King's Own Institute ACC200: Job Costing Homework Assignment Solution

VerifiedAdded on 2022/11/18

|9

|1375

|77

Homework Assignment

AI Summary

This assignment solution focuses on job costing, a cost accounting method used to track costs for products made to customer specifications. The solution addresses several questions related to job costing, including calculating predetermined overhead rates, applying overhead costs to jobs, analyzing under-applied overhead, and comparing traditional costing with activity-based costing (ABC). The assignment includes calculations for direct materials, direct labor, and overhead costs, with examples for different job numbers. It also explores the advantages of ABC in allocating costs more accurately and the impact of overhead allocation on product costing. The solution further provides an analysis of the balance of finished goods and relevant references.

Running Head: JOB COSTING

JOB COSTING

JOB COSTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: JOB COSTING

Table of Contents

Job costing...................................................................................................................................................3

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................4

Question 3...................................................................................................................................................5

Question 4...................................................................................................................................................6

Question 5...................................................................................................................................................7

Question 6...................................................................................................................................................8

Table of Contents

Job costing...................................................................................................................................................3

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................4

Question 3...................................................................................................................................................5

Question 4...................................................................................................................................................6

Question 5...................................................................................................................................................7

Question 6...................................................................................................................................................8

Running Head: JOB COSTING

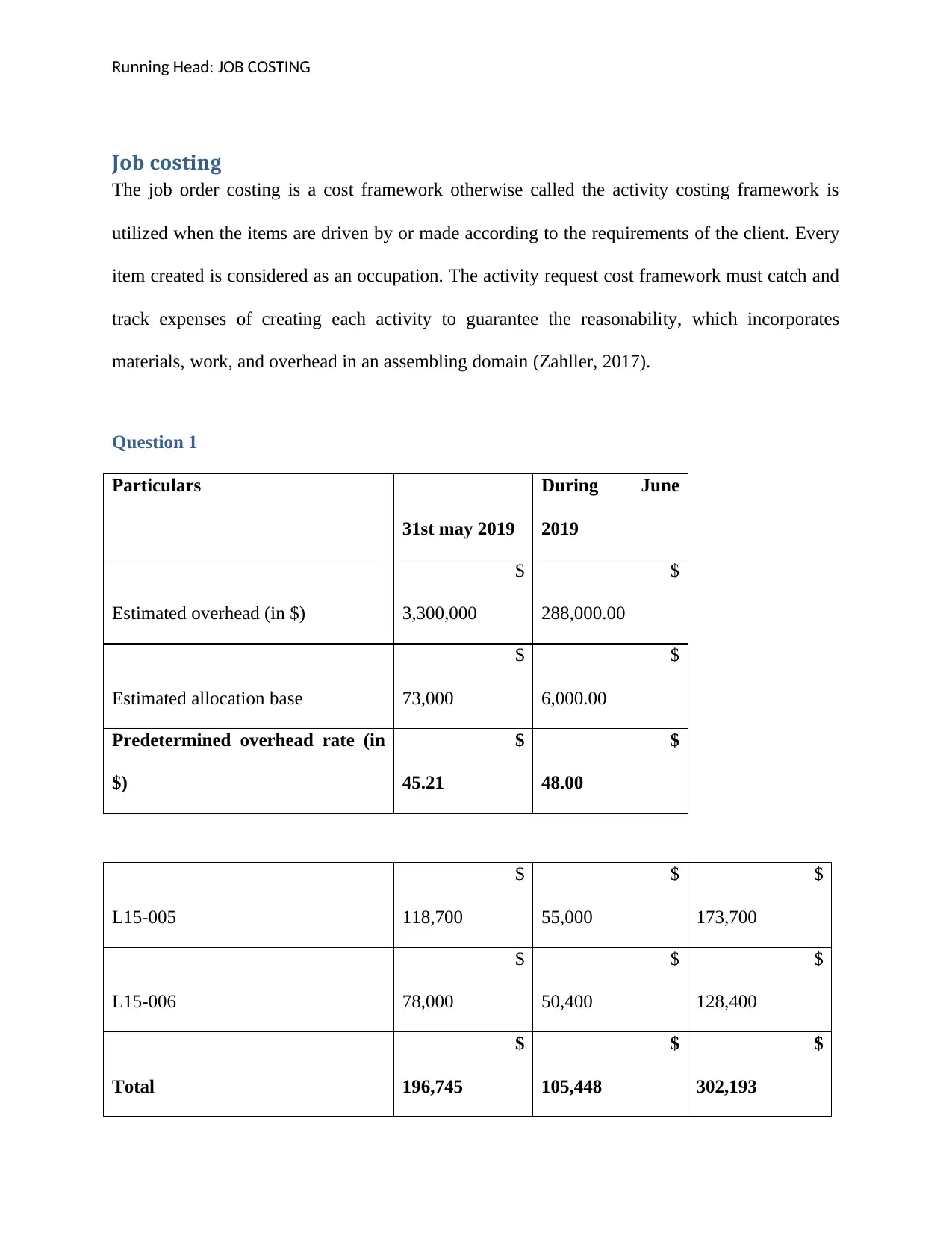

Job costing

The job order costing is a cost framework otherwise called the activity costing framework is

utilized when the items are driven by or made according to the requirements of the client. Every

item created is considered as an occupation. The activity request cost framework must catch and

track expenses of creating each activity to guarantee the reasonability, which incorporates

materials, work, and overhead in an assembling domain (Zahller, 2017).

Question 1

Particulars

31st may 2019

During June

2019

Estimated overhead (in $)

$

3,300,000

$

288,000.00

Estimated allocation base

$

73,000

$

6,000.00

Predetermined overhead rate (in

$)

$

45.21

$

48.00

L15-005

$

118,700

$

55,000

$

173,700

L15-006

$

78,000

$

50,400

$

128,400

Total

$

196,745

$

105,448

$

302,193

Job costing

The job order costing is a cost framework otherwise called the activity costing framework is

utilized when the items are driven by or made according to the requirements of the client. Every

item created is considered as an occupation. The activity request cost framework must catch and

track expenses of creating each activity to guarantee the reasonability, which incorporates

materials, work, and overhead in an assembling domain (Zahller, 2017).

Question 1

Particulars

31st may 2019

During June

2019

Estimated overhead (in $)

$

3,300,000

$

288,000.00

Estimated allocation base

$

73,000

$

6,000.00

Predetermined overhead rate (in

$)

