Report on KPMG Accounting Scandals and Standard Updates FASB

VerifiedAdded on 2023/06/04

|20

|3683

|486

Report

AI Summary

This report discusses current developments in accounting, focusing on KPMG's accounting issues and an update on accounting standards by the Financial Accounting Standards Board (FASB). The analysis of KPMG addresses concerns raised about the firm's role in accounting scandals, its financial health, and regulatory scrutiny, suggesting a need for market intervention and a spin-off of non-audit work. The report also examines the FASB's proposed accounting standard update on collaborative arrangements (Topic 808), highlighting targeted improvements and seeking public comments on the proposal to enhance comparability and revenue recognition. The update aims to align accounting practices with Topic 606, ensuring consistent and transparent financial reporting.

Current Developments in Accounting 1

Current Developments in Accounting

Current Developments in Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Developments in Accounting 2

Table of Contents

Q.1 Accounting Issues.................................................................................................................................3

Introduction.............................................................................................................................................3

Discussion on the Article.........................................................................................................................4

Discussion of the Theory and its Application on KPMG.........................................................................5

Conclusion...............................................................................................................................................7

Q.2 Accounting Standard Update................................................................................................................8

Opinions and Comments of Other industry Players on the Changes......................................................11

Discussion and Analysis of Comments..................................................................................................14

References.................................................................................................................................................18

Table of Contents

Q.1 Accounting Issues.................................................................................................................................3

Introduction.............................................................................................................................................3

Discussion on the Article.........................................................................................................................4

Discussion of the Theory and its Application on KPMG.........................................................................5

Conclusion...............................................................................................................................................7

Q.2 Accounting Standard Update................................................................................................................8

Opinions and Comments of Other industry Players on the Changes......................................................11

Discussion and Analysis of Comments..................................................................................................14

References.................................................................................................................................................18

