Kidman Resources: Refinery vs. Outsourcing for Tesla Contract Analysis

VerifiedAdded on 2023/04/04

|9

|1635

|51

Report

AI Summary

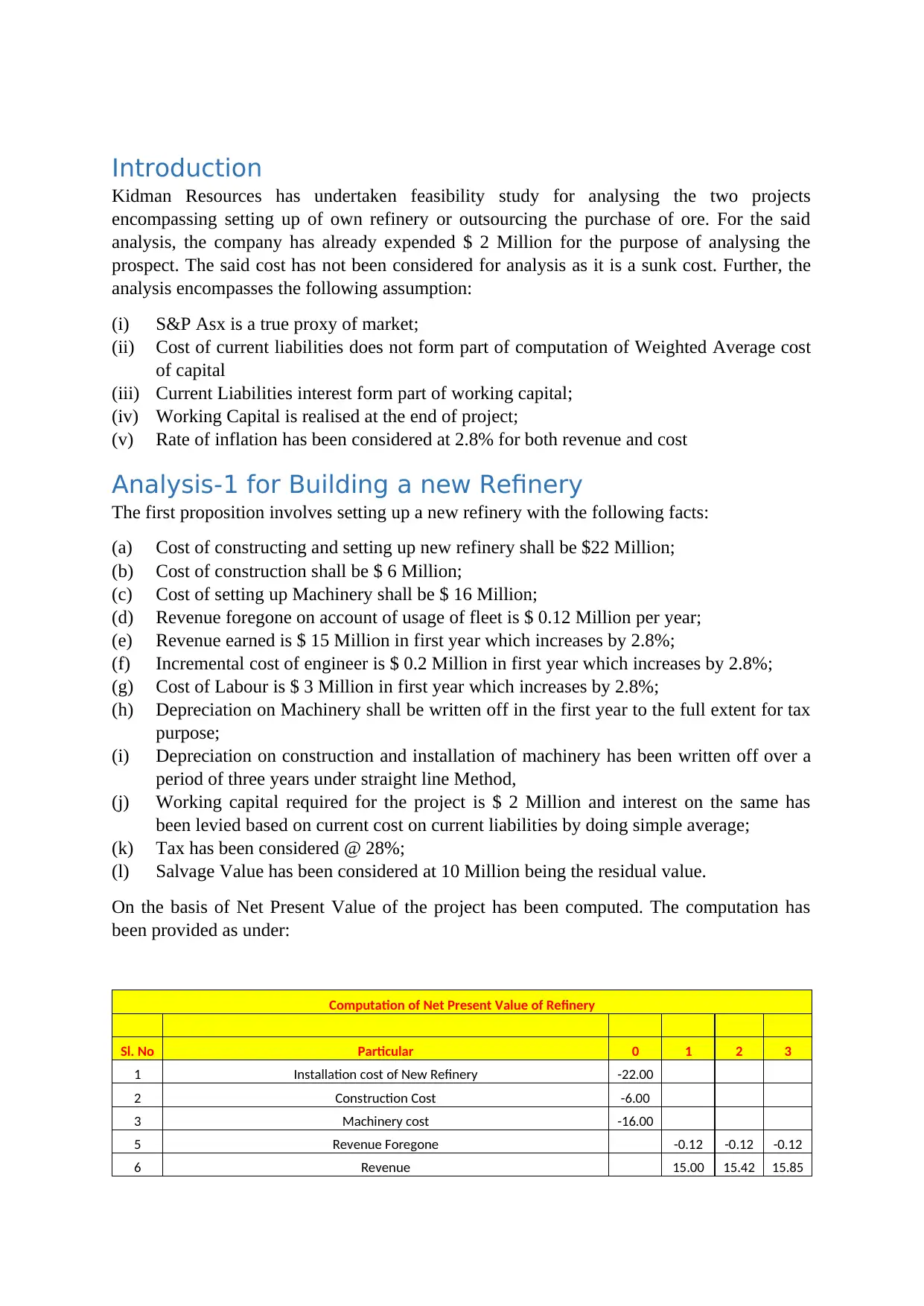

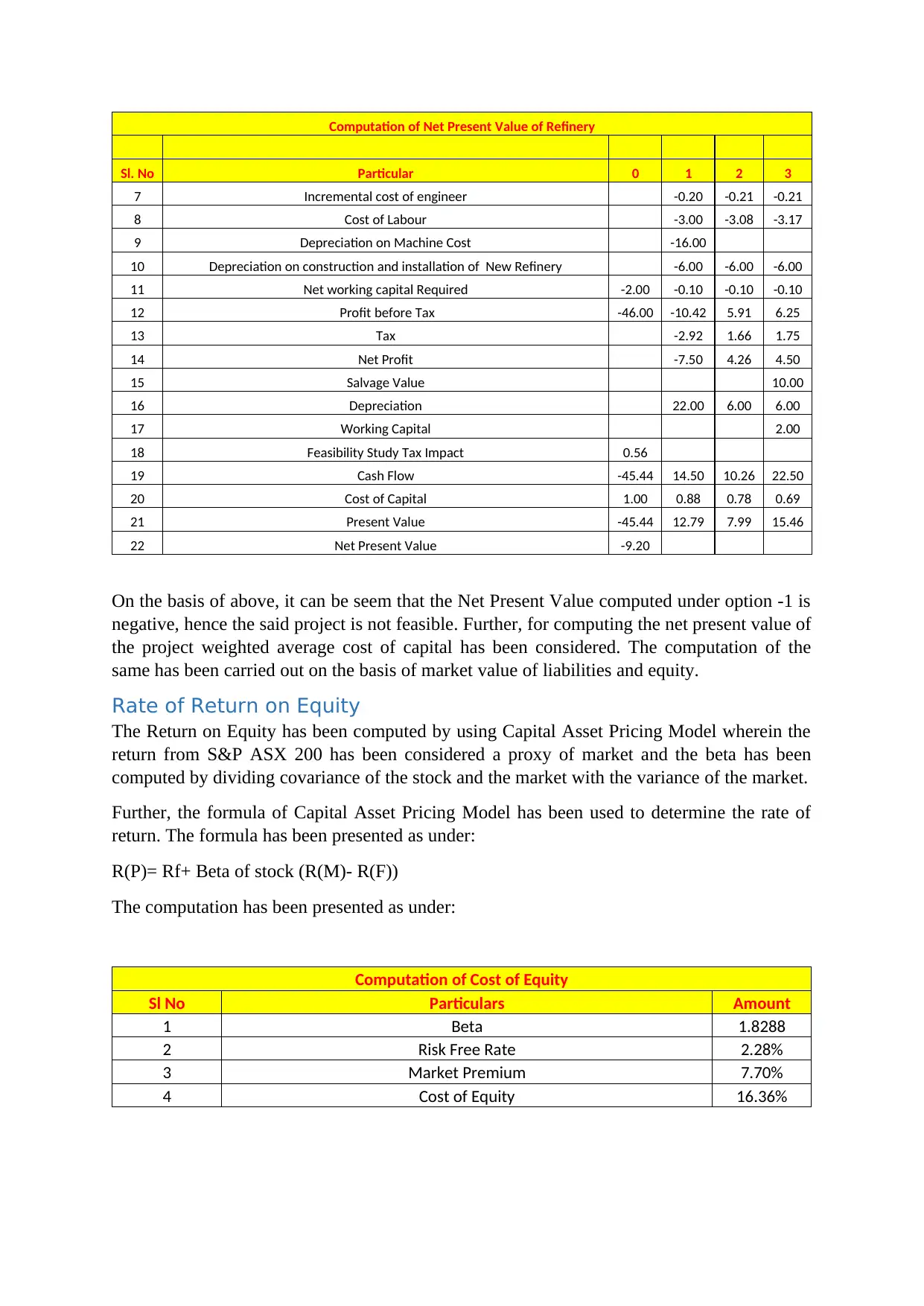