$

45.21

$

48.00

L15-005

$

118,700

$

55,000

$

173,700

L15-006

$

78,000

$

50,400

$

128,400

Total

$

196,745

$

105,448

$

302,193

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: JOB COSTING

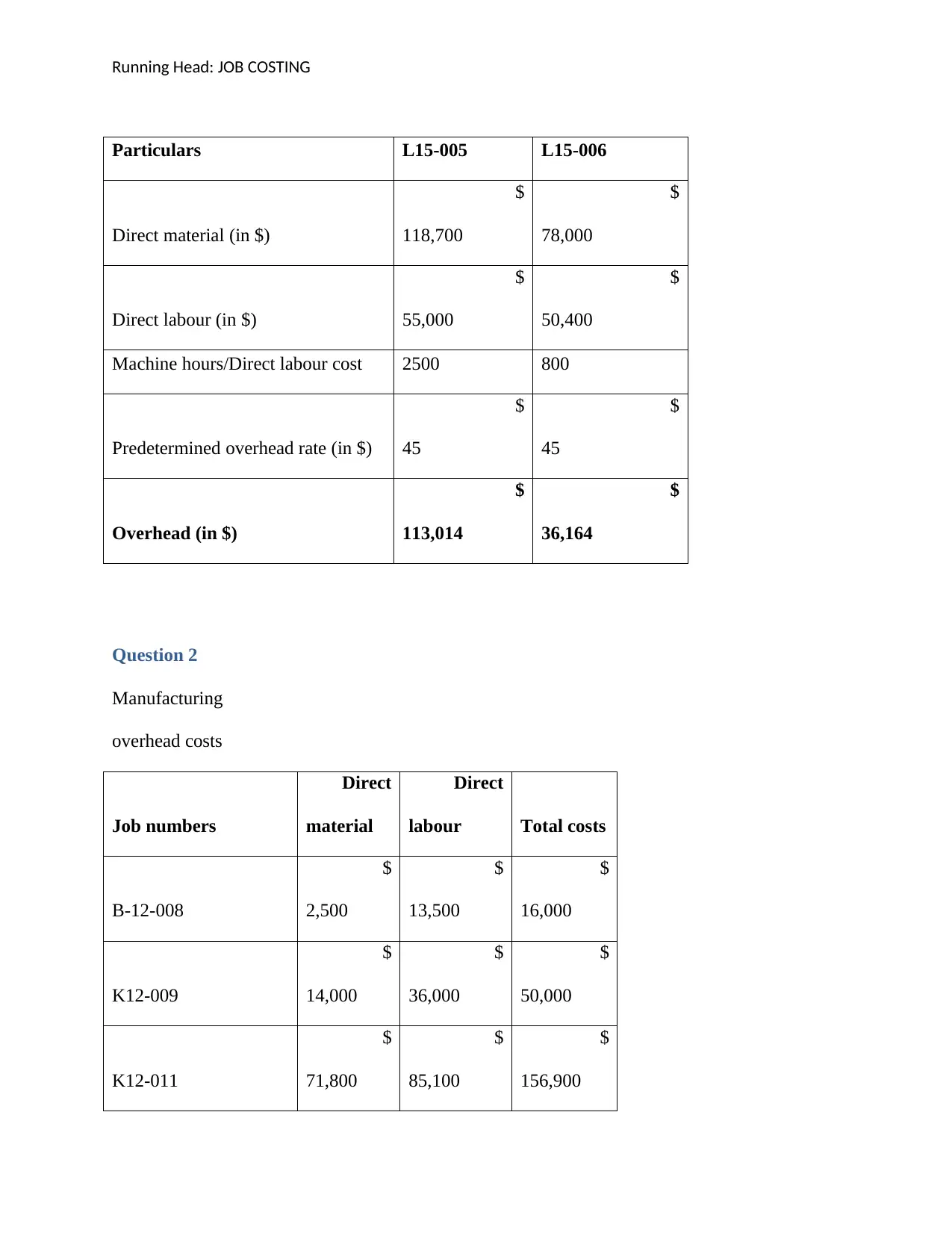

Particulars L15-005 L15-006

Direct material (in $)

$

118,700

$

78,000

Direct labour (in $)

$

55,000

$

50,400

Machine hours/Direct labour cost 2500 800

Predetermined overhead rate (in $)

$

45

$

45

Overhead (in $)

$

113,014

$

36,164

Question 2

Manufacturing

overhead costs

Job numbers

Direct

material

Direct

labour Total costs

B-12-008

$

2,500

$

13,500

$

16,000

K12-009

$

14,000

$

36,000

$

50,000

K12-011

$

71,800

$

85,100

$

156,900

Particulars L15-005 L15-006

Direct material (in $)

$

118,700

$

78,000

Direct labour (in $)

$

55,000

$

50,400

Machine hours/Direct labour cost 2500 800

Predetermined overhead rate (in $)

$

45

$

45

Overhead (in $)

