Management Accounting Report: KEF Ltd Analysis and Solutions

VerifiedAdded on 2023/01/17

|23

|5558

|41

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on a case study of KEF Ltd, a UK manufacturing company. The report begins by defining management accounting and its benefits, differentiating it from financial accounting, and exploring various management accounting systems like inventory management, cost accounting, and price optimization. It then delves into managerial reporting aspects, including inventory reports, budget reports, accounts receivable aging reports, and cost reports, evaluating their integration within organizational processes. The core of the report involves computing net profit using both absorption and marginal costing methods, highlighting their differences. Furthermore, it examines different planning tools used in budgetary control, analyzing their advantages, disadvantages, and applications, while also addressing how financial problems can be responded to using these tools. The report concludes by summarizing the key findings and emphasizing the importance of management accounting in strategic decision-making and financial management within KEF Ltd.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Explaining management accounting systems along with its benefits of different systems.........3

Presenting methods used for managerial reporting aspects.........................................................4

Critically evaluating how management accounting systems and reporting is integrated within

organizational process.................................................................................................................5

LO2..................................................................................................................................................6

Computation of net profit by employing absorption and marginal costing.................................6

LO3..................................................................................................................................................9

Explaining the advantages and disadvantages of different planning tools used in budgetary

control..........................................................................................................................................9

Analyzing the usage and application of different planning tools used in budgetary control....11

Exhibits the manner in which financial problems can be responded.........................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

LO1..................................................................................................................................................3

Explaining management accounting systems along with its benefits of different systems.........3

Presenting methods used for managerial reporting aspects.........................................................4

Critically evaluating how management accounting systems and reporting is integrated within

organizational process.................................................................................................................5

LO2..................................................................................................................................................6

Computation of net profit by employing absorption and marginal costing.................................6

LO3..................................................................................................................................................9

Explaining the advantages and disadvantages of different planning tools used in budgetary

control..........................................................................................................................................9

Analyzing the usage and application of different planning tools used in budgetary control....11

Exhibits the manner in which financial problems can be responded.........................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Management accounting emphasizes on analysing business cost and operations with the

motive to prepare appropriate financial reports. In the recent times, business unit lays high level

of emphasis on undertaking management accounting tools with the motive to manage internal

financial operations effectually. By undertaking MA tools firm can develop competent strategic

and policy framework for the upcoming time period. This report is based on the case scenario of

KEF Ltd which is involved in UK manufacturing sector. In this, report will provide deeper

insight about management accounting tools and techniques that can be undertaken by KEF Ltd.

Further, it also presents how managerial reporting can be used for the purpose of decision

making. Report will develop understanding about how absorption and marginal costing system

can be used for analysing profitability aspects. It also entails how MA tools can be employed for

the purpose of planning and budgetary control. Besides this, it will shed light on the manner in

which monetary problems can be responded using management accounting tools.

LO1

Explaining management accounting systems along with its benefits of different systems

Management accounting (MA) can be defined as a technique or a process which is used

by organisations in order to facilitate their business in the aspect of recording the transactions

that are taking place and the other activities that facilitate the operational activities in an

organisation (Agrawal and Cooper, 2017). Management accounting helps the accountants,

mangers and other financiers working in a business in ascertaining the costs that are incurred or

will be incurred in the business by using various tools and techniques and further, management

accounting also assists in controlling or minimising such costs that are pre-determined so that

unnecessary expenditure can be avoided.

Purpose of MA

It helps in doing planning about future with regards to setting budget that contributes in

cost reduction and profit maximization.

MA also provides high level of assistance in identifying gaps that take place in existing

performance and thereby helps in taking appropriate actions for improvement.

Management accounting emphasizes on analysing business cost and operations with the

motive to prepare appropriate financial reports. In the recent times, business unit lays high level

of emphasis on undertaking management accounting tools with the motive to manage internal

financial operations effectually. By undertaking MA tools firm can develop competent strategic

and policy framework for the upcoming time period. This report is based on the case scenario of

KEF Ltd which is involved in UK manufacturing sector. In this, report will provide deeper

insight about management accounting tools and techniques that can be undertaken by KEF Ltd.

Further, it also presents how managerial reporting can be used for the purpose of decision

making. Report will develop understanding about how absorption and marginal costing system

can be used for analysing profitability aspects. It also entails how MA tools can be employed for

the purpose of planning and budgetary control. Besides this, it will shed light on the manner in

which monetary problems can be responded using management accounting tools.

LO1

Explaining management accounting systems along with its benefits of different systems

Management accounting (MA) can be defined as a technique or a process which is used

by organisations in order to facilitate their business in the aspect of recording the transactions

that are taking place and the other activities that facilitate the operational activities in an

organisation (Agrawal and Cooper, 2017). Management accounting helps the accountants,

mangers and other financiers working in a business in ascertaining the costs that are incurred or

will be incurred in the business by using various tools and techniques and further, management

accounting also assists in controlling or minimising such costs that are pre-determined so that

unnecessary expenditure can be avoided.

Purpose of MA

It helps in doing planning about future with regards to setting budget that contributes in

cost reduction and profit maximization.

MA also provides high level of assistance in identifying gaps that take place in existing

performance and thereby helps in taking appropriate actions for improvement.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition to this, the main motive of MA is to ensure liaison between personnel and

