King Edward VII College: BSBFIM501 Business Diploma Solution

VerifiedAdded on 2023/05/26

|13

|2833

|477

Homework Assignment

AI Summary

This assignment solution covers several aspects of a Business Diploma, including double-entry bookkeeping, cash and accrual accounting, depreciation, GST regulations, and employer tax obligations. It also includes a projected and actual marketing budget for 2017, analyzing variances and proposing adjustments, such as increasing the TV advertisement budget. The solution further analyzes the financial performance of Melbourne and Sydney campuses, comparing budget vs. actual sales, expenses, and net profit, identifying significant variances in expenses like electricity, gas, and office supplies. The document also touches upon key principles for managing a chart of accounts and the purpose of a profit and loss statement. Finally, aged debtor summaries and finance policies are mentioned, showcasing a broad understanding of financial management within a business context. Desklib offers additional resources like past papers and solved assignments for students.

Running Head: BUSINESS DIPLOMA 1

Business Diploma

Business Diploma

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS DIPLOMA 2

Table of Contents

Assessment 1...................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................4

Question 3....................................................................................................................................4

Question 4....................................................................................................................................5

Question 5....................................................................................................................................5

Question 6....................................................................................................................................5

Question 7....................................................................................................................................6

Question 8....................................................................................................................................6

Question 9....................................................................................................................................6

Question 10..................................................................................................................................6

Question 11..................................................................................................................................6

Question 12..................................................................................................................................7

Question 13..................................................................................................................................7

Question 14..................................................................................................................................7

Question 15..................................................................................................................................7

Question 16..................................................................................................................................8

Question 17..................................................................................................................................8

Question 18..................................................................................................................................8

Table of Contents

Assessment 1...................................................................................................................................4

Question 1....................................................................................................................................4

Question 2....................................................................................................................................4

Question 3....................................................................................................................................4

Question 4....................................................................................................................................5

Question 5....................................................................................................................................5

Question 6....................................................................................................................................5

Question 7....................................................................................................................................6

Question 8....................................................................................................................................6

Question 9....................................................................................................................................6

Question 10..................................................................................................................................6

Question 11..................................................................................................................................6

Question 12..................................................................................................................................7

Question 13..................................................................................................................................7

Question 14..................................................................................................................................7

Question 15..................................................................................................................................7

Question 16..................................................................................................................................8

Question 17..................................................................................................................................8

Question 18..................................................................................................................................8

BUSINESS DIPLOMA 3

Question 19..................................................................................................................................8

Question 20..................................................................................................................................9

Assessment 2...................................................................................................................................9

Assessment 3.................................................................................................................................10

Assessment 4.................................................................................................................................10

Assessment 5.................................................................................................................................11

References......................................................................................................................................13

Question 19..................................................................................................................................8

Question 20..................................................................................................................................9

Assessment 2...................................................................................................................................9

Assessment 3.................................................................................................................................10

Assessment 4.................................................................................................................................10

Assessment 5.................................................................................................................................11

References......................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS DIPLOMA 4

Assessment 1

Question 1

The basic principle of double entry book keeping is that, for every transaction, there are

always two entries. One entry is known as the debit entry and the other is known as the credit

entry (Sangster, 2015). These entries are often displayed in the 'T' accounts. The debit here refers

to increase in an asset, increase in an expense, decrease in a liability or decrease in income

(Sangster, 2015). And the credit represents the decrease in an acid, decrease in an expense,

increase in a liability and increase in income (Sangster, 2015).

Question 2

In accounting method where the payment receipts are recorded during the time when they

are received, where as the expenses are recorded at the time when they are actually paid, is

known as cash accounting (Kieso, Weygandt & Warfield, 2010). It is also known as cash-basis

accounting because the recording of revenue and expenses is done only when cash is paid and

received. One of the advantages of cash accounting as that it is the simplest method of recording

transactions as there only related to cash. The main disadvantage of this method is that it is not

very accurate.