Current Developments in Accounting 3

Q.1 Accounting Issues

Introduction

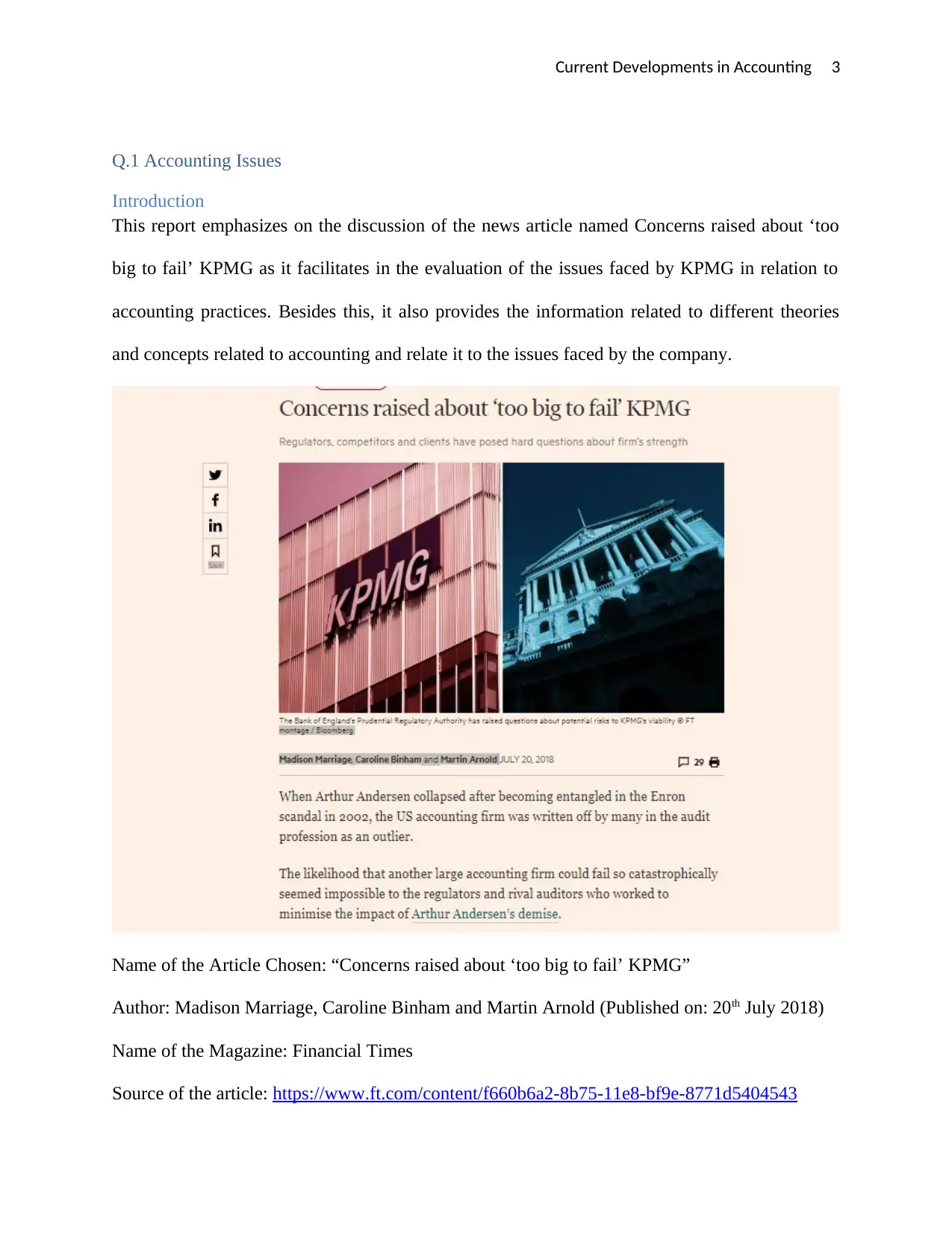

This report emphasizes on the discussion of the news article named Concerns raised about ‘too

big to fail’ KPMG as it facilitates in the evaluation of the issues faced by KPMG in relation to

accounting practices. Besides this, it also provides the information related to different theories

and concepts related to accounting and relate it to the issues faced by the company.

Name of the Article Chosen: “Concerns raised about ‘too big to fail’ KPMG”

Author: Madison Marriage, Caroline Binham and Martin Arnold (Published on: 20th July 2018)

Name of the Magazine: Financial Times

Source of the article: https://www.ft.com/content/f660b6a2-8b75-11e8-bf9e-8771d5404543

Q.1 Accounting Issues

Introduction

This report emphasizes on the discussion of the news article named Concerns raised about ‘too

big to fail’ KPMG as it facilitates in the evaluation of the issues faced by KPMG in relation to

accounting practices. Besides this, it also provides the information related to different theories

and concepts related to accounting and relate it to the issues faced by the company.

Name of the Article Chosen: “Concerns raised about ‘too big to fail’ KPMG”

Author: Madison Marriage, Caroline Binham and Martin Arnold (Published on: 20th July 2018)

Name of the Magazine: Financial Times

Source of the article: https://www.ft.com/content/f660b6a2-8b75-11e8-bf9e-8771d5404543

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Developments in Accounting 4

Discussion on the Article

It is identified that there are several companies such as Arthur Anderson that has collapsed due to

the existence of the accounting scandal by Enron in the year 2002 due to which the company has

written off various audit professions. It is also found out that there are various big accounting

firms that could fail in a catastrophic manner due to the impact of Arthur Andersen demise. It is

also found out that there is a decline in the profits of the KPMG before tax to fifth in the year

2017 to £301 million. The company has put aside £ 56 million for the purpose of meeting out the

potential fines and legal costs. It is also estimated that KPMG will overcome its recent

difficulties as it is in favor of the interests of regulators and competitors such as PwC, Deloitte

and EY. KPMG is involved in several big scandals across three continents in spite of this, its

biggest international clients are not distancing from the firm (Marriage, Binham & Arnold,

2018).

The different scandals in which there is an involvement of KPMG such as collapse of Carillion

and from the investigation it is found out that the three partners of the KPMG are accused of

leaking confidential information in improving inspection of the results for the firm. Despite of

the involvement in different accounting scandal, the company is able to attain the contract of

audit for the mining company such as Rio Tinto. The financial health of KPMG is strong and

have gained growth across advisory, audit and tax. KPMG has failed in spotting the signs of

financial instability which led to financial crisis due to which the regulators have increased its

scrutiny (Marriage, Binham & Arnold, 2018).

