Analysis of Key Audit Matters in the Banking Sector

VerifiedAdded on 2022/11/23

|16

|3249

|1

Report

AI Summary

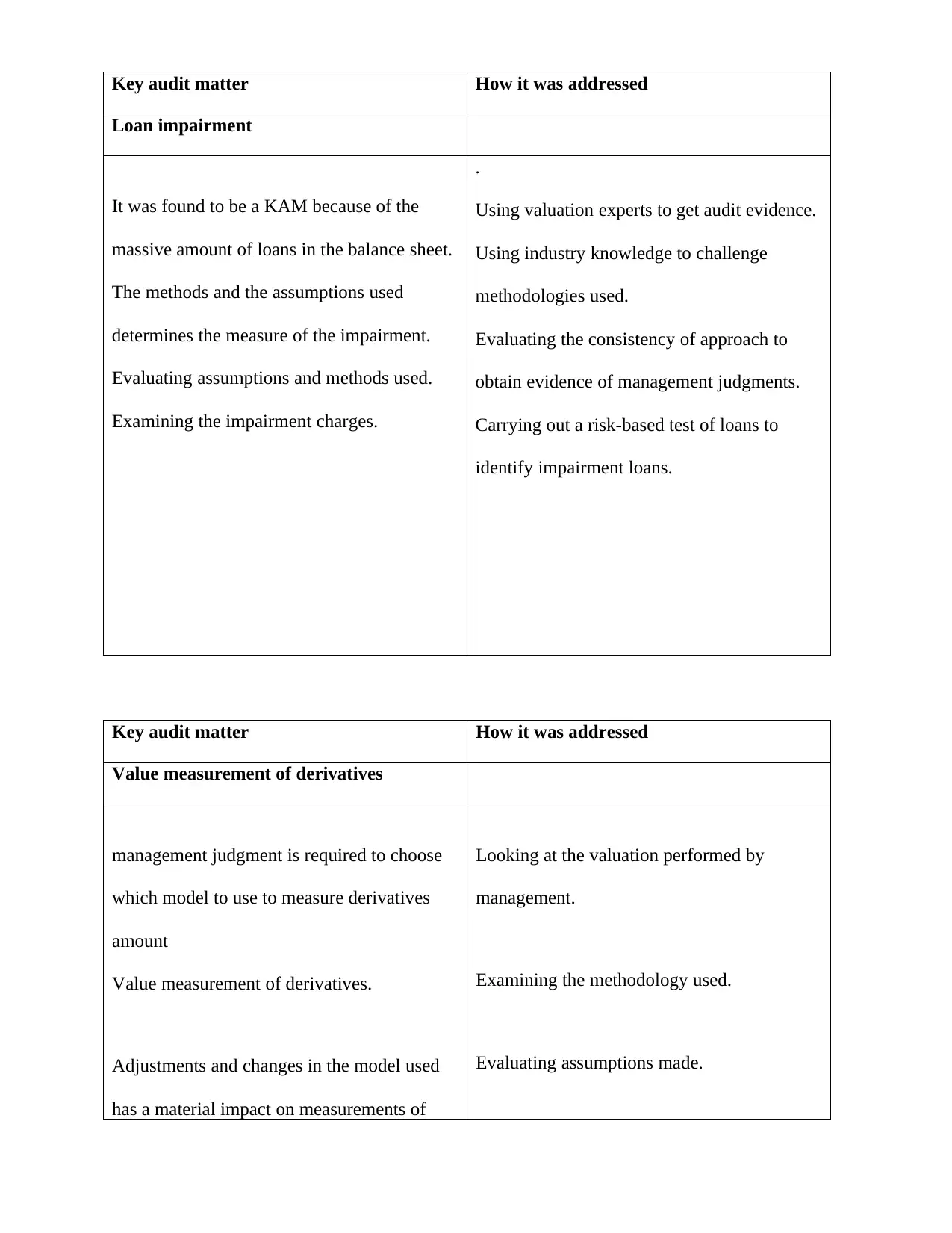

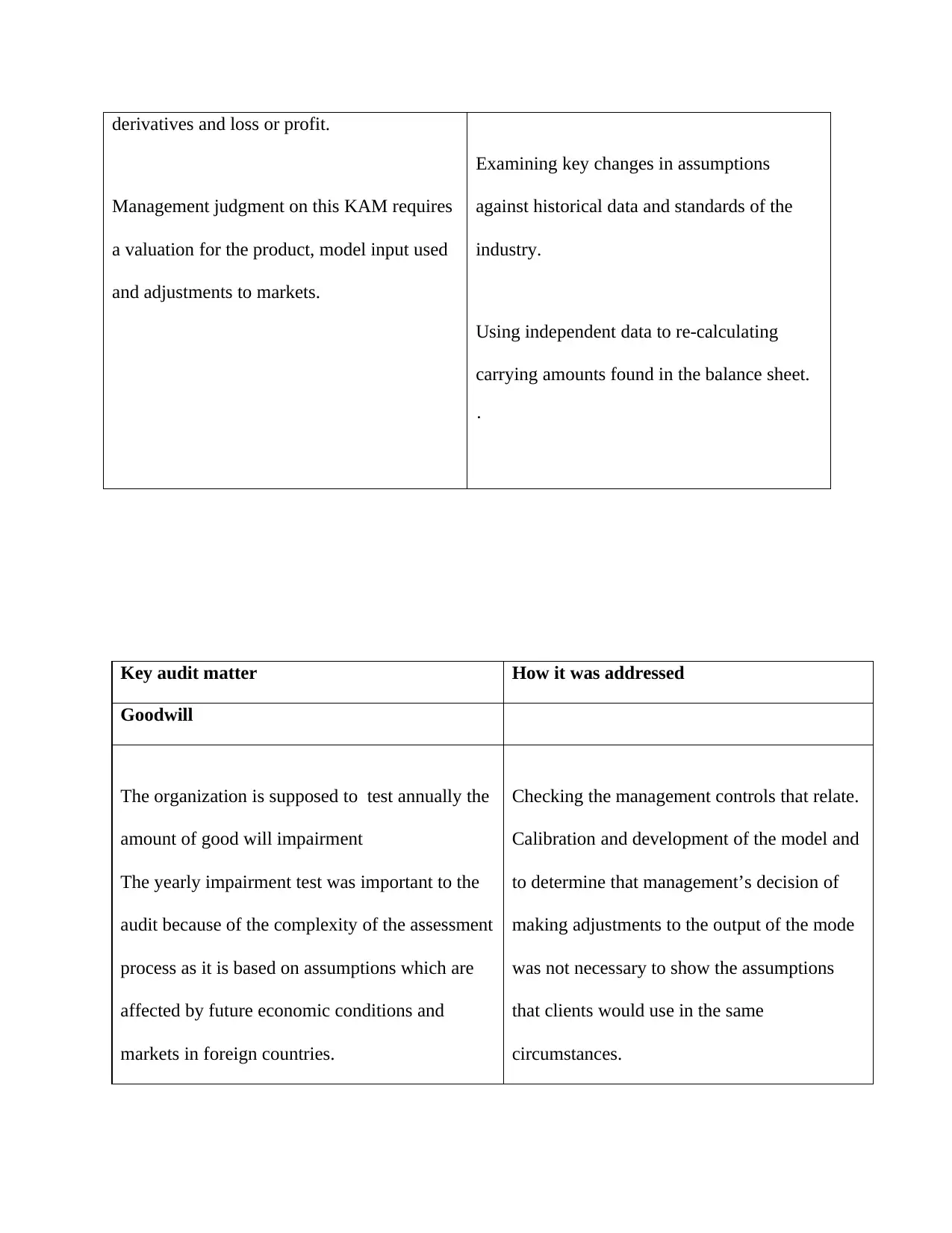

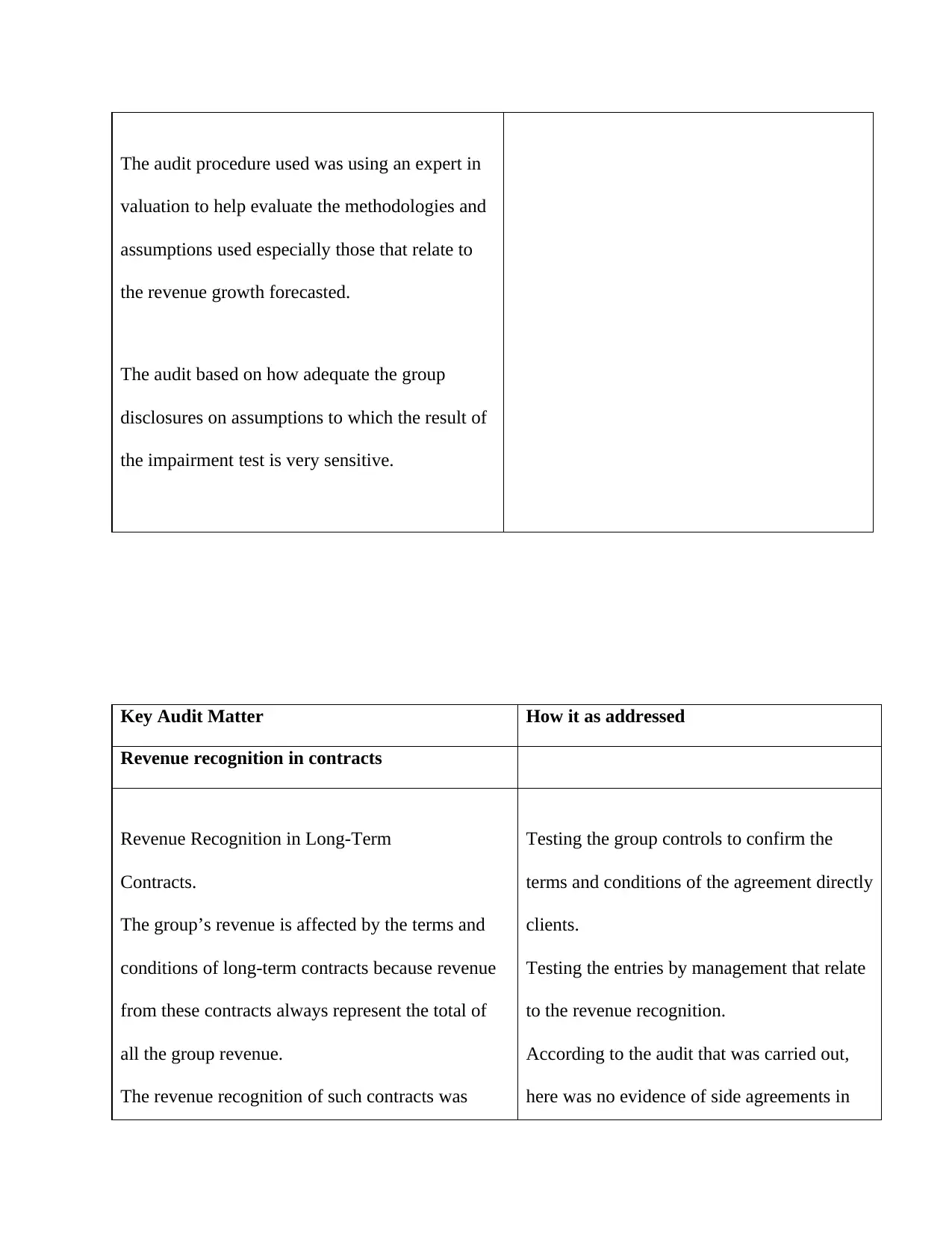