Question 3

Accrual basis of accounting is that accounting method where the transactions are

recorded as and when they occur, which means only at the time of their occurrence (Needles,

Powers & Crosson, 2013). The advantage of accrual basis of accounting is that it is very

accurate. The main disadvantage is that it requires the recording of transactions to be done only

at the time of their occurrence.

Assessment 1

Question 1

The basic principle of double entry book keeping is that, for every transaction, there are

always two entries. One entry is known as the debit entry and the other is known as the credit

entry (Sangster, 2015). These entries are often displayed in the 'T' accounts. The debit here refers

to increase in an asset, increase in an expense, decrease in a liability or decrease in income

(Sangster, 2015). And the credit represents the decrease in an acid, decrease in an expense,

increase in a liability and increase in income (Sangster, 2015).

Question 2

In accounting method where the payment receipts are recorded during the time when they

are received, where as the expenses are recorded at the time when they are actually paid, is

known as cash accounting (Kieso, Weygandt & Warfield, 2010). It is also known as cash-basis

accounting because the recording of revenue and expenses is done only when cash is paid and

received. One of the advantages of cash accounting as that it is the simplest method of recording

transactions as there only related to cash. The main disadvantage of this method is that it is not

very accurate.

Question 3

Accrual basis of accounting is that accounting method where the transactions are

recorded as and when they occur, which means only at the time of their occurrence (Needles,

Powers & Crosson, 2013). The advantage of accrual basis of accounting is that it is very

accurate. The main disadvantage is that it requires the recording of transactions to be done only

at the time of their occurrence.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS DIPLOMA 5

Question 4

The reporting in calculation of depreciation is based upon to accounting principles named

cost principle and matching principle (Cotter, 2012). The former requires the expense of

depreciation and the asset amount to be based on the original cost of the asset. The letter

principal requires that the cost of an asset should be allocated to the expense of depreciation over

the asset's life.

Question 5

The New Tax System Act 1999 serves the purposes of tax periods and invoices, financial

supplies and reduced input tax credits (James, Sawyer & Wallschutzky, 2015). It prescribes the

additional information required for being contained in the tax invoices. It gives meaning to the

term financial supply which is input taxed under the GST act. It also sets out a list of decreased

credit acquisition.

Question 6

An employer is obligated to pay the employees portion of taxes. Firstly they should

register for the PAYG withholding (Lignier, Evans & Tran-Nam, 2014). Then an employer

should work out the status of the employees, next the need to work out the amount to be

withheld. The vigil amount should be reported and paid to the government. Finally, payment

summary should be provided to employees. Under the guarantee of superannuation, the

employees need to pay superannuation contributions of 9.5 per cent of the ordinary earnings of

an employee (Lignier, Evans & Tran-Nam, 2014).

Question 4

The reporting in calculation of depreciation is based upon to accounting principles named

cost principle and matching principle (Cotter, 2012). The former requires the expense of

depreciation and the asset amount to be based on the original cost of the asset. The letter

principal requires that the cost of an asset should be allocated to the expense of depreciation over

the asset's life.

Question 5

The New Tax System Act 1999 serves the purposes of tax periods and invoices, financial

supplies and reduced input tax credits (James, Sawyer & Wallschutzky, 2015). It prescribes the

additional information required for being contained in the tax invoices. It gives meaning to the

term financial supply which is input taxed under the GST act. It also sets out a list of decreased

credit acquisition.

Question 6

An employer is obligated to pay the employees portion of taxes. Firstly they should

register for the PAYG withholding (Lignier, Evans & Tran-Nam, 2014). Then an employer

should work out the status of the employees, next the need to work out the amount to be

withheld. The vigil amount should be reported and paid to the government. Finally, payment

summary should be provided to employees. Under the guarantee of superannuation, the

employees need to pay superannuation contributions of 9.5 per cent of the ordinary earnings of

an employee (Lignier, Evans & Tran-Nam, 2014).

BUSINESS DIPLOMA 6

Question 7

The items which are exempted under the GST what do not attract GST are raw silk and

silk waste, printed books and newspapers, agricultural implements, hand tools like spades and

shovels (Kaur, 2016).

