Financial Analysis: Capital Budgeting Decision for KKP Ltd. Project

VerifiedAdded on 2023/06/08

|13

|1840

|487

Report

AI Summary

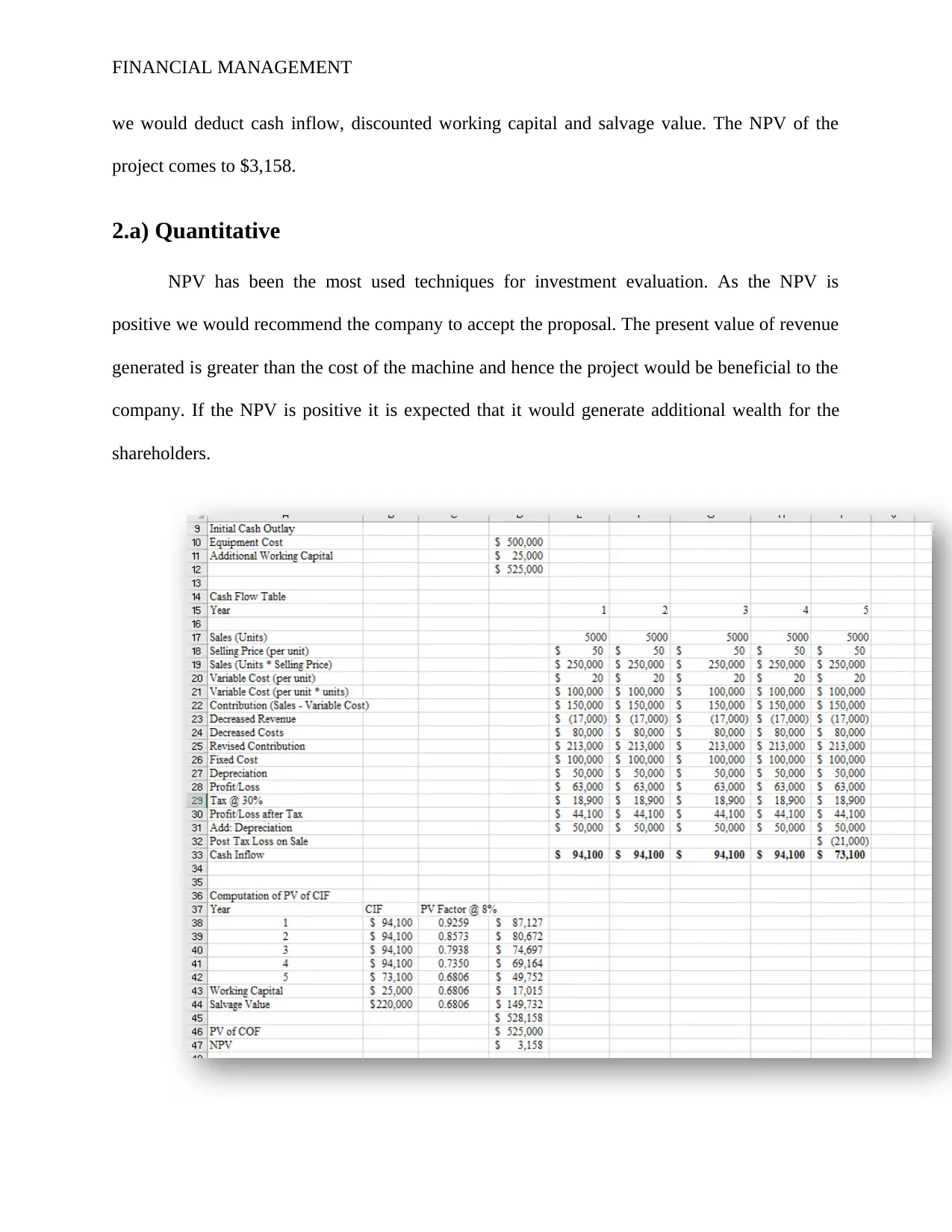

This report provides a financial analysis of KKP Ltd's potential investment in proximity sensors for the food industry, utilizing capital budgeting techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), and payback period. The analysis considers initial cash outflows, depreciation, revenue, variable costs, fixed costs, and salvage value to determine the project's feasibility. Quantitative findings reveal a positive NPV and an IRR exceeding the required rate of return, suggesting the project's viability. Qualitative factors such as competitive advantage, company culture, product quality, environmental concerns, and ethical considerations are also evaluated to provide a holistic recommendation for KKP Ltd to proceed with the investment, supported by the potential for wealth generation and synergy. Desklib offers a range of study tools and solved assignments for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.