$

113,014

$

36,164

Question 2

Manufacturing

overhead costs

Job numbers

Direct

material

Direct

labour Total costs

B-12-008

$

2,500

$

13,500

$

16,000

K12-009

$

14,000

$

36,000

$

50,000

K12-011

$

71,800

$

85,100

$

156,900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: JOB COSTING

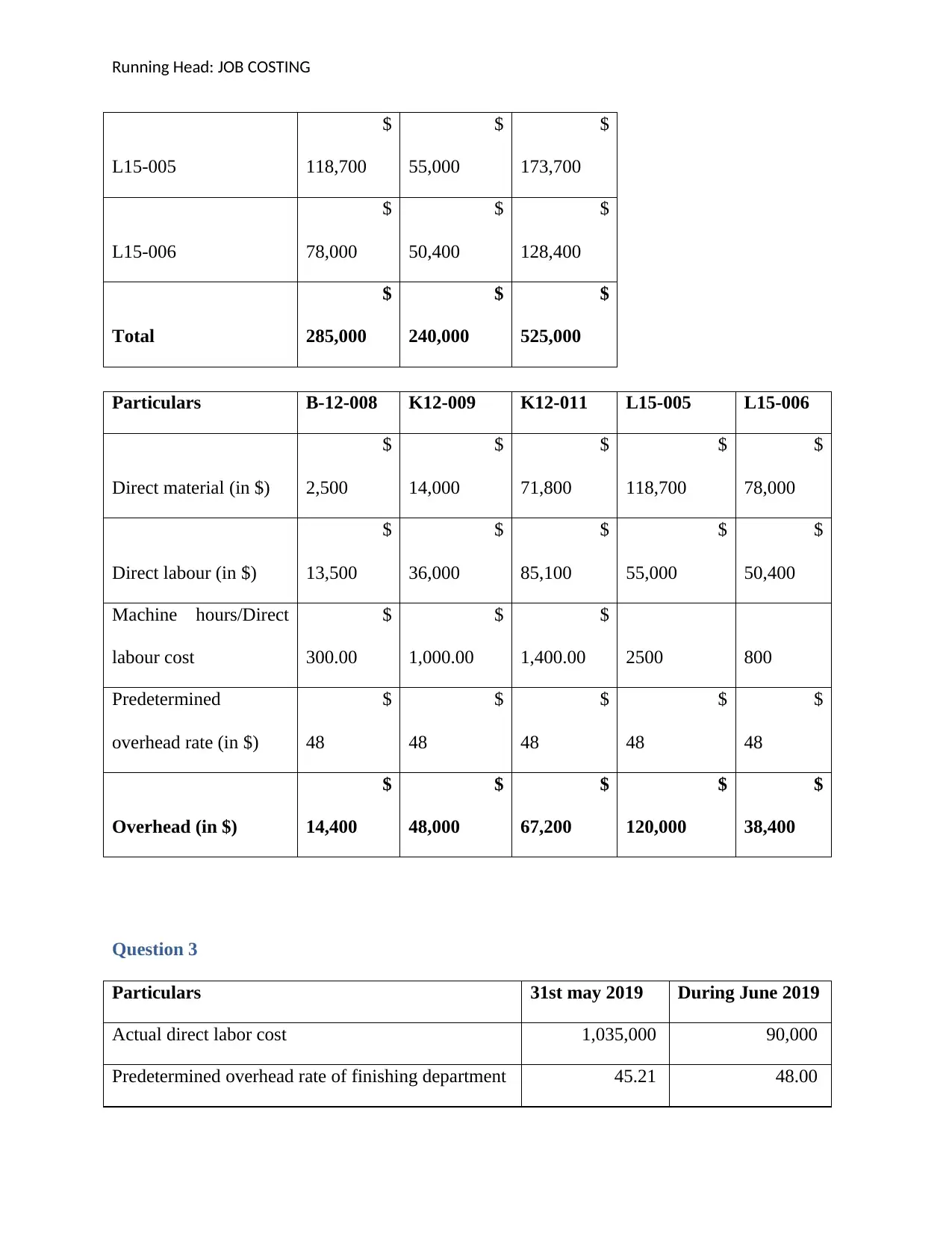

L15-005

$

118,700

$

55,000

$

173,700

L15-006

$

78,000

$

50,400

$

128,400

Total

$

285,000

$

240,000

$

525,000

Particulars B-12-008 K12-009 K12-011 L15-005 L15-006

Direct material (in $)

$

2,500

$

14,000

$

71,800

$

118,700

$

78,000

Direct labour (in $)

$

13,500

$

36,000

$

85,100

$

55,000

$

50,400

Machine hours/Direct

labour cost

$

300.00

$

1,000.00

$

1,400.00 2500 800

Predetermined

overhead rate (in $)

$

48

$

48

$

48

$

48

$

48

Overhead (in $)

$

14,400

$

48,000

$

67,200

$

120,000

$

38,400

Question 3

Particulars 31st may 2019 During June 2019

Actual direct labor cost 1,035,000 90,000

Predetermined overhead rate of finishing department 45.21 48.00

L15-005

$

118,700

$

55,000

$

173,700

L15-006

$

78,000

$

50,400

$

128,400

Total

$

285,000

$

240,000

$

525,000

Particulars B-12-008 K12-009 K12-011 L15-005 L15-006

Direct material (in $)

$

2,500

$

14,000

$

71,800

$

118,700

$

78,000

Direct labour (in $)