Question 8

A business can report GST to the Australian tax office either monthly, quarterly or

annually. If it chooses to report its GST annually then it can go for the simpler BAS reporting

method. The business would need to report on the total sales, GST sales GST on purchases,

export sales, capital purchases and non capital purchases.

Question 9

If supplier does not provide an ABN and the total payment for the services and goods

exceeds $75 excluding the amount of GST, then the top rate of tax is usually withheld from the

payment and is paid to the government.

Question 10

Non profit organization would need to register for GST after it has a turnover of more

$150,000 per year.

Question 11

The key information that should be included in a tax invoice for sales of more than

$1,000 are the document of tax invoice, the seller's identity, ABN number, date of issue of

invoice, description of items sold, amount of GST.

Question 7

The items which are exempted under the GST what do not attract GST are raw silk and

silk waste, printed books and newspapers, agricultural implements, hand tools like spades and

shovels (Kaur, 2016).

Question 8

A business can report GST to the Australian tax office either monthly, quarterly or

annually. If it chooses to report its GST annually then it can go for the simpler BAS reporting

method. The business would need to report on the total sales, GST sales GST on purchases,

export sales, capital purchases and non capital purchases.

Question 9

If supplier does not provide an ABN and the total payment for the services and goods

exceeds $75 excluding the amount of GST, then the top rate of tax is usually withheld from the

payment and is paid to the government.

Question 10

Non profit organization would need to register for GST after it has a turnover of more

$150,000 per year.

Question 11

The key information that should be included in a tax invoice for sales of more than

$1,000 are the document of tax invoice, the seller's identity, ABN number, date of issue of

invoice, description of items sold, amount of GST.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS DIPLOMA 7

Question 12

The three basic types of financial statements are balance sheets, income statements and

cash flow statements (Brigham & Houston, 2012). The purpose of a balance sheet is to provide

detailed information regarding the assets, shareholder’s equity and the liabilities of a company.

The purpose of an income statement is to determine the revenue of a company which it earns

over a specific period of time. The cash flow statements are used for reporting the inflow and

outflow of cash of a company.

Question 13

The entities which are required to have financial reports audited are public companies,

private businesses, large retirement funds and non-profit organizations.

Question 14

The primary purpose of a financial or it is providing and objective independent

examination of the financial reports which increases the credibility and value of the financial

statements produced by a company. Hence financial audit increases the confidence of a user in

the financial statements and also reduces the investor risk. The objective of an auditor's report is

documenting reasonable assurance which a company's financial statements are free from.

Question 15

It is important for companies to develop budget for determining the economic objectives,

boundaries and limitations on expenditures of a business. It helps in holding company

accountable for each expense, reducing the costs and preparing for a worst case scenario.

Question 12

The three basic types of financial statements are balance sheets, income statements and

cash flow statements (Brigham & Houston, 2012). The purpose of a balance sheet is to provide

detailed information regarding the assets, shareholder’s equity and the liabilities of a company.

The purpose of an income statement is to determine the revenue of a company which it earns

over a specific period of time. The cash flow statements are used for reporting the inflow and

outflow of cash of a company.

Question 13

The entities which are required to have financial reports audited are public companies,

private businesses, large retirement funds and non-profit organizations.

Question 14

The primary purpose of a financial or it is providing and objective independent

examination of the financial reports which increases the credibility and value of the financial

statements produced by a company. Hence financial audit increases the confidence of a user in

the financial statements and also reduces the investor risk. The objective of an auditor's report is

documenting reasonable assurance which a company's financial statements are free from.

Question 15

It is important for companies to develop budget for determining the economic objectives,

boundaries and limitations on expenditures of a business. It helps in holding company

accountable for each expense, reducing the costs and preparing for a worst case scenario.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS DIPLOMA 8

Question 16

The simple steps of a budgeting process include calculating the overall expenses,

determining the income, setting the goals of savings and debt pay-off and recording the spending

and tracking progress.

Question 17

The common ways of improving cash inflow are, instead of buying one should lease, an

organization should always offer discounts on loans, a buying Co-Operative should be formed,

credit checks on customer should be conducted, invoices should be sent out immediately,

inventory should be improved up on, electronic payment should be used and the suppliers should

be paid less.

