Analysis and Evaluation of Key Audit Matters in Financial Reports

VerifiedAdded on 2022/11/13

|18

|3362

|262

Report

AI Summary

This report provides a comprehensive analysis and evaluation of key audit matters (KAMs) within independent auditor's reports, with a particular focus on ASA 701 and its implications. The study begins with an examination of the rationale, objectives, and application of KAMs, followed by a detailed case study of the Lehman Brothers collapse, analyzing the auditing failures and how KAMs could have addressed the issues. The report also explores the revision of ASA 570 concerning going concern and its importance in auditor's reports. Furthermore, the efficiency of KAMs is evaluated through an analysis of the financial reports of several Australian banks, including Commonwealth Bank of Australia, Queensland Bank, Westpac, ANZ, National Bank of Australia, and Macquarie Group. The analysis assesses whether KAMs have achieved their intended purpose in the industry, offering insights into their impact on financial reporting transparency and investor decision-making. The report concludes with a synthesis of the findings and their implications for auditing practices.

Running head: CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN

THE INDEPENDENT AUDITORS REPORT

Critically analyze and evaluate key audit matters in the independent auditors report

Name of the student

Name of the university

Student ID

Author note

THE INDEPENDENT AUDITORS REPORT

Critically analyze and evaluate key audit matters in the independent auditors report

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Executive summary:

The paper intends to conduct an in depth analysis of the ASA 701 that was introduced in the

wake of financial crisis and several corporate collapse. One such corporate collapse is the

case of Lehman brothers that have been analyzed and evaluated in respect of ASA 701. In

addition to this, the paper also focuses on ASA 570 that seeks auditors to take into account

the going concern issue when forming the judgment on the entity’s financial performance.

The later section of the report conducts an analysis and evaluation of (KAM) key audit

matters of the banking organizations such as Commonwealth bank of Australia, Queensland

bank, Westapc bank, ANZ bank and National bank of Australia and Macquarie group limited.

From the analysis it is ascertained that the disclosure of key audit matters have served the

purpose in the industry.

INDEPENDENT AUDITORS REPORT

Executive summary:

The paper intends to conduct an in depth analysis of the ASA 701 that was introduced in the

wake of financial crisis and several corporate collapse. One such corporate collapse is the

case of Lehman brothers that have been analyzed and evaluated in respect of ASA 701. In

addition to this, the paper also focuses on ASA 570 that seeks auditors to take into account

the going concern issue when forming the judgment on the entity’s financial performance.

The later section of the report conducts an analysis and evaluation of (KAM) key audit

matters of the banking organizations such as Commonwealth bank of Australia, Queensland

bank, Westapc bank, ANZ bank and National bank of Australia and Macquarie group limited.

From the analysis it is ascertained that the disclosure of key audit matters have served the

purpose in the industry.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................4

Rationale and objectives of key audit matters:..........................................................................4

Application and requirement of key audit matter:.....................................................................4

Lehman brother case issue:........................................................................................................4

What did auditors do wrong?.....................................................................................................4

How key audit matters address the case:....................................................................................4

Revision of ASA 570:................................................................................................................4

Importance of going concern in auditor’s report:......................................................................4

Evaluating the efficiency of key audit matters in the financial report of the chosen banks:.....4

Does key audit matters achieved the purpose in the industry:...................................................4

Conclusion:................................................................................................................................4

References list:...........................................................................................................................5

INDEPENDENT AUDITORS REPORT

Table of Contents

Introduction:...............................................................................................................................4

Discussion:.................................................................................................................................4

Rationale and objectives of key audit matters:..........................................................................4

Application and requirement of key audit matter:.....................................................................4

Lehman brother case issue:........................................................................................................4

What did auditors do wrong?.....................................................................................................4

How key audit matters address the case:....................................................................................4

Revision of ASA 570:................................................................................................................4

Importance of going concern in auditor’s report:......................................................................4

Evaluating the efficiency of key audit matters in the financial report of the chosen banks:.....4

Does key audit matters achieved the purpose in the industry:...................................................4

Conclusion:................................................................................................................................4

References list:...........................................................................................................................5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Introduction:

The report elucidates the evaluatio of the key audit matters of the banking

organizations listed on the ASX (Australian stock exchange). Such analysis is done to

contribute to the importance of understanding the key audit matters and it presentation in the

independent auditor’s report. The facts presented under ASA 701 “ASA 701 for

communicating the key audit matters in the independent auditors report” is essential to

take into account for assessment of the key audit matters of different companies. In the

aftermath of the financial crisis and the failure of several corporate organizations, the

standard board has introduced the revised auditing standard for enhancing the communication

value of the auditor report. The objective of introducing this new auditing standard is to

augmenting the financial information transparency that is presented in the annual report and

assist the investors in making strategic investment decision. The detailed investigation into

the auditing standard has been done by presenting the case of Lehman brother and how did

the auditors went wrong on disclosing the accounting defects and issued fair view on the

financial statements. The revision of ASA 570 concerning the importance that is placed on

the issue of going concern of entity has also been evaluated.