It is identified that the commission has reported that the auditors have failed to expose the risks

related to the banks in their financial statements in the year 2013 during the crisis. The audit

done by KPMG has failed to inform the users about the financial condition of the banks in an

accurate manner. The commission has criticized as the quality of the audits in an effective

Discussion on the Article

It is identified that there are several companies such as Arthur Anderson that has collapsed due to

the existence of the accounting scandal by Enron in the year 2002 due to which the company has

written off various audit professions. It is also found out that there are various big accounting

firms that could fail in a catastrophic manner due to the impact of Arthur Andersen demise. It is

also found out that there is a decline in the profits of the KPMG before tax to fifth in the year

2017 to £301 million. The company has put aside £ 56 million for the purpose of meeting out the

potential fines and legal costs. It is also estimated that KPMG will overcome its recent

difficulties as it is in favor of the interests of regulators and competitors such as PwC, Deloitte

and EY. KPMG is involved in several big scandals across three continents in spite of this, its

biggest international clients are not distancing from the firm (Marriage, Binham & Arnold,

2018).

The different scandals in which there is an involvement of KPMG such as collapse of Carillion

and from the investigation it is found out that the three partners of the KPMG are accused of

leaking confidential information in improving inspection of the results for the firm. Despite of

the involvement in different accounting scandal, the company is able to attain the contract of

audit for the mining company such as Rio Tinto. The financial health of KPMG is strong and

have gained growth across advisory, audit and tax. KPMG has failed in spotting the signs of

financial instability which led to financial crisis due to which the regulators have increased its

scrutiny (Marriage, Binham & Arnold, 2018).

It is identified that the commission has reported that the auditors have failed to expose the risks

related to the banks in their financial statements in the year 2013 during the crisis. The audit

done by KPMG has failed to inform the users about the financial condition of the banks in an

accurate manner. The commission has criticized as the quality of the audits in an effective

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Developments in Accounting 5

manner. There is a presence of various fears regarding the shape of the audit market despite of

the various attempts by different international authorities to lose the grip on the market such as

introduction of mandatory audit or rotation across Europe caps on the amount of consulting work

auditors (Marriage, Binham & Arnold, 2018).

The CMA is required to investigate the cases of audit firms in order to reduce the competition

and overcome the conflicts of interest in the sector. The collapse of the KPMG would results in

leaving of the three big audit firms in the market which has a significant influence on the level of

competition existed in the market. In order to resolve the issues there is a requirement of the

intervention in the market by the government to prevent the disruption of the collapse of the

firm. It is suggested that KPMG should spin off the non audit work by creating a separate firm.

KPMG Audit should only focus on audit and should invest more in the company to ensure

effective implementation of the audit operations (Marriage, Binham & Arnold, 2018).

Discussion of the Theory and its Application on KPMG

It is essential for the firms to comply with the standards and principles of accounting while

recording the financial transactions in the form of different financial statements in order to

communicate accurate information related to the financial performance and position of the

company to the users. The main reason behind the compliance with the standards and principles

of accounting facilitates in bringing consistency and uniformity in the presentation of the

information in different financial statements which in turn provides the benefits to the users to

compare the information with other players in the market in order to make financial decisions.

This also helps in elimination of the occurrence of the conflicts among the different stakeholders

of the company (Moran Reynolds & Gannon, 2018).

Apart from this, nowadays, there is a establishment of the regulatory authority that intervenes in

the activities of the company in order to protect the interests of the stakeholders. The companies

manner. There is a presence of various fears regarding the shape of the audit market despite of

the various attempts by different international authorities to lose the grip on the market such as

introduction of mandatory audit or rotation across Europe caps on the amount of consulting work

auditors (Marriage, Binham & Arnold, 2018).

The CMA is required to investigate the cases of audit firms in order to reduce the competition

and overcome the conflicts of interest in the sector. The collapse of the KPMG would results in

leaving of the three big audit firms in the market which has a significant influence on the level of

competition existed in the market. In order to resolve the issues there is a requirement of the

intervention in the market by the government to prevent the disruption of the collapse of the

firm. It is suggested that KPMG should spin off the non audit work by creating a separate firm.

KPMG Audit should only focus on audit and should invest more in the company to ensure

effective implementation of the audit operations (Marriage, Binham & Arnold, 2018).