Question 18

Electronic spreadsheets are very useful in the development of budgets. They are used in

the preparation and tracking of budgets, calculating expenses conducting numerical analysis and

estimating the cost of job. It helps in keeping the track of expenses and income. It has the useful

feature of displaying results graphically. The related data can be linked easily in budgets.

Question 19

The three key principles related to the management of a chart of accounts are, the

information should be simply presented by the financial statements; one should be cautious

regarding adding extra accounts to the chart of accounts; the chart of account should be

streamlined in order to get the key information needed.

Question 16

The simple steps of a budgeting process include calculating the overall expenses,

determining the income, setting the goals of savings and debt pay-off and recording the spending

and tracking progress.

Question 17

The common ways of improving cash inflow are, instead of buying one should lease, an

organization should always offer discounts on loans, a buying Co-Operative should be formed,

credit checks on customer should be conducted, invoices should be sent out immediately,

inventory should be improved up on, electronic payment should be used and the suppliers should

be paid less.

Question 18

Electronic spreadsheets are very useful in the development of budgets. They are used in

the preparation and tracking of budgets, calculating expenses conducting numerical analysis and

estimating the cost of job. It helps in keeping the track of expenses and income. It has the useful

feature of displaying results graphically. The related data can be linked easily in budgets.

Question 19

The three key principles related to the management of a chart of accounts are, the

information should be simply presented by the financial statements; one should be cautious

regarding adding extra accounts to the chart of accounts; the chart of account should be

streamlined in order to get the key information needed.

