KOI Trimester 1, 2019 FIN700 - Financial Management Group Assignment 2

VerifiedAdded on 2023/01/10

|11

|1855

|98

Homework Assignment

AI Summary

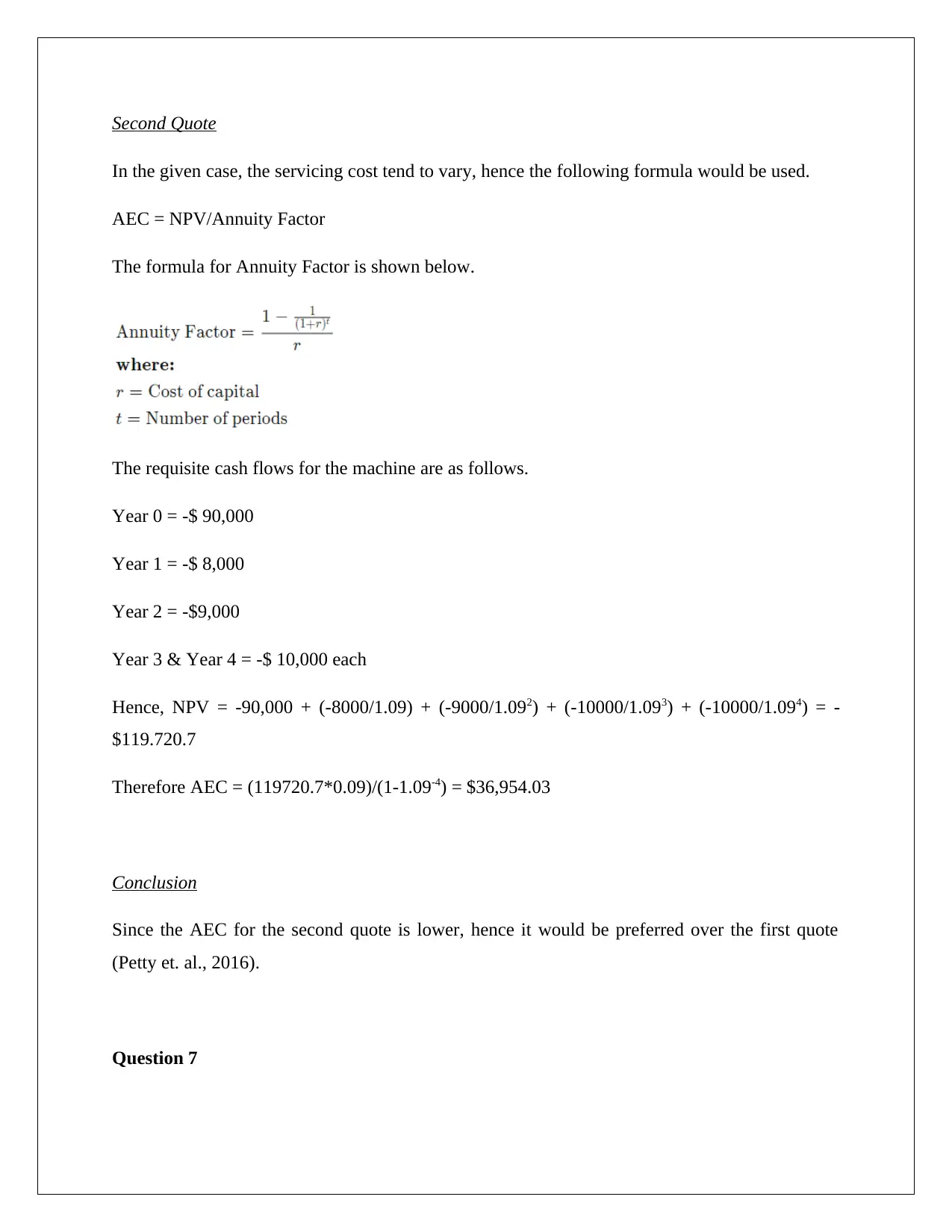

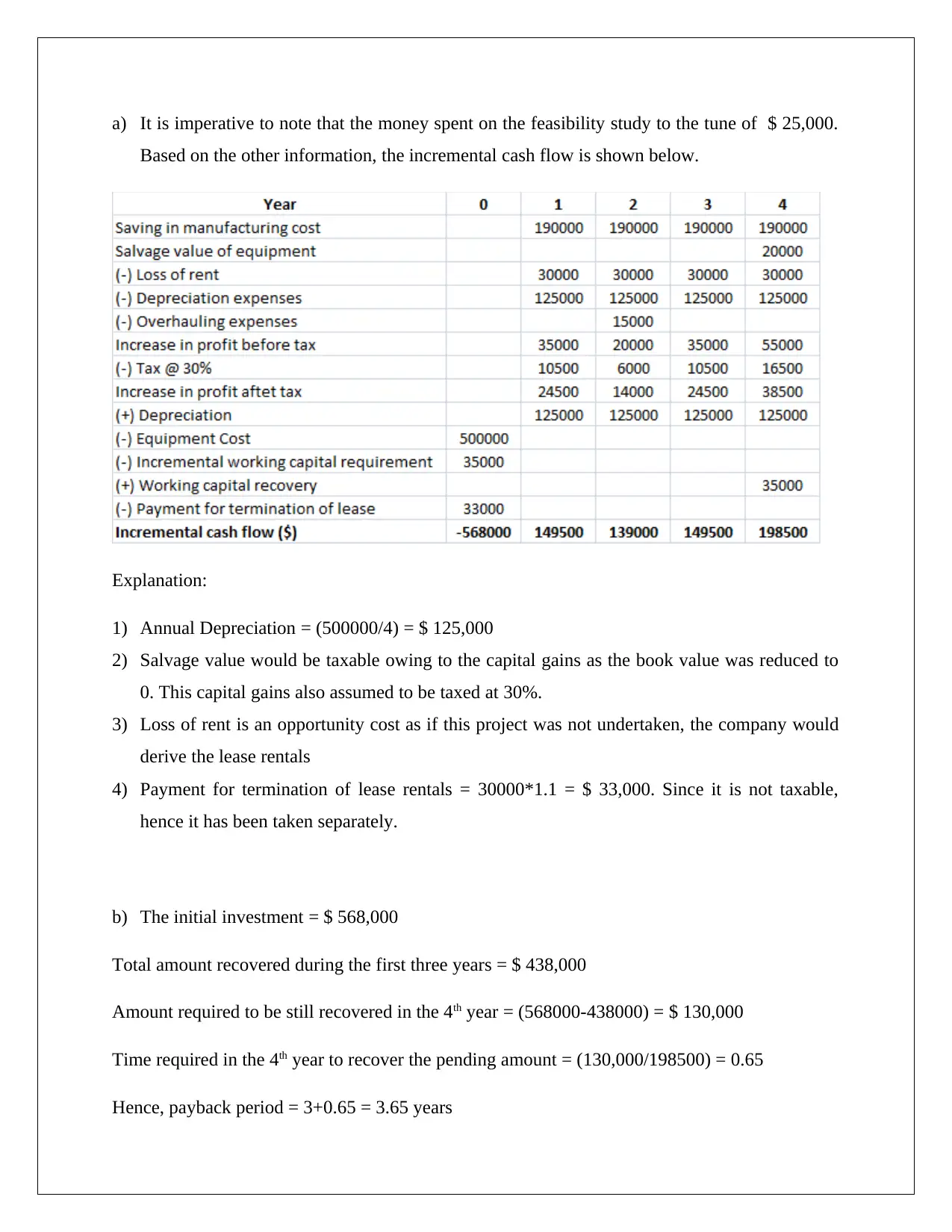

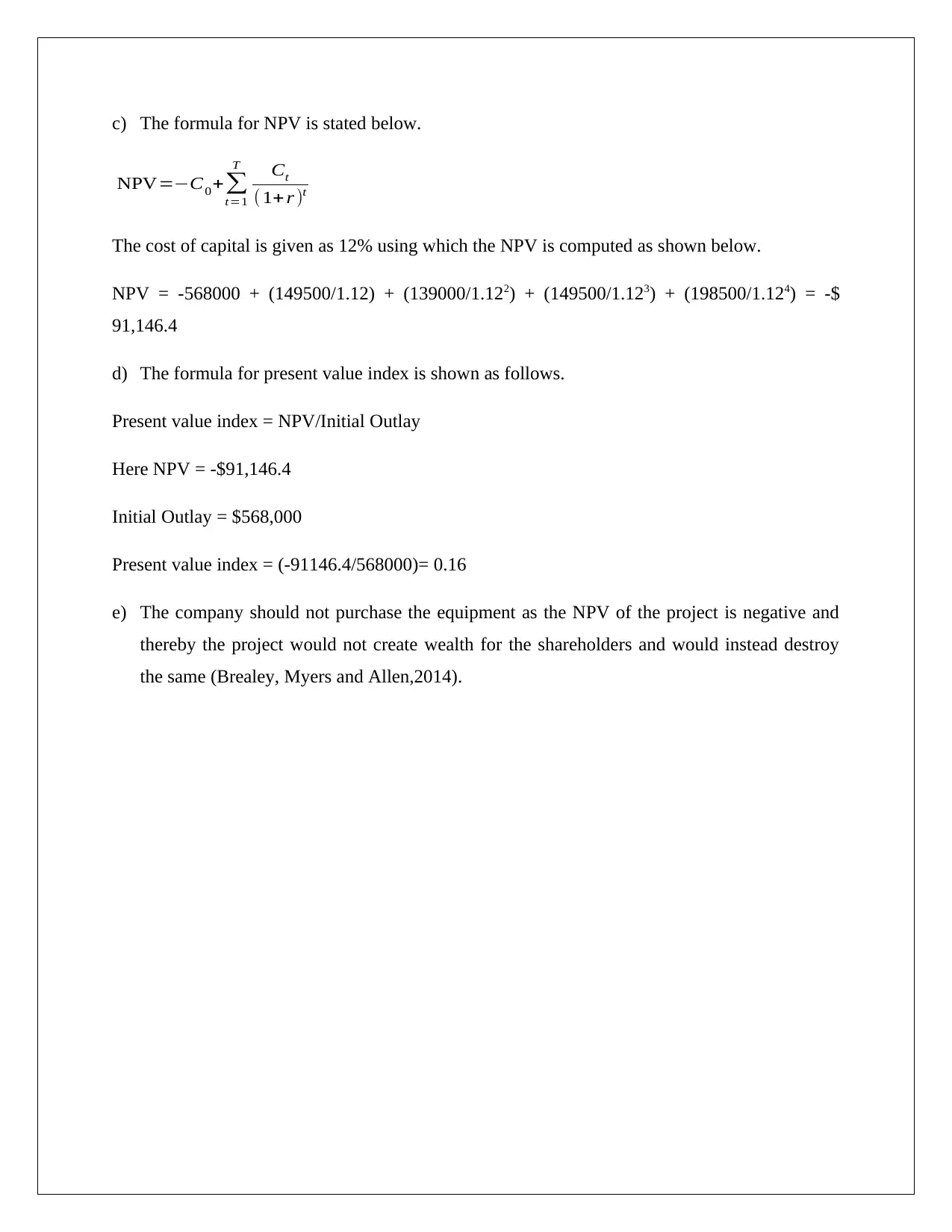

This document provides a comprehensive solution to a Financial Management assignment (FIN700) from KOI, Trimester 1, 2019. The assignment covers seven problems, including calculating Karina Adams' dividend income and loan requirements, EMI and amortization for a house loan, present value of cash flows and investment decisions, bond pricing and sensitivity analysis, Altron's share valuation using the dividend growth model, Annual Equivalent Cost (AEC) comparison of investment quotes, and capital budgeting decisions involving NPV, payback period, and present value index. Each question is solved with detailed formulas, step-by-step calculations, and relevant explanations, providing a complete guide for understanding the financial concepts and problem-solving techniques required for the assignment. The document references several financial management texts to support the solutions and recommendations.

1 out of 11

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.