Corporate Finance Report: Investment Appraisal of ClearView Drug

VerifiedAdded on 2023/06/09

|7

|1439

|131

Report

AI Summary

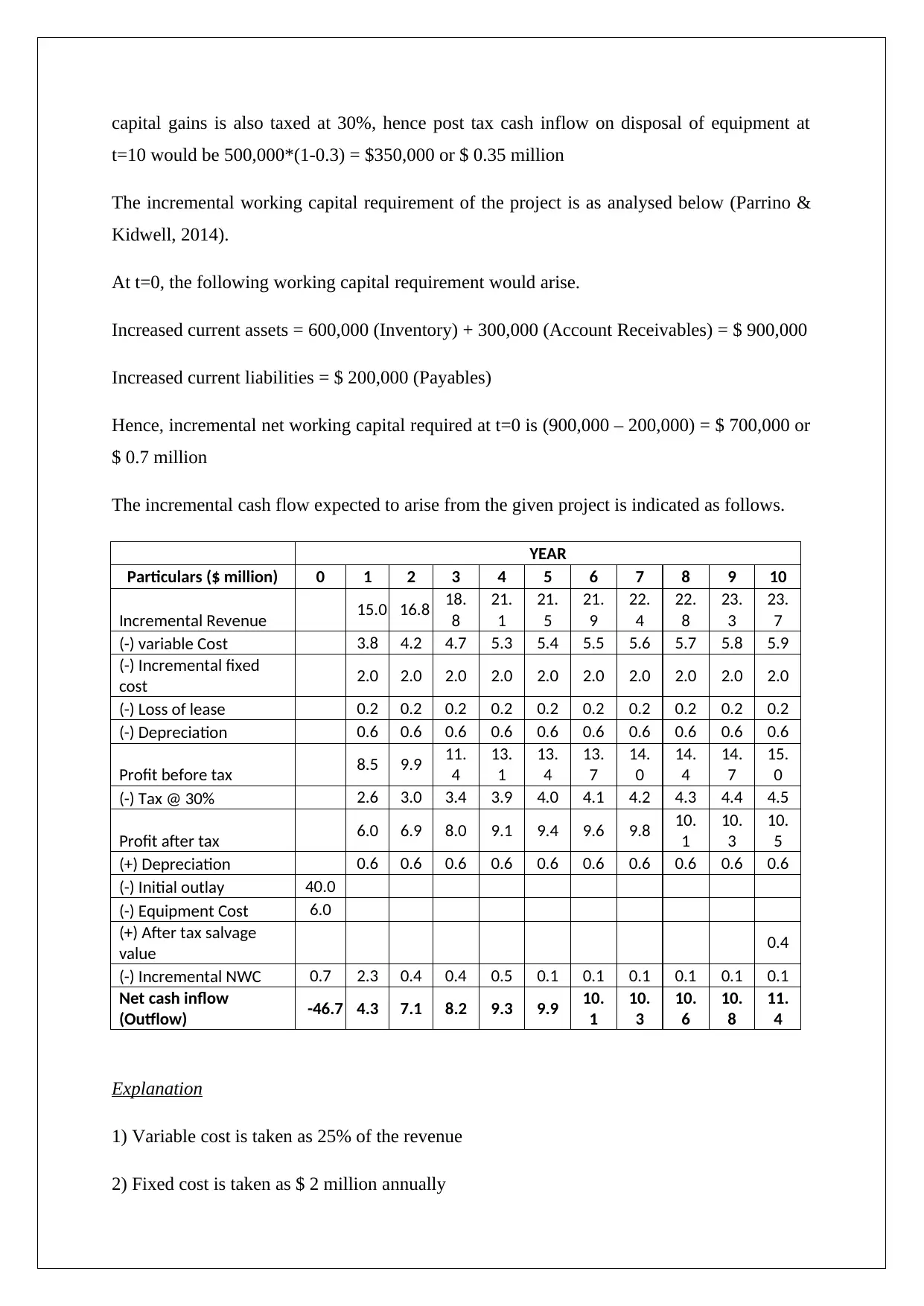

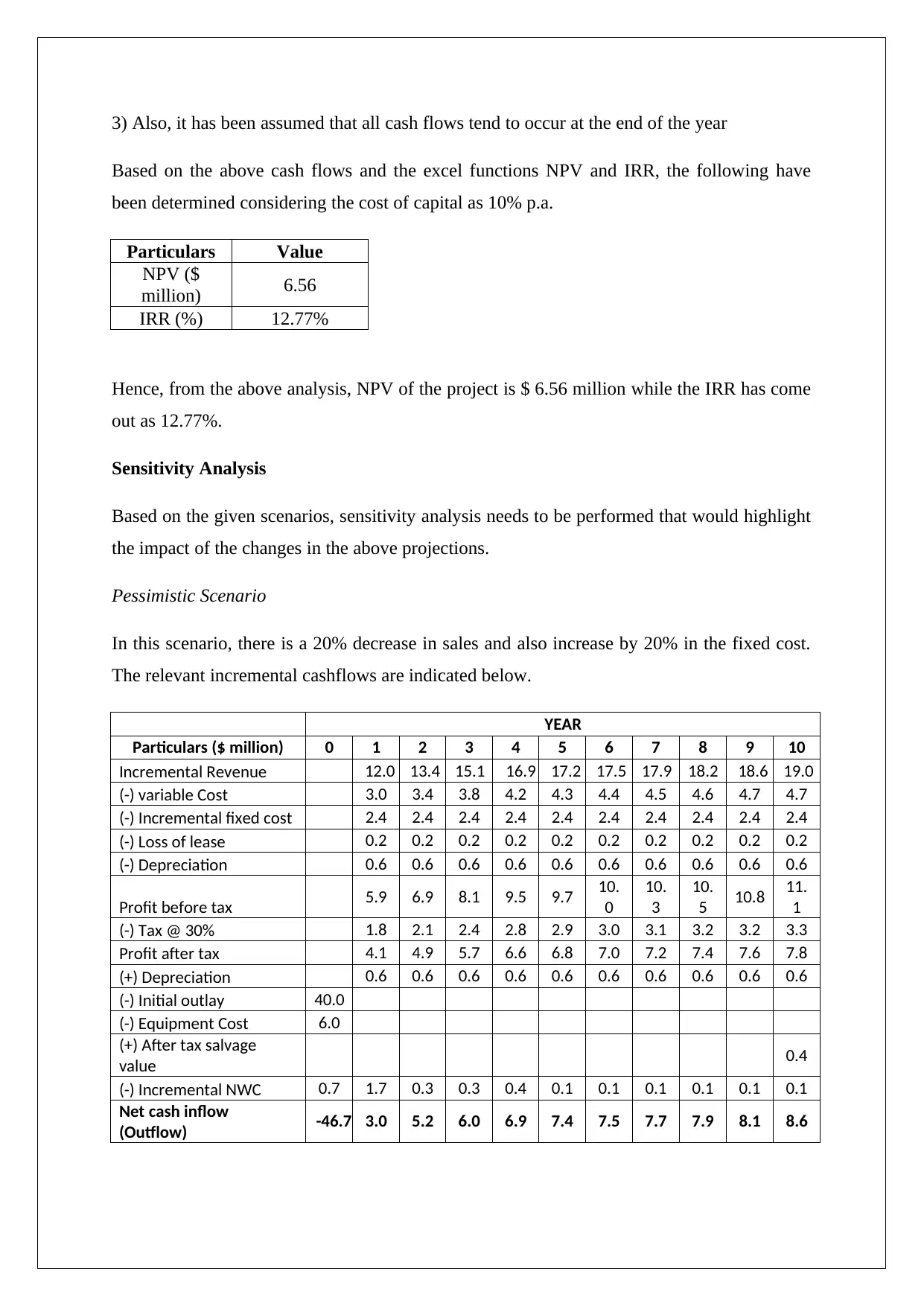

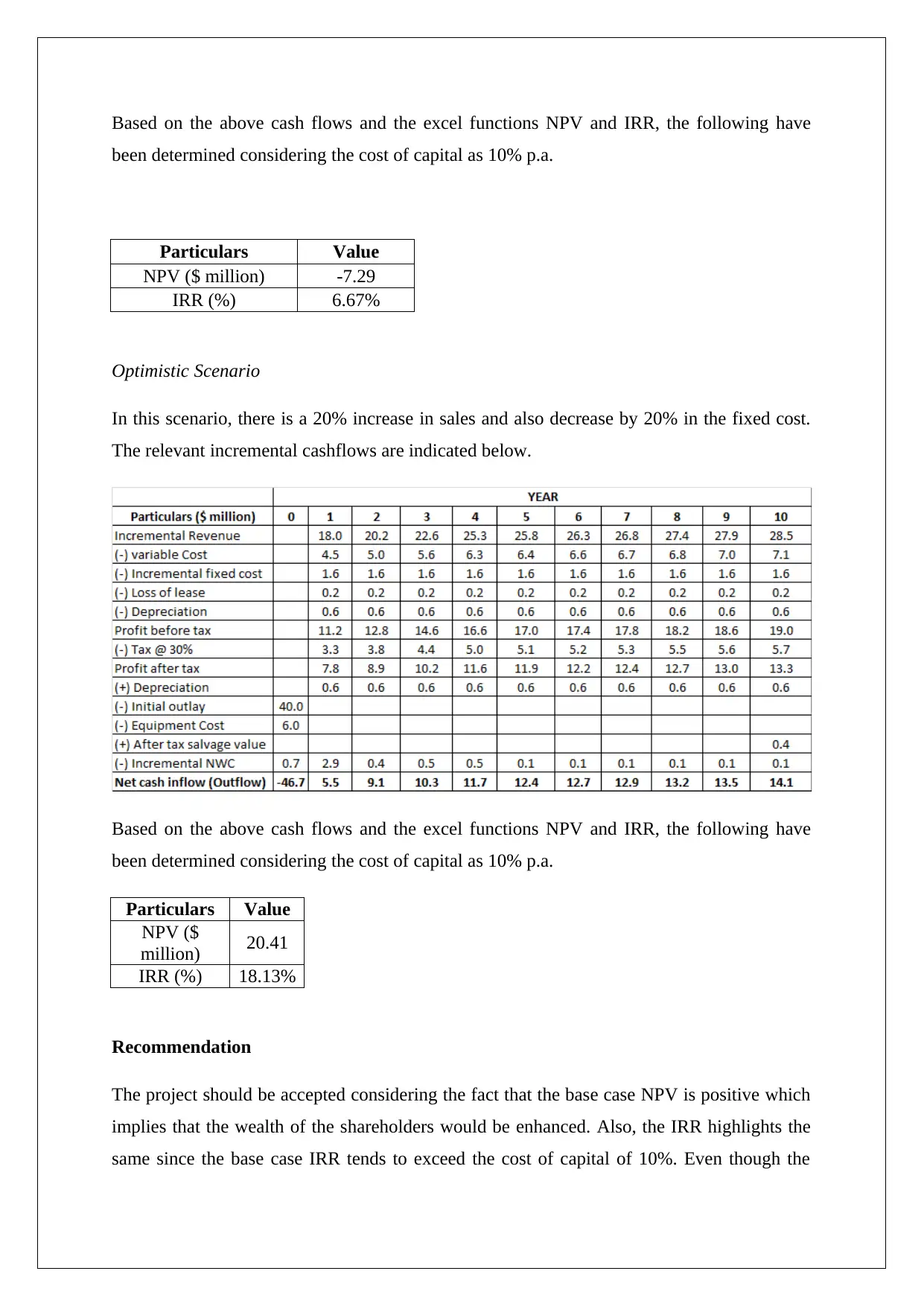

This report assesses Kline Pharmaceuticals' potential investment in a new myopia drug, ClearView, using capital budgeting techniques such as NPV and IRR. The analysis considers the initial outlay, including equipment costs and working capital requirements, along with incremental revenues, variable and fixed costs, and depreciation. A base-case scenario, along with pessimistic and optimistic scenarios, are analyzed through sensitivity analysis. The base case NPV is positive at $6.56 million with an IRR of 12.77%, suggesting the project is viable. The pessimistic scenario shows a negative NPV, while the optimistic scenario shows a higher positive NPV. The report concludes with a recommendation to accept the project based on the positive base-case NPV, indicating enhanced shareholder wealth. Desklib provides access to similar solved assignments and past papers for students.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.