Audit Planning Report: BAO3306 Assignment for Kneomedia Limited Audit

VerifiedAdded on 2022/10/06

|9

|3357

|16

Report

AI Summary

This report provides an executive summary and detailed analysis of the audit planning process for Kneomedia Limited, adhering to Australian Auditing Standards. The report focuses on the initial steps required when auditing a company for the first time, emphasizing the auditor's responsibility in expressing an opinion on the financial statements' true and fair view to stakeholders. It highlights the importance of effective audit planning, including gaining an understanding of the client, identifying significant accounts at risk of material misstatement, and setting the planning materiality level. The report analyzes the impact of various auditing standards, such as ASA 210, ASA 220, ASA 230, and ASA 250, on the audit planning process. It identifies and discusses five significant accounts from Kneomedia Limited's 2018 annual report that are at risk of material misstatement, providing explanations for the identified risks. The analysis includes a focus on revenue, cash and cash equivalents, finance costs, and share-based payment expenses, demonstrating the application of auditing standards in practice. The report concludes by summarizing the key aspects of audit planning and its importance in ensuring reliable and transparent audit processes.

AUDITING

ASSIGNMENT

BAO3306

1

ASSIGNMENT

BAO3306

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY:

This paper has been analysed in lines with Auditing Standards prevailing in Australia issued by the

respective board so as to have uniformity and quality in the process of Audit. The major focus of

the paper is the steps and the aspects required to be analysed while planning the audit of an entity

for the first time. The auditors are responsible for stating the opinion on the true and fair view of the

financial statements being prepared by the management so that the stakeholders can use the same

with confidence for taking decisions in respect of the entity concerned. Furthermore, Auditors are

require to disclose even the matters that they think are at risk in their report. All this helps the

auditors to frame effective Audit Planning that will help in having them in having the sampling to

be more reliable and transparent. The standards have been analysed taking the company Kneomedia

Limited’s last year annual reports in account. The paper discusses impact of the various auditing

standards on the process of Audit Planning which are required to be considered by the Auditors

during the process of audit to make it more reliable and acceptable.

2

This paper has been analysed in lines with Auditing Standards prevailing in Australia issued by the

respective board so as to have uniformity and quality in the process of Audit. The major focus of

the paper is the steps and the aspects required to be analysed while planning the audit of an entity

for the first time. The auditors are responsible for stating the opinion on the true and fair view of the

financial statements being prepared by the management so that the stakeholders can use the same

with confidence for taking decisions in respect of the entity concerned. Furthermore, Auditors are

require to disclose even the matters that they think are at risk in their report. All this helps the

auditors to frame effective Audit Planning that will help in having them in having the sampling to

be more reliable and transparent. The standards have been analysed taking the company Kneomedia

Limited’s last year annual reports in account. The paper discusses impact of the various auditing

standards on the process of Audit Planning which are required to be considered by the Auditors

during the process of audit to make it more reliable and acceptable.

2

Table of Contents

EXECUTIVE SUMMARY:.....................................................................................................................................2

INTRODUCTION................................................................................................................................................4

KEY INFORMATION...........................................................................................................................................4

a) GAIN AN UNDERSTANDING OF THE CLIENT..........................................................................................5

b) IDENTIFYING SIGNIFICANT ACCOUNTS MOST AT RISK OF BEING MATERIALLY MISSTATED:................6

c) SET PLANNING MATERIALITY LEVEL:.....................................................................................................7

d) IDENTIFICATION OF THE AUDIT RISK ASSESSMENT OF THE SELECTED FIVE ACCOUNTS:......................7

CONCLUSION:...................................................................................................................................................8

REFERENCES:....................................................................................................................................................9

3

EXECUTIVE SUMMARY:.....................................................................................................................................2

INTRODUCTION................................................................................................................................................4

KEY INFORMATION...........................................................................................................................................4

a) GAIN AN UNDERSTANDING OF THE CLIENT..........................................................................................5

b) IDENTIFYING SIGNIFICANT ACCOUNTS MOST AT RISK OF BEING MATERIALLY MISSTATED:................6

c) SET PLANNING MATERIALITY LEVEL:.....................................................................................................7

d) IDENTIFICATION OF THE AUDIT RISK ASSESSMENT OF THE SELECTED FIVE ACCOUNTS:......................7

CONCLUSION:...................................................................................................................................................8

REFERENCES:....................................................................................................................................................9

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Auditing is a very vital process which involves examination of the books of accounts prepared by

the management and expression of opinion on the true and fair view of the books by the auditor.