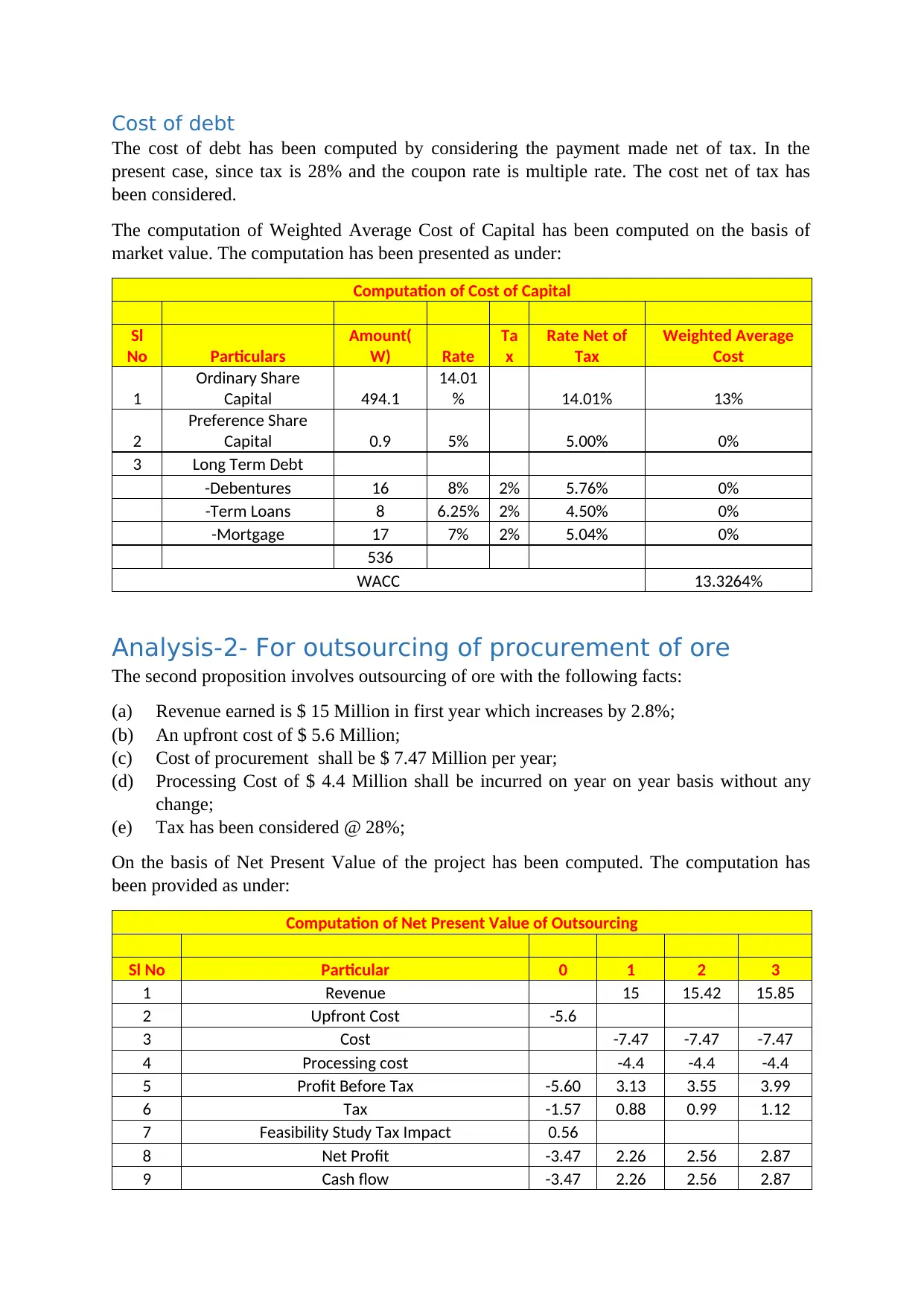

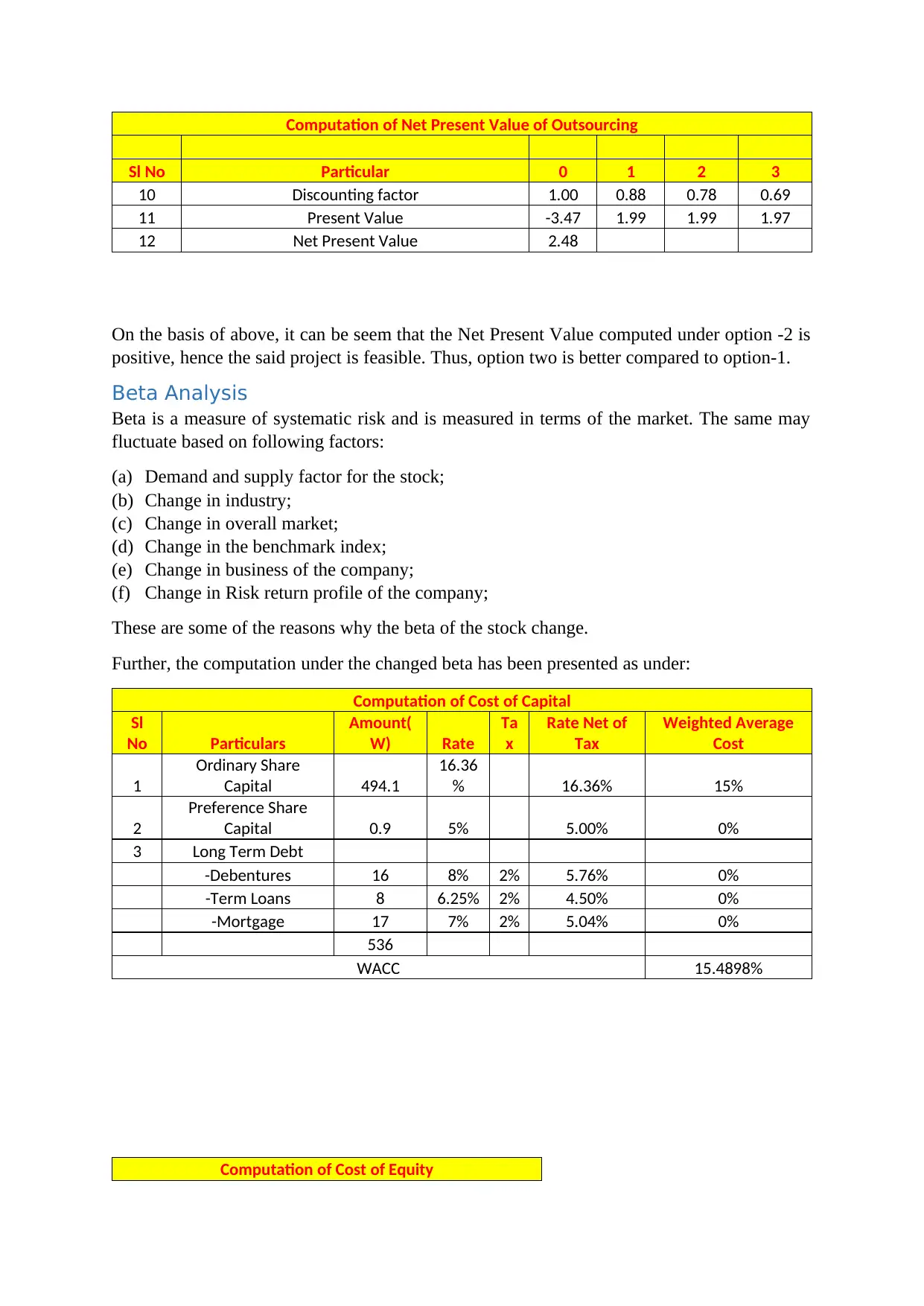

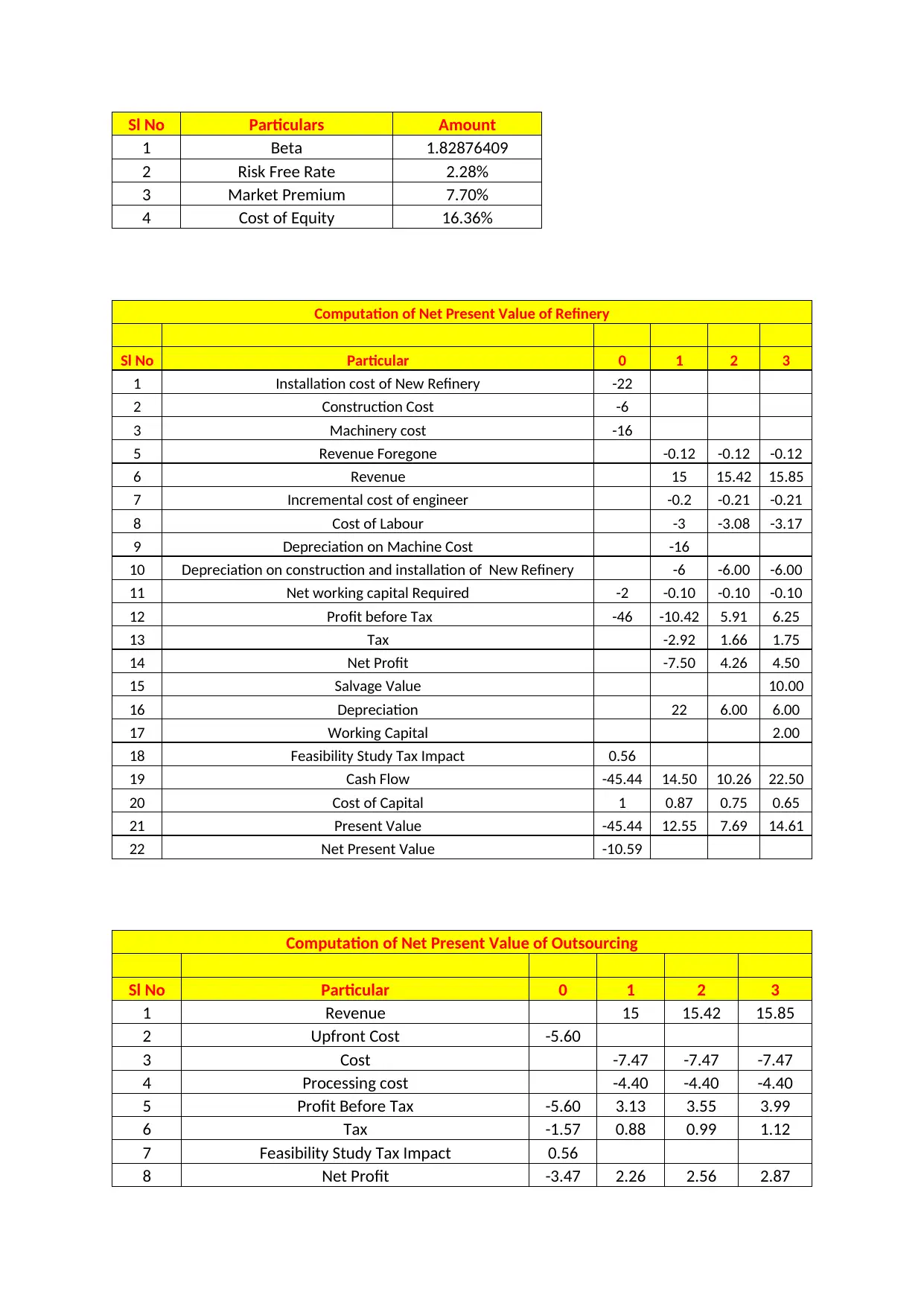

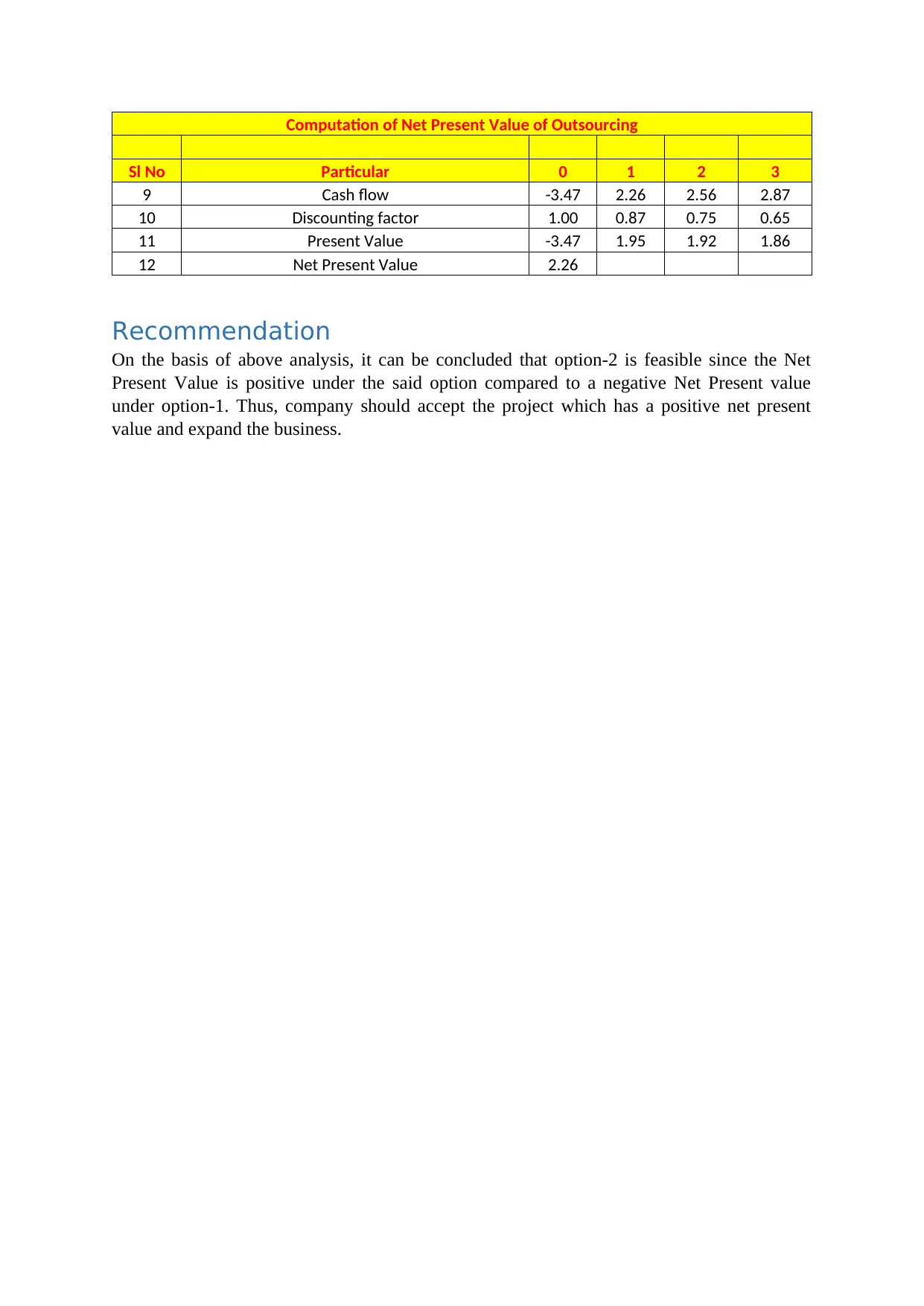

This report analyzes two business opportunities for Kidman Resources, stemming from a contract with Tesla to supply 5000 tonnes of Lithium Hydroxide over three years. The company must decide between building a refinery or outsourcing ore supply. The analysis, based on a feasibility study, evaluates the Net Present Value (NPV) of each option. The report considers costs of construction, machinery, revenue, labor, depreciation, working capital, and tax implications. It utilizes the Capital Asset Pricing Model (CAPM) to determine the cost of equity and calculates the Weighted Average Cost of Capital (WACC). The analysis reveals a negative NPV for building a refinery, making it infeasible, while outsourcing shows a positive NPV. The report also includes beta analysis and concludes that outsourcing is the more financially viable option, recommending its adoption to expand the business and fulfill the Tesla contract. The analysis also provides all the required financial data for each option.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.