BUSINESS DIPLOMA 9

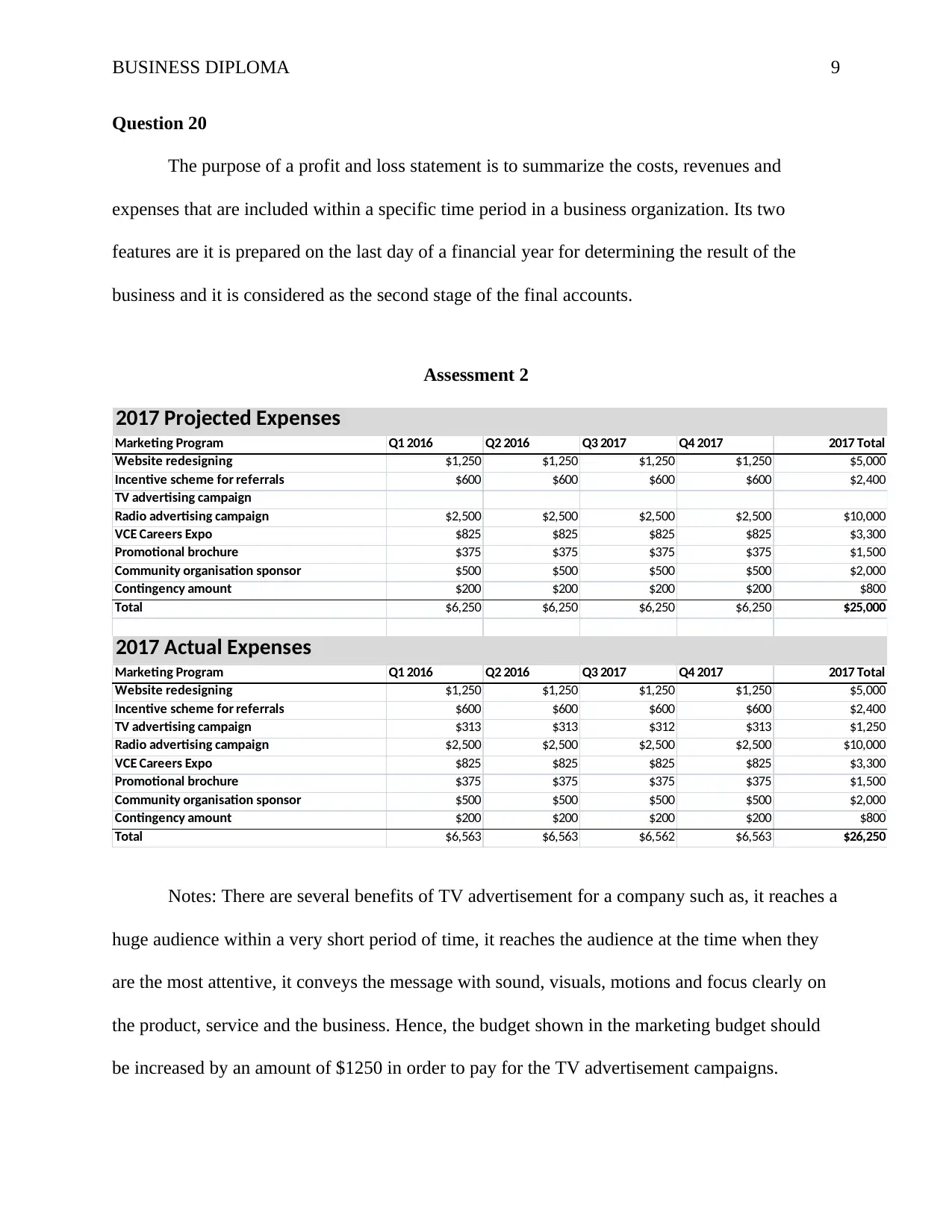

Question 20

The purpose of a profit and loss statement is to summarize the costs, revenues and

expenses that are included within a specific time period in a business organization. Its two

features are it is prepared on the last day of a financial year for determining the result of the

business and it is considered as the second stage of the final accounts.

Assessment 2

2017 Projected Expenses

Marketing Program Q1 2016 Q2 2016 Q3 2017 Q4 2017 2017 Total

Website redesigning $1,250 $1,250 $1,250 $1,250 $5,000

Incentive scheme for referrals $600 $600 $600 $600 $2,400

TV advertising campaign

Radio advertising campaign $2,500 $2,500 $2,500 $2,500 $10,000

VCE Careers Expo $825 $825 $825 $825 $3,300

Promotional brochure $375 $375 $375 $375 $1,500

Community organisation sponsor $500 $500 $500 $500 $2,000

Contingency amount $200 $200 $200 $200 $800

Total $6,250 $6,250 $6,250 $6,250 $25,000

2017 Actual Expenses

Marketing Program Q1 2016 Q2 2016 Q3 2017 Q4 2017 2017 Total

Website redesigning $1,250 $1,250 $1,250 $1,250 $5,000

Incentive scheme for referrals $600 $600 $600 $600 $2,400

TV advertising campaign $313 $313 $312 $313 $1,250

Radio advertising campaign $2,500 $2,500 $2,500 $2,500 $10,000

VCE Careers Expo $825 $825 $825 $825 $3,300

Promotional brochure $375 $375 $375 $375 $1,500

Community organisation sponsor $500 $500 $500 $500 $2,000

Contingency amount $200 $200 $200 $200 $800

Total $6,563 $6,563 $6,562 $6,563 $26,250

Notes: There are several benefits of TV advertisement for a company such as, it reaches a

huge audience within a very short period of time, it reaches the audience at the time when they

are the most attentive, it conveys the message with sound, visuals, motions and focus clearly on

the product, service and the business. Hence, the budget shown in the marketing budget should

be increased by an amount of $1250 in order to pay for the TV advertisement campaigns.

Question 20

The purpose of a profit and loss statement is to summarize the costs, revenues and

expenses that are included within a specific time period in a business organization. Its two

features are it is prepared on the last day of a financial year for determining the result of the

business and it is considered as the second stage of the final accounts.