The matters that are considered noteworthy by the auditors as per their professional

judgment in the auditing of the financial report are regarded as key audit matters (Christensen

et al. 2016). All such matters in the respective financial report of the entities have been

addressed by auditors for forming view on the financial report.

Discussion:

Rationale and objectives of key audit matters:

The auditors are responsible for communication the identified key audit matters along

with the form and content of the communication and the judgment that they have used in

evaluating the identified matters. Investors and users are provided with greater transparency

when seeking the financial information with the help of presentation of key audit matters and

thereby contribute to enhance the value of the prepared auditors report. It is indented by such

matter to assist the users in assessing making the significant judgment made by the

management of organization (Ahmed and Anifowose 2016). Moreover, it also contributes to

the engagement of the users with the management and personnel who are changed with

governance in an organization.

Requirement of key audit matter:

Since the key audit matters are considered to be relevant in the decision making

process of investors, it is essential for the reporting entity to make a presentation of such

matters in their financial report as per the new auditing standard. The importance of

presentation of such matters is attributable to the fact that they helps in determining the

existence of materiality in such accounts and how they would contribute to material

misstatement existence in the financial statements (Auasb.gov.au 2019). Therefore, it is of

utmost importance for the auditors to identify the key audit matters.

The auditing process is provided with several benefits due to the incorporation of the key

audit matter and its identification in the report. In this regard, it can be inferred that some of

the specific areas in reporting would improved due to identification of such matters and

INDEPENDENT AUDITORS REPORT

Introduction:

The report elucidates the evaluatio of the key audit matters of the banking

organizations listed on the ASX (Australian stock exchange). Such analysis is done to

contribute to the importance of understanding the key audit matters and it presentation in the

independent auditor’s report. The facts presented under ASA 701 “ASA 701 for

communicating the key audit matters in the independent auditors report” is essential to

take into account for assessment of the key audit matters of different companies. In the

aftermath of the financial crisis and the failure of several corporate organizations, the

standard board has introduced the revised auditing standard for enhancing the communication

value of the auditor report. The objective of introducing this new auditing standard is to

augmenting the financial information transparency that is presented in the annual report and

assist the investors in making strategic investment decision. The detailed investigation into

the auditing standard has been done by presenting the case of Lehman brother and how did

the auditors went wrong on disclosing the accounting defects and issued fair view on the

financial statements. The revision of ASA 570 concerning the importance that is placed on

the issue of going concern of entity has also been evaluated.

The matters that are considered noteworthy by the auditors as per their professional

judgment in the auditing of the financial report are regarded as key audit matters (Christensen

et al. 2016). All such matters in the respective financial report of the entities have been

addressed by auditors for forming view on the financial report.

Discussion:

Rationale and objectives of key audit matters:

The auditors are responsible for communication the identified key audit matters along

with the form and content of the communication and the judgment that they have used in

evaluating the identified matters. Investors and users are provided with greater transparency

when seeking the financial information with the help of presentation of key audit matters and

thereby contribute to enhance the value of the prepared auditors report. It is indented by such

matter to assist the users in assessing making the significant judgment made by the

management of organization (Ahmed and Anifowose 2016). Moreover, it also contributes to

the engagement of the users with the management and personnel who are changed with

governance in an organization.

Requirement of key audit matter:

Since the key audit matters are considered to be relevant in the decision making

process of investors, it is essential for the reporting entity to make a presentation of such

matters in their financial report as per the new auditing standard. The importance of

presentation of such matters is attributable to the fact that they helps in determining the

existence of materiality in such accounts and how they would contribute to material

misstatement existence in the financial statements (Auasb.gov.au 2019). Therefore, it is of

utmost importance for the auditors to identify the key audit matters.

