Recording Business Transactions & Accounting Report for Kool Kit Ltd

VerifiedAdded on 2023/04/06

|12

|1984

|332

Report

AI Summary

This report analyzes the accounting practices of Kool Kit Ltd, a small business manufacturing kilts. Part 1 provides a management report, discussing the importance of accounting information, differentiating between gross and net profit with a numerical example, and explaining the differences between current and non-current assets/liabilities. It also describes the double-entry bookkeeping system, its history, and the meaning of debit and credit. Part 2 focuses on recording business transactions, including journal entries, T-accounts, and a trial balance for Kool Kit Limited, demonstrating the application of accounting principles to real-world business scenarios. The report references key accounting concepts and principles, providing a solid foundation for understanding financial management in a business context.

1

Recording Business transaction

Resit Assignment A1

Recording Business transaction

Resit Assignment A1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Part 1: Management Report.............................................................................................................3

A: Importance of accounting information in the business organization......................................3

B: Difference between gross profit and net profit through using the numerical example...........3

C: Difference between non-current assets and current assets; and non-current liabilities and

current liabilities..........................................................................................................................4

D: Double entry bookkeeping system..........................................................................................5

E: History of double entry bookkeeping......................................................................................5

F: Meaning of debit and credit.....................................................................................................5

Part 2: Recording Business Transactions........................................................................................7

A: Journal Entries.........................................................................................................................7

B: T-Accounts of Kool Kit Limited.............................................................................................9

C: Trial Balance of Kool Kit Limited........................................................................................11

References......................................................................................................................................12

Contents

Part 1: Management Report.............................................................................................................3

A: Importance of accounting information in the business organization......................................3

B: Difference between gross profit and net profit through using the numerical example...........3

C: Difference between non-current assets and current assets; and non-current liabilities and

current liabilities..........................................................................................................................4

D: Double entry bookkeeping system..........................................................................................5

E: History of double entry bookkeeping......................................................................................5

F: Meaning of debit and credit.....................................................................................................5

Part 2: Recording Business Transactions........................................................................................7

A: Journal Entries.........................................................................................................................7

B: T-Accounts of Kool Kit Limited.............................................................................................9

C: Trial Balance of Kool Kit Limited........................................................................................11

References......................................................................................................................................12

3

Part 1: Management Report

A: Importance of accounting information in the business organization

Accounting refers to as systematic process of recording and preparing book of accounts

for all the financial transactions related with the business organization. Accounting comprises of

recording, analyzing, summarizing and reporting of financial transactions so that information can

be used by various stakeholders of the business organization. Information gathered through

accounting can be used in different ways by the users of financial information. Management uses

financial information to ascertain the financial performance and financial position of the business

organization at the given point of time. Accounting information helps ion decision making

process, planning and also helps in controlling other processes. Through use of accounting

information such as profit & loss account, balance sheet and other information management can

make plans to formulate the budgets. Government officials required accounting information to

calculate the tax and also assess the financial position of the company. Information gathered

through accounting is used by the investors to make the investment decision. Information

provided in the financial statements is used by investors, business managers and creditors to

analysis the financial performance of the company and make decision accordingly. So it can be

said that accounting information is highly important for any business organization (Brigham and

Michael, 2013).

B: Difference between gross profit and net profit through using the numerical example

Profit is regarded as the difference between revenue earned and total cost for the

particular period. So profit is monetary reward that business receives during the normal conduct

of the business. Total cost of the business process can be divided into two major parts and they

are cost of goods sold and operating expenses including finance cost and tax. Gross profit

referred to as profit which is calculated by deducting cost of goods sold from sales revenue. Cost

of goods sold include expenses such as purchases, custom duty, inward carriage, labour expenses

and other expenses directly related with the product or services. On the other hand net profit is

calculated after deducting all the indirect expenses or operating expenses from gross profit.

Operating expenses includes expenses required to pay for running the business and selling the

goods. It can be said that gross profit is not the true profit of the company but net profit is the

true profit of the company. Gross profit cannot be used by the investors to judge the profitability

performance of the business but net profit reflects the actual profitability position of the company

(Damodaran, 2011).

Numerical Example: Suppose, a company made net sales $ 115,000 during the year and

expenses include $25000 purchases, $20000 labour charges, $10500 other direct expense and

$36000 operating expenses. Calculate gross profit and net profit.

Gross profit: Sales – cost of goods sold

Part 1: Management Report

A: Importance of accounting information in the business organization

Accounting refers to as systematic process of recording and preparing book of accounts

for all the financial transactions related with the business organization. Accounting comprises of

recording, analyzing, summarizing and reporting of financial transactions so that information can

be used by various stakeholders of the business organization. Information gathered through

accounting can be used in different ways by the users of financial information. Management uses

financial information to ascertain the financial performance and financial position of the business

organization at the given point of time. Accounting information helps ion decision making

process, planning and also helps in controlling other processes. Through use of accounting

information such as profit & loss account, balance sheet and other information management can

make plans to formulate the budgets. Government officials required accounting information to

calculate the tax and also assess the financial position of the company. Information gathered

through accounting is used by the investors to make the investment decision. Information

provided in the financial statements is used by investors, business managers and creditors to

analysis the financial performance of the company and make decision accordingly. So it can be

said that accounting information is highly important for any business organization (Brigham and

Michael, 2013).

B: Difference between gross profit and net profit through using the numerical example

Profit is regarded as the difference between revenue earned and total cost for the

particular period. So profit is monetary reward that business receives during the normal conduct

of the business. Total cost of the business process can be divided into two major parts and they

are cost of goods sold and operating expenses including finance cost and tax. Gross profit

referred to as profit which is calculated by deducting cost of goods sold from sales revenue. Cost

of goods sold include expenses such as purchases, custom duty, inward carriage, labour expenses

and other expenses directly related with the product or services. On the other hand net profit is

calculated after deducting all the indirect expenses or operating expenses from gross profit.

Operating expenses includes expenses required to pay for running the business and selling the

goods. It can be said that gross profit is not the true profit of the company but net profit is the

true profit of the company. Gross profit cannot be used by the investors to judge the profitability

performance of the business but net profit reflects the actual profitability position of the company

(Damodaran, 2011).