Assessment 2

2017 Projected Expenses

Marketing Program Q1 2016 Q2 2016 Q3 2017 Q4 2017 2017 Total

Website redesigning $1,250 $1,250 $1,250 $1,250 $5,000

Incentive scheme for referrals $600 $600 $600 $600 $2,400

TV advertising campaign

Radio advertising campaign $2,500 $2,500 $2,500 $2,500 $10,000

VCE Careers Expo $825 $825 $825 $825 $3,300

Promotional brochure $375 $375 $375 $375 $1,500

Community organisation sponsor $500 $500 $500 $500 $2,000

Contingency amount $200 $200 $200 $200 $800

Total $6,250 $6,250 $6,250 $6,250 $25,000

2017 Actual Expenses

Marketing Program Q1 2016 Q2 2016 Q3 2017 Q4 2017 2017 Total

Website redesigning $1,250 $1,250 $1,250 $1,250 $5,000

Incentive scheme for referrals $600 $600 $600 $600 $2,400

TV advertising campaign $313 $313 $312 $313 $1,250

Radio advertising campaign $2,500 $2,500 $2,500 $2,500 $10,000

VCE Careers Expo $825 $825 $825 $825 $3,300

Promotional brochure $375 $375 $375 $375 $1,500

Community organisation sponsor $500 $500 $500 $500 $2,000

Contingency amount $200 $200 $200 $200 $800

Total $6,563 $6,563 $6,562 $6,563 $26,250

Notes: There are several benefits of TV advertisement for a company such as, it reaches a

huge audience within a very short period of time, it reaches the audience at the time when they

are the most attentive, it conveys the message with sound, visuals, motions and focus clearly on

the product, service and the business. Hence, the budget shown in the marketing budget should

be increased by an amount of $1250 in order to pay for the TV advertisement campaigns.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS DIPLOMA 10

Assessment 3

The projected expenses in the marketing budget for the year 2016 consists of items like

website redesigning, Incentive scheme for referral, Radio advertising campaign, VCE Careers

Expo, Promotional brochure, Community organization sponsor, and other contingency amount.

The total amount of budget which was allocated or projected was $25,000. However, TV

advertisement campaign is proposed to the organization and is included in the updated marketing

budget or the table showing actual expenses. Here the TV ad campaign expenses are included.

The proposal is for $10,000, however only a standard deviance of 5% is allowed. Hence, only

$1250 would be added to the proposed budget.

In the marketing expenditure, the website redesigning has been taken off due to problems with

the content and design and the need of increasing the SEO optimization. The incentive payments

have been paid more than expected and the student referrals have been poor, hence it was

removed. The allocation of the contingency amount was included however it was not adequate

for meeting the overrun.

Assessment 4

The actual sales of Melbourne were $475,000 which was $25,000 higher than the budget

amount. The total expenses of Melbourne amounted to be $365,800, which was $1400 greater

than the budgeted expenses. The actual net profit amount for Melbourne amounted to be

$109,200 which were $23,600 more than the budgeted net profit. This signifies that the actual

performance of the campus was good since it earned greater amount than its budgeted net profit.

For Melbourne, there was a 100 per cent variance in the expenses of electricity and gas,

the variance in the expenses of office supplies was 71.4 per cent, the stationery expenses

Assessment 3

The projected expenses in the marketing budget for the year 2016 consists of items like

website redesigning, Incentive scheme for referral, Radio advertising campaign, VCE Careers

Expo, Promotional brochure, Community organization sponsor, and other contingency amount.

The total amount of budget which was allocated or projected was $25,000. However, TV

advertisement campaign is proposed to the organization and is included in the updated marketing

budget or the table showing actual expenses. Here the TV ad campaign expenses are included.

The proposal is for $10,000, however only a standard deviance of 5% is allowed. Hence, only

$1250 would be added to the proposed budget.

In the marketing expenditure, the website redesigning has been taken off due to problems with

the content and design and the need of increasing the SEO optimization. The incentive payments

have been paid more than expected and the student referrals have been poor, hence it was

removed. The allocation of the contingency amount was included however it was not adequate

for meeting the overrun.

Assessment 4

The actual sales of Melbourne were $475,000 which was $25,000 higher than the budget

amount. The total expenses of Melbourne amounted to be $365,800, which was $1400 greater

than the budgeted expenses. The actual net profit amount for Melbourne amounted to be

$109,200 which were $23,600 more than the budgeted net profit. This signifies that the actual

performance of the campus was good since it earned greater amount than its budgeted net profit.