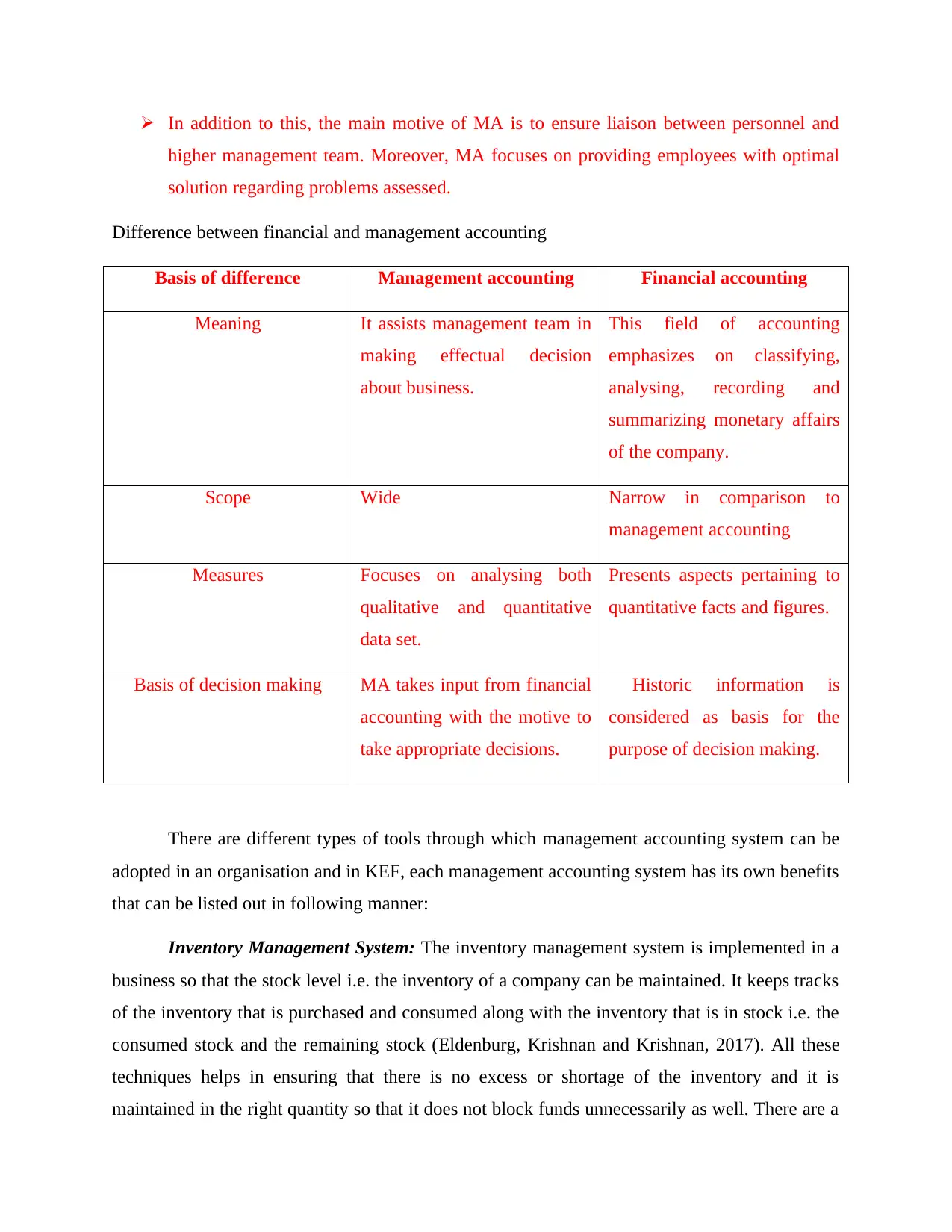

higher management team. Moreover, MA focuses on providing employees with optimal

solution regarding problems assessed.

Difference between financial and management accounting

Basis of difference Management accounting Financial accounting

Meaning It assists management team in

making effectual decision

about business.

This field of accounting

emphasizes on classifying,

analysing, recording and

summarizing monetary affairs

of the company.

Scope Wide Narrow in comparison to

management accounting

Measures Focuses on analysing both

qualitative and quantitative

data set.

Presents aspects pertaining to

quantitative facts and figures.

Basis of decision making MA takes input from financial

accounting with the motive to

take appropriate decisions.

Historic information is

considered as basis for the

purpose of decision making.

There are different types of tools through which management accounting system can be

adopted in an organisation and in KEF, each management accounting system has its own benefits

that can be listed out in following manner:

Inventory Management System: The inventory management system is implemented in a

business so that the stock level i.e. the inventory of a company can be maintained. It keeps tracks

of the inventory that is purchased and consumed along with the inventory that is in stock i.e. the

consumed stock and the remaining stock (Eldenburg, Krishnan and Krishnan, 2017). All these

techniques helps in ensuring that there is no excess or shortage of the inventory and it is

maintained in the right quantity so that it does not block funds unnecessarily as well. There are a

higher management team. Moreover, MA focuses on providing employees with optimal

solution regarding problems assessed.

Difference between financial and management accounting

Basis of difference Management accounting Financial accounting

Meaning It assists management team in

making effectual decision

about business.

This field of accounting

emphasizes on classifying,

analysing, recording and

summarizing monetary affairs

of the company.

Scope Wide Narrow in comparison to

management accounting

Measures Focuses on analysing both

qualitative and quantitative

data set.

Presents aspects pertaining to

quantitative facts and figures.

Basis of decision making MA takes input from financial

accounting with the motive to

take appropriate decisions.

Historic information is

considered as basis for the

purpose of decision making.

There are different types of tools through which management accounting system can be

adopted in an organisation and in KEF, each management accounting system has its own benefits

that can be listed out in following manner:

Inventory Management System: The inventory management system is implemented in a

business so that the stock level i.e. the inventory of a company can be maintained. It keeps tracks

of the inventory that is purchased and consumed along with the inventory that is in stock i.e. the

consumed stock and the remaining stock (Eldenburg, Krishnan and Krishnan, 2017). All these

techniques helps in ensuring that there is no excess or shortage of the inventory and it is

maintained in the right quantity so that it does not block funds unnecessarily as well. There are a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

variety of techniques that can be used such as FIFO (First In First Out), LIFO (Last In First Out),

EOQ (Economic Order quantity) etc. LIFO deals with the earliest of consumption of the latest

stock that is in the warehouse and FIFO uses the older stock first and then the latest one. EOQ on

the other hand deduces a reorder level or point at which a particular quantity of goods should be

reordered so that the production of the company can keep running. For KEF, the best strategy

would be EOQ method since it ensures that the funds i.e. the working capital of the company

does not gets blocked unnecessarily and the stock is made available at all times.

Advantages Disadvantages

Ensures uninterrupted production

activities

It also helps in reducing storage as well

as ordering cost and thereby increases

profitability

For dealing with inventory

management systems business unit

needs to conduct training session. This

in turn imposes cost in front of the

company.

Time consuming process

Cost Accounting System: This technique of cost management helps the management in

ascertaining the cost that will be incurred on order to manufacture a particular product and also

determines whether it will be profitable or not to manufacture this product (Lopez-Valeiras,

Gomez-Conde and Naranjo-Gil, 2015).