Therefore, Auditors plays a very crucial role in the financial world as because their opinion on the

genuineness of the books of the companies acts as a reference and decision making documents for

the stakeholders (Best, 2001). Therefore, there is a need for independence of the auditor and it is

expected from the auditor that he will conduct the audit efficiently. Further, accepting audit of new

client requires enhanced control procedures by the Auditors that includes the following aspects:

• Asking the right questions: The auditor is required to ask the right questions with respect to

the business of the client. This is the first step which helps in creating a relationship.

• Selectivity: The auditor is required to select the audit crucially. They are needed to analyse

the ethical movements of the clients.

• Performing Due Diligence: The auditors should perform due diligence on the prospective

client’s i.e. reasonable steps shall be taken by the auditor to avoid any fraud or misrepresentation.

Once the auditor has assessed the above mentioned parameters he is required to plan his audit

procedure. The planning of audit in a specific way and under a specific guideline while conducting

an audit is called as Audit Planning. Audit planning helps the auditor in the following ways:

• Evidences can be obtained that are sufficient

• Audit costs can be reduced by way of effective planning

• Misunderstanding with the client can be avoided.

In case of Kneomedia Limited., the firm are being approached by the management of the company

for the financial audit. Since the audit is being conducted for the first time by the firm, the firm shall

crucially examine and follow the standard process before taking up the Audit. The firm is required

to ask question from the key personnel of the company. The questions should be such that helps in

building a relationship in between firm and the key management personnel of the company. The

firm shall then select the key areas that requires special attention and is required to perform due

diligence on the clients business. The firm is also required to plan its audit effectively so as to

minimise the time and the cost of audit.

KEY INFORMATION

There is requirement on part of the external auditor to collect and gather all the key information in

relation to the entity whose audit would be conducted by them so that they can make policies for

their Audit effectively. Appropriate Audit Planning helps the firm to get the audit done smoothly.

The key information required to be gathered by the Auditor prior to the start of audit includes

gathering of information so as to have understanding of the entity whose audit will be conducted.

Furthermore, the auditors sets the materiality level and identifies accounts that have a risk of

material misstatement. All this helps in making the process of Audit smooth and reduces the risks of

ignorance of material misstatement (Simnett, 2016). Along with the identification of the accounts

that are at risk of material misstatement they should state the risk assessment of the accounts

selected.

The Key Information have been discussed herewith below.

4

Auditing is a very vital process which involves examination of the books of accounts prepared by

the management and expression of opinion on the true and fair view of the books by the auditor.

Therefore, Auditors plays a very crucial role in the financial world as because their opinion on the

genuineness of the books of the companies acts as a reference and decision making documents for

the stakeholders (Best, 2001). Therefore, there is a need for independence of the auditor and it is

expected from the auditor that he will conduct the audit efficiently. Further, accepting audit of new

client requires enhanced control procedures by the Auditors that includes the following aspects:

• Asking the right questions: The auditor is required to ask the right questions with respect to

the business of the client. This is the first step which helps in creating a relationship.

• Selectivity: The auditor is required to select the audit crucially. They are needed to analyse

the ethical movements of the clients.

• Performing Due Diligence: The auditors should perform due diligence on the prospective

client’s i.e. reasonable steps shall be taken by the auditor to avoid any fraud or misrepresentation.

Once the auditor has assessed the above mentioned parameters he is required to plan his audit

procedure. The planning of audit in a specific way and under a specific guideline while conducting

an audit is called as Audit Planning. Audit planning helps the auditor in the following ways:

• Evidences can be obtained that are sufficient

• Audit costs can be reduced by way of effective planning

• Misunderstanding with the client can be avoided.

In case of Kneomedia Limited., the firm are being approached by the management of the company

for the financial audit. Since the audit is being conducted for the first time by the firm, the firm shall

crucially examine and follow the standard process before taking up the Audit. The firm is required

to ask question from the key personnel of the company. The questions should be such that helps in

building a relationship in between firm and the key management personnel of the company. The

firm shall then select the key areas that requires special attention and is required to perform due

diligence on the clients business. The firm is also required to plan its audit effectively so as to

minimise the time and the cost of audit.