Discussion of the Theory and its Application on KPMG

It is essential for the firms to comply with the standards and principles of accounting while

recording the financial transactions in the form of different financial statements in order to

communicate accurate information related to the financial performance and position of the

company to the users. The main reason behind the compliance with the standards and principles

of accounting facilitates in bringing consistency and uniformity in the presentation of the

information in different financial statements which in turn provides the benefits to the users to

compare the information with other players in the market in order to make financial decisions.

This also helps in elimination of the occurrence of the conflicts among the different stakeholders

of the company (Moran Reynolds & Gannon, 2018).

Apart from this, nowadays, there is a establishment of the regulatory authority that intervenes in

the activities of the company in order to protect the interests of the stakeholders. The companies

Current Developments in Accounting 6

nowadays appoint external auditors to oversee the financial statements of the company before

communicating it to the end users as it facilitates in presenting the accurate information to the

end users, but now the auditing is transformed into a separate profession and there is an existence

of big companies or auditing firms that carries out audit function and are involved in various

accounting scandals (Duska, Duska & Kury, 2018).

In case of KPMG, it is required by the company to adopt ethical practices and check or monitor

the financial results of the company in accordance with the set accounting standards and

accounting principles in order to bring transparency in the operations carried out by the firms. It

is essential for the regulatory authorities to impose penalties of large amount on the auditing

firms if they adopt fraudulent activities while carrying out the audit function due to

misrepresentation of the information in the financial statements of the company. The main reason

behind it is that it results in the creation of the conflict between the interests of different

stakeholders (Duska, Duska & Kury, 2018).

It is essential for the audit company i.e. KPMG to gain information related to different operations

and activities being performed by the company in order to provide true insights related to the

financial strength and position of the company and protect the interest of the stakeholders in a

significant manner. It is also identified that KPMG is able to measure the loss in the quantitative

or monetary terms incurred by it in the form of provisions set by them to meet out the penalties

and charges levied. Although it is also identified that the companies that have faced accounting

scandal has complied with the accounting standards developed by IASB but has made

modifications in them in order to attain the desired results in order to fulfill their goal of profit

maximization in order to attract more number of stakeholders (Leitoniene, Sapkauskiene &

Dagiliene, 2015).

nowadays appoint external auditors to oversee the financial statements of the company before

communicating it to the end users as it facilitates in presenting the accurate information to the

end users, but now the auditing is transformed into a separate profession and there is an existence

of big companies or auditing firms that carries out audit function and are involved in various

accounting scandals (Duska, Duska & Kury, 2018).

In case of KPMG, it is required by the company to adopt ethical practices and check or monitor

the financial results of the company in accordance with the set accounting standards and

accounting principles in order to bring transparency in the operations carried out by the firms. It

is essential for the regulatory authorities to impose penalties of large amount on the auditing

firms if they adopt fraudulent activities while carrying out the audit function due to

misrepresentation of the information in the financial statements of the company. The main reason

behind it is that it results in the creation of the conflict between the interests of different

stakeholders (Duska, Duska & Kury, 2018).

It is essential for the audit company i.e. KPMG to gain information related to different operations

and activities being performed by the company in order to provide true insights related to the

financial strength and position of the company and protect the interest of the stakeholders in a

significant manner. It is also identified that KPMG is able to measure the loss in the quantitative

or monetary terms incurred by it in the form of provisions set by them to meet out the penalties

and charges levied. Although it is also identified that the companies that have faced accounting

scandal has complied with the accounting standards developed by IASB but has made

modifications in them in order to attain the desired results in order to fulfill their goal of profit

maximization in order to attract more number of stakeholders (Leitoniene, Sapkauskiene &

Dagiliene, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Developments in Accounting 7

The audit company is able to measure the performance of the company in accounting and

quantitative terms which helps in provision of the adoption of the actions that can be applied in a

real manner. It is required by the audit company to expose the risks faced by the banks through

their financial statements which help in reducing the occurrence of bankruptcy of the financial

institutions and banks on a large scale. It is required by the government to establish a regulatory

authority that monitors the performance of the audit firms in order to prevent the situation of the

occurrence of the accounting scandal in the economy as a whole (Kuznetsova, Bogataya,

Khakhonova & Katerinin, 2017).