Numerical Example: Suppose, a company made net sales $ 115,000 during the year and

expenses include $25000 purchases, $20000 labour charges, $10500 other direct expense and

$36000 operating expenses. Calculate gross profit and net profit.

Gross profit: Sales – cost of goods sold

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

= $115,000 – ($25000+$20000+$10500)

= $59500

Net Profit = Gross Profit – all indirect expenses (operating expenses)

= $59500-$ 36000

= $23500

C: Difference between non-current assets and current assets; and non-current liabilities

and current liabilities

Non-Current asset and current asset

Assets that are used within the business can be divided into two major parts; current

assets and non-current assets. Current assets are referred to those items that have capability to be

converted into cash and cash equivalents within one fiscal year. It includes financial items such

as cash, bank balance, short term investments, account receivable, inventory etc. On the other

hand non-current asset are those assets that have life for more than 1 year and they are easily

convertible into cash. Some of important non-current assets are fixed assets like plant, equipment

etc, intangible assets, long term investment etc.

Current liabilities and non-current liabilities

Current liabilities referred to the payments that need to pay within one year time period

and non-current liabilities refers to payments that need to be settled after one year on the balance

sheet date. Current liabilities are generally paid through current assets and difference between

current assets and current liabilities is regarded as working capital.

Numerical Example: Consider the below balance sheet and divide all items into current assets,

non-current assets, current liabilities and non-current liabilities (Davies and Crawford, 2011)

Liabilities Amount Assets Amount

Account payable (short term) £ 15,000.00 Prepaid expenses £ 1,500.00

Unearned income £ 5,000.00 Bank Balance £ 25,500.00

Bank Loan (Long Term) £ 50,000.00 Plant and equipments £ 65,000.00

Tax expenses £ 6,500.00 Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

Inventory £ 35,000.00

Current Liabilities Amount Current Assets Amount

Account payable (short term) £ 15,000.00 Prepaid expenses £ 1,500.00

Unearned income £ 5,000.00 Bank Balance £ 25,500.00

Inventory £ 35,000.00

= $115,000 – ($25000+$20000+$10500)

= $59500

Net Profit = Gross Profit – all indirect expenses (operating expenses)

= $59500-$ 36000

= $23500

C: Difference between non-current assets and current assets; and non-current liabilities

and current liabilities

Non-Current asset and current asset

Assets that are used within the business can be divided into two major parts; current

assets and non-current assets. Current assets are referred to those items that have capability to be

converted into cash and cash equivalents within one fiscal year. It includes financial items such

as cash, bank balance, short term investments, account receivable, inventory etc. On the other

hand non-current asset are those assets that have life for more than 1 year and they are easily

convertible into cash. Some of important non-current assets are fixed assets like plant, equipment

etc, intangible assets, long term investment etc.

Current liabilities and non-current liabilities

Current liabilities referred to the payments that need to pay within one year time period

and non-current liabilities refers to payments that need to be settled after one year on the balance

sheet date. Current liabilities are generally paid through current assets and difference between

current assets and current liabilities is regarded as working capital.

Numerical Example: Consider the below balance sheet and divide all items into current assets,

non-current assets, current liabilities and non-current liabilities (Davies and Crawford, 2011)

