounting reports can be defined as those written

documents which provide data that companies want to cut costs, award fast-performing

workers, cut stagnating products and reinvest in the products which provide the

company with the best possible return (Schwaiger and Abmayer, 2013). Below some

types of reports are described in such manner:

cost of their goods for the study of productivity, stock assessment and controlling

costs. It is important for successful operations to determine the exact cost of

products. A business must know that goods are competitive and which ones are

not, and this can only be calculated if the appropriate cost of the product has

been measured. Hence, it is essential for companies for accurate estimation of

costs and for reducing total expenditures. In the KEF limited company, their

finance department applies this system for managing cost of overall operations

and activities.

Price optimisation system – It is a type of accounting system which is aligned to

process of assessing how demand fluctuates at various price segments and after

that combining that data with information on costs to suggest prices which will

enhance profitability. This accounting system plays a key role for those

companies who want to make focus on targeted customers. In the aspect of KEF

limited company, they apply this accounting system which contributes them in

setting prices of products and services.

Job order costing system- Job order costing system is a cost accounting process

which accumulates manufacturing costs of each job individually. This accounting

system is applied in those businesses which manufacture products and services

in accordance of order of any party. As well as it is essential for companies in

computing cost of job which involves in process of operations.

In the KEF limited company, they apply this accounting system for better

management of cost of job.

Different method of MA reports.

MA reports- Management accounting reports can be defined as those written

documents which provide data that companies want to cut costs, award fast-performing

workers, cut stagnating products and reinvest in the products which provide the

company with the best possible return (Schwaiger and Abmayer, 2013). Below some

types of reports are described in such manner:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts receivable ageing report – This report indicates the outstanding

balance of the invoice along with the time they are exceptional for. Accounts

receivable ageing reporting help companies recognize open receipts and enable

them to stay on top of slow paying customers. Basically, the receivable occurs in

companies due to selling of products and services of debt. In the KEF limited

company, they are using this report for making better evaluation of debt payment

and receiving.

Budget report- Budget reporting is the method of assessing a firm's actual

accomplishment against its expected statistics. It lets them see if they are on

track to meet their business goals. It also allows the company to take appropriate

action where appropriate. On the basis of this report, managers of companies

keep in touch with overall performance. As well as they become able to make

and formulate effective strategies. In the KEF limited company, they prepare this

report for better management of performance.

Performance report- A performance report deals with the results of an individual's

behaviour or function. The document compares actual results with a plan or

norm, as well as the disparity between the two estimates (Yerdavletova, 2015). If

there is an adverse difference, the receiver of a progress report is supposed to

take action. By help of this report, performance of employees and different

functions is managed in an effective manner. In the KEF limited company, they

prepare this report for keeping performance of each aspect over standards.

Cost accounting report- A cost report provides an overview of all details regards

to raw material cost, overhead, labour cost etc. This report provides

administrators with the ability to recognize items' cost versus their sales prices.

Through these documents, profitability are measured and tracked as managers

have a clear understanding of all the costs involved in manufacturing or

distribution of the products. In the above company, their accountant prepares this

report for controlling cost of activities.

balance of the invoice along with the time they are exceptional for. Accounts

receivable ageing reporting help companies recognize open receipts and enable

them to stay on top of slow paying customers. Basically, the receivable occurs in

companies due to selling of products and services of debt. In the KEF limited

company, they are using this report for making better evaluation of debt payment

and receiving.

Budget report- Budget reporting is the method of assessing a firm's actual

accomplishment against its expected statistics. It lets them see if they are on

track to meet their business goals. It also allows the company to take appropriate

action where appropriate. On the basis of this report, managers of companies

keep in touch with overall performance. As well as they become able to make

and formulate effective strategies. In the KEF limited company, they prepare this

report for better management of performance.

Performance report- A performance report deals with the results of an individual's

behaviour or function. The document compares actual results with a plan or

norm, as well as the disparity between the two estimates (Yerdavletova, 2015). If

there is an adverse difference, the receiver of a progress report is supposed to

take action. By help of this report, performance of employees and different

functions is managed in an effective manner. In the KEF limited company, they

prepare this report for keeping performance of each aspect over standards.

Cost accounting report- A cost report provides an overview of all details regards

to raw material cost, overhead, labour cost etc. This report provides

administrators with the ability to recognize items' cost versus their sales prices.

Through these documents, profitability are measured and tracked as managers

have a clear understanding of all the costs involved in manufacturing or

distribution of the products. In the above company, their accountant prepares this

report for controlling cost of activities.