KEY INFORMATION

There is requirement on part of the external auditor to collect and gather all the key information in

relation to the entity whose audit would be conducted by them so that they can make policies for

their Audit effectively. Appropriate Audit Planning helps the firm to get the audit done smoothly.

The key information required to be gathered by the Auditor prior to the start of audit includes

gathering of information so as to have understanding of the entity whose audit will be conducted.

Furthermore, the auditors sets the materiality level and identifies accounts that have a risk of

material misstatement. All this helps in making the process of Audit smooth and reduces the risks of

ignorance of material misstatement (Simnett, 2016). Along with the identification of the accounts

that are at risk of material misstatement they should state the risk assessment of the accounts

selected.

The Key Information have been discussed herewith below.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

a) GAIN AN UNDERSTANDING OF THE CLIENT

The company Kneomedia Limited is a company which is into the business of publishing of online

games. The company is into the core business of development of edutainment games i.e. the games

that contains education as well as entertainment. These games are published by the company

through its entity which is based in United States namely, Kneoworld Inc. The company is a public

company which is listed under the Australian Stock Exchange (ASX) as KNM. The industry in

which the company operates is broadly known as “Interactive Home Entertainment”. The company

believes in the policy of expansion of its operations so as to have a broaden opportunities in various

countries where it have its presence and specifically the United States of America.

The country have geographical presence at various places specifically in the developed countries

and have its headquarters at Australia. This company was founded in the year 1987. The last audited

financials of the company contains the financial movements of the company that happened during

the year and thus analysing the same would help the auditors in selecting the areas that requires

detailed analysis for the purpose of Audit. The company have taken programmes so as to broad its

markets in the various countries so as to have transformation in the earnings of the same. The same

is being attained by it by offering advanced products i.e. Software as a Service (SaaS). From the

perspective of an Auditor as required under the Auditing Standard ASA 210 which states that the

auditor needs to ensure the means that has been used by the management of the company

were appropriate. ASA 210 is applicable on all the audits that are being conducted under the

Corporations Act, 2001 and Audits conducted for any other purposes (Power, 2003). This standard

came into force on 1st January 2010. This standard requires the Auditor to agree its terms of audit

and any preconditions of the audit with the management of the company or any other person who

possess the responsibility of corporate governance. Complying with ASA 201 will help the auditor

of Kneomedia Limited to have its preconditions of audit being established along with having a

common understanding between the company’s management and them.

Auditors needs to have application of Quality Control while conducting audit, having proper

documentation of the same for the purpose of audit, considering the provisions of laws along with

having a concrete plan for Auditing. All these aspects are governed by Auditing Standards that

governs these areas. ASA 220 identifies the requirement of having Quality Control of audits along

with analysis of the financial information. As per this standard there are responsibilities in specific

being outlined on part of the Auditor regarding procedures being undertaken for maintenance of

control during conduct of Audit. ASA 230 deals in relation with Documentation that has to be

maintained and collected by Auditor during course of Audit. The Auditors should have

documents properly collected and kept while conducting of the financial reports. The objective of

maintaining and keeping documents is to have proper record which acts as the basis of the report of

audit and also it helps in providing evidence that the audit performed was in accordance with

standards of auditing prevailing as per Australian Law. The audit performed should have record of

the procedures being adopted by the auditors in order to ensure the audit being conducted in true

and fair. The auditor should consider the laws and regulations while conducting audit of a financial

report as required by the ASA 250 (Porter, 1993). As per this standard, it is required on part of the

auditor to have proper understanding of all the relevant laws applicable on the entity and on the

industry in which the entity operates thereby having the conduct of audit to be more proper.

5

The company Kneomedia Limited is a company which is into the business of publishing of online

games. The company is into the core business of development of edutainment games i.e. the games

that contains education as well as entertainment. These games are published by the company

through its entity which is based in United States namely, Kneoworld Inc. The company is a public

company which is listed under the Australian Stock Exchange (ASX) as KNM. The industry in

which the company operates is broadly known as “Interactive Home Entertainment”. The company

believes in the policy of expansion of its operations so as to have a broaden opportunities in various

countries where it have its presence and specifically the United States of America.