Liabilities Amount Assets Amount

Account payable (short term) £ 15,000.00 Prepaid expenses £ 1,500.00

Unearned income £ 5,000.00 Bank Balance £ 25,500.00

Bank Loan (Long Term) £ 50,000.00 Plant and equipments £ 65,000.00

Tax expenses £ 6,500.00 Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

Inventory £ 35,000.00

Current Liabilities Amount Current Assets Amount

Account payable (short term) £ 15,000.00 Prepaid expenses £ 1,500.00

Unearned income £ 5,000.00 Bank Balance £ 25,500.00

Inventory £ 35,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

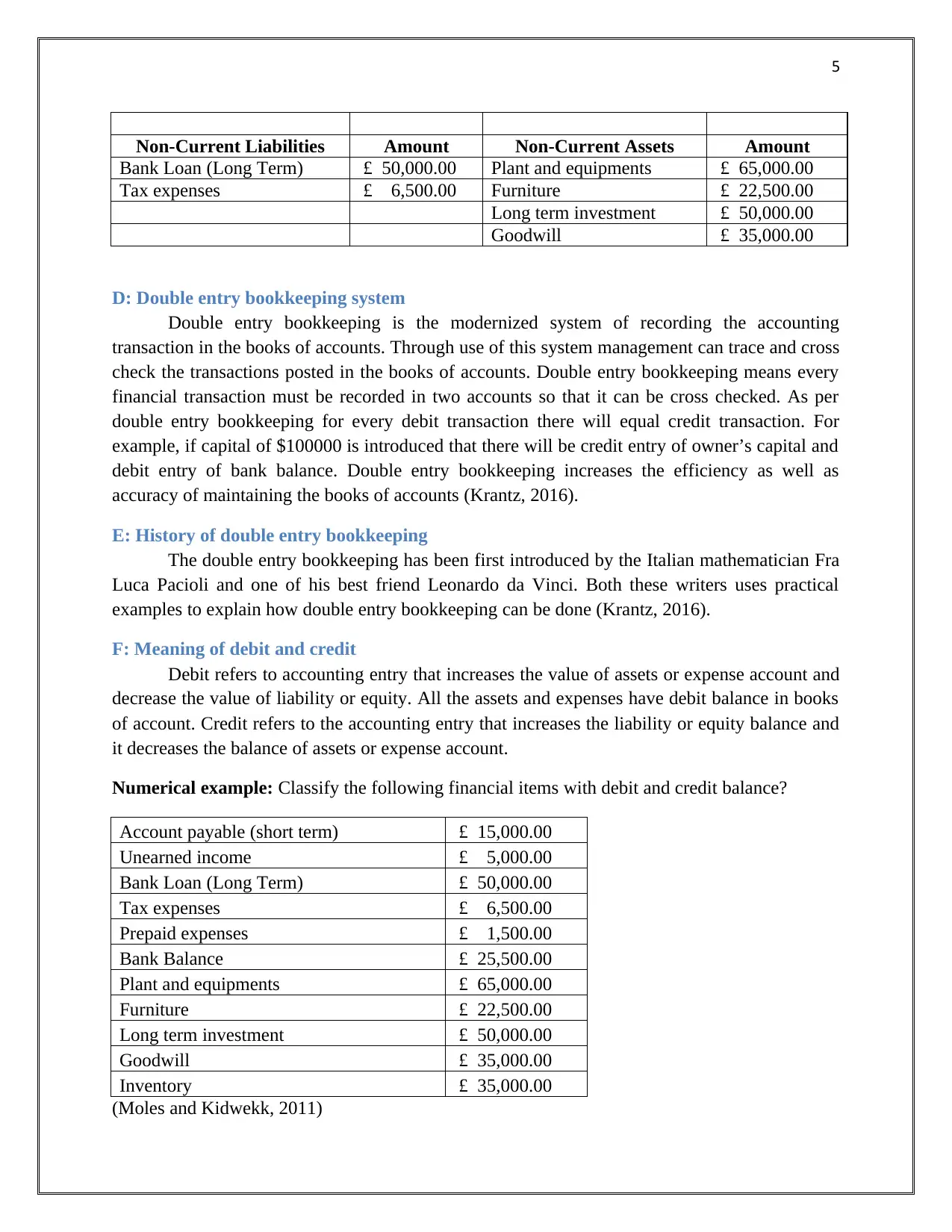

Non-Current Liabilities Amount Non-Current Assets Amount

Bank Loan (Long Term) £ 50,000.00 Plant and equipments £ 65,000.00

Tax expenses £ 6,500.00 Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

D: Double entry bookkeeping system

Double entry bookkeeping is the modernized system of recording the accounting

transaction in the books of accounts. Through use of this system management can trace and cross

check the transactions posted in the books of accounts. Double entry bookkeeping means every

financial transaction must be recorded in two accounts so that it can be cross checked. As per

double entry bookkeeping for every debit transaction there will equal credit transaction. For

example, if capital of $100000 is introduced that there will be credit entry of owner’s capital and

debit entry of bank balance. Double entry bookkeeping increases the efficiency as well as

accuracy of maintaining the books of accounts (Krantz, 2016).

E: History of double entry bookkeeping

The double entry bookkeeping has been first introduced by the Italian mathematician Fra

Luca Pacioli and one of his best friend Leonardo da Vinci. Both these writers uses practical

examples to explain how double entry bookkeeping can be done (Krantz, 2016).

F: Meaning of debit and credit

Debit refers to accounting entry that increases the value of assets or expense account and

decrease the value of liability or equity. All the assets and expenses have debit balance in books

of account. Credit refers to the accounting entry that increases the liability or equity balance and

it decreases the balance of assets or expense account.

Numerical example: Classify the following financial items with debit and credit balance?

Account payable (short term) £ 15,000.00

Unearned income £ 5,000.00

Bank Loan (Long Term) £ 50,000.00

Tax expenses £ 6,500.00

Prepaid expenses £ 1,500.00

Bank Balance £ 25,500.00

Plant and equipments £ 65,000.00

Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

Inventory £ 35,000.00

(Moles and Kidwekk, 2011)

Non-Current Liabilities Amount Non-Current Assets Amount

Bank Loan (Long Term) £ 50,000.00 Plant and equipments £ 65,000.00

Tax expenses £ 6,500.00 Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

D: Double entry bookkeeping system

Double entry bookkeeping is the modernized system of recording the accounting

transaction in the books of accounts. Through use of this system management can trace and cross

check the transactions posted in the books of accounts. Double entry bookkeeping means every

financial transaction must be recorded in two accounts so that it can be cross checked. As per

double entry bookkeeping for every debit transaction there will equal credit transaction. For

example, if capital of $100000 is introduced that there will be credit entry of owner’s capital and

debit entry of bank balance. Double entry bookkeeping increases the efficiency as well as

accuracy of maintaining the books of accounts (Krantz, 2016).

E: History of double entry bookkeeping

The double entry bookkeeping has been first introduced by the Italian mathematician Fra

Luca Pacioli and one of his best friend Leonardo da Vinci. Both these writers uses practical

examples to explain how double entry bookkeeping can be done (Krantz, 2016).

F: Meaning of debit and credit

Debit refers to accounting entry that increases the value of assets or expense account and

decrease the value of liability or equity. All the assets and expenses have debit balance in books

of account. Credit refers to the accounting entry that increases the liability or equity balance and

it decreases the balance of assets or expense account.

Numerical example: Classify the following financial items with debit and credit balance?

Account payable (short term) £ 15,000.00

Unearned income £ 5,000.00

Bank Loan (Long Term) £ 50,000.00

Tax expenses £ 6,500.00

Prepaid expenses £ 1,500.00

Bank Balance £ 25,500.00

Plant and equipments £ 65,000.00

Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

Inventory £ 35,000.00

(Moles and Kidwekk, 2011)