Conclusion

It can be concluded that despite of the fact that KPMG is involved in various accounting

scandals, the companies at the international level appoints it to audit their financial statements

and accounts in order to provide accurate information to their users. Along with this, it is

identified that the accounting issues due to which the scandals have happened is due to the non

compliance of different accounting theories in an effective manner.

The audit company is able to measure the performance of the company in accounting and

quantitative terms which helps in provision of the adoption of the actions that can be applied in a

real manner. It is required by the audit company to expose the risks faced by the banks through

their financial statements which help in reducing the occurrence of bankruptcy of the financial

institutions and banks on a large scale. It is required by the government to establish a regulatory

authority that monitors the performance of the audit firms in order to prevent the situation of the

occurrence of the accounting scandal in the economy as a whole (Kuznetsova, Bogataya,

Khakhonova & Katerinin, 2017).

Conclusion

It can be concluded that despite of the fact that KPMG is involved in various accounting

scandals, the companies at the international level appoints it to audit their financial statements

and accounts in order to provide accurate information to their users. Along with this, it is

identified that the accounting issues due to which the scandals have happened is due to the non

compliance of different accounting theories in an effective manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Developments in Accounting 8

Q.2 Accounting Standard Update

The Proposed Accounting Standards Update: Collaborative Arrangements (Topic 808): Targeted

Improvements

Issued: 26th April 2018

Comments due: 11th June 2018

Source: https://www.fasb.org/jsp/FASB/Document_C/DocumentPage?

cid=1176170411165&acceptedDisclaimer=true

Q.2 Accounting Standard Update

The Proposed Accounting Standards Update: Collaborative Arrangements (Topic 808): Targeted

Improvements

Issued: 26th April 2018

Comments due: 11th June 2018

Source: https://www.fasb.org/jsp/FASB/Document_C/DocumentPage?

cid=1176170411165&acceptedDisclaimer=true

Current Developments in Accounting 9

The accounting standard authority named Financial Accounting Standards Board (FASB) has

released the exposure draft related to the proposal before the implementation of the Accounting

Standard in Australia. The main reason behind the release of the exposure draft related to the

proposed amendments in the accounting standard is to seek comments from the public on the

proposal. FASB has released the exposure draft to make proposed amendments related to

targeted improvements in Topic 808 i.e. Collaborative Arrangements. As per Topic 808,

collaborative arrangements refers to contractual arrangement in which two or more parties to

actively participate in a joint operating activity exposed to significant risks and rewards

depending on the commercial success of the activity (FASB, 2018).

The main reason behind the issuance of the proposed accounting standard update is that Topic

808 does not include the comprehensive recognition or measurement for collaborative

arrangements and its accounting is based on accounting policy election and analogy to other

accounting literature. It is also found out that there is an occurrence of the differences in the

application of the method to recognize their arrangements that results in diversity in practice

adopted to account the transactions from the perspective of the economics of the collaborative

arrangement (FASB, 2018).

This accounting update affects those entities that are involved in collaborative arrangements.

This amendments in proposed update helps in making targeted improvements in generally

accepted accounting principles for collaborative arrangements. There is a requirement of addition

of account guidance in this accounting standard in order to align it with Topic 606. In case the

participant in the collaborative arrangements is customer then there is a need of gaining

clarification of the transactions among collaborative participants to account for revenue under

Topic 606 (FASB, 2018).

The accounting standard authority named Financial Accounting Standards Board (FASB) has

released the exposure draft related to the proposal before the implementation of the Accounting

Standard in Australia. The main reason behind the release of the exposure draft related to the

proposed amendments in the accounting standard is to seek comments from the public on the

proposal. FASB has released the exposure draft to make proposed amendments related to

targeted improvements in Topic 808 i.e. Collaborative Arrangements. As per Topic 808,

collaborative arrangements refers to contractual arrangement in which two or more parties to

actively participate in a joint operating activity exposed to significant risks and rewards

depending on the commercial success of the activity (FASB, 2018).

The main reason behind the issuance of the proposed accounting standard update is that Topic

808 does not include the comprehensive recognition or measurement for collaborative

arrangements and its accounting is based on accounting policy election and analogy to other

accounting literature. It is also found out that there is an occurrence of the differences in the

application of the method to recognize their arrangements that results in diversity in practice

adopted to account the transactions from the perspective of the economics of the collaborative

arrangement (FASB, 2018).