The auditing process is provided with several benefits due to the incorporation of the key

audit matter and its identification in the report. In this regard, it can be inferred that some of

the specific areas in reporting would improved due to identification of such matters and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

thereby creating a positive impact on the overall reporting process of entity. Furthermore,

concerning the issues identified in the accounting treatment relating to any account, there

would be creation of transparency between such issues between the audit committee and

auditor due ti the identification of key audit matters.

Lehman brother case issue:

What did auditors do wrong?

This section discusses about the ineffective auditing practice due to the ineffective

auditing standards that failed to ascertain the accounting defects of the Lehman brother. The

failure of Lehman brother is considered as the largest collapse of the financial system with

the secondary reason attributable to the fair opinion by the auditors which duped many

investors into the wrongful investment decision making. Investors of the company were not

provided with great assistance in understanding the true financial performance of the Lehman

brother because the auditors and the auditing process was ineffective in identifying the key

audit matters that resulted in the failure of the corporate organization. The auditors were

negligent in reviewing the subprime loans that was issued by the banks for investors and the

long term projections considering the market uncertainties and risk was not reported by the

auditors. No investigation was conducted by the auditors on the defective accounting policy

of Repo 105 that was adopted by the large investment bank and accordingly they issued a

favorable audit opinion on the financial information (Gimbar et al. 2015). It was required by

the auditors to identify the reason for excess borrowing and its basis and their failure resulted

in the collapse. Therefore, it can be said that the failure was basically due to issue of

unqualified audit opinion as per the requirement of old auditing standard.

How key audit matters address the case:

Assessment of professional judgment by auditors is done in the new auditing standard

regarding the matters that should be communicated in the report. The transparency of the

financial report would have been enhanced by accounting for the key audit matters and

provided investors with the detailed of the financial information presented in the report. It is

done by the auditors highlighting the areas of material misstatements identified according to

the auditing standard. Furthermore, the auditors while framing the significant judgment and

determining the accounting estimates, uncertainty and assumptions would have evaluated the

management’s judgment (Auasb.gov.au 2019). Therefore, it is said that auditors would have

been able to identify the areas of significant judgment in the valuation of the accounts and

treatment under the auditing standard 701. The users would have been alerted on the defects

and the accounting gimmicks that misrepresented the financial statements.

Revision of ASA 570:

Investors have become well acquainted with the issues of the organization and their

organization’s ability to operate persistently due to the failure of organizations and after the

financial crisis. It is essential for the auditors to take into account the analysis of the

uncertainties which the organizations are exposed to for assessing their ability to operate

persistently. An assessment of the going concern should be conducted by the auditor along

with evaluating the appropriateness of the accounting policy associated with this particular

aspect. The auditor should make a conclusion remark on accounting policy used by the

INDEPENDENT AUDITORS REPORT

thereby creating a positive impact on the overall reporting process of entity. Furthermore,

concerning the issues identified in the accounting treatment relating to any account, there

would be creation of transparency between such issues between the audit committee and

auditor due ti the identification of key audit matters.

Lehman brother case issue:

What did auditors do wrong?

This section discusses about the ineffective auditing practice due to the ineffective

auditing standards that failed to ascertain the accounting defects of the Lehman brother. The

failure of Lehman brother is considered as the largest collapse of the financial system with

the secondary reason attributable to the fair opinion by the auditors which duped many

investors into the wrongful investment decision making. Investors of the company were not

provided with great assistance in understanding the true financial performance of the Lehman

brother because the auditors and the auditing process was ineffective in identifying the key

audit matters that resulted in the failure of the corporate organization. The auditors were

negligent in reviewing the subprime loans that was issued by the banks for investors and the

long term projections considering the market uncertainties and risk was not reported by the

auditors. No investigation was conducted by the auditors on the defective accounting policy

of Repo 105 that was adopted by the large investment bank and accordingly they issued a

favorable audit opinion on the financial information (Gimbar et al. 2015). It was required by

the auditors to identify the reason for excess borrowing and its basis and their failure resulted

in the collapse. Therefore, it can be said that the failure was basically due to issue of

unqualified audit opinion as per the requirement of old auditing standard.

How key audit matters address the case:

Assessment of professional judgment by auditors is done in the new auditing standard

regarding the matters that should be communicated in the report. The transparency of the

financial report would have been enhanced by accounting for the key audit matters and

provided investors with the detailed of the financial information presented in the report. It is

done by the auditors highlighting the areas of material misstatements identified according to

the auditing standard. Furthermore, the auditors while framing the significant judgment and

determining the accounting estimates, uncertainty and assumptions would have evaluated the

management’s judgment (Auasb.gov.au 2019). Therefore, it is said that auditors would have

been able to identify the areas of significant judgment in the valuation of the accounts and

treatment under the auditing standard 701. The users would have been alerted on the defects

and the accounting gimmicks that misrepresented the financial statements.