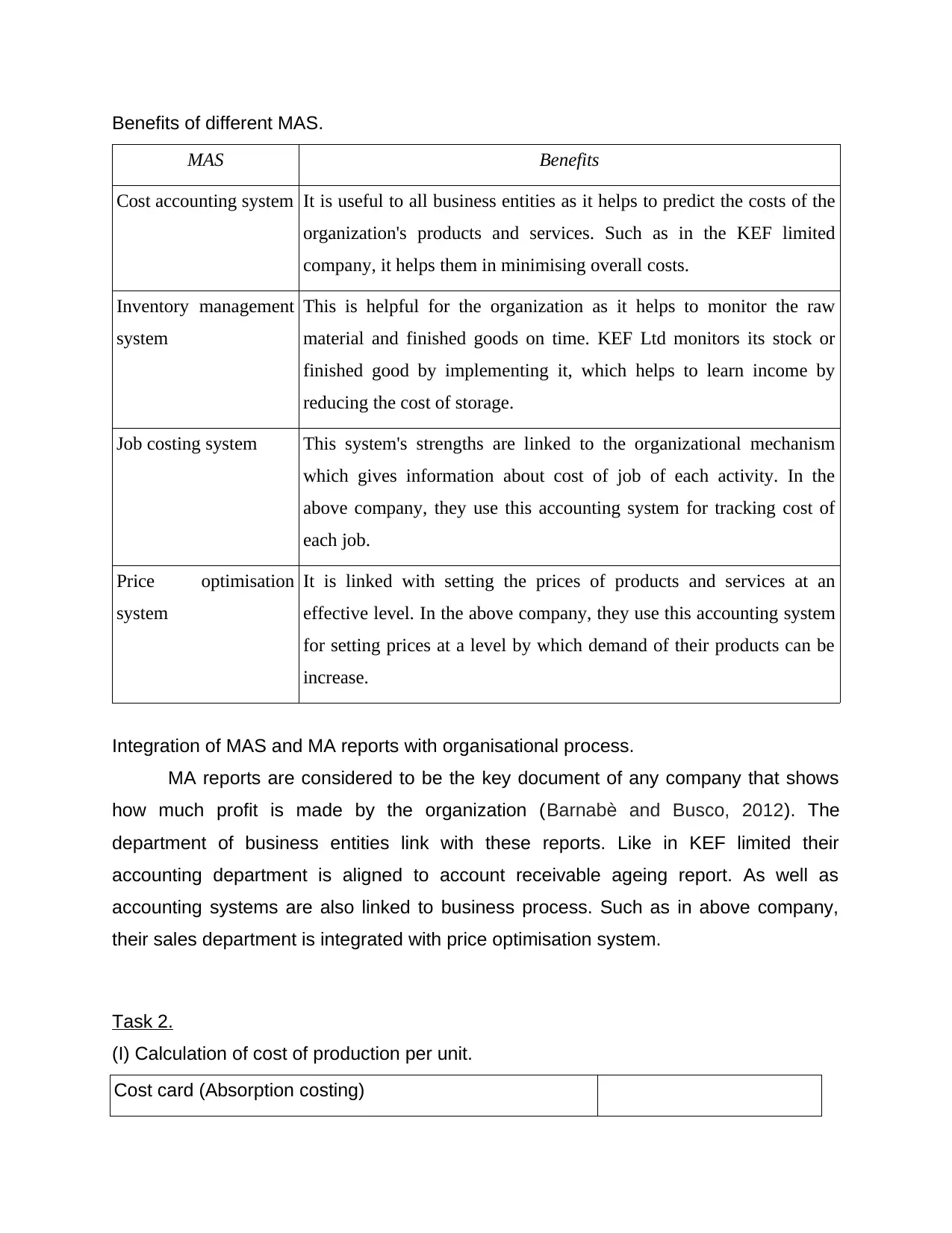

Benefits of different MAS.

MAS Benefits

Cost accounting system It is useful to all business entities as it helps to predict the costs of the

organization's products and services. Such as in the KEF limited

company, it helps them in minimising overall costs.

Inventory management

system

This is helpful for the organization as it helps to monitor the raw

material and finished goods on time. KEF Ltd monitors its stock or

finished good by implementing it, which helps to learn income by

reducing the cost of storage.

Job costing system This system's strengths are linked to the organizational mechanism

which gives information about cost of job of each activity. In the

above company, they use this accounting system for tracking cost of

each job.

Price optimisation

system

It is linked with setting the prices of products and services at an

effective level. In the above company, they use this accounting system

for setting prices at a level by which demand of their products can be

increase.

Integration of MAS and MA reports with organisational process.

MA reports are considered to be the key document of any company that shows

how much profit is made by the organization (Barnabè and Busco, 2012). The

department of business entities link with these reports. Like in KEF limited their

accounting department is aligned to account receivable ageing report. As well as

accounting systems are also linked to business process. Such as in above company,

their sales department is integrated with price optimisation system.

Task 2.

(I) Calculation of cost of production per unit.

Cost card (Absorption costing)

MAS Benefits

Cost accounting system It is useful to all business entities as it helps to predict the costs of the

organization's products and services. Such as in the KEF limited

company, it helps them in minimising overall costs.