This accounting update affects those entities that are involved in collaborative arrangements.

This amendments in proposed update helps in making targeted improvements in generally

accepted accounting principles for collaborative arrangements. There is a requirement of addition

of account guidance in this accounting standard in order to align it with Topic 606. In case the

participant in the collaborative arrangements is customer then there is a need of gaining

clarification of the transactions among collaborative participants to account for revenue under

Topic 606 (FASB, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Current Developments in Accounting 10

In such situations the guidance in Topic 606 is applied that includes measurement, recognition,

disclosure and presentation requirements. It is also required for the companies to present the

transaction not as revenue if the transaction is not directly related to sales to third parties and the

counterparty participant in collaborative arrangements is not a customer. The main provisions

differ from current generally accepted accounting principles as it provides the guidance related to

whether some of the transactions carried out between the collaborative participants are accounted

for revenue aligned with the guidance in Topic 606 (FASB, 2018).

These amendments facilitates in provision of effective comparability in the categorization as

revenue between collaborative participants. It is also identified that prior to the issuance of Topic

606 the revenue from collaborative arrangements have been included by stakeholders as the

revenue recognized as per Topic 605 i.e. revenue recognition, recognized through analogy to the

guidance in Topic 605 and revenue recognized through the application of a policy election. The

amendments proposed related to collaborative arrangements reflect that it helps in the

improvement in comparability as these amendments has permitted that the revenue will be

recognized only in the case of those transactions where collaborative arrangements are indirectly

related to sale to third parties in accordance to Topic 606. There is no change have been made in

the requirements for those transactions that are directly related to sales to third parties (FASB,

2018).

It is also found out that FASB also invites organizations and individuals to provide their views

and opinions and comment on the matters included in the proposed update on the issues and

questions related to the amendments made. The comments are requested in the form of provision

of support and against towards the proposed guidance which is helpful for identification and

explanation of the issue or question to which they relate. Besides this, those people or

In such situations the guidance in Topic 606 is applied that includes measurement, recognition,

disclosure and presentation requirements. It is also required for the companies to present the

transaction not as revenue if the transaction is not directly related to sales to third parties and the

counterparty participant in collaborative arrangements is not a customer. The main provisions

differ from current generally accepted accounting principles as it provides the guidance related to

whether some of the transactions carried out between the collaborative participants are accounted

for revenue aligned with the guidance in Topic 606 (FASB, 2018).

These amendments facilitates in provision of effective comparability in the categorization as

revenue between collaborative participants. It is also identified that prior to the issuance of Topic

606 the revenue from collaborative arrangements have been included by stakeholders as the

revenue recognized as per Topic 605 i.e. revenue recognition, recognized through analogy to the

guidance in Topic 605 and revenue recognized through the application of a policy election. The

amendments proposed related to collaborative arrangements reflect that it helps in the

improvement in comparability as these amendments has permitted that the revenue will be

recognized only in the case of those transactions where collaborative arrangements are indirectly

related to sale to third parties in accordance to Topic 606. There is no change have been made in

the requirements for those transactions that are directly related to sales to third parties (FASB,

2018).

It is also found out that FASB also invites organizations and individuals to provide their views

and opinions and comment on the matters included in the proposed update on the issues and

questions related to the amendments made. The comments are requested in the form of provision

of support and against towards the proposed guidance which is helpful for identification and

explanation of the issue or question to which they relate. Besides this, those people or

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current Developments in Accounting 11

organisation that disagrees with the amendments is allowed to provide suggestion with suitable

justification in an effective manner (FASB, 2018).