The country have geographical presence at various places specifically in the developed countries

and have its headquarters at Australia. This company was founded in the year 1987. The last audited

financials of the company contains the financial movements of the company that happened during

the year and thus analysing the same would help the auditors in selecting the areas that requires

detailed analysis for the purpose of Audit. The company have taken programmes so as to broad its

markets in the various countries so as to have transformation in the earnings of the same. The same

is being attained by it by offering advanced products i.e. Software as a Service (SaaS). From the

perspective of an Auditor as required under the Auditing Standard ASA 210 which states that the

auditor needs to ensure the means that has been used by the management of the company

were appropriate. ASA 210 is applicable on all the audits that are being conducted under the

Corporations Act, 2001 and Audits conducted for any other purposes (Power, 2003). This standard

came into force on 1st January 2010. This standard requires the Auditor to agree its terms of audit

and any preconditions of the audit with the management of the company or any other person who

possess the responsibility of corporate governance. Complying with ASA 201 will help the auditor

of Kneomedia Limited to have its preconditions of audit being established along with having a

common understanding between the company’s management and them.

Auditors needs to have application of Quality Control while conducting audit, having proper

documentation of the same for the purpose of audit, considering the provisions of laws along with

having a concrete plan for Auditing. All these aspects are governed by Auditing Standards that

governs these areas. ASA 220 identifies the requirement of having Quality Control of audits along

with analysis of the financial information. As per this standard there are responsibilities in specific

being outlined on part of the Auditor regarding procedures being undertaken for maintenance of

control during conduct of Audit. ASA 230 deals in relation with Documentation that has to be

maintained and collected by Auditor during course of Audit. The Auditors should have

documents properly collected and kept while conducting of the financial reports. The objective of

maintaining and keeping documents is to have proper record which acts as the basis of the report of

audit and also it helps in providing evidence that the audit performed was in accordance with

standards of auditing prevailing as per Australian Law. The audit performed should have record of

the procedures being adopted by the auditors in order to ensure the audit being conducted in true

and fair. The auditor should consider the laws and regulations while conducting audit of a financial

report as required by the ASA 250 (Porter, 1993). As per this standard, it is required on part of the

auditor to have proper understanding of all the relevant laws applicable on the entity and on the

industry in which the entity operates thereby having the conduct of audit to be more proper.