Advantages Disadvantages

Helps in avoiding wastage, losses and

inefficiencies

Assists in identifying reason related to

profit or loss generated

Ensures cost reduction and profit

maximization

This accounting system leads problem

related to under or over absorption

Time consuming exercise as it requires

maintenance of many costing records

EOQ (Economic Order quantity) etc. LIFO deals with the earliest of consumption of the latest

stock that is in the warehouse and FIFO uses the older stock first and then the latest one. EOQ on

the other hand deduces a reorder level or point at which a particular quantity of goods should be

reordered so that the production of the company can keep running. For KEF, the best strategy

would be EOQ method since it ensures that the funds i.e. the working capital of the company

does not gets blocked unnecessarily and the stock is made available at all times.

Advantages Disadvantages

Ensures uninterrupted production

activities

It also helps in reducing storage as well

as ordering cost and thereby increases

profitability

For dealing with inventory

management systems business unit

needs to conduct training session. This

in turn imposes cost in front of the

company.

Time consuming process

Cost Accounting System: This technique of cost management helps the management in

ascertaining the cost that will be incurred on order to manufacture a particular product and also

determines whether it will be profitable or not to manufacture this product (Lopez-Valeiras,

Gomez-Conde and Naranjo-Gil, 2015).

Advantages Disadvantages

Helps in avoiding wastage, losses and

inefficiencies

Assists in identifying reason related to

profit or loss generated

Ensures cost reduction and profit

maximization

This accounting system leads problem

related to under or over absorption

Time consuming exercise as it requires

maintenance of many costing records

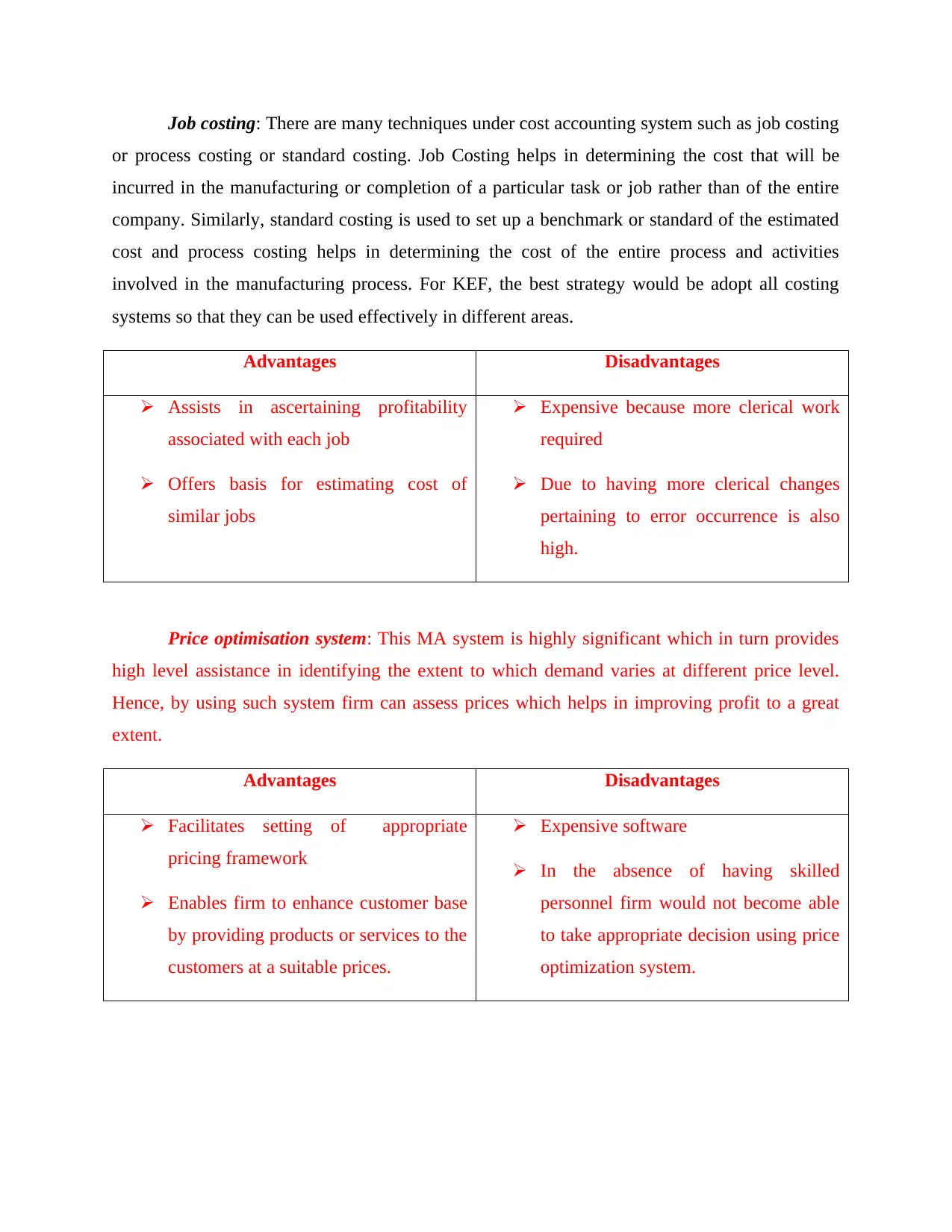

Job costing: There are many techniques under cost accounting system such as job costing

or process costing or standard costing. Job Costing helps in determining the cost that will be

incurred in the manufacturing or completion of a particular task or job rather than of the entire

company. Similarly, standard costing is used to set up a benchmark or standard of the estimated

cost and process costing helps in determining the cost of the entire process and activities

involved in the manufacturing process. For KEF, the best strategy would be adopt all costing

systems so that they can be used effectively in different areas.

Advantages Disadvantages

Assists in ascertaining profitability

associated with each job

Offers basis for estimating cost of

similar jobs

Expensive because more clerical work

required

Due to having more clerical changes

pertaining to error occurrence is also

high.

Price optimisation system: This MA system is highly significant which in turn provides

high level assistance in identifying the extent to which demand varies at different price level.

Hence, by using such system firm can assess prices which helps in improving profit to a great

extent.

Advantages Disadvantages

Facilitates setting of appropriate

pricing framework

Enables firm to enhance customer base

by providing products or services to the

customers at a suitable prices.