6

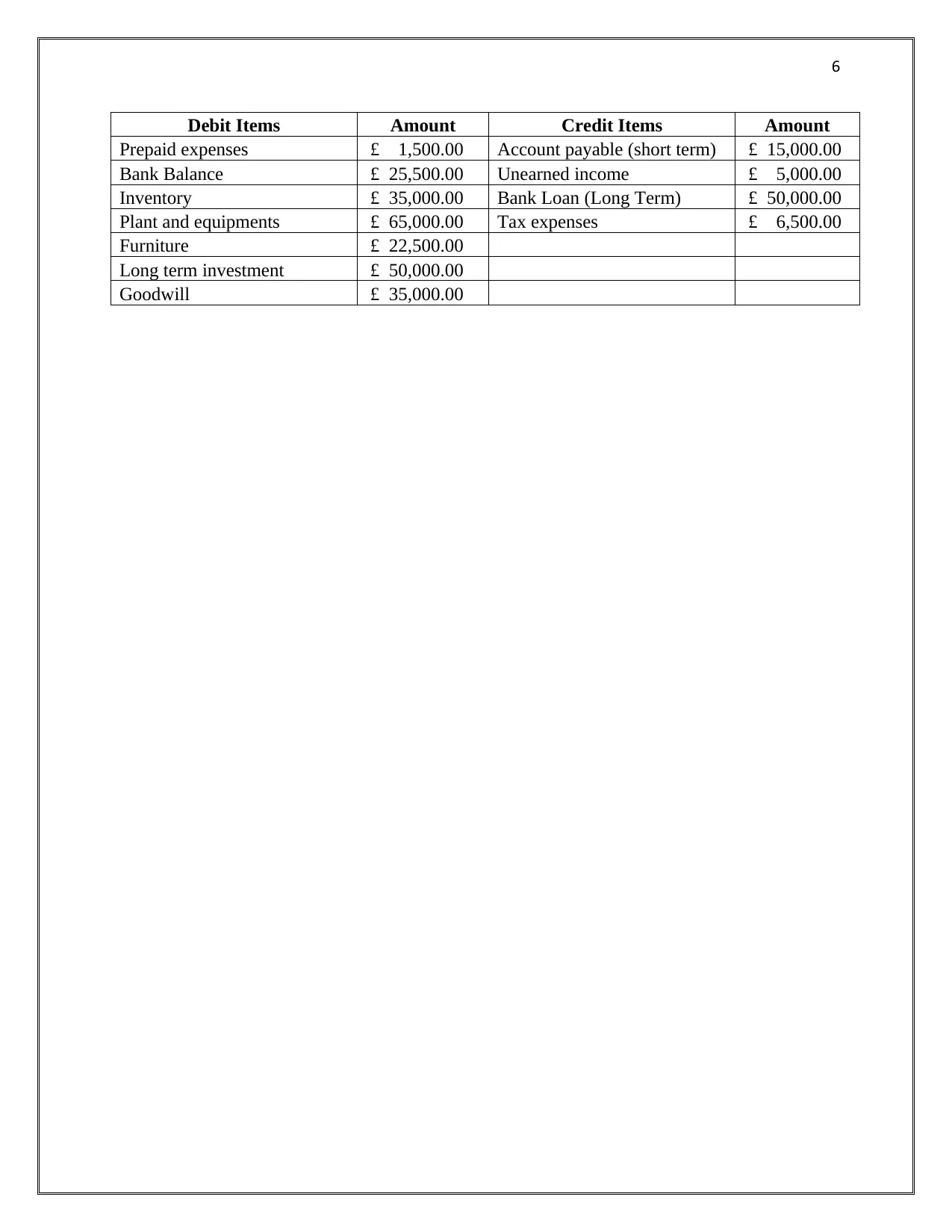

Debit Items Amount Credit Items Amount

Prepaid expenses £ 1,500.00 Account payable (short term) £ 15,000.00

Bank Balance £ 25,500.00 Unearned income £ 5,000.00

Inventory £ 35,000.00 Bank Loan (Long Term) £ 50,000.00

Plant and equipments £ 65,000.00 Tax expenses £ 6,500.00

Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

Debit Items Amount Credit Items Amount

Prepaid expenses £ 1,500.00 Account payable (short term) £ 15,000.00

Bank Balance £ 25,500.00 Unearned income £ 5,000.00

Inventory £ 35,000.00 Bank Loan (Long Term) £ 50,000.00

Plant and equipments £ 65,000.00 Tax expenses £ 6,500.00

Furniture £ 22,500.00

Long term investment £ 50,000.00

Goodwill £ 35,000.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Part 2: Recording Business Transactions