Revision of ASA 570:

Investors have become well acquainted with the issues of the organization and their

organization’s ability to operate persistently due to the failure of organizations and after the

financial crisis. It is essential for the auditors to take into account the analysis of the

uncertainties which the organizations are exposed to for assessing their ability to operate

persistently. An assessment of the going concern should be conducted by the auditor along

with evaluating the appropriateness of the accounting policy associated with this particular

aspect. The auditor should make a conclusion remark on accounting policy used by the

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

management for going concern (Auasb.gov.au 2019). Furthermore, they are also required to

make reporting of the uncertainty if any with the going concern issue.

Importance of going concern in auditor’s report:

Auditors are entrusted with the responsibility for evaluating and analyzing the issue

associated with the going concern of reporting entity. It would be required by the auditor to

issue an adverse opinion on financial report of the entity for which there is an evidence of

using an inappropriate using the assumptions and the accounting basis regarding the going

concern. In this regard, it is essential for the auditors to obtain sufficient and appropriate audit

evidence on the assumptions and estimates made by the management regarding the entity to

continue as going concern (Knechel and Salterio 2016). Furthermore, it is also required on

the part of auditors regarding the existence of any material uncertainty doubting the ability of

the organization to continue as going concern to make conclusion and state why they think

there are issues with the same.

Evaluating the efficiency of key audit matters in the financial report of the chosen

banks:

In this section, the evaluation and analysis of the key audit matters presented in the

financial report of the banking organizations listed on the ASX has been demonstrated. The

selected organizations comprise of Commonwealth bank of Australia, Queensland bank,

Westapc bank, ANZ bank and National bank of Australia and Macquarie group limited.

The auditors of Queensland bank of Australia have assessed key audit matters such as

goodwill valuation, fair value measurements of financial instruments, intangible computer

software valuation and collective impairment provisions. All the key audit matters have been

identified and presented in a separate section for which a detailed explanation on the reasons

of why particular account is regarded as material. The identified key audit matters are

addressed by employing appropriate technique such as developing the test of control and

using the appropriate sampling plan (Boq.com.au 2019). The key audit matters are assessed

by making reference to the notes to financial statements where details of each of the accounts

are given.

When analyzing the financial report of National bank of Australia, it has been

ascertained that the auditors have not identified any key audit matters for the year ending

2018. The auditors have presented a relevant view of the financial statements of the bank and

have based their opinion as per the auditing standard of Australia and according to the

requirements of the code of ethics. Therefore, it can be inferred that either there are not any

key audit matters identified from the financial information produced by the bank or the

auditor have not complied with the requirement of ASA 701 (Capital.nab.com.au 2019).

The auditors of Macquarie group limited have formed their opinion based on the

proficient judgment and identification of the key audit matters. Such matters identified relates

to the consolidated entity and the company as a whole. Some of the key audit matters that

have been identified include valuation of financial liabilities sand assets, provision for loss, It

system and control, impairment of assets, deferred tax liabilities and tax payable. The reason

why the accounts are considered to be of most significance has been disclosed by referring to

the notes to financial statements (Static.macquarie.com 2019).

INDEPENDENT AUDITORS REPORT

management for going concern (Auasb.gov.au 2019). Furthermore, they are also required to

make reporting of the uncertainty if any with the going concern issue.

Importance of going concern in auditor’s report:

Auditors are entrusted with the responsibility for evaluating and analyzing the issue

associated with the going concern of reporting entity. It would be required by the auditor to

issue an adverse opinion on financial report of the entity for which there is an evidence of

using an inappropriate using the assumptions and the accounting basis regarding the going

concern. In this regard, it is essential for the auditors to obtain sufficient and appropriate audit

evidence on the assumptions and estimates made by the management regarding the entity to

continue as going concern (Knechel and Salterio 2016). Furthermore, it is also required on

the part of auditors regarding the existence of any material uncertainty doubting the ability of

the organization to continue as going concern to make conclusion and state why they think

there are issues with the same.