Inventory management

system

This is helpful for the organization as it helps to monitor the raw

material and finished goods on time. KEF Ltd monitors its stock or

finished good by implementing it, which helps to learn income by

reducing the cost of storage.

Job costing system This system's strengths are linked to the organizational mechanism

which gives information about cost of job of each activity. In the

above company, they use this accounting system for tracking cost of

each job.

Price optimisation

system

It is linked with setting the prices of products and services at an

effective level. In the above company, they use this accounting system

for setting prices at a level by which demand of their products can be

increase.

Integration of MAS and MA reports with organisational process.

MA reports are considered to be the key document of any company that shows

how much profit is made by the organization (Barnabè and Busco, 2012). The

department of business entities link with these reports. Like in KEF limited their

accounting department is aligned to account receivable ageing report. As well as

accounting systems are also linked to business process. Such as in above company,

their sales department is integrated with price optimisation system.

Task 2.

(I) Calculation of cost of production per unit.

Cost card (Absorption costing)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

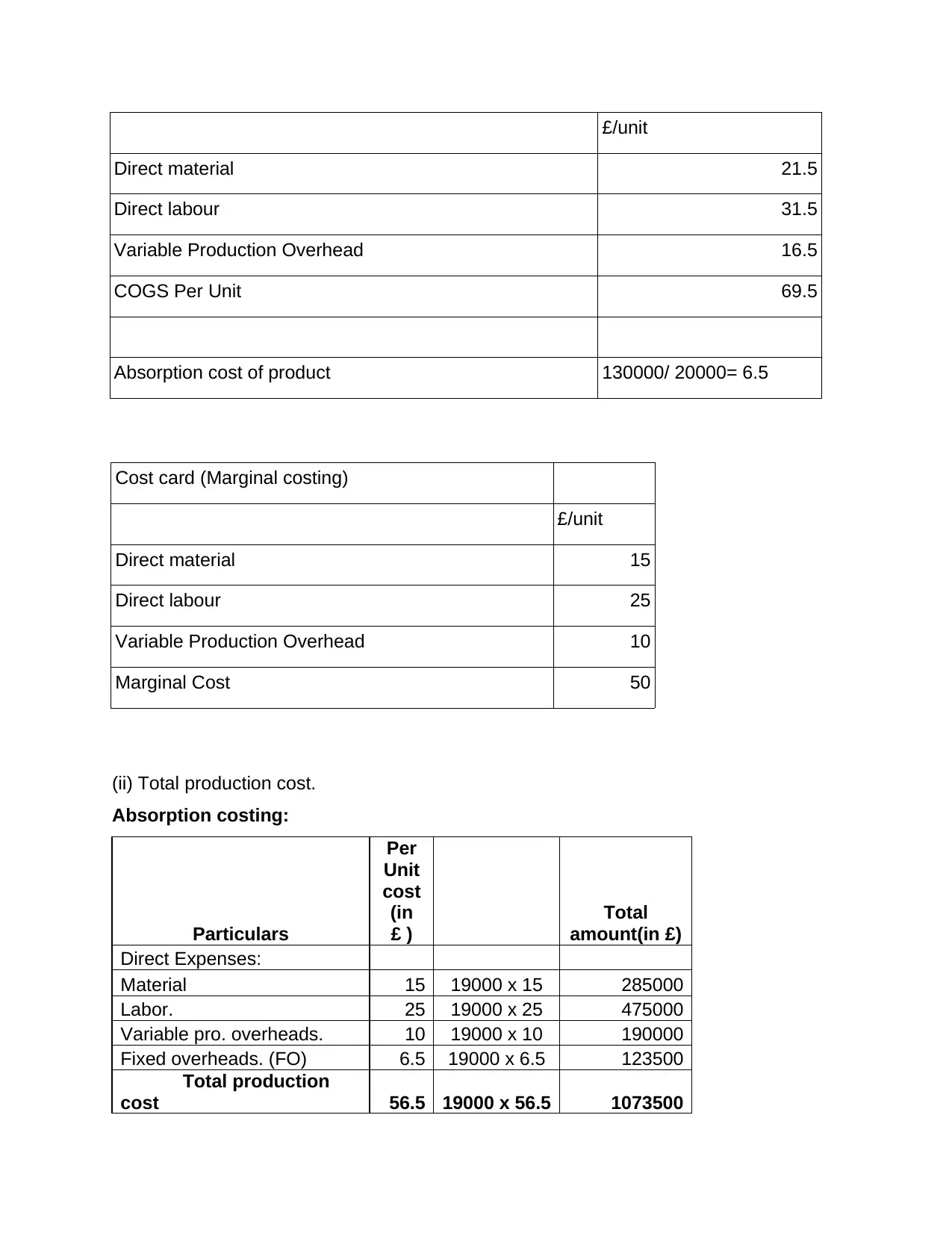

£/unit

Direct material 21.5

Direct labour 31.5

Variable Production Overhead 16.5

COGS Per Unit 69.5

Absorption cost of product 130000/ 20000= 6.5

Cost card (Marginal costing)

£/unit

Direct material 15

Direct labour 25

Variable Production Overhead 10

Marginal Cost 50

(ii) Total production cost.