Opinions and Comments of Other industry Players on the Changes

Comments of four market players are discussed below on the proposed changes. The names of

these organizations are

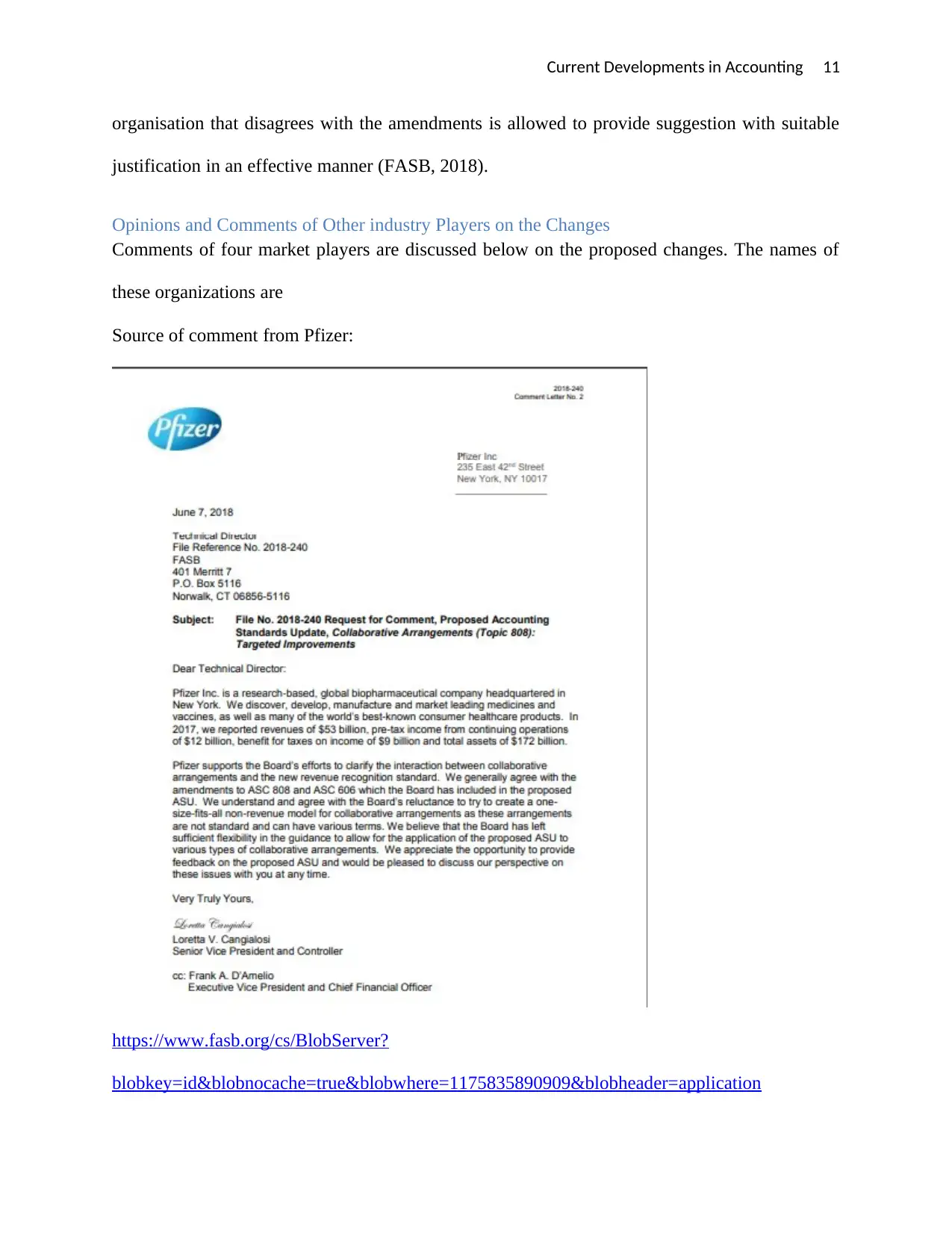

Source of comment from Pfizer:

https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175835890909&blobheader=application

organisation that disagrees with the amendments is allowed to provide suggestion with suitable

justification in an effective manner (FASB, 2018).

Opinions and Comments of Other industry Players on the Changes

Comments of four market players are discussed below on the proposed changes. The names of

these organizations are

Source of comment from Pfizer:

https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175835890909&blobheader=application

Current Developments in Accounting 12

%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=650813&blobheadervalue1=filename