5

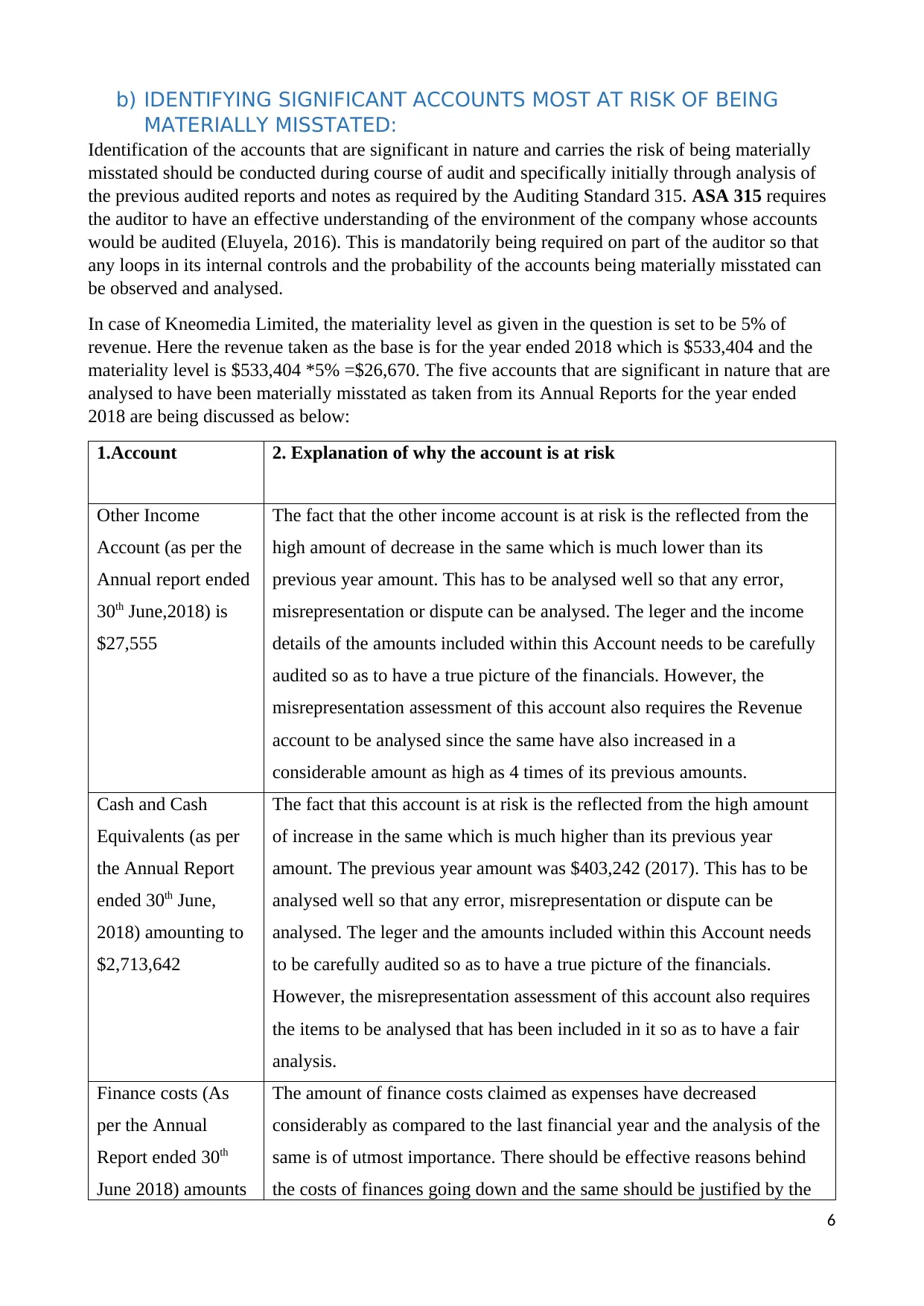

b) IDENTIFYING SIGNIFICANT ACCOUNTS MOST AT RISK OF BEING

MATERIALLY MISSTATED:

Identification of the accounts that are significant in nature and carries the risk of being materially

misstated should be conducted during course of audit and specifically initially through analysis of

the previous audited reports and notes as required by the Auditing Standard 315. ASA 315 requires

the auditor to have an effective understanding of the environment of the company whose accounts

would be audited (Eluyela, 2016). This is mandatorily being required on part of the auditor so that

any loops in its internal controls and the probability of the accounts being materially misstated can

be observed and analysed.

In case of Kneomedia Limited, the materiality level as given in the question is set to be 5% of

revenue. Here the revenue taken as the base is for the year ended 2018 which is $533,404 and the

materiality level is $533,404 *5% =$26,670. The five accounts that are significant in nature that are

analysed to have been materially misstated as taken from its Annual Reports for the year ended

2018 are being discussed as below:

1.Account 2. Explanation of why the account is at risk

Other Income

Account (as per the

Annual report ended

30th June,2018) is

$27,555

The fact that the other income account is at risk is the reflected from the

high amount of decrease in the same which is much lower than its

previous year amount. This has to be analysed well so that any error,

misrepresentation or dispute can be analysed. The leger and the income

details of the amounts included within this Account needs to be carefully

audited so as to have a true picture of the financials. However, the

misrepresentation assessment of this account also requires the Revenue

account to be analysed since the same have also increased in a

considerable amount as high as 4 times of its previous amounts.

Cash and Cash

Equivalents (as per

the Annual Report

ended 30th June,

2018) amounting to

$2,713,642

The fact that this account is at risk is the reflected from the high amount

of increase in the same which is much higher than its previous year

amount. The previous year amount was $403,242 (2017). This has to be

analysed well so that any error, misrepresentation or dispute can be

analysed. The leger and the amounts included within this Account needs

to be carefully audited so as to have a true picture of the financials.

However, the misrepresentation assessment of this account also requires

the items to be analysed that has been included in it so as to have a fair

analysis.

Finance costs (As

per the Annual

Report ended 30th

June 2018) amounts

The amount of finance costs claimed as expenses have decreased

considerably as compared to the last financial year and the analysis of the

same is of utmost importance. There should be effective reasons behind

the costs of finances going down and the same should be justified by the

6

MATERIALLY MISSTATED:

Identification of the accounts that are significant in nature and carries the risk of being materially

misstated should be conducted during course of audit and specifically initially through analysis of

the previous audited reports and notes as required by the Auditing Standard 315. ASA 315 requires

the auditor to have an effective understanding of the environment of the company whose accounts

would be audited (Eluyela, 2016). This is mandatorily being required on part of the auditor so that

any loops in its internal controls and the probability of the accounts being materially misstated can

be observed and analysed.