Absorption costing:

Particulars

Per

Unit

cost

(in

£ )

Total

amount(in £)

Direct Expenses:

Material 15 19000 x 15 285000

Labor. 25 19000 x 25 475000

Variable pro. overheads. 10 19000 x 10 190000

Fixed overheads. (FO) 6.5 19000 x 6.5 123500

Total production

cost 56.5 19000 x 56.5 1073500

Direct material 21.5

Direct labour 31.5

Variable Production Overhead 16.5

COGS Per Unit 69.5

Absorption cost of product 130000/ 20000= 6.5

Cost card (Marginal costing)

£/unit

Direct material 15

Direct labour 25

Variable Production Overhead 10

Marginal Cost 50

(ii) Total production cost.

Absorption costing:

Particulars

Per

Unit

cost

(in

£ )

Total

amount(in £)

Direct Expenses:

Material 15 19000 x 15 285000

Labor. 25 19000 x 25 475000

Variable pro. overheads. 10 19000 x 10 190000

Fixed overheads. (FO) 6.5 19000 x 6.5 123500

Total production

cost 56.5 19000 x 56.5 1073500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

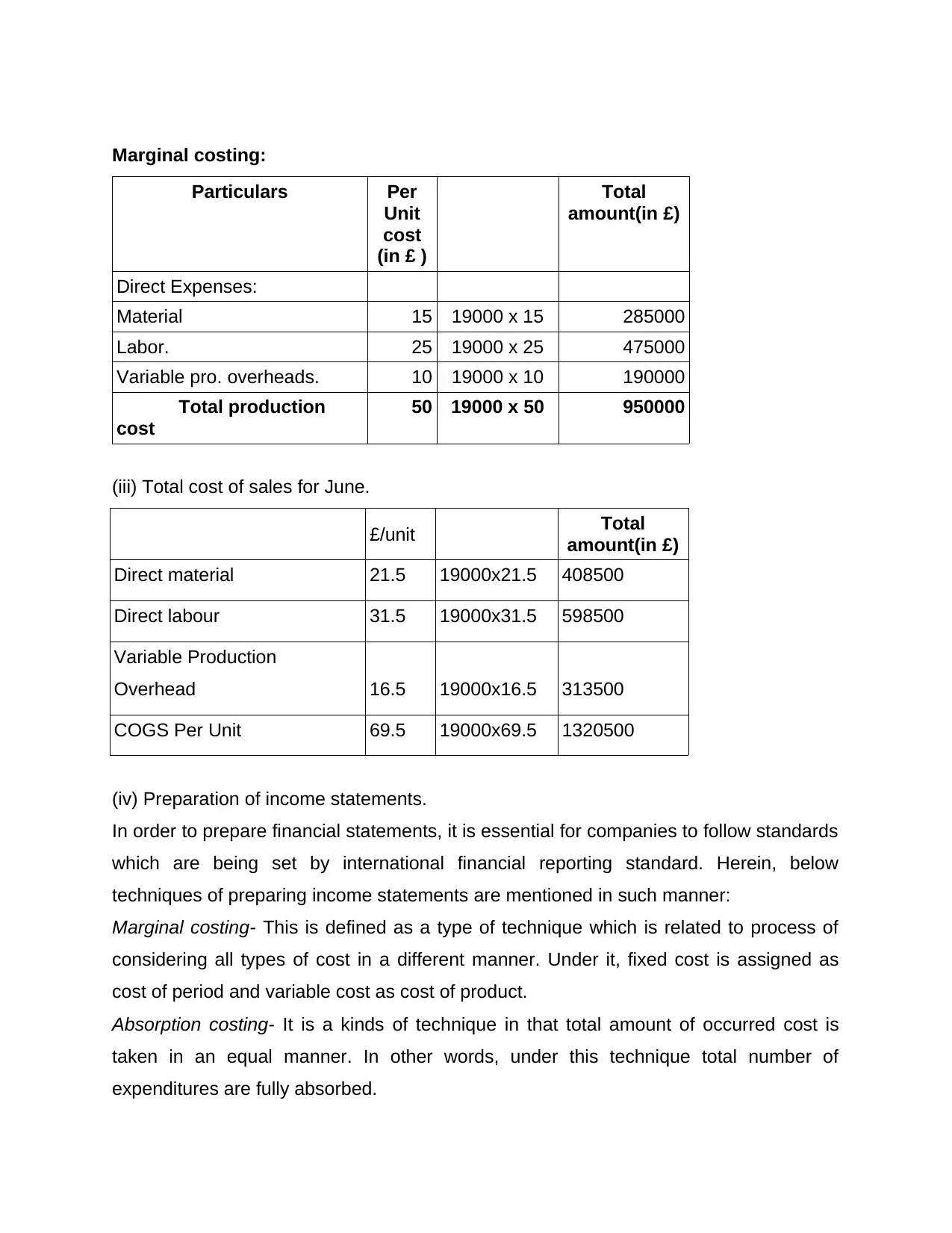

Marginal costing:

Particulars Per

Unit

cost

(in £ )

Total

amount(in £)

Direct Expenses:

Material 15 19000 x 15 285000

Labor. 25 19000 x 25 475000

Variable pro. overheads. 10 19000 x 10 190000

Total production

cost

50 19000 x 50 950000

(iii) Total cost of sales for June.