%3DCOLLAB.ED.002.PFIZER_INC._LORETTA_V._CANGIALOSI.pdf&blobcol=urldata&bl

obtable=MungoBlobs

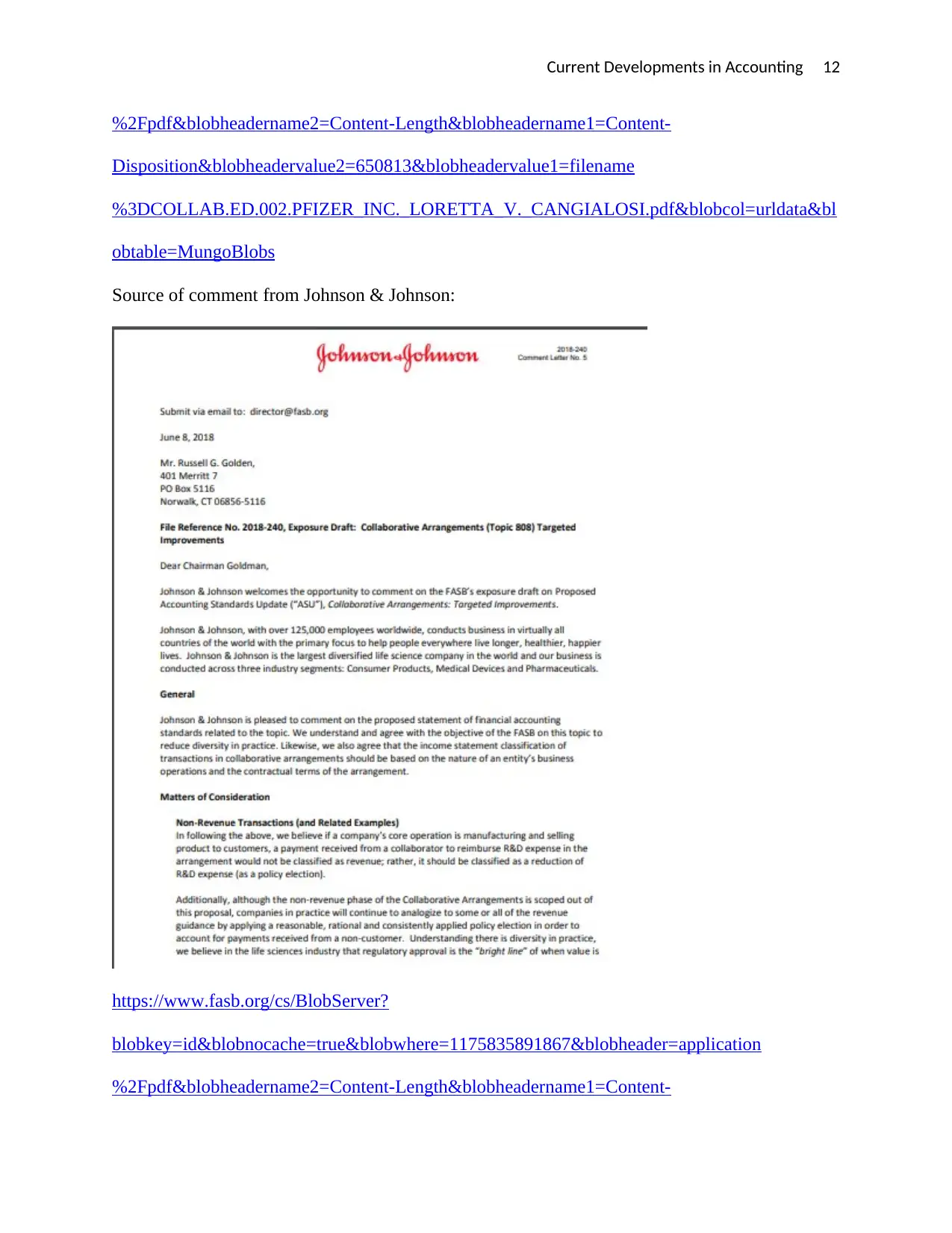

Source of comment from Johnson & Johnson:

https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175835891867&blobheader=application

%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

Disposition&blobheadervalue2=650813&blobheadervalue1=filename

%3DCOLLAB.ED.002.PFIZER_INC._LORETTA_V._CANGIALOSI.pdf&blobcol=urldata&bl

obtable=MungoBlobs

Source of comment from Johnson & Johnson:

https://www.fasb.org/cs/BlobServer?

blobkey=id&blobnocache=true&blobwhere=1175835891867&blobheader=application

%2Fpdf&blobheadername2=Content-Length&blobheadername1=Content-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.