Expensive software

In the absence of having skilled

personnel firm would not become able

to take appropriate decision using price

optimization system.

or process costing or standard costing. Job Costing helps in determining the cost that will be

incurred in the manufacturing or completion of a particular task or job rather than of the entire

company. Similarly, standard costing is used to set up a benchmark or standard of the estimated

cost and process costing helps in determining the cost of the entire process and activities

involved in the manufacturing process. For KEF, the best strategy would be adopt all costing

systems so that they can be used effectively in different areas.

Advantages Disadvantages

Assists in ascertaining profitability

associated with each job

Offers basis for estimating cost of

similar jobs

Expensive because more clerical work

required

Due to having more clerical changes

pertaining to error occurrence is also

high.

Price optimisation system: This MA system is highly significant which in turn provides

high level assistance in identifying the extent to which demand varies at different price level.

Hence, by using such system firm can assess prices which helps in improving profit to a great

extent.

Advantages Disadvantages

Facilitates setting of appropriate

pricing framework

Enables firm to enhance customer base

by providing products or services to the

customers at a suitable prices.

Expensive software

In the absence of having skilled

personnel firm would not become able

to take appropriate decision using price

optimization system.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

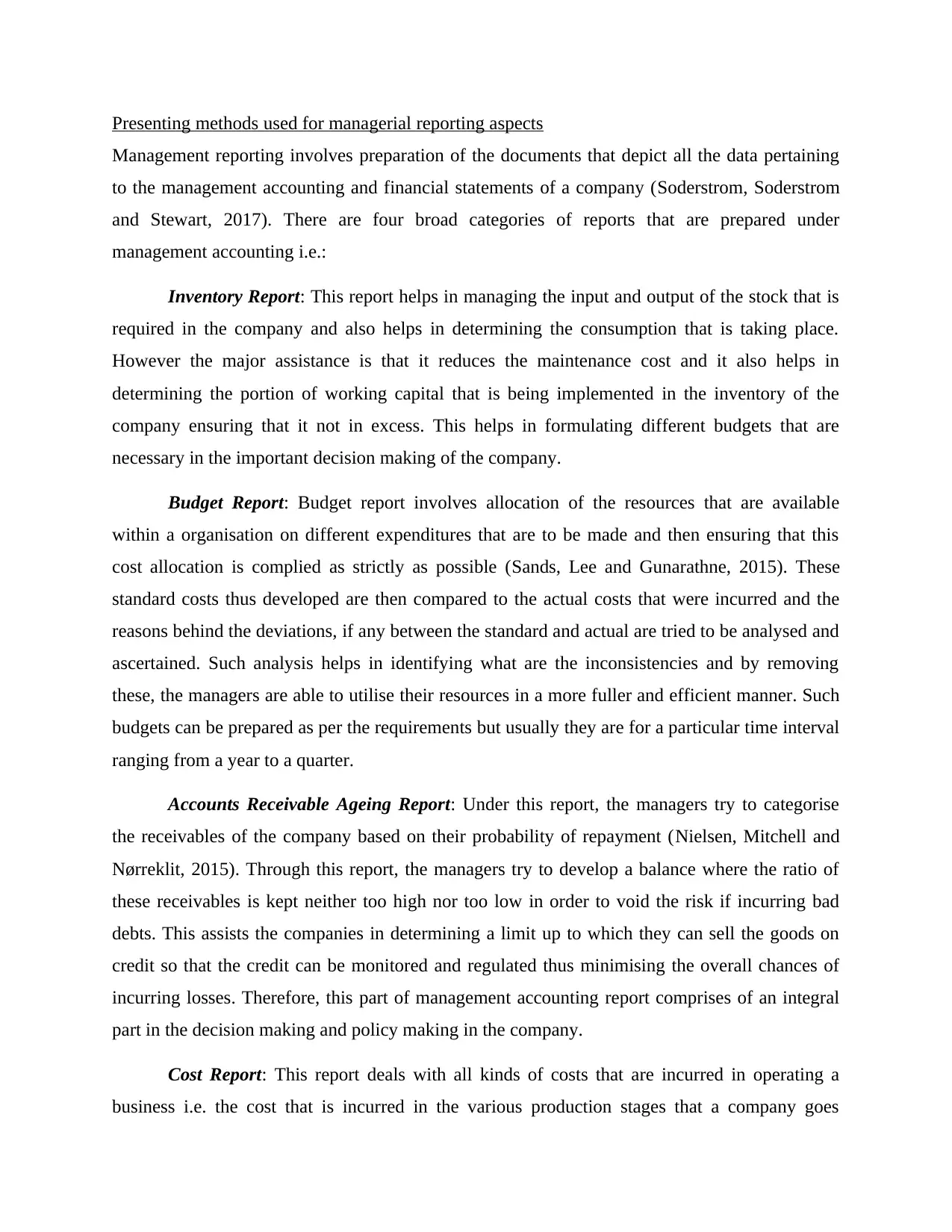

Presenting methods used for managerial reporting aspects

Management reporting involves preparation of the documents that depict all the data pertaining

to the management accounting and financial statements of a company (Soderstrom, Soderstrom

and Stewart, 2017). There are four broad categories of reports that are prepared under

management accounting i.e.:

Inventory Report: This report helps in managing the input and output of the stock that is

required in the company and also helps in determining the consumption that is taking place.

However the major assistance is that it reduces the maintenance cost and it also helps in

determining the portion of working capital that is being implemented in the inventory of the

company ensuring that it not in excess. This helps in formulating different budgets that are

necessary in the important decision making of the company.

Budget Report: Budget report involves allocation of the resources that are available

within a organisation on different expenditures that are to be made and then ensuring that this

cost allocation is complied as strictly as possible (Sands, Lee and Gunarathne, 2015). These

standard costs thus developed are then compared to the actual costs that were incurred and the

reasons behind the deviations, if any between the standard and actual are tried to be analysed and

ascertained. Such analysis helps in identifying what are the inconsistencies and by removing

these, the managers are able to utilise their resources in a more fuller and efficient manner. Such

budgets can be prepared as per the requirements but usually they are for a particular time interval

ranging from a year to a quarter.