A: Journal Entries

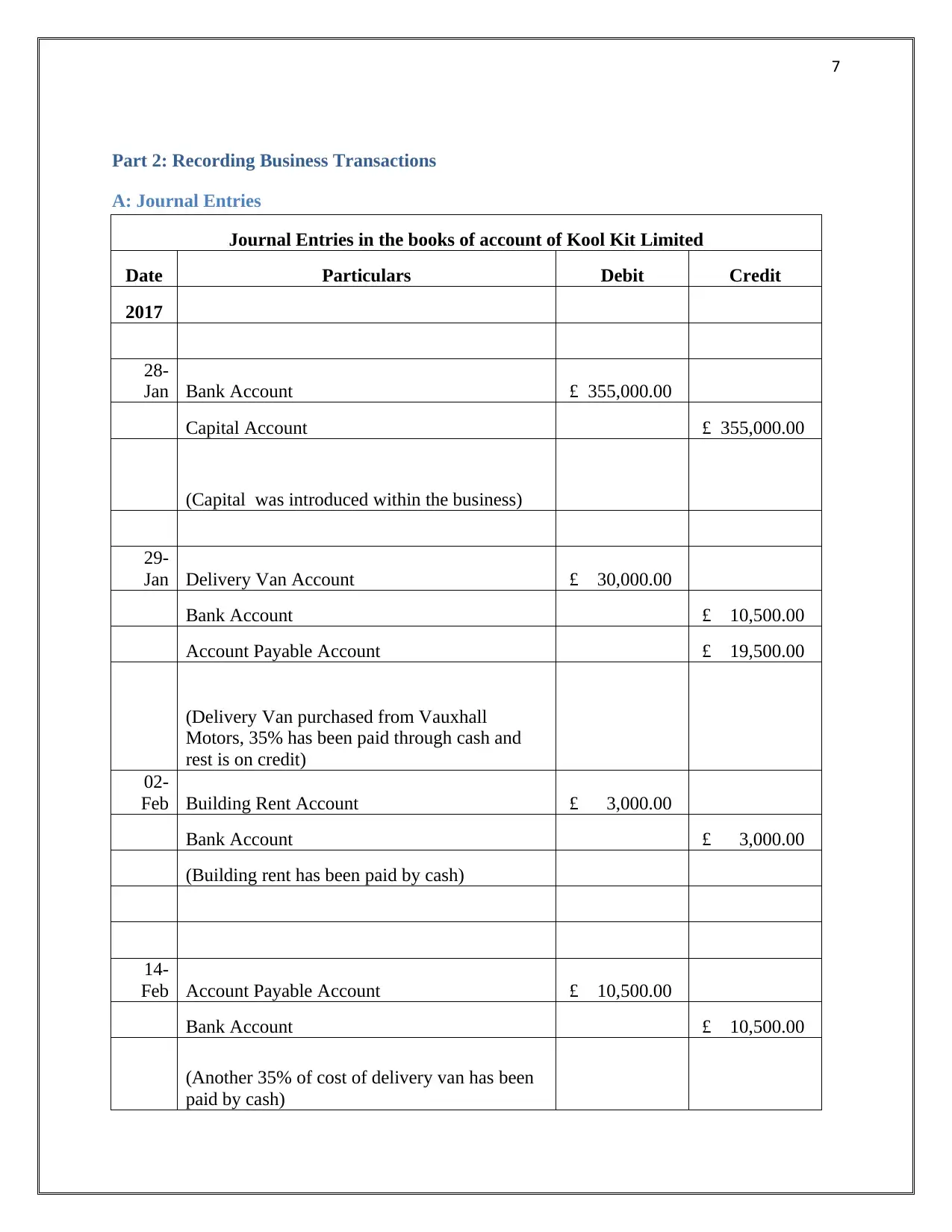

Journal Entries in the books of account of Kool Kit Limited

Date Particulars Debit Credit

2017

28-

Jan Bank Account £ 355,000.00

Capital Account £ 355,000.00

(Capital was introduced within the business)

29-

Jan Delivery Van Account £ 30,000.00

Bank Account £ 10,500.00

Account Payable Account £ 19,500.00

(Delivery Van purchased from Vauxhall

Motors, 35% has been paid through cash and

rest is on credit)

02-

Feb Building Rent Account £ 3,000.00

Bank Account £ 3,000.00

(Building rent has been paid by cash)

14-

Feb Account Payable Account £ 10,500.00

Bank Account £ 10,500.00

(Another 35% of cost of delivery van has been

paid by cash)

Part 2: Recording Business Transactions

A: Journal Entries

Journal Entries in the books of account of Kool Kit Limited

Date Particulars Debit Credit

2017

28-

Jan Bank Account £ 355,000.00

Capital Account £ 355,000.00

(Capital was introduced within the business)

29-

Jan Delivery Van Account £ 30,000.00

Bank Account £ 10,500.00

Account Payable Account £ 19,500.00

(Delivery Van purchased from Vauxhall

Motors, 35% has been paid through cash and

rest is on credit)

02-

Feb Building Rent Account £ 3,000.00

Bank Account £ 3,000.00

(Building rent has been paid by cash)

14-

Feb Account Payable Account £ 10,500.00

Bank Account £ 10,500.00

(Another 35% of cost of delivery van has been

paid by cash)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

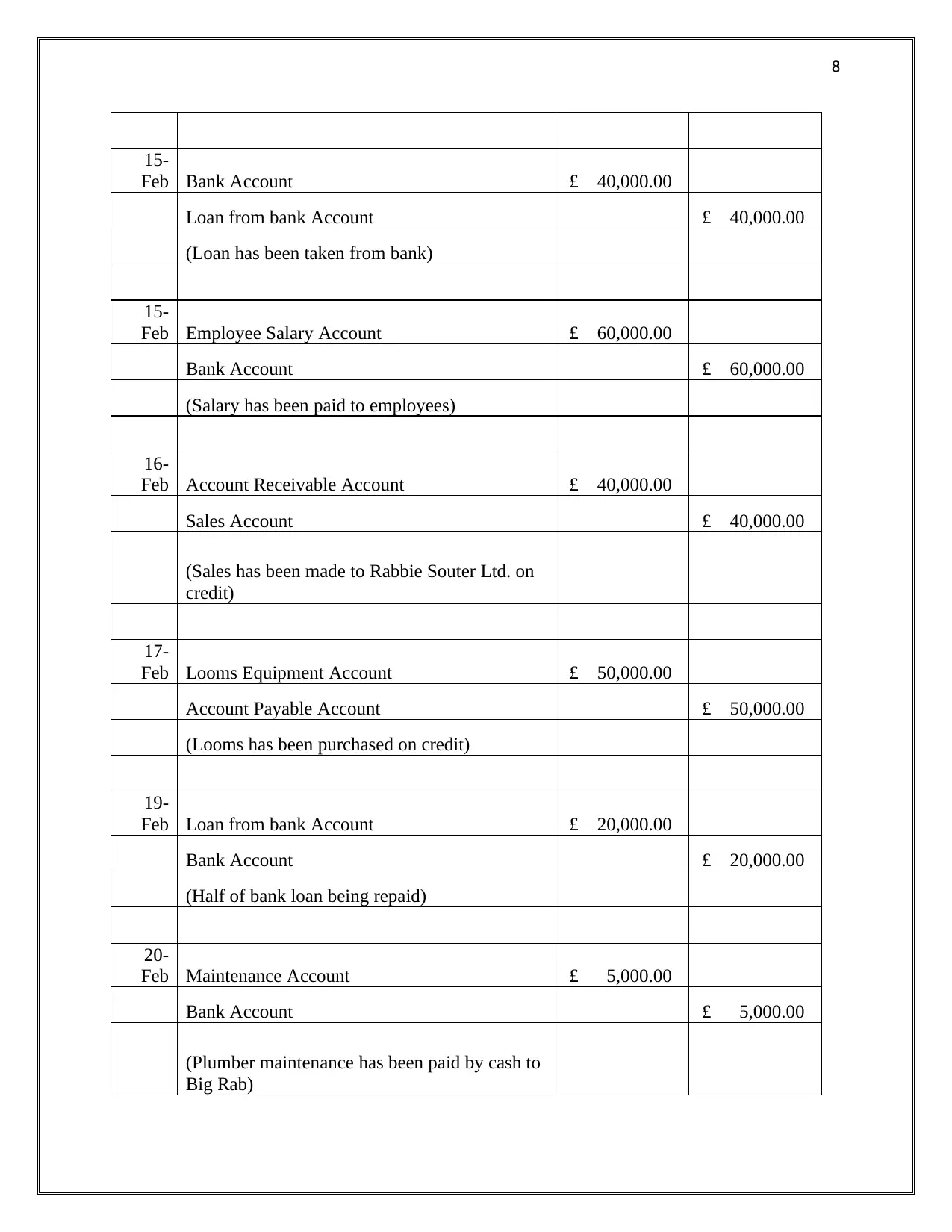

15-

Feb Bank Account £ 40,000.00

Loan from bank Account £ 40,000.00

(Loan has been taken from bank)