$

13,500

$

36,000

$

85,100

$

55,000

$

50,400

Machine hours/Direct

labour cost

$

300.00

$

1,000.00

$

1,400.00 2500 800

Predetermined

overhead rate (in $)

$

48

$

48

$

48

$

48

$

48

Overhead (in $)

$

14,400

$

48,000

$

67,200

$

120,000

$

38,400

Question 3

Particulars 31st may 2019 During June 2019

Actual direct labor cost 1,035,000 90,000

Predetermined overhead rate of finishing department 45.21 48.00

Running Head: JOB COSTING

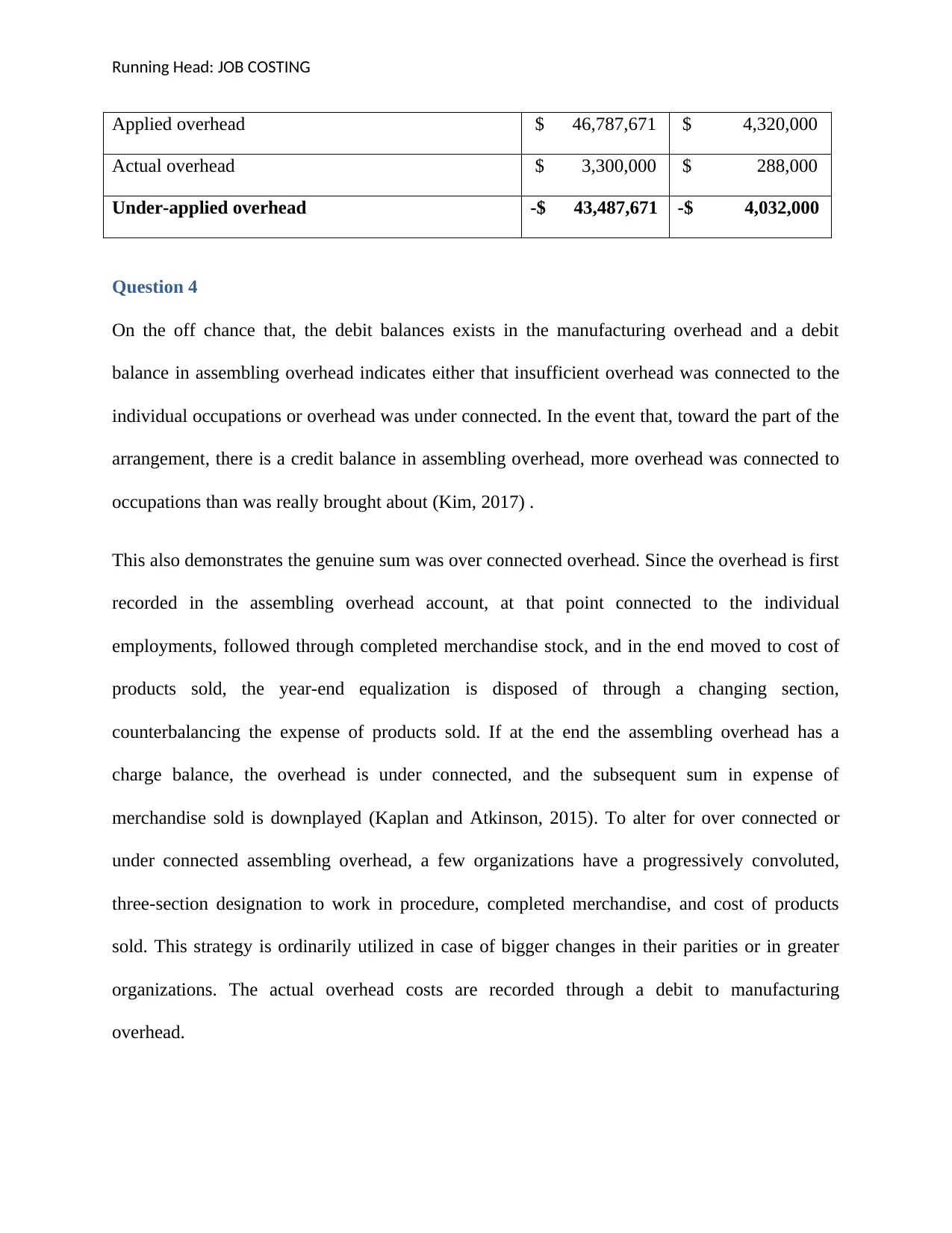

Applied overhead $ 46,787,671 $ 4,320,000

Actual overhead $ 3,300,000 $ 288,000

Under-applied overhead -$ 43,487,671 -$ 4,032,000

Question 4

On the off chance that, the debit balances exists in the manufacturing overhead and a debit