Accounts Receivable Ageing Report: Under this report, the managers try to categorise

the receivables of the company based on their probability of repayment (Nielsen, Mitchell and

Nørreklit, 2015). Through this report, the managers try to develop a balance where the ratio of

these receivables is kept neither too high nor too low in order to void the risk if incurring bad

debts. This assists the companies in determining a limit up to which they can sell the goods on

credit so that the credit can be monitored and regulated thus minimising the overall chances of

incurring losses. Therefore, this part of management accounting report comprises of an integral

part in the decision making and policy making in the company.

Cost Report: This report deals with all kinds of costs that are incurred in operating a

business i.e. the cost that is incurred in the various production stages that a company goes

Management reporting involves preparation of the documents that depict all the data pertaining

to the management accounting and financial statements of a company (Soderstrom, Soderstrom

and Stewart, 2017). There are four broad categories of reports that are prepared under

management accounting i.e.:

Inventory Report: This report helps in managing the input and output of the stock that is

required in the company and also helps in determining the consumption that is taking place.

However the major assistance is that it reduces the maintenance cost and it also helps in

determining the portion of working capital that is being implemented in the inventory of the

company ensuring that it not in excess. This helps in formulating different budgets that are

necessary in the important decision making of the company.

Budget Report: Budget report involves allocation of the resources that are available

within a organisation on different expenditures that are to be made and then ensuring that this

cost allocation is complied as strictly as possible (Sands, Lee and Gunarathne, 2015). These

standard costs thus developed are then compared to the actual costs that were incurred and the

reasons behind the deviations, if any between the standard and actual are tried to be analysed and

ascertained. Such analysis helps in identifying what are the inconsistencies and by removing

these, the managers are able to utilise their resources in a more fuller and efficient manner. Such

budgets can be prepared as per the requirements but usually they are for a particular time interval

ranging from a year to a quarter.

Accounts Receivable Ageing Report: Under this report, the managers try to categorise

the receivables of the company based on their probability of repayment (Nielsen, Mitchell and

Nørreklit, 2015). Through this report, the managers try to develop a balance where the ratio of

these receivables is kept neither too high nor too low in order to void the risk if incurring bad

debts. This assists the companies in determining a limit up to which they can sell the goods on

credit so that the credit can be monitored and regulated thus minimising the overall chances of

incurring losses. Therefore, this part of management accounting report comprises of an integral

part in the decision making and policy making in the company.

Cost Report: This report deals with all kinds of costs that are incurred in operating a

business i.e. the cost that is incurred in the various production stages that a company goes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through. Under this, a comparison is made between the past and current costs that were incurred

so that a trend analysis can be established which assists the managers in deciding whether such

increase or decrease in cost is beneficial or not (Endrikat, Hartmann and Schreck, 2017). This

also points out if there is need of any specific policies that are to be implemented and there are

various techniques such as Job Costing etc. that can be used in these report’s preparation.

Critically evaluating how management accounting systems and reporting is integrated within

organizational process

From evaluation, it has identified that aspects of management accounting and reporting

are highly integrated with each other. Moreover, management accounting systems clearly entails

the manner through business unit can ensure effectual management of costing, stock and

profitability aspects (Otley, 2016). Further, report furnishes information about the extent to

which each department is performing in a well manner. Thus, by making assessment of reporting

aspect management team of KEF ltd can ascertain areas where extra efforts need to be made.

Thus, by taking significant measure on the basis of reporting management of KEF ltd can

achieve organizational goals and objectives.

LO2

Computation of net profit by employing absorption and marginal costing

Marginal costing- It means ascertainment through differentiating in between the fixed

and the variable cost of the marginal cost and an effect of the profit changes in respect of type

and the volume of an output (Ray and Gramlich, 2015). Marginal costing method is been used

for analyzing and interpreting cost data in order to determine product’s profitability, department,

process and the cost centre.

Absorption costing- It is referred to the method of accumulating cost attached with the

process of production and in apportioning them to the individual product (Konopczak and Welfe,

2017). It is the costing technique that is needed by an accounting standard for creating valuation

of an inventory which is stated in the balance sheet of an enterprise.