Evaluating the efficiency of key audit matters in the financial report of the chosen

banks:

In this section, the evaluation and analysis of the key audit matters presented in the

financial report of the banking organizations listed on the ASX has been demonstrated. The

selected organizations comprise of Commonwealth bank of Australia, Queensland bank,

Westapc bank, ANZ bank and National bank of Australia and Macquarie group limited.

The auditors of Queensland bank of Australia have assessed key audit matters such as

goodwill valuation, fair value measurements of financial instruments, intangible computer

software valuation and collective impairment provisions. All the key audit matters have been

identified and presented in a separate section for which a detailed explanation on the reasons

of why particular account is regarded as material. The identified key audit matters are

addressed by employing appropriate technique such as developing the test of control and

using the appropriate sampling plan (Boq.com.au 2019). The key audit matters are assessed

by making reference to the notes to financial statements where details of each of the accounts

are given.

When analyzing the financial report of National bank of Australia, it has been

ascertained that the auditors have not identified any key audit matters for the year ending

2018. The auditors have presented a relevant view of the financial statements of the bank and

have based their opinion as per the auditing standard of Australia and according to the

requirements of the code of ethics. Therefore, it can be inferred that either there are not any

key audit matters identified from the financial information produced by the bank or the

auditor have not complied with the requirement of ASA 701 (Capital.nab.com.au 2019).

The auditors of Macquarie group limited have formed their opinion based on the

proficient judgment and identification of the key audit matters. Such matters identified relates

to the consolidated entity and the company as a whole. Some of the key audit matters that

have been identified include valuation of financial liabilities sand assets, provision for loss, It

system and control, impairment of assets, deferred tax liabilities and tax payable. The reason

why the accounts are considered to be of most significance has been disclosed by referring to

the notes to financial statements (Static.macquarie.com 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