balance in assembling overhead indicates either that insufficient overhead was connected to the

individual occupations or overhead was under connected. In the event that, toward the part of the

arrangement, there is a credit balance in assembling overhead, more overhead was connected to

occupations than was really brought about (Kim, 2017) .

This also demonstrates the genuine sum was over connected overhead. Since the overhead is first

recorded in the assembling overhead account, at that point connected to the individual

employments, followed through completed merchandise stock, and in the end moved to cost of

products sold, the year-end equalization is disposed of through a changing section,

counterbalancing the expense of products sold. If at the end the assembling overhead has a

charge balance, the overhead is under connected, and the subsequent sum in expense of

merchandise sold is downplayed (Kaplan and Atkinson, 2015). To alter for over connected or

under connected assembling overhead, a few organizations have a progressively convoluted,

three-section designation to work in procedure, completed merchandise, and cost of products

sold. This strategy is ordinarily utilized in case of bigger changes in their parities or in greater

organizations. The actual overhead costs are recorded through a debit to manufacturing

overhead.

Applied overhead $ 46,787,671 $ 4,320,000

Actual overhead $ 3,300,000 $ 288,000

Under-applied overhead -$ 43,487,671 -$ 4,032,000

Question 4

On the off chance that, the debit balances exists in the manufacturing overhead and a debit

balance in assembling overhead indicates either that insufficient overhead was connected to the

individual occupations or overhead was under connected. In the event that, toward the part of the

arrangement, there is a credit balance in assembling overhead, more overhead was connected to

occupations than was really brought about (Kim, 2017) .

This also demonstrates the genuine sum was over connected overhead. Since the overhead is first

recorded in the assembling overhead account, at that point connected to the individual

employments, followed through completed merchandise stock, and in the end moved to cost of

products sold, the year-end equalization is disposed of through a changing section,

counterbalancing the expense of products sold. If at the end the assembling overhead has a

charge balance, the overhead is under connected, and the subsequent sum in expense of

merchandise sold is downplayed (Kaplan and Atkinson, 2015). To alter for over connected or

under connected assembling overhead, a few organizations have a progressively convoluted,

three-section designation to work in procedure, completed merchandise, and cost of products

sold. This strategy is ordinarily utilized in case of bigger changes in their parities or in greater

organizations. The actual overhead costs are recorded through a debit to manufacturing

overhead.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running Head: JOB COSTING

Question 5

Activity based costing is the method of costing that helps in the allocation of the costs on the

basis of the activity assigned to the particular items. Activity based costing is the procedure

where the expenses have been determined and apportioned based on the action key drivers. A

movement based costing technique perceives the connection between the expenses and the

results of the administrations just as producers and through this relationship the expenses of the

aberrant nature are doled out less self-assertively than the ordinary strategies (Childers and

Maggard-Gibbons, 2018).

In case of the traditional or the conventional system of recording the costs, which is subjected to

the volume include though in the action based costing, it orders the units delivered regarding the

bunch level movement, unit level action, association continuing action, client level action and

ultimately based on the item level action (Cooper, 2017).

As observed in many corporate manufacturing companies there are several measures by which

the activity based costing helps in improving the procedure of the costing. Such ways are

resolved in the total way.

First it extends the quantity of the pools by the movement; also it makes the elective

reason for the appointing the expenses of the overheads based on the machine hours or

the immediate expenses (Dale and Plunkett, 2017).

The change of the idea of the few backhanded costs helps the association in moving the

overhead costs from the results of the high volume to the low volume items.

Maybe a couple of different advantages that will help the association after the

establishment of the ABC costing is it makes a stage for the challenge, gives the cost

Question 5

Activity based costing is the method of costing that helps in the allocation of the costs on the

basis of the activity assigned to the particular items. Activity based costing is the procedure

where the expenses have been determined and apportioned based on the action key drivers. A

movement based costing technique perceives the connection between the expenses and the

results of the administrations just as producers and through this relationship the expenses of the

aberrant nature are doled out less self-assertively than the ordinary strategies (Childers and

Maggard-Gibbons, 2018).