15-

Feb Employee Salary Account £ 60,000.00

Bank Account £ 60,000.00

(Salary has been paid to employees)

16-

Feb Account Receivable Account £ 40,000.00

Sales Account £ 40,000.00

(Sales has been made to Rabbie Souter Ltd. on

credit)

17-

Feb Looms Equipment Account £ 50,000.00

Account Payable Account £ 50,000.00

(Looms has been purchased on credit)

19-

Feb Loan from bank Account £ 20,000.00

Bank Account £ 20,000.00

(Half of bank loan being repaid)

20-

Feb Maintenance Account £ 5,000.00

Bank Account £ 5,000.00

(Plumber maintenance has been paid by cash to

Big Rab)

15-

Feb Bank Account £ 40,000.00

Loan from bank Account £ 40,000.00

(Loan has been taken from bank)

15-

Feb Employee Salary Account £ 60,000.00

Bank Account £ 60,000.00

(Salary has been paid to employees)

16-

Feb Account Receivable Account £ 40,000.00

Sales Account £ 40,000.00

(Sales has been made to Rabbie Souter Ltd. on

credit)

17-

Feb Looms Equipment Account £ 50,000.00

Account Payable Account £ 50,000.00

(Looms has been purchased on credit)

19-

Feb Loan from bank Account £ 20,000.00

Bank Account £ 20,000.00

(Half of bank loan being repaid)

20-

Feb Maintenance Account £ 5,000.00

Bank Account £ 5,000.00

(Plumber maintenance has been paid by cash to

Big Rab)