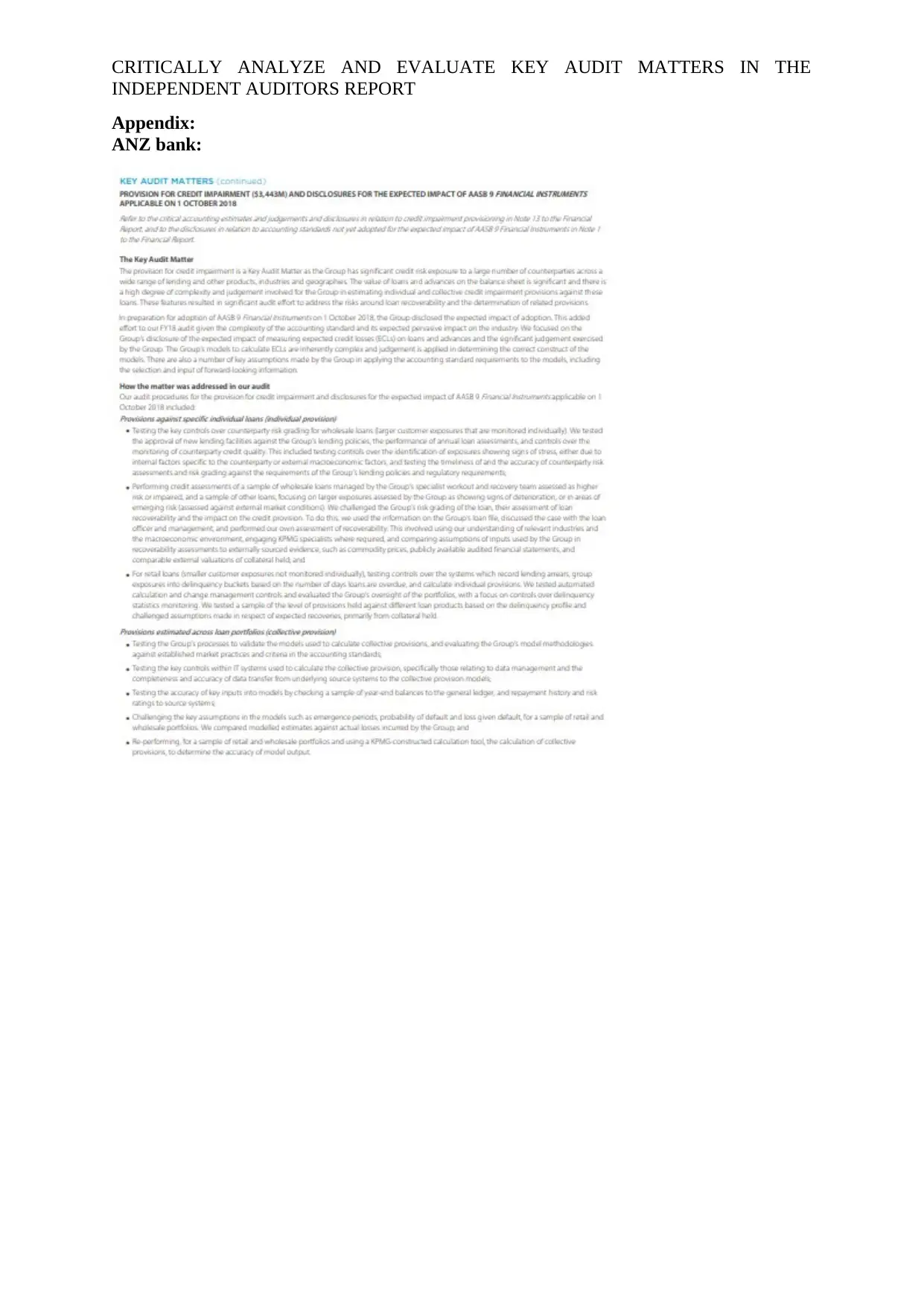

The identification of key audit matter of ANZ bank is done by auditors in relation to

the financial report as a whole. The identified key matters include provision for customer

remediation, accounting for divestments, financial instruments valuation, credit impairment

provisions and IT control and system. All the matters that are of significance in the auditing

process shave been addressed by the auditors using the appropriate audit procedures and

performing the proper assessments (Shareholder.anz.com 2019). In addition to this, auditors

also conducted an enquiry and obtained an understanding if the process of entity. Moreover,

the sampling plan has been developed that helps in testing the assertions related to each of the

accounts identified.

When analyzing the financial report of the Westpac bank of Australia, it was found

that an ongoing dialogue was maintained between the external auditor and audit committee

that the matters which are considered to be significantly important would be regarded the key

audit matters. A favorable opinion has been on the financial statements which indicate that

they present a true and fair view and there do not exist any material information leading to

materially misstate the financial information.

The auditors of Commonwealth bank of Australia have identified some of the key

audit matters such as provision for loan impairment, financial instruments assessment,

expected credit loss and provision for regulator action and risk. The assessment of the key

audit matters is done by developing the test of control and procedures such as testing the

accuracy and evaluating the valuation model (Commbank.com.au 2019).

It is inferred from the analysis of the key audit matters for the chosen banks all such

matters have been identified as per the requirements and responsibilities of the evaluation of

the financial statements and in the preparation of the financial report. In addition to this, there

has not been any separate opinion on the matters that are important for audit. Nevertheless,

the opinion on the financial system has been formed on the basis of the facts derived from the

key audit matters. In addition to this, the auditors are addressed such matters by developing

the analytical procedures and performing the proper test of control and conducting inspection

wherever required.

Does key audit matters achieved the purpose in the industry:

Evaluation of the financial report of all banks listed on ASX, it can be deduced that

while identifying the key audit matters, auditors have maintained professional judgment and

have determined appropriate threshold. Auditors have also presented the detailed reason by

referring to the financial statements notes in relation to the particular account explaining why

the matter was regarded as key audit matters and how it is relevant in the auditing process

and plan. Furthermore, auditors have implemented appropriate techniques wherever required

to address the matters identified. The financial report is an evident of the well documentation

and announcement of the key audit matters to the people and management as a whole

(George and Melinda 2015). Such disclosures have enhanced the transparency of the

financial information provided and therefore they formed the basis of strategic investment

decision making by the investors.

Conclusion:

The current paper demonstrating the importance of the new auditing standard has

revealed that its introduction has resulted in improving the transparency of information

provided to the users. It was also ascertained that the introduction of ASA 701 in the

aftermath of the financial crisis have necessitated the discourse of key financial matters.

INDEPENDENT AUDITORS REPORT

The identification of key audit matter of ANZ bank is done by auditors in relation to

the financial report as a whole. The identified key matters include provision for customer

remediation, accounting for divestments, financial instruments valuation, credit impairment

provisions and IT control and system. All the matters that are of significance in the auditing

process shave been addressed by the auditors using the appropriate audit procedures and

performing the proper assessments (Shareholder.anz.com 2019). In addition to this, auditors

also conducted an enquiry and obtained an understanding if the process of entity. Moreover,

the sampling plan has been developed that helps in testing the assertions related to each of the

accounts identified.