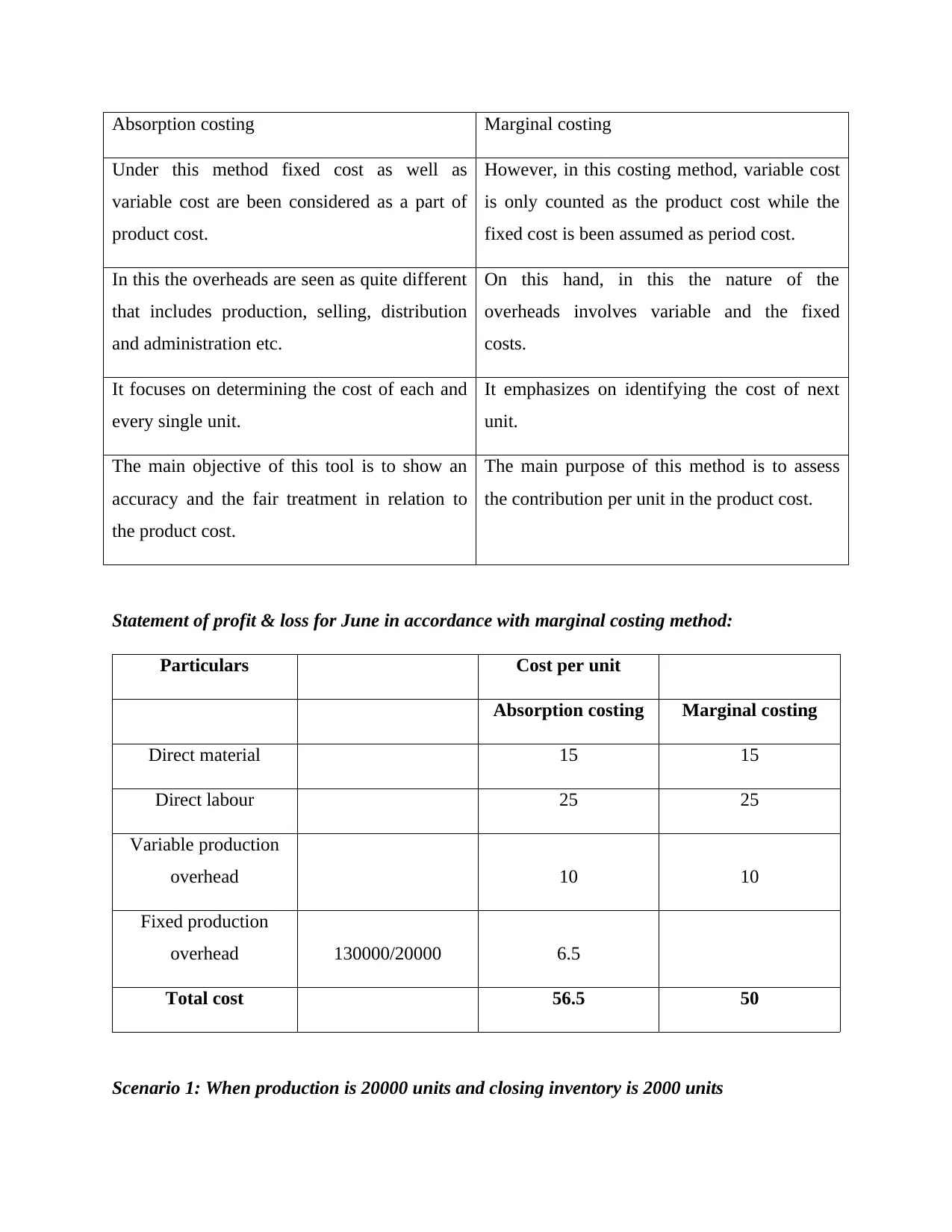

Difference between marginal and absorption costing

so that a trend analysis can be established which assists the managers in deciding whether such

increase or decrease in cost is beneficial or not (Endrikat, Hartmann and Schreck, 2017). This

also points out if there is need of any specific policies that are to be implemented and there are

various techniques such as Job Costing etc. that can be used in these report’s preparation.

Critically evaluating how management accounting systems and reporting is integrated within

organizational process

From evaluation, it has identified that aspects of management accounting and reporting

are highly integrated with each other. Moreover, management accounting systems clearly entails

the manner through business unit can ensure effectual management of costing, stock and

profitability aspects (Otley, 2016). Further, report furnishes information about the extent to

which each department is performing in a well manner. Thus, by making assessment of reporting

aspect management team of KEF ltd can ascertain areas where extra efforts need to be made.

Thus, by taking significant measure on the basis of reporting management of KEF ltd can

achieve organizational goals and objectives.

LO2

Computation of net profit by employing absorption and marginal costing

Marginal costing- It means ascertainment through differentiating in between the fixed

and the variable cost of the marginal cost and an effect of the profit changes in respect of type

and the volume of an output (Ray and Gramlich, 2015). Marginal costing method is been used

for analyzing and interpreting cost data in order to determine product’s profitability, department,

process and the cost centre.

Absorption costing- It is referred to the method of accumulating cost attached with the

process of production and in apportioning them to the individual product (Konopczak and Welfe,

2017). It is the costing technique that is needed by an accounting standard for creating valuation

of an inventory which is stated in the balance sheet of an enterprise.

Difference between marginal and absorption costing

Absorption costing Marginal costing

Under this method fixed cost as well as

variable cost are been considered as a part of

product cost.

However, in this costing method, variable cost

is only counted as the product cost while the

fixed cost is been assumed as period cost.

In this the overheads are seen as quite different

that includes production, selling, distribution

and administration etc.

On this hand, in this the nature of the

overheads involves variable and the fixed

costs.

It focuses on determining the cost of each and

every single unit.

It emphasizes on identifying the cost of next

unit.

The main objective of this tool is to show an

accuracy and the fair treatment in relation to

the product cost.

The main purpose of this method is to assess

the contribution per unit in the product cost.

Statement of profit & loss for June in accordance with marginal costing method:

Particulars Cost per unit

Absorption costing Marginal costing

Direct material 15 15

Direct labour 25 25

Variable production

overhead 10 10

Fixed production

overhead 130000/20000 6.5

Total cost 56.5 50

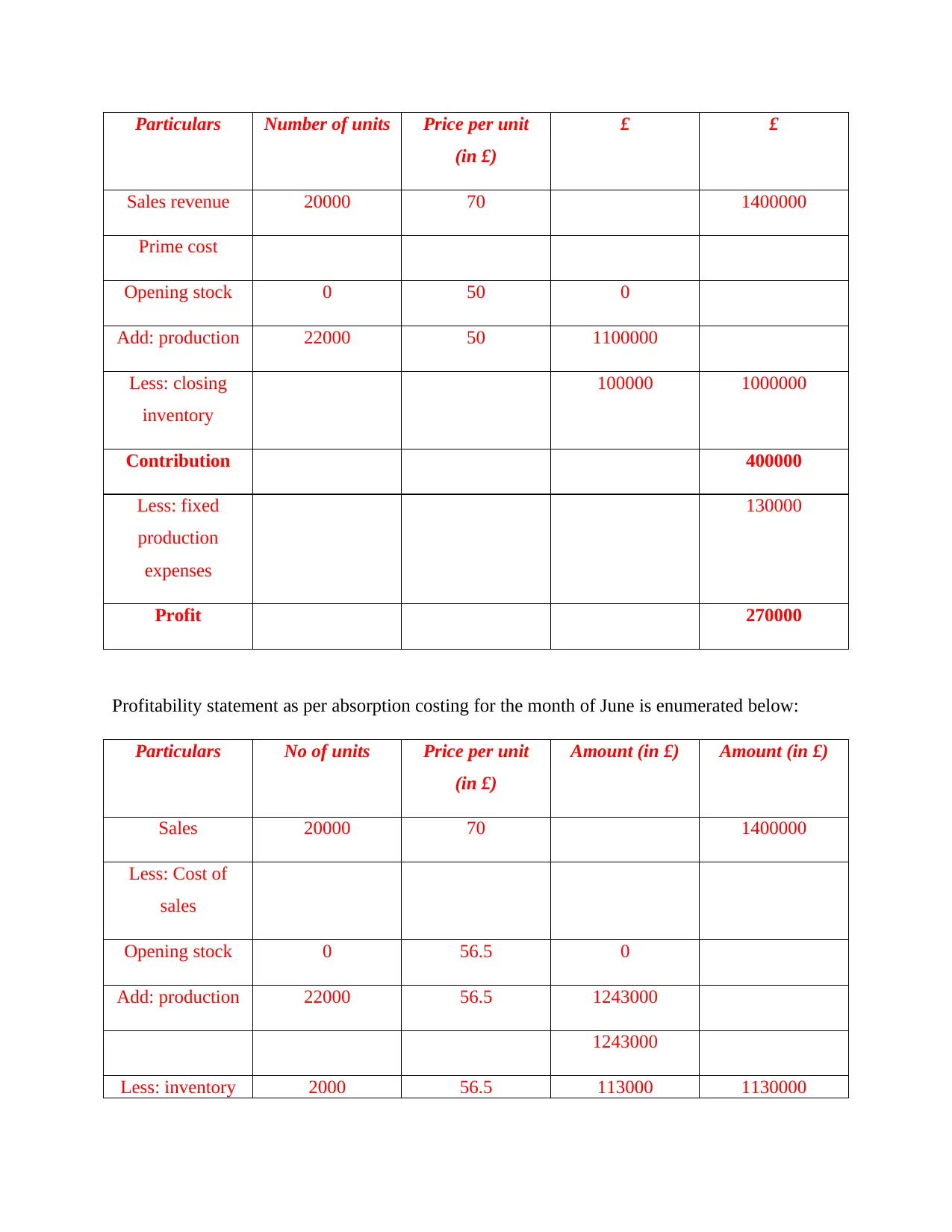

Scenario 1: When production is 20000 units and closing inventory is 2000 units

Under this method fixed cost as well as

variable cost are been considered as a part of

product cost.

However, in this costing method, variable cost

is only counted as the product cost while the

fixed cost is been assumed as period cost.

In this the overheads are seen as quite different

that includes production, selling, distribution

and administration etc.

On this hand, in this the nature of the

overheads involves variable and the fixed

costs.

It focuses on determining the cost of each and

every single unit.

It emphasizes on identifying the cost of next

unit.

The main objective of this tool is to show an

accuracy and the fair treatment in relation to

the product cost.

The main purpose of this method is to assess

the contribution per unit in the product cost.

Statement of profit & loss for June in accordance with marginal costing method:

Particulars Cost per unit

Absorption costing Marginal costing

Direct material 15 15

Direct labour 25 25

Variable production

overhead 10 10

Fixed production

overhead 130000/20000 6.5

Total cost 56.5 50

Scenario 1: When production is 20000 units and closing inventory is 2000 units

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars Number of units Price per unit

(in £)

£ £

Sales revenue 20000 70 1400000

Prime cost

Opening stock 0 50 0

Add: production 22000 50 1100000

Less: closing

inventory

100000 1000000

Contribution 400000

Less: fixed

production

expenses

130000

Profit 270000

Profitability statement as per absorption costing for the month of June is enumerated below:

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 20000 70 1400000

Less: Cost of

sales

Opening stock 0 56.5 0

Add: production 22000 56.5 1243000

1243000

Less: inventory 2000 56.5 113000 1130000

(in £)

£ £

Sales revenue 20000 70 1400000

Prime cost

Opening stock 0 50 0

Add: production 22000 50 1100000

Less: closing

inventory

100000 1000000

Contribution 400000

Less: fixed

production

expenses

130000

Profit 270000

Profitability statement as per absorption costing for the month of June is enumerated below:

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 20000 70 1400000

Less: Cost of

sales

Opening stock 0 56.5 0

Add: production 22000 56.5 1243000

1243000

Less: inventory 2000 56.5 113000 1130000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

at the end of

period

Profit 270000

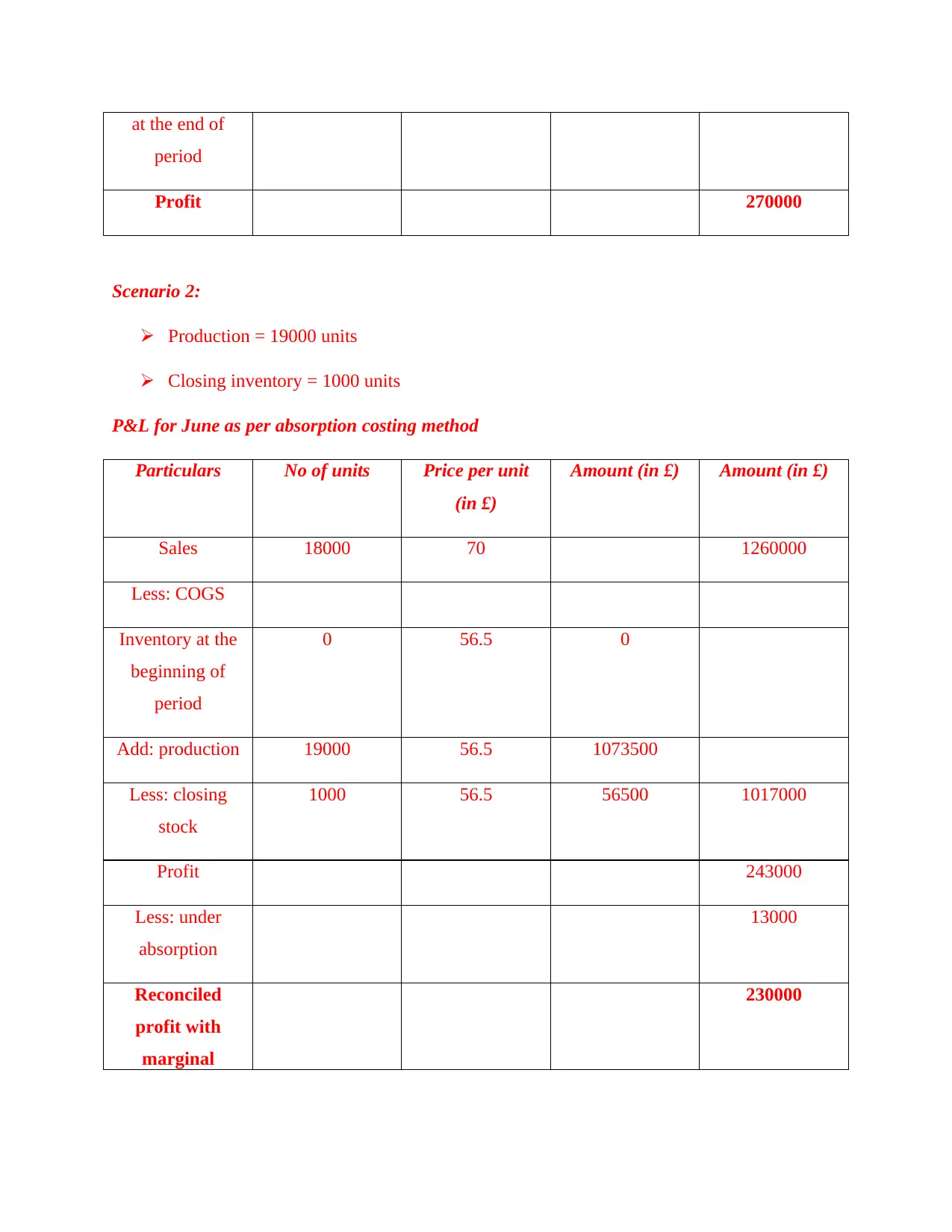

Scenario 2:

Production = 19000 units

Closing inventory = 1000 units

P&L for June as per absorption costing method

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 18000 70 1260000

Less: COGS

Inventory at the

beginning of

period

0 56.5 0

Add: production 19000 56.5 1073500

Less: closing

stock

1000 56.5 56500 1017000

Profit 243000

Less: under

absorption

13000

Reconciled

profit with

marginal

230000

period

Profit 270000

Scenario 2:

Production = 19000 units

Closing inventory = 1000 units

P&L for June as per absorption costing method

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Sales 18000 70 1260000

Less: COGS

Inventory at the

beginning of

period

0 56.5 0

Add: production 19000 56.5 1073500

Less: closing

stock

1000 56.5 56500 1017000

Profit 243000

Less: under

absorption

13000

Reconciled

profit with

marginal

230000

costing

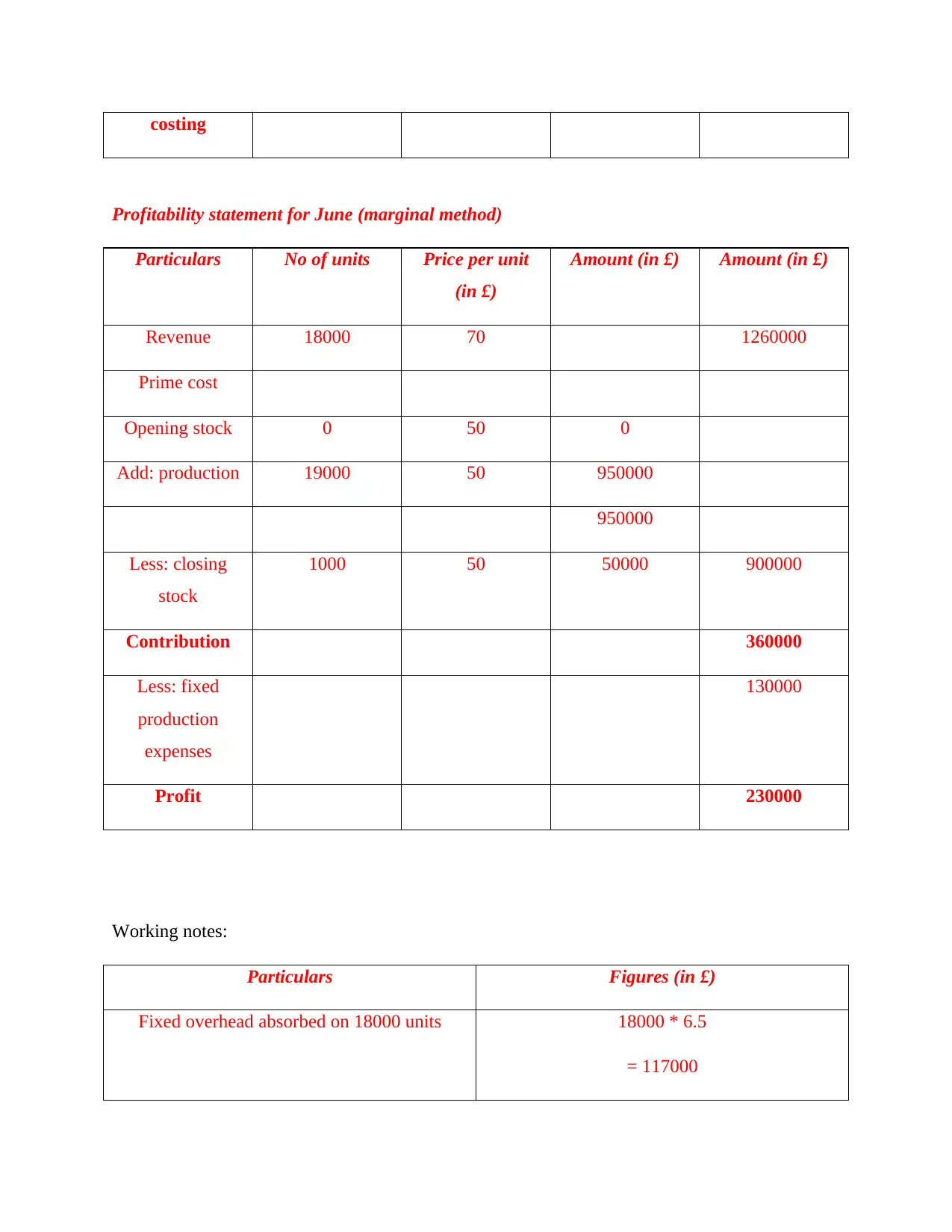

Profitability statement for June (marginal method)

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Revenue 18000 70 1260000

Prime cost

Opening stock 0 50 0

Add: production 19000 50 950000

950000

Less: closing

stock

1000 50 50000 900000

Contribution 360000

Less: fixed

production

expenses

130000

Profit 230000

Working notes:

Particulars Figures (in £)

Fixed overhead absorbed on 18000 units 18000 * 6.5

= 117000

Profitability statement for June (marginal method)

Particulars No of units Price per unit

(in £)

Amount (in £) Amount (in £)

Revenue 18000 70 1260000

Prime cost

Opening stock 0 50 0

Add: production 19000 50 950000

950000

Less: closing

stock

1000 50 50000 900000

Contribution 360000

Less: fixed

production

expenses

130000

Profit 230000

Working notes:

Particulars Figures (in £)

Fixed overhead absorbed on 18000 units 18000 * 6.5

= 117000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.