£/unit Total

amount(in £)

Direct material 21.5 19000x21.5 408500

Direct labour 31.5 19000x31.5 598500

Variable Production

Overhead 16.5 19000x16.5 313500

COGS Per Unit 69.5 19000x69.5 1320500

(iv) Preparation of income statements.

In order to prepare financial statements, it is essential for companies to follow standards

which are being set by international financial reporting standard. Herein, below

techniques of preparing income statements are mentioned in such manner:

Marginal costing- This is defined as a type of technique which is related to process of

considering all types of cost in a different manner. Under it, fixed cost is assigned as

cost of period and variable cost as cost of product.

Absorption costing- It is a kinds of technique in that total amount of occurred cost is

taken in an equal manner. In other words, under this technique total number of

expenditures are fully absorbed.

Particulars Per

Unit

cost

(in £ )

Total

amount(in £)

Direct Expenses:

Material 15 19000 x 15 285000

Labor. 25 19000 x 25 475000

Variable pro. overheads. 10 19000 x 10 190000

Total production

cost

50 19000 x 50 950000

(iii) Total cost of sales for June.

£/unit Total

amount(in £)

Direct material 21.5 19000x21.5 408500

Direct labour 31.5 19000x31.5 598500

Variable Production

Overhead 16.5 19000x16.5 313500

COGS Per Unit 69.5 19000x69.5 1320500

(iv) Preparation of income statements.

In order to prepare financial statements, it is essential for companies to follow standards

which are being set by international financial reporting standard. Herein, below

techniques of preparing income statements are mentioned in such manner:

Marginal costing- This is defined as a type of technique which is related to process of

considering all types of cost in a different manner. Under it, fixed cost is assigned as

cost of period and variable cost as cost of product.

Absorption costing- It is a kinds of technique in that total amount of occurred cost is

taken in an equal manner. In other words, under this technique total number of

expenditures are fully absorbed.