When analyzing the financial report of the Westpac bank of Australia, it was found

that an ongoing dialogue was maintained between the external auditor and audit committee

that the matters which are considered to be significantly important would be regarded the key

audit matters. A favorable opinion has been on the financial statements which indicate that

they present a true and fair view and there do not exist any material information leading to

materially misstate the financial information.

The auditors of Commonwealth bank of Australia have identified some of the key

audit matters such as provision for loan impairment, financial instruments assessment,

expected credit loss and provision for regulator action and risk. The assessment of the key

audit matters is done by developing the test of control and procedures such as testing the

accuracy and evaluating the valuation model (Commbank.com.au 2019).

It is inferred from the analysis of the key audit matters for the chosen banks all such

matters have been identified as per the requirements and responsibilities of the evaluation of

the financial statements and in the preparation of the financial report. In addition to this, there

has not been any separate opinion on the matters that are important for audit. Nevertheless,

the opinion on the financial system has been formed on the basis of the facts derived from the

key audit matters. In addition to this, the auditors are addressed such matters by developing

the analytical procedures and performing the proper test of control and conducting inspection

wherever required.

Does key audit matters achieved the purpose in the industry:

Evaluation of the financial report of all banks listed on ASX, it can be deduced that

while identifying the key audit matters, auditors have maintained professional judgment and

have determined appropriate threshold. Auditors have also presented the detailed reason by

referring to the financial statements notes in relation to the particular account explaining why

the matter was regarded as key audit matters and how it is relevant in the auditing process

and plan. Furthermore, auditors have implemented appropriate techniques wherever required

to address the matters identified. The financial report is an evident of the well documentation

and announcement of the key audit matters to the people and management as a whole

(George and Melinda 2015). Such disclosures have enhanced the transparency of the

financial information provided and therefore they formed the basis of strategic investment

decision making by the investors.

Conclusion:

The current paper demonstrating the importance of the new auditing standard has

revealed that its introduction has resulted in improving the transparency of information

provided to the users. It was also ascertained that the introduction of ASA 701 in the

aftermath of the financial crisis have necessitated the discourse of key financial matters.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Moreover, the auditors have also placed great importance on addressing the issues associated

with going concern and its relevance in determining the financial position of the entity. It has

been found from investigation on the case of Lehman brothers that the favorable opinion on

the misrepresented financial statements of the bank has resulted in its downfall. From the

analysis of the key audit matters of the chosen banks, it has been ascertained that the auditors

have identified as well addressed such matters and formed their audit opinion based on their

professional judgment as well as key audit matters.

References list:

Ahmed Haji, A. and Anifowose, M., 2016. Audit committee and integrated reporting

practice: does internal assurance matter?. Managerial Auditing Journal, 31(8/9), pp.915-948.

INDEPENDENT AUDITORS REPORT

Moreover, the auditors have also placed great importance on addressing the issues associated

with going concern and its relevance in determining the financial position of the entity. It has

been found from investigation on the case of Lehman brothers that the favorable opinion on

the misrepresented financial statements of the bank has resulted in its downfall. From the

analysis of the key audit matters of the chosen banks, it has been ascertained that the auditors

have identified as well addressed such matters and formed their audit opinion based on their

professional judgment as well as key audit matters.

References list:

Ahmed Haji, A. and Anifowose, M., 2016. Audit committee and integrated reporting

practice: does internal assurance matter?. Managerial Auditing Journal, 31(8/9), pp.915-948.

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Bédard, J., Coram, P., Espahbodi, R. and Mock, T.J., 2016. Does recent academic research

support changes to audit reporting standards?. Accounting Horizons, 30(2), pp.255-275.

Auasb.gov.au. (2019). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 21 May

2019].

Auasb.gov.au. (2019). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 21 May

2019].

Boq.com.au. (2019). [online] Available at:

https://www.boq.com.au/content/dam/boq/files/shareholder-centre/financial-results/2018/

FY2018_Annual_Report.pdf [Accessed 21 May 2019].

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), pp.1345-1362.

Capital.nab.com.au. (2019). [online] Available at:

https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.pdf [Accessed 21 May

2019].

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting

Research, 33(4), pp.1648-1684.

Commbank.com.au. (2019). [online] Available at:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/results/

fy18/cba-annual-report-2018.pdf [Accessed 21 May 2019].