9

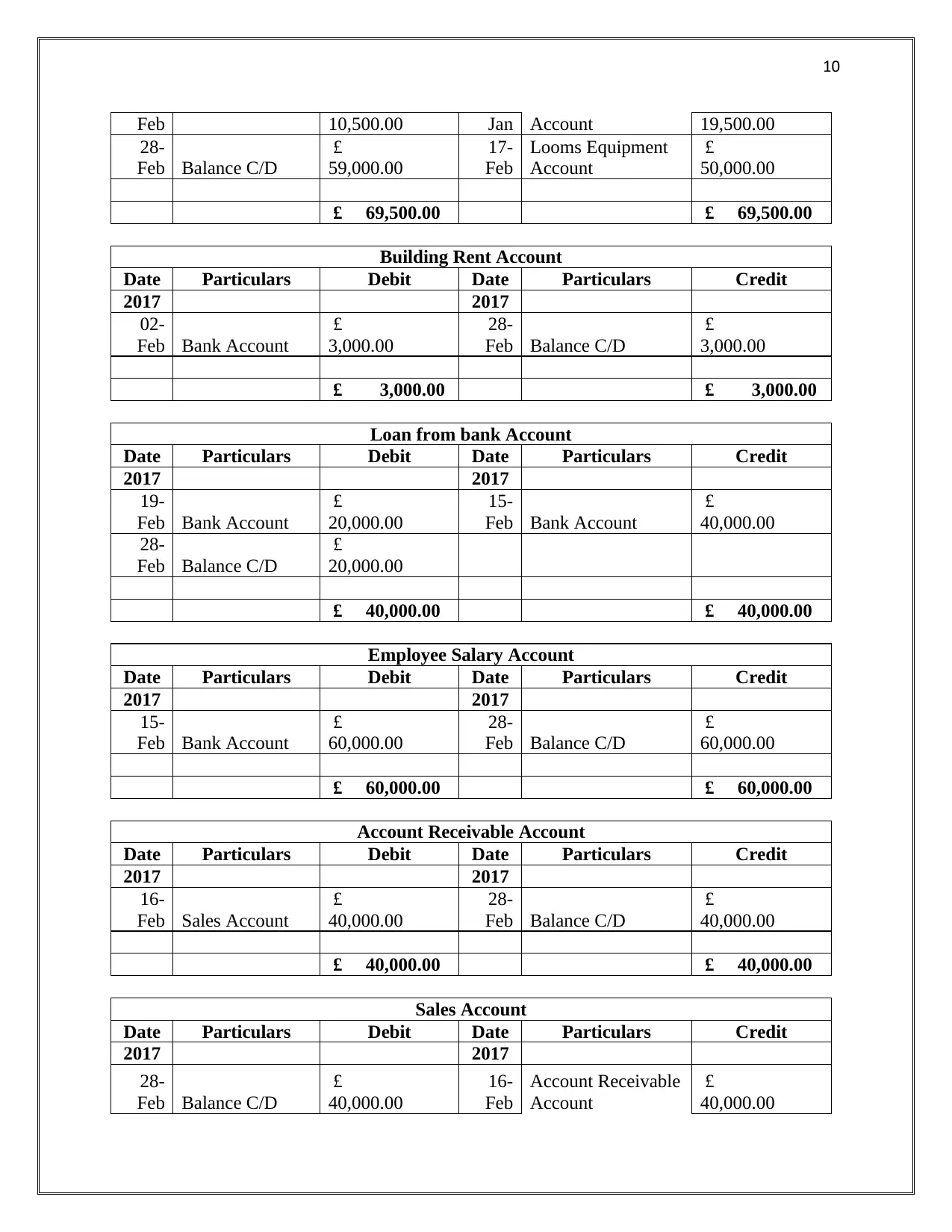

B: T-Accounts of Kool Kit Limited

Bank Account

Date Particulars Debit Date Particulars Credit

2017 2017

28-

Jan Capital Account £ 355,000.00

29-

Jan

Delivery Van

Account

£

10,500.00

15-

Feb

Loan from bank

Account

£

40,000.00

02-

Feb

Building Rent

Account

£

3,000.00

14-

Feb

Account Payable

Account

£

10,500.00

15-

Feb

Employee Salary

Account

£

60,000.00

19-

Feb

Loan from bank

Account

£

20,000.00

20-

Feb

Maintenance

Account

£

5,000.00

28-

Feb Balance C/D £ 286,000.00

£ 395,000.00 £ 395,000.00

Capital Account

Date Particulars Debit Date Particulars Credit

2017 2017

28-

Feb Balance C/D £ 355,000.00

28-

Jan Bank Account £ 355,000.00

£ 355,000.00 £ 355,000.00

Delivery Van Account

Date Particulars Debit Date Particulars Credit

2017 2017

29-

Jan Bank Account

£

10,500.00

29-

Jan

Account Payable

Account

£

19,500.00

28-

Feb Balance C/D

£

30,000.00

£ 30,000.00 £ 30,000.00

Account Payable Account

Date Particulars Debit Date Particulars Credit

2017 2017

14- Bank account £ 29- Delivery Van £

B: T-Accounts of Kool Kit Limited

Bank Account

Date Particulars Debit Date Particulars Credit

2017 2017

28-

Jan Capital Account £ 355,000.00

29-

Jan

Delivery Van

Account

£

10,500.00

15-

Feb

Loan from bank

Account

£

40,000.00

02-

Feb

Building Rent

Account

£

3,000.00

14-

Feb

Account Payable

Account

£

10,500.00

15-

Feb

Employee Salary

Account

£

60,000.00

19-

Feb

Loan from bank

Account

£

20,000.00

20-

Feb

Maintenance

Account

£

5,000.00

28-

Feb Balance C/D £ 286,000.00

£ 395,000.00 £ 395,000.00

Capital Account

Date Particulars Debit Date Particulars Credit

2017 2017

28-

Feb Balance C/D £ 355,000.00

28-

Jan Bank Account £ 355,000.00

£ 355,000.00 £ 355,000.00

Delivery Van Account

Date Particulars Debit Date Particulars Credit

2017 2017

29-

Jan Bank Account

£

10,500.00

29-

Jan

Account Payable

Account

£

19,500.00

28-

Feb Balance C/D

£

30,000.00

£ 30,000.00 £ 30,000.00

Account Payable Account

Date Particulars Debit Date Particulars Credit

2017 2017

14- Bank account £ 29- Delivery Van £

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Feb 10,500.00 Jan Account 19,500.00