In case of Kneomedia Limited, the materiality level as given in the question is set to be 5% of

revenue. Here the revenue taken as the base is for the year ended 2018 which is $533,404 and the

materiality level is $533,404 *5% =$26,670. The five accounts that are significant in nature that are

analysed to have been materially misstated as taken from its Annual Reports for the year ended

2018 are being discussed as below:

1.Account 2. Explanation of why the account is at risk

Other Income

Account (as per the

Annual report ended

30th June,2018) is

$27,555

The fact that the other income account is at risk is the reflected from the

high amount of decrease in the same which is much lower than its

previous year amount. This has to be analysed well so that any error,

misrepresentation or dispute can be analysed. The leger and the income

details of the amounts included within this Account needs to be carefully

audited so as to have a true picture of the financials. However, the

misrepresentation assessment of this account also requires the Revenue

account to be analysed since the same have also increased in a

considerable amount as high as 4 times of its previous amounts.

Cash and Cash

Equivalents (as per

the Annual Report

ended 30th June,

2018) amounting to

$2,713,642

The fact that this account is at risk is the reflected from the high amount

of increase in the same which is much higher than its previous year

amount. The previous year amount was $403,242 (2017). This has to be

analysed well so that any error, misrepresentation or dispute can be

analysed. The leger and the amounts included within this Account needs

to be carefully audited so as to have a true picture of the financials.

However, the misrepresentation assessment of this account also requires

the items to be analysed that has been included in it so as to have a fair

analysis.

Finance costs (As

per the Annual

Report ended 30th

June 2018) amounts

The amount of finance costs claimed as expenses have decreased

considerably as compared to the last financial year and the analysis of the

same is of utmost importance. There should be effective reasons behind

the costs of finances going down and the same should be justified by the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to $18,271 management to the auditors so that the current year analysis can be done.

Share based

payments expenses

(As per the annual

Report for the period

ended 30th June

2018) amounting to

$660,833

The amount of share based payments expenses claimed as expenses is a

new expense being incurred in the current year which was absent in the

previous year.

Trade and other

payables (as on 30th

June 2018) amounts

to $313,087

There has been increase in the cash equivalents but the trade payables

have considerably decreased as compared to the last year requiring an

detailed analysis with proper justifications from the management.

Thus, the accounts identified above are the significant accounts having risks that they are misstated

by the management of the company and the people responsible for it governance.

c) SET PLANNING MATERIALITY LEVEL:

The audit process requires the auditors to set the materiality level while conducting and planning its

audit process. Materiality level is of utmost importance and cannot be same for the different

countries. It depends on many factors and ASA 320 outlines the provisions with respect to

auditors for setting materiality level in planning and while performing the audit process.

Setting up the materiality level helps the auditor to reduce the probability of incorrect and

misstatements in the financial statements (Firth, 1979). The level of materiality is set by the auditor

during the planning stage so that the risks of material misstatement can be determined. This can be

revised as necessary by the auditor during course of audit time. The materiality level are set using

the combination of both qualitative and quantitative methods. This is the tolerable misstatement

limits being set in terms of the financial statements. This concept to some extent is similar to the

materiality concept being used during the preparation of financial statements as per accounting

standards.

In the given case, as mentioned in the problem specifically, the materiality level has been set to 5%

of Sales Revenue which in the given case is Sales Revenue of 2018 * 5% i.e. $533,404 *5%

=$26,670.

d) IDENTIFICATION OF THE AUDIT RISK ASSESSMENT OF THE

SELECTED FIVE ACCOUNTS:

The Auditors as required under the ASA 330 should response to risks assessed by them during

the course of audit. This is done by the auditor so as to address the risks being assessed, to design

and perform any further procedures of audit, test controls to be kept in place, adapting substantive

procedures, assessing the overall financial statements and documentation in relation to the same

(Jennings, 1987). The audit risk assessment of the selected accounts are as follows:

7

Share based

payments expenses

(As per the annual

Report for the period

ended 30th June

2018) amounting to

$660,833

The amount of share based payments expenses claimed as expenses is a

new expense being incurred in the current year which was absent in the

previous year.

Trade and other

payables (as on 30th

June 2018) amounts

to $313,087

There has been increase in the cash equivalents but the trade payables

have considerably decreased as compared to the last year requiring an

detailed analysis with proper justifications from the management.