Czerney, K., Schmidt, J.J. and Thompson, A.M., 2019. Do investors respond to explanatory

language included in unqualified audit reports?. Contemporary Accounting Research, 36(1),

pp.198-229.

George-Silviu, C. and Melinda-Timea, F., 2015. New audit reporting challenges: auditing the

going concern basis of accounting. Procedia Economics and Finance, 32, pp.216-224.

Gimbar, C., Hansen, B. and Ozlanski, M.E., 2016. The effects of critical audit matter

paragraphs and accounting standard precision on auditor liability. The Accounting

Review, 91(6), pp.1629-1646.

He, X., Pittman, J.A., Rui, O.M. and Wu, D., 2017. Do social ties between external auditors

and audit committee members affect audit quality?. The Accounting Review, 92(5), pp.61-87.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

INDEPENDENT AUDITORS REPORT

Bédard, J., Coram, P., Espahbodi, R. and Mock, T.J., 2016. Does recent academic research

support changes to audit reporting standards?. Accounting Horizons, 30(2), pp.255-275.

Auasb.gov.au. (2019). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 21 May

2019].

Auasb.gov.au. (2019). [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_570_2015.pdf [Accessed 21 May

2019].

Boq.com.au. (2019). [online] Available at:

https://www.boq.com.au/content/dam/boq/files/shareholder-centre/financial-results/2018/

FY2018_Annual_Report.pdf [Accessed 21 May 2019].

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), pp.1345-1362.

Capital.nab.com.au. (2019). [online] Available at:

https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.pdf [Accessed 21 May

2019].

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting

Research, 33(4), pp.1648-1684.

Commbank.com.au. (2019). [online] Available at:

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/results/

fy18/cba-annual-report-2018.pdf [Accessed 21 May 2019].

Czerney, K., Schmidt, J.J. and Thompson, A.M., 2019. Do investors respond to explanatory

language included in unqualified audit reports?. Contemporary Accounting Research, 36(1),

pp.198-229.

George-Silviu, C. and Melinda-Timea, F., 2015. New audit reporting challenges: auditing the

going concern basis of accounting. Procedia Economics and Finance, 32, pp.216-224.

Gimbar, C., Hansen, B. and Ozlanski, M.E., 2016. The effects of critical audit matter

paragraphs and accounting standard precision on auditor liability. The Accounting

Review, 91(6), pp.1629-1646.

He, X., Pittman, J.A., Rui, O.M. and Wu, D., 2017. Do social ties between external auditors

and audit committee members affect audit quality?. The Accounting Review, 92(5), pp.61-87.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Shareholder.anz.com. (2019). [online] Available at:

https://shareholder.anz.com/sites/default/files/anz_2018_annual_report_final.pdf [Accessed

21 May 2019].

Static.macquarie.com. (2019). [online] Available at:

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/results/

2018/Macquarie-Group-FY18-Annual-Report.pdf? [Accessed 21 May 2019].

Velte, P., 2018. Does gender diversity in the audit committee influence key audit matters'

readability in the audit report? UK evidence. Corporate social responsibility and

environmental management, 25(5), pp.748-755.

Westpac.com.au. (2019). [online] Available at:

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/

ASX_FY17_Financial_Results_Bookmarked.pdf [Accessed 21 May 2019].

INDEPENDENT AUDITORS REPORT

Shareholder.anz.com. (2019). [online] Available at:

https://shareholder.anz.com/sites/default/files/anz_2018_annual_report_final.pdf [Accessed

21 May 2019].

Static.macquarie.com. (2019). [online] Available at:

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/results/

2018/Macquarie-Group-FY18-Annual-Report.pdf? [Accessed 21 May 2019].

Velte, P., 2018. Does gender diversity in the audit committee influence key audit matters'

readability in the audit report? UK evidence. Corporate social responsibility and

environmental management, 25(5), pp.748-755.

Westpac.com.au. (2019). [online] Available at:

https://www.westpac.com.au/content/dam/public/wbc/documents/pdf/aw/ic/

ASX_FY17_Financial_Results_Bookmarked.pdf [Accessed 21 May 2019].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Appendix:

ANZ bank:

INDEPENDENT AUDITORS REPORT

Appendix:

ANZ bank:

CRITICALLY ANALYZE AND EVALUATE KEY AUDIT MATTERS IN THE

INDEPENDENT AUDITORS REPORT

Commonwealth bank of Australia:

INDEPENDENT AUDITORS REPORT

Commonwealth bank of Australia:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.