For Melbourne, there was a 100 per cent variance in the expenses of electricity and gas,

the variance in the expenses of office supplies was 71.4 per cent, the stationery expenses

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS DIPLOMA 11

variance was 62.5 per cent, and finally the variance in the expenses for water consumption was

30 per cent.

The actual sales of Sydney were $410,000 which was $60,000 or 17.14% higher than the

budget amount. The total expenses of Sydney amounted to be $334,720, which were $11,200

greater than the budgeted expenses. The actual net profit amount for Sydney amounted to be

$75,280 which were $48,800 or 184.29% more than the budgeted net profit. This signifies that

the actual performance of the campus was extraordinary since it earned a very high amount than

its budgeted net profit.

For Sydney, the variance in the total sales came out to be 17.14 per cent, the variance in

the expenses of electricity and gas, office supplies and stationery was one 33.33%, 100% and

78.57% respectively. Finally, the variance in the net profit was 184.29%.

Assessment 5

The age of data summary of the company shows that the total amount of receivables

equal to $3,320. Ryan has taken a credit from the company of 450, which has not been recovered

from him from the last 30 days. Michelle is 920 to the company which she took 90 days back.

The final receivable of the company is from Betty who took 750 from the company 60 days ago.

This shows with the company has a higher amount of receivables however, its collection process

is poor. Giving out too much credit is not a good thing for a company. Hence the company

should work on it's collection process. The best methods by which the company can improve

upon its debtors are, proper distribution of monthly aging report to the sales manager, reviewing

the terms of credits properly, reducing the payment term days to 10 days to 14 days depending

on the customers, offering incentives for oily payment. If payment terms are offered for more

variance was 62.5 per cent, and finally the variance in the expenses for water consumption was

30 per cent.

The actual sales of Sydney were $410,000 which was $60,000 or 17.14% higher than the

budget amount. The total expenses of Sydney amounted to be $334,720, which were $11,200

greater than the budgeted expenses. The actual net profit amount for Sydney amounted to be

$75,280 which were $48,800 or 184.29% more than the budgeted net profit. This signifies that

the actual performance of the campus was extraordinary since it earned a very high amount than

its budgeted net profit.

For Sydney, the variance in the total sales came out to be 17.14 per cent, the variance in

the expenses of electricity and gas, office supplies and stationery was one 33.33%, 100% and

78.57% respectively. Finally, the variance in the net profit was 184.29%.

Assessment 5

The age of data summary of the company shows that the total amount of receivables

equal to $3,320. Ryan has taken a credit from the company of 450, which has not been recovered

from him from the last 30 days. Michelle is 920 to the company which she took 90 days back.

The final receivable of the company is from Betty who took 750 from the company 60 days ago.

This shows with the company has a higher amount of receivables however, its collection process

is poor. Giving out too much credit is not a good thing for a company. Hence the company

should work on it's collection process. The best methods by which the company can improve

upon its debtors are, proper distribution of monthly aging report to the sales manager, reviewing

the terms of credits properly, reducing the payment term days to 10 days to 14 days depending

on the customers, offering incentives for oily payment. If payment terms are offered for more

BUSINESS DIPLOMA 12

than 30 days then, courtesy reminder should be sent. Credit card and online payment method

should be set up and selling on credit to the customers who usually feel it should be

discontinued.

A debtor management procedure should be developed and implemented in relation to customer

invoices. The steps here would be, setting up Credit Policy and terms of trade, setting up

estimates and invoicing, establishing accounts receivable processes, conducting Credit Checks

for identifying and mitigating risks, reviewing system and ledger monitoring, managing systems

and data, developing Credit Management services and finally provisioning bad debts.

than 30 days then, courtesy reminder should be sent. Credit card and online payment method

should be set up and selling on credit to the customers who usually feel it should be

discontinued.

A debtor management procedure should be developed and implemented in relation to customer

invoices. The steps here would be, setting up Credit Policy and terms of trade, setting up

estimates and invoicing, establishing accounts receivable processes, conducting Credit Checks

for identifying and mitigating risks, reviewing system and ledger monitoring, managing systems

and data, developing Credit Management services and finally provisioning bad debts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.