In case of the traditional or the conventional system of recording the costs, which is subjected to

the volume include though in the action based costing, it orders the units delivered regarding the

bunch level movement, unit level action, association continuing action, client level action and

ultimately based on the item level action (Cooper, 2017).

As observed in many corporate manufacturing companies there are several measures by which

the activity based costing helps in improving the procedure of the costing. Such ways are

resolved in the total way.

First it extends the quantity of the pools by the movement; also it makes the elective

reason for the appointing the expenses of the overheads based on the machine hours or

the immediate expenses (Dale and Plunkett, 2017).

The change of the idea of the few backhanded costs helps the association in moving the

overhead costs from the results of the high volume to the low volume items.

Maybe a couple of different advantages that will help the association after the

establishment of the ABC costing is it makes a stage for the challenge, gives the cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running Head: JOB COSTING

sparing chances and aides in modifying the items. Henceforth, in general the action based

costing is profitable and beneficial (Dwivedi and Chakraborty, 2016).

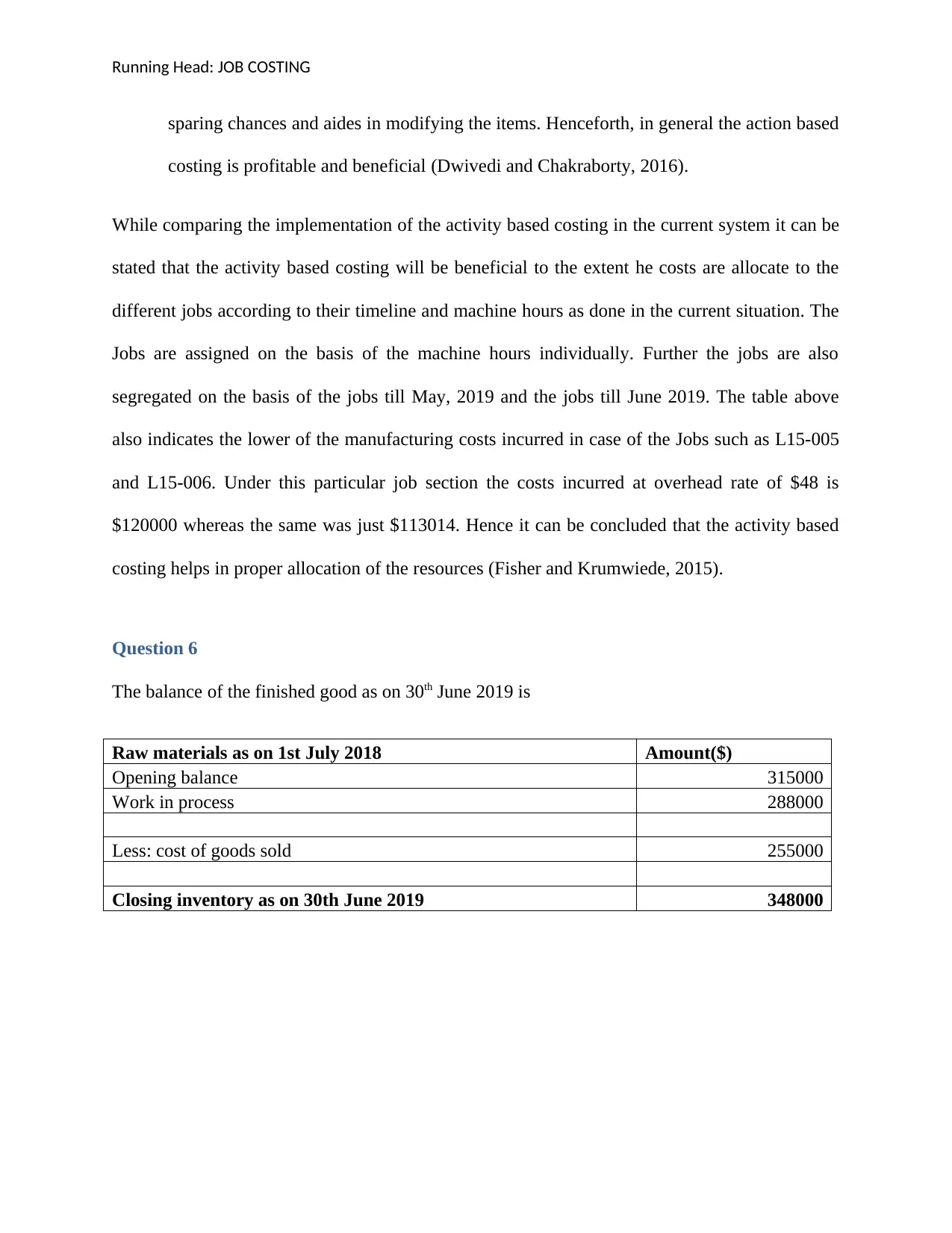

While comparing the implementation of the activity based costing in the current system it can be

stated that the activity based costing will be beneficial to the extent he costs are allocate to the

different jobs according to their timeline and machine hours as done in the current situation. The

Jobs are assigned on the basis of the machine hours individually. Further the jobs are also

segregated on the basis of the jobs till May, 2019 and the jobs till June 2019. The table above

also indicates the lower of the manufacturing costs incurred in case of the Jobs such as L15-005

and L15-006. Under this particular job section the costs incurred at overhead rate of $48 is

$120000 whereas the same was just $113014. Hence it can be concluded that the activity based

costing helps in proper allocation of the resources (Fisher and Krumwiede, 2015).

Question 6

The balance of the finished good as on 30th June 2019 is

Raw materials as on 1st July 2018 Amount($)

Opening balance 315000

Work in process 288000

Less: cost of goods sold 255000

Closing inventory as on 30th June 2019 348000

sparing chances and aides in modifying the items. Henceforth, in general the action based

