Business Finance: Investment Appraisal, NPV & Funding for K PLC

VerifiedAdded on 2023/06/16

|19

|3950

|285

Report

AI Summary

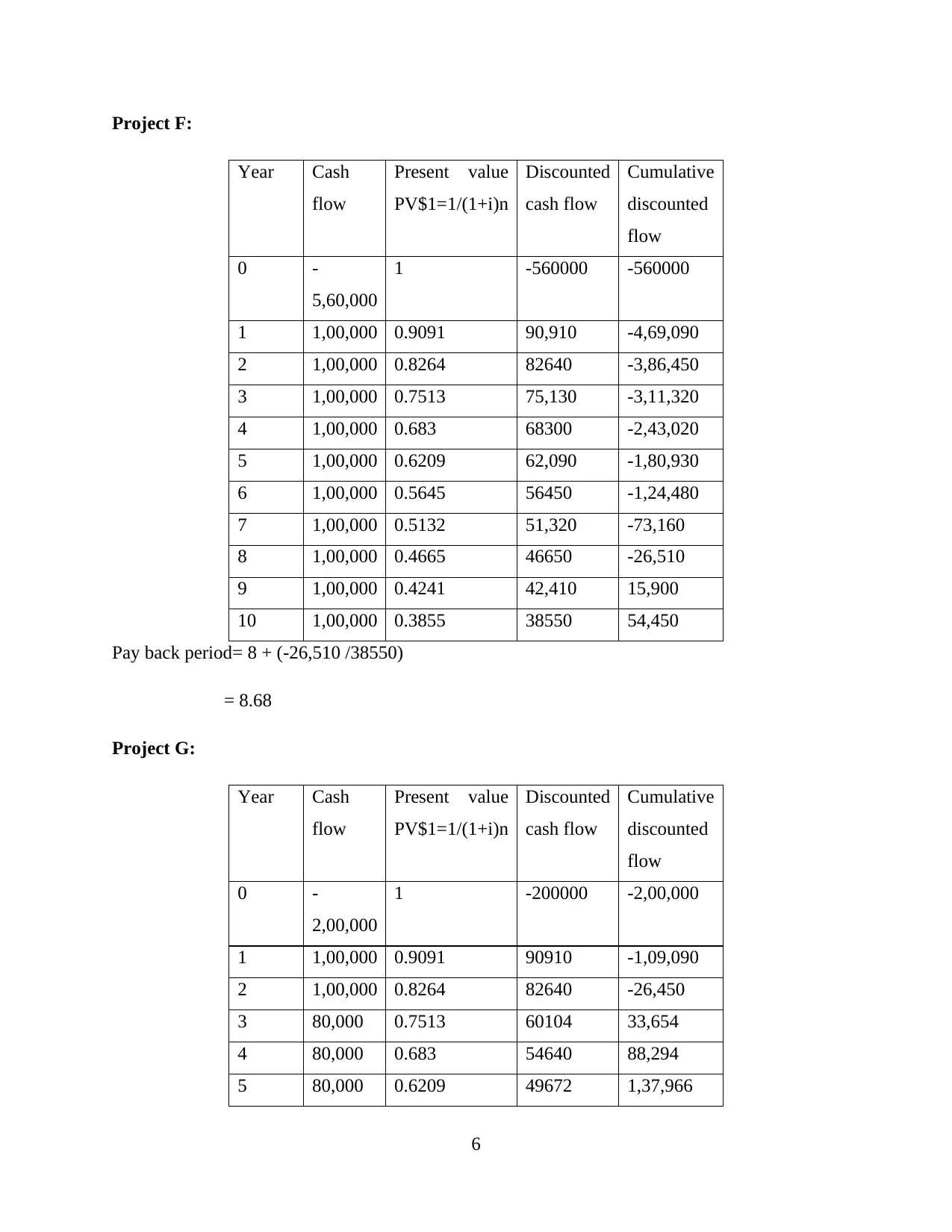

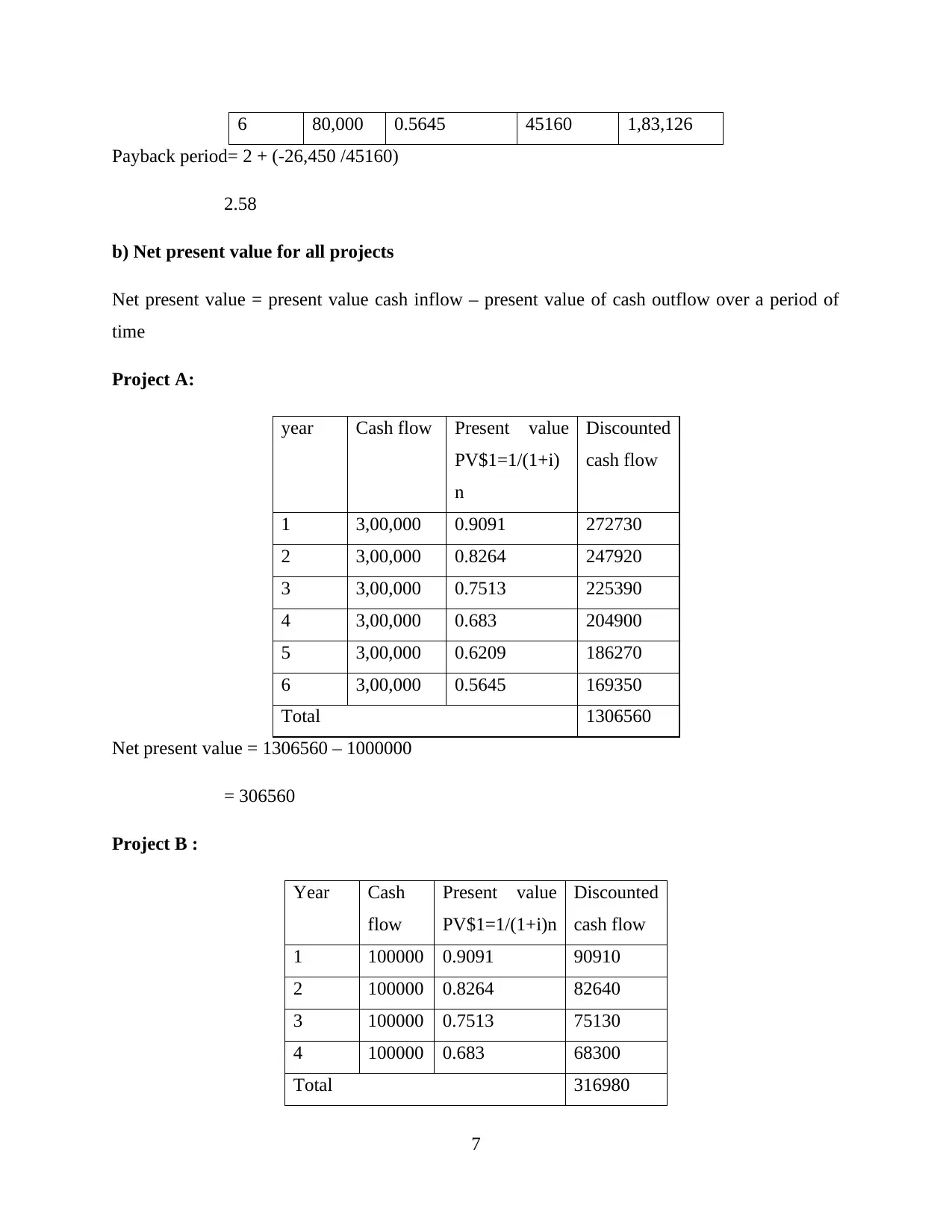