28-

Feb Balance C/D

£

59,000.00

17-

Feb

Looms Equipment

Account

£

50,000.00

£ 69,500.00 £ 69,500.00

Building Rent Account

Date Particulars Debit Date Particulars Credit

2017 2017

02-

Feb Bank Account

£

3,000.00

28-

Feb Balance C/D

£

3,000.00

£ 3,000.00 £ 3,000.00

Loan from bank Account

Date Particulars Debit Date Particulars Credit

2017 2017

19-

Feb Bank Account

£

20,000.00

15-

Feb Bank Account

£

40,000.00

28-

Feb Balance C/D

£

20,000.00

£ 40,000.00 £ 40,000.00

Employee Salary Account

Date Particulars Debit Date Particulars Credit

2017 2017

15-

Feb Bank Account

£

60,000.00

28-

Feb Balance C/D

£

60,000.00

£ 60,000.00 £ 60,000.00

Account Receivable Account

Date Particulars Debit Date Particulars Credit

2017 2017

16-

Feb Sales Account

£

40,000.00

28-

Feb Balance C/D

£

40,000.00

£ 40,000.00 £ 40,000.00

Sales Account

Date Particulars Debit Date Particulars Credit

2017 2017

28-

Feb Balance C/D

£

40,000.00

16-

Feb

Account Receivable

Account

£

40,000.00

Feb 10,500.00 Jan Account 19,500.00

28-

Feb Balance C/D

£

59,000.00

17-

Feb

Looms Equipment

Account

£

50,000.00

£ 69,500.00 £ 69,500.00

Building Rent Account

Date Particulars Debit Date Particulars Credit

2017 2017

02-

Feb Bank Account

£

3,000.00

28-

Feb Balance C/D

£

3,000.00

£ 3,000.00 £ 3,000.00

Loan from bank Account

Date Particulars Debit Date Particulars Credit

2017 2017

19-

Feb Bank Account

£

20,000.00

15-

Feb Bank Account

£

40,000.00

28-

Feb Balance C/D

£

20,000.00

£ 40,000.00 £ 40,000.00

Employee Salary Account

Date Particulars Debit Date Particulars Credit

2017 2017

15-

Feb Bank Account

£

60,000.00

28-

Feb Balance C/D

£

60,000.00

£ 60,000.00 £ 60,000.00

Account Receivable Account

Date Particulars Debit Date Particulars Credit

2017 2017

16-

Feb Sales Account

£

40,000.00

28-

Feb Balance C/D

£

40,000.00

£ 40,000.00 £ 40,000.00

Sales Account

Date Particulars Debit Date Particulars Credit

2017 2017

28-

Feb Balance C/D

£

40,000.00

16-

Feb

Account Receivable

Account

£

40,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

£ 40,000.00 £ 40,000.00

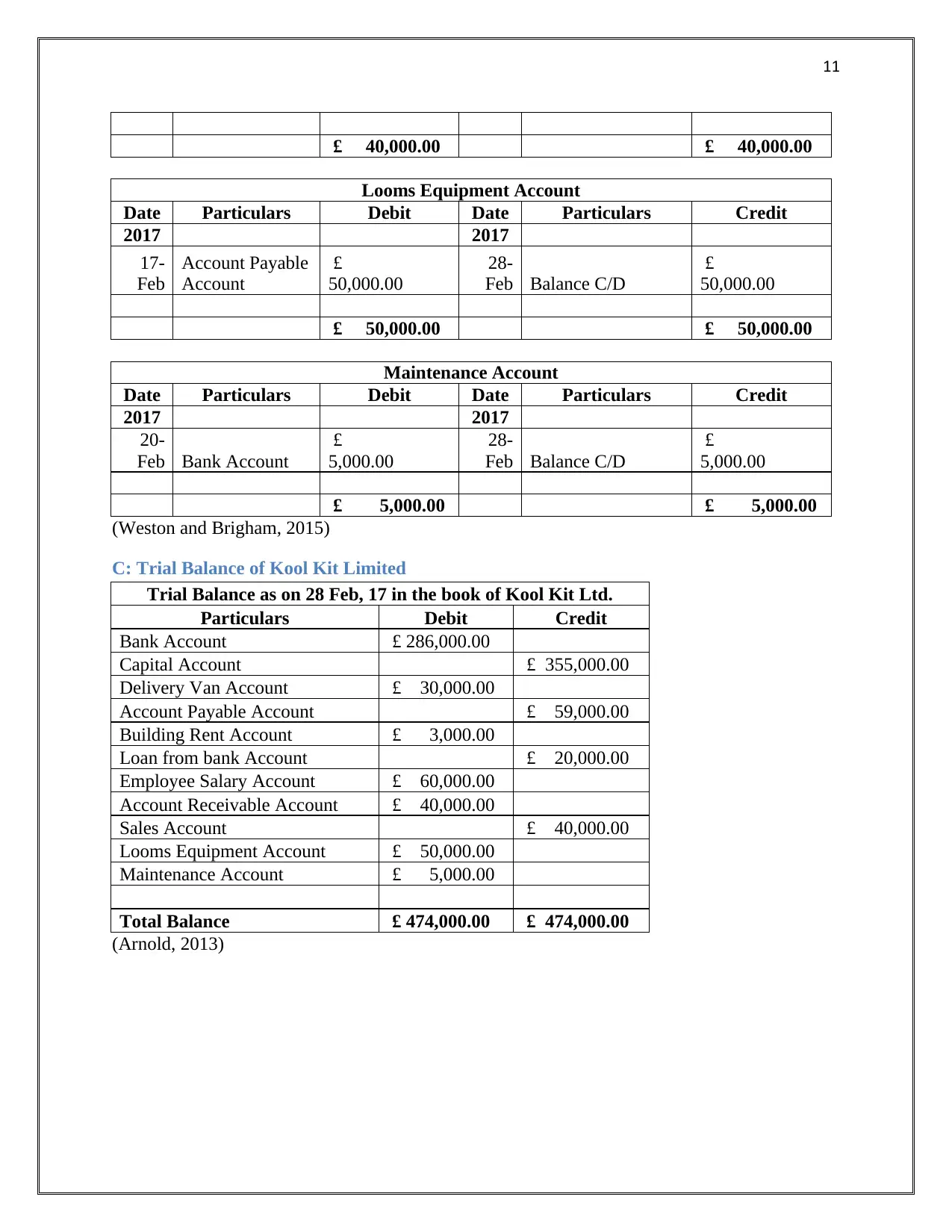

Looms Equipment Account

Date Particulars Debit Date Particulars Credit

2017 2017

17-

Feb

Account Payable

Account

£

50,000.00

28-

Feb Balance C/D

£

50,000.00

£ 50,000.00 £ 50,000.00

Maintenance Account

Date Particulars Debit Date Particulars Credit

2017 2017

20-

Feb Bank Account

£

5,000.00

28-

Feb Balance C/D

£

5,000.00

£ 5,000.00 £ 5,000.00

(Weston and Brigham, 2015)

C: Trial Balance of Kool Kit Limited

Trial Balance as on 28 Feb, 17 in the book of Kool Kit Ltd.

Particulars Debit Credit

Bank Account £ 286,000.00

Capital Account £ 355,000.00

Delivery Van Account £ 30,000.00

Account Payable Account £ 59,000.00

Building Rent Account £ 3,000.00

Loan from bank Account £ 20,000.00

Employee Salary Account £ 60,000.00

Account Receivable Account £ 40,000.00

Sales Account £ 40,000.00

Looms Equipment Account £ 50,000.00

Maintenance Account £ 5,000.00

Total Balance £ 474,000.00 £ 474,000.00

(Arnold, 2013)

£ 40,000.00 £ 40,000.00

Looms Equipment Account

Date Particulars Debit Date Particulars Credit

2017 2017

17-

Feb

Account Payable

Account

£

50,000.00

28-

Feb Balance C/D

£

50,000.00

£ 50,000.00 £ 50,000.00

Maintenance Account

Date Particulars Debit Date Particulars Credit

2017 2017

20-

Feb Bank Account

£

5,000.00

28-

Feb Balance C/D

£

5,000.00

£ 5,000.00 £ 5,000.00

(Weston and Brigham, 2015)

C: Trial Balance of Kool Kit Limited

Trial Balance as on 28 Feb, 17 in the book of Kool Kit Ltd.

Particulars Debit Credit

Bank Account £ 286,000.00

Capital Account £ 355,000.00

Delivery Van Account £ 30,000.00

Account Payable Account £ 59,000.00

Building Rent Account £ 3,000.00

Loan from bank Account £ 20,000.00

Employee Salary Account £ 60,000.00

Account Receivable Account £ 40,000.00

Sales Account £ 40,000.00

Looms Equipment Account £ 50,000.00

Maintenance Account £ 5,000.00

Total Balance £ 474,000.00 £ 474,000.00

(Arnold, 2013)

12

References

Arnold, G., 2013. Corporate financial management. USA: Pearson Higher Ed.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. USA: Cengage

Learning.

Damodaran, A, 2011. Applied corporate finance. Canada: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Krantz, M. 2016. Fundamental Analysis for Dummies. Canada: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. Canada: John Wiley &sons.

Weston, J.F. and Brigham, E.F., 2015. Managerial finance. Australia: Hinsdale, IL: Dryden

Press.

References

Arnold, G., 2013. Corporate financial management. USA: Pearson Higher Ed.

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. USA: Cengage

Learning.

Damodaran, A, 2011. Applied corporate finance. Canada: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Krantz, M. 2016. Fundamental Analysis for Dummies. Canada: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. Canada: John Wiley &sons.

Weston, J.F. and Brigham, E.F., 2015. Managerial finance. Australia: Hinsdale, IL: Dryden

Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.