Thus, the accounts identified above are the significant accounts having risks that they are misstated

by the management of the company and the people responsible for it governance.

c) SET PLANNING MATERIALITY LEVEL:

The audit process requires the auditors to set the materiality level while conducting and planning its

audit process. Materiality level is of utmost importance and cannot be same for the different

countries. It depends on many factors and ASA 320 outlines the provisions with respect to

auditors for setting materiality level in planning and while performing the audit process.

Setting up the materiality level helps the auditor to reduce the probability of incorrect and

misstatements in the financial statements (Firth, 1979). The level of materiality is set by the auditor

during the planning stage so that the risks of material misstatement can be determined. This can be

revised as necessary by the auditor during course of audit time. The materiality level are set using

the combination of both qualitative and quantitative methods. This is the tolerable misstatement

limits being set in terms of the financial statements. This concept to some extent is similar to the

materiality concept being used during the preparation of financial statements as per accounting

standards.

In the given case, as mentioned in the problem specifically, the materiality level has been set to 5%

of Sales Revenue which in the given case is Sales Revenue of 2018 * 5% i.e. $533,404 *5%

=$26,670.

d) IDENTIFICATION OF THE AUDIT RISK ASSESSMENT OF THE

SELECTED FIVE ACCOUNTS:

The Auditors as required under the ASA 330 should response to risks assessed by them during

the course of audit. This is done by the auditor so as to address the risks being assessed, to design

and perform any further procedures of audit, test controls to be kept in place, adapting substantive

procedures, assessing the overall financial statements and documentation in relation to the same

(Jennings, 1987). The audit risk assessment of the selected accounts are as follows:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other Revenue: There has been considerable decrease in the amount of the other revenue

along with the increase in the Sales Revenue. This account possess the risk of omission and

the risk of wrong ledgers entry being involved.

Cash and Cash Equivalents: This has increased and requires to be analysed so as to see

any commission entries are not included within it.

Finance Costs: Reduction in the finance costs should be analysed so as to have

understanding of whether the finances have been repaid and their sources.

Share Based Payment Expenses: This has been appeared and needs to be analysed

effectively.

Trade and other Payables: Although there have been increase in the expenses and overall

decrease in the revenue but the trade payables have reduced considerably and requires

analysis.

Thus, the objective of identifying the material misstatement is to obtain sufficient evidences

regarding its assessment and analysing the extent of its being misstated through designing of

responses and implementation of the same. It is the duty and responsibility on part of the Auditor to

have designing and implementation of the responses for addressing the risks of material

misstatement. This is done by the Auditor at the level of financial report itself. The Auditing

Standard ASA 520 requires an auditor to apply analytical review procedures during conduct of its

audit. This is done with the purpose of including comparison of the information being financial in

nature with that of the prior period, budgets and the information of similar industry (Messier, 2005).

This is applied all throughout the audit i.e. during planning, substantive test and also while

reviewing at the end of audit (Koh, 1998). It again depends on many factors such as the nature of

the business, extent of reliance on the management, information being financial and non-financial

and their sources.

CONCLUSION:

Auditing being an important part of the accounting process requires to comply by the standards that

are being applicable on it so as to have the audit conducted in an appropriate manner. Auditors are

required to pay special attention and care while taking up audits for the first time in order to have

the same conducted smoothly. Effectively conducting Audit helps the users of the financial

statements to make and take investment decisions in the company and further helps in increasing

the value and the creditability of the financial reports and statements being prepared and presented

by the management of the company. All this helps not only the investors but all the stakeholders of

the company.

8

along with the increase in the Sales Revenue. This account possess the risk of omission and

the risk of wrong ledgers entry being involved.

Cash and Cash Equivalents: This has increased and requires to be analysed so as to see

any commission entries are not included within it.

Finance Costs: Reduction in the finance costs should be analysed so as to have

understanding of whether the finances have been repaid and their sources.

Share Based Payment Expenses: This has been appeared and needs to be analysed

effectively.

Trade and other Payables: Although there have been increase in the expenses and overall

decrease in the revenue but the trade payables have reduced considerably and requires

analysis.