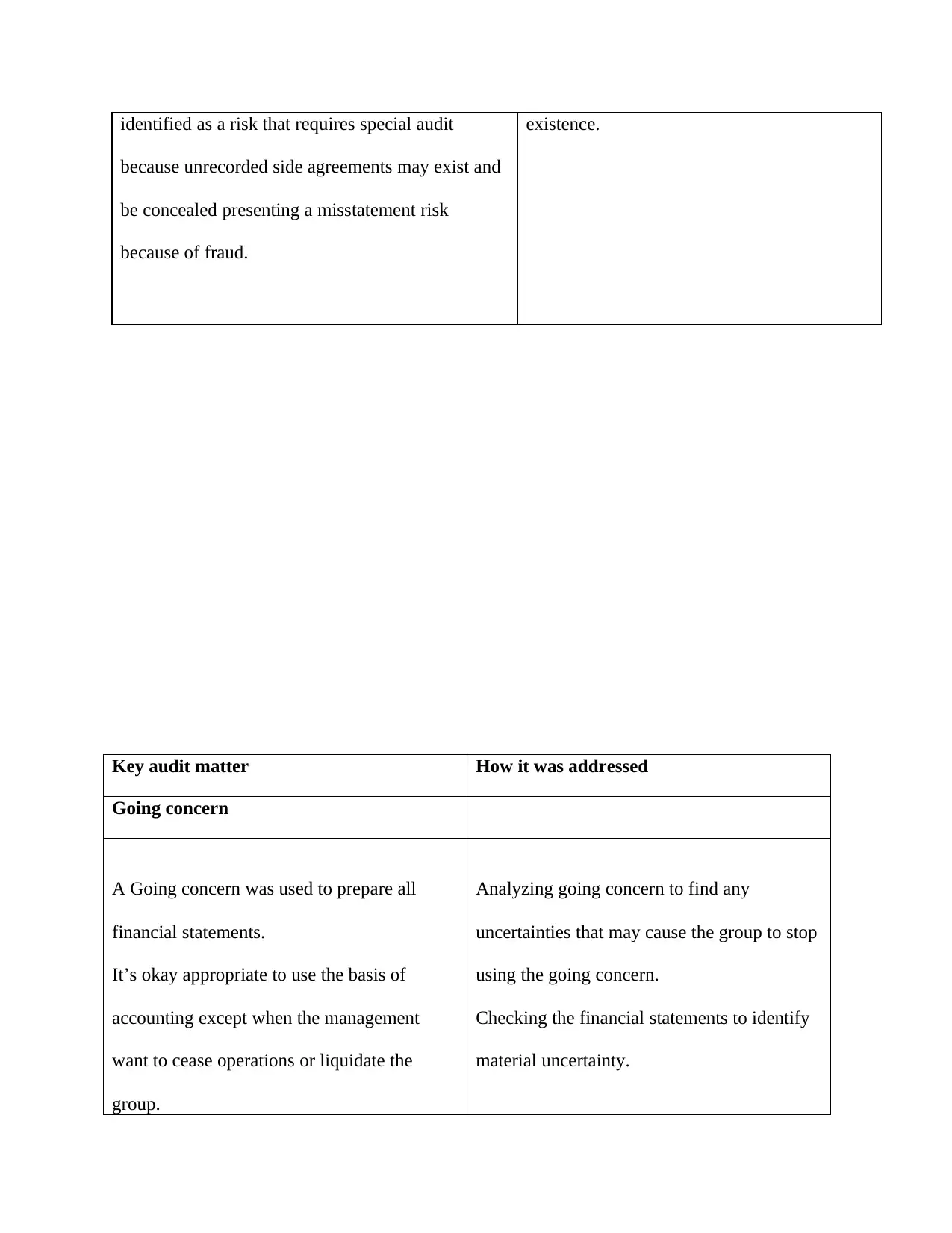

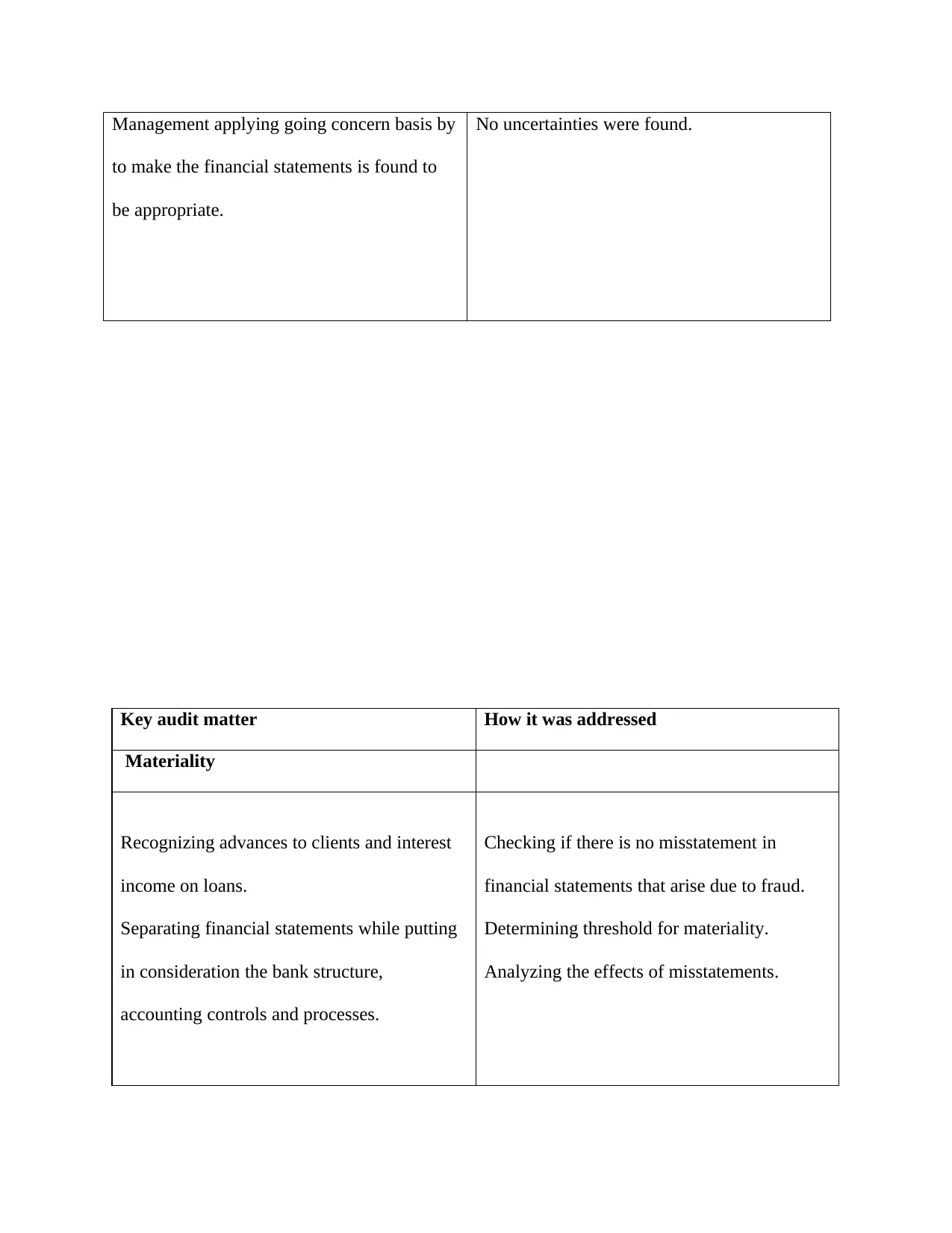

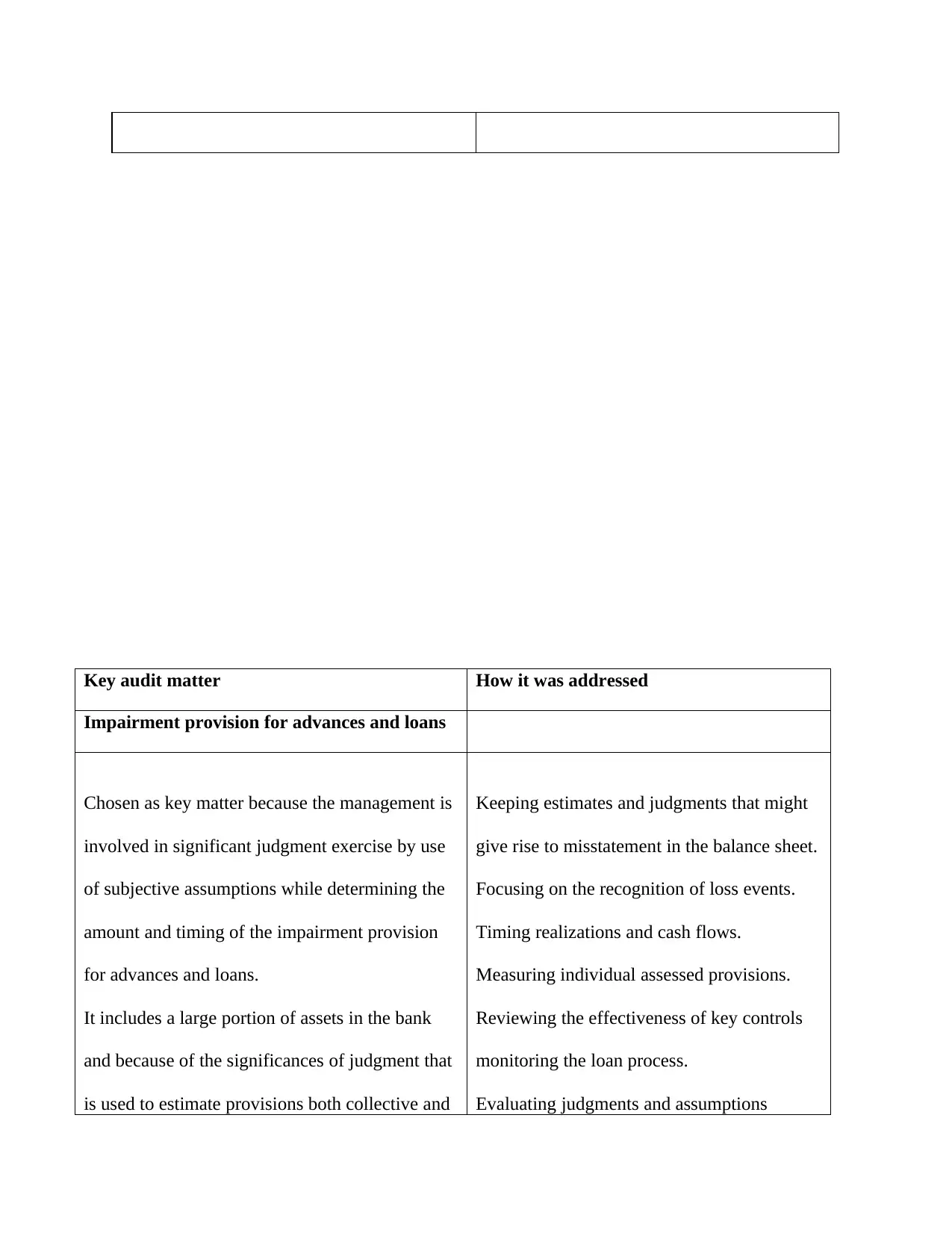

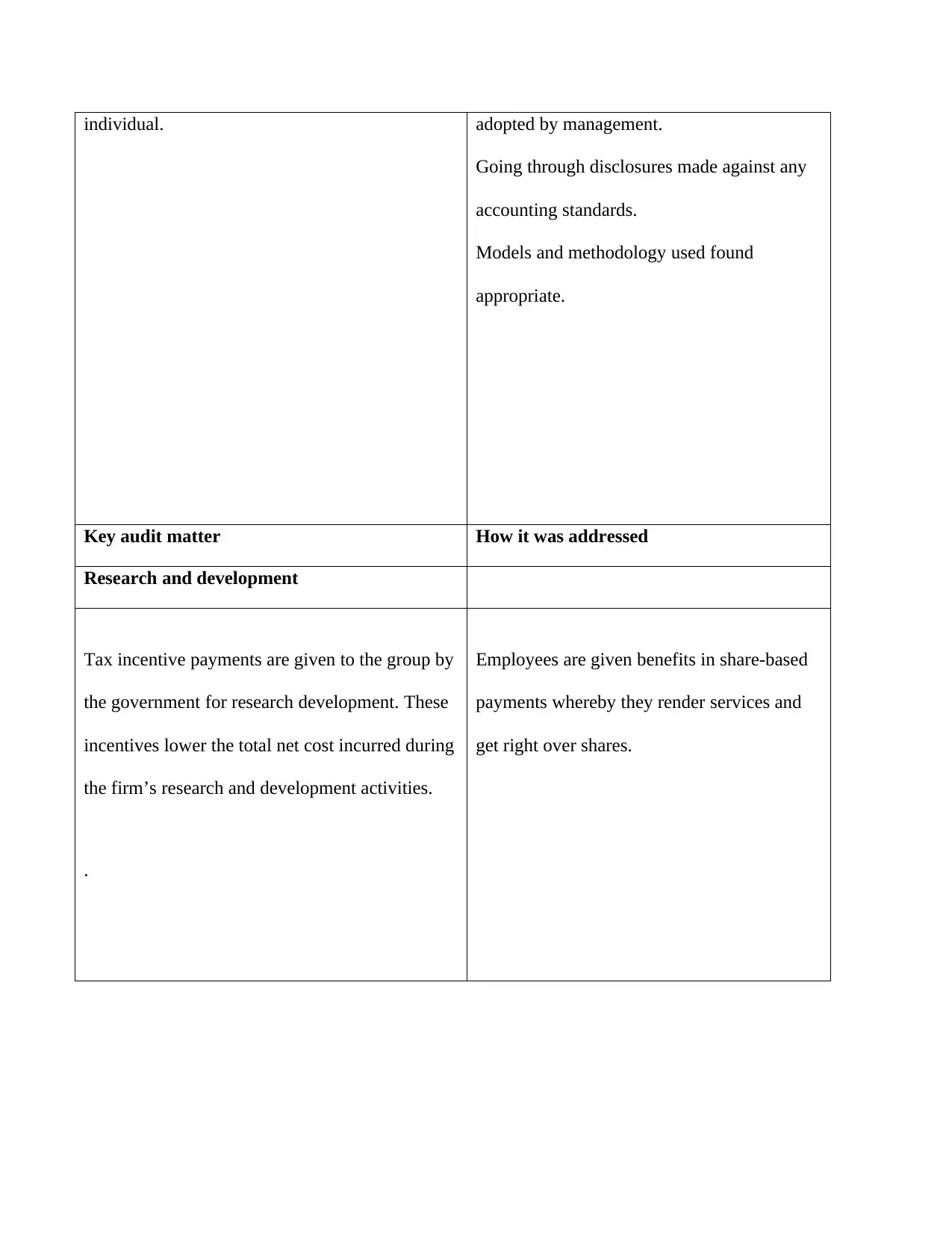

This report provides a comprehensive analysis and evaluation of key audit matters (KAM) within the banking industry, focusing on the implications of the new auditing standard ISA 701. The paper begins by defining KAMs and outlining the responsibilities of auditors and those charged with governance in their identification and communication. It then examines the factors influencing the inclusion of KAMs in audit reports, emphasizing the need for clear and concise reporting. A significant portion of the report is dedicated to the case of Lehman Brothers, detailing the company's fraudulent financial practices, the role of its auditors, and the subsequent regulatory changes. The analysis extends to specific KAMs in the banking sector, such as loan impairment, value measurement of derivatives, goodwill, revenue recognition, and going concern, providing detailed explanations of how these matters are addressed in audit reports and the procedures followed. The report concludes by emphasizing the importance of KAMs in enhancing transparency and investor confidence in the banking industry. The report also includes key audit matters arising from the banking industry in the following six banks that are listed in the ASX: ABC, ASX limited, ANZ Banking Group Limited, AMP, Danske, and APA group and how they were addressed.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.