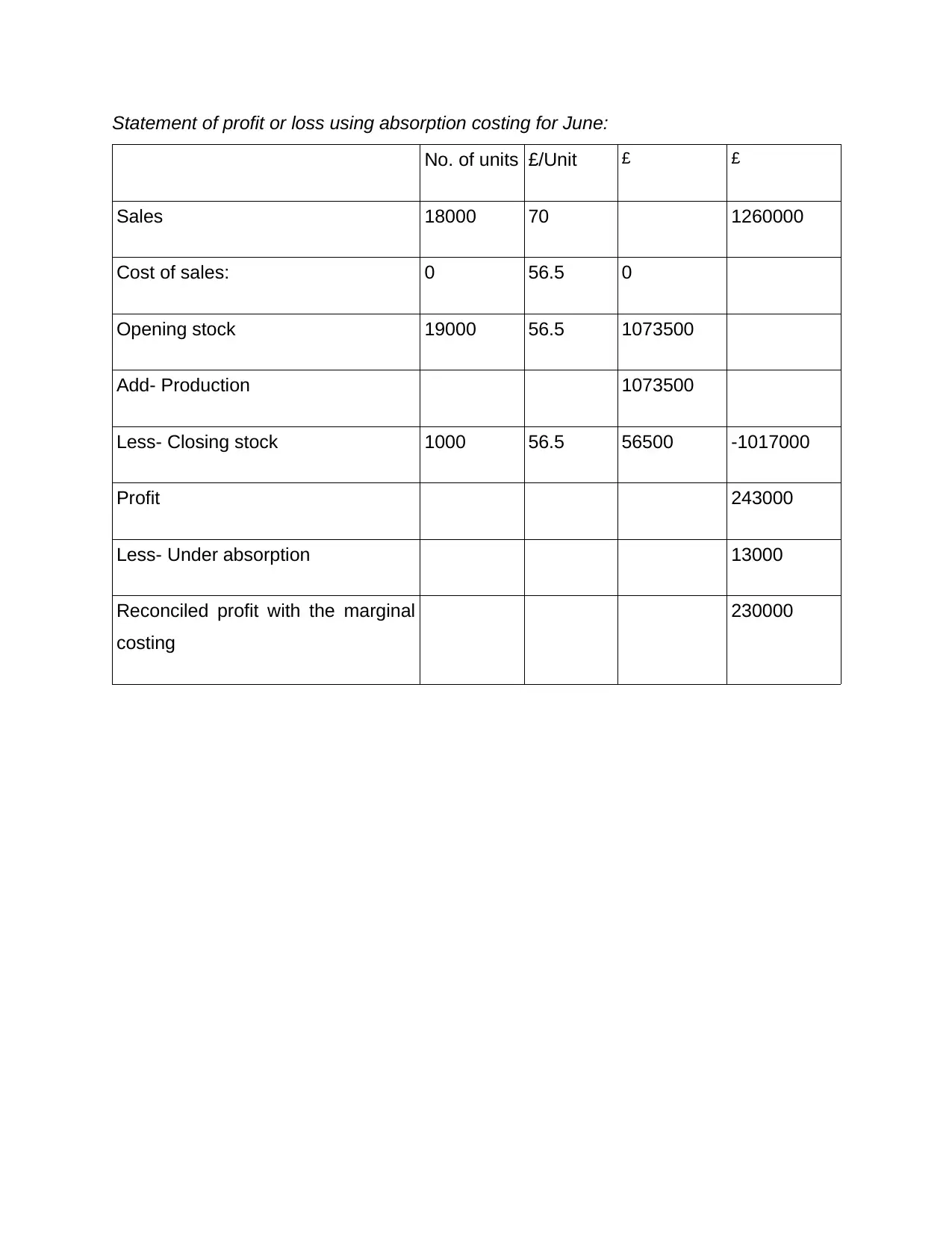

Statement of profit or loss using absorption costing for June:

No. of units £/Unit £ £

Sales 18000 70 1260000

Cost of sales: 0 56.5 0

Opening stock 19000 56.5 1073500

Add- Production 1073500

Less- Closing stock 1000 56.5 56500 -1017000

Profit 243000

Less- Under absorption 13000

Reconciled profit with the marginal

costing

230000

No. of units £/Unit £ £

Sales 18000 70 1260000

Cost of sales: 0 56.5 0

Opening stock 19000 56.5 1073500

Add- Production 1073500

Less- Closing stock 1000 56.5 56500 -1017000

Profit 243000

Less- Under absorption 13000

Reconciled profit with the marginal

costing

230000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working Note:

Fixed overheads absorbed on 18000 units (18000*6.5) = 117000

Fixed production overheads = 130000

Under absorbed the fixed cost= -13000

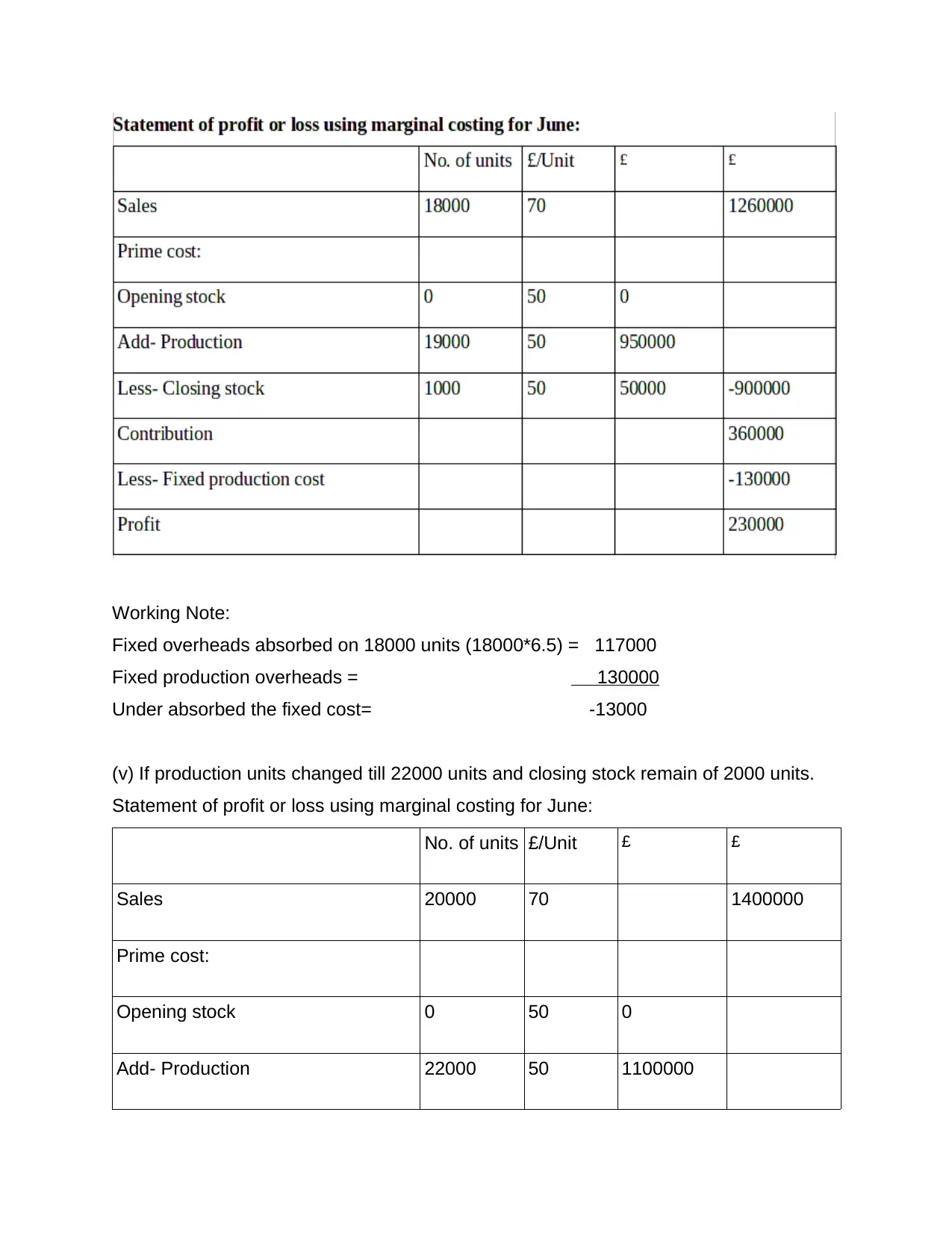

(v) If production units changed till 22000 units and closing stock remain of 2000 units.

Statement of profit or loss using marginal costing for June:

No. of units £/Unit £ £

Sales 20000 70 1400000

Prime cost:

Opening stock 0 50 0

Add- Production 22000 50 1100000

Fixed overheads absorbed on 18000 units (18000*6.5) = 117000

Fixed production overheads = 130000

Under absorbed the fixed cost= -13000

(v) If production units changed till 22000 units and closing stock remain of 2000 units.

Statement of profit or loss using marginal costing for June:

No. of units £/Unit £ £

Sales 20000 70 1400000

Prime cost:

Opening stock 0 50 0

Add- Production 22000 50 1100000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