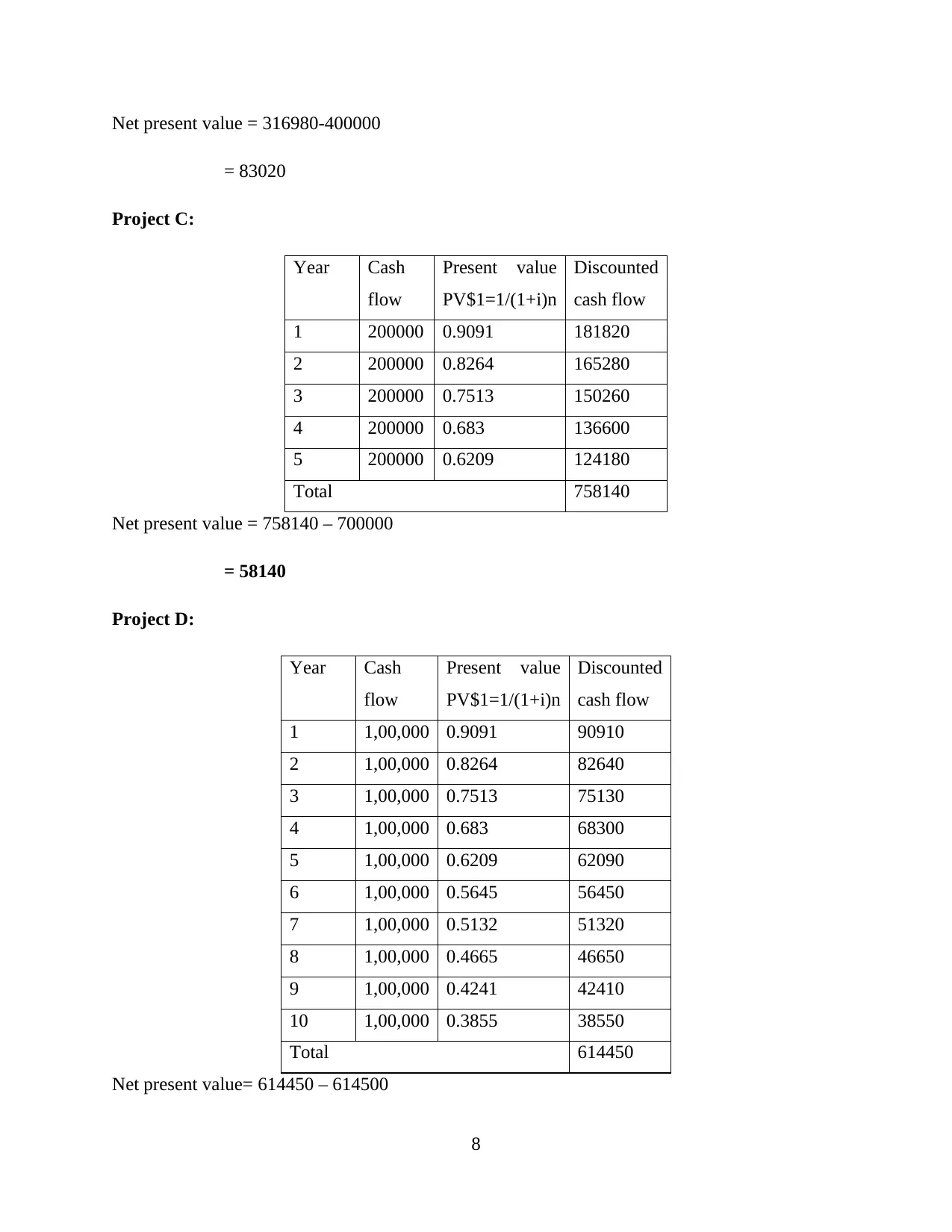

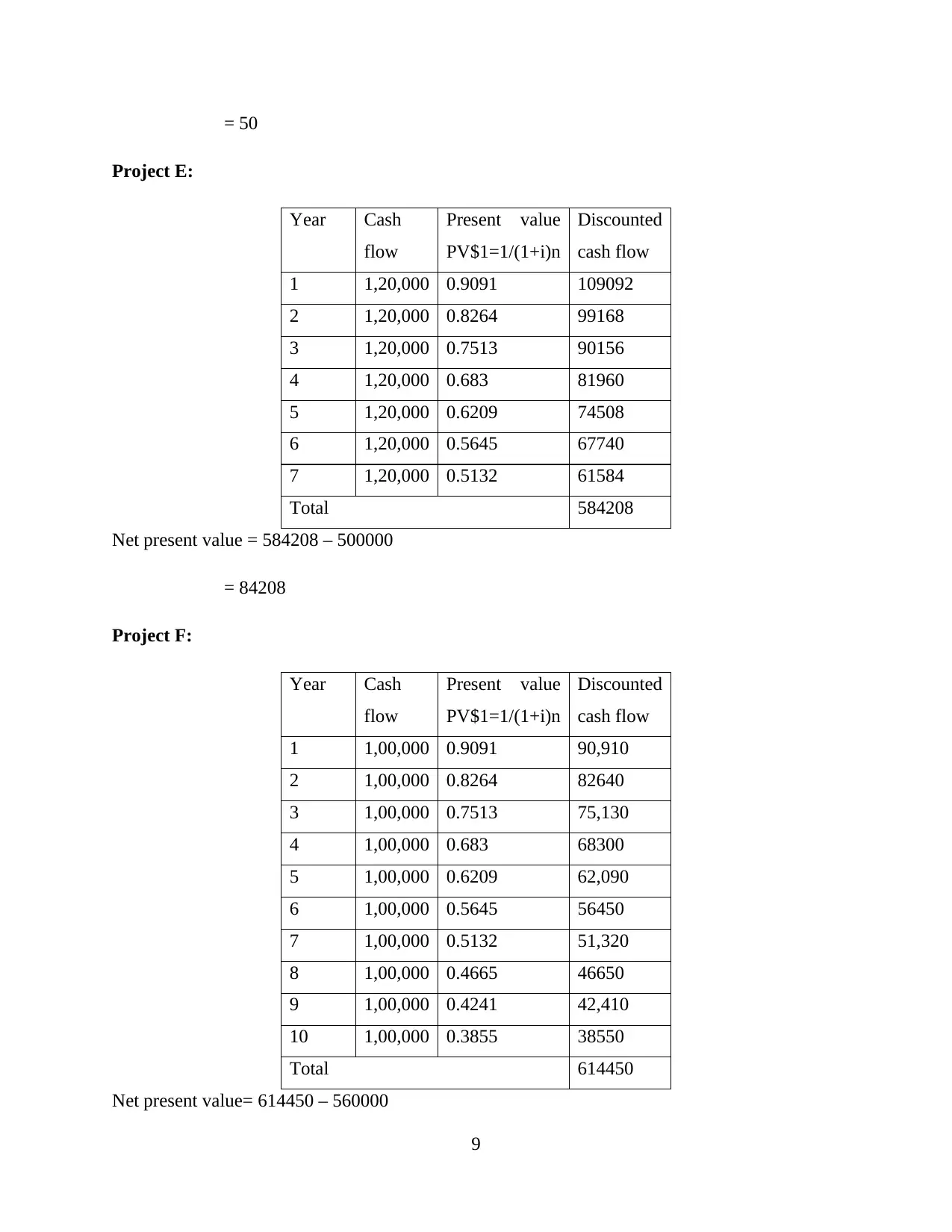

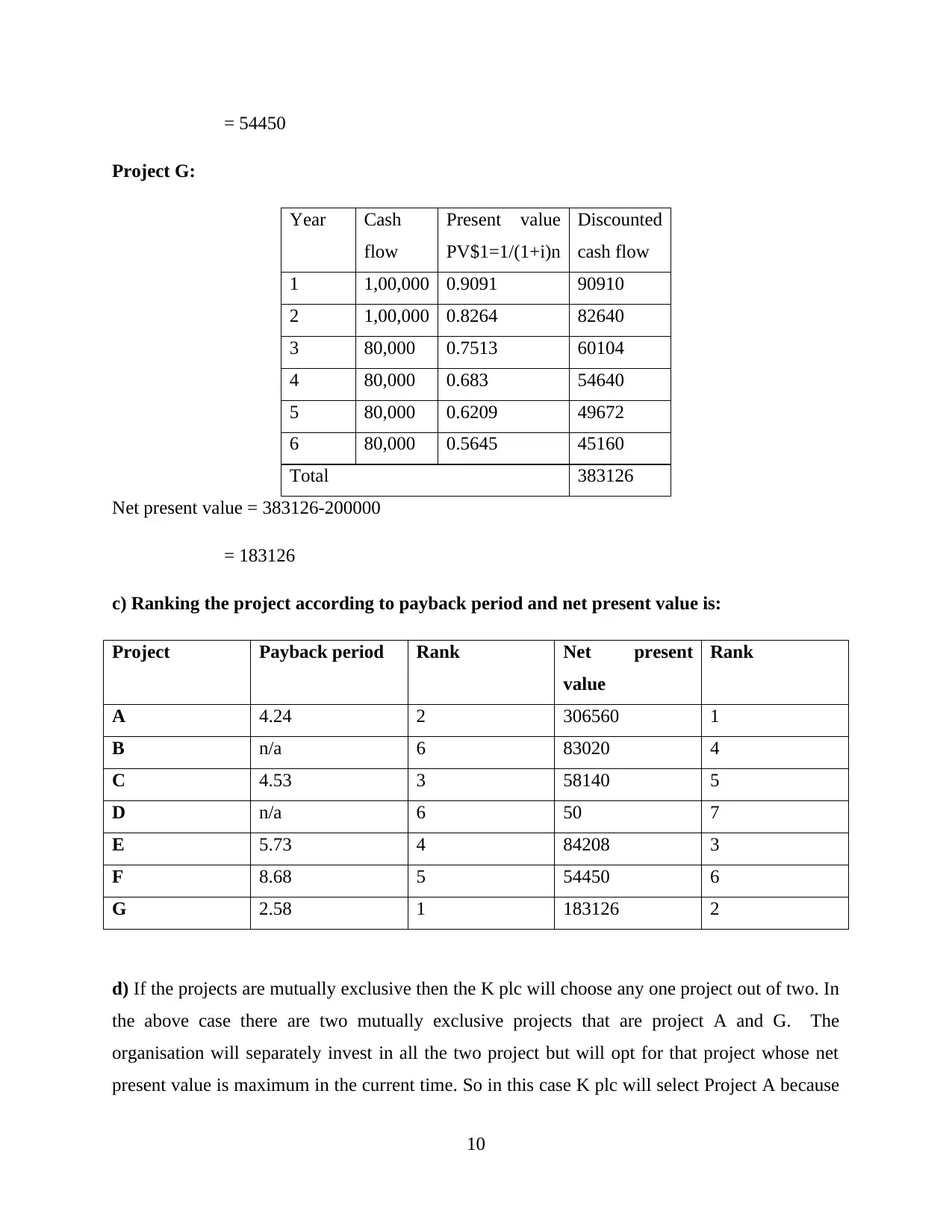

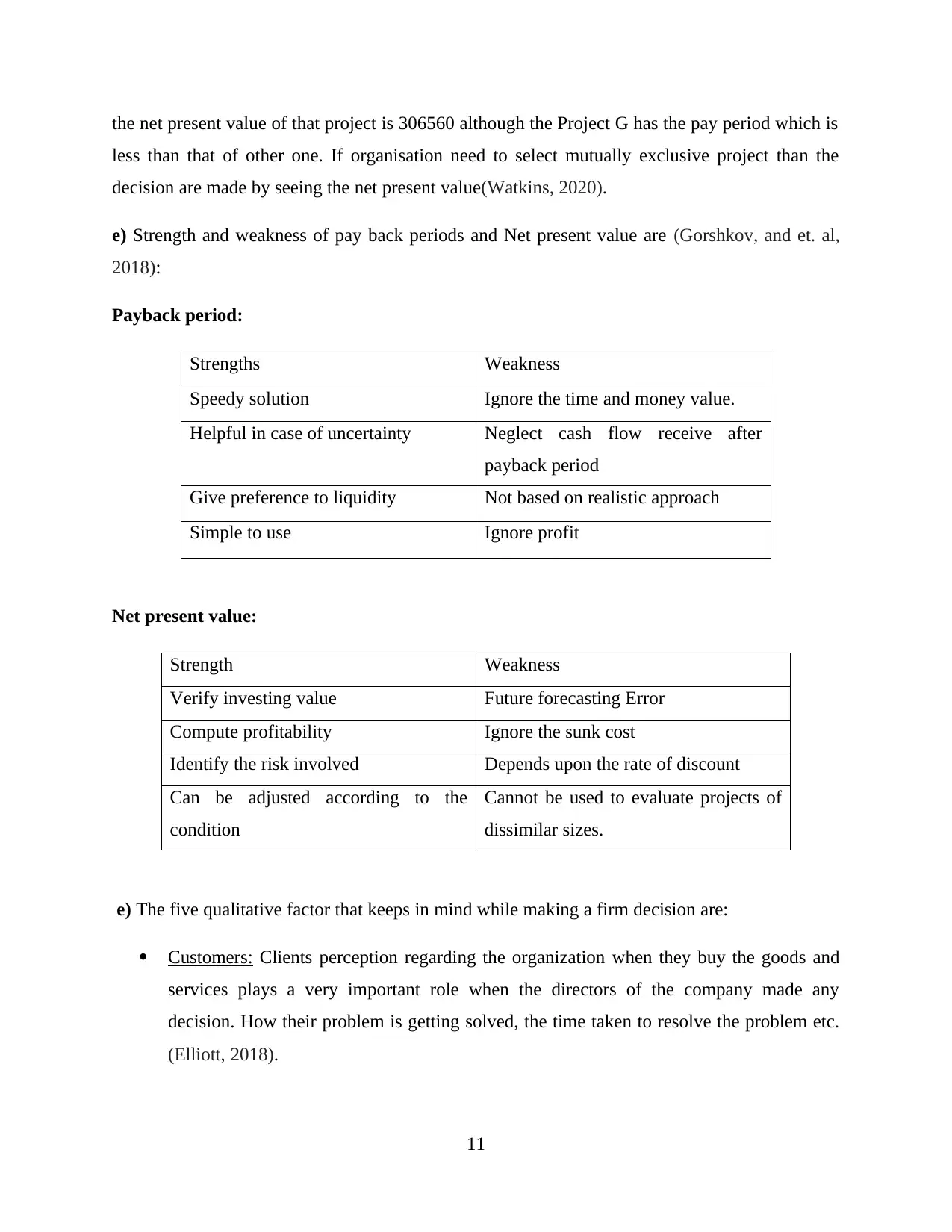

This report provides a comprehensive analysis of business finance principles, focusing on project evaluation techniques and capital raising strategies. It begins with an evaluation of several projects using discounted payback period and net present value (NPV) methods, ranking them based on these metrics. The report discusses the strengths and weaknesses of both payback period and NPV, along with qualitative factors influencing investment decisions. Furthermore, it explores alternative external sources of capital, including debt capital, trade credit, and factoring, linking investment choices to financial decisions. The report includes a variance analysis statement of variable costs, identifying areas where resource utilization can be improved. This document, contributed by a student and available on Desklib, offers valuable insights for students studying finance.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.