costing is profitable and beneficial (Dwivedi and Chakraborty, 2016).

While comparing the implementation of the activity based costing in the current system it can be

stated that the activity based costing will be beneficial to the extent he costs are allocate to the

different jobs according to their timeline and machine hours as done in the current situation. The

Jobs are assigned on the basis of the machine hours individually. Further the jobs are also

segregated on the basis of the jobs till May, 2019 and the jobs till June 2019. The table above

also indicates the lower of the manufacturing costs incurred in case of the Jobs such as L15-005

and L15-006. Under this particular job section the costs incurred at overhead rate of $48 is

$120000 whereas the same was just $113014. Hence it can be concluded that the activity based

costing helps in proper allocation of the resources (Fisher and Krumwiede, 2015).

Question 6

The balance of the finished good as on 30th June 2019 is

Raw materials as on 1st July 2018 Amount($)

Opening balance 315000

Work in process 288000

Less: cost of goods sold 255000

Closing inventory as on 30th June 2019 348000

Running Head: JOB COSTING

References

Childers, C.P. and Maggard-Gibbons, M., 2018. Understanding costs of care in the operating

room. JAMA surgery, 153(4), pp.e176233-e176233.

Cooper, R., 2017. Target costing and value engineering. Routledge.

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Dwivedi, R. and Chakraborty, S., 2016. Adoption of an activity based costing model in an Indian

steel plant. Business: Theory and Practice, 17(4), pp.289-298.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kim, Y.W., 2017. Activity Based Costing for Construction Companies. John Wiley & Sons.

Zahller, K.A., 2017. Truffle in paradise: Job costing for a small business. Journal of Accounting

Education, 40, pp.32-42.

References

Childers, C.P. and Maggard-Gibbons, M., 2018. Understanding costs of care in the operating

room. JAMA surgery, 153(4), pp.e176233-e176233.

Cooper, R., 2017. Target costing and value engineering. Routledge.

Dale, B.G. and Plunkett, J.J., 2017. Quality costing. Routledge.

Dwivedi, R. and Chakraborty, S., 2016. Adoption of an activity based costing model in an Indian

steel plant. Business: Theory and Practice, 17(4), pp.289-298.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kim, Y.W., 2017. Activity Based Costing for Construction Companies. John Wiley & Sons.

Zahller, K.A., 2017. Truffle in paradise: Job costing for a small business. Journal of Accounting

Education, 40, pp.32-42.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.