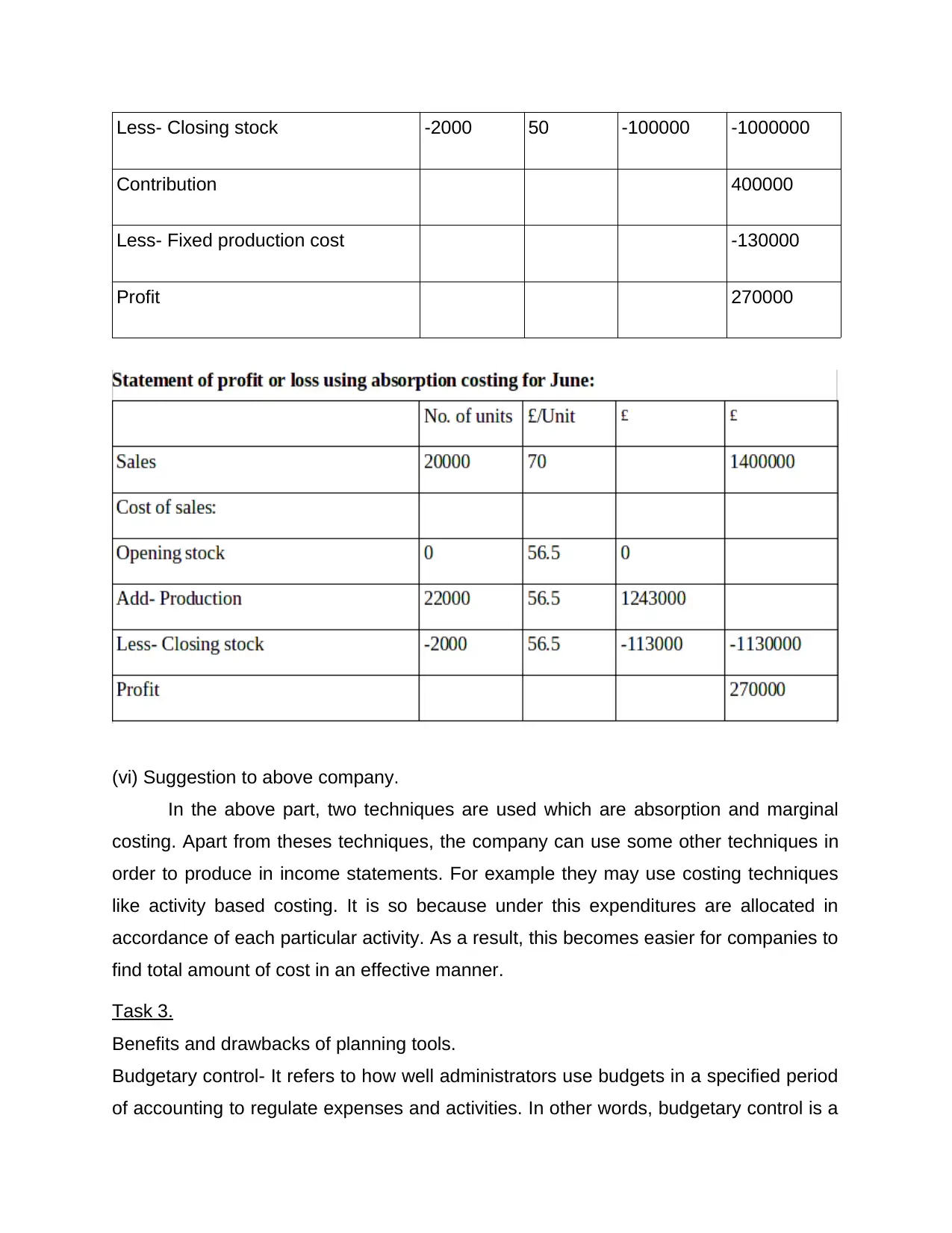

Less- Closing stock -2000 50 -100000 -1000000

Contribution 400000

Less- Fixed production cost -130000

Profit 270000

(vi) Suggestion to above company.

In the above part, two techniques are used which are absorption and marginal

costing. Apart from theses techniques, the company can use some other techniques in

order to produce in income statements. For example they may use costing techniques

like activity based costing. It is so because under this expenditures are allocated in

accordance of each particular activity. As a result, this becomes easier for companies to

find total amount of cost in an effective manner.

Task 3.

Benefits and drawbacks of planning tools.

Budgetary control- It refers to how well administrators use budgets in a specified period

of accounting to regulate expenses and activities. In other words, budgetary control is a

Contribution 400000

Less- Fixed production cost -130000

Profit 270000

(vi) Suggestion to above company.

In the above part, two techniques are used which are absorption and marginal

costing. Apart from theses techniques, the company can use some other techniques in

order to produce in income statements. For example they may use costing techniques

like activity based costing. It is so because under this expenditures are allocated in

accordance of each particular activity. As a result, this becomes easier for companies to

find total amount of cost in an effective manner.

Task 3.

Benefits and drawbacks of planning tools.

Budgetary control- It refers to how well administrators use budgets in a specified period

of accounting to regulate expenses and activities. In other words, budgetary control is a

mechanism for management to set budget-based monetary and performance targets

then compare total results, and modify performance as necessary. This includes

different types of planning tools which are mentioned below in such manner:

Capital budget - It is one of the most significant cap used to maintain the firm's large

expenses. It includes land, machinery, and building costs (Alfian, 2017). The senior

management also makes the decision for long term investment under such budget and

obtains the approval for it. Basically, this budgeting technique evaluate efficiency of

different types of projects in an effective manner by help of investment appraisal

methods such as net present value, internal rate of return etc. In the aspect of KEF

limited company, they use this budget for making appropriate selection of investment

proposals.

Benefits –

It contributes to finance managers in order to do long time period capital

planning.

Provide great help in making decisions about which investment alternative to

choose for.

Drawbacks-

Preparation of this type of budget needs higher excellence in accounting and it is

not affordable for all types of business entities.

This budget makes just an estimation of future projects, companies can not relay

on its outcome completely. If companies consider only this budget for making

choice of investment then it may lead to lose in some cases.

Activity based budgeting - Activity-based budgeting is a top-down budgeting method

which specifies how much input is necessary to support the business's goals or

outcomes. A company, for example, establishes a sales production target of $100

million. The corporation would first need to identify the practices that ought to be

performed to achieve the sales goal, and then figure out the cost of undertaking those

activities. This budget is being prepared and used by KEF limited company with an aim

of finding those number of activities which will be needed to implement for achievement

then compare total results, and modify performance as necessary. This includes

different types of planning tools which are mentioned below in such manner:

Capital budget - It is one of the most significant cap used to maintain the firm's large

expenses. It includes land, machinery, and building costs (Alfian, 2017). The senior

management also makes the decision for long term investment under such budget and

obtains the approval for it. Basically, this budgeting technique evaluate efficiency of

different types of projects in an effective manner by help of investment appraisal

methods such as net present value, internal rate of return etc. In the aspect of KEF

limited company, they use this budget for making appropriate selection of investment

proposals.

Benefits –

It contributes to finance managers in order to do long time period capital

planning.

Provide great help in making decisions about which investment alternative to

choose for.

Drawbacks-

Preparation of this type of budget needs higher excellence in accounting and it is

not affordable for all types of business entities.

This budget makes just an estimation of future projects, companies can not relay

on its outcome completely. If companies consider only this budget for making

choice of investment then it may lead to lose in some cases.

Activity based budgeting - Activity-based budgeting is a top-down budgeting method

which specifies how much input is necessary to support the business's goals or

outcomes. A company, for example, establishes a sales production target of $100

million. The corporation would first need to identify the practices that ought to be

performed to achieve the sales goal, and then figure out the cost of undertaking those

activities. This budget is being prepared and used by KEF limited company with an aim

of finding those number of activities which will be needed to implement for achievement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.