Thus, the objective of identifying the material misstatement is to obtain sufficient evidences

regarding its assessment and analysing the extent of its being misstated through designing of

responses and implementation of the same. It is the duty and responsibility on part of the Auditor to

have designing and implementation of the responses for addressing the risks of material

misstatement. This is done by the Auditor at the level of financial report itself. The Auditing

Standard ASA 520 requires an auditor to apply analytical review procedures during conduct of its

audit. This is done with the purpose of including comparison of the information being financial in

nature with that of the prior period, budgets and the information of similar industry (Messier, 2005).

This is applied all throughout the audit i.e. during planning, substantive test and also while

reviewing at the end of audit (Koh, 1998). It again depends on many factors such as the nature of

the business, extent of reliance on the management, information being financial and non-financial

and their sources.

CONCLUSION:

Auditing being an important part of the accounting process requires to comply by the standards that

are being applicable on it so as to have the audit conducted in an appropriate manner. Auditors are

required to pay special attention and care while taking up audits for the first time in order to have

the same conducted smoothly. Effectively conducting Audit helps the users of the financial

statements to make and take investment decisions in the company and further helps in increasing

the value and the creditability of the financial reports and statements being prepared and presented

by the management of the company. All this helps not only the investors but all the stakeholders of

the company.

8

REFERENCES:

Best, P.J., Buckby, S., Tan, C. (2001). Evidence of the audit expectation gap in Singapore.

Managerial Auditing Journal, 16(3), 134–144.

Eluyela, Damilola & Ilogho, Simon. (2016). Audit Standards and Performance of Auditors':

Evidence From Nigerian Banking Industry. 10.13140/RG.2.2.32379.72481.

Firth, M. (1979). Consensus views and judgments models in materiality decisions. Accounting,

Organizations and Society, 4(4), 283–295

Jennings, M., Kneer, D.C., Reckers, P.M.J. (1987). A reexamination of the concept of materiality:

Views of auditors, users, and officers of the court. Auditing: A Journal of Practice and Theory,

6(2), 104–115.

Koh, H.C. , & Woo, E-Sah. (1998). The expectation gap in auditing. Managerial Auditing Journal,

13(3), 147–154.

Messier, W.F., Martinov-Bennie, N., Eilifsen, A. (2005). A review and integration of empirical

research on materiality: Two decades later. Auditing: A Journal of Practice & Theory, 24(2), 153–

187.

Porter, B. (1993). An empirical study of the audit expectation-performance gap. Accounting and

Business Research, 24(93), 49–68.

Power, M.K. (2003). Auditing and the production of legitimacy. Accounting, Organizations and

Society, 28(4), 379–394.

Simnett, Roger & Carson, Elizabeth & Vanstraelen, Ann. (2016). International Archival Auditing

and Assurance Research: Trends, Methodological Issues and Opportunities. AUDITING: A

Journal of Practice & Theory. 35. 10.2308/ajpt-51377.

9

Best, P.J., Buckby, S., Tan, C. (2001). Evidence of the audit expectation gap in Singapore.

Managerial Auditing Journal, 16(3), 134–144.

Eluyela, Damilola & Ilogho, Simon. (2016). Audit Standards and Performance of Auditors':

Evidence From Nigerian Banking Industry. 10.13140/RG.2.2.32379.72481.

Firth, M. (1979). Consensus views and judgments models in materiality decisions. Accounting,

Organizations and Society, 4(4), 283–295

Jennings, M., Kneer, D.C., Reckers, P.M.J. (1987). A reexamination of the concept of materiality:

Views of auditors, users, and officers of the court. Auditing: A Journal of Practice and Theory,

6(2), 104–115.

Koh, H.C. , & Woo, E-Sah. (1998). The expectation gap in auditing. Managerial Auditing Journal,

13(3), 147–154.

Messier, W.F., Martinov-Bennie, N., Eilifsen, A. (2005). A review and integration of empirical

research on materiality: Two decades later. Auditing: A Journal of Practice & Theory, 24(2), 153–

187.

Porter, B. (1993). An empirical study of the audit expectation-performance gap. Accounting and

Business Research, 24(93), 49–68.

Power, M.K. (2003). Auditing and the production of legitimacy. Accounting, Organizations and

Society, 28(4), 379–394.

Simnett, Roger & Carson, Elizabeth & Vanstraelen, Ann. (2016). International Archival Auditing

and Assurance Research: Trends, Methodological Issues and Opportunities. AUDITING: A

Journal of Practice & Theory. 35. 10.2308